Management Accounting Systems, Financial Reports, and Cost Analysis

VerifiedAdded on 2023/01/03

|18

|4659

|81

Report

AI Summary

This report provides a comprehensive overview of management accounting practices within Capital Joinery. It begins by defining management accounting and outlining the essential requirements of various systems, including price optimization, job costing, inventory management, and cost accounting. The report then describes different management accounting reports such as budget, accounts receivable, performance, and inventory management reports, evaluating their advantages. Furthermore, it includes calculations for income statements using marginal and absorption costing methods, along with material variance analysis and inventory valuation using LIFO and average cost methods. The report also discusses budgetary control tools, their advantages, and disadvantages, and analyzes the adoption of management accounting systems in response to financial problems, including evaluating ways planning tools respond for solving problems related to finance for leading organization to sustainable success.

Management

Accounting Systems

Accounting Systems

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Description of management accounting and providing essential requirements of different

systems of management accounting: ..........................................................................................1

P2 Describing various methods of management accounting reports:..........................................3

M1 Evaluating advantages of management accounting system and its application in context to

business:.......................................................................................................................................4

D1 Critically evaluating ways in which management accounting reports and systems are

integrated within process of organization:...................................................................................4

TASK 2............................................................................................................................................5

P3 Calculation of adequate techniques of cost analysis for the purpose of preparing income

statement by marginal and absorption costs:...............................................................................5

M2 Accurate application of techniques of management accounting for production of financial

reporting documents:...................................................................................................................9

D2 Production of financial reports that accurately applies and interprets business activities:....9

TASK 3............................................................................................................................................9

P4 Evaluating advantages and disadvantages of different planning tools of budgetary control: 9

M3 Uses of different planning tools that are applied for budget preparation and forecasting:. 11

TASK 4..........................................................................................................................................11

P4 Comparing adoption of management accounting systems by organizations as a respond to

financial problems:.....................................................................................................................11

M4 Analysis of respond towards financial problem with management accounting for achieving

success of business:....................................................................................................................13

D3: Evaluating ways in which planning tools respond for solving problems related to finance

for leading organization to sustainable success:........................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Description of management accounting and providing essential requirements of different

systems of management accounting: ..........................................................................................1

P2 Describing various methods of management accounting reports:..........................................3

M1 Evaluating advantages of management accounting system and its application in context to

business:.......................................................................................................................................4

D1 Critically evaluating ways in which management accounting reports and systems are

integrated within process of organization:...................................................................................4

TASK 2............................................................................................................................................5

P3 Calculation of adequate techniques of cost analysis for the purpose of preparing income

statement by marginal and absorption costs:...............................................................................5

M2 Accurate application of techniques of management accounting for production of financial

reporting documents:...................................................................................................................9

D2 Production of financial reports that accurately applies and interprets business activities:....9

TASK 3............................................................................................................................................9

P4 Evaluating advantages and disadvantages of different planning tools of budgetary control: 9

M3 Uses of different planning tools that are applied for budget preparation and forecasting:. 11

TASK 4..........................................................................................................................................11

P4 Comparing adoption of management accounting systems by organizations as a respond to

financial problems:.....................................................................................................................11

M4 Analysis of respond towards financial problem with management accounting for achieving

success of business:....................................................................................................................13

D3: Evaluating ways in which planning tools respond for solving problems related to finance

for leading organization to sustainable success:........................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting can be explained as a practice that involves identification,

measurement, analysis, interpretation as well as communication of financial data that an

organization pertains. This information is utilised by managers of company with the motive of

obtaining goals of an enterprise. It differs from financial accounting as purpose consisted with

management accounting is providing assistance to internal users of an entity for making well-

informed decisions (Bebbington, 2017). Basis of this report is examination of management

accounting practices incorporated in Capital Joinery. In this report various types of management

accounting systems are evaluated along with their essential requirements. Further, management

accounting reports are described and essential requirement incorporated with it is analysed.

Along with it, income statement in prepared on the basis of marginal as well as absorption

costing. Further, planning tools consisted for budgetary control is identified and their advantages

as well as limitations are discussed. Additionally, financial problems are interpreted and

monitory control measures which can be implemented for solving such issues are identified.

TASK 1

P1 Description of management accounting and providing essential requirements of different

systems of management accounting:

Management accounting is a technique that records transactions related to finance

which can be used by managers to gain necessary information about company's position for

improving their strategy making procedure and making adequate decisions regarding important

matters of n organization (Bromwich and Lapsley, 2017). Management accounting system is a

platform that tracks financial details of an enterprise. It enables management of Capital Joinery

to gain clear overview about fund transactions pertained in business. Management accounting

system are of various types which are discussed below along with their benefits:

Price optimisation system: This system is utilised for calculating variations in demand

in relevance to changes in price level of products of company. This data results in

combination of cost information and level of stock for recommending suitable price that

leads to profit improvement.

Essential requirement: Application of this system in Capital Joinery results in providing

financial benefit to an enterprise as adequate price level of product helps in attracting and

1

Management accounting can be explained as a practice that involves identification,

measurement, analysis, interpretation as well as communication of financial data that an

organization pertains. This information is utilised by managers of company with the motive of

obtaining goals of an enterprise. It differs from financial accounting as purpose consisted with

management accounting is providing assistance to internal users of an entity for making well-

informed decisions (Bebbington, 2017). Basis of this report is examination of management

accounting practices incorporated in Capital Joinery. In this report various types of management

accounting systems are evaluated along with their essential requirements. Further, management

accounting reports are described and essential requirement incorporated with it is analysed.

Along with it, income statement in prepared on the basis of marginal as well as absorption

costing. Further, planning tools consisted for budgetary control is identified and their advantages

as well as limitations are discussed. Additionally, financial problems are interpreted and

monitory control measures which can be implemented for solving such issues are identified.

TASK 1

P1 Description of management accounting and providing essential requirements of different

systems of management accounting:

Management accounting is a technique that records transactions related to finance

which can be used by managers to gain necessary information about company's position for

improving their strategy making procedure and making adequate decisions regarding important

matters of n organization (Bromwich and Lapsley, 2017). Management accounting system is a

platform that tracks financial details of an enterprise. It enables management of Capital Joinery

to gain clear overview about fund transactions pertained in business. Management accounting

system are of various types which are discussed below along with their benefits:

Price optimisation system: This system is utilised for calculating variations in demand

in relevance to changes in price level of products of company. This data results in

combination of cost information and level of stock for recommending suitable price that

leads to profit improvement.

Essential requirement: Application of this system in Capital Joinery results in providing

financial benefit to an enterprise as adequate price level of product helps in attracting and

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

retaining customers for longer time period. It fulfils information requirement of an enterprise in

relation to customer reactions through demand variations. It helps is aligning business goals and

expectations of consumers (Burritt, 2015). It automates the process of price setting and helps in

gaining optimization in context to price. Hence, quick decisions can be made by management

which pertains positive influence on company.

Job costing system: It involves procedure of information accumulation in relation to

costs that is associated with specific job or production process. This tracking method

determines cost of separate job which enables Capital Joinery to track information

regarding performance of each job.

Essential requirement: This system of job costing enhances profitability of Capital Joinery as it

separately assigns cost to each operations which provides required information to managers to

calculate profit margin of each job. This helps in setting adequate organizational structure in a

way that ensures expense minimization and performance maximization. It improves accuracy

and scalability in monitoring of business operations (Callahan, Stetz and Brooks, 2016).

Inventory management system: Utilization of this system is for the purpose of

managing and monitoring position of stock in in organization. It tracks amount of

inventory available in Capital Joinery which provides warning to managers to purchase of

required inventory and avoid over stocking as well as under stocking.

Essential requirement: Inventory management system is vital for analysing level of stock in

business. This helps management in keeping required information regarding stock and ensuring

that needed safety stock is available so that business operations are not hindered. This

information play a critical role in adopting efficient management style for productivity

improvement.

Cost accounting system: It is a platform which tracks cost information associated in

business. In other words, this framework helps managers of Capital Joinery in estimating

cost of its products with the motive of profitability analysis (Davies and Crawford,

2018). This system computes expenses associated with manufacturing or production

costs. Different types of costs, such as, labour, raw material, overhead etc. are taken

consideration while preparing this system. Hence, cost accounting report provides

summary of information regarding expenditure.

2

relation to customer reactions through demand variations. It helps is aligning business goals and

expectations of consumers (Burritt, 2015). It automates the process of price setting and helps in

gaining optimization in context to price. Hence, quick decisions can be made by management

which pertains positive influence on company.

Job costing system: It involves procedure of information accumulation in relation to

costs that is associated with specific job or production process. This tracking method

determines cost of separate job which enables Capital Joinery to track information

regarding performance of each job.

Essential requirement: This system of job costing enhances profitability of Capital Joinery as it

separately assigns cost to each operations which provides required information to managers to

calculate profit margin of each job. This helps in setting adequate organizational structure in a

way that ensures expense minimization and performance maximization. It improves accuracy

and scalability in monitoring of business operations (Callahan, Stetz and Brooks, 2016).

Inventory management system: Utilization of this system is for the purpose of

managing and monitoring position of stock in in organization. It tracks amount of

inventory available in Capital Joinery which provides warning to managers to purchase of

required inventory and avoid over stocking as well as under stocking.

Essential requirement: Inventory management system is vital for analysing level of stock in

business. This helps management in keeping required information regarding stock and ensuring

that needed safety stock is available so that business operations are not hindered. This

information play a critical role in adopting efficient management style for productivity

improvement.

Cost accounting system: It is a platform which tracks cost information associated in

business. In other words, this framework helps managers of Capital Joinery in estimating

cost of its products with the motive of profitability analysis (Davies and Crawford,

2018). This system computes expenses associated with manufacturing or production

costs. Different types of costs, such as, labour, raw material, overhead etc. are taken

consideration while preparing this system. Hence, cost accounting report provides

summary of information regarding expenditure.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Essential requirement: Cost accounting system helps in disclosing costs incurred in business

which guides management in applying organizational structure which enhance future policies of

production. It ensures implementation of controlling activities for expenses assigned towards

material and supply activities. It enables managers to realise margin of profit that Capital

Joinery enjoys in context to business expenses. This is an effective technique which provides

guidelines for implementation of cost control activities for improvement of net profit.

P2 Describing various methods of management accounting reports:

Management accounting reports is a technique that enables management of business to

record its financial results. It enables providing financial information regarding day to day

business operations to administrators of Capital Joinery for the purpose of enhancing their short

term and long tern decision making process (Endenich and Trapp, 2020). This information is

essential for internal stakeholders of an organization for improvising sustainability of an

enterprise. Types of management accounting report are discussed below:

Budget report: This managerial accounting report is a critical tool for measuring

performance of company as it helps managers of Capital Joinery to understand costs

incurred in business as well as revenues generated by it. It evaluates expenses of past

years and hence enables management to adequately estimates expenses and income for

upcoming period of time.

Accounts receivable report: This report is focused on credit that is incorporated with

business. This report is prepared for recording receivables of Capital Joinery along with

time period that is taken by company to receive payments from its debtors. It helps

managers to eliminate high account receivable period so that a organization does not have

to face issues regarding cash flow. In addition to it, risk factor linked with occurrence of

bad debt is also reduced by preparation of accounts receivable report (Fry, Steele and

Saladin, 2019).

Performance report: Computation of this report is for the purpose of performance

evaluation of company. This report provides overview of performance of different

departments within Capital Joinery. It outlines performance of business and hence assists

management of an enterprise in development of an enterprise. Recording of entity

performance is essential for evaluating sectors which are profitable and identifying as

well as improving unprofitable sector.

3

which guides management in applying organizational structure which enhance future policies of

production. It ensures implementation of controlling activities for expenses assigned towards

material and supply activities. It enables managers to realise margin of profit that Capital

Joinery enjoys in context to business expenses. This is an effective technique which provides

guidelines for implementation of cost control activities for improvement of net profit.

P2 Describing various methods of management accounting reports:

Management accounting reports is a technique that enables management of business to

record its financial results. It enables providing financial information regarding day to day

business operations to administrators of Capital Joinery for the purpose of enhancing their short

term and long tern decision making process (Endenich and Trapp, 2020). This information is

essential for internal stakeholders of an organization for improvising sustainability of an

enterprise. Types of management accounting report are discussed below:

Budget report: This managerial accounting report is a critical tool for measuring

performance of company as it helps managers of Capital Joinery to understand costs

incurred in business as well as revenues generated by it. It evaluates expenses of past

years and hence enables management to adequately estimates expenses and income for

upcoming period of time.

Accounts receivable report: This report is focused on credit that is incorporated with

business. This report is prepared for recording receivables of Capital Joinery along with

time period that is taken by company to receive payments from its debtors. It helps

managers to eliminate high account receivable period so that a organization does not have

to face issues regarding cash flow. In addition to it, risk factor linked with occurrence of

bad debt is also reduced by preparation of accounts receivable report (Fry, Steele and

Saladin, 2019).

Performance report: Computation of this report is for the purpose of performance

evaluation of company. This report provides overview of performance of different

departments within Capital Joinery. It outlines performance of business and hence assists

management of an enterprise in development of an enterprise. Recording of entity

performance is essential for evaluating sectors which are profitable and identifying as

well as improving unprofitable sector.

3

Inventory management report: Management of inventory is vital for business for

analysis its expenditures in relation to stock management. Hence, inventory management

report is prepared by company to evaluate position of its stock so that management can

ensure availability of required inventory in order to maintain smooth operations of an

organization.

M1 Evaluating advantages of management accounting system and its application in context to

business:

Management accounting system is very helpful in managing the accounts of the financial

statements of the organization in a efficient manner by the analyse of the different system.

In the price optimization system it is used for decide the price of the manufacture product

to meet the customer demand by the Capital Joinery Ltd.

In the job costings system it is used to distribute the job cost among different department.

In the inventory management system it is used to manage the inventory, so there is no

shortage of the raw material is identified in the production department.

In the cost accounting system there is the determination of the cost is used by different

methods like cost control.

D1 Critically evaluating ways in which management accounting reports and systems are

integrated within process of organization:

In the Capital Joinery limited, there is the use of the reports and system for the better

management accounting if the financial statements. In the system there is inventory management

system and price optimization is used to determine the stock and price of the product which help

in increase the revenue of the firm (Håkansson, Kraus and Lind, 2015). In the reports there is use

of the budget report which is used for making budget for the revenue and expenditure. In

performance report thus report is made to determine the performance of the different department

in the company, in which there is the need of improvement.

4

analysis its expenditures in relation to stock management. Hence, inventory management

report is prepared by company to evaluate position of its stock so that management can

ensure availability of required inventory in order to maintain smooth operations of an

organization.

M1 Evaluating advantages of management accounting system and its application in context to

business:

Management accounting system is very helpful in managing the accounts of the financial

statements of the organization in a efficient manner by the analyse of the different system.

In the price optimization system it is used for decide the price of the manufacture product

to meet the customer demand by the Capital Joinery Ltd.

In the job costings system it is used to distribute the job cost among different department.

In the inventory management system it is used to manage the inventory, so there is no

shortage of the raw material is identified in the production department.

In the cost accounting system there is the determination of the cost is used by different

methods like cost control.

D1 Critically evaluating ways in which management accounting reports and systems are

integrated within process of organization:

In the Capital Joinery limited, there is the use of the reports and system for the better

management accounting if the financial statements. In the system there is inventory management

system and price optimization is used to determine the stock and price of the product which help

in increase the revenue of the firm (Håkansson, Kraus and Lind, 2015). In the reports there is use

of the budget report which is used for making budget for the revenue and expenditure. In

performance report thus report is made to determine the performance of the different department

in the company, in which there is the need of improvement.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

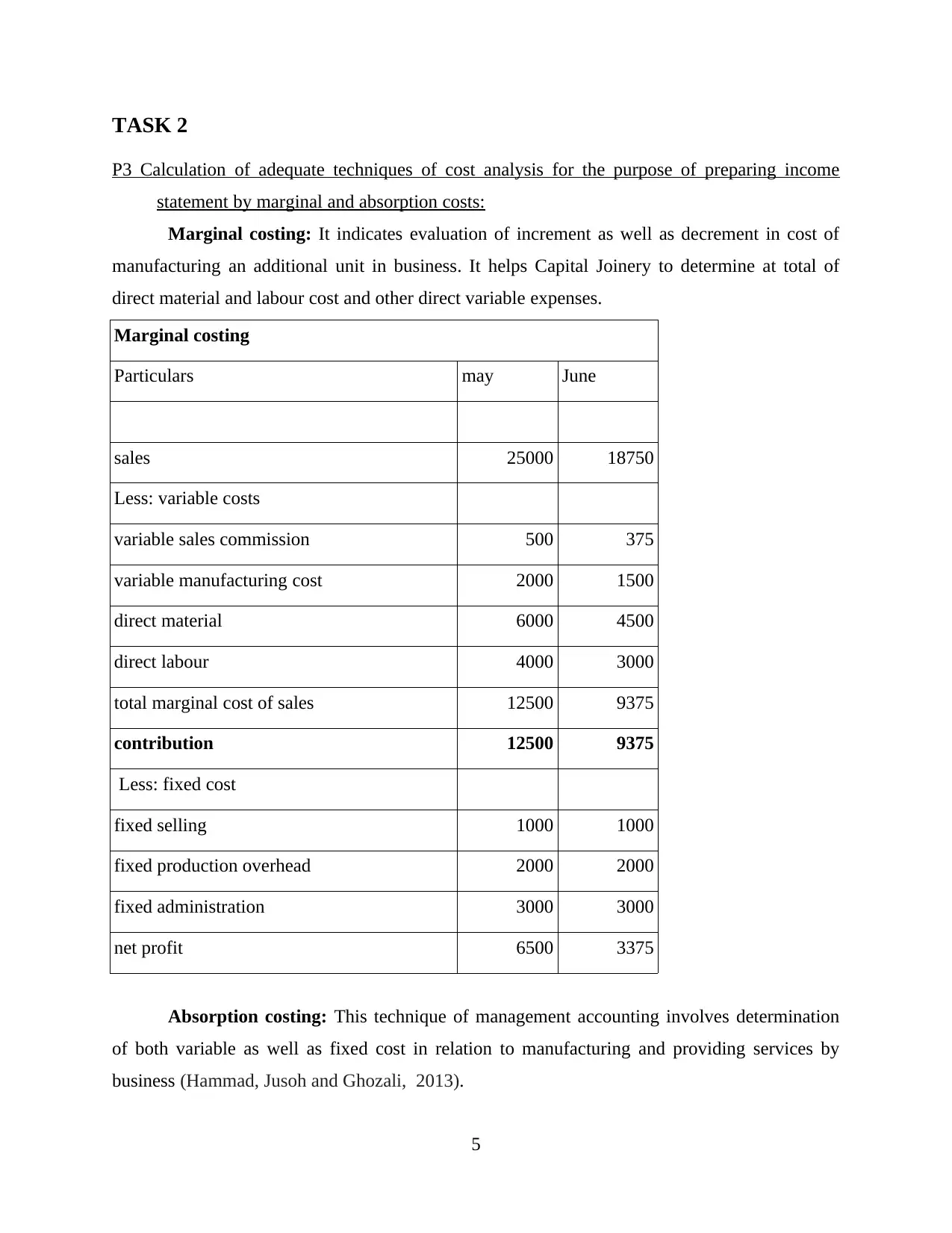

TASK 2

P3 Calculation of adequate techniques of cost analysis for the purpose of preparing income

statement by marginal and absorption costs:

Marginal costing: It indicates evaluation of increment as well as decrement in cost of

manufacturing an additional unit in business. It helps Capital Joinery to determine at total of

direct material and labour cost and other direct variable expenses.

Marginal costing

Particulars may June

sales 25000 18750

Less: variable costs

variable sales commission 500 375

variable manufacturing cost 2000 1500

direct material 6000 4500

direct labour 4000 3000

total marginal cost of sales 12500 9375

contribution 12500 9375

Less: fixed cost

fixed selling 1000 1000

fixed production overhead 2000 2000

fixed administration 3000 3000

net profit 6500 3375

Absorption costing: This technique of management accounting involves determination

of both variable as well as fixed cost in relation to manufacturing and providing services by

business (Hammad, Jusoh and Ghozali, 2013).

5

P3 Calculation of adequate techniques of cost analysis for the purpose of preparing income

statement by marginal and absorption costs:

Marginal costing: It indicates evaluation of increment as well as decrement in cost of

manufacturing an additional unit in business. It helps Capital Joinery to determine at total of

direct material and labour cost and other direct variable expenses.

Marginal costing

Particulars may June

sales 25000 18750

Less: variable costs

variable sales commission 500 375

variable manufacturing cost 2000 1500

direct material 6000 4500

direct labour 4000 3000

total marginal cost of sales 12500 9375

contribution 12500 9375

Less: fixed cost

fixed selling 1000 1000

fixed production overhead 2000 2000

fixed administration 3000 3000

net profit 6500 3375

Absorption costing: This technique of management accounting involves determination

of both variable as well as fixed cost in relation to manufacturing and providing services by

business (Hammad, Jusoh and Ghozali, 2013).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

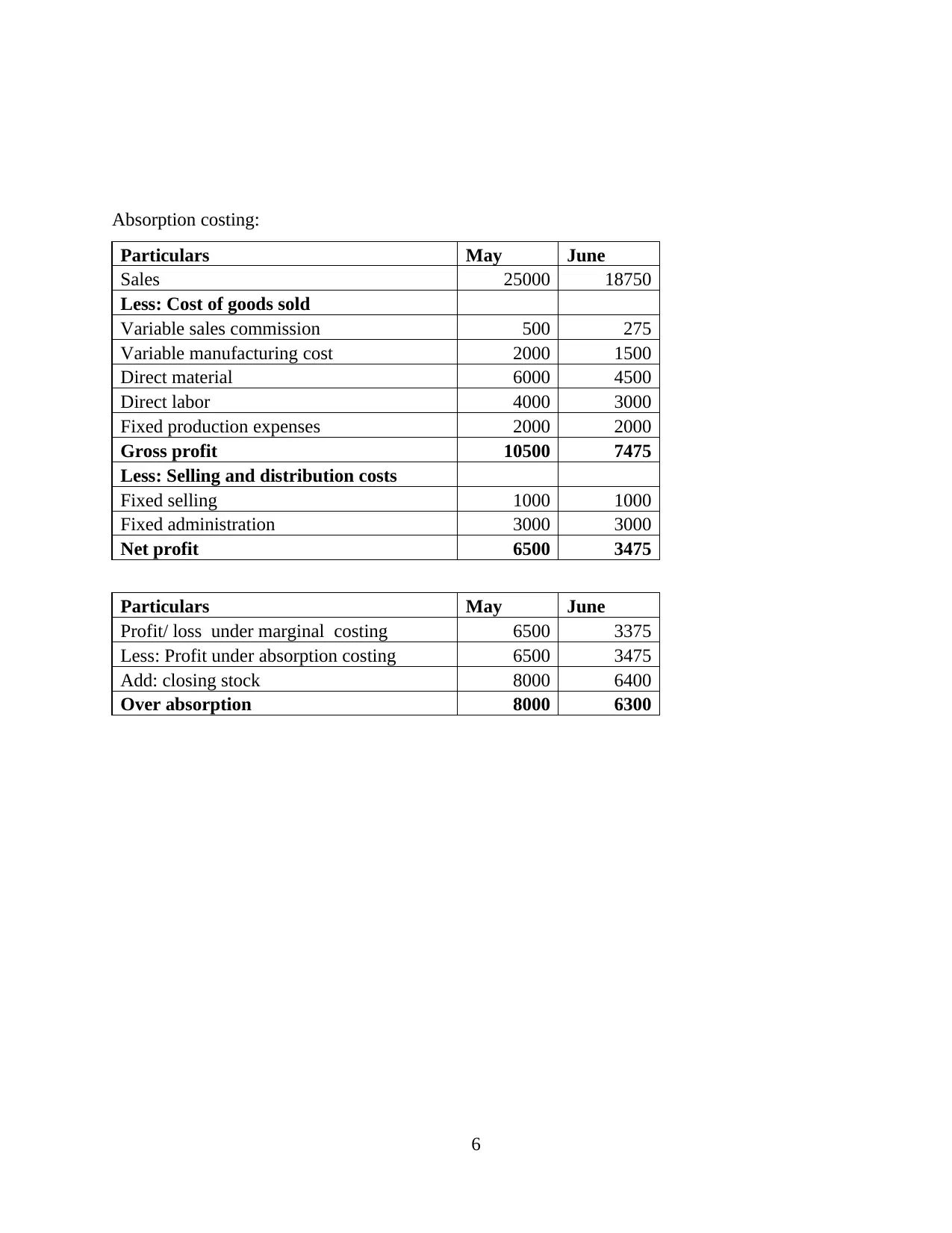

Absorption costing:

Particulars May June

Sales 25000 18750

Less: Cost of goods sold

Variable sales commission 500 275

Variable manufacturing cost 2000 1500

Direct material 6000 4500

Direct labor 4000 3000

Fixed production expenses 2000 2000

Gross profit 10500 7475

Less: Selling and distribution costs

Fixed selling 1000 1000

Fixed administration 3000 3000

Net profit 6500 3475

Particulars May June

Profit/ loss under marginal costing 6500 3375

Less: Profit under absorption costing 6500 3475

Add: closing stock 8000 6400

Over absorption 8000 6300

6

Particulars May June

Sales 25000 18750

Less: Cost of goods sold

Variable sales commission 500 275

Variable manufacturing cost 2000 1500

Direct material 6000 4500

Direct labor 4000 3000

Fixed production expenses 2000 2000

Gross profit 10500 7475

Less: Selling and distribution costs

Fixed selling 1000 1000

Fixed administration 3000 3000

Net profit 6500 3475

Particulars May June

Profit/ loss under marginal costing 6500 3375

Less: Profit under absorption costing 6500 3475

Add: closing stock 8000 6400

Over absorption 8000 6300

6

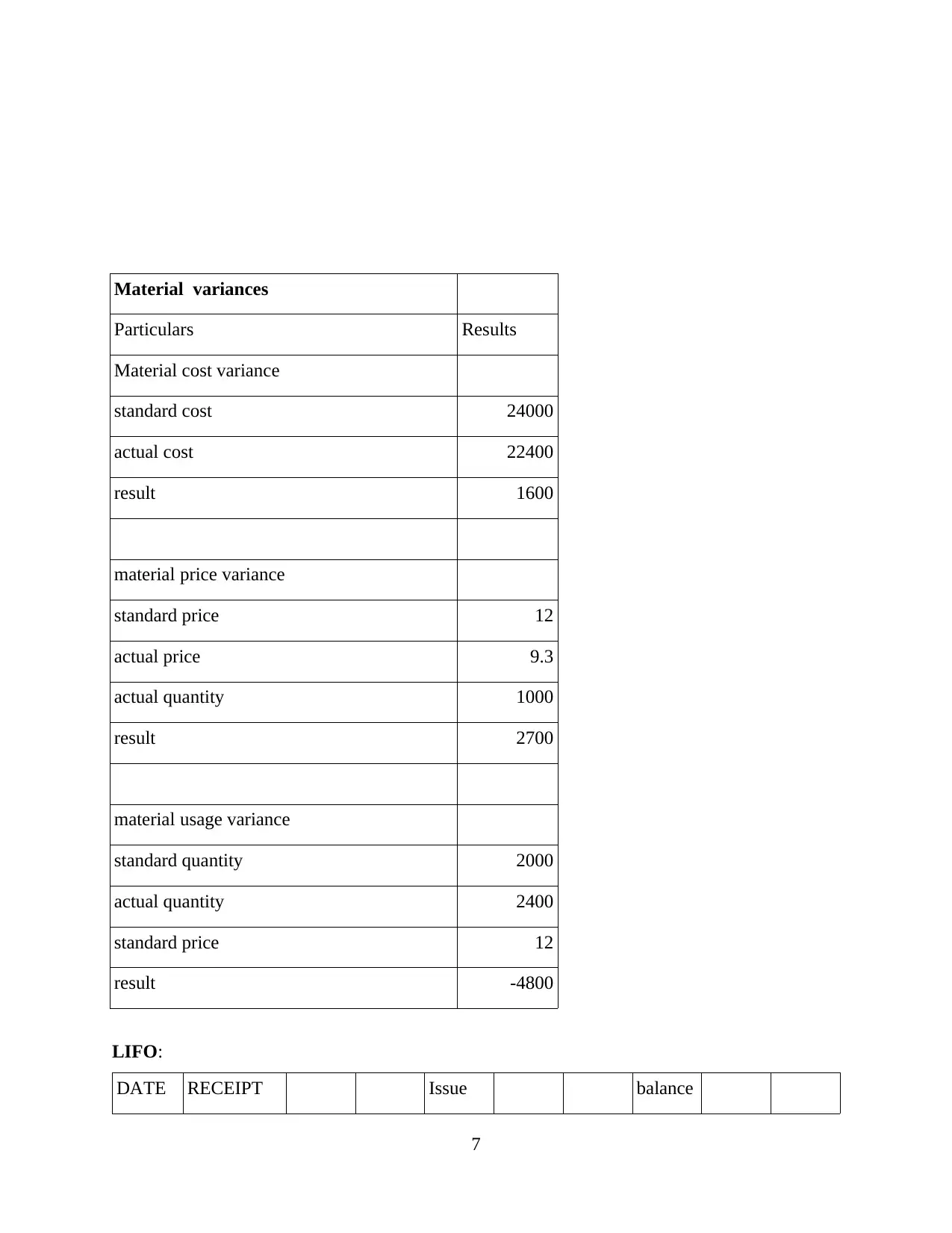

Material variances

Particulars Results

Material cost variance

standard cost 24000

actual cost 22400

result 1600

material price variance

standard price 12

actual price 9.3

actual quantity 1000

result 2700

material usage variance

standard quantity 2000

actual quantity 2400

standard price 12

result -4800

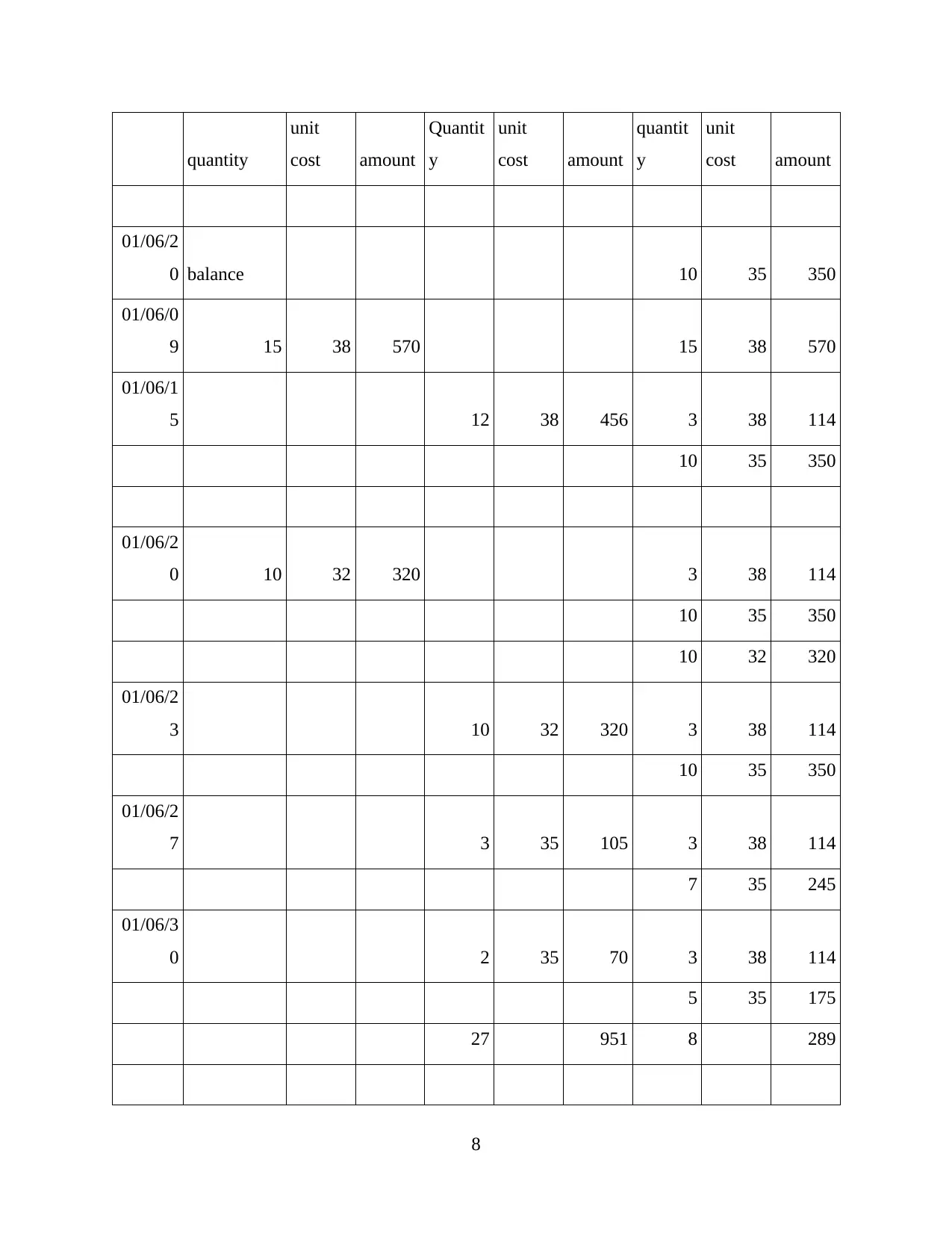

LIFO:

DATE RECEIPT Issue balance

7

Particulars Results

Material cost variance

standard cost 24000

actual cost 22400

result 1600

material price variance

standard price 12

actual price 9.3

actual quantity 1000

result 2700

material usage variance

standard quantity 2000

actual quantity 2400

standard price 12

result -4800

LIFO:

DATE RECEIPT Issue balance

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

quantity

unit

cost amount

Quantit

y

unit

cost amount

quantit

y

unit

cost amount

01/06/2

0 balance 10 35 350

01/06/0

9 15 38 570 15 38 570

01/06/1

5 12 38 456 3 38 114

10 35 350

01/06/2

0 10 32 320 3 38 114

10 35 350

10 32 320

01/06/2

3 10 32 320 3 38 114

10 35 350

01/06/2

7 3 35 105 3 38 114

7 35 245

01/06/3

0 2 35 70 3 38 114

5 35 175

27 951 8 289

8

unit

cost amount

Quantit

y

unit

cost amount

quantit

y

unit

cost amount

01/06/2

0 balance 10 35 350

01/06/0

9 15 38 570 15 38 570

01/06/1

5 12 38 456 3 38 114

10 35 350

01/06/2

0 10 32 320 3 38 114

10 35 350

10 32 320

01/06/2

3 10 32 320 3 38 114

10 35 350

01/06/2

7 3 35 105 3 38 114

7 35 245

01/06/3

0 2 35 70 3 38 114

5 35 175

27 951 8 289

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

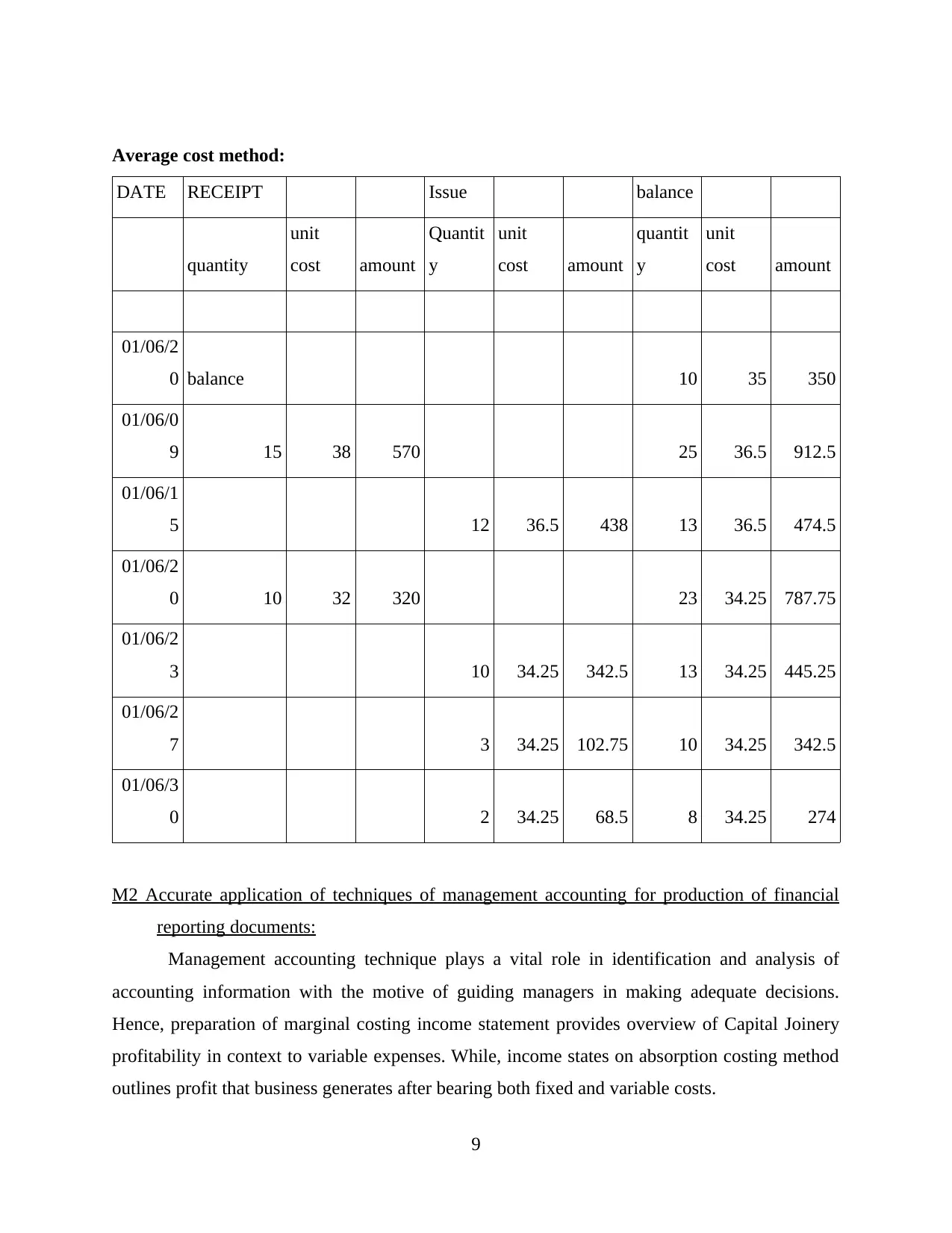

Average cost method:

DATE RECEIPT Issue balance

quantity

unit

cost amount

Quantit

y

unit

cost amount

quantit

y

unit

cost amount

01/06/2

0 balance 10 35 350

01/06/0

9 15 38 570 25 36.5 912.5

01/06/1

5 12 36.5 438 13 36.5 474.5

01/06/2

0 10 32 320 23 34.25 787.75

01/06/2

3 10 34.25 342.5 13 34.25 445.25

01/06/2

7 3 34.25 102.75 10 34.25 342.5

01/06/3

0 2 34.25 68.5 8 34.25 274

M2 Accurate application of techniques of management accounting for production of financial

reporting documents:

Management accounting technique plays a vital role in identification and analysis of

accounting information with the motive of guiding managers in making adequate decisions.

Hence, preparation of marginal costing income statement provides overview of Capital Joinery

profitability in context to variable expenses. While, income states on absorption costing method

outlines profit that business generates after bearing both fixed and variable costs.

9

DATE RECEIPT Issue balance

quantity

unit

cost amount

Quantit

y

unit

cost amount

quantit

y

unit

cost amount

01/06/2

0 balance 10 35 350

01/06/0

9 15 38 570 25 36.5 912.5

01/06/1

5 12 36.5 438 13 36.5 474.5

01/06/2

0 10 32 320 23 34.25 787.75

01/06/2

3 10 34.25 342.5 13 34.25 445.25

01/06/2

7 3 34.25 102.75 10 34.25 342.5

01/06/3

0 2 34.25 68.5 8 34.25 274

M2 Accurate application of techniques of management accounting for production of financial

reporting documents:

Management accounting technique plays a vital role in identification and analysis of

accounting information with the motive of guiding managers in making adequate decisions.

Hence, preparation of marginal costing income statement provides overview of Capital Joinery

profitability in context to variable expenses. While, income states on absorption costing method

outlines profit that business generates after bearing both fixed and variable costs.

9

D2 Production of financial reports that accurately applies and interprets business activities:

On the basis of above income statement of Capital Joinery it can be interpreted that

business should focus on improving its profitability as its net profit has reduced from May to

June. It net profit through marginal costing was 6500 in May while it reduced to 3375 in June.

Similarly, in absorption costing it produced reduced from 8500 to 5375.

TASK 3

P4 Evaluating advantages and disadvantages of different planning tools of budgetary control:

Budget: It is a type of financial plan which is used by the companies for the purpose of

assuring proper utilisation of resources. It is essential for all the management accountants to

make sure that they are able to formulate the budgets in systematic manner (Henri, 2018). In

Capital Joinery the managers are formulating budgets to carry out all the operational activities

systematically. While planning to take control over budgets the managers are paying attention

towards budgetary control. It facilitates the ignorance of overspending of funds. There are

various types of planning tools that are used by the managers in Capital Joinery for the purpose

of carrying out all the activities in systematic manner. Discussion of all the planning tools is as

follows:

Cash budget: In this budget detailed information regarding cash inflow and outflow is

recorded so that the managers can determine actual available funds for the operational activities.

In Capital Joinery it is formulated by the management for keeping detailed information of

receipts and payments that are made in cash. By using it managers try to analyse the liquidity of

business so that funds could be assigned to different activities. The advantages and disadvantages

of it are described below:

Advantages: By using it actual cash which is available to business could be analysed. In

this type of budget all the expenses and incomes are classified on the basis of cash if they

will not be in the form of cash then they will not be recorded in it.

Disadvantages: The information which is recorded in it is historic which may affect the

accuracy of results. There is lack of originality in this type of budget because most of the

companies are making transactions on credit basis rather than cash basis.

Zero based budget: It could be defined as a budget which is used by the business for

determining actual information regarding transactions for current year as it starts with zero base

10

On the basis of above income statement of Capital Joinery it can be interpreted that

business should focus on improving its profitability as its net profit has reduced from May to

June. It net profit through marginal costing was 6500 in May while it reduced to 3375 in June.

Similarly, in absorption costing it produced reduced from 8500 to 5375.

TASK 3

P4 Evaluating advantages and disadvantages of different planning tools of budgetary control:

Budget: It is a type of financial plan which is used by the companies for the purpose of

assuring proper utilisation of resources. It is essential for all the management accountants to

make sure that they are able to formulate the budgets in systematic manner (Henri, 2018). In

Capital Joinery the managers are formulating budgets to carry out all the operational activities

systematically. While planning to take control over budgets the managers are paying attention

towards budgetary control. It facilitates the ignorance of overspending of funds. There are

various types of planning tools that are used by the managers in Capital Joinery for the purpose

of carrying out all the activities in systematic manner. Discussion of all the planning tools is as

follows:

Cash budget: In this budget detailed information regarding cash inflow and outflow is

recorded so that the managers can determine actual available funds for the operational activities.

In Capital Joinery it is formulated by the management for keeping detailed information of

receipts and payments that are made in cash. By using it managers try to analyse the liquidity of

business so that funds could be assigned to different activities. The advantages and disadvantages

of it are described below:

Advantages: By using it actual cash which is available to business could be analysed. In

this type of budget all the expenses and incomes are classified on the basis of cash if they

will not be in the form of cash then they will not be recorded in it.

Disadvantages: The information which is recorded in it is historic which may affect the

accuracy of results. There is lack of originality in this type of budget because most of the

companies are making transactions on credit basis rather than cash basis.

Zero based budget: It could be defined as a budget which is used by the business for

determining actual information regarding transactions for current year as it starts with zero base

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.