Detailed Report on Management Accounting for KEF Ltd

VerifiedAdded on 2023/01/17

|13

|3803

|50

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and their application within KEF Ltd, a medium-sized manufacturing company. It begins by defining management accounting and exploring different types of systems like cost accounting, job costing, and price optimization. The report then details various reporting methods, including financial, sales, and budget reports, emphasizing their importance in business decision-making. A significant portion of the report focuses on cost calculation methods, specifically absorption costing and marginal costing, with detailed examples and interpretations. Furthermore, it analyzes the advantages and disadvantages of planning tools such as capital and flexible budgets, and discusses the integration of management accounting systems and reporting. The report also examines how management accounting systems can address financial problems and contribute to a company's success, offering valuable insights for students of business development.

MANAGEMENT

ACCOUTING

ACCOUTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

P 1 Management accounting and types of its system.............................................................3

P 2 Various methods of reporting for management accounting.............................................4

M 1 Benefits and application..................................................................................................4

D 1 Integration of management accounting system and reporting.........................................5

P 3 Calculate cost...................................................................................................................5

P 4 Advantages and disadvantages of planning tools.............................................................8

M 3 Use of different planning tools.....................................................................................10

P 5 Management accounting system for dealing with financial problems...........................10

M 4 How dealing with financial problems help company in attaining success...................11

D 3 Evaluation of planning tool in responding to financial problem leading to success.....12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

P 1 Management accounting and types of its system.............................................................3

P 2 Various methods of reporting for management accounting.............................................4

M 1 Benefits and application..................................................................................................4

D 1 Integration of management accounting system and reporting.........................................5

P 3 Calculate cost...................................................................................................................5

P 4 Advantages and disadvantages of planning tools.............................................................8

M 3 Use of different planning tools.....................................................................................10

P 5 Management accounting system for dealing with financial problems...........................10

M 4 How dealing with financial problems help company in attaining success...................11

D 3 Evaluation of planning tool in responding to financial problem leading to success.....12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is that branch of accounting which helps the company in taking

decisions relating to the management of the various activities of the business. Management

accounting is very crucial for the success of the company as it helps the company in evaluating

the different areas of concern for the management and to improve those areas (Otley, 2016). The

present study is based in the KEF Ltd company which is a medium sized manufacturing

company.

The present report will start by discussing the different types of management accounting

system along with the different type of reporting of management accounting. Further some

calculation outlining the marginal costing and absorption costing will be discussed in the report.

Next the different planning tools and their advantages and disadvantages will be highlighted. In

the end the application of different management accounting system for the solution of some

financial problems will be discussed.

MAIN BODY

P 1 Management accounting and types of its system

The management accounting is defined as the presentation of the accounting information

and financial statements in such a way that it assists the managers in taking decision relating to

the day to day operations of the company (Meaning and definition of management accounting,

2019). There are many different types of management accounting system which helps the

company in taking various types of decision. These systems are discussed in the following points

connected below-

Cost accounting- this is a system under the management accounting system which helps

KEF Ltd in recording and reporting systematically all the cost related to the manufacturing of the

goods and services. This system help company in allocating the cost to different production units

and ensuring that the cost is not overutilized.

Job costing- this is a type of system which helps the company in allocating the cost to

specific or particular job. Under this the manufacturing cost is systematically divided in different

job like the overhead, direct labour, direct material and other activities which are required to

accomplish and finish the process of manufacturing (Maas, Schaltegger and Crutzen, 2016).

Price optimisation- this is a system which help KEF Ltd in analysing the different price

level for the product and service produced and the reaction of the consumers over it. This system

Management accounting is that branch of accounting which helps the company in taking

decisions relating to the management of the various activities of the business. Management

accounting is very crucial for the success of the company as it helps the company in evaluating

the different areas of concern for the management and to improve those areas (Otley, 2016). The

present study is based in the KEF Ltd company which is a medium sized manufacturing

company.

The present report will start by discussing the different types of management accounting

system along with the different type of reporting of management accounting. Further some

calculation outlining the marginal costing and absorption costing will be discussed in the report.

Next the different planning tools and their advantages and disadvantages will be highlighted. In

the end the application of different management accounting system for the solution of some

financial problems will be discussed.

MAIN BODY

P 1 Management accounting and types of its system

The management accounting is defined as the presentation of the accounting information

and financial statements in such a way that it assists the managers in taking decision relating to

the day to day operations of the company (Meaning and definition of management accounting,

2019). There are many different types of management accounting system which helps the

company in taking various types of decision. These systems are discussed in the following points

connected below-

Cost accounting- this is a system under the management accounting system which helps

KEF Ltd in recording and reporting systematically all the cost related to the manufacturing of the

goods and services. This system help company in allocating the cost to different production units

and ensuring that the cost is not overutilized.

Job costing- this is a type of system which helps the company in allocating the cost to

specific or particular job. Under this the manufacturing cost is systematically divided in different

job like the overhead, direct labour, direct material and other activities which are required to

accomplish and finish the process of manufacturing (Maas, Schaltegger and Crutzen, 2016).

Price optimisation- this is a system which help KEF Ltd in analysing the different price

level for the product and service produced and the reaction of the consumers over it. This system

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

helps the company in fixing the most suitable price so that the consumers are comfortable and

the company also earns profits.

P 2 Various methods of reporting for management accounting

The report helps the company in recording and displaying the different records of the

company relating to its different departments like manufacturing, sales, budgeting and many

other different areas of business (Cooper, Ezzamel and Qu, 2017). There are various kinds of

reports which are being prepared for the efficient management of the company. These reports

have been discussed in the below discussed points-

Financial reports- these are the report which comprises of the financial information

relating to all the financial transaction which takes place within the business. Thus, this report

helps KEF Ltd in analysing all the financial transaction and taking care of the money and how it

is being used in the business.

Sales report- this is a type of report which records all the transactions relating to the sales

of the company. Thus, it is very necessary for the company to record all the sales transaction to

know that how many are the cash and how much is the credit and how much money needs to be

recovered from others.

Budget report- this is the most essential report for the company and its successfulness.

This is majorly because of the reason that under this reporting system all the estimated income

and expenses are being recorded in the budget. This provides an estimation to KEF Ltd that this

much of income and expenses will be incurred and company can plan its working in accordance

with that estimation.

M 1 Benefits and application

The management accounting is applied within the business in order to plan and control

the way the company will work. This is majorly because of the reason that this helps in preparing

budgets which help the company to plan and to work in accordance to those planned budgets

only. Also, this helps the company in controlling the planned work by comparing actual work

with the planned work.

The major benefit of management accounting system is that this increases the efficiency

of the business (Bromwich and Scapens, 2016). This is majorly because of the reason that all the

work is planned in advance and every employee knows what they want to do. Thus, this also

increases the profitability of the company and its operation. Another benefit is that the company

the company also earns profits.

P 2 Various methods of reporting for management accounting

The report helps the company in recording and displaying the different records of the

company relating to its different departments like manufacturing, sales, budgeting and many

other different areas of business (Cooper, Ezzamel and Qu, 2017). There are various kinds of

reports which are being prepared for the efficient management of the company. These reports

have been discussed in the below discussed points-

Financial reports- these are the report which comprises of the financial information

relating to all the financial transaction which takes place within the business. Thus, this report

helps KEF Ltd in analysing all the financial transaction and taking care of the money and how it

is being used in the business.

Sales report- this is a type of report which records all the transactions relating to the sales

of the company. Thus, it is very necessary for the company to record all the sales transaction to

know that how many are the cash and how much is the credit and how much money needs to be

recovered from others.

Budget report- this is the most essential report for the company and its successfulness.

This is majorly because of the reason that under this reporting system all the estimated income

and expenses are being recorded in the budget. This provides an estimation to KEF Ltd that this

much of income and expenses will be incurred and company can plan its working in accordance

with that estimation.

M 1 Benefits and application

The management accounting is applied within the business in order to plan and control

the way the company will work. This is majorly because of the reason that this helps in preparing

budgets which help the company to plan and to work in accordance to those planned budgets

only. Also, this helps the company in controlling the planned work by comparing actual work

with the planned work.

The major benefit of management accounting system is that this increases the efficiency

of the business (Bromwich and Scapens, 2016). This is majorly because of the reason that all the

work is planned in advance and every employee knows what they want to do. Thus, this also

increases the profitability of the company and its operation. Another benefit is that the company

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

is able to take effective and efficient decision for the growth and development of the company.

This is pertaining to the fact that the planned work helps the company in deciding in which area

to go for development (Chenhall and Moers, 2015).

D 1 Integration of management accounting system and reporting

Both the management accounting system and the management accounting reporting are

integrated together for achieving the success. If these two things not work in coordinated manner

then the company will not be able to succeed in its working. This is majorly because of the

reason that if management accounting system are not used effectively then the report will not be

prepared in effective manner. This is due to the fact that the reports are being made on the basis

of the management system and their working.

It is so pertaining to the fact that if the cost is not allocated then how the cost report will

be made. Similarly, if the budgets are not prepared then how the cost will be allocated and how

the work will be done. Thus, it is very necessary for the KEF Ltd to integrate its reporting with

various different management accounting system.

P 3 Calculate cost

Absorption costing- This method referred as the costing technique that indicates all the

cost that incurred in manufacturing the product had been allocated or assigned towards the units

that is been produced. It means that for producing the finished product, various cost is included

that cost of direct material, manufacturing overhead, direct labour and fixed production

overhead. Absorption costing helps in complying the accounting standards and makes a greater

job in tracking the profits accurately than the variable costing. The major limitation of this

method is it could skew the profitability picture of the company and is not seen as helpful in

making assessment for improving the business operations or in comparing the product lines.

Marginal costing- It means the cost of an additional unit or an output and it is the method

utilised for determining the optimum quantity of the product for an enterprise where it cost for a

least amount in producing an additional unit (Weetman, 2019). Marginal cost eliminates variance

cost per unit as fixed cost are not been charged directly to the production cost under marginal

costing and the units that have a standard cost. This costing technique helps in planning for short

period through representation of the charts and the graphs of the break even and profitability.

This is pertaining to the fact that the planned work helps the company in deciding in which area

to go for development (Chenhall and Moers, 2015).

D 1 Integration of management accounting system and reporting

Both the management accounting system and the management accounting reporting are

integrated together for achieving the success. If these two things not work in coordinated manner

then the company will not be able to succeed in its working. This is majorly because of the

reason that if management accounting system are not used effectively then the report will not be

prepared in effective manner. This is due to the fact that the reports are being made on the basis

of the management system and their working.

It is so pertaining to the fact that if the cost is not allocated then how the cost report will

be made. Similarly, if the budgets are not prepared then how the cost will be allocated and how

the work will be done. Thus, it is very necessary for the KEF Ltd to integrate its reporting with

various different management accounting system.

P 3 Calculate cost

Absorption costing- This method referred as the costing technique that indicates all the

cost that incurred in manufacturing the product had been allocated or assigned towards the units

that is been produced. It means that for producing the finished product, various cost is included

that cost of direct material, manufacturing overhead, direct labour and fixed production

overhead. Absorption costing helps in complying the accounting standards and makes a greater

job in tracking the profits accurately than the variable costing. The major limitation of this

method is it could skew the profitability picture of the company and is not seen as helpful in

making assessment for improving the business operations or in comparing the product lines.

Marginal costing- It means the cost of an additional unit or an output and it is the method

utilised for determining the optimum quantity of the product for an enterprise where it cost for a

least amount in producing an additional unit (Weetman, 2019). Marginal cost eliminates variance

cost per unit as fixed cost are not been charged directly to the production cost under marginal

costing and the units that have a standard cost. This costing technique helps in planning for short

period through representation of the charts and the graphs of the break even and profitability.

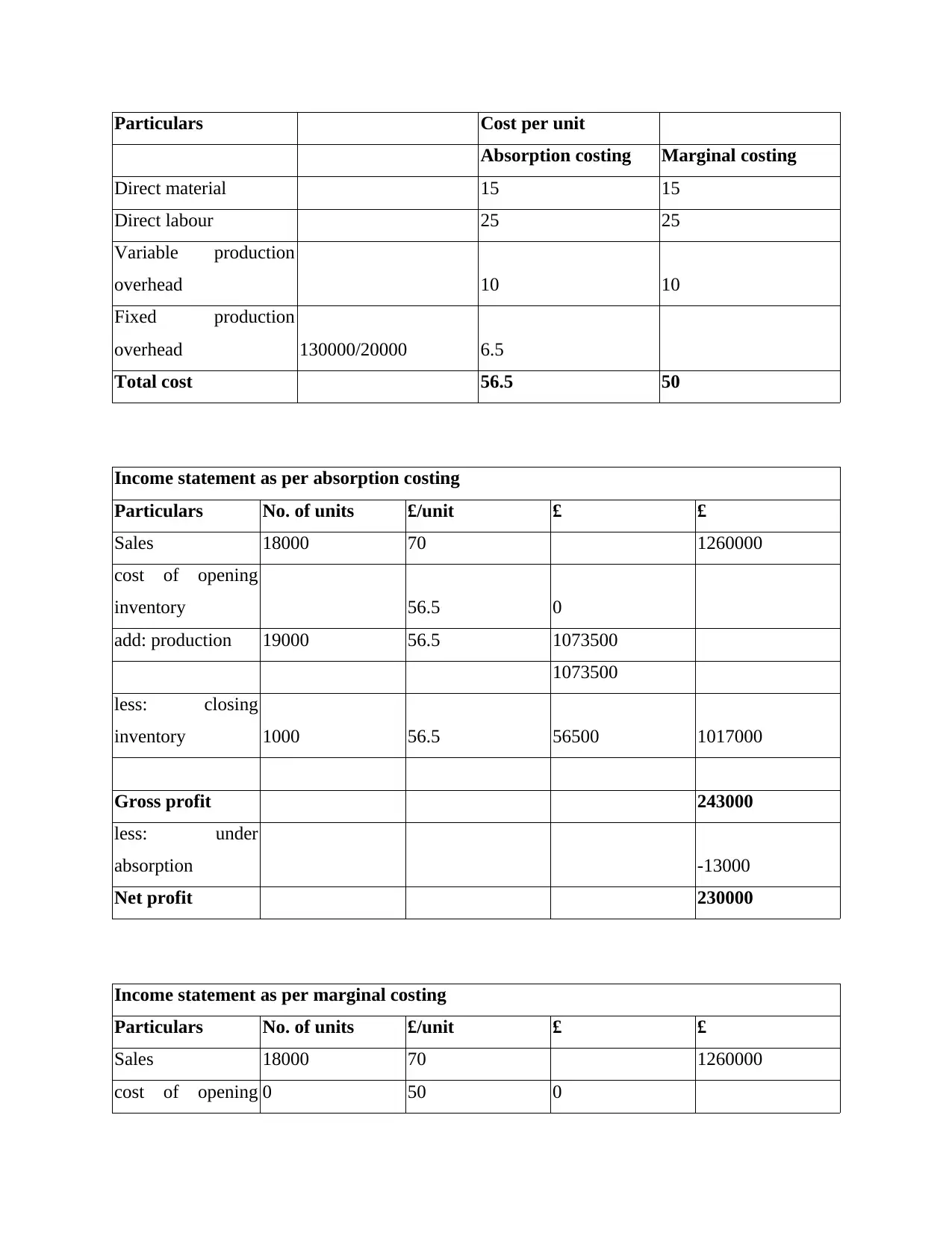

Particulars Cost per unit

Absorption costing Marginal costing

Direct material 15 15

Direct labour 25 25

Variable production

overhead 10 10

Fixed production

overhead 130000/20000 6.5

Total cost 56.5 50

Income statement as per absorption costing

Particulars No. of units £/unit £ £

Sales 18000 70 1260000

cost of opening

inventory 56.5 0

add: production 19000 56.5 1073500

1073500

less: closing

inventory 1000 56.5 56500 1017000

Gross profit 243000

less: under

absorption -13000

Net profit 230000

Income statement as per marginal costing

Particulars No. of units £/unit £ £

Sales 18000 70 1260000

cost of opening 0 50 0

Absorption costing Marginal costing

Direct material 15 15

Direct labour 25 25

Variable production

overhead 10 10

Fixed production

overhead 130000/20000 6.5

Total cost 56.5 50

Income statement as per absorption costing

Particulars No. of units £/unit £ £

Sales 18000 70 1260000

cost of opening

inventory 56.5 0

add: production 19000 56.5 1073500

1073500

less: closing

inventory 1000 56.5 56500 1017000

Gross profit 243000

less: under

absorption -13000

Net profit 230000

Income statement as per marginal costing

Particulars No. of units £/unit £ £

Sales 18000 70 1260000

cost of opening 0 50 0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

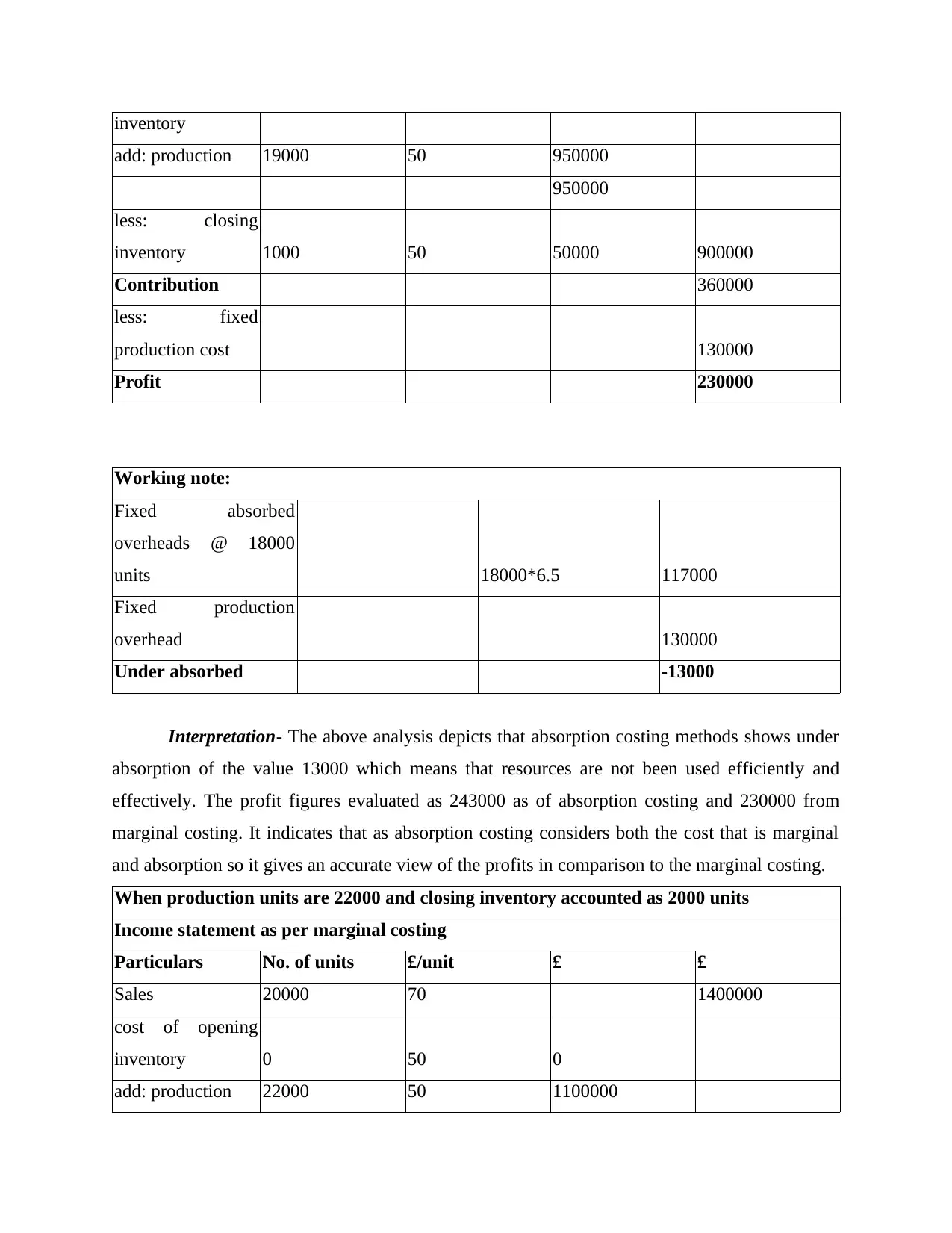

inventory

add: production 19000 50 950000

950000

less: closing

inventory 1000 50 50000 900000

Contribution 360000

less: fixed

production cost 130000

Profit 230000

Working note:

Fixed absorbed

overheads @ 18000

units 18000*6.5 117000

Fixed production

overhead 130000

Under absorbed -13000

Interpretation- The above analysis depicts that absorption costing methods shows under

absorption of the value 13000 which means that resources are not been used efficiently and

effectively. The profit figures evaluated as 243000 as of absorption costing and 230000 from

marginal costing. It indicates that as absorption costing considers both the cost that is marginal

and absorption so it gives an accurate view of the profits in comparison to the marginal costing.

When production units are 22000 and closing inventory accounted as 2000 units

Income statement as per marginal costing

Particulars No. of units £/unit £ £

Sales 20000 70 1400000

cost of opening

inventory 0 50 0

add: production 22000 50 1100000

add: production 19000 50 950000

950000

less: closing

inventory 1000 50 50000 900000

Contribution 360000

less: fixed

production cost 130000

Profit 230000

Working note:

Fixed absorbed

overheads @ 18000

units 18000*6.5 117000

Fixed production

overhead 130000

Under absorbed -13000

Interpretation- The above analysis depicts that absorption costing methods shows under

absorption of the value 13000 which means that resources are not been used efficiently and

effectively. The profit figures evaluated as 243000 as of absorption costing and 230000 from

marginal costing. It indicates that as absorption costing considers both the cost that is marginal

and absorption so it gives an accurate view of the profits in comparison to the marginal costing.

When production units are 22000 and closing inventory accounted as 2000 units

Income statement as per marginal costing

Particulars No. of units £/unit £ £

Sales 20000 70 1400000

cost of opening

inventory 0 50 0

add: production 22000 50 1100000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

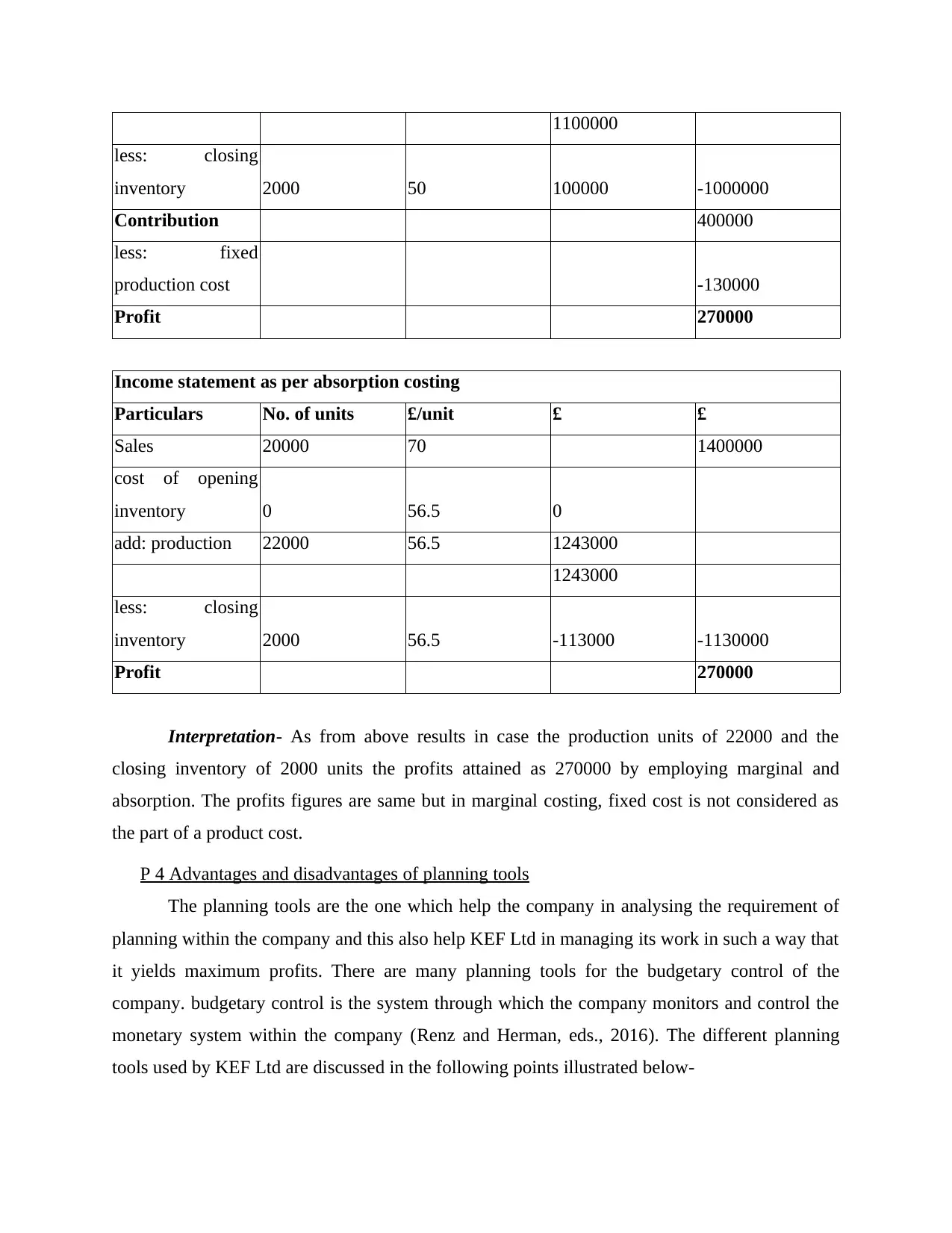

1100000

less: closing

inventory 2000 50 100000 -1000000

Contribution 400000

less: fixed

production cost -130000

Profit 270000

Income statement as per absorption costing

Particulars No. of units £/unit £ £

Sales 20000 70 1400000

cost of opening

inventory 0 56.5 0

add: production 22000 56.5 1243000

1243000

less: closing

inventory 2000 56.5 -113000 -1130000

Profit 270000

Interpretation- As from above results in case the production units of 22000 and the

closing inventory of 2000 units the profits attained as 270000 by employing marginal and

absorption. The profits figures are same but in marginal costing, fixed cost is not considered as

the part of a product cost.

P 4 Advantages and disadvantages of planning tools

The planning tools are the one which help the company in analysing the requirement of

planning within the company and this also help KEF Ltd in managing its work in such a way that

it yields maximum profits. There are many planning tools for the budgetary control of the

company. budgetary control is the system through which the company monitors and control the

monetary system within the company (Renz and Herman, eds., 2016). The different planning

tools used by KEF Ltd are discussed in the following points illustrated below-

less: closing

inventory 2000 50 100000 -1000000

Contribution 400000

less: fixed

production cost -130000

Profit 270000

Income statement as per absorption costing

Particulars No. of units £/unit £ £

Sales 20000 70 1400000

cost of opening

inventory 0 56.5 0

add: production 22000 56.5 1243000

1243000

less: closing

inventory 2000 56.5 -113000 -1130000

Profit 270000

Interpretation- As from above results in case the production units of 22000 and the

closing inventory of 2000 units the profits attained as 270000 by employing marginal and

absorption. The profits figures are same but in marginal costing, fixed cost is not considered as

the part of a product cost.

P 4 Advantages and disadvantages of planning tools

The planning tools are the one which help the company in analysing the requirement of

planning within the company and this also help KEF Ltd in managing its work in such a way that

it yields maximum profits. There are many planning tools for the budgetary control of the

company. budgetary control is the system through which the company monitors and control the

monetary system within the company (Renz and Herman, eds., 2016). The different planning

tools used by KEF Ltd are discussed in the following points illustrated below-

Capital budget- this is a type of budget which is used in order to allocate the money in

respect of maintenance and acquisition of the fixed assets and equipment. The capital budgeting

is a process of planning for determining the fact that whether the company need to go for long

term investment in machines, new plant, products and many other equipment (Dekker, 2016).

For analysing the worth of the project many techniques are being used like payback period, net

present value, internal rate of return and many others.

Advantages- the major advantage of this planning tool is that this help the company in

gaining knowledge that which investment option is better for the growth of the company

and which can provide for the maximum of the profits.

Disadvantages- the drawback of using capital budgeting is that operational cost of the

company is increased as more investment is being done in the fixed assets of the

company. Also, another drawback is that preparation of the capital budget requires

specialised skills and expertise and this requires a lot of money.

Flexible budget- the flexible budget is the one which adjust in accordance with the

changes taking place in the volume of the production. This is an estimation of the income and the

expenses based on the current output for the future use. Under this budget the future work is

estimated keeping the current production as the base for the company.

Advantages- the major advantage of this type of budget is that this budget adjust in

accordance with the changes taking place in the business environment. Another

advantage of use of this budget is that this helps in the better control of the cost and to be

updated with the current data. This is helpful because of the fact that this helps the

company in analysing the current situation and then to react in the required manner.

Disadvantages- the major negative point of this budget is that it is very time consuming

for the company to analyse and research for the changes taking place in the market. Also,

the other disadvantage of this budget is that this is dependent of the future changes and

whose are uncertain and need to managed in effective and efficient manner.

Variance analysis- this is a tool of budgetary control because under this technique the

difference between the standard output and the actual output is made. This help the company in

setting the standards first and then work in accordance with the set standard (Granlund and

Lukka, 2017). After the completion of the work it is compared with the standard to the difference

and to take corrective actions.

respect of maintenance and acquisition of the fixed assets and equipment. The capital budgeting

is a process of planning for determining the fact that whether the company need to go for long

term investment in machines, new plant, products and many other equipment (Dekker, 2016).

For analysing the worth of the project many techniques are being used like payback period, net

present value, internal rate of return and many others.

Advantages- the major advantage of this planning tool is that this help the company in

gaining knowledge that which investment option is better for the growth of the company

and which can provide for the maximum of the profits.

Disadvantages- the drawback of using capital budgeting is that operational cost of the

company is increased as more investment is being done in the fixed assets of the

company. Also, another drawback is that preparation of the capital budget requires

specialised skills and expertise and this requires a lot of money.

Flexible budget- the flexible budget is the one which adjust in accordance with the

changes taking place in the volume of the production. This is an estimation of the income and the

expenses based on the current output for the future use. Under this budget the future work is

estimated keeping the current production as the base for the company.

Advantages- the major advantage of this type of budget is that this budget adjust in

accordance with the changes taking place in the business environment. Another

advantage of use of this budget is that this helps in the better control of the cost and to be

updated with the current data. This is helpful because of the fact that this helps the

company in analysing the current situation and then to react in the required manner.

Disadvantages- the major negative point of this budget is that it is very time consuming

for the company to analyse and research for the changes taking place in the market. Also,

the other disadvantage of this budget is that this is dependent of the future changes and

whose are uncertain and need to managed in effective and efficient manner.

Variance analysis- this is a tool of budgetary control because under this technique the

difference between the standard output and the actual output is made. This help the company in

setting the standards first and then work in accordance with the set standard (Granlund and

Lukka, 2017). After the completion of the work it is compared with the standard to the difference

and to take corrective actions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Advantages- the major advantage is that this is good tool of measuring the performance

of the work of the company. It is majorly because of the fact that if the performance is

less then the expected value then major changes can take place (van Helden and Uddin,

2016). Another advantage is that this setting up of direction provides a direction to the

company in which they need to work.

Disadvantages- the major drawback of this is that this technique is difficult to be applied

in the companies which deals in providing services to others. This is majorly due to the

fact that under this business it is not possible to set some standards.

M 3 Use of different planning tools

The different planning tools discussed above help KEF Ltd in planning its work in

effective and efficient manner. These tools help the company in identifying some ways in which

the company can improve its working capacity. Thus, these tools are applied in different manner

and for different purposes. Like for instance, the capital budgeting is used for deciding that

whether the company need to go for some huge investment or not. In the same way, variance

analysis is applied to see that whether there is any deviation in the planned work and the actual

work or not. But this is also expensive for the company to employ all these tools as this requires

expert knowledge and for this some professionals need to be hired and they will require high

salary and fees.

P 5 Management accounting system for dealing with financial problems

The business run in environment which is very dynamic and changing hence, it is very

essential for the company to evaluate all its working and make sure that there is not much

problem being faced by the company. KEF Ltd also encounters with some financial problems

while running the business. Thus, it is very necessary for the company to manage all these

financial problems so that the company can go in the direction of growth and development. The

financial problem are the difficulties which the company faces because of some money or fund

related issues.

System KEF Ltd Dali speakers

Benchmarking- this is a

system which is being used by

the companies in order to

compare its working with that

The company uses

benchmarking in order to deal

with the financial problem.

The major problem faced by

The competitor also uses this

technique of solving the

financial problems. But Dali

speaker uses benchmarking in

of the work of the company. It is majorly because of the fact that if the performance is

less then the expected value then major changes can take place (van Helden and Uddin,

2016). Another advantage is that this setting up of direction provides a direction to the

company in which they need to work.

Disadvantages- the major drawback of this is that this technique is difficult to be applied

in the companies which deals in providing services to others. This is majorly due to the

fact that under this business it is not possible to set some standards.

M 3 Use of different planning tools

The different planning tools discussed above help KEF Ltd in planning its work in

effective and efficient manner. These tools help the company in identifying some ways in which

the company can improve its working capacity. Thus, these tools are applied in different manner

and for different purposes. Like for instance, the capital budgeting is used for deciding that

whether the company need to go for some huge investment or not. In the same way, variance

analysis is applied to see that whether there is any deviation in the planned work and the actual

work or not. But this is also expensive for the company to employ all these tools as this requires

expert knowledge and for this some professionals need to be hired and they will require high

salary and fees.

P 5 Management accounting system for dealing with financial problems

The business run in environment which is very dynamic and changing hence, it is very

essential for the company to evaluate all its working and make sure that there is not much

problem being faced by the company. KEF Ltd also encounters with some financial problems

while running the business. Thus, it is very necessary for the company to manage all these

financial problems so that the company can go in the direction of growth and development. The

financial problem are the difficulties which the company faces because of some money or fund

related issues.

System KEF Ltd Dali speakers

Benchmarking- this is a

system which is being used by

the companies in order to

compare its working with that

The company uses

benchmarking in order to deal

with the financial problem.

The major problem faced by

The competitor also uses this

technique of solving the

financial problems. But Dali

speaker uses benchmarking in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of the other competitor. This is

a technique which is used in

order to compare the position

of one country with that of the

other and can compare its

problem in order to get some

solutions.

the company was the low

profits of the company. this

problem was solved by taking

benchmarking as a solution.

This is because of the reason

that this comparison will help

KEF Ltd to compare the

working with the popular

competitor and then find ways

of better performance of the

competitors.

order to analyse the fact that

what other companies are

bringing changes and how the

other companies are dealing

with the changes taking place

in the market (Nitzl, 2016).

Key performance indicator-

this is defined as the type of

measuring performance by

setting an indicator against

which the performance of

company will be assessed.

KEF Ltd uses this measure in

order to manage its financial

growth and stability. The

company has marked the key

performance indicator as the

operational cash flow. Now

for assessing the growth of the

company the company

compares its performance

against the operational cash

flow. That is the company

compares the cash flow of the

company with its past record

as well as with other

competitors in industry.

Dali speakers also use this

method for dealing with the

different problems and to find

their solutions. Thus. For this

their performance indicator is

the percentage of market

share. This is chosen as an

indicator because of the reason

that the market share decides

that how much the company is

popular within the market.

M 4 How dealing with financial problems help company in attaining success

The solution to the financial problem helps the company in attaining success to a great

extent. This is majorly because of the reason that if the company will take measures to solve the

financial problem then evidently the company will attain success. This is majorly because of the

a technique which is used in

order to compare the position

of one country with that of the

other and can compare its

problem in order to get some

solutions.

the company was the low

profits of the company. this

problem was solved by taking

benchmarking as a solution.

This is because of the reason

that this comparison will help

KEF Ltd to compare the

working with the popular

competitor and then find ways

of better performance of the

competitors.

order to analyse the fact that

what other companies are

bringing changes and how the

other companies are dealing

with the changes taking place

in the market (Nitzl, 2016).

Key performance indicator-

this is defined as the type of

measuring performance by

setting an indicator against

which the performance of

company will be assessed.

KEF Ltd uses this measure in

order to manage its financial

growth and stability. The

company has marked the key

performance indicator as the

operational cash flow. Now

for assessing the growth of the

company the company

compares its performance

against the operational cash

flow. That is the company

compares the cash flow of the

company with its past record

as well as with other

competitors in industry.

Dali speakers also use this

method for dealing with the

different problems and to find

their solutions. Thus. For this

their performance indicator is

the percentage of market

share. This is chosen as an

indicator because of the reason

that the market share decides

that how much the company is

popular within the market.

M 4 How dealing with financial problems help company in attaining success

The solution to the financial problem helps the company in attaining success to a great

extent. This is majorly because of the reason that if the company will take measures to solve the

financial problem then evidently the company will attain success. This is majorly because of the

reason that if the problem will be sought out then the company will work smoothly and this will

improve the working od the company.

D 3 Evaluation of planning tool in responding to financial problem leading to success

The planning tools also assist in responding to the financial problem as these tools help

the company in planning the way the working will take place (Shields, 2015). This is majorly

because of the fact that these planning tools will help the company in analysing the areas where

the company can improve its working and how they can develop the company to grow faster.

Hence, these planning tools will assist KEF Ltd in managing all the problems within the

company and will help the company in going in direction of success.

CONCLUSION

From the above report it can be summed up that use of management accounting is very

helpful for the company in managing its operations and working towards success. This is majorly

because of the reason that this will help the company in analysing and interpreting the financial

information and then taking decisions for the betterment of the company. The present report

discussed about the different management system like cost accounting, job costing and many

other.

Further the different report was discussed like budget report, financial report and other

was demonstrated. Next the calculation illustrating the marginal and absorption costing was done

along with different planning tools. These planning tools were like capital budget, variance

analysis and many others. in the end different tools for managing financial problems was

highlighted like benchmarking, key performance indicator and many others.

improve the working od the company.

D 3 Evaluation of planning tool in responding to financial problem leading to success

The planning tools also assist in responding to the financial problem as these tools help

the company in planning the way the working will take place (Shields, 2015). This is majorly

because of the fact that these planning tools will help the company in analysing the areas where

the company can improve its working and how they can develop the company to grow faster.

Hence, these planning tools will assist KEF Ltd in managing all the problems within the

company and will help the company in going in direction of success.

CONCLUSION

From the above report it can be summed up that use of management accounting is very

helpful for the company in managing its operations and working towards success. This is majorly

because of the reason that this will help the company in analysing and interpreting the financial

information and then taking decisions for the betterment of the company. The present report

discussed about the different management system like cost accounting, job costing and many

other.

Further the different report was discussed like budget report, financial report and other

was demonstrated. Next the calculation illustrating the marginal and absorption costing was done

along with different planning tools. These planning tools were like capital budget, variance

analysis and many others. in the end different tools for managing financial problems was

highlighted like benchmarking, key performance indicator and many others.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.