University Management Accounting Report: Pricing Strategies Analysis

VerifiedAdded on 2021/05/31

|9

|849

|127

Report

AI Summary

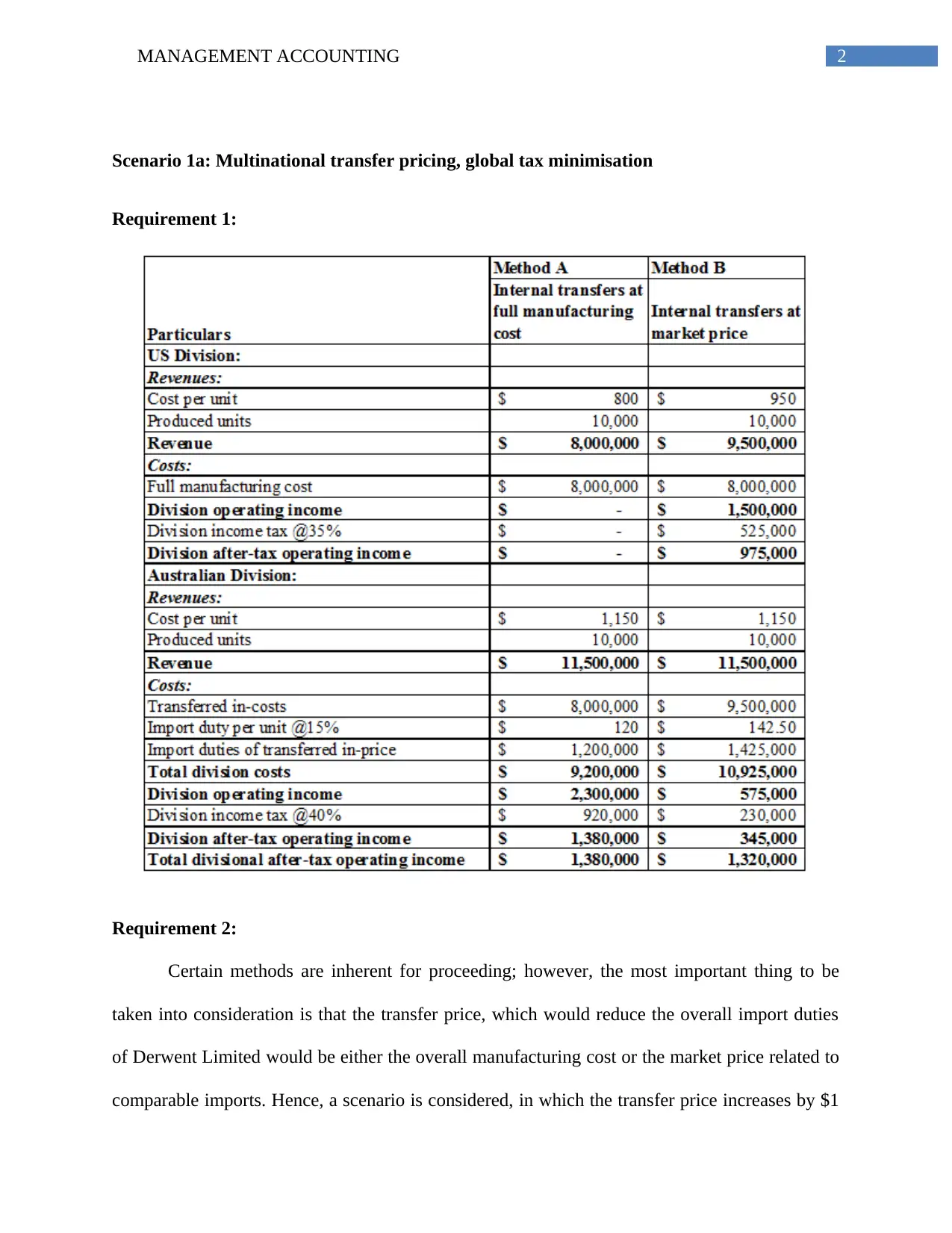

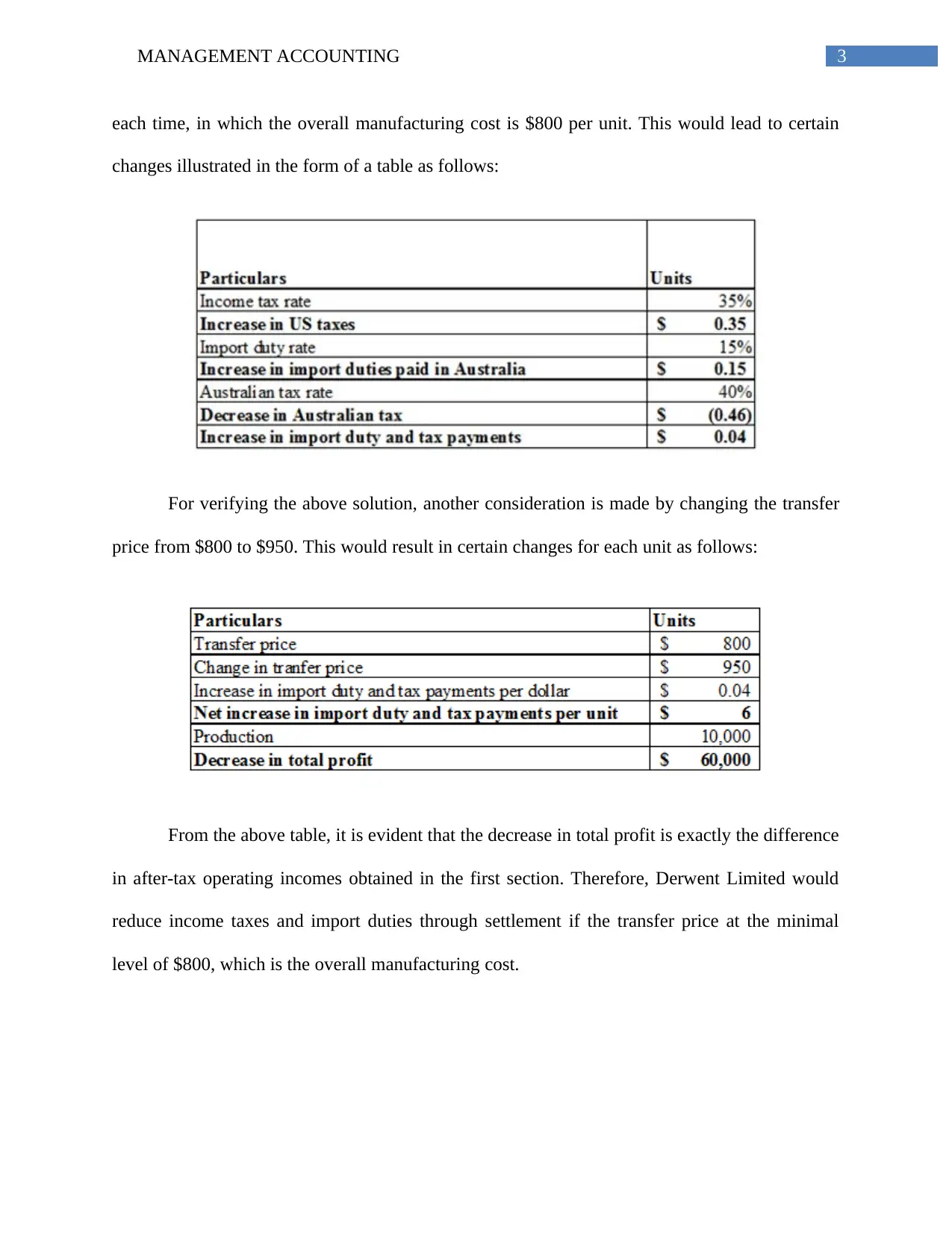

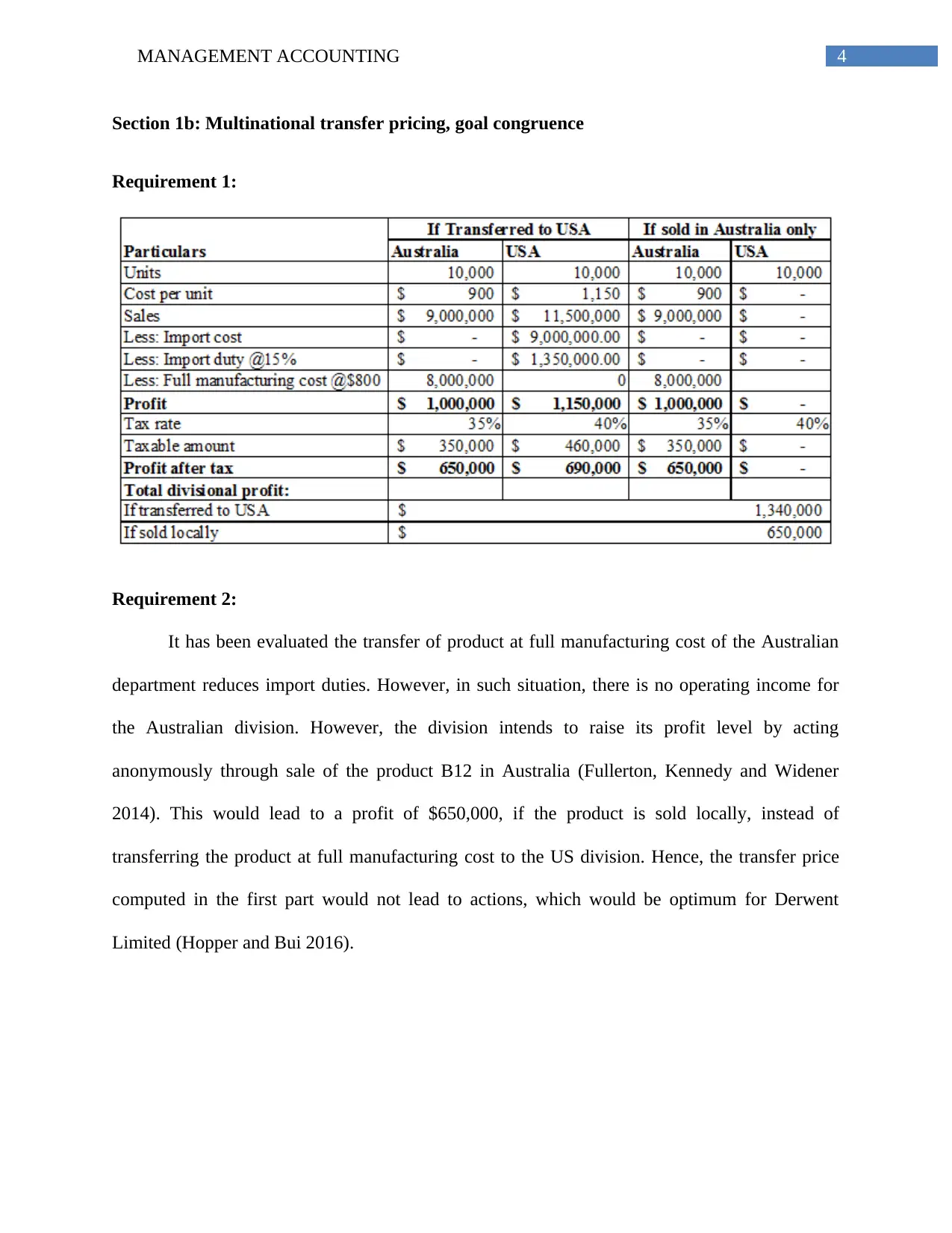

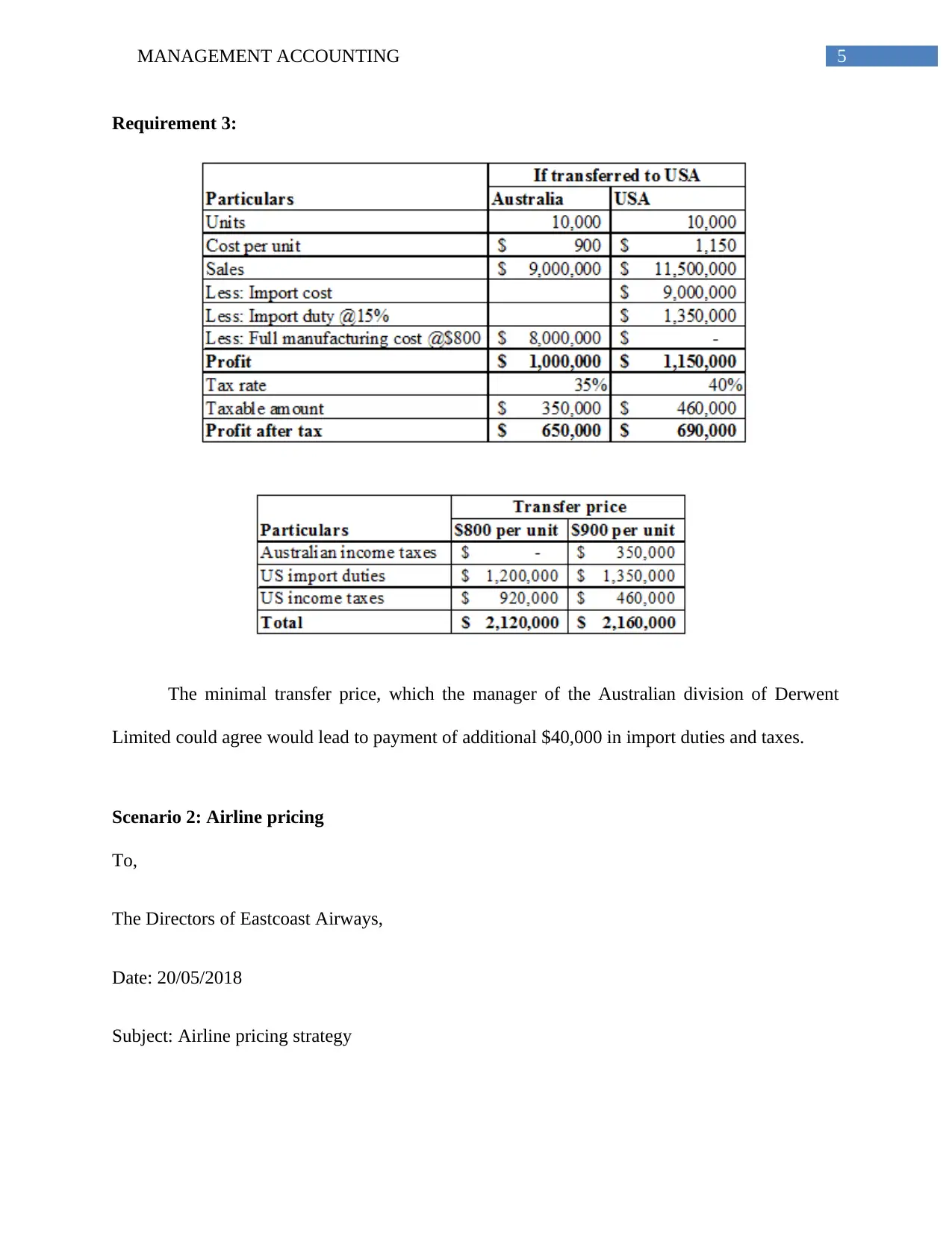

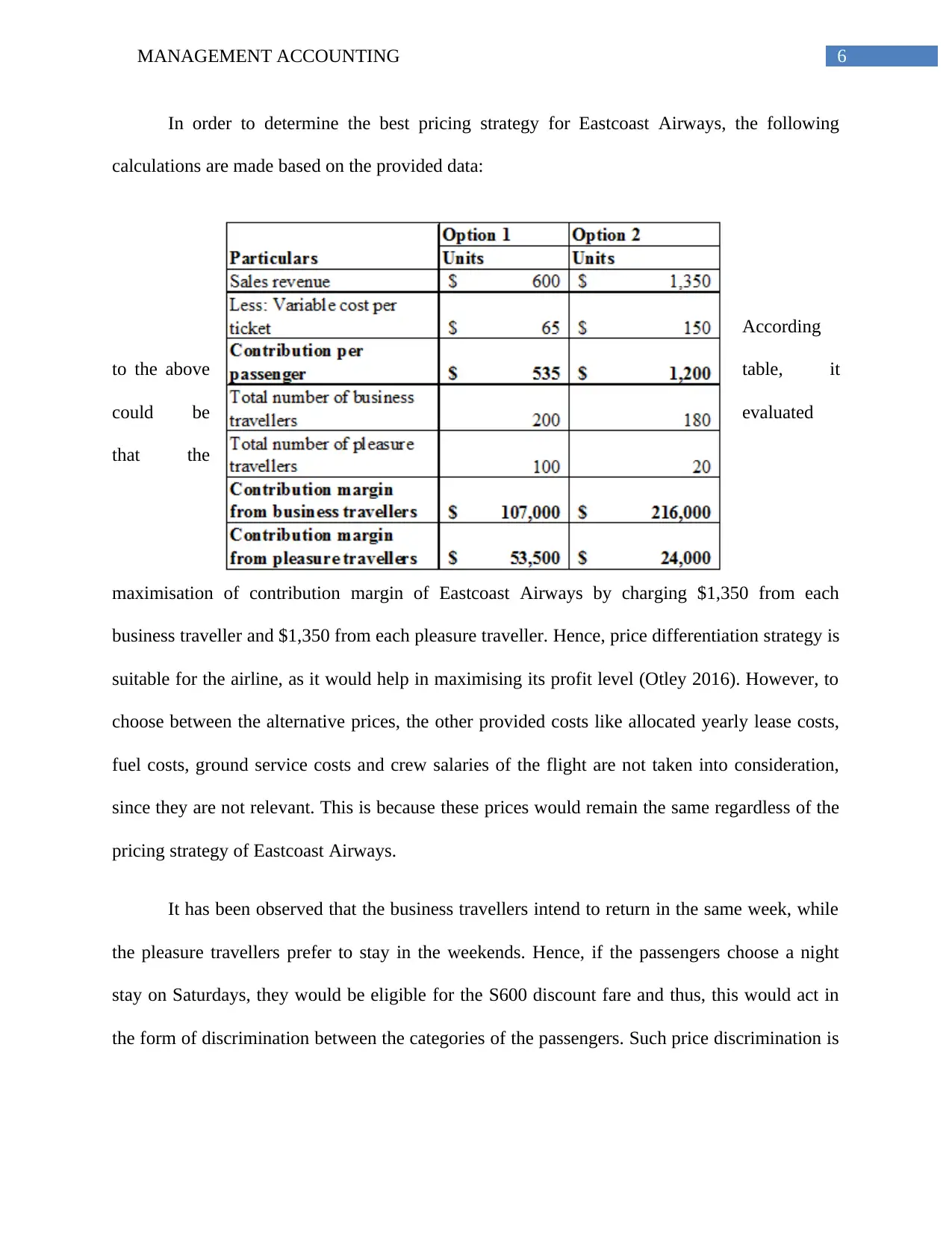

This management accounting report analyzes two key scenarios: multinational transfer pricing and airline pricing. The first scenario explores how Derwent Limited can minimize import duties and income taxes through strategic transfer pricing, considering manufacturing costs and market prices. The analysis includes a table illustrating the impact of different transfer prices on profit and tax liabilities. The second scenario focuses on Eastcoast Airways, evaluating optimal pricing strategies for business and pleasure travelers to maximize contribution margin. The report recommends a price differentiation strategy and discusses the legality of such practices, while excluding irrelevant costs like allocated yearly lease costs and fuel costs. The report references several academic sources to support its findings.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.