Comprehensive Management Accounting Report: Tech UK Limited Financials

VerifiedAdded on 2021/06/17

|25

|5201

|57

Report

AI Summary

This report analyzes the management accounting practices of Tech UK Limited, covering key areas such as the differences between management and financial accounting, the importance of management accounting for decision-making, and various cost accounting and inventory management systems. It delves into the types of managerial accounting reports, including budget reports, and emphasizes the significance of presenting information in an understandable manner. The report includes an income statement using absorption costing and explores budgeting for planning and control, along with the advantages and disadvantages of budgeting. Furthermore, it examines the application of management accounting to address financial problems and the implementation of a balanced scorecard for Tech UK Limited, concluding with a comprehensive overview of the company's financial performance and strategic planning.

Management Accounting

Tech (U.K) Limited

5/9/2018

Tech (U.K) Limited

5/9/2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING 1

Table of Contents

Introduction................................................................................................................................2

Task 1.....................................................................................................................................2

iii. Cost Accounting Systems.............................................................................................5

Iv Inventory Management Systems....................................................................................6

v. Job Costing System........................................................................................................6

i. Types of Managerial accounting reports.........................................................................7

ii. Importance of presentation of the information in an understandable manner...............8

Task 2.....................................................................................................................................8

Absorption Costing................................................................................................................8

Income Statement of Tech (UK) Limited using Absorption Costing......................................10

Marginal Costing..................................................................................................................10

Task 3...................................................................................................................................12

Kinds of Budget...............................................................................................................12

Advantages of Budget......................................................................................................14

Disadvantages of Budget..................................................................................................14

Task 4...................................................................................................................................16

Use of Management Accounting to overcome financial problems..................................16

Balanced Scorecard for Tech UK Limited.......................................................................16

Conclusion................................................................................................................................19

References................................................................................................................................20

Table of Contents

Introduction................................................................................................................................2

Task 1.....................................................................................................................................2

iii. Cost Accounting Systems.............................................................................................5

Iv Inventory Management Systems....................................................................................6

v. Job Costing System........................................................................................................6

i. Types of Managerial accounting reports.........................................................................7

ii. Importance of presentation of the information in an understandable manner...............8

Task 2.....................................................................................................................................8

Absorption Costing................................................................................................................8

Income Statement of Tech (UK) Limited using Absorption Costing......................................10

Marginal Costing..................................................................................................................10

Task 3...................................................................................................................................12

Kinds of Budget...............................................................................................................12

Advantages of Budget......................................................................................................14

Disadvantages of Budget..................................................................................................14

Task 4...................................................................................................................................16

Use of Management Accounting to overcome financial problems..................................16

Balanced Scorecard for Tech UK Limited.......................................................................16

Conclusion................................................................................................................................19

References................................................................................................................................20

MANAGEMENT ACCOUNTING 2

Introduction

Accounting means the procedure of recording, categorizing and summarizing the events and

transaction of the business in financial terms, and understanding the consequences (Bazley,

Hancock and Robinson, 2014). This report is being prepared in order to highlight the

functions of Management Accounting systems which will involve four tasks. Task one will

provide the description of management accounting and important requirements of the system

of management accounting in the Tech UK Limited. In Task two income statement of the

company will be presented. Task three will explain the use of budget for planning and control

purposes and in Task four different ways will be explained by which the balanced scorecard

method can be utilized to respond company’s financial or economic problems.

Task 1

a) i. What is Management Accounting and difference between Financial accounting and

Management Accounting.

Management accounting and financial accounting are the two accounting branches.

Management accounting objects at offering both quantitative and qualitative information to

the administrators, so as to support them in the process of decision making and therefore

maximizing the profit (Nørreklit, 2017). On the contrary financial accounting focuses on

providing a fair and true review of the company’s financial position to different parties

(Narayanaswamy, 2014).

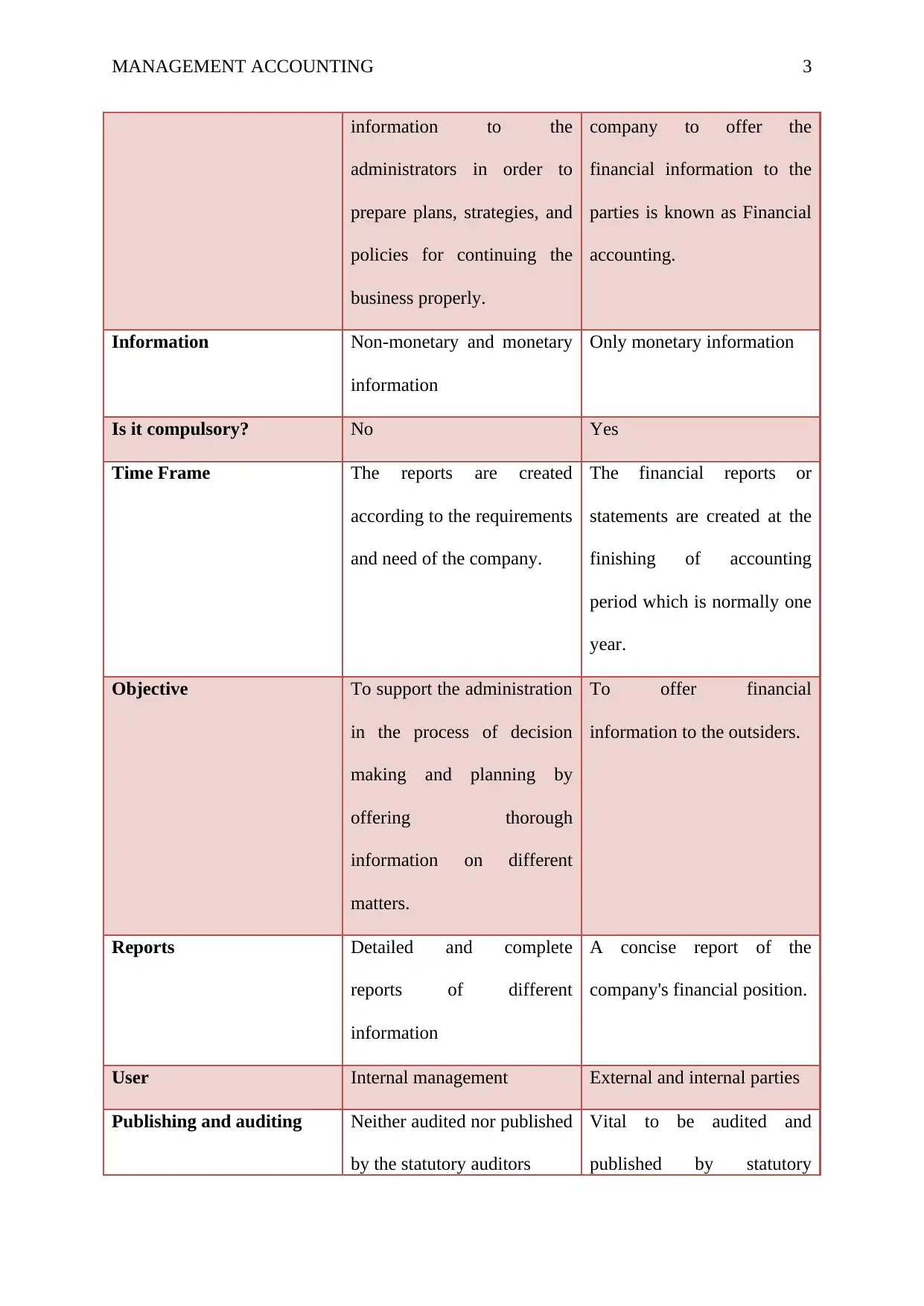

Basis Management Accounting Financial Accounting

Meaning Management accounting is

the system of accounting

which offers significant

A system of accounting that

emphasis on the financial

statement preparation of a

Introduction

Accounting means the procedure of recording, categorizing and summarizing the events and

transaction of the business in financial terms, and understanding the consequences (Bazley,

Hancock and Robinson, 2014). This report is being prepared in order to highlight the

functions of Management Accounting systems which will involve four tasks. Task one will

provide the description of management accounting and important requirements of the system

of management accounting in the Tech UK Limited. In Task two income statement of the

company will be presented. Task three will explain the use of budget for planning and control

purposes and in Task four different ways will be explained by which the balanced scorecard

method can be utilized to respond company’s financial or economic problems.

Task 1

a) i. What is Management Accounting and difference between Financial accounting and

Management Accounting.

Management accounting and financial accounting are the two accounting branches.

Management accounting objects at offering both quantitative and qualitative information to

the administrators, so as to support them in the process of decision making and therefore

maximizing the profit (Nørreklit, 2017). On the contrary financial accounting focuses on

providing a fair and true review of the company’s financial position to different parties

(Narayanaswamy, 2014).

Basis Management Accounting Financial Accounting

Meaning Management accounting is

the system of accounting

which offers significant

A system of accounting that

emphasis on the financial

statement preparation of a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGEMENT ACCOUNTING 3

information to the

administrators in order to

prepare plans, strategies, and

policies for continuing the

business properly.

company to offer the

financial information to the

parties is known as Financial

accounting.

Information Non-monetary and monetary

information

Only monetary information

Is it compulsory? No Yes

Time Frame The reports are created

according to the requirements

and need of the company.

The financial reports or

statements are created at the

finishing of accounting

period which is normally one

year.

Objective To support the administration

in the process of decision

making and planning by

offering thorough

information on different

matters.

To offer financial

information to the outsiders.

Reports Detailed and complete

reports of different

information

A concise report of the

company's financial position.

User Internal management External and internal parties

Publishing and auditing Neither audited nor published

by the statutory auditors

Vital to be audited and

published by statutory

information to the

administrators in order to

prepare plans, strategies, and

policies for continuing the

business properly.

company to offer the

financial information to the

parties is known as Financial

accounting.

Information Non-monetary and monetary

information

Only monetary information

Is it compulsory? No Yes

Time Frame The reports are created

according to the requirements

and need of the company.

The financial reports or

statements are created at the

finishing of accounting

period which is normally one

year.

Objective To support the administration

in the process of decision

making and planning by

offering thorough

information on different

matters.

To offer financial

information to the outsiders.

Reports Detailed and complete

reports of different

information

A concise report of the

company's financial position.

User Internal management External and internal parties

Publishing and auditing Neither audited nor published

by the statutory auditors

Vital to be audited and

published by statutory

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING 4

auditors (Surbhi, 2014)

ii. The importance of information of the management accounting as a tool of decision-

making for the managers of department

Management accounting is very essential for every company so as for Tech (UK) Limited.

Some of the management accounting importance is:

Support in making the plan – Current era is the period of planning. Producers who are said

to be the most successful producers are those who produce articles as per the needs and plan

of the consumers. Before making any plan the administration of the Tech UK Limited

Company should study and evaluate the future and present of the business.

Better services to the consumers – Management accounting which is also called as cost

control device allows the decrease in the product prices. Every employee in the concern is

made cost Curious. The product quality of the Tech UK Limited will become effective due to

the implementation of quality standards. The consumers are delivered goods at reasonable

prices.

Easy to make a judgment – Before making any plan or defining policies, there are various

policies or plan in front of the management based on which they decide which policy and

plan need to the adopted such that may become more helpful and useful.

Performance Measurements – The budgeting control standard costing techniques allows

measuring the presentation or performance. In the standard costing, standards are defined first

and then the actual or definite cost is associated with the standard costing. This system will

support the management of Tech UK Limited to identify deviations between actual cost and

auditors (Surbhi, 2014)

ii. The importance of information of the management accounting as a tool of decision-

making for the managers of department

Management accounting is very essential for every company so as for Tech (UK) Limited.

Some of the management accounting importance is:

Support in making the plan – Current era is the period of planning. Producers who are said

to be the most successful producers are those who produce articles as per the needs and plan

of the consumers. Before making any plan the administration of the Tech UK Limited

Company should study and evaluate the future and present of the business.

Better services to the consumers – Management accounting which is also called as cost

control device allows the decrease in the product prices. Every employee in the concern is

made cost Curious. The product quality of the Tech UK Limited will become effective due to

the implementation of quality standards. The consumers are delivered goods at reasonable

prices.

Easy to make a judgment – Before making any plan or defining policies, there are various

policies or plan in front of the management based on which they decide which policy and

plan need to the adopted such that may become more helpful and useful.

Performance Measurements – The budgeting control standard costing techniques allows

measuring the presentation or performance. In the standard costing, standards are defined first

and then the actual or definite cost is associated with the standard costing. This system will

support the management of Tech UK Limited to identify deviations between actual cost and

MANAGEMENT ACCOUNTING 5

standard cost. The effective performance of the company can be identified if the actual cost

does not surpass the standard cost.

Increase effectiveness of the business - The business effectiveness increases through

management accounting. The objectives of various subdivisions of the company are defined

in advance and the success of these goals is considered as a instrument for assessing their

competence (Management study online, 2018).

iii. Cost Accounting Systems

A framework utilized by the companies to identify the product cost for inventory analysis

cost control and profitability analysis is known as Cost accounting systems. Identifying the

precise product cost is serious for lucrative operations. It is very important for Tech UK

Limited to see which product is moneymaking and which one is not effective, and this can be

determined when it possesses projected accurate product cost. In addition to this, a system of

product costing supports in approximating the concluding cost of materials inventory,

finished goods inventory and work-in-progress inventory for the drive of financial

preparation (Accounting Explained, 2013). The types of costing system are:

Historical Costing – In this, the costs are determined only when they have incurred. The key

purpose of it is to determine costs which had been incurred in past. The historical costs are

utilized for investigation of incurred actual costs and it will be very late to control or manage.

The actual statistics can be associated only when the performance standards exist.

For instance: The Washington Company built a building in 2005, with a cost of $45,000. On

December 31, 2017, the building’s fair market value is $65,000 however still stands on it

original cost of $45,000 on balance sheet.

standard cost. The effective performance of the company can be identified if the actual cost

does not surpass the standard cost.

Increase effectiveness of the business - The business effectiveness increases through

management accounting. The objectives of various subdivisions of the company are defined

in advance and the success of these goals is considered as a instrument for assessing their

competence (Management study online, 2018).

iii. Cost Accounting Systems

A framework utilized by the companies to identify the product cost for inventory analysis

cost control and profitability analysis is known as Cost accounting systems. Identifying the

precise product cost is serious for lucrative operations. It is very important for Tech UK

Limited to see which product is moneymaking and which one is not effective, and this can be

determined when it possesses projected accurate product cost. In addition to this, a system of

product costing supports in approximating the concluding cost of materials inventory,

finished goods inventory and work-in-progress inventory for the drive of financial

preparation (Accounting Explained, 2013). The types of costing system are:

Historical Costing – In this, the costs are determined only when they have incurred. The key

purpose of it is to determine costs which had been incurred in past. The historical costs are

utilized for investigation of incurred actual costs and it will be very late to control or manage.

The actual statistics can be associated only when the performance standards exist.

For instance: The Washington Company built a building in 2005, with a cost of $45,000. On

December 31, 2017, the building’s fair market value is $65,000 however still stands on it

original cost of $45,000 on balance sheet.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGEMENT ACCOUNTING 6

Absorption Costing – Under this system, all variable and fixed costs are assigned to the cost

units and entire overheads are engaged as per the level of activity. In this, fixed overheads of

manufacturing are assigned to products, and these are comprised in the valuation of the stock.

Direct Costing – In direct costing, the amount of the product is charged with those costs that

vary in terms of volume. Direct or variable costs such as direct labor, expenses of variable

manufacturing, and the direct material are some of the examples of costs charged to the

product (Aisha, 2018).

Iv Inventory Management Systems

Inventory management system supports business in tracking the goods by the overall supply

chain or the part of its business functions in. That involves every aspect from manufacture to

retail, warehousing to delivery, and all the stock movements (Marder, 2017).

Examples of inventory management system are radio frequency identification, barcode

tracking, and manual inventory (Hamlett, 2018).

v. Job Costing System

The procedure of collecting information of the cost related to a certain production or service

job is known as Job Costing system. This type of information might be needed to submit the

information of cost to the consumer under a contract where costs are repaid (Accounting

Tools, 2018).

For instance: XYZ Corporation starts up Job 1001. In the initial operation month, the job

collects direct material cost of $10,000, direct labor costs of $4,500, and is assigned overhead

expenses of $2,000. Therefore, at the end of the month, the system has accumulated $16,500

total of for Job 1001. This cost is provisionally kept as an inventory asset. XYZ then finishes

Absorption Costing – Under this system, all variable and fixed costs are assigned to the cost

units and entire overheads are engaged as per the level of activity. In this, fixed overheads of

manufacturing are assigned to products, and these are comprised in the valuation of the stock.

Direct Costing – In direct costing, the amount of the product is charged with those costs that

vary in terms of volume. Direct or variable costs such as direct labor, expenses of variable

manufacturing, and the direct material are some of the examples of costs charged to the

product (Aisha, 2018).

Iv Inventory Management Systems

Inventory management system supports business in tracking the goods by the overall supply

chain or the part of its business functions in. That involves every aspect from manufacture to

retail, warehousing to delivery, and all the stock movements (Marder, 2017).

Examples of inventory management system are radio frequency identification, barcode

tracking, and manual inventory (Hamlett, 2018).

v. Job Costing System

The procedure of collecting information of the cost related to a certain production or service

job is known as Job Costing system. This type of information might be needed to submit the

information of cost to the consumer under a contract where costs are repaid (Accounting

Tools, 2018).

For instance: XYZ Corporation starts up Job 1001. In the initial operation month, the job

collects direct material cost of $10,000, direct labor costs of $4,500, and is assigned overhead

expenses of $2,000. Therefore, at the end of the month, the system has accumulated $16,500

total of for Job 1001. This cost is provisionally kept as an inventory asset. XYZ then finishes

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING 7

the job and bills the consumer. At that point of time, the $16,500 is moved out of inventory

and into the COGS.

(b) You then need to present financial information to the management covering:

i. Types of Managerial accounting reports

Reports of Managerial accounting are considered as tools for recognizing what is being done

in the business quantitatively. Additionally, reports of standard accounting that are completed

for the purpose of tax; managerial accounting comprises any accumulation of data that can

provide valuable information about the operations. Whereas reports of standard financial are

arranged to normally accepted principles of accounting, reports of managerial accounting can

be prearranged in any form that makes some logic for the business (Gartenstein, 2018).

Budget report - The budget reports are possibly the most important report in the managerial

accounting. It supports holders of the business to recognize and control costs in the company,

whether it’s a combined organization or has numerous subdivisions. By assessing expenses in

previous years, it becomes conceivable to approximate the budgets for the next years and find

spaces to cut costs.

Account Receivable Aging Report – These types of reports are very vital for all the business

same as for Tech UK Limited that provide credit to customers. It delivers a summary of

credit balances as per age, classically comprising distinct sets for items that are 30, 60, and 90

days late. This can support in adjusting the policies of credit in order to arrange them with

customers’ reimbursement abilities.

Job Cost Report – Job cost report offers a side-by-side vision of the overall cost ensued in a

sole project associated with the predictable revenue produced by that project. This type of

the job and bills the consumer. At that point of time, the $16,500 is moved out of inventory

and into the COGS.

(b) You then need to present financial information to the management covering:

i. Types of Managerial accounting reports

Reports of Managerial accounting are considered as tools for recognizing what is being done

in the business quantitatively. Additionally, reports of standard accounting that are completed

for the purpose of tax; managerial accounting comprises any accumulation of data that can

provide valuable information about the operations. Whereas reports of standard financial are

arranged to normally accepted principles of accounting, reports of managerial accounting can

be prearranged in any form that makes some logic for the business (Gartenstein, 2018).

Budget report - The budget reports are possibly the most important report in the managerial

accounting. It supports holders of the business to recognize and control costs in the company,

whether it’s a combined organization or has numerous subdivisions. By assessing expenses in

previous years, it becomes conceivable to approximate the budgets for the next years and find

spaces to cut costs.

Account Receivable Aging Report – These types of reports are very vital for all the business

same as for Tech UK Limited that provide credit to customers. It delivers a summary of

credit balances as per age, classically comprising distinct sets for items that are 30, 60, and 90

days late. This can support in adjusting the policies of credit in order to arrange them with

customers’ reimbursement abilities.

Job Cost Report – Job cost report offers a side-by-side vision of the overall cost ensued in a

sole project associated with the predictable revenue produced by that project. This type of

MANAGEMENT ACCOUNTING 8

report supports leaders in evaluating the profitability of particular kinds of job and enhances

their processes by concentrating on the jobs that are classically the most lucrative overall.

Manufacturing and Inventory Report - Businesses that create physical products particularly

that part of manufacturing with a low fault lenience consider these reports important. They

support unify data on inventory costs, labor, and other types of overhead comprised in the

procedure of production, offering raw data to enhance machining (Hoddy, 2014).

ii. Importance of presentation of the information in an understandable manner

The owners of the business are the bosses that operate the show. They have reasonable goals

to develop their businesses and increase their profits. They attain their aims by being

innovative, without having fixed hours working, by possessing a vision and by acting on

instinct.

In order to achieve the goals of business Tech, UK Limited owners need a dependable

method to evaluate activity and growth. They have to do comparisons of the performance of

business with preceding periods, with economic yardsticks and with industry. Deprived of

these comparisons and measurements they will not be able to know how well or severely

their business is operating. Besides this, they will not be capable to steer their operations of

the businesses towards the direction of success and achievement of their goals (Constantine

Savva Accountants, 2015).

Task 2

Absorption Costing

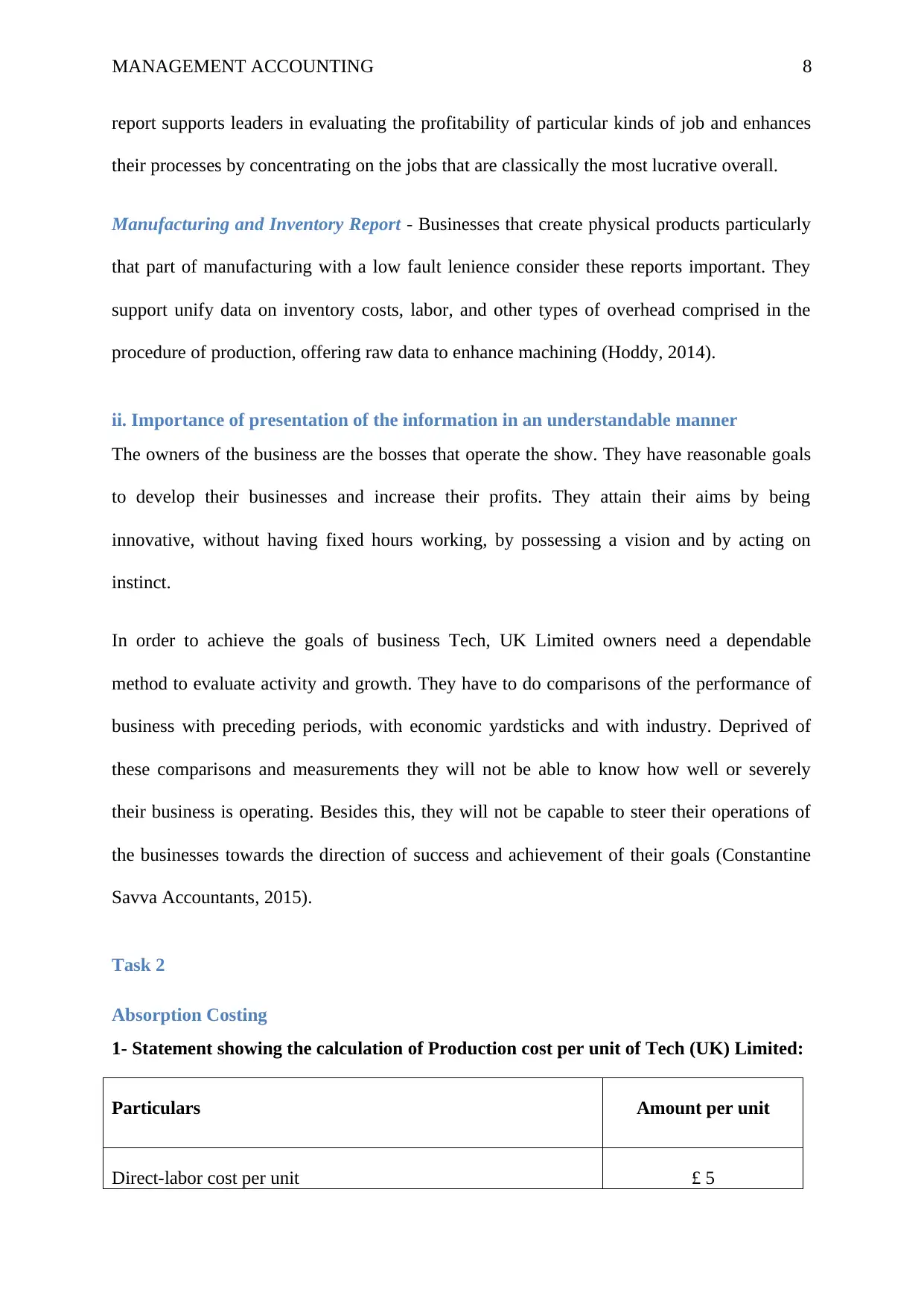

1- Statement showing the calculation of Production cost per unit of Tech (UK) Limited:

Particulars Amount per unit

Direct-labor cost per unit £ 5

report supports leaders in evaluating the profitability of particular kinds of job and enhances

their processes by concentrating on the jobs that are classically the most lucrative overall.

Manufacturing and Inventory Report - Businesses that create physical products particularly

that part of manufacturing with a low fault lenience consider these reports important. They

support unify data on inventory costs, labor, and other types of overhead comprised in the

procedure of production, offering raw data to enhance machining (Hoddy, 2014).

ii. Importance of presentation of the information in an understandable manner

The owners of the business are the bosses that operate the show. They have reasonable goals

to develop their businesses and increase their profits. They attain their aims by being

innovative, without having fixed hours working, by possessing a vision and by acting on

instinct.

In order to achieve the goals of business Tech, UK Limited owners need a dependable

method to evaluate activity and growth. They have to do comparisons of the performance of

business with preceding periods, with economic yardsticks and with industry. Deprived of

these comparisons and measurements they will not be able to know how well or severely

their business is operating. Besides this, they will not be capable to steer their operations of

the businesses towards the direction of success and achievement of their goals (Constantine

Savva Accountants, 2015).

Task 2

Absorption Costing

1- Statement showing the calculation of Production cost per unit of Tech (UK) Limited:

Particulars Amount per unit

Direct-labor cost per unit £ 5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGEMENT ACCOUNTING 9

Direct-material cost per unit £ 8

Variable-production o/h per unit £ 2

Fixed-production o/h incurred in the month £ 15,000

Total-units manufactured in a month 2000 units

Fixed-production o/h per unit [£ 15000 / 2000 units] £ 7.50 per unit

Standard production cost [£ 5 per unit + £ 8 per unit + £ 2 per

unit + £ 7.50 per unit]

£ 22.50 per unit and per

month

2- Calculation of Total Cost of Production of Teck (UK) Limited:

Particulars Amount

Cost of production (Standard) £ 22.50 per unit

Total units produced in a month 2,000 units in a month

Cost of production [2000 units X 22.50 per unit] £ 45,000

3 – Calculation of Total Closing Stock of Teck (UK) Limited:

Particulars Units

Total production in a month 2000 units

Total units sold in a month 1500 units

Direct-material cost per unit £ 8

Variable-production o/h per unit £ 2

Fixed-production o/h incurred in the month £ 15,000

Total-units manufactured in a month 2000 units

Fixed-production o/h per unit [£ 15000 / 2000 units] £ 7.50 per unit

Standard production cost [£ 5 per unit + £ 8 per unit + £ 2 per

unit + £ 7.50 per unit]

£ 22.50 per unit and per

month

2- Calculation of Total Cost of Production of Teck (UK) Limited:

Particulars Amount

Cost of production (Standard) £ 22.50 per unit

Total units produced in a month 2,000 units in a month

Cost of production [2000 units X 22.50 per unit] £ 45,000

3 – Calculation of Total Closing Stock of Teck (UK) Limited:

Particulars Units

Total production in a month 2000 units

Total units sold in a month 1500 units

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING 10

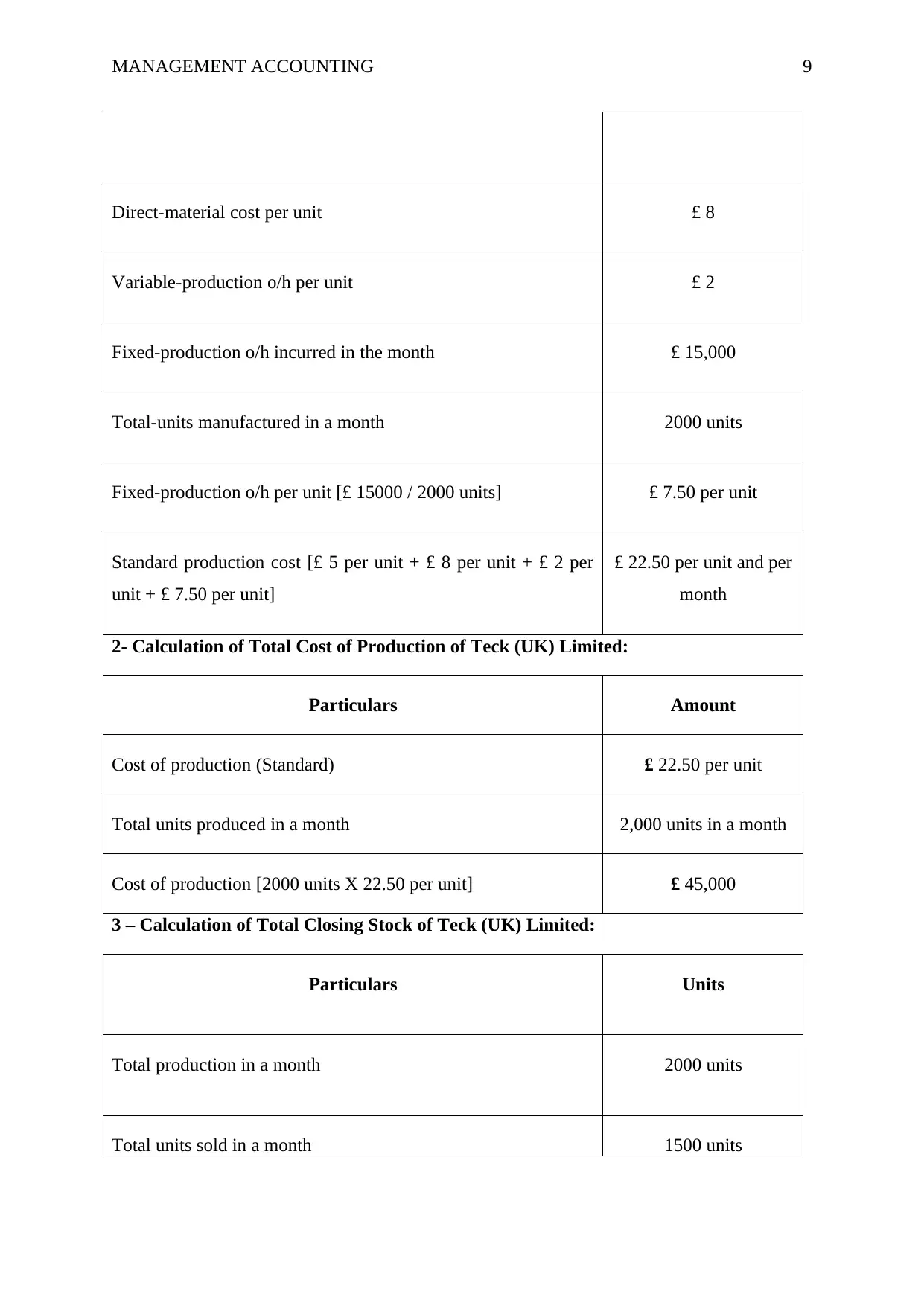

Closing stock [2000 units – 1500 unit] 500 units

Income Statement of Tech (UK) Limited using Absorption Costing

Particulars Amount

Sales [15,000 units x £ 35 per unit] £ 52,500

Cost of goods £ 45, 000

Add: Opening stock Nil

Less: Closing stock [500 units X £ 20 per unit] (10,000)

Gross Profit £ 17,5000

Selling, Distribution, and Administration Expenses

Fixed expenses = £ 10,000

Variable expenses = £ 7, 875 (15 % of £ 52,500)

£ 17,875

Net Loss (£ 375)

Marginal Costing

1- Statement showing the calculation of Production cost per unit of Teck (UK) Limited:

Particulars Amount

Closing stock [2000 units – 1500 unit] 500 units

Income Statement of Tech (UK) Limited using Absorption Costing

Particulars Amount

Sales [15,000 units x £ 35 per unit] £ 52,500

Cost of goods £ 45, 000

Add: Opening stock Nil

Less: Closing stock [500 units X £ 20 per unit] (10,000)

Gross Profit £ 17,5000

Selling, Distribution, and Administration Expenses

Fixed expenses = £ 10,000

Variable expenses = £ 7, 875 (15 % of £ 52,500)

£ 17,875

Net Loss (£ 375)

Marginal Costing

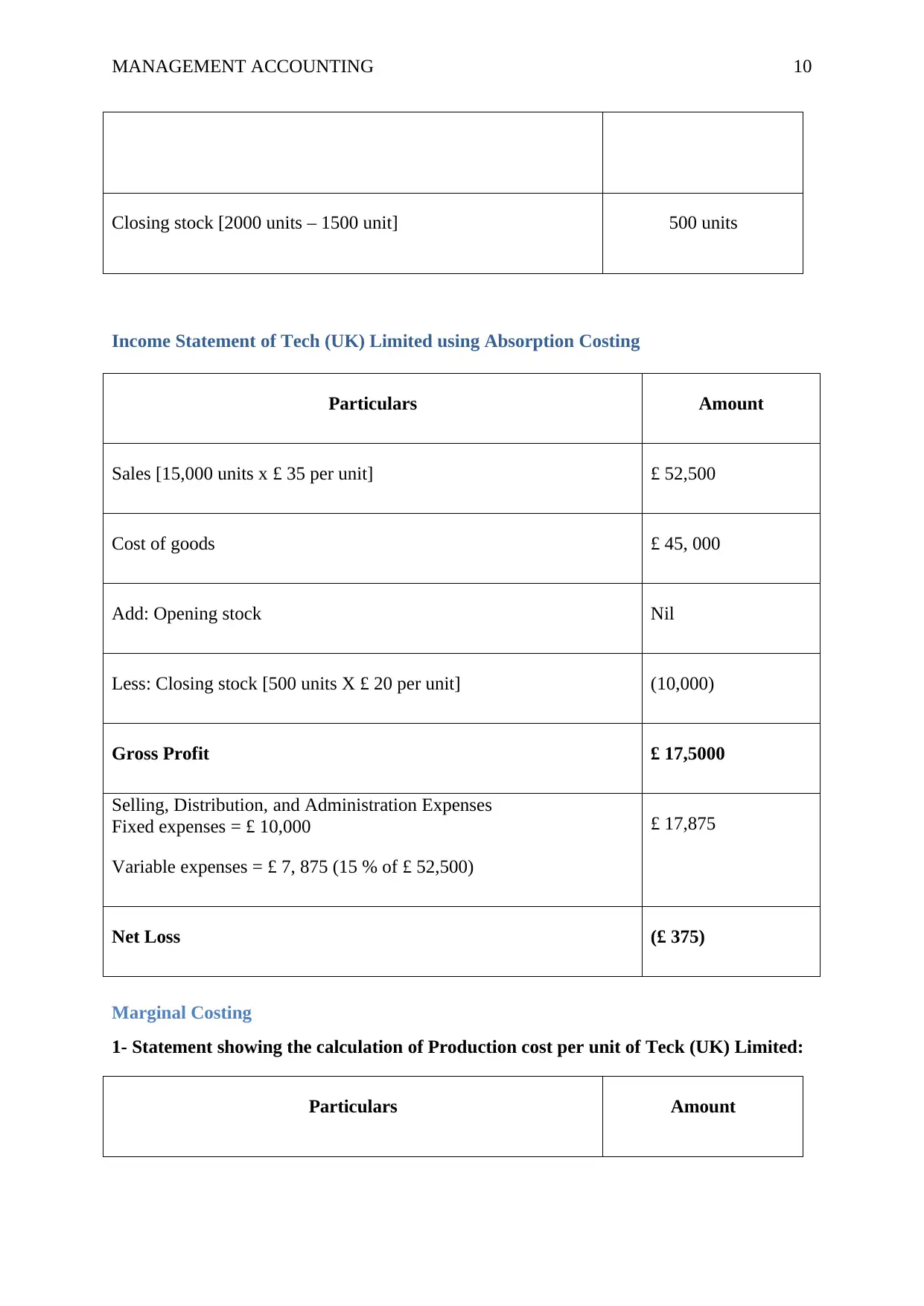

1- Statement showing the calculation of Production cost per unit of Teck (UK) Limited:

Particulars Amount

MANAGEMENT ACCOUNTING 11

Direct-labor cost £ 5 per unit

Direct-material cost £ 8 per unit

Variable-production o/h £ 2 per unit

Total Marginal Cost of Production [5 per unit + 8 per unit + 2

per unit]

£ 15 per unit

Total units produced in a month 2000 units

Total marginal Cost or variable cost of production [2000

units x £ 15]

£ 30,000

Direct-labor cost £ 5 per unit

Direct-material cost £ 8 per unit

Variable-production o/h £ 2 per unit

Total Marginal Cost of Production [5 per unit + 8 per unit + 2

per unit]

£ 15 per unit

Total units produced in a month 2000 units

Total marginal Cost or variable cost of production [2000

units x £ 15]

£ 30,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.