Management Accounting Report: Master Budget and Analysis

VerifiedAdded on 2021/05/30

|14

|1816

|81

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, focusing on the formulation of a master budget, analysis of a production program, and a comparison between participative and imposed budgeting approaches. The report includes detailed figures illustrating sales, production, direct labor, purchase, direct material, manufacturing overhead, cash flow, cost of goods manufactured, and income statements. The analysis of the production program evaluates the impact of a new production plan on revenue and costs, utilizing budget figures to forecast sales volume, production volume, and direct material requirements. The report also contrasts participative and imposed budgets, discussing their respective advantages and disadvantages in terms of employee involvement, communication, and cost-effectiveness. The report concludes by highlighting the importance of participative budgeting in implementing business strategies and objectives.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

MANAGEMENT ACCOUNTING

Table of Contents

Part A.................................................................................................................................2

Formulation of Master Budget........................................................................................2

Part B.................................................................................................................................8

Analysis of Production Program.....................................................................................8

Part C...............................................................................................................................10

Participative Budget and Imposed Budget...................................................................10

Reference........................................................................................................................12

MANAGEMENT ACCOUNTING

Table of Contents

Part A.................................................................................................................................2

Formulation of Master Budget........................................................................................2

Part B.................................................................................................................................8

Analysis of Production Program.....................................................................................8

Part C...............................................................................................................................10

Participative Budget and Imposed Budget...................................................................10

Reference........................................................................................................................12

2

MANAGEMENT ACCOUNTING

Part A

Formulation of Master Budget

Figure 1: (Image Showing Sales Budget)

Source: (Created by Author)

Figure 2: (Image Showing Production Budget)

Source: (Created by Author)

MANAGEMENT ACCOUNTING

Part A

Formulation of Master Budget

Figure 1: (Image Showing Sales Budget)

Source: (Created by Author)

Figure 2: (Image Showing Production Budget)

Source: (Created by Author)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

MANAGEMENT ACCOUNTING

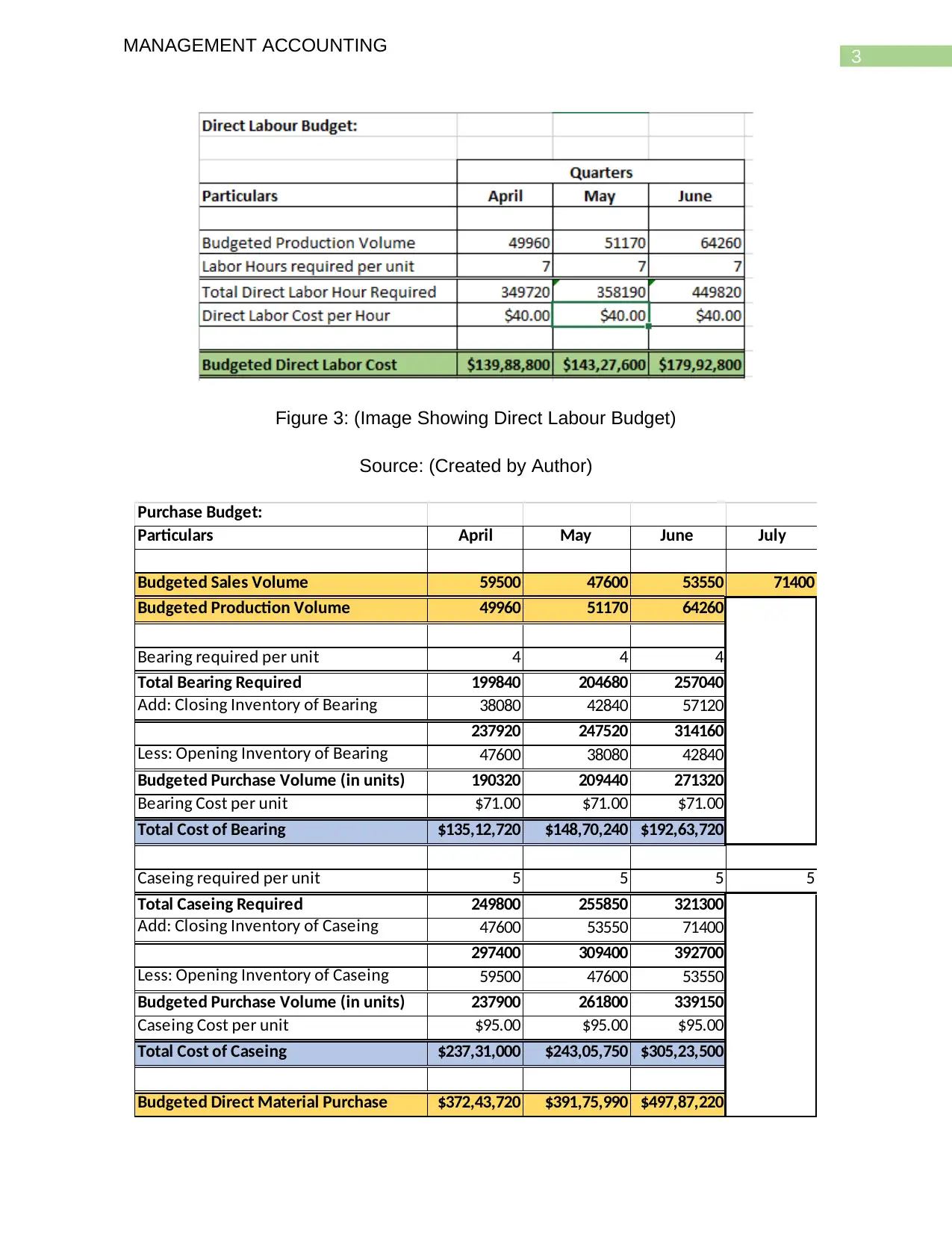

Figure 3: (Image Showing Direct Labour Budget)

Source: (Created by Author)

Purchase Budget:

Particulars April May June July

Budgeted Sales Volume 59500 47600 53550 71400

Budgeted Production Volume 49960 51170 64260

Bearing required per unit 4 4 4

Total Bearing Required 199840 204680 257040

Add: Closing Inventory of Bearing 38080 42840 57120

237920 247520 314160

Less: Opening Inventory of Bearing 47600 38080 42840

Budgeted Purchase Volume (in units) 190320 209440 271320

Bearing Cost per unit $71.00 $71.00 $71.00

Total Cost of Bearing $135,12,720 $148,70,240 $192,63,720

Caseing required per unit 5 5 5 5

Total Caseing Required 249800 255850 321300

Add: Closing Inventory of Caseing 47600 53550 71400

297400 309400 392700

Less: Opening Inventory of Caseing 59500 47600 53550

Budgeted Purchase Volume (in units) 237900 261800 339150

Caseing Cost per unit $95.00 $95.00 $95.00

Total Cost of Caseing $237,31,000 $243,05,750 $305,23,500

Budgeted Direct Material Purchase $372,43,720 $391,75,990 $497,87,220

MANAGEMENT ACCOUNTING

Figure 3: (Image Showing Direct Labour Budget)

Source: (Created by Author)

Purchase Budget:

Particulars April May June July

Budgeted Sales Volume 59500 47600 53550 71400

Budgeted Production Volume 49960 51170 64260

Bearing required per unit 4 4 4

Total Bearing Required 199840 204680 257040

Add: Closing Inventory of Bearing 38080 42840 57120

237920 247520 314160

Less: Opening Inventory of Bearing 47600 38080 42840

Budgeted Purchase Volume (in units) 190320 209440 271320

Bearing Cost per unit $71.00 $71.00 $71.00

Total Cost of Bearing $135,12,720 $148,70,240 $192,63,720

Caseing required per unit 5 5 5 5

Total Caseing Required 249800 255850 321300

Add: Closing Inventory of Caseing 47600 53550 71400

297400 309400 392700

Less: Opening Inventory of Caseing 59500 47600 53550

Budgeted Purchase Volume (in units) 237900 261800 339150

Caseing Cost per unit $95.00 $95.00 $95.00

Total Cost of Caseing $237,31,000 $243,05,750 $305,23,500

Budgeted Direct Material Purchase $372,43,720 $391,75,990 $497,87,220

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

MANAGEMENT ACCOUNTING

Figure 4: (Image Showing Purchase Budget)

Source: (Created by Author)

Figure 5: (Image Showing Direct Material Budget)

Source: (Created by Author)

MANAGEMENT ACCOUNTING

Figure 4: (Image Showing Purchase Budget)

Source: (Created by Author)

Figure 5: (Image Showing Direct Material Budget)

Source: (Created by Author)

5

MANAGEMENT ACCOUNTING

Manufacturing Overhead Budget:

Particulars April May June

Direct Labour Hour 349720 358190 449820

Indirect Labor Cost per DLH $49.98 $49.98 $49.98

Total Indirect Labor Cost $174,79,006 $179,02,336 $224,82,004

Power Cost per DLH $4.76 $4.76 $4.76

Total Power Cost $16,64,667 $17,04,984 $21,41,143

Variable Maintenance Cost per unit $37.78 $37.78 $37.78

Variable Maintenance Cost $132,11,644 $135,31,622 $169,93,200

Fixed Maintenance $270,65,889 $270,65,889 $270,65,889

Total Maintenance Costs $402,77,533 $405,97,511 $440,59,089

Other Variable Cost per unit $35.70 $35.70 $35.70

Other Variable Cost $124,85,004 $127,87,383 $160,58,574

Other Fixed Cost $119,00,000 $119,00,000 $119,00,000

Other Manufacturing Costs $243,85,004 $246,87,383 $279,58,574

Supervision $333,20,000 $333,20,000 $333,20,000

Depreciation $29,75,000 $29,75,000 $29,75,000

Rates & Utilities $24,58,500 $24,58,500 $24,58,500

Budgeted Manufacturing Overhead $1225,59,710 $1236,45,715 $1353,94,310

Figure 6: (Image Showing Manufacturing Overhead Budget)

Source: (Created by Author)

MANAGEMENT ACCOUNTING

Manufacturing Overhead Budget:

Particulars April May June

Direct Labour Hour 349720 358190 449820

Indirect Labor Cost per DLH $49.98 $49.98 $49.98

Total Indirect Labor Cost $174,79,006 $179,02,336 $224,82,004

Power Cost per DLH $4.76 $4.76 $4.76

Total Power Cost $16,64,667 $17,04,984 $21,41,143

Variable Maintenance Cost per unit $37.78 $37.78 $37.78

Variable Maintenance Cost $132,11,644 $135,31,622 $169,93,200

Fixed Maintenance $270,65,889 $270,65,889 $270,65,889

Total Maintenance Costs $402,77,533 $405,97,511 $440,59,089

Other Variable Cost per unit $35.70 $35.70 $35.70

Other Variable Cost $124,85,004 $127,87,383 $160,58,574

Other Fixed Cost $119,00,000 $119,00,000 $119,00,000

Other Manufacturing Costs $243,85,004 $246,87,383 $279,58,574

Supervision $333,20,000 $333,20,000 $333,20,000

Depreciation $29,75,000 $29,75,000 $29,75,000

Rates & Utilities $24,58,500 $24,58,500 $24,58,500

Budgeted Manufacturing Overhead $1225,59,710 $1236,45,715 $1353,94,310

Figure 6: (Image Showing Manufacturing Overhead Budget)

Source: (Created by Author)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

MANAGEMENT ACCOUNTING

Figure 7: (Image Showing Total Collection from Debtors)

Source: (Created by Author)

Cash Budget:

Particulars April May June TOTAL

Cash Flow from Operational Activities:

Collection from Debtors $2834,07,360 $2781,03,000 $2930,25,600 $8545,35,960

Payment to Suppliers -$372,43,720 -$391,75,990 -$497,87,220 -$1262,06,930

Direct Labour Cost Paid -$139,88,800 -$143,27,600 -$179,92,800 -$463,09,200

Indirect Labor Cost -$174,79,006 -$179,02,336 -$224,82,004 -$578,63,345

Power Cost -$16,64,667 -$17,04,984 -$21,41,143 -$55,10,795

Maintenance Charges Paid -$402,77,533 -$405,97,511 -$440,59,089 -$1249,34,133

Other Manufacturing Cost -$243,85,004 -$246,87,383 -$279,58,574 -$770,30,961

Supervision -$333,20,000 -$333,20,000 -$333,20,000 -$999,60,000

Rates & Utilities -$24,58,500 -$24,58,500 -$24,58,500 -$73,75,500

Selling & Administration Expenses -$709,49,460 -$223,26,600 -$273,21,900 -$1205,97,960

Net Cash Flow from Operating Activities $416,40,670 $816,02,095 $655,04,370 $1887,47,135

Cash Flow from Investing Activities:

Purchase of Land -$309,40,000 -$309,40,000

Net Cash Flow from Investing Activities $0 -$309,40,000 $0 -$309,40,000

Cash Flow from Financing Activities:

Dividend Paid -$10,53,150 -$10,53,150

Loan from Bank $0

Repayment of Loan $0 $0 $0

Interest Paid $0 $0 $0

Net Cash Flow from Financing Activities $0 -$10,53,150 $0 -$10,53,150

Net Increase/(Decrease) in Cash Flows $416,40,670 $496,08,945 $655,04,370 $1567,53,985

Add: Opening Cash Balance $29,75,000 $446,15,670 $942,24,615 $29,75,000

Closing Cash Balance $446,15,670 $942,24,615 $1597,28,985 $1597,28,985

Figure 8: (Image Showing Cash Budget)

Source: (Created by Author)

MANAGEMENT ACCOUNTING

Figure 7: (Image Showing Total Collection from Debtors)

Source: (Created by Author)

Cash Budget:

Particulars April May June TOTAL

Cash Flow from Operational Activities:

Collection from Debtors $2834,07,360 $2781,03,000 $2930,25,600 $8545,35,960

Payment to Suppliers -$372,43,720 -$391,75,990 -$497,87,220 -$1262,06,930

Direct Labour Cost Paid -$139,88,800 -$143,27,600 -$179,92,800 -$463,09,200

Indirect Labor Cost -$174,79,006 -$179,02,336 -$224,82,004 -$578,63,345

Power Cost -$16,64,667 -$17,04,984 -$21,41,143 -$55,10,795

Maintenance Charges Paid -$402,77,533 -$405,97,511 -$440,59,089 -$1249,34,133

Other Manufacturing Cost -$243,85,004 -$246,87,383 -$279,58,574 -$770,30,961

Supervision -$333,20,000 -$333,20,000 -$333,20,000 -$999,60,000

Rates & Utilities -$24,58,500 -$24,58,500 -$24,58,500 -$73,75,500

Selling & Administration Expenses -$709,49,460 -$223,26,600 -$273,21,900 -$1205,97,960

Net Cash Flow from Operating Activities $416,40,670 $816,02,095 $655,04,370 $1887,47,135

Cash Flow from Investing Activities:

Purchase of Land -$309,40,000 -$309,40,000

Net Cash Flow from Investing Activities $0 -$309,40,000 $0 -$309,40,000

Cash Flow from Financing Activities:

Dividend Paid -$10,53,150 -$10,53,150

Loan from Bank $0

Repayment of Loan $0 $0 $0

Interest Paid $0 $0 $0

Net Cash Flow from Financing Activities $0 -$10,53,150 $0 -$10,53,150

Net Increase/(Decrease) in Cash Flows $416,40,670 $496,08,945 $655,04,370 $1567,53,985

Add: Opening Cash Balance $29,75,000 $446,15,670 $942,24,615 $29,75,000

Closing Cash Balance $446,15,670 $942,24,615 $1597,28,985 $1597,28,985

Figure 8: (Image Showing Cash Budget)

Source: (Created by Author)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGEMENT ACCOUNTING

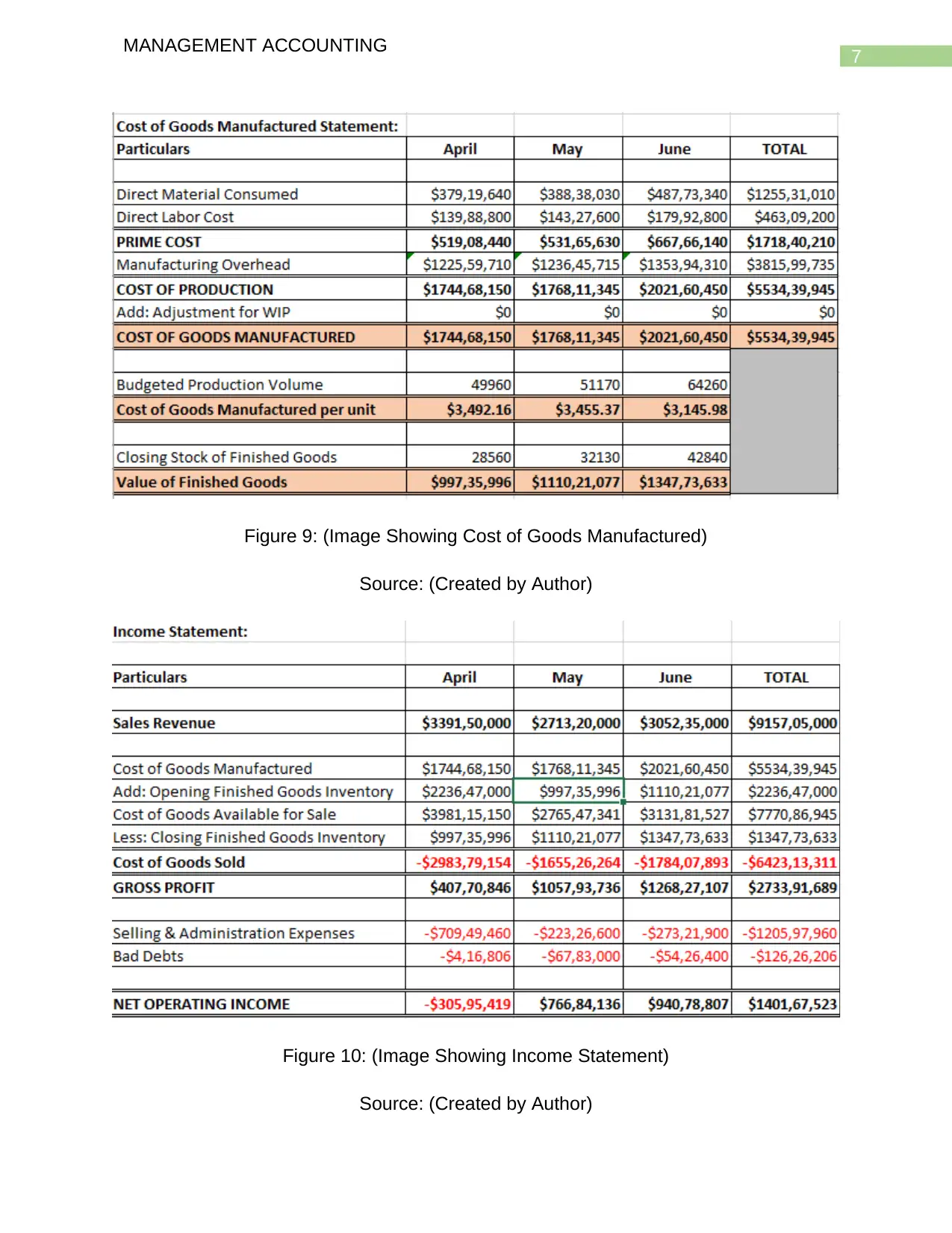

Figure 9: (Image Showing Cost of Goods Manufactured)

Source: (Created by Author)

Figure 10: (Image Showing Income Statement)

Source: (Created by Author)

MANAGEMENT ACCOUNTING

Figure 9: (Image Showing Cost of Goods Manufactured)

Source: (Created by Author)

Figure 10: (Image Showing Income Statement)

Source: (Created by Author)

8

MANAGEMENT ACCOUNTING

Part B

Analysis of Production Program

The sales manager of Weiming Pty ltd is considering introducing a new

production program which can benefit the company and thereby increase the production

volume of the business. The sales manager is of the opinion that the new production

plan will be increasing the revenue of the company but in order to be sure the

management will be preparing a master budget which will be estimating the revenue

and the costs which are associated with the production plan (Cox 2014). The analysis of

the budget is discussed in the paragraph which are given below.

As per the budget which is prepared by the company, the sales budget shows

that the sales volume has decreased from the month of April to May and then it has

again increased from May to June. The sales volume has further increased from 53550

in June to 71400 in July. The Budgeted sales revenue is shown to be $ 4069,80,000 in

the month of July which is due to the increase in the production units (Hutchings et al.

2014). The production budget shows that the production volume of the company has

increased from April which was 49960 and has become 64260 in the month of June

which shows the increase in the production of the company. Such an increase in the

production is estimated due to the increase in the production capacity of the company.

The direct material budget shows that it is estimated that the direct labour hours which

are required to achieve the production target will also increase with the increase in the

production volume of the company (Brown and Koettl 2015). The direct labour hour

which is anticipated in the month of June which is highest in terms of production volume

shows that 449820 hours will be required. The budgeted direct labour cost which are

incurred is estimated to be highest in the month of June as per the quarterly analysis

which is shown to be $ 179,92,800 as per the budget. As the sales volume and

production volume is expected to increase and reach a highest by the month of June,

the direct material requirement will also be high (Drury 2013). The material which is

used by the business is bearing which is estimated to cost $ 192,63,720 in the month of

June which shows a tremendous increase as per the estimate for the month of May

which was $ 148,70,240. The cost of caseing is estimated to be $ 305,23,500 for the

MANAGEMENT ACCOUNTING

Part B

Analysis of Production Program

The sales manager of Weiming Pty ltd is considering introducing a new

production program which can benefit the company and thereby increase the production

volume of the business. The sales manager is of the opinion that the new production

plan will be increasing the revenue of the company but in order to be sure the

management will be preparing a master budget which will be estimating the revenue

and the costs which are associated with the production plan (Cox 2014). The analysis of

the budget is discussed in the paragraph which are given below.

As per the budget which is prepared by the company, the sales budget shows

that the sales volume has decreased from the month of April to May and then it has

again increased from May to June. The sales volume has further increased from 53550

in June to 71400 in July. The Budgeted sales revenue is shown to be $ 4069,80,000 in

the month of July which is due to the increase in the production units (Hutchings et al.

2014). The production budget shows that the production volume of the company has

increased from April which was 49960 and has become 64260 in the month of June

which shows the increase in the production of the company. Such an increase in the

production is estimated due to the increase in the production capacity of the company.

The direct material budget shows that it is estimated that the direct labour hours which

are required to achieve the production target will also increase with the increase in the

production volume of the company (Brown and Koettl 2015). The direct labour hour

which is anticipated in the month of June which is highest in terms of production volume

shows that 449820 hours will be required. The budgeted direct labour cost which are

incurred is estimated to be highest in the month of June as per the quarterly analysis

which is shown to be $ 179,92,800 as per the budget. As the sales volume and

production volume is expected to increase and reach a highest by the month of June,

the direct material requirement will also be high (Drury 2013). The material which is

used by the business is bearing which is estimated to cost $ 192,63,720 in the month of

June which shows a tremendous increase as per the estimate for the month of May

which was $ 148,70,240. The cost of caseing is estimated to be $ 305,23,500 for the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

MANAGEMENT ACCOUNTING

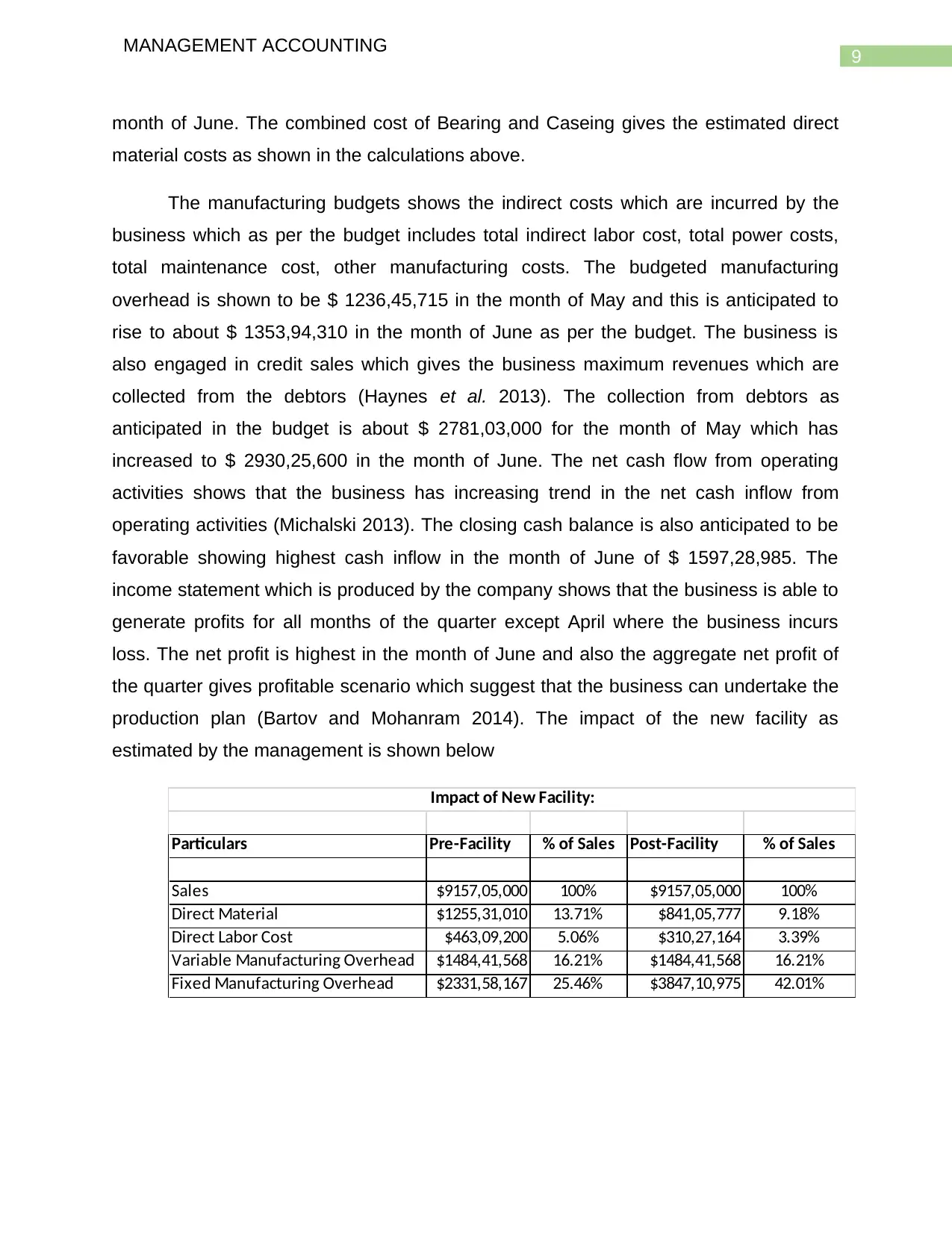

month of June. The combined cost of Bearing and Caseing gives the estimated direct

material costs as shown in the calculations above.

The manufacturing budgets shows the indirect costs which are incurred by the

business which as per the budget includes total indirect labor cost, total power costs,

total maintenance cost, other manufacturing costs. The budgeted manufacturing

overhead is shown to be $ 1236,45,715 in the month of May and this is anticipated to

rise to about $ 1353,94,310 in the month of June as per the budget. The business is

also engaged in credit sales which gives the business maximum revenues which are

collected from the debtors (Haynes et al. 2013). The collection from debtors as

anticipated in the budget is about $ 2781,03,000 for the month of May which has

increased to $ 2930,25,600 in the month of June. The net cash flow from operating

activities shows that the business has increasing trend in the net cash inflow from

operating activities (Michalski 2013). The closing cash balance is also anticipated to be

favorable showing highest cash inflow in the month of June of $ 1597,28,985. The

income statement which is produced by the company shows that the business is able to

generate profits for all months of the quarter except April where the business incurs

loss. The net profit is highest in the month of June and also the aggregate net profit of

the quarter gives profitable scenario which suggest that the business can undertake the

production plan (Bartov and Mohanram 2014). The impact of the new facility as

estimated by the management is shown below

Particulars Pre-Facility % of Sales Post-Facility % of Sales

Sales $9157,05,000 100% $9157,05,000 100%

Direct Material $1255,31,010 13.71% $841,05,777 9.18%

Direct Labor Cost $463,09,200 5.06% $310,27,164 3.39%

Variable Manufacturing Overhead $1484,41,568 16.21% $1484,41,568 16.21%

Fixed Manufacturing Overhead $2331,58,167 25.46% $3847,10,975 42.01%

Impact of New Facility:

MANAGEMENT ACCOUNTING

month of June. The combined cost of Bearing and Caseing gives the estimated direct

material costs as shown in the calculations above.

The manufacturing budgets shows the indirect costs which are incurred by the

business which as per the budget includes total indirect labor cost, total power costs,

total maintenance cost, other manufacturing costs. The budgeted manufacturing

overhead is shown to be $ 1236,45,715 in the month of May and this is anticipated to

rise to about $ 1353,94,310 in the month of June as per the budget. The business is

also engaged in credit sales which gives the business maximum revenues which are

collected from the debtors (Haynes et al. 2013). The collection from debtors as

anticipated in the budget is about $ 2781,03,000 for the month of May which has

increased to $ 2930,25,600 in the month of June. The net cash flow from operating

activities shows that the business has increasing trend in the net cash inflow from

operating activities (Michalski 2013). The closing cash balance is also anticipated to be

favorable showing highest cash inflow in the month of June of $ 1597,28,985. The

income statement which is produced by the company shows that the business is able to

generate profits for all months of the quarter except April where the business incurs

loss. The net profit is highest in the month of June and also the aggregate net profit of

the quarter gives profitable scenario which suggest that the business can undertake the

production plan (Bartov and Mohanram 2014). The impact of the new facility as

estimated by the management is shown below

Particulars Pre-Facility % of Sales Post-Facility % of Sales

Sales $9157,05,000 100% $9157,05,000 100%

Direct Material $1255,31,010 13.71% $841,05,777 9.18%

Direct Labor Cost $463,09,200 5.06% $310,27,164 3.39%

Variable Manufacturing Overhead $1484,41,568 16.21% $1484,41,568 16.21%

Fixed Manufacturing Overhead $2331,58,167 25.46% $3847,10,975 42.01%

Impact of New Facility:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

MANAGEMENT ACCOUNTING

Part C

Participative Budget and Imposed Budget

A Participative Budget refers to a budget which is prepared with the collaboration

of the all the people who are affected by the implementation of the budget. In case of a

participative budget the employees are involved in the preparation of the budget and

participative approach towards budget preparation is also known as down to top budget

(Heinle, Ross and Saouma 2013). A participative budget is also favorable for the

business as it boasts the morale of the employees and also the employee are motivated

for achieving the goals or standards of the company as specified in the budget. Due to a

large number of employees are involved in a participative budget, therefore it takes

more time to be prepared than in the case of normal budget. The cost of labor for

preparing such a budget is also comparatively higher. In case of a participative budget

effective communication can flow between departments while preparation of the budget.

The basic idea which is behind the budget is that the subordinate should be assigned

responsibility regarding aspects of budget (Derfuss 2016). Such types of budget also

facilitate transferal of information from the subordinates to superior of the business. The

subordinates can discuss their problems with the superiors and this kind of a budget

involves every individual which is present in the organization who is affected or likely to

be affected by the activities of the budget.

In case of an imposed budget, the budgets are prepared by the top-level

managers and then imposed down on the lower level management of the company. In

preparation of such a budget, there is not input taken from the lower level employee of

the organization and the objectives and decisions are imposed on such employees

(Allard et al. 2013). These types of budgets are also known as top to bottom budgets as

they are prepared by the top-level management and imposed on the lower level

management. This type of approach for preparation of budget is less costly and more

direct but it lacks the participation and thus the human touch and it does not facilitate

communication between the top-level management and the lower-level management.

MANAGEMENT ACCOUNTING

Part C

Participative Budget and Imposed Budget

A Participative Budget refers to a budget which is prepared with the collaboration

of the all the people who are affected by the implementation of the budget. In case of a

participative budget the employees are involved in the preparation of the budget and

participative approach towards budget preparation is also known as down to top budget

(Heinle, Ross and Saouma 2013). A participative budget is also favorable for the

business as it boasts the morale of the employees and also the employee are motivated

for achieving the goals or standards of the company as specified in the budget. Due to a

large number of employees are involved in a participative budget, therefore it takes

more time to be prepared than in the case of normal budget. The cost of labor for

preparing such a budget is also comparatively higher. In case of a participative budget

effective communication can flow between departments while preparation of the budget.

The basic idea which is behind the budget is that the subordinate should be assigned

responsibility regarding aspects of budget (Derfuss 2016). Such types of budget also

facilitate transferal of information from the subordinates to superior of the business. The

subordinates can discuss their problems with the superiors and this kind of a budget

involves every individual which is present in the organization who is affected or likely to

be affected by the activities of the budget.

In case of an imposed budget, the budgets are prepared by the top-level

managers and then imposed down on the lower level management of the company. In

preparation of such a budget, there is not input taken from the lower level employee of

the organization and the objectives and decisions are imposed on such employees

(Allard et al. 2013). These types of budgets are also known as top to bottom budgets as

they are prepared by the top-level management and imposed on the lower level

management. This type of approach for preparation of budget is less costly and more

direct but it lacks the participation and thus the human touch and it does not facilitate

communication between the top-level management and the lower-level management.

11

MANAGEMENT ACCOUNTING

In case of participatory budget, the company which has been analyzed in Part B

of the assignment would be preparing budgets with the collective collaboration of all

departments which are present in the business. The budget would be prepared with the

collective effort of all the employees of the business. On the other hand, if the

management uses imposed budget than all the vital decision is taken by the

management and there is little or no participation of the staff and lower level

management. It can be said that a participative budget is more effective for

implementing the strategies and objectives of the business.

MANAGEMENT ACCOUNTING

In case of participatory budget, the company which has been analyzed in Part B

of the assignment would be preparing budgets with the collective collaboration of all

departments which are present in the business. The budget would be prepared with the

collective effort of all the employees of the business. On the other hand, if the

management uses imposed budget than all the vital decision is taken by the

management and there is little or no participation of the staff and lower level

management. It can be said that a participative budget is more effective for

implementing the strategies and objectives of the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.