Management Accounting Report: Cost Analysis, Systems, and Budgets

VerifiedAdded on 2023/01/12

|25

|4847

|91

Report

AI Summary

This report delves into the core concepts of management accounting, examining its crucial requirements and diverse systems, with a specific focus on UCK Furniture. It explores the integration of management accounting (MA) systems within organizational processes, emphasizing the importance of timely and relevant information for managerial decision-making. The report analyzes cost accounting methods, including marginal and absorption costing, with detailed calculations and the preparation of income statements. It also covers the application of various management accounting techniques and the creation of financial reporting documents. Furthermore, the report discusses budgeting, its purpose, and how organizations adapt management accounting systems to address financial challenges. It concludes with an evaluation of planning tools and an analysis of how management accounting can enhance financial performance and ensure sustainable success. The report includes cost cards, income statements, and working notes to illustrate the concepts discussed.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

Section one.......................................................................................................................................3

1.1 Management Accounting and crucial necessary requirements its multiple systems:............3

1.2 Management Accounting Reporting:.....................................................................................5

1.3 Evaluation of benefits of Management accounting systems:................................................5

1.4 Critical evaluation about how MAS and MA is united within organisation’s processes:.....6

Section Two.....................................................................................................................................6

2.1 Cost card using marginal costing:..........................................................................................6

2.2. Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs:..........................................................................9

2.3 Accurately apply a range of management accounting techniques and produce a financial

reporting document:...................................................................................................................11

(a)...............................................................................................................................................11

(b.)..............................................................................................................................................12

3.1. Define and explain the purpose of budget:.........................................................................13

4.1 Compare how organisations are adapting management accounting systems to respond to 19

financial problems:....................................................................................................................19

4.2. Analyse how management accounting can help improve the financial performance of both

...................................................................................................................................................22

companies to achieve the sustainable success:..........................................................................22

4.3 Evaluation of the planning tools:.........................................................................................22

REFERENCES..............................................................................................................................25

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

Section one.......................................................................................................................................3

1.1 Management Accounting and crucial necessary requirements its multiple systems:............3

1.2 Management Accounting Reporting:.....................................................................................5

1.3 Evaluation of benefits of Management accounting systems:................................................5

1.4 Critical evaluation about how MAS and MA is united within organisation’s processes:.....6

Section Two.....................................................................................................................................6

2.1 Cost card using marginal costing:..........................................................................................6

2.2. Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs:..........................................................................9

2.3 Accurately apply a range of management accounting techniques and produce a financial

reporting document:...................................................................................................................11

(a)...............................................................................................................................................11

(b.)..............................................................................................................................................12

3.1. Define and explain the purpose of budget:.........................................................................13

4.1 Compare how organisations are adapting management accounting systems to respond to 19

financial problems:....................................................................................................................19

4.2. Analyse how management accounting can help improve the financial performance of both

...................................................................................................................................................22

companies to achieve the sustainable success:..........................................................................22

4.3 Evaluation of the planning tools:.........................................................................................22

REFERENCES..............................................................................................................................25

INTRODUCTION

Management Accounting contains the procedure of summarising management reports as

well as statements that support to offer reliable and prompt budgetary and fiscal information

needed by senior management to undertake important financial choices. Apart from financial

accounting, which offers annual accounts, management accounting offers regular accounting

updates within the company for users on a regular basis like administrative executives and

managing director (Akbar, 2010). The study report discusses about multiple core elements of

management accounting and its systems in relation to UCK furniture. It also involves

calculations and explanation about planning tools along with comparison of two entities as to

adoption of MA systems.

TASK

Section one

1.1 Management Accounting and crucial necessary requirements its multiple systems:

Managerial Accounting is method of bringing financial reports into the framework. This is

dedicated to information actually required by organizational administration. In simple words,

management accounting is collection of procedures and processes targeted at presenting

information for the managers, taking decisions effectively and retaining good control of

enterprise resources (Callahan, Stetz and Brooks, 2011). Through this

mechanism entity's internal financial dept exchanges records and details (like balance sheets and

payslips) with managers of the organization. The managers use these reports and details to render

informed and reliable business operations, organization, and business productivity decisions.

Main perquisite of management accounting is adoption of systematic framework which

consists of several key processes which enable managers to take effective business decisions.

This also require collection, processing and transmission of critical information for managerial

decision making.

MA is mostly important in providing timely, relevant and effective information to top

management and other key managing personnel. By offering guidance on future expenses and

sales, management accounting makes important contributes to the business's funds forecasts and

long term of fiscal planning. This also provides mentor the cycle of planning, tracking and

managing the budget according to defined strategies and processes. Management

Management Accounting contains the procedure of summarising management reports as

well as statements that support to offer reliable and prompt budgetary and fiscal information

needed by senior management to undertake important financial choices. Apart from financial

accounting, which offers annual accounts, management accounting offers regular accounting

updates within the company for users on a regular basis like administrative executives and

managing director (Akbar, 2010). The study report discusses about multiple core elements of

management accounting and its systems in relation to UCK furniture. It also involves

calculations and explanation about planning tools along with comparison of two entities as to

adoption of MA systems.

TASK

Section one

1.1 Management Accounting and crucial necessary requirements its multiple systems:

Managerial Accounting is method of bringing financial reports into the framework. This is

dedicated to information actually required by organizational administration. In simple words,

management accounting is collection of procedures and processes targeted at presenting

information for the managers, taking decisions effectively and retaining good control of

enterprise resources (Callahan, Stetz and Brooks, 2011). Through this

mechanism entity's internal financial dept exchanges records and details (like balance sheets and

payslips) with managers of the organization. The managers use these reports and details to render

informed and reliable business operations, organization, and business productivity decisions.

Main perquisite of management accounting is adoption of systematic framework which

consists of several key processes which enable managers to take effective business decisions.

This also require collection, processing and transmission of critical information for managerial

decision making.

MA is mostly important in providing timely, relevant and effective information to top

management and other key managing personnel. By offering guidance on future expenses and

sales, management accounting makes important contributes to the business's funds forecasts and

long term of fiscal planning. This also provides mentor the cycle of planning, tracking and

managing the budget according to defined strategies and processes. Management

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

accounting helps to align performance expectations and organization expectations or forecasts

for actual results/outcomes, and evaluate any variances. It is achieved by means of a technique

recognized as the analysis of variation.

The organisations can maximize their degree of efficiency in handling the business

records and records in a smarter way with aid of management accounting

systems. Different system renders the information processing simpler for corporation. MA

system leads to the creation of successful strategic strategies. This lets the organization create

more realistic strategies so that they could better strengthen their performance levels. MA system

is quite helpful when it comes to properly managing the actual expenses of the company. This

specific program helps to recognize the companies 'perfect cost management including cost

controlling approaches which helps to boost the enterprises' performance level.

Inventory management system: It is mainly a practice that defines the configuration and

placement of the raw materials, finished goods, processed goods in storage. It is feasible to

implement the normal and prescribed path of operation and storing of products promptly at

different locations with aim to safeguarding these stock items. This is a system cantered on

a technical method like LIFO, FIFO etc. that are used to track manufacturing levels, orders,

shipments and sales (Hopper and Bui, 2016). In certain scenarios, this method is utilized in the

manufacturing field to generate a purchase order, bills of items, as well as other product-relevant

services. For UCK Furniture it is primarily necessary to use this system in order to suppress

over-storage and often under-stocking concerns throughout inventories handling processes.

Job costing system: This is regulated system of evaluating the costs or expenses they pay

on a single job which is relevant for organization. The framework is widely employed

for allocation of expenses for particular projects of a company. Many companies utilizing this

accounting method to fix specific costs for every job which is effectively needed to lower

manufacturing costs that further lead to optimizing UCK Furniture business's competitiveness as

well as increasing profitability.

Price optimisation: This approach is employed against buyer desire to pay to achieve the

optimal spot pricing or demand maximisation. Company devotes a substantial period to demand

control and ensuring that their products are distributed effectively at the appropriate prices while

also making rational profits. Complying with commercial priorities is necessary for UCK

for actual results/outcomes, and evaluate any variances. It is achieved by means of a technique

recognized as the analysis of variation.

The organisations can maximize their degree of efficiency in handling the business

records and records in a smarter way with aid of management accounting

systems. Different system renders the information processing simpler for corporation. MA

system leads to the creation of successful strategic strategies. This lets the organization create

more realistic strategies so that they could better strengthen their performance levels. MA system

is quite helpful when it comes to properly managing the actual expenses of the company. This

specific program helps to recognize the companies 'perfect cost management including cost

controlling approaches which helps to boost the enterprises' performance level.

Inventory management system: It is mainly a practice that defines the configuration and

placement of the raw materials, finished goods, processed goods in storage. It is feasible to

implement the normal and prescribed path of operation and storing of products promptly at

different locations with aim to safeguarding these stock items. This is a system cantered on

a technical method like LIFO, FIFO etc. that are used to track manufacturing levels, orders,

shipments and sales (Hopper and Bui, 2016). In certain scenarios, this method is utilized in the

manufacturing field to generate a purchase order, bills of items, as well as other product-relevant

services. For UCK Furniture it is primarily necessary to use this system in order to suppress

over-storage and often under-stocking concerns throughout inventories handling processes.

Job costing system: This is regulated system of evaluating the costs or expenses they pay

on a single job which is relevant for organization. The framework is widely employed

for allocation of expenses for particular projects of a company. Many companies utilizing this

accounting method to fix specific costs for every job which is effectively needed to lower

manufacturing costs that further lead to optimizing UCK Furniture business's competitiveness as

well as increasing profitability.

Price optimisation: This approach is employed against buyer desire to pay to achieve the

optimal spot pricing or demand maximisation. Company devotes a substantial period to demand

control and ensuring that their products are distributed effectively at the appropriate prices while

also making rational profits. Complying with commercial priorities is necessary for UCK

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Furniture to match its customer expectations related to price and demand. In UCK this by this

system entity can fix effective price of products at which demand and profit margin is maximum.

1.2 Management Accounting Reporting:

Cost Report: Costs are determined under this report based on the charges of materials,

wages, overhead costs and other costs/expenses. The overall costs involved in the processing

or manufacturing are divided by the amounts of units processed to come at unit cost. Cost reports

incorporate all details to help managers determine the cost per unit of manufacturing goods to

include an internal accountability framework. In UCK furniture this report is used by production

managers to asses the cost of each manufactured furniture item.

Job Cost Reports: Job cost reports usually imply costs on a particular kind

of job/task that company is undertaking. These are commonly paired with revenue forecasts such

that managing staff can measure the effectiveness of the task/job. In UCK furniture, it allows

them acknowledge the company 'greater-earning zones so that it should concentrate more

attention on tasks with minor earnings levels rather than wasting efforts and energy there.

This report used to review costs as specified job is under way so that excess factors can be

corrected until costs grow out of grasp.

Inventory Report: This essential report is used by almost all the organisation specially

manufacturing concerns like UCK which have wide amount and range of inventories. This

contributes in managing each single items of inventory within entity. This report classifies all the

inventories items based upon their specific importance, cost and process or division. It also

defines basis of measuring of cost of different inventories. In UCK, this report is used by

different units of manufacturing to assess the ultimate value of stock left at the end of a certain

period which may be daily, weekly, monthly or yearly as per the requirement of corporation.

1.3 Evaluation of benefits of Management accounting systems:

Systems Major benefits

Inventory Management System In UCK, this system benefitable for managers

to assess or evaluate the accurate cost of

different range of inventories as well as to

recognise the need of placing order. This also

helpful in pointing out areas which are leading

system entity can fix effective price of products at which demand and profit margin is maximum.

1.2 Management Accounting Reporting:

Cost Report: Costs are determined under this report based on the charges of materials,

wages, overhead costs and other costs/expenses. The overall costs involved in the processing

or manufacturing are divided by the amounts of units processed to come at unit cost. Cost reports

incorporate all details to help managers determine the cost per unit of manufacturing goods to

include an internal accountability framework. In UCK furniture this report is used by production

managers to asses the cost of each manufactured furniture item.

Job Cost Reports: Job cost reports usually imply costs on a particular kind

of job/task that company is undertaking. These are commonly paired with revenue forecasts such

that managing staff can measure the effectiveness of the task/job. In UCK furniture, it allows

them acknowledge the company 'greater-earning zones so that it should concentrate more

attention on tasks with minor earnings levels rather than wasting efforts and energy there.

This report used to review costs as specified job is under way so that excess factors can be

corrected until costs grow out of grasp.

Inventory Report: This essential report is used by almost all the organisation specially

manufacturing concerns like UCK which have wide amount and range of inventories. This

contributes in managing each single items of inventory within entity. This report classifies all the

inventories items based upon their specific importance, cost and process or division. It also

defines basis of measuring of cost of different inventories. In UCK, this report is used by

different units of manufacturing to assess the ultimate value of stock left at the end of a certain

period which may be daily, weekly, monthly or yearly as per the requirement of corporation.

1.3 Evaluation of benefits of Management accounting systems:

Systems Major benefits

Inventory Management System In UCK, this system benefitable for managers

to assess or evaluate the accurate cost of

different range of inventories as well as to

recognise the need of placing order. This also

helpful in pointing out areas which are leading

to increased cost of different inventories.

Job Costing System In UCK, this system is beneficial in several

units which are working on project basis to

establish accountability and asses the cost of

different jobs lined with project.

Price Optimisation This is quite beneficial of UCK in setting

effective and efficient prices for its products

that also ensure maximum demand and

sustainability in profitability margin. It also

provides competitive advantages by assisting

in determining prices’ effect on specific

product item demand (Lavia López and Hiebl,

2014).

1.4 Critical evaluation about how MAS and MA is united within organisation’s processes:

Multiple operations and processes act as core ground of different systems of MA as

organisational processes develop base for adoption of these systems. Outcomes of different

processes of organisation are essential requirements of aforementioned systems. As in UCK,

production, accounting and finance processes are carried out by managers which provides key

information and reports to price optimisation systems and inventory management system like

cost details, inventory status, demands and other accounting or fiscal information (Leitner,

2013). Thus, is essential to integrate all the processes with MA systems.

Section Two

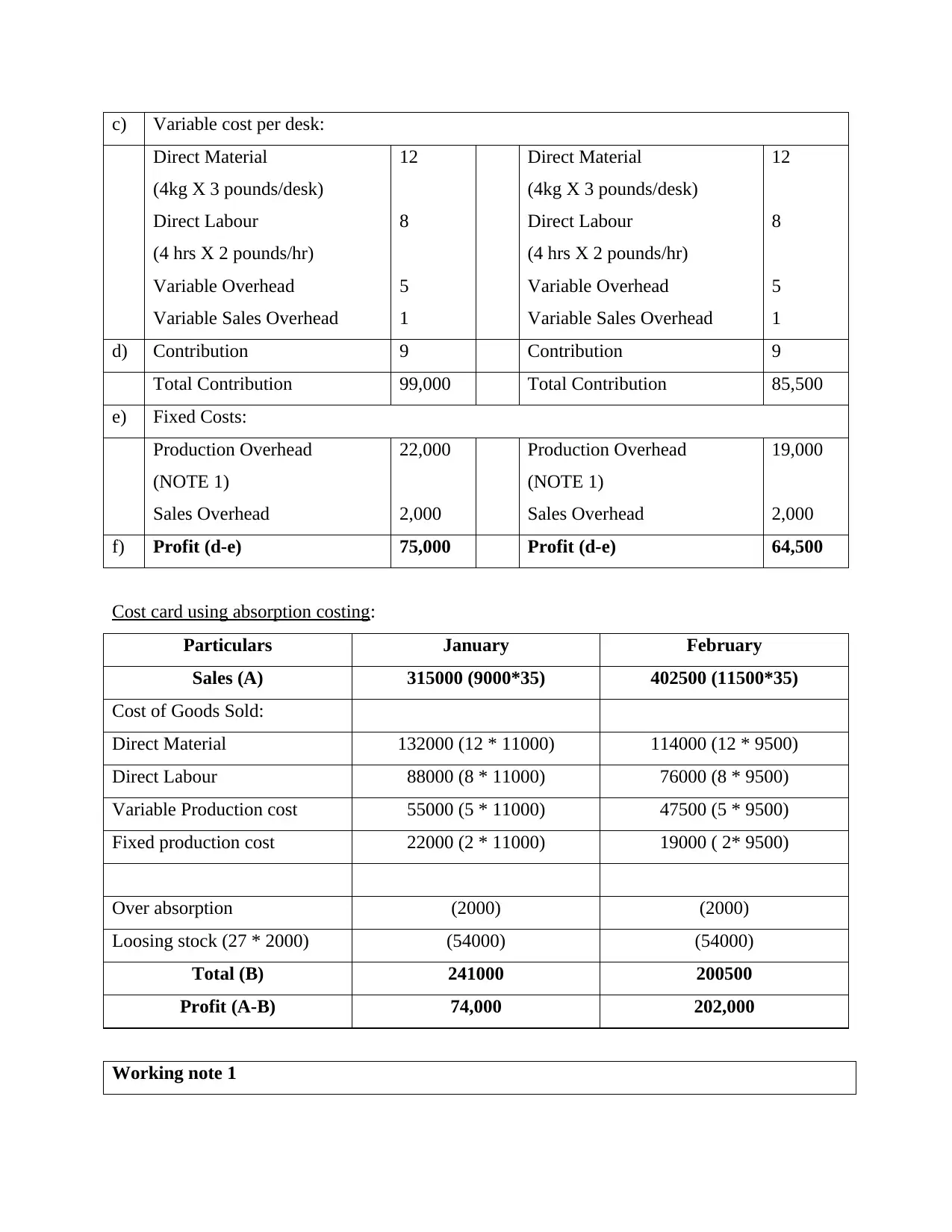

2.1 Cost card using marginal costing:

January February

Particulars Amounts

(GBP)

Particulars Amounts

(GBP)

a) Units Produced

(11000)

Units Produced

(9500)

b) Sales Price Per Desk 35 Sales Price Per Desk 35

Job Costing System In UCK, this system is beneficial in several

units which are working on project basis to

establish accountability and asses the cost of

different jobs lined with project.

Price Optimisation This is quite beneficial of UCK in setting

effective and efficient prices for its products

that also ensure maximum demand and

sustainability in profitability margin. It also

provides competitive advantages by assisting

in determining prices’ effect on specific

product item demand (Lavia López and Hiebl,

2014).

1.4 Critical evaluation about how MAS and MA is united within organisation’s processes:

Multiple operations and processes act as core ground of different systems of MA as

organisational processes develop base for adoption of these systems. Outcomes of different

processes of organisation are essential requirements of aforementioned systems. As in UCK,

production, accounting and finance processes are carried out by managers which provides key

information and reports to price optimisation systems and inventory management system like

cost details, inventory status, demands and other accounting or fiscal information (Leitner,

2013). Thus, is essential to integrate all the processes with MA systems.

Section Two

2.1 Cost card using marginal costing:

January February

Particulars Amounts

(GBP)

Particulars Amounts

(GBP)

a) Units Produced

(11000)

Units Produced

(9500)

b) Sales Price Per Desk 35 Sales Price Per Desk 35

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

c) Variable cost per desk:

Direct Material

(4kg X 3 pounds/desk)

Direct Labour

(4 hrs X 2 pounds/hr)

Variable Overhead

Variable Sales Overhead

12

8

5

1

Direct Material

(4kg X 3 pounds/desk)

Direct Labour

(4 hrs X 2 pounds/hr)

Variable Overhead

Variable Sales Overhead

12

8

5

1

d) Contribution 9 Contribution 9

Total Contribution 99,000 Total Contribution 85,500

e) Fixed Costs:

Production Overhead

(NOTE 1)

Sales Overhead

22,000

2,000

Production Overhead

(NOTE 1)

Sales Overhead

19,000

2,000

f) Profit (d-e) 75,000 Profit (d-e) 64,500

Cost card using absorption costing:

Particulars January February

Sales (A) 315000 (9000*35) 402500 (11500*35)

Cost of Goods Sold:

Direct Material 132000 (12 * 11000) 114000 (12 * 9500)

Direct Labour 88000 (8 * 11000) 76000 (8 * 9500)

Variable Production cost 55000 (5 * 11000) 47500 (5 * 9500)

Fixed production cost 22000 (2 * 11000) 19000 ( 2* 9500)

Over absorption (2000) (2000)

Loosing stock (27 * 2000) (54000) (54000)

Total (B) 241000 200500

Profit (A-B) 74,000 202,000

Working note 1

Direct Material

(4kg X 3 pounds/desk)

Direct Labour

(4 hrs X 2 pounds/hr)

Variable Overhead

Variable Sales Overhead

12

8

5

1

Direct Material

(4kg X 3 pounds/desk)

Direct Labour

(4 hrs X 2 pounds/hr)

Variable Overhead

Variable Sales Overhead

12

8

5

1

d) Contribution 9 Contribution 9

Total Contribution 99,000 Total Contribution 85,500

e) Fixed Costs:

Production Overhead

(NOTE 1)

Sales Overhead

22,000

2,000

Production Overhead

(NOTE 1)

Sales Overhead

19,000

2,000

f) Profit (d-e) 75,000 Profit (d-e) 64,500

Cost card using absorption costing:

Particulars January February

Sales (A) 315000 (9000*35) 402500 (11500*35)

Cost of Goods Sold:

Direct Material 132000 (12 * 11000) 114000 (12 * 9500)

Direct Labour 88000 (8 * 11000) 76000 (8 * 9500)

Variable Production cost 55000 (5 * 11000) 47500 (5 * 9500)

Fixed production cost 22000 (2 * 11000) 19000 ( 2* 9500)

Over absorption (2000) (2000)

Loosing stock (27 * 2000) (54000) (54000)

Total (B) 241000 200500

Profit (A-B) 74,000 202,000

Working note 1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Production overhead is considered taking into account average production each month, i.e. 10000

units.

Therefore, for the month of Jan. overhead would amount to = (20,000 / 10,000) * 11000

Thus, for the month of Feb., the overhead would amount to = (20,000 / 10,000) * 9500

(b)Explain the potential merits and demerits of the both methods.

Marginal costing method- This can be understood as a type of accounting technique

which is linked to taking fixed cost as cost of period and variable cost as cost of product. It has

some benefits and drawbacks such as:

Benefits: This reduces the level of expenses recover or under recovery because fixed overheads

are separated from production costs (Renz, 2016).

Drawbacks- Cost division into fixed and variable is a challenging task. Fixed costs should not

allow into consideration semi-variable or semi-fixed expenses.

Absorption costing method- It is variant in nature as compared to marginal costing method. In

this fixed cost and variable costs are taken as cost of product. Underneath, its benefits and

drawbacks are mentioned:

Benefits- One of the major benefits of taking absorption costs is that GAAP is compliant and

essential in this method.

Drawbacks- It is not beneficial for operational efficiency (Otley and Emmanuel, 2013).

units.

Therefore, for the month of Jan. overhead would amount to = (20,000 / 10,000) * 11000

Thus, for the month of Feb., the overhead would amount to = (20,000 / 10,000) * 9500

(b)Explain the potential merits and demerits of the both methods.

Marginal costing method- This can be understood as a type of accounting technique

which is linked to taking fixed cost as cost of period and variable cost as cost of product. It has

some benefits and drawbacks such as:

Benefits: This reduces the level of expenses recover or under recovery because fixed overheads

are separated from production costs (Renz, 2016).

Drawbacks- Cost division into fixed and variable is a challenging task. Fixed costs should not

allow into consideration semi-variable or semi-fixed expenses.

Absorption costing method- It is variant in nature as compared to marginal costing method. In

this fixed cost and variable costs are taken as cost of product. Underneath, its benefits and

drawbacks are mentioned:

Benefits- One of the major benefits of taking absorption costs is that GAAP is compliant and

essential in this method.

Drawbacks- It is not beneficial for operational efficiency (Otley and Emmanuel, 2013).

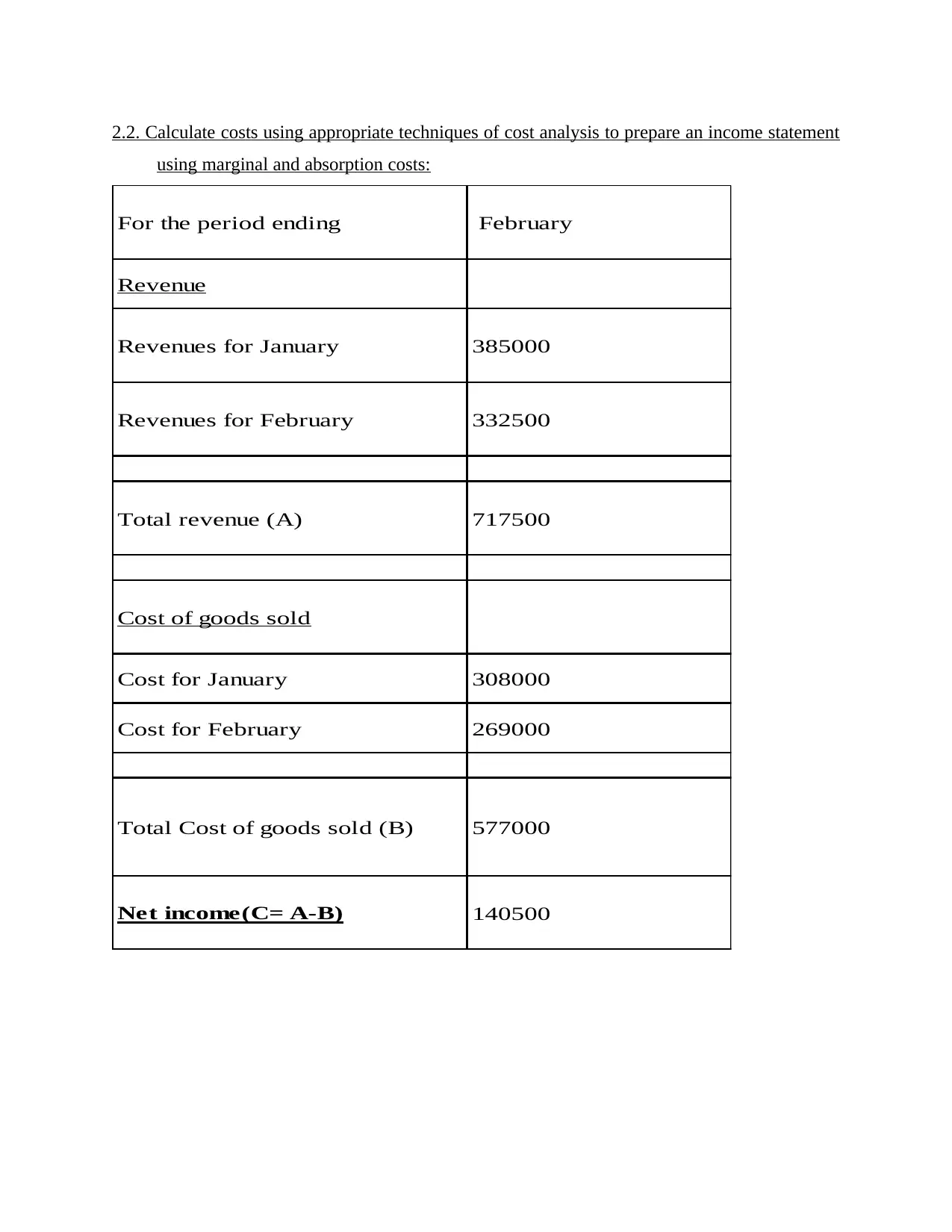

2.2. Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs:

For the period ending February

Revenue

Revenues for January 385000

Revenues for February 332500

Total revenue (A) 717500

Cost of goods sold

Cost for January 308000

Cost for February 269000

Total Cost of goods sold (B) 577000

Net income(C= A-B) 140500

using marginal and absorption costs:

For the period ending February

Revenue

Revenues for January 385000

Revenues for February 332500

Total revenue (A) 717500

Cost of goods sold

Cost for January 308000

Cost for February 269000

Total Cost of goods sold (B) 577000

Net income(C= A-B) 140500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Descriptions Descript

ions

Amount

(GBP)

Descript

ions

Amount

(GBP)

Units produced 11000 9500

a) Direct Material

(4kilo-

gramx3p

ound/kil

o-

gramx11

000)

132000

(4kilo-

gramx3p

ound/kil

o-

gramx95

00)

114000

b) Direct Labour

(4 hours

x

2pound/h

ours

x11000)

88000

(4 hours

x

2pound/h

ours

x9500)

76000

c) Variable Overhead

(5GBP/d

eskx110

00)

55000

(5GBP/d

eskx950

0)

47500

d) Prime Cost 275000 237500

e) Production overhead 20000 20000

f) Cost of goods produced 295000 257500

g) Variable revenues cost

(1pound/

deskx11

000)

11000

(1pound/

deskx95

00)

9500

h) fixed selling cost 2000 2000

i) Cost of Goods sold 308000 269000

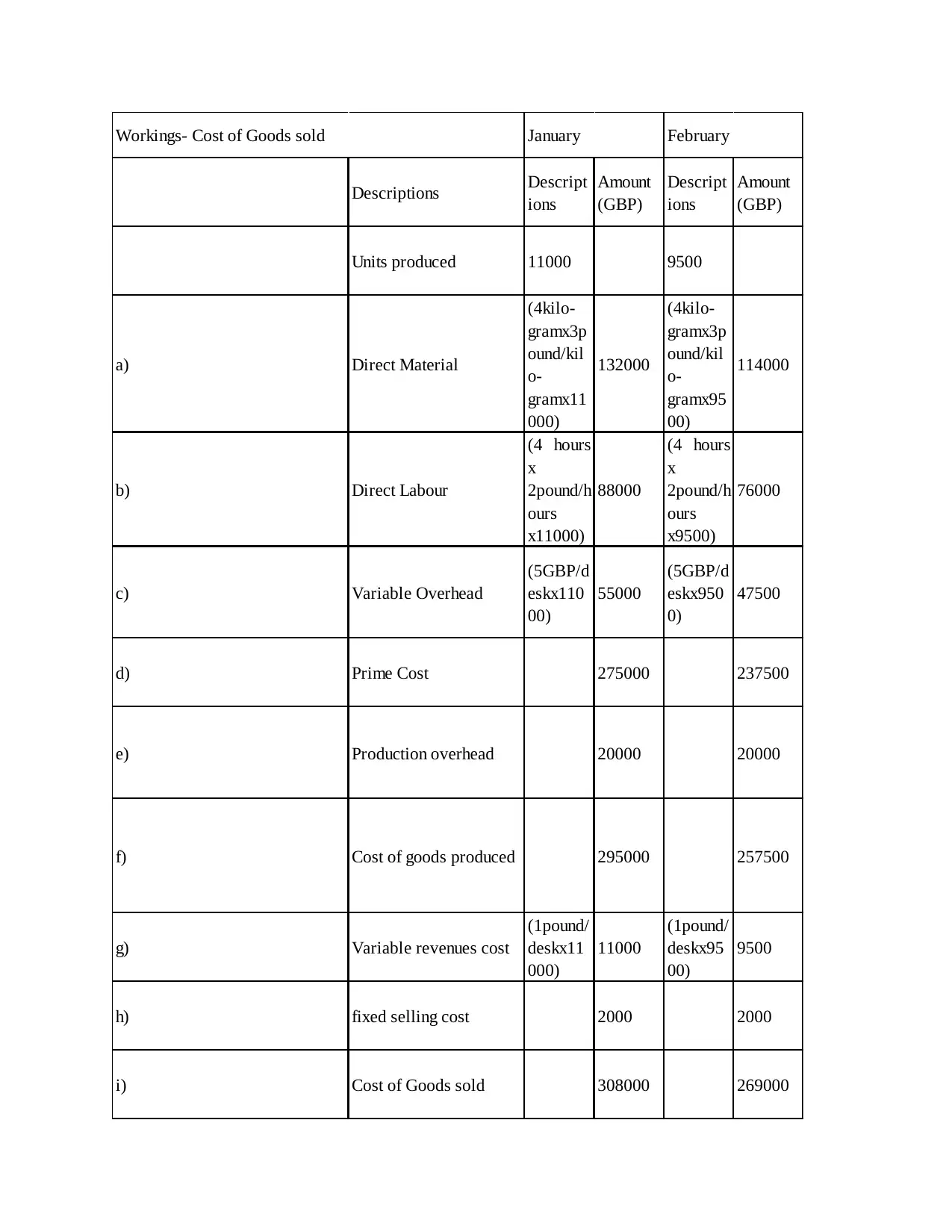

Workings- Cost of Goods sold January February

ions

Amount

(GBP)

Descript

ions

Amount

(GBP)

Units produced 11000 9500

a) Direct Material

(4kilo-

gramx3p

ound/kil

o-

gramx11

000)

132000

(4kilo-

gramx3p

ound/kil

o-

gramx95

00)

114000

b) Direct Labour

(4 hours

x

2pound/h

ours

x11000)

88000

(4 hours

x

2pound/h

ours

x9500)

76000

c) Variable Overhead

(5GBP/d

eskx110

00)

55000

(5GBP/d

eskx950

0)

47500

d) Prime Cost 275000 237500

e) Production overhead 20000 20000

f) Cost of goods produced 295000 257500

g) Variable revenues cost

(1pound/

deskx11

000)

11000

(1pound/

deskx95

00)

9500

h) fixed selling cost 2000 2000

i) Cost of Goods sold 308000 269000

Workings- Cost of Goods sold January February

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

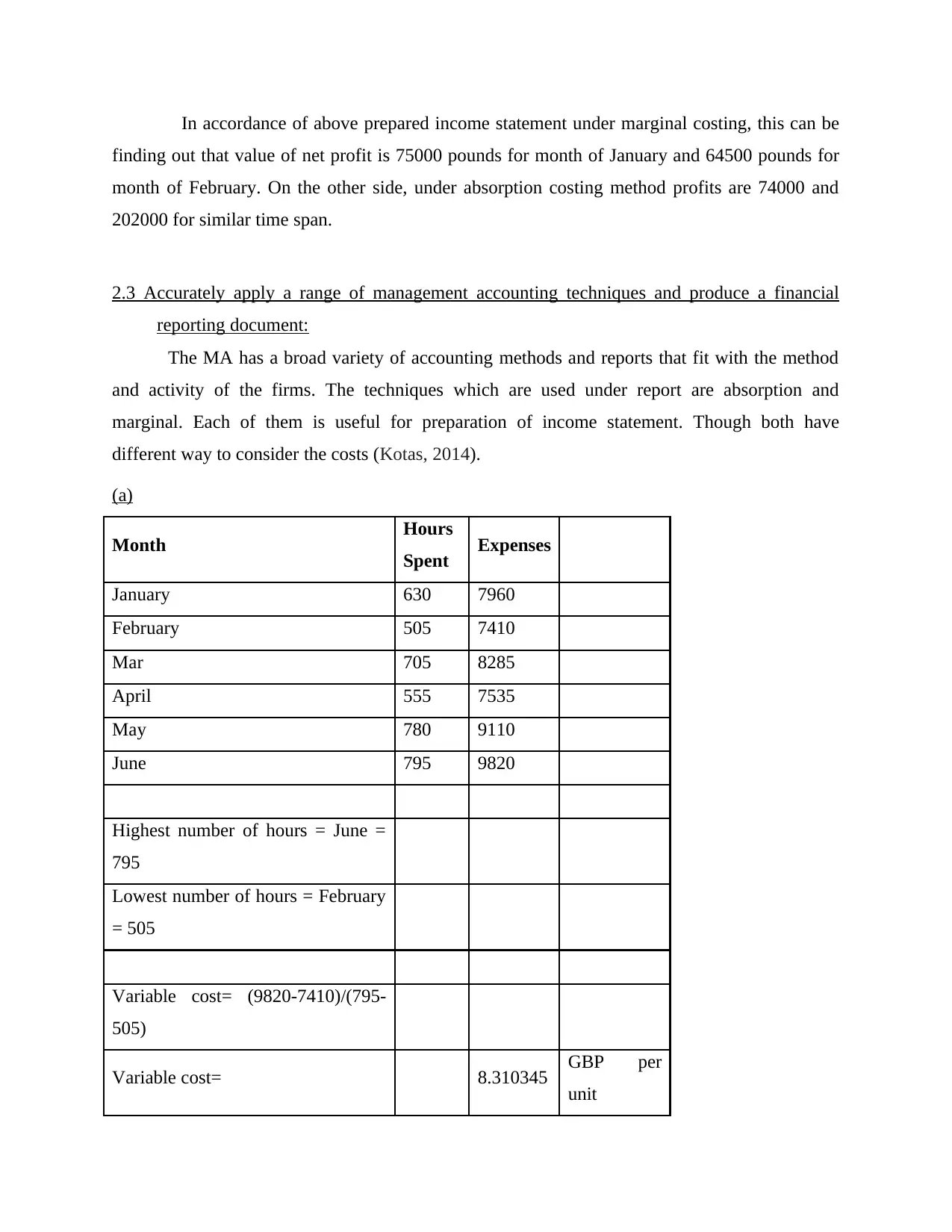

In accordance of above prepared income statement under marginal costing, this can be

finding out that value of net profit is 75000 pounds for month of January and 64500 pounds for

month of February. On the other side, under absorption costing method profits are 74000 and

202000 for similar time span.

2.3 Accurately apply a range of management accounting techniques and produce a financial

reporting document:

The MA has a broad variety of accounting methods and reports that fit with the method

and activity of the firms. The techniques which are used under report are absorption and

marginal. Each of them is useful for preparation of income statement. Though both have

different way to consider the costs (Kotas, 2014).

(a)

Month Hours

Spent Expenses

January 630 7960

February 505 7410

Mar 705 8285

April 555 7535

May 780 9110

June 795 9820

Highest number of hours = June =

795

Lowest number of hours = February

= 505

Variable cost= (9820-7410)/(795-

505)

Variable cost= 8.310345 GBP per

unit

finding out that value of net profit is 75000 pounds for month of January and 64500 pounds for

month of February. On the other side, under absorption costing method profits are 74000 and

202000 for similar time span.

2.3 Accurately apply a range of management accounting techniques and produce a financial

reporting document:

The MA has a broad variety of accounting methods and reports that fit with the method

and activity of the firms. The techniques which are used under report are absorption and

marginal. Each of them is useful for preparation of income statement. Though both have

different way to consider the costs (Kotas, 2014).

(a)

Month Hours

Spent Expenses

January 630 7960

February 505 7410

Mar 705 8285

April 555 7535

May 780 9110

June 795 9820

Highest number of hours = June =

795

Lowest number of hours = February

= 505

Variable cost= (9820-7410)/(795-

505)

Variable cost= 8.310345 GBP per

unit

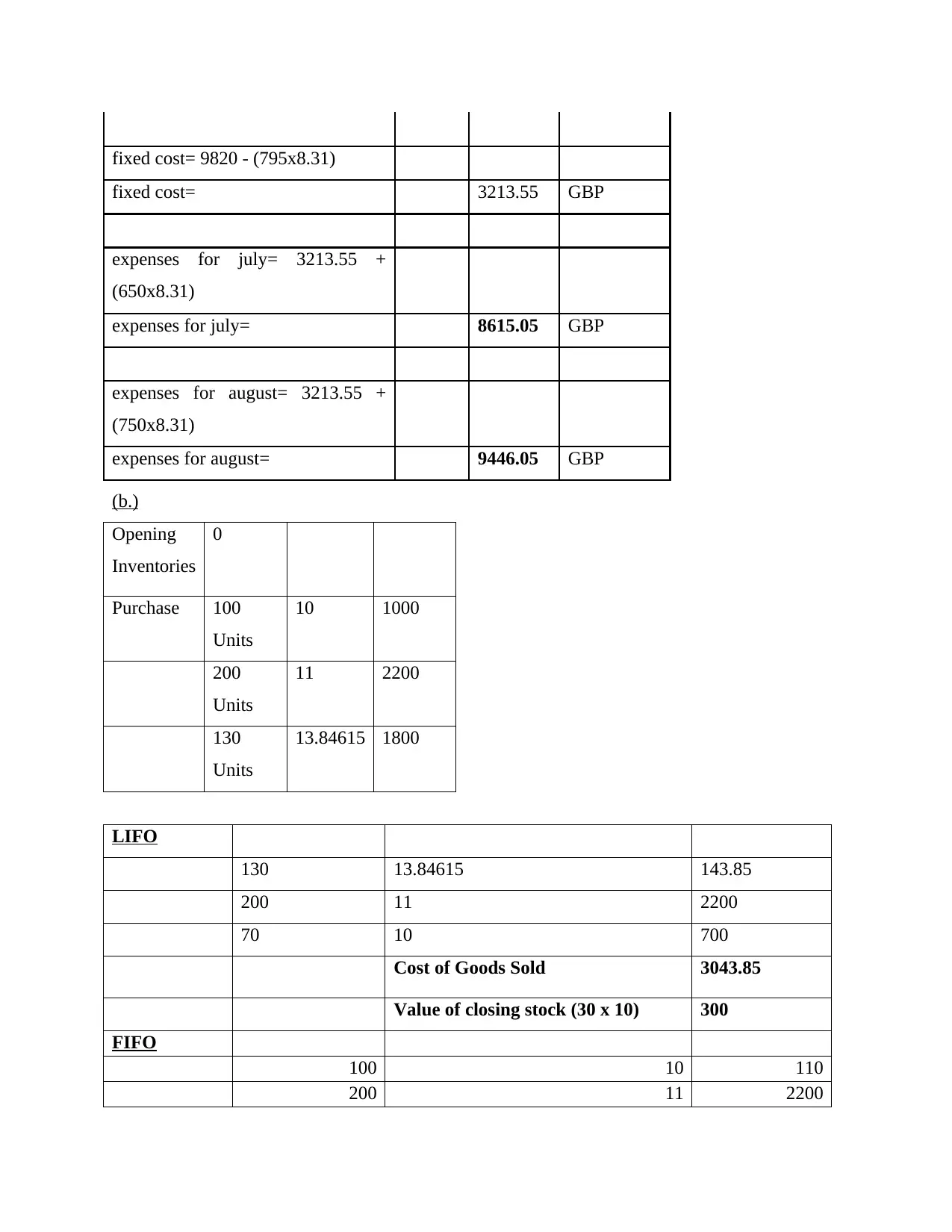

fixed cost= 9820 - (795x8.31)

fixed cost= 3213.55 GBP

expenses for july= 3213.55 +

(650x8.31)

expenses for july= 8615.05 GBP

expenses for august= 3213.55 +

(750x8.31)

expenses for august= 9446.05 GBP

(b.)

Opening

Inventories

0

Purchase 100

Units

10 1000

200

Units

11 2200

130

Units

13.84615 1800

LIFO

130 13.84615 143.85

200 11 2200

70 10 700

Cost of Goods Sold 3043.85

Value of closing stock (30 x 10) 300

FIFO

100 10 110

200 11 2200

fixed cost= 3213.55 GBP

expenses for july= 3213.55 +

(650x8.31)

expenses for july= 8615.05 GBP

expenses for august= 3213.55 +

(750x8.31)

expenses for august= 9446.05 GBP

(b.)

Opening

Inventories

0

Purchase 100

Units

10 1000

200

Units

11 2200

130

Units

13.84615 1800

LIFO

130 13.84615 143.85

200 11 2200

70 10 700

Cost of Goods Sold 3043.85

Value of closing stock (30 x 10) 300

FIFO

100 10 110

200 11 2200

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.