Management Accounting: ABC, Budgeting, Break-Even Analysis, Scorecard

VerifiedAdded on 2022/12/19

|11

|2593

|97

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, including Activity-Based Costing (ABC), budgeting, break-even analysis, and the application of balance scorecards. The report begins by defining ABC, outlining its advantages, and demonstrating its application within Olah Bhd, including cost allocation and the identification of idle capacity. It then evaluates contribution margins, sales levels, and break-even points for a company, incorporating both single and double-shift scenarios, and analyzes sales level units. Furthermore, the report delves into the preparation of budgets for Aliza Ltd across all quarters of 2015, covering sales, production, component, and production cost budgets. It includes detailed calculations and financial analysis, emphasizing the importance of sales forecasting and cost management. Finally, the report examines the implementation of a balance scorecard for a school director, focusing on strategic priorities, financial targets, customer perspectives, internal processes, and organizational capacity to improve teaching techniques and student outcomes. The report concludes with a discussion of the results and recommendations for the director, highlighting the need for a long-term vision and strategic investment.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question 1. define Activity Based Costing for Olah Bhd...........................................................1

Question 2. Evaluate contribution, sales level, break even point................................................2

Question 3. Preparation for budgets for Aliza Ltd for all Quarter of 2015.................................4

Question 4. Balance Scorecard for director of school to set bench-mark...................................6

REFERENCES................................................................................................................................8

Question 1. define Activity Based Costing for Olah Bhd...........................................................1

Question 2. Evaluate contribution, sales level, break even point................................................2

Question 3. Preparation for budgets for Aliza Ltd for all Quarter of 2015.................................4

Question 4. Balance Scorecard for director of school to set bench-mark...................................6

REFERENCES................................................................................................................................8

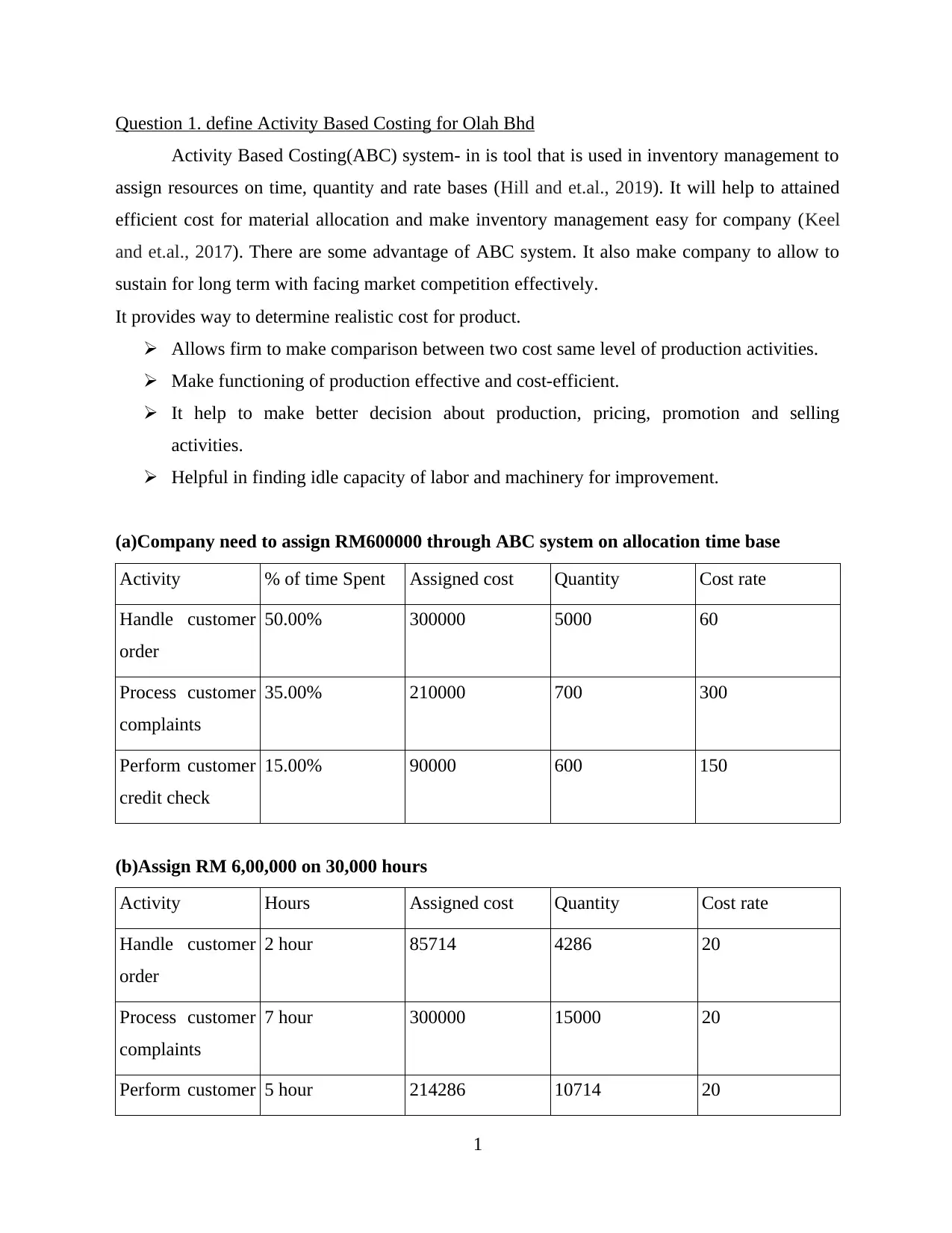

Question 1. define Activity Based Costing for Olah Bhd

Activity Based Costing(ABC) system- in is tool that is used in inventory management to

assign resources on time, quantity and rate bases (Hill and et.al., 2019). It will help to attained

efficient cost for material allocation and make inventory management easy for company (Keel

and et.al., 2017). There are some advantage of ABC system. It also make company to allow to

sustain for long term with facing market competition effectively.

It provides way to determine realistic cost for product.

Allows firm to make comparison between two cost same level of production activities.

Make functioning of production effective and cost-efficient.

It help to make better decision about production, pricing, promotion and selling

activities.

Helpful in finding idle capacity of labor and machinery for improvement.

(a)Company need to assign RM600000 through ABC system on allocation time base

Activity % of time Spent Assigned cost Quantity Cost rate

Handle customer

order

50.00% 300000 5000 60

Process customer

complaints

35.00% 210000 700 300

Perform customer

credit check

15.00% 90000 600 150

(b)Assign RM 6,00,000 on 30,000 hours

Activity Hours Assigned cost Quantity Cost rate

Handle customer

order

2 hour 85714 4286 20

Process customer

complaints

7 hour 300000 15000 20

Perform customer 5 hour 214286 10714 20

1

Activity Based Costing(ABC) system- in is tool that is used in inventory management to

assign resources on time, quantity and rate bases (Hill and et.al., 2019). It will help to attained

efficient cost for material allocation and make inventory management easy for company (Keel

and et.al., 2017). There are some advantage of ABC system. It also make company to allow to

sustain for long term with facing market competition effectively.

It provides way to determine realistic cost for product.

Allows firm to make comparison between two cost same level of production activities.

Make functioning of production effective and cost-efficient.

It help to make better decision about production, pricing, promotion and selling

activities.

Helpful in finding idle capacity of labor and machinery for improvement.

(a)Company need to assign RM600000 through ABC system on allocation time base

Activity % of time Spent Assigned cost Quantity Cost rate

Handle customer

order

50.00% 300000 5000 60

Process customer

complaints

35.00% 210000 700 300

Perform customer

credit check

15.00% 90000 600 150

(b)Assign RM 6,00,000 on 30,000 hours

Activity Hours Assigned cost Quantity Cost rate

Handle customer

order

2 hour 85714 4286 20

Process customer

complaints

7 hour 300000 15000 20

Perform customer 5 hour 214286 10714 20

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

credit check

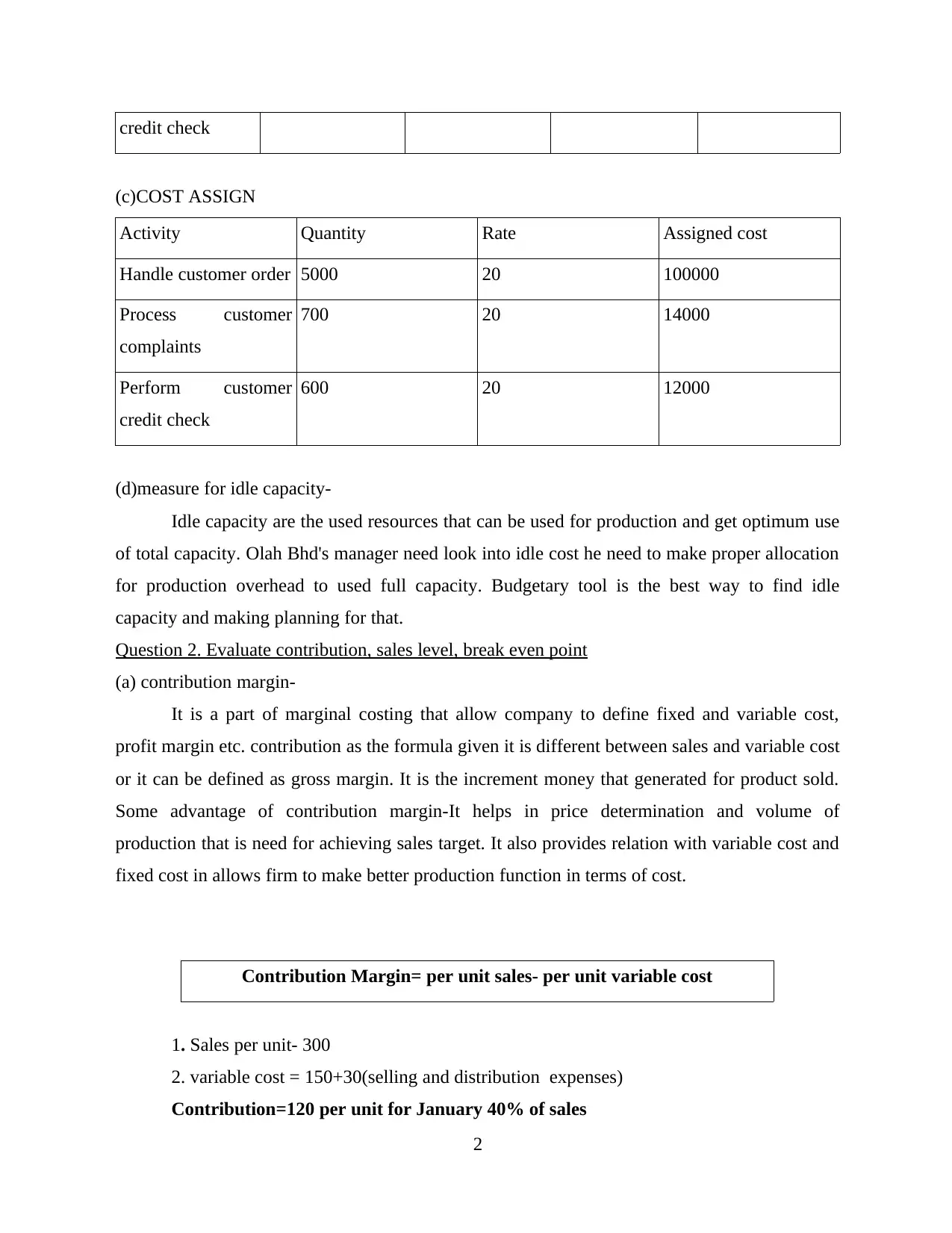

(c)COST ASSIGN

Activity Quantity Rate Assigned cost

Handle customer order 5000 20 100000

Process customer

complaints

700 20 14000

Perform customer

credit check

600 20 12000

(d)measure for idle capacity-

Idle capacity are the used resources that can be used for production and get optimum use

of total capacity. Olah Bhd's manager need look into idle cost he need to make proper allocation

for production overhead to used full capacity. Budgetary tool is the best way to find idle

capacity and making planning for that.

Question 2. Evaluate contribution, sales level, break even point

(a) contribution margin-

It is a part of marginal costing that allow company to define fixed and variable cost,

profit margin etc. contribution as the formula given it is different between sales and variable cost

or it can be defined as gross margin. It is the increment money that generated for product sold.

Some advantage of contribution margin-It helps in price determination and volume of

production that is need for achieving sales target. It also provides relation with variable cost and

fixed cost in allows firm to make better production function in terms of cost.

Contribution Margin= per unit sales- per unit variable cost

1. Sales per unit- 300

2. variable cost = 150+30(selling and distribution expenses)

Contribution=120 per unit for January 40% of sales

2

(c)COST ASSIGN

Activity Quantity Rate Assigned cost

Handle customer order 5000 20 100000

Process customer

complaints

700 20 14000

Perform customer

credit check

600 20 12000

(d)measure for idle capacity-

Idle capacity are the used resources that can be used for production and get optimum use

of total capacity. Olah Bhd's manager need look into idle cost he need to make proper allocation

for production overhead to used full capacity. Budgetary tool is the best way to find idle

capacity and making planning for that.

Question 2. Evaluate contribution, sales level, break even point

(a) contribution margin-

It is a part of marginal costing that allow company to define fixed and variable cost,

profit margin etc. contribution as the formula given it is different between sales and variable cost

or it can be defined as gross margin. It is the increment money that generated for product sold.

Some advantage of contribution margin-It helps in price determination and volume of

production that is need for achieving sales target. It also provides relation with variable cost and

fixed cost in allows firm to make better production function in terms of cost.

Contribution Margin= per unit sales- per unit variable cost

1. Sales per unit- 300

2. variable cost = 150+30(selling and distribution expenses)

Contribution=120 per unit for January 40% of sales

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

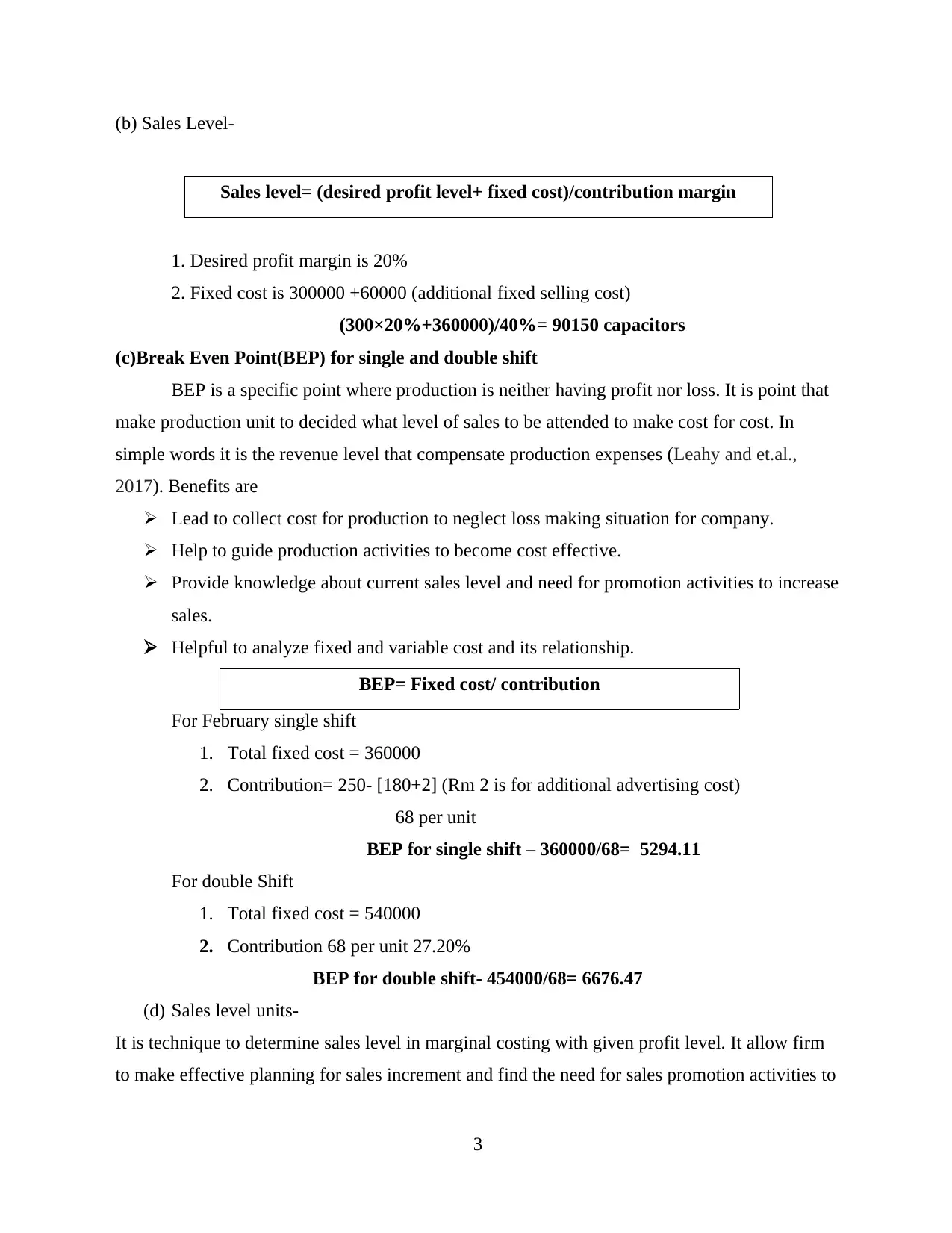

(b) Sales Level-

Sales level= (desired profit level+ fixed cost)/contribution margin

1. Desired profit margin is 20%

2. Fixed cost is 300000 +60000 (additional fixed selling cost)

(300×20%+360000)/40%= 90150 capacitors

(c)Break Even Point(BEP) for single and double shift

BEP is a specific point where production is neither having profit nor loss. It is point that

make production unit to decided what level of sales to be attended to make cost for cost. In

simple words it is the revenue level that compensate production expenses (Leahy and et.al.,

2017). Benefits are

Lead to collect cost for production to neglect loss making situation for company.

Help to guide production activities to become cost effective.

Provide knowledge about current sales level and need for promotion activities to increase

sales.

Helpful to analyze fixed and variable cost and its relationship.

BEP= Fixed cost/ contribution

For February single shift

1. Total fixed cost = 360000

2. Contribution= 250- [180+2] (Rm 2 is for additional advertising cost)

68 per unit

BEP for single shift – 360000/68= 5294.11

For double Shift

1. Total fixed cost = 540000

2. Contribution 68 per unit 27.20%

BEP for double shift- 454000/68= 6676.47

(d) Sales level units-

It is technique to determine sales level in marginal costing with given profit level. It allow firm

to make effective planning for sales increment and find the need for sales promotion activities to

3

Sales level= (desired profit level+ fixed cost)/contribution margin

1. Desired profit margin is 20%

2. Fixed cost is 300000 +60000 (additional fixed selling cost)

(300×20%+360000)/40%= 90150 capacitors

(c)Break Even Point(BEP) for single and double shift

BEP is a specific point where production is neither having profit nor loss. It is point that

make production unit to decided what level of sales to be attended to make cost for cost. In

simple words it is the revenue level that compensate production expenses (Leahy and et.al.,

2017). Benefits are

Lead to collect cost for production to neglect loss making situation for company.

Help to guide production activities to become cost effective.

Provide knowledge about current sales level and need for promotion activities to increase

sales.

Helpful to analyze fixed and variable cost and its relationship.

BEP= Fixed cost/ contribution

For February single shift

1. Total fixed cost = 360000

2. Contribution= 250- [180+2] (Rm 2 is for additional advertising cost)

68 per unit

BEP for single shift – 360000/68= 5294.11

For double Shift

1. Total fixed cost = 540000

2. Contribution 68 per unit 27.20%

BEP for double shift- 454000/68= 6676.47

(d) Sales level units-

It is technique to determine sales level in marginal costing with given profit level. It allow firm

to make effective planning for sales increment and find the need for sales promotion activities to

3

make functioning better and company will not is need to compromise with profit due to less

production.

Sales level= (desired profit level+ fixed cost)/contribution margin

1. Desired profit margin 20% of sales

2. Fixed cost- 454000

(250×20%+454000)/27.2%= 1669301 units

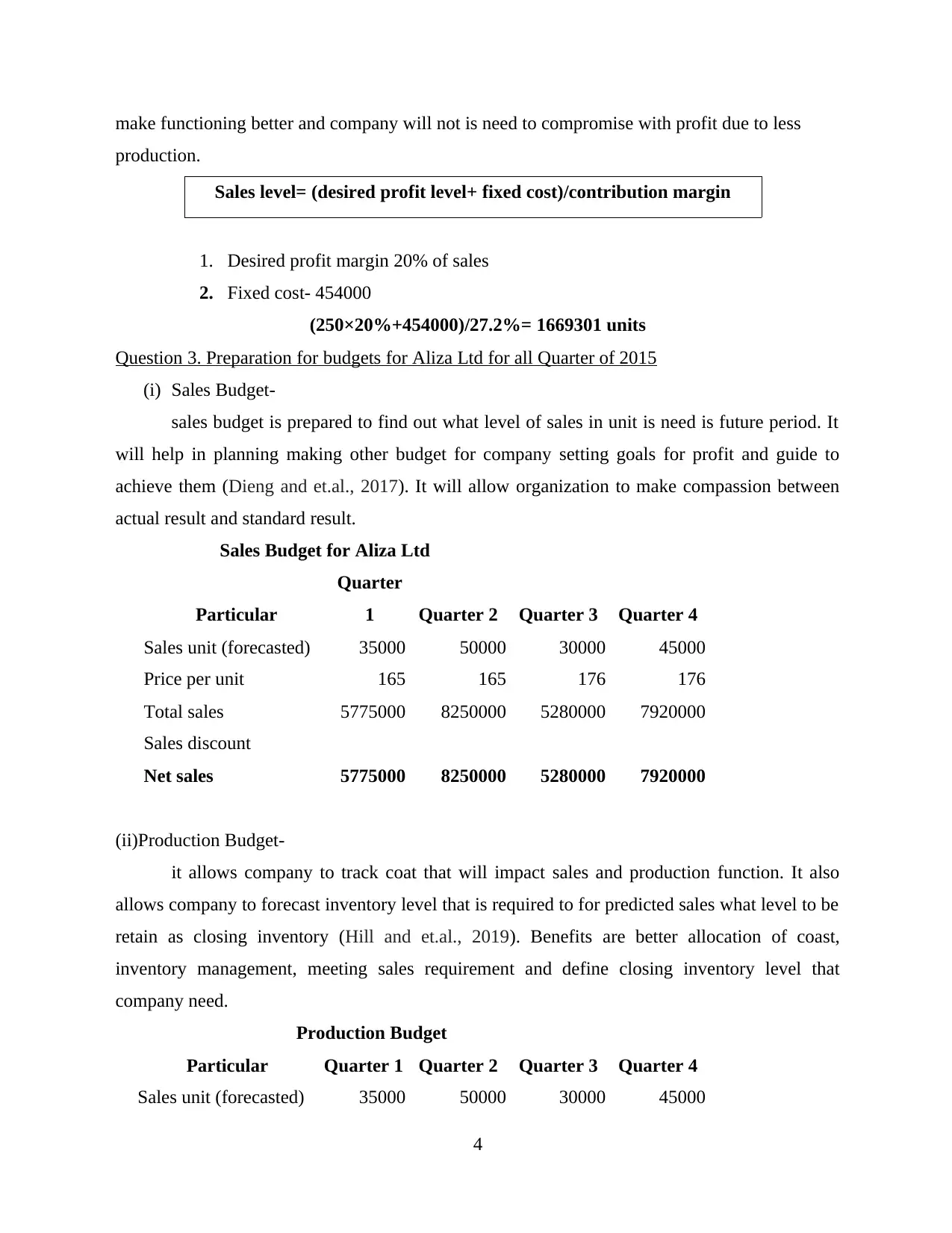

Question 3. Preparation for budgets for Aliza Ltd for all Quarter of 2015

(i) Sales Budget-

sales budget is prepared to find out what level of sales in unit is need is future period. It

will help in planning making other budget for company setting goals for profit and guide to

achieve them (Dieng and et.al., 2017). It will allow organization to make compassion between

actual result and standard result.

Sales Budget for Aliza Ltd

Particular

Quarter

1 Quarter 2 Quarter 3 Quarter 4

Sales unit (forecasted) 35000 50000 30000 45000

Price per unit 165 165 176 176

Total sales 5775000 8250000 5280000 7920000

Sales discount

Net sales 5775000 8250000 5280000 7920000

(ii)Production Budget-

it allows company to track coat that will impact sales and production function. It also

allows company to forecast inventory level that is required to for predicted sales what level to be

retain as closing inventory (Hill and et.al., 2019). Benefits are better allocation of coast,

inventory management, meeting sales requirement and define closing inventory level that

company need.

Production Budget

Particular Quarter 1 Quarter 2 Quarter 3 Quarter 4

Sales unit (forecasted) 35000 50000 30000 45000

4

production.

Sales level= (desired profit level+ fixed cost)/contribution margin

1. Desired profit margin 20% of sales

2. Fixed cost- 454000

(250×20%+454000)/27.2%= 1669301 units

Question 3. Preparation for budgets for Aliza Ltd for all Quarter of 2015

(i) Sales Budget-

sales budget is prepared to find out what level of sales in unit is need is future period. It

will help in planning making other budget for company setting goals for profit and guide to

achieve them (Dieng and et.al., 2017). It will allow organization to make compassion between

actual result and standard result.

Sales Budget for Aliza Ltd

Particular

Quarter

1 Quarter 2 Quarter 3 Quarter 4

Sales unit (forecasted) 35000 50000 30000 45000

Price per unit 165 165 176 176

Total sales 5775000 8250000 5280000 7920000

Sales discount

Net sales 5775000 8250000 5280000 7920000

(ii)Production Budget-

it allows company to track coat that will impact sales and production function. It also

allows company to forecast inventory level that is required to for predicted sales what level to be

retain as closing inventory (Hill and et.al., 2019). Benefits are better allocation of coast,

inventory management, meeting sales requirement and define closing inventory level that

company need.

Production Budget

Particular Quarter 1 Quarter 2 Quarter 3 Quarter 4

Sales unit (forecasted) 35000 50000 30000 45000

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

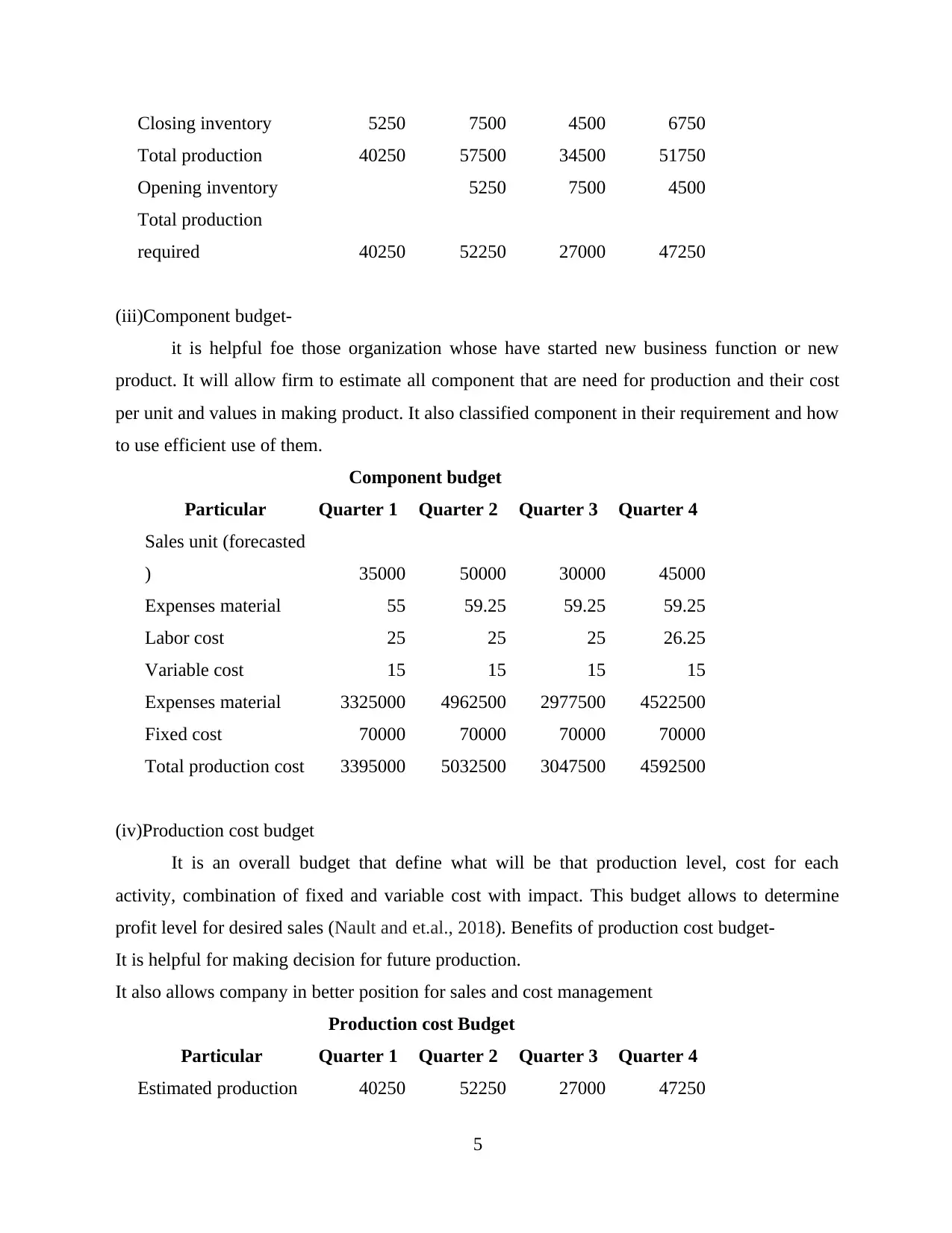

Closing inventory 5250 7500 4500 6750

Total production 40250 57500 34500 51750

Opening inventory 5250 7500 4500

Total production

required 40250 52250 27000 47250

(iii)Component budget-

it is helpful foe those organization whose have started new business function or new

product. It will allow firm to estimate all component that are need for production and their cost

per unit and values in making product. It also classified component in their requirement and how

to use efficient use of them.

Component budget

Particular Quarter 1 Quarter 2 Quarter 3 Quarter 4

Sales unit (forecasted

) 35000 50000 30000 45000

Expenses material 55 59.25 59.25 59.25

Labor cost 25 25 25 26.25

Variable cost 15 15 15 15

Expenses material 3325000 4962500 2977500 4522500

Fixed cost 70000 70000 70000 70000

Total production cost 3395000 5032500 3047500 4592500

(iv)Production cost budget

It is an overall budget that define what will be that production level, cost for each

activity, combination of fixed and variable cost with impact. This budget allows to determine

profit level for desired sales (Nault and et.al., 2018). Benefits of production cost budget-

It is helpful for making decision for future production.

It also allows company in better position for sales and cost management

Production cost Budget

Particular Quarter 1 Quarter 2 Quarter 3 Quarter 4

Estimated production 40250 52250 27000 47250

5

Total production 40250 57500 34500 51750

Opening inventory 5250 7500 4500

Total production

required 40250 52250 27000 47250

(iii)Component budget-

it is helpful foe those organization whose have started new business function or new

product. It will allow firm to estimate all component that are need for production and their cost

per unit and values in making product. It also classified component in their requirement and how

to use efficient use of them.

Component budget

Particular Quarter 1 Quarter 2 Quarter 3 Quarter 4

Sales unit (forecasted

) 35000 50000 30000 45000

Expenses material 55 59.25 59.25 59.25

Labor cost 25 25 25 26.25

Variable cost 15 15 15 15

Expenses material 3325000 4962500 2977500 4522500

Fixed cost 70000 70000 70000 70000

Total production cost 3395000 5032500 3047500 4592500

(iv)Production cost budget

It is an overall budget that define what will be that production level, cost for each

activity, combination of fixed and variable cost with impact. This budget allows to determine

profit level for desired sales (Nault and et.al., 2018). Benefits of production cost budget-

It is helpful for making decision for future production.

It also allows company in better position for sales and cost management

Production cost Budget

Particular Quarter 1 Quarter 2 Quarter 3 Quarter 4

Estimated production 40250 52250 27000 47250

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

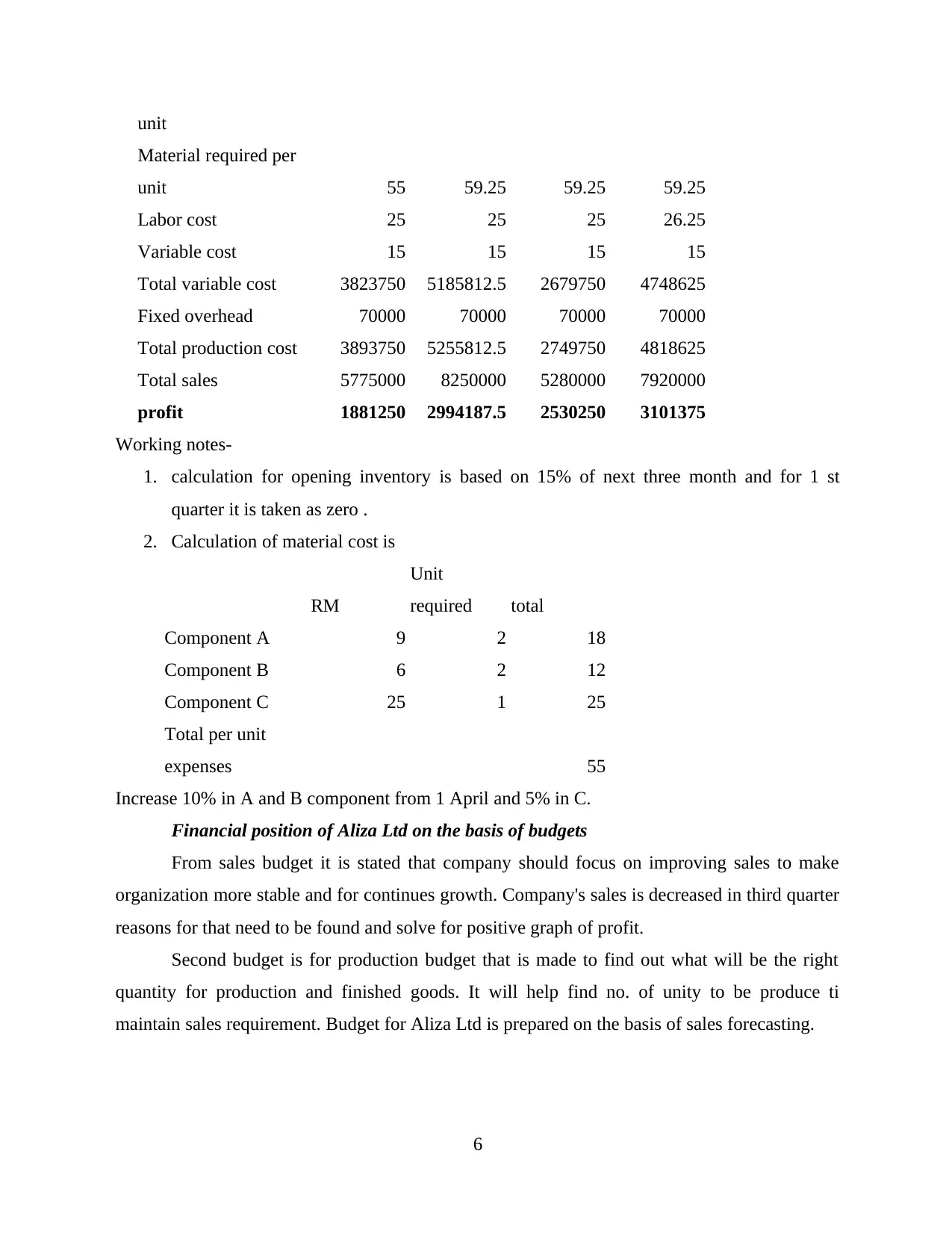

unit

Material required per

unit 55 59.25 59.25 59.25

Labor cost 25 25 25 26.25

Variable cost 15 15 15 15

Total variable cost 3823750 5185812.5 2679750 4748625

Fixed overhead 70000 70000 70000 70000

Total production cost 3893750 5255812.5 2749750 4818625

Total sales 5775000 8250000 5280000 7920000

profit 1881250 2994187.5 2530250 3101375

Working notes-

1. calculation for opening inventory is based on 15% of next three month and for 1 st

quarter it is taken as zero .

2. Calculation of material cost is

RM

Unit

required total

Component A 9 2 18

Component B 6 2 12

Component C 25 1 25

Total per unit

expenses 55

Increase 10% in A and B component from 1 April and 5% in C.

Financial position of Aliza Ltd on the basis of budgets

From sales budget it is stated that company should focus on improving sales to make

organization more stable and for continues growth. Company's sales is decreased in third quarter

reasons for that need to be found and solve for positive graph of profit.

Second budget is for production budget that is made to find out what will be the right

quantity for production and finished goods. It will help find no. of unity to be produce ti

maintain sales requirement. Budget for Aliza Ltd is prepared on the basis of sales forecasting.

6

Material required per

unit 55 59.25 59.25 59.25

Labor cost 25 25 25 26.25

Variable cost 15 15 15 15

Total variable cost 3823750 5185812.5 2679750 4748625

Fixed overhead 70000 70000 70000 70000

Total production cost 3893750 5255812.5 2749750 4818625

Total sales 5775000 8250000 5280000 7920000

profit 1881250 2994187.5 2530250 3101375

Working notes-

1. calculation for opening inventory is based on 15% of next three month and for 1 st

quarter it is taken as zero .

2. Calculation of material cost is

RM

Unit

required total

Component A 9 2 18

Component B 6 2 12

Component C 25 1 25

Total per unit

expenses 55

Increase 10% in A and B component from 1 April and 5% in C.

Financial position of Aliza Ltd on the basis of budgets

From sales budget it is stated that company should focus on improving sales to make

organization more stable and for continues growth. Company's sales is decreased in third quarter

reasons for that need to be found and solve for positive graph of profit.

Second budget is for production budget that is made to find out what will be the right

quantity for production and finished goods. It will help find no. of unity to be produce ti

maintain sales requirement. Budget for Aliza Ltd is prepared on the basis of sales forecasting.

6

Third is Competent budget that is prepared to find out level of material and labor to

optimum production level that help for achieving BEP in less time. It also defines change that

may accrue in production function like increasing prices of material and labor.

Last one is production cost budget that is helpful in defining overall cost of production.

That will make price determination easy and also to fixed profit margin. It shows variable cost

and fixed cost to determine for production it makes cost-effectiveness easy for organization.

Question 4. Balance Scorecard for director of school to set bench-mark

Selected university is “Kuala Lumpur” which is Malaysian university

Vision –To improve Teaching Techniques for better learning

Purpose- Make system to provide knowledge through online mode

Strategic priorities- attraction of students satisfaction Brand Image

Strategic result- increase in no. of students. Student are more satisfied and willing to improve

their knowledge. It leads to make a special Image of school that they are more focused on

effective learning not on increasing no. of students.

Financial this will create special brand image and lead to increase no. of student that

help to collect more fees charge, ultimately overall revenue increase. Target set by school are

50% increase in no. of student and to make get 20% high jump in net profit

Customer- parent/student are the customer that are potential customer for focused. And

more important is to attract student because they will have to make carrier and need to get

effective learning. Target that director has decided to introduce online learning and concept of

less paper study to get attention.

Internal process- for collecting higher attention director has make changes in internally,

for that introducing new learning technique are made, high level of promotion activities, crating

brand image and for cost control some methods are implemented. Director should implement

new software and teacher in favor of better learning.

Organizational Capacity- director need to train teacher for knowledge based study. Use

technologies for attractive study, more case based and practical part rather than book study.

Strategic result-

School are is on the way to desired result, and they started using new teaching techniques that

help them to reach stage where student are more satisfied with learning through online and case

7

optimum production level that help for achieving BEP in less time. It also defines change that

may accrue in production function like increasing prices of material and labor.

Last one is production cost budget that is helpful in defining overall cost of production.

That will make price determination easy and also to fixed profit margin. It shows variable cost

and fixed cost to determine for production it makes cost-effectiveness easy for organization.

Question 4. Balance Scorecard for director of school to set bench-mark

Selected university is “Kuala Lumpur” which is Malaysian university

Vision –To improve Teaching Techniques for better learning

Purpose- Make system to provide knowledge through online mode

Strategic priorities- attraction of students satisfaction Brand Image

Strategic result- increase in no. of students. Student are more satisfied and willing to improve

their knowledge. It leads to make a special Image of school that they are more focused on

effective learning not on increasing no. of students.

Financial this will create special brand image and lead to increase no. of student that

help to collect more fees charge, ultimately overall revenue increase. Target set by school are

50% increase in no. of student and to make get 20% high jump in net profit

Customer- parent/student are the customer that are potential customer for focused. And

more important is to attract student because they will have to make carrier and need to get

effective learning. Target that director has decided to introduce online learning and concept of

less paper study to get attention.

Internal process- for collecting higher attention director has make changes in internally,

for that introducing new learning technique are made, high level of promotion activities, crating

brand image and for cost control some methods are implemented. Director should implement

new software and teacher in favor of better learning.

Organizational Capacity- director need to train teacher for knowledge based study. Use

technologies for attractive study, more case based and practical part rather than book study.

Strategic result-

School are is on the way to desired result, and they started using new teaching techniques that

help them to reach stage where student are more satisfied with learning through online and case

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

studies. School have increased its capacity by almost 30% and retention ration for is also

become more impressive (Kempa and Tutupary, 2020). It has positive impact on overall profit as

increase by 10% this can be better however, school have to make some extra expenses on

facilities of training of teacher and online equipment. This new concept has improved efficiency

level of both teacher and student. Teacher are more focused on practical knowledge and student

are learning with minimum effort.

Director has also able to create school's brand image for providing online learning and case

based studies that help student not only for academic but also in professional carrier. It will lead

school to cut cost for future promotion because, school have created brand value and

student/parent will make mouth publicity.

Director has to have long termed vision for need not worry if short term losses may accrue and

should consider expenses as investment for future earning (Sahrul, Kamase and Tenriwaru,

2021). Moreover, result are attended in first year and think about vision most important think is

that school are not have losses and purpose in fulfilled to make improvement in financial result.

8

become more impressive (Kempa and Tutupary, 2020). It has positive impact on overall profit as

increase by 10% this can be better however, school have to make some extra expenses on

facilities of training of teacher and online equipment. This new concept has improved efficiency

level of both teacher and student. Teacher are more focused on practical knowledge and student

are learning with minimum effort.

Director has also able to create school's brand image for providing online learning and case

based studies that help student not only for academic but also in professional carrier. It will lead

school to cut cost for future promotion because, school have created brand value and

student/parent will make mouth publicity.

Director has to have long termed vision for need not worry if short term losses may accrue and

should consider expenses as investment for future earning (Sahrul, Kamase and Tenriwaru,

2021). Moreover, result are attended in first year and think about vision most important think is

that school are not have losses and purpose in fulfilled to make improvement in financial result.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

de Rubens, G. Z., Noel, L. and Sovacool, B.K., 2018. Dismissive and deceptive car dealerships

create barriers to electric vehicle adoption at the point of sale. Nature Energy. 3(6).

pp.501-507.

Dieng, H. B., and et.al., 2017. New estimate of the current rate of sea level rise from a sea level

budget approach. Geophysical Research Letters. 44(8). pp.3744-3751.

Hill, G., and et.al., 2019. The role of electric vehicles in near-term mitigation pathways and

achieving the UK’s carbon budget. Applied Energy. 251. p.113111.

Keel, G., and et.al., 2017. Time-driven activity-based costing in health care: a systematic review

of the literature. Health Policy. 121(7). pp.755-763.

Kempa, R. and Tutupary, R., 2020. PERFORMANCE ANALYSIS OF 19 AMBON STATE

MIDDLE SCHOOL USING BALANCE SCORECARD APPROACH. EDU SCIENCES

JOURNAL. 1(3). pp.177-187.

Knoblauch, C., and et.al., 2018. Methane production as key to the greenhouse gas budget of

thawing permafrost. Nature Climate Change. 8(4). pp.309-312.

Leahy, M. F., and et.al., 2017. Improved outcomes and reduced costs associated with a health‐

system–wide patient blood management program: a retrospective observational study

in four major adult tertiary‐care hospitals. Transfusion. 57(6). pp.1347-1358.

Nault, B. A., and et.al., 2018. Secondary organic aerosol production from local emissions

dominates the organic aerosol budget over Seoul, South Korea, during KORUS-

AQ. Atmospheric Chemistry and Physics. 18(24). pp.17769-17800.

Sahrul, A. M., Kamase, J. and Tenriwaru, T., 2021. ANALISIS KINERJA MENGGUNAKAN

PENDEKATAN BALANCE SCORECARD PADA PT TELKOMSEL. Jurnal Ilmu

Manajemen Profitability. 5(1). pp.11-20.

Online

Production Budget. 2021. [Online]. Available through:

<https://www.myaccountingcourse.com/accounting-dictionary/production-budget>.

Strategy Focused Schools: An Implementation of the Balanced Scorecard in Provision of

Educational Services. 2021. [Online}. Available

Through:<https://www.sciencedirect.com/science/article/pii/S1877042813049057>

9

Books and Journals

de Rubens, G. Z., Noel, L. and Sovacool, B.K., 2018. Dismissive and deceptive car dealerships

create barriers to electric vehicle adoption at the point of sale. Nature Energy. 3(6).

pp.501-507.

Dieng, H. B., and et.al., 2017. New estimate of the current rate of sea level rise from a sea level

budget approach. Geophysical Research Letters. 44(8). pp.3744-3751.

Hill, G., and et.al., 2019. The role of electric vehicles in near-term mitigation pathways and

achieving the UK’s carbon budget. Applied Energy. 251. p.113111.

Keel, G., and et.al., 2017. Time-driven activity-based costing in health care: a systematic review

of the literature. Health Policy. 121(7). pp.755-763.

Kempa, R. and Tutupary, R., 2020. PERFORMANCE ANALYSIS OF 19 AMBON STATE

MIDDLE SCHOOL USING BALANCE SCORECARD APPROACH. EDU SCIENCES

JOURNAL. 1(3). pp.177-187.

Knoblauch, C., and et.al., 2018. Methane production as key to the greenhouse gas budget of

thawing permafrost. Nature Climate Change. 8(4). pp.309-312.

Leahy, M. F., and et.al., 2017. Improved outcomes and reduced costs associated with a health‐

system–wide patient blood management program: a retrospective observational study

in four major adult tertiary‐care hospitals. Transfusion. 57(6). pp.1347-1358.

Nault, B. A., and et.al., 2018. Secondary organic aerosol production from local emissions

dominates the organic aerosol budget over Seoul, South Korea, during KORUS-

AQ. Atmospheric Chemistry and Physics. 18(24). pp.17769-17800.

Sahrul, A. M., Kamase, J. and Tenriwaru, T., 2021. ANALISIS KINERJA MENGGUNAKAN

PENDEKATAN BALANCE SCORECARD PADA PT TELKOMSEL. Jurnal Ilmu

Manajemen Profitability. 5(1). pp.11-20.

Online

Production Budget. 2021. [Online]. Available through:

<https://www.myaccountingcourse.com/accounting-dictionary/production-budget>.

Strategy Focused Schools: An Implementation of the Balanced Scorecard in Provision of

Educational Services. 2021. [Online}. Available

Through:<https://www.sciencedirect.com/science/article/pii/S1877042813049057>

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.