Management Accounting Report: Planning, Tools, and Methods

VerifiedAdded on 2023/01/19

|20

|5817

|59

Report

AI Summary

This report delves into the core concepts of management accounting, emphasizing its critical role in organizational decision-making and planning, contrasting it with financial accounting. It explores various management accounting systems, including inventory management (LIFO, FIFO, AVCO), cost accounting (job costing, process costing), and price optimization. The report highlights the importance of these systems in operational efficiency, cost control, and pricing strategies. It further examines various managerial accounting reporting methods such as budget, execution, inventory, manufacturing, job costing, performance, and accounts receivable reports, illustrating their significance in informed decision-making. The report also discusses the use of planning tools and the adaptation of management accounting systems in different organizations. The report concludes by highlighting the benefits of these systems, such as the AVCO technique for cost allocation in inventory management, which is particularly beneficial for companies like Corus. Overall, the report provides a comprehensive overview of management accounting principles and their practical applications in a business setting.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

LO 1.................................................................................................................................................3

P1 Management Accounting and various management accounting systems..............................3

P2 Methods used for managerial accounting reporting...............................................................6

P3 Marginal and absorption costing............................................................................................8

M2..............................................................................................................................................10

LO 3...............................................................................................................................................10

Use of planning tool in context of management accounting.....................................................10

M 3) Use of different planning tools.........................................................................................13

LO 4...............................................................................................................................................13

The ways in which companies use management accounting methods......................................13

M 4) How responding to financial problems lead success of business.....................................15

CONCLUSION..............................................................................................................................16

REFERENCES................................................................................................................................1

APPENDIX......................................................................................................................................3

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

LO 1.................................................................................................................................................3

P1 Management Accounting and various management accounting systems..............................3

P2 Methods used for managerial accounting reporting...............................................................6

P3 Marginal and absorption costing............................................................................................8

M2..............................................................................................................................................10

LO 3...............................................................................................................................................10

Use of planning tool in context of management accounting.....................................................10

M 3) Use of different planning tools.........................................................................................13

LO 4...............................................................................................................................................13

The ways in which companies use management accounting methods......................................13

M 4) How responding to financial problems lead success of business.....................................15

CONCLUSION..............................................................................................................................16

REFERENCES................................................................................................................................1

APPENDIX......................................................................................................................................3

INTRODUCTION

Management Accounting is an extremely important concept in any organisation that is

operating and assists in the overall decision-making as well as the planning in the organisation.

Management Accounting helps in simplifying the process through which the company conducts

tis daily operations and take decisions related to the financing of the company. In the present

report, the concept of management accounting along with financial accounting and various

management accounting systems have been discussed in this report. This report will also analyse

the concept of marginal and absorption costing method and the various advantages as well as

disadvantages of the budgetary control tools will be identified and discussed in this report.

Lastly, this report will also identify the manner in which different organisations are adapting to

the management accounting systems and a comparison will be made.

MAIN BODY

LO 1

P1 Management Accounting and various management accounting systems

Management Accounting can be defined as that process or technique which assists the

managers and accountants of a company in determining what is the operational cost that is

incurred in carrying out the entire business activities (Honggowati and et.al., 2017). IMA defines

management accounting as a profession through which the management of the company gets

assistance in the decision making process as well as in planning the resource requirement for the

company. The major purposes behind incorporating management accounting in Corus, a

company under Tata Steel Europe involve: Planning: Management Accounting helps in analysing the current information that is

available and predicts the future trends that assist in planning for the future. They plan for

the future needs and formulate budgets and strategies that would assist in increasing the

profitability of the company. Decision-Making: The decision making of the managers regarding various management

accounting tools is based on the data that has been collected in the management

accounting analysis. This assists the managers in taking appropriate decisions that

simplify the decision making process.

Management Accounting is an extremely important concept in any organisation that is

operating and assists in the overall decision-making as well as the planning in the organisation.

Management Accounting helps in simplifying the process through which the company conducts

tis daily operations and take decisions related to the financing of the company. In the present

report, the concept of management accounting along with financial accounting and various

management accounting systems have been discussed in this report. This report will also analyse

the concept of marginal and absorption costing method and the various advantages as well as

disadvantages of the budgetary control tools will be identified and discussed in this report.

Lastly, this report will also identify the manner in which different organisations are adapting to

the management accounting systems and a comparison will be made.

MAIN BODY

LO 1

P1 Management Accounting and various management accounting systems

Management Accounting can be defined as that process or technique which assists the

managers and accountants of a company in determining what is the operational cost that is

incurred in carrying out the entire business activities (Honggowati and et.al., 2017). IMA defines

management accounting as a profession through which the management of the company gets

assistance in the decision making process as well as in planning the resource requirement for the

company. The major purposes behind incorporating management accounting in Corus, a

company under Tata Steel Europe involve: Planning: Management Accounting helps in analysing the current information that is

available and predicts the future trends that assist in planning for the future. They plan for

the future needs and formulate budgets and strategies that would assist in increasing the

profitability of the company. Decision-Making: The decision making of the managers regarding various management

accounting tools is based on the data that has been collected in the management

accounting analysis. This assists the managers in taking appropriate decisions that

simplify the decision making process.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Controlling: The plans that have been implemented in the company after proper

evaluation and data analysis are regularly monitored where the mangers evaluate what is

going right and what is going wrong, whether the budgets formulated are being achieved

and what are the reasons behind deviations if there are any (Mills, 2018).

However, Financial Accounting and Management Accounting are two different areas of

accounting that are similar but are differentiated by a fine line. Financial Accounting is related

to preparing financial reports that are usually prepared for presenting to external parties or

stakeholders that are interested in the business activities and the profits or losses earned by the

business. There are certain points based on which a distinction can be made between

management accounting norms and financial accounting norms:

MANAGEMENT ACCOUNTING FINANCIAL ACCOUNTING

This is done usually for the internal

management and for facilitating the operation

of organisation.

This is done for external parties so that they

can be interested in the organisational function

and invest in it.

It is not a statutory requirement to prepare

management accounting budgets (Mack and

Goretzki, 2017).

It is a statutory requirement to prepare financial

accounting statements.

Management accounting usually relates to a

particular products for particular segment of

the entire organisations.

Financial accounts are prepared for the entire

organisation and incorporate al the activities.

These are prepared as per the convenience of

the internal management of the company.

These are prepared between a fixed time

periods which is usually one year as

determined by the statutory requirements.

Management accounting is usually related to

increasing the efficiency of the operational

activities carried out in the company.

Financial Accounting is related to the

increasing the profitability and presentability of

the entire business so that investments can be

invited.

There are various methods and tools incorporated under management accounting systems

and these can be categorised in a following manner:

Inventory Management System: The inventory management system can be defined as

the one which keeps a check on the input and output of the inventory in the organisation and

evaluation and data analysis are regularly monitored where the mangers evaluate what is

going right and what is going wrong, whether the budgets formulated are being achieved

and what are the reasons behind deviations if there are any (Mills, 2018).

However, Financial Accounting and Management Accounting are two different areas of

accounting that are similar but are differentiated by a fine line. Financial Accounting is related

to preparing financial reports that are usually prepared for presenting to external parties or

stakeholders that are interested in the business activities and the profits or losses earned by the

business. There are certain points based on which a distinction can be made between

management accounting norms and financial accounting norms:

MANAGEMENT ACCOUNTING FINANCIAL ACCOUNTING

This is done usually for the internal

management and for facilitating the operation

of organisation.

This is done for external parties so that they

can be interested in the organisational function

and invest in it.

It is not a statutory requirement to prepare

management accounting budgets (Mack and

Goretzki, 2017).

It is a statutory requirement to prepare financial

accounting statements.

Management accounting usually relates to a

particular products for particular segment of

the entire organisations.

Financial accounts are prepared for the entire

organisation and incorporate al the activities.

These are prepared as per the convenience of

the internal management of the company.

These are prepared between a fixed time

periods which is usually one year as

determined by the statutory requirements.

Management accounting is usually related to

increasing the efficiency of the operational

activities carried out in the company.

Financial Accounting is related to the

increasing the profitability and presentability of

the entire business so that investments can be

invited.

There are various methods and tools incorporated under management accounting systems

and these can be categorised in a following manner:

Inventory Management System: The inventory management system can be defined as

the one which keeps a check on the input and output of the inventory in the organisation and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ascertains the cost incurred in maintaining the required inventory levels in the organisation

without incurring additional costs. It further assists in keeping the track of the duration for which

inventory is kept in the warehouse, its incoming and outgoing. There are various techniques that

are implemented under inventory management system. These can be categorised in following

manner:

LIFO: Under this, the inventory is recorded and used on the basis of “Last in First Out”

i.e. the stock which entered in the warehouse on the latest date is used first in the

organisation and the older stock is used after the consumption of the latest stock (Khan

and Jain, 2018). It is usually beneficial in case of perishable goods where the latest goods

are used earlier so that the desired quality of goods can be maintained.

FIFO: This is another technique and under this, the inventory is recorded and used on the

basis of “First in First Out” i.e. as per this technique, the first stock of inventory that

entered the company is used initially and the stock entering latest in the warehouse is

consumed after the initial stocks of inventory are consumed. This technique is used for

those products where the durability of the goods is much longer and can be preserved for

a longer time period. AVCO: Inventory costing method is the average costing method that is used in the

companies when the goods are consumed regularly and their costs need to be

apportioned. AVCO depicts the average inventory cost that is calculated by division of

the cost of stock in the warehouse at a given point of time with the total number of goods

in inventory at that particular time. It is beneficial for those industries where the goods

are required on a continuous basis and that too in huge quantities.

Cost Accounting Systems: These cost accounting systems are used to estimate or pre

formulate the cost of products which is used for profitability analysis and inventory valuation

and cost control. Estimation of accurate costs is extremely necessary in conducting profitable

operations in the company and for this purpose, there are certain techniques that can be

implemented. These are Job Costing and Process Costing. Job Costing helps in deterring

separate costs for manufacturing process related to individual jobs and are appropriate for

companies like vent management etc. who are required to meet short term objectives. There are

several benefits which in turn associated with both cost accounting aspects such as elimination of

inefficiencies, cost reduction etc. Moreover, cost accounting system emphasizes on fixing

without incurring additional costs. It further assists in keeping the track of the duration for which

inventory is kept in the warehouse, its incoming and outgoing. There are various techniques that

are implemented under inventory management system. These can be categorised in following

manner:

LIFO: Under this, the inventory is recorded and used on the basis of “Last in First Out”

i.e. the stock which entered in the warehouse on the latest date is used first in the

organisation and the older stock is used after the consumption of the latest stock (Khan

and Jain, 2018). It is usually beneficial in case of perishable goods where the latest goods

are used earlier so that the desired quality of goods can be maintained.

FIFO: This is another technique and under this, the inventory is recorded and used on the

basis of “First in First Out” i.e. as per this technique, the first stock of inventory that

entered the company is used initially and the stock entering latest in the warehouse is

consumed after the initial stocks of inventory are consumed. This technique is used for

those products where the durability of the goods is much longer and can be preserved for

a longer time period. AVCO: Inventory costing method is the average costing method that is used in the

companies when the goods are consumed regularly and their costs need to be

apportioned. AVCO depicts the average inventory cost that is calculated by division of

the cost of stock in the warehouse at a given point of time with the total number of goods

in inventory at that particular time. It is beneficial for those industries where the goods

are required on a continuous basis and that too in huge quantities.

Cost Accounting Systems: These cost accounting systems are used to estimate or pre

formulate the cost of products which is used for profitability analysis and inventory valuation

and cost control. Estimation of accurate costs is extremely necessary in conducting profitable

operations in the company and for this purpose, there are certain techniques that can be

implemented. These are Job Costing and Process Costing. Job Costing helps in deterring

separate costs for manufacturing process related to individual jobs and are appropriate for

companies like vent management etc. who are required to meet short term objectives. There are

several benefits which in turn associated with both cost accounting aspects such as elimination of

inefficiencies, cost reduction etc. Moreover, cost accounting system emphasizes on fixing

standards for each & every activity. This in turn avoids wastage, losses as well as inefficiencies

from operations and thereby facilitates cost reduction & profit maximization. In addition to this,

job costing system also offers measures which assists in business decision making. By

considering this, firm can assess cost related to each job and thereby take pricing decisions

effectually. Further, profit earned from each job can easily be ascertained by the firm through

employing such system.

Price optimization system: By undertaking this system company can identify the price

which customers are ready to pay for the concerned products or services. Hence, referring

customer’s preferences and sensitivity regarding price company can take appropriate pricing

decisions. Along with this, there are several strategies which can be undertaken by the business

for setting prices such as: Competitive: On the basis of this, company sets prices of product by taking into account

and analysing pricing framework of competitors.

Cost-plus pricing strategy: According to this, by adding profit %, which company wants

to attain by selling product, in unit cost company can determine selling price.

Price: unit cost + (cost * mark-up%)

Penetration pricing strategy: For gaining high market share, initially company sets lower

prices of the products or services offered. Hence, after getting desired outcome and

building customer loyalty company increases prices of products.

P2 Methods used for managerial accounting reporting. Budget report: It is the one of the most important report that is used by the managers to

make cost related decisions. On periodic basis budget reports are prepared and variance

analysis is given in them. One of major benefit of budget report is that on basis of

variance analysis results manager prepare strategy to control cost at the workplace.

Variance if identified then in that case previous time period budget performance is also

evaluated and it is identified whether variance was earlier present. Consistency in

variance reflect management failure and require immediate attention from their side in

order to control condition on initial stage (Trucco, 2015).

from operations and thereby facilitates cost reduction & profit maximization. In addition to this,

job costing system also offers measures which assists in business decision making. By

considering this, firm can assess cost related to each job and thereby take pricing decisions

effectually. Further, profit earned from each job can easily be ascertained by the firm through

employing such system.

Price optimization system: By undertaking this system company can identify the price

which customers are ready to pay for the concerned products or services. Hence, referring

customer’s preferences and sensitivity regarding price company can take appropriate pricing

decisions. Along with this, there are several strategies which can be undertaken by the business

for setting prices such as: Competitive: On the basis of this, company sets prices of product by taking into account

and analysing pricing framework of competitors.

Cost-plus pricing strategy: According to this, by adding profit %, which company wants

to attain by selling product, in unit cost company can determine selling price.

Price: unit cost + (cost * mark-up%)

Penetration pricing strategy: For gaining high market share, initially company sets lower

prices of the products or services offered. Hence, after getting desired outcome and

building customer loyalty company increases prices of products.

P2 Methods used for managerial accounting reporting. Budget report: It is the one of the most important report that is used by the managers to

make cost related decisions. On periodic basis budget reports are prepared and variance

analysis is given in them. One of major benefit of budget report is that on basis of

variance analysis results manager prepare strategy to control cost at the workplace.

Variance if identified then in that case previous time period budget performance is also

evaluated and it is identified whether variance was earlier present. Consistency in

variance reflect management failure and require immediate attention from their side in

order to control condition on initial stage (Trucco, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Execution report: Many time targets is determined in respect to performance of any

business activity. Execution report tell manager percentage of task completed till the date

and time that will be required to perform remaining task and it is its major benefit. On

basis of report manager identify whether there is need to speed up work or current speed

must be continuing to ensure timely completion of business activity. It can be said that

there is huge significance of the execution report for the managers. Inventory report: In this report detail data about inventory is available (Leitner and Wall,

2015). On daily basis analyst prepare Excel sheet about items sold or dispatched from

warehouse and quantity needed at same place to meet upcoming demand. On weekly

basis analyst submit inventory report to the manager to make decisions. Thus, scope of

inventory report is wide and it to large extent assist management in making prudent

inventory purchase decisions. Manufacturing report: It is another report which provide information to the manager

about number of units produced at the workplace. Report also provide information about

units that need to be produced to meet demand of the general public. Forecast also given

in the report so that accordingly plan can be prepared in respect to purchase of raw

material. It is major benefit of manufacturing report. Thus, management accounting

report have significance for the business firm. Job costing report: This report exhibits expenditures associated with specific business

project. Hence, through using this report manufacturing department can make estimation

about both expenses and profitability aspect. By this, manager of the firm would become

able to assess high-performing areas and thereby become able to make optimum

utilization of resources. Performance report: Performance report cover an information about overall performance

of the business firm. Performance can be measured on multiple areas like cost and time

taken to complete task etc (Kalkhouran and et.al., 2015). It depends on the manager

whether they use both options to evaluate firm performance or use specific one. Thus, it

can be said that performance report has due importance for the firm and due to this

reason, it is time to time used by the managers for making decisions.

Account receivable report: Bill receivable management is very important at the

workplace because it cover large portion of the current asset of the company (Novas and

business activity. Execution report tell manager percentage of task completed till the date

and time that will be required to perform remaining task and it is its major benefit. On

basis of report manager identify whether there is need to speed up work or current speed

must be continuing to ensure timely completion of business activity. It can be said that

there is huge significance of the execution report for the managers. Inventory report: In this report detail data about inventory is available (Leitner and Wall,

2015). On daily basis analyst prepare Excel sheet about items sold or dispatched from

warehouse and quantity needed at same place to meet upcoming demand. On weekly

basis analyst submit inventory report to the manager to make decisions. Thus, scope of

inventory report is wide and it to large extent assist management in making prudent

inventory purchase decisions. Manufacturing report: It is another report which provide information to the manager

about number of units produced at the workplace. Report also provide information about

units that need to be produced to meet demand of the general public. Forecast also given

in the report so that accordingly plan can be prepared in respect to purchase of raw

material. It is major benefit of manufacturing report. Thus, management accounting

report have significance for the business firm. Job costing report: This report exhibits expenditures associated with specific business

project. Hence, through using this report manufacturing department can make estimation

about both expenses and profitability aspect. By this, manager of the firm would become

able to assess high-performing areas and thereby become able to make optimum

utilization of resources. Performance report: Performance report cover an information about overall performance

of the business firm. Performance can be measured on multiple areas like cost and time

taken to complete task etc (Kalkhouran and et.al., 2015). It depends on the manager

whether they use both options to evaluate firm performance or use specific one. Thus, it

can be said that performance report has due importance for the firm and due to this

reason, it is time to time used by the managers for making decisions.

Account receivable report: Bill receivable management is very important at the

workplace because it cover large portion of the current asset of the company (Novas and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

et.al., 2017). In case receivable portion is high then in that case there is a chance that

some of amount get blocked in asset. Hence, manager on weekly basis evaluate status of

bill receivable and accordingly decide whether to further sell goods on credit basis.

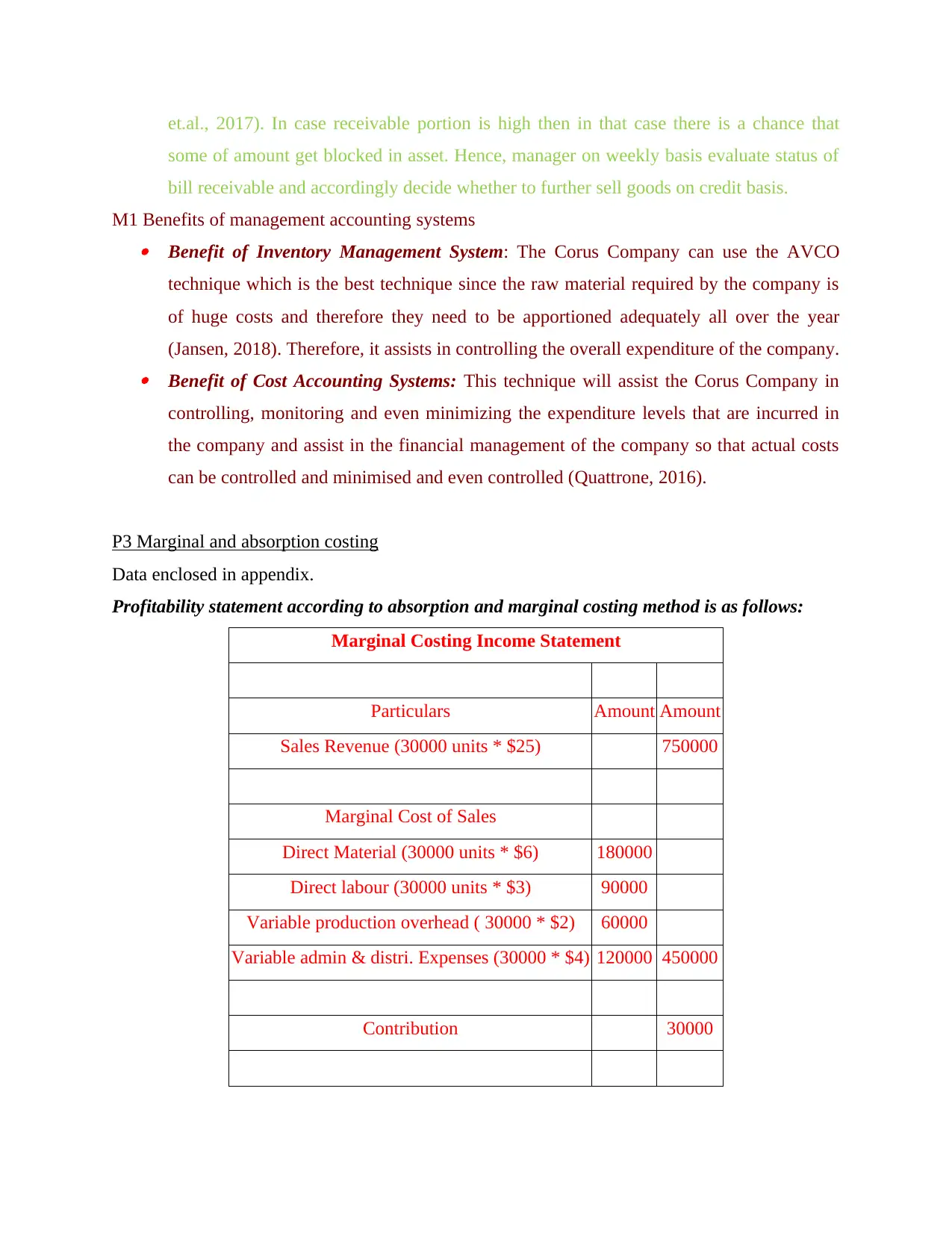

M1 Benefits of management accounting systems Benefit of Inventory Management System: The Corus Company can use the AVCO

technique which is the best technique since the raw material required by the company is

of huge costs and therefore they need to be apportioned adequately all over the year

(Jansen, 2018). Therefore, it assists in controlling the overall expenditure of the company. Benefit of Cost Accounting Systems: This technique will assist the Corus Company in

controlling, monitoring and even minimizing the expenditure levels that are incurred in

the company and assist in the financial management of the company so that actual costs

can be controlled and minimised and even controlled (Quattrone, 2016).

P3 Marginal and absorption costing

Data enclosed in appendix.

Profitability statement according to absorption and marginal costing method is as follows:

Marginal Costing Income Statement

Particulars Amount Amount

Sales Revenue (30000 units * $25) 750000

Marginal Cost of Sales

Direct Material (30000 units * $6) 180000

Direct labour (30000 units * $3) 90000

Variable production overhead ( 30000 * $2) 60000

Variable admin & distri. Expenses (30000 * $4) 120000 450000

Contribution 30000

some of amount get blocked in asset. Hence, manager on weekly basis evaluate status of

bill receivable and accordingly decide whether to further sell goods on credit basis.

M1 Benefits of management accounting systems Benefit of Inventory Management System: The Corus Company can use the AVCO

technique which is the best technique since the raw material required by the company is

of huge costs and therefore they need to be apportioned adequately all over the year

(Jansen, 2018). Therefore, it assists in controlling the overall expenditure of the company. Benefit of Cost Accounting Systems: This technique will assist the Corus Company in

controlling, monitoring and even minimizing the expenditure levels that are incurred in

the company and assist in the financial management of the company so that actual costs

can be controlled and minimised and even controlled (Quattrone, 2016).

P3 Marginal and absorption costing

Data enclosed in appendix.

Profitability statement according to absorption and marginal costing method is as follows:

Marginal Costing Income Statement

Particulars Amount Amount

Sales Revenue (30000 units * $25) 750000

Marginal Cost of Sales

Direct Material (30000 units * $6) 180000

Direct labour (30000 units * $3) 90000

Variable production overhead ( 30000 * $2) 60000

Variable admin & distri. Expenses (30000 * $4) 120000 450000

Contribution 30000

Fixed Costs

Fixed manufacturing overheads 160000

Fixed Selling & admin costs 50000

Net Profit 90000

Absorption Costing

Absorption Costing Income Statement

Particulars Amoun

t (in £)

Amoun

t (in £)

Sales Revenue (30000 units * $25) 750000

Marginal Cost of Sales

Direct Material (30000 units * $6) 180000

Direct labour (30000 units * $3) 90000

Variable production overhead ( 30000 * $2) 60000

Fixed manufacturing overheads 160000 490000

Gross profit 260000

Distribution & admin costs

Variable (30000 * $4) 120000

Fixed 50000 170000

Fixed manufacturing overheads 160000

Fixed Selling & admin costs 50000

Net Profit 90000

Absorption Costing

Absorption Costing Income Statement

Particulars Amoun

t (in £)

Amoun

t (in £)

Sales Revenue (30000 units * $25) 750000

Marginal Cost of Sales

Direct Material (30000 units * $6) 180000

Direct labour (30000 units * $3) 90000

Variable production overhead ( 30000 * $2) 60000

Fixed manufacturing overheads 160000 490000

Gross profit 260000

Distribution & admin costs

Variable (30000 * $4) 120000

Fixed 50000 170000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Net Profit 90000

Table 1Marginal and absorption income statement

Marginal and absorption costing both are different from each other. In case of marginal

costing method both fixed and variable expenses are taken in to account. On other hand, in case

of absorption costing method only variable expenses are taken in to account. Thus, it can be said

that both approaches are different and have equal importance for the firm. Sometime manager

may want to measure impact of variable expenses alone on the business profit. Then in that case

it can use absorption costing method (Wildavsky, 2017). On other hand, if manager want to find

out cumulative impact of both fixed and variable expenses on profit then in that case it can use

marginal costing method in the business. Thus, it can be said that there is huge importance of

marginal and absorption costing method. It depends on the manager that which method they find

more suitable for decision making purpose. Managers according to their requirements can use

any of these methods in order to make business decisions.

M2

It can be observed from above table that marginal costing profit is 90000 and same of

absorption costing method is 90000. Hence, it can be said that on both costing approaches profit

is earned. In case of marginal costing method overall cost of production is 450000 for variable

expenses and same for absorption cost method is 490000. Hence, cost will be always higher in

absorption cost then marginal cost.

LO 3

Use of planning tool in context of management accounting

Budgets refer to financial planning which is carried by the accountant in respect of

determining the overall integrity of the company. Through the accurate planning, it determines

the company stability to enter into particular project or also helps company to manage their

internal and external matter in right manner (Miller, Hildreth, and Rabin, 2018). In context of

CORUS company, the budgets are prepared by the financial manager which carries the liability

to examines the company stability in pertaining to particular task. It also carries various planning

tool through the accounting can be managed in accurate way. It includes the following such as :

Table 1Marginal and absorption income statement

Marginal and absorption costing both are different from each other. In case of marginal

costing method both fixed and variable expenses are taken in to account. On other hand, in case

of absorption costing method only variable expenses are taken in to account. Thus, it can be said

that both approaches are different and have equal importance for the firm. Sometime manager

may want to measure impact of variable expenses alone on the business profit. Then in that case

it can use absorption costing method (Wildavsky, 2017). On other hand, if manager want to find

out cumulative impact of both fixed and variable expenses on profit then in that case it can use

marginal costing method in the business. Thus, it can be said that there is huge importance of

marginal and absorption costing method. It depends on the manager that which method they find

more suitable for decision making purpose. Managers according to their requirements can use

any of these methods in order to make business decisions.

M2

It can be observed from above table that marginal costing profit is 90000 and same of

absorption costing method is 90000. Hence, it can be said that on both costing approaches profit

is earned. In case of marginal costing method overall cost of production is 450000 for variable

expenses and same for absorption cost method is 490000. Hence, cost will be always higher in

absorption cost then marginal cost.

LO 3

Use of planning tool in context of management accounting

Budgets refer to financial planning which is carried by the accountant in respect of

determining the overall integrity of the company. Through the accurate planning, it determines

the company stability to enter into particular project or also helps company to manage their

internal and external matter in right manner (Miller, Hildreth, and Rabin, 2018). In context of

CORUS company, the budgets are prepared by the financial manager which carries the liability

to examines the company stability in pertaining to particular task. It also carries various planning

tool through the accounting can be managed in accurate way. It includes the following such as :

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sales Budgets: It is one of the types of important budgets which is prepared to guide the

company regarding investing in particular activity (What is Sales Budget? Importance of

Sales Budgeting, 2019). As before selling any products, the budgets is prepares regarding

attaining the particular task such as by determiner the market needs, by producing the

goods and services, by marketing the particular products, by examining the actual cost

and also the ratio of buying the products in market (Kaye III, Frances J. Kaye and III,

2016). The main advantages of preferring this planning tool is that

1. It helps companies to organise their overall objectivity in right manner and also they

can make proper planning through preferring their budget.

2. Through the sales budgets, it guides every department regarding working under

certain criteria and thus through this perspective, it manages every department of the

company.

The disadvantage o0f choosing this budget is that

1. This is less chances of accuracy in this budgets as the transaction are changing on regular

perspective.2. It is more time consuming budgets as it requires lot of modification in reaching to certain

stages.

Purchase budgets: This budgets are prepared to helps companies to examines the

expenses which is incurred at the time of purchasing the inventory or dealing in any raw

material to prepare a particular product (Gallani and et.al., 2019). CORUS is the steel

company and thus requires various inventories to manage the productivity in the

company. The main advantages of choosing this planning tool is that

1. It helps owners to examined the budget by referring the previous budgets and then

prepare the actual budgets.

2. As large number of employees are carrying the business thus various inventories are

needed to accomplish the task, in such manner purchase budgets helps in setting the

particular budgets for each activity (What Is a Purchases Budget?, 2019).

Disadvantage of purchase budgets is that in case of changes in taste of consumer,

purchase budgets not reflect the 100% accuracy in pertaining to particular task. It is carried to be

most expensive procedure as in respect of changing in any decision resulting in wastages of the

raw material and also it is sometimes not reusable.

company regarding investing in particular activity (What is Sales Budget? Importance of

Sales Budgeting, 2019). As before selling any products, the budgets is prepares regarding

attaining the particular task such as by determiner the market needs, by producing the

goods and services, by marketing the particular products, by examining the actual cost

and also the ratio of buying the products in market (Kaye III, Frances J. Kaye and III,

2016). The main advantages of preferring this planning tool is that

1. It helps companies to organise their overall objectivity in right manner and also they

can make proper planning through preferring their budget.

2. Through the sales budgets, it guides every department regarding working under

certain criteria and thus through this perspective, it manages every department of the

company.

The disadvantage o0f choosing this budget is that

1. This is less chances of accuracy in this budgets as the transaction are changing on regular

perspective.2. It is more time consuming budgets as it requires lot of modification in reaching to certain

stages.

Purchase budgets: This budgets are prepared to helps companies to examines the

expenses which is incurred at the time of purchasing the inventory or dealing in any raw

material to prepare a particular product (Gallani and et.al., 2019). CORUS is the steel

company and thus requires various inventories to manage the productivity in the

company. The main advantages of choosing this planning tool is that

1. It helps owners to examined the budget by referring the previous budgets and then

prepare the actual budgets.

2. As large number of employees are carrying the business thus various inventories are

needed to accomplish the task, in such manner purchase budgets helps in setting the

particular budgets for each activity (What Is a Purchases Budget?, 2019).

Disadvantage of purchase budgets is that in case of changes in taste of consumer,

purchase budgets not reflect the 100% accuracy in pertaining to particular task. It is carried to be

most expensive procedure as in respect of changing in any decision resulting in wastages of the

raw material and also it is sometimes not reusable.

Zero budgets: This budgets mainly prepared from the starting. As company cannot refer

any of the transaction from the previous statement. They had to prepare all the activities

from, starting. In respect of CORUS, the planning tool is effective as the managers can

personally interact with every department regarding examining their issue and then

applied them in company to get better results (Miller, 2018.). The advantages of

preferring the Zero budgets is that by applying this budget, it result in enhancing the

communication at work place by communicating with each department to examined their

reviews and thoughts. It also resulting in getting more accurate results regarding the

company information as the budgets is prepared from the zero base. It also saves the

resources of the company by dealing in only that products which resulting in costing

benefits to company.

The disadvantage of applying this planning tool is that this budgets is not effective in

case of company engaged with large number of employees. There are more chances of fraud in

entries and thus the budgets not relies on authenticity. It also results in distracting the mind of the

employees in respect of getting familiar with the company actual position in market. The major

advantages which is examined is relating to using the high man power to accomplish such task,

as it is not necessary that very company had large number of employees to accomplish such

activity.

Kaizen Budget: This budgets is initiated in respect of improving the process through

reducing cost. Thus the main reason of choosing this planning tool by CORUS is that the

changes are needed for better improvement in products which results in sustaining the

business for longer time period. The main advantages of preferring the Kaizen budget is

that by adapting this budgets it results in saving cost in company. Thus, by this

perspective, they can expand their business easily (Wildavsky, 2017). Through this

aspects, it mainly focuses on improving the performances through reducing waste.

Through this budgets, the major advantages which they carry is relating to improving the

employee’s satisfaction at work place. Through this manner they gain major advantages

are retaining the skilled and loyal employees in work premises.

The disadvantage of preferring their budgets is that it distract the whole working of the

system and also employees not easily accept for such changes. It undertakes the long procedure

in respect of providing training to employees to provide better results. As employees are set with

any of the transaction from the previous statement. They had to prepare all the activities

from, starting. In respect of CORUS, the planning tool is effective as the managers can

personally interact with every department regarding examining their issue and then

applied them in company to get better results (Miller, 2018.). The advantages of

preferring the Zero budgets is that by applying this budget, it result in enhancing the

communication at work place by communicating with each department to examined their

reviews and thoughts. It also resulting in getting more accurate results regarding the

company information as the budgets is prepared from the zero base. It also saves the

resources of the company by dealing in only that products which resulting in costing

benefits to company.

The disadvantage of applying this planning tool is that this budgets is not effective in

case of company engaged with large number of employees. There are more chances of fraud in

entries and thus the budgets not relies on authenticity. It also results in distracting the mind of the

employees in respect of getting familiar with the company actual position in market. The major

advantages which is examined is relating to using the high man power to accomplish such task,

as it is not necessary that very company had large number of employees to accomplish such

activity.

Kaizen Budget: This budgets is initiated in respect of improving the process through

reducing cost. Thus the main reason of choosing this planning tool by CORUS is that the

changes are needed for better improvement in products which results in sustaining the

business for longer time period. The main advantages of preferring the Kaizen budget is

that by adapting this budgets it results in saving cost in company. Thus, by this

perspective, they can expand their business easily (Wildavsky, 2017). Through this

aspects, it mainly focuses on improving the performances through reducing waste.

Through this budgets, the major advantages which they carry is relating to improving the

employee’s satisfaction at work place. Through this manner they gain major advantages

are retaining the skilled and loyal employees in work premises.

The disadvantage of preferring their budgets is that it distract the whole working of the

system and also employees not easily accept for such changes. It undertakes the long procedure

in respect of providing training to employees to provide better results. As employees are set with

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.