Management Accounting Report for Cool Destinations: ACC202 Analysis

VerifiedAdded on 2022/11/14

|15

|2543

|226

Report

AI Summary

This management accounting report analyzes Cool Destinations' financial performance, focusing on profitability, cost analysis, and strategic recommendations. The report begins with an executive summary and table of contents, followed by detailed answers to eight questions. Question 1 examines cost per unit, cost per day, and profitability. Question 2 delves into profitability ratios and hybrid costing systems. Question 3 defines hybrid costing. Question 4 analyzes meal costs. Question 5 discusses cost estimation and pricing strategies. Question 6 calculates profit or loss for tours. Question 7 provides recommendations to improve profitability. Question 8 explores strategic variables. The report concludes with a discussion of key findings and recommendations for Cool Destinations to improve its financial performance. The report uses financial data to provide an in-depth analysis of the company's operations. It examines various cost elements, revenue streams, and profitability measures to assess the company's overall financial health and provide insights for strategic decision-making. The report also analyzes the company's tour operations, including costing, pricing, and profitability analysis, to identify areas for improvement and provide recommendations for enhancing the company's financial performance.

Running Head: MANAGEMENT ACOCUNTING

MANAGEMENT ACCOUNTING

MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: MANAGEMENT ACOCUNTING

Executive summary

Management accounting is the process which is used to identify, analyzing recording and

presenting the financial information in order to take the management decisions for future

possibility. The accounts share a detailed overview of how the company like Cool Destinations is

spending on its operations and business and how the cash flow level is in terms of debts and

assets. In order to bring the organization in its top most capacity, the profitability of the company

has been assessed and Snowy Mountains turns out to be the profitable (Giannetti, Magnacca and

Mariani, 2018).

Executive summary

Management accounting is the process which is used to identify, analyzing recording and

presenting the financial information in order to take the management decisions for future

possibility. The accounts share a detailed overview of how the company like Cool Destinations is

spending on its operations and business and how the cash flow level is in terms of debts and

assets. In order to bring the organization in its top most capacity, the profitability of the company

has been assessed and Snowy Mountains turns out to be the profitable (Giannetti, Magnacca and

Mariani, 2018).

Running Head: MANAGEMENT ACOCUNTING

Table of Contents

Executive summary.....................................................................................................................................2

Question 1...................................................................................................................................................4

Question 2...................................................................................................................................................7

Question 3...................................................................................................................................................8

Question 4...................................................................................................................................................9

Question 5.................................................................................................................................................10

Question 6.................................................................................................................................................11

Question 7.................................................................................................................................................12

Question 8.................................................................................................................................................13

Recommendations.....................................................................................................................................13

Conclusion.................................................................................................................................................13

References.................................................................................................................................................14

Table of Contents

Executive summary.....................................................................................................................................2

Question 1...................................................................................................................................................4

Question 2...................................................................................................................................................7

Question 3...................................................................................................................................................8

Question 4...................................................................................................................................................9

Question 5.................................................................................................................................................10

Question 6.................................................................................................................................................11

Question 7.................................................................................................................................................12

Question 8.................................................................................................................................................13

Recommendations.....................................................................................................................................13

Conclusion.................................................................................................................................................13

References.................................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: MANAGEMENT ACOCUNTING

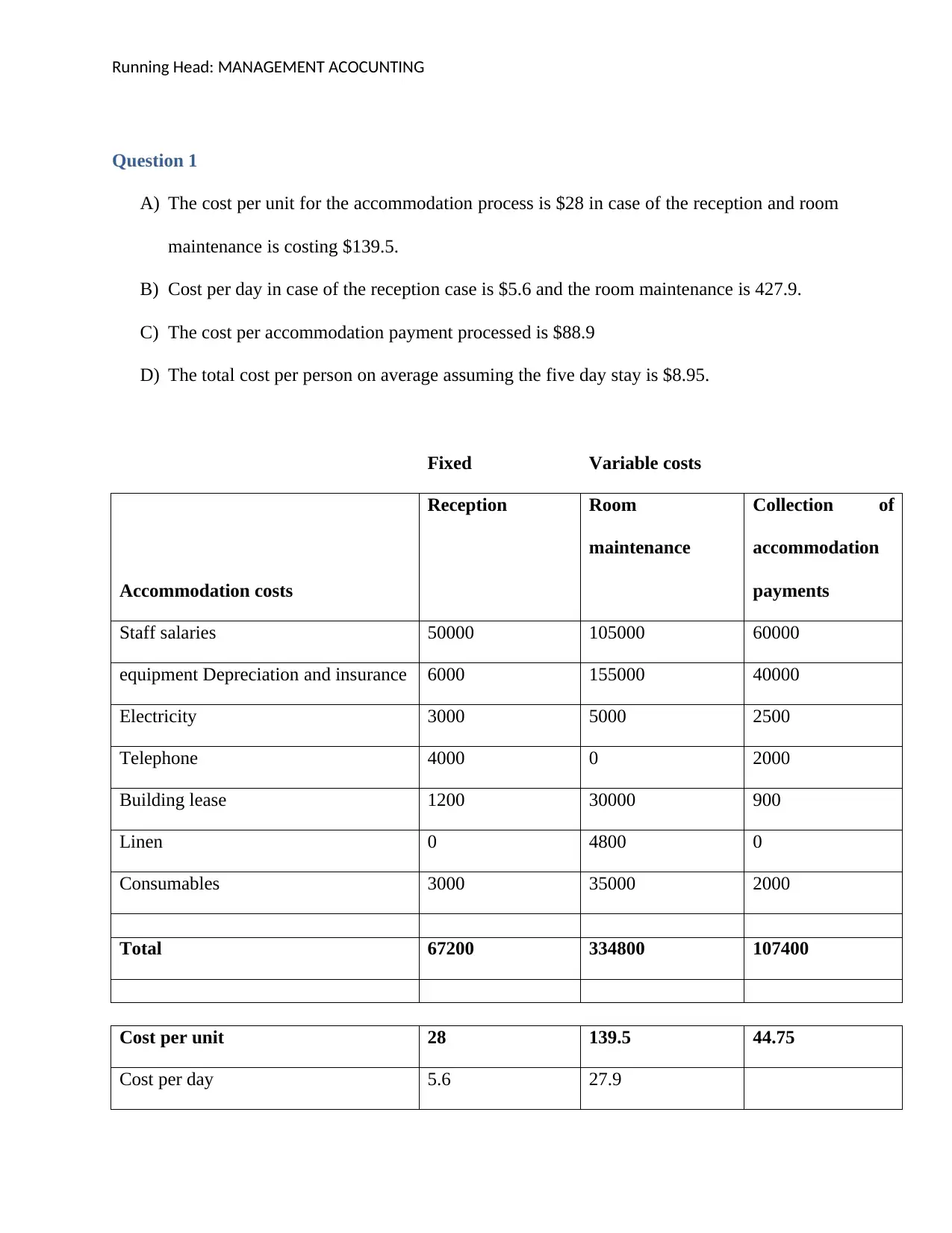

Question 1

A) The cost per unit for the accommodation process is $28 in case of the reception and room

maintenance is costing $139.5.

B) Cost per day in case of the reception case is $5.6 and the room maintenance is 427.9.

C) The cost per accommodation payment processed is $88.9

D) The total cost per person on average assuming the five day stay is $8.95.

Fixed Variable costs

Accommodation costs

Reception Room

maintenance

Collection of

accommodation

payments

Staff salaries 50000 105000 60000

equipment Depreciation and insurance 6000 155000 40000

Electricity 3000 5000 2500

Telephone 4000 0 2000

Building lease 1200 30000 900

Linen 0 4800 0

Consumables 3000 35000 2000

Total 67200 334800 107400

Cost per unit 28 139.5 44.75

Cost per day 5.6 27.9

Question 1

A) The cost per unit for the accommodation process is $28 in case of the reception and room

maintenance is costing $139.5.

B) Cost per day in case of the reception case is $5.6 and the room maintenance is 427.9.

C) The cost per accommodation payment processed is $88.9

D) The total cost per person on average assuming the five day stay is $8.95.

Fixed Variable costs

Accommodation costs

Reception Room

maintenance

Collection of

accommodation

payments

Staff salaries 50000 105000 60000

equipment Depreciation and insurance 6000 155000 40000

Electricity 3000 5000 2500

Telephone 4000 0 2000

Building lease 1200 30000 900

Linen 0 4800 0

Consumables 3000 35000 2000

Total 67200 334800 107400

Cost per unit 28 139.5 44.75

Cost per day 5.6 27.9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: MANAGEMENT ACOCUNTING

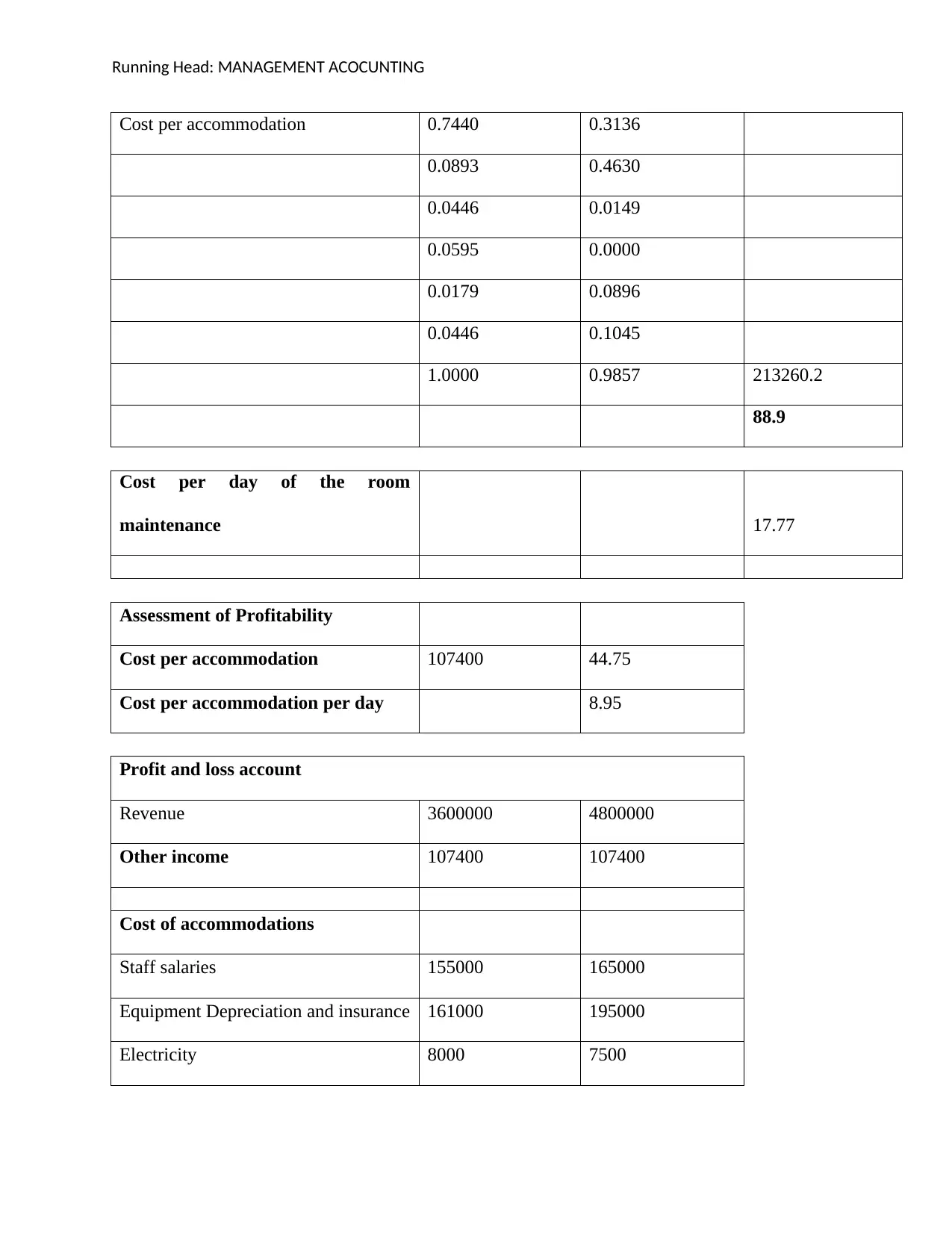

Cost per accommodation 0.7440 0.3136

0.0893 0.4630

0.0446 0.0149

0.0595 0.0000

0.0179 0.0896

0.0446 0.1045

1.0000 0.9857 213260.2

88.9

Cost per day of the room

maintenance 17.77

Assessment of Profitability

Cost per accommodation 107400 44.75

Cost per accommodation per day 8.95

Profit and loss account

Revenue 3600000 4800000

Other income 107400 107400

Cost of accommodations

Staff salaries 155000 165000

Equipment Depreciation and insurance 161000 195000

Electricity 8000 7500

Cost per accommodation 0.7440 0.3136

0.0893 0.4630

0.0446 0.0149

0.0595 0.0000

0.0179 0.0896

0.0446 0.1045

1.0000 0.9857 213260.2

88.9

Cost per day of the room

maintenance 17.77

Assessment of Profitability

Cost per accommodation 107400 44.75

Cost per accommodation per day 8.95

Profit and loss account

Revenue 3600000 4800000

Other income 107400 107400

Cost of accommodations

Staff salaries 155000 165000

Equipment Depreciation and insurance 161000 195000

Electricity 8000 7500

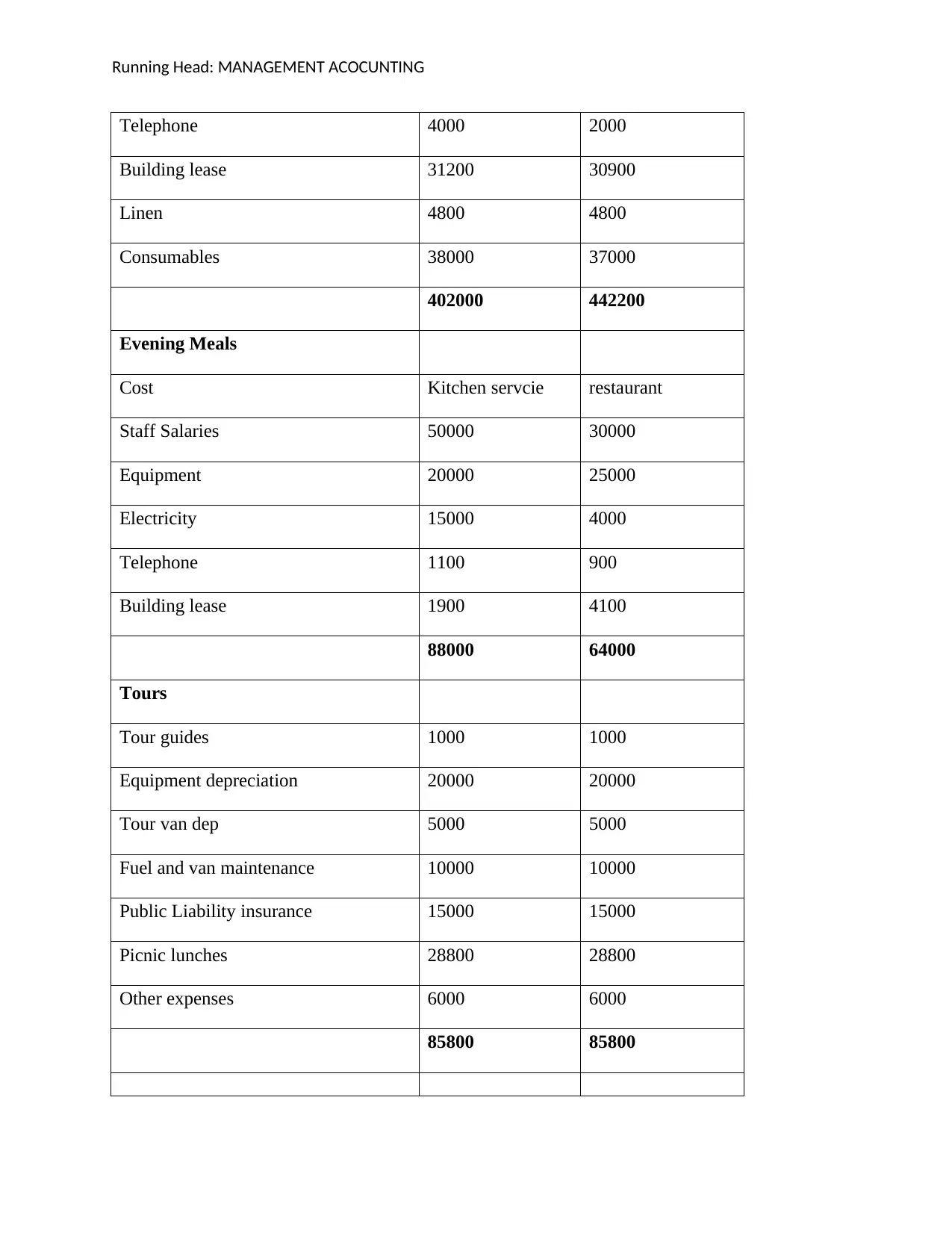

Running Head: MANAGEMENT ACOCUNTING

Telephone 4000 2000

Building lease 31200 30900

Linen 4800 4800

Consumables 38000 37000

402000 442200

Evening Meals

Cost Kitchen servcie restaurant

Staff Salaries 50000 30000

Equipment 20000 25000

Electricity 15000 4000

Telephone 1100 900

Building lease 1900 4100

88000 64000

Tours

Tour guides 1000 1000

Equipment depreciation 20000 20000

Tour van dep 5000 5000

Fuel and van maintenance 10000 10000

Public Liability insurance 15000 15000

Picnic lunches 28800 28800

Other expenses 6000 6000

85800 85800

Telephone 4000 2000

Building lease 31200 30900

Linen 4800 4800

Consumables 38000 37000

402000 442200

Evening Meals

Cost Kitchen servcie restaurant

Staff Salaries 50000 30000

Equipment 20000 25000

Electricity 15000 4000

Telephone 1100 900

Building lease 1900 4100

88000 64000

Tours

Tour guides 1000 1000

Equipment depreciation 20000 20000

Tour van dep 5000 5000

Fuel and van maintenance 10000 10000

Public Liability insurance 15000 15000

Picnic lunches 28800 28800

Other expenses 6000 6000

85800 85800

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: MANAGEMENT ACOCUNTING

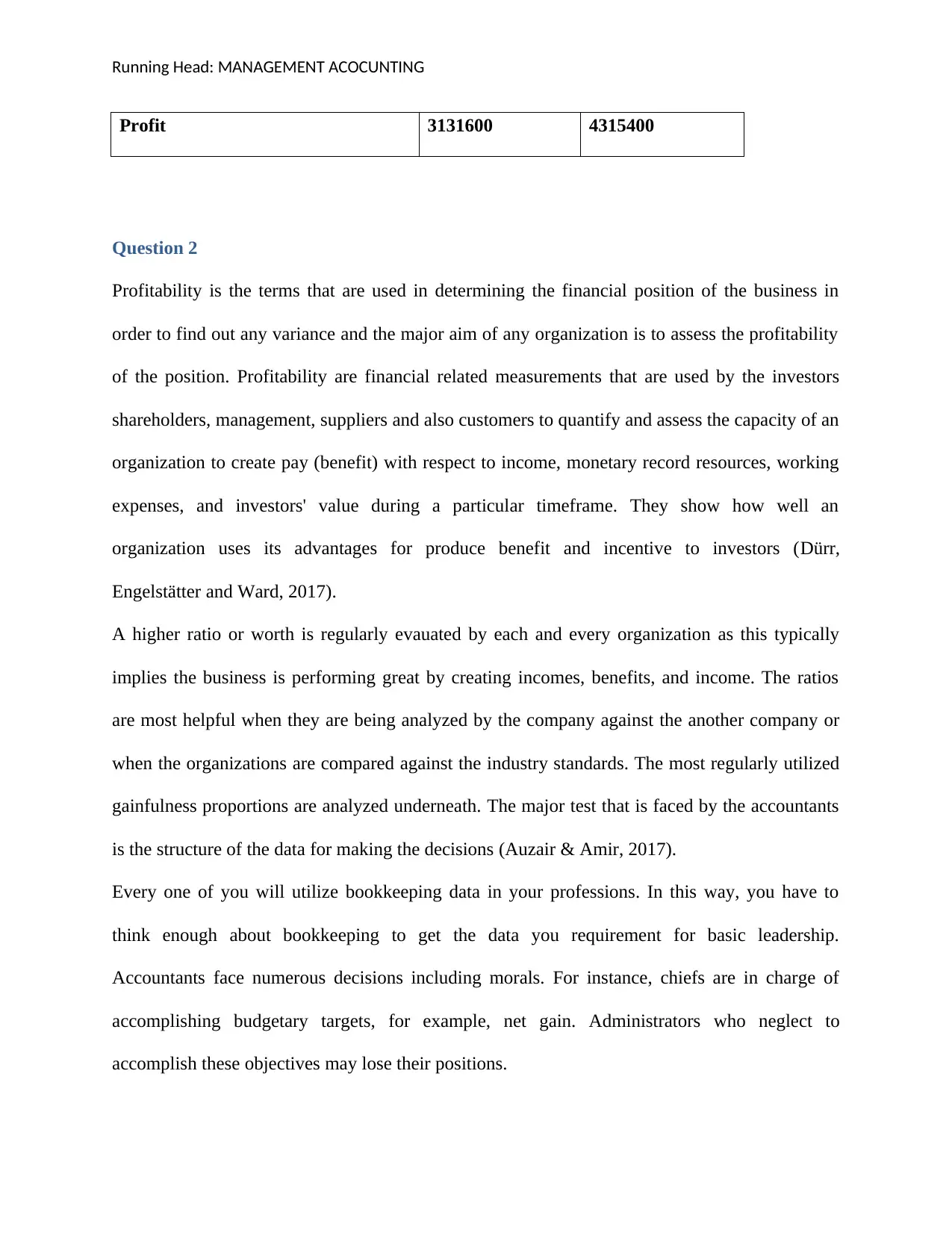

Profit 3131600 4315400

Question 2

Profitability is the terms that are used in determining the financial position of the business in

order to find out any variance and the major aim of any organization is to assess the profitability

of the position. Profitability are financial related measurements that are used by the investors

shareholders, management, suppliers and also customers to quantify and assess the capacity of an

organization to create pay (benefit) with respect to income, monetary record resources, working

expenses, and investors' value during a particular timeframe. They show how well an

organization uses its advantages for produce benefit and incentive to investors (Dürr,

Engelstätter and Ward, 2017).

A higher ratio or worth is regularly evauated by each and every organization as this typically

implies the business is performing great by creating incomes, benefits, and income. The ratios

are most helpful when they are being analyzed by the company against the another company or

when the organizations are compared against the industry standards. The most regularly utilized

gainfulness proportions are analyzed underneath. The major test that is faced by the accountants

is the structure of the data for making the decisions (Auzair & Amir, 2017).

Every one of you will utilize bookkeeping data in your professions. In this way, you have to

think enough about bookkeeping to get the data you requirement for basic leadership.

Accountants face numerous decisions including morals. For instance, chiefs are in charge of

accomplishing budgetary targets, for example, net gain. Administrators who neglect to

accomplish these objectives may lose their positions.

Profit 3131600 4315400

Question 2

Profitability is the terms that are used in determining the financial position of the business in

order to find out any variance and the major aim of any organization is to assess the profitability

of the position. Profitability are financial related measurements that are used by the investors

shareholders, management, suppliers and also customers to quantify and assess the capacity of an

organization to create pay (benefit) with respect to income, monetary record resources, working

expenses, and investors' value during a particular timeframe. They show how well an

organization uses its advantages for produce benefit and incentive to investors (Dürr,

Engelstätter and Ward, 2017).

A higher ratio or worth is regularly evauated by each and every organization as this typically

implies the business is performing great by creating incomes, benefits, and income. The ratios

are most helpful when they are being analyzed by the company against the another company or

when the organizations are compared against the industry standards. The most regularly utilized

gainfulness proportions are analyzed underneath. The major test that is faced by the accountants

is the structure of the data for making the decisions (Auzair & Amir, 2017).

Every one of you will utilize bookkeeping data in your professions. In this way, you have to

think enough about bookkeeping to get the data you requirement for basic leadership.

Accountants face numerous decisions including morals. For instance, chiefs are in charge of

accomplishing budgetary targets, for example, net gain. Administrators who neglect to

accomplish these objectives may lose their positions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: MANAGEMENT ACOCUNTING

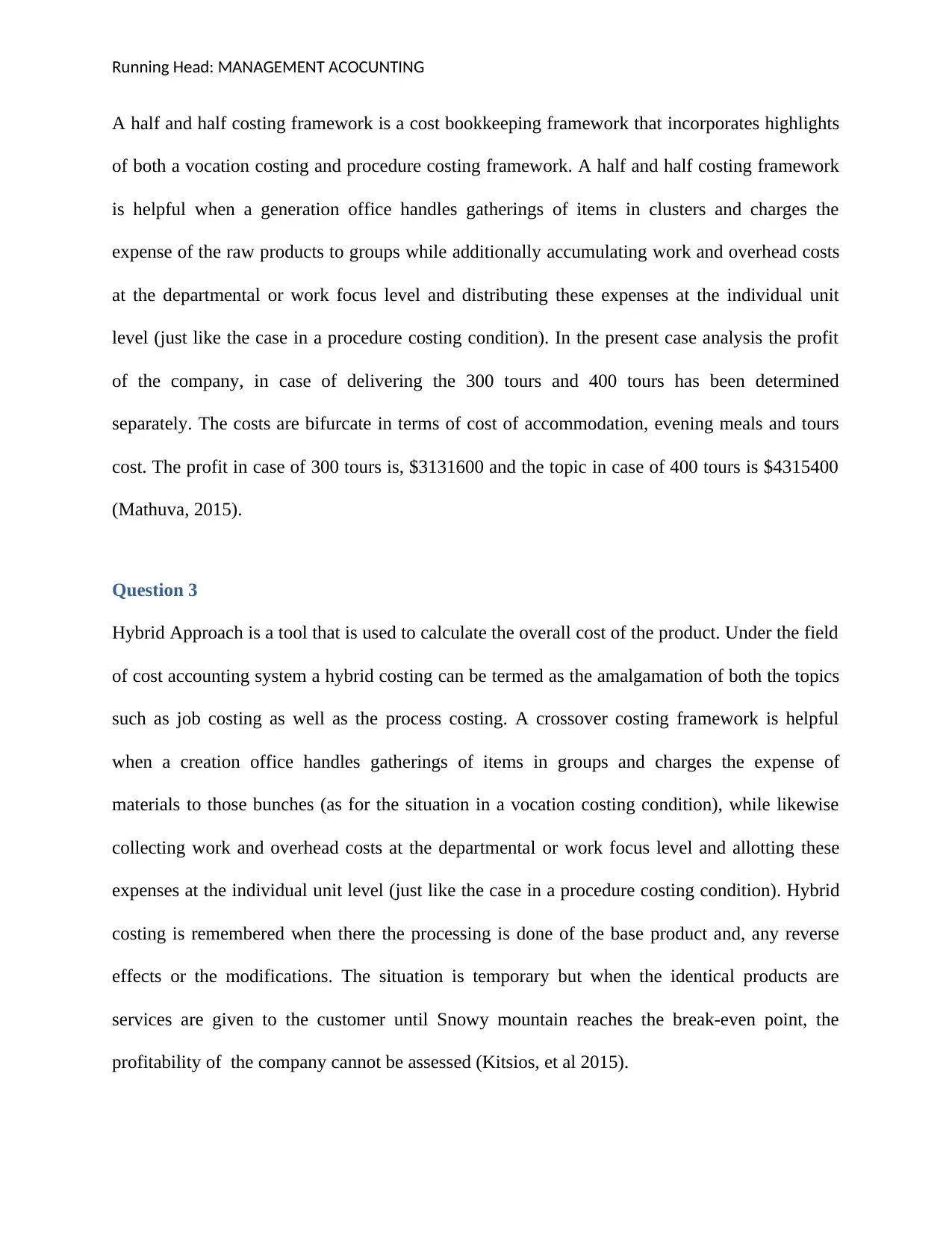

A half and half costing framework is a cost bookkeeping framework that incorporates highlights

of both a vocation costing and procedure costing framework. A half and half costing framework

is helpful when a generation office handles gatherings of items in clusters and charges the

expense of the raw products to groups while additionally accumulating work and overhead costs

at the departmental or work focus level and distributing these expenses at the individual unit

level (just like the case in a procedure costing condition). In the present case analysis the profit

of the company, in case of delivering the 300 tours and 400 tours has been determined

separately. The costs are bifurcate in terms of cost of accommodation, evening meals and tours

cost. The profit in case of 300 tours is, $3131600 and the topic in case of 400 tours is $4315400

(Mathuva, 2015).

Question 3

Hybrid Approach is a tool that is used to calculate the overall cost of the product. Under the field

of cost accounting system a hybrid costing can be termed as the amalgamation of both the topics

such as job costing as well as the process costing. A crossover costing framework is helpful

when a creation office handles gatherings of items in groups and charges the expense of

materials to those bunches (as for the situation in a vocation costing condition), while likewise

collecting work and overhead costs at the departmental or work focus level and allotting these

expenses at the individual unit level (just like the case in a procedure costing condition). Hybrid

costing is remembered when there the processing is done of the base product and, any reverse

effects or the modifications. The situation is temporary but when the identical products are

services are given to the customer until Snowy mountain reaches the break-even point, the

profitability of the company cannot be assessed (Kitsios, et al 2015).

A half and half costing framework is a cost bookkeeping framework that incorporates highlights

of both a vocation costing and procedure costing framework. A half and half costing framework

is helpful when a generation office handles gatherings of items in clusters and charges the

expense of the raw products to groups while additionally accumulating work and overhead costs

at the departmental or work focus level and distributing these expenses at the individual unit

level (just like the case in a procedure costing condition). In the present case analysis the profit

of the company, in case of delivering the 300 tours and 400 tours has been determined

separately. The costs are bifurcate in terms of cost of accommodation, evening meals and tours

cost. The profit in case of 300 tours is, $3131600 and the topic in case of 400 tours is $4315400

(Mathuva, 2015).

Question 3

Hybrid Approach is a tool that is used to calculate the overall cost of the product. Under the field

of cost accounting system a hybrid costing can be termed as the amalgamation of both the topics

such as job costing as well as the process costing. A crossover costing framework is helpful

when a creation office handles gatherings of items in groups and charges the expense of

materials to those bunches (as for the situation in a vocation costing condition), while likewise

collecting work and overhead costs at the departmental or work focus level and allotting these

expenses at the individual unit level (just like the case in a procedure costing condition). Hybrid

costing is remembered when there the processing is done of the base product and, any reverse

effects or the modifications. The situation is temporary but when the identical products are

services are given to the customer until Snowy mountain reaches the break-even point, the

profitability of the company cannot be assessed (Kitsios, et al 2015).

Running Head: MANAGEMENT ACOCUNTING

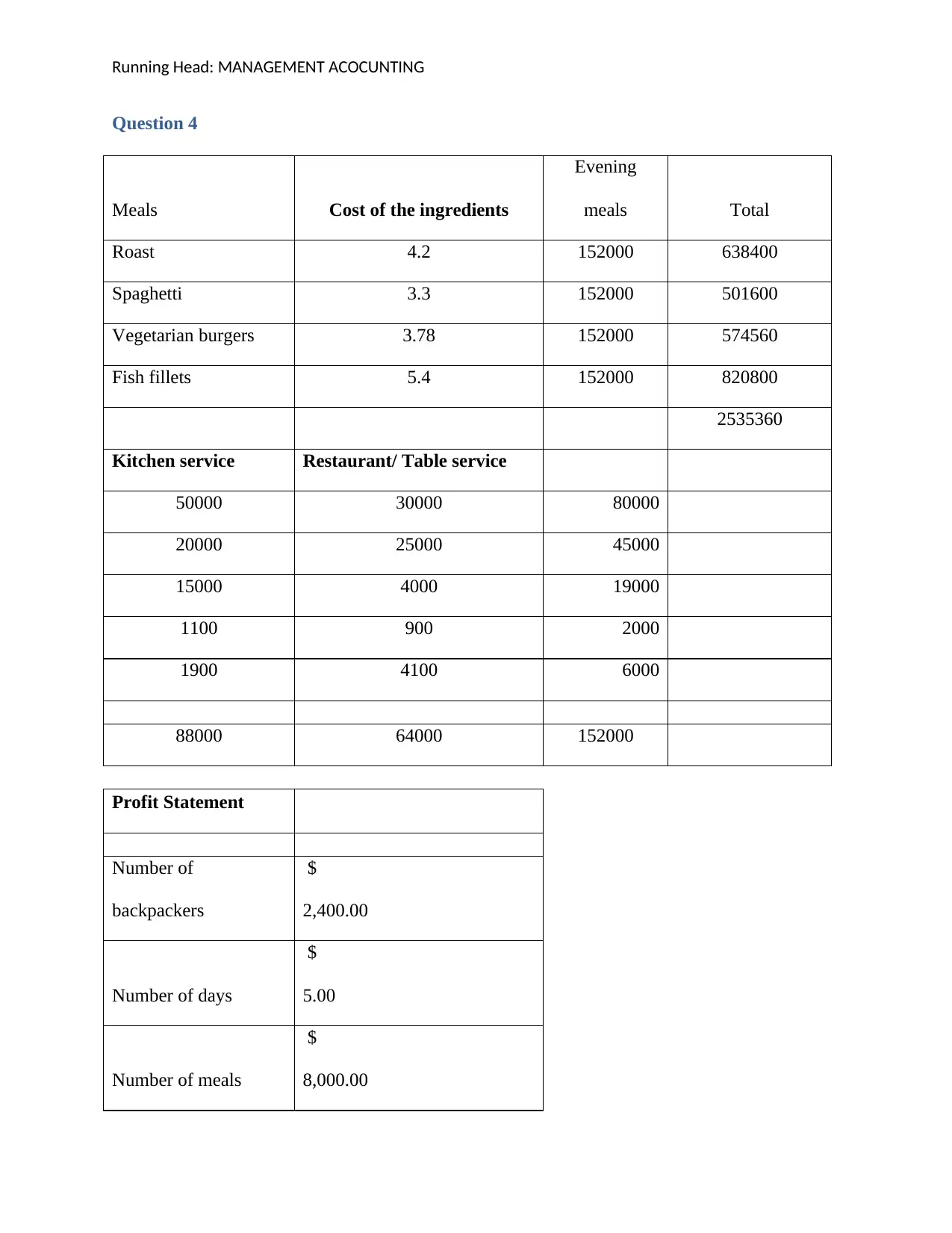

Question 4

Meals Cost of the ingredients

Evening

meals Total

Roast 4.2 152000 638400

Spaghetti 3.3 152000 501600

Vegetarian burgers 3.78 152000 574560

Fish fillets 5.4 152000 820800

2535360

Kitchen service Restaurant/ Table service

50000 30000 80000

20000 25000 45000

15000 4000 19000

1100 900 2000

1900 4100 6000

88000 64000 152000

Profit Statement

Number of

backpackers

$

2,400.00

Number of days

$

5.00

Number of meals

$

8,000.00

Question 4

Meals Cost of the ingredients

Evening

meals Total

Roast 4.2 152000 638400

Spaghetti 3.3 152000 501600

Vegetarian burgers 3.78 152000 574560

Fish fillets 5.4 152000 820800

2535360

Kitchen service Restaurant/ Table service

50000 30000 80000

20000 25000 45000

15000 4000 19000

1100 900 2000

1900 4100 6000

88000 64000 152000

Profit Statement

Number of

backpackers

$

2,400.00

Number of days

$

5.00

Number of meals

$

8,000.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: MANAGEMENT ACOCUNTING

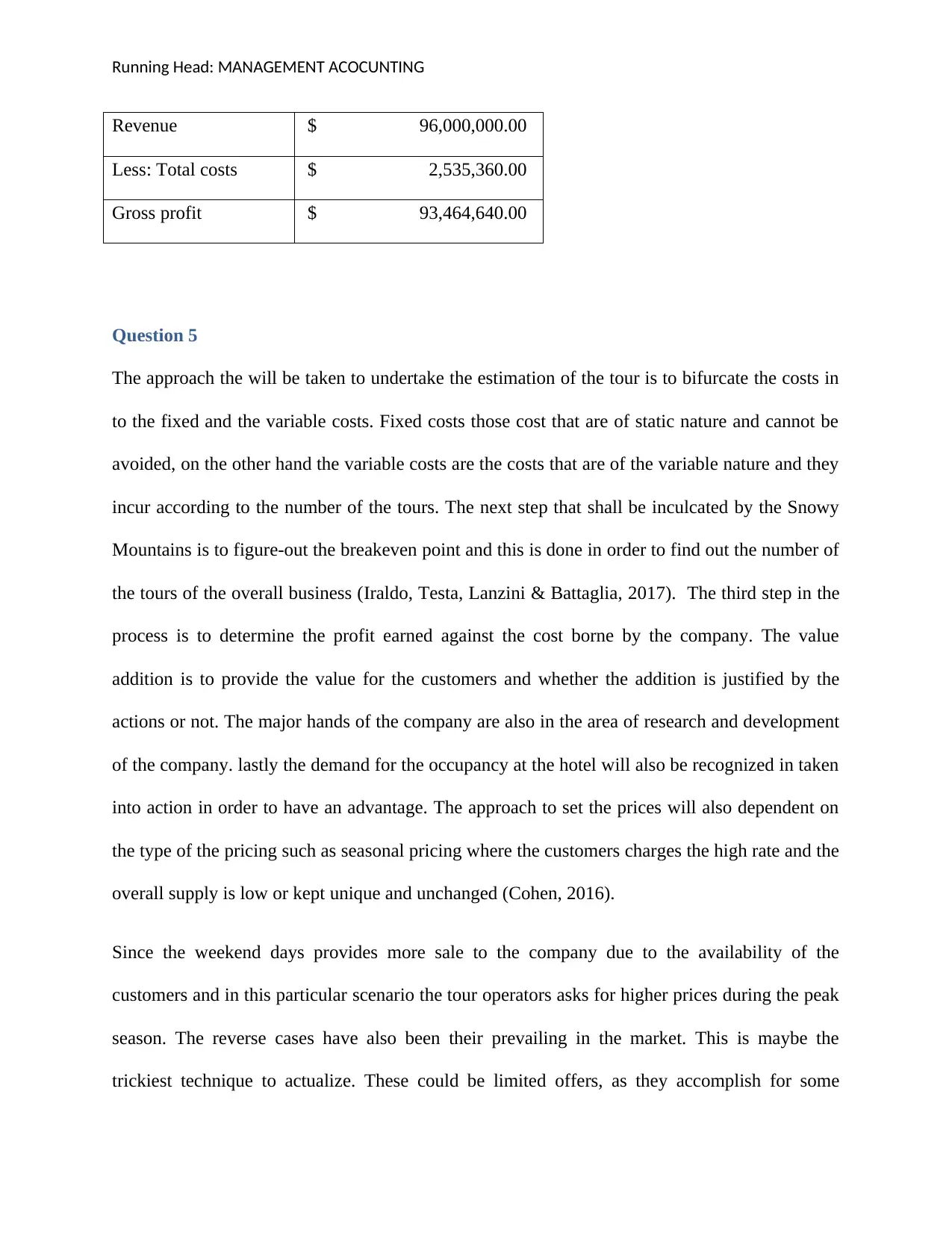

Revenue $ 96,000,000.00

Less: Total costs $ 2,535,360.00

Gross profit $ 93,464,640.00

Question 5

The approach the will be taken to undertake the estimation of the tour is to bifurcate the costs in

to the fixed and the variable costs. Fixed costs those cost that are of static nature and cannot be

avoided, on the other hand the variable costs are the costs that are of the variable nature and they

incur according to the number of the tours. The next step that shall be inculcated by the Snowy

Mountains is to figure-out the breakeven point and this is done in order to find out the number of

the tours of the overall business (Iraldo, Testa, Lanzini & Battaglia, 2017). The third step in the

process is to determine the profit earned against the cost borne by the company. The value

addition is to provide the value for the customers and whether the addition is justified by the

actions or not. The major hands of the company are also in the area of research and development

of the company. lastly the demand for the occupancy at the hotel will also be recognized in taken

into action in order to have an advantage. The approach to set the prices will also dependent on

the type of the pricing such as seasonal pricing where the customers charges the high rate and the

overall supply is low or kept unique and unchanged (Cohen, 2016).

Since the weekend days provides more sale to the company due to the availability of the

customers and in this particular scenario the tour operators asks for higher prices during the peak

season. The reverse cases have also been their prevailing in the market. This is maybe the

trickiest technique to actualize. These could be limited offers, as they accomplish for some

Revenue $ 96,000,000.00

Less: Total costs $ 2,535,360.00

Gross profit $ 93,464,640.00

Question 5

The approach the will be taken to undertake the estimation of the tour is to bifurcate the costs in

to the fixed and the variable costs. Fixed costs those cost that are of static nature and cannot be

avoided, on the other hand the variable costs are the costs that are of the variable nature and they

incur according to the number of the tours. The next step that shall be inculcated by the Snowy

Mountains is to figure-out the breakeven point and this is done in order to find out the number of

the tours of the overall business (Iraldo, Testa, Lanzini & Battaglia, 2017). The third step in the

process is to determine the profit earned against the cost borne by the company. The value

addition is to provide the value for the customers and whether the addition is justified by the

actions or not. The major hands of the company are also in the area of research and development

of the company. lastly the demand for the occupancy at the hotel will also be recognized in taken

into action in order to have an advantage. The approach to set the prices will also dependent on

the type of the pricing such as seasonal pricing where the customers charges the high rate and the

overall supply is low or kept unique and unchanged (Cohen, 2016).

Since the weekend days provides more sale to the company due to the availability of the

customers and in this particular scenario the tour operators asks for higher prices during the peak

season. The reverse cases have also been their prevailing in the market. This is maybe the

trickiest technique to actualize. These could be limited offers, as they accomplish for some

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: MANAGEMENT ACOCUNTING

auditorium appears, where clients are just permitted to purchase a ticket a couple of hours before

the show or on the day itself (Lee, 2015).

In the event that your definitive objective is to get your visits booked to limit, this would be a

decent procedure to push for a minute ago deals. Notwithstanding, you have to choose if this

exceeds the potential salary you could have produced using un-limited appointments.

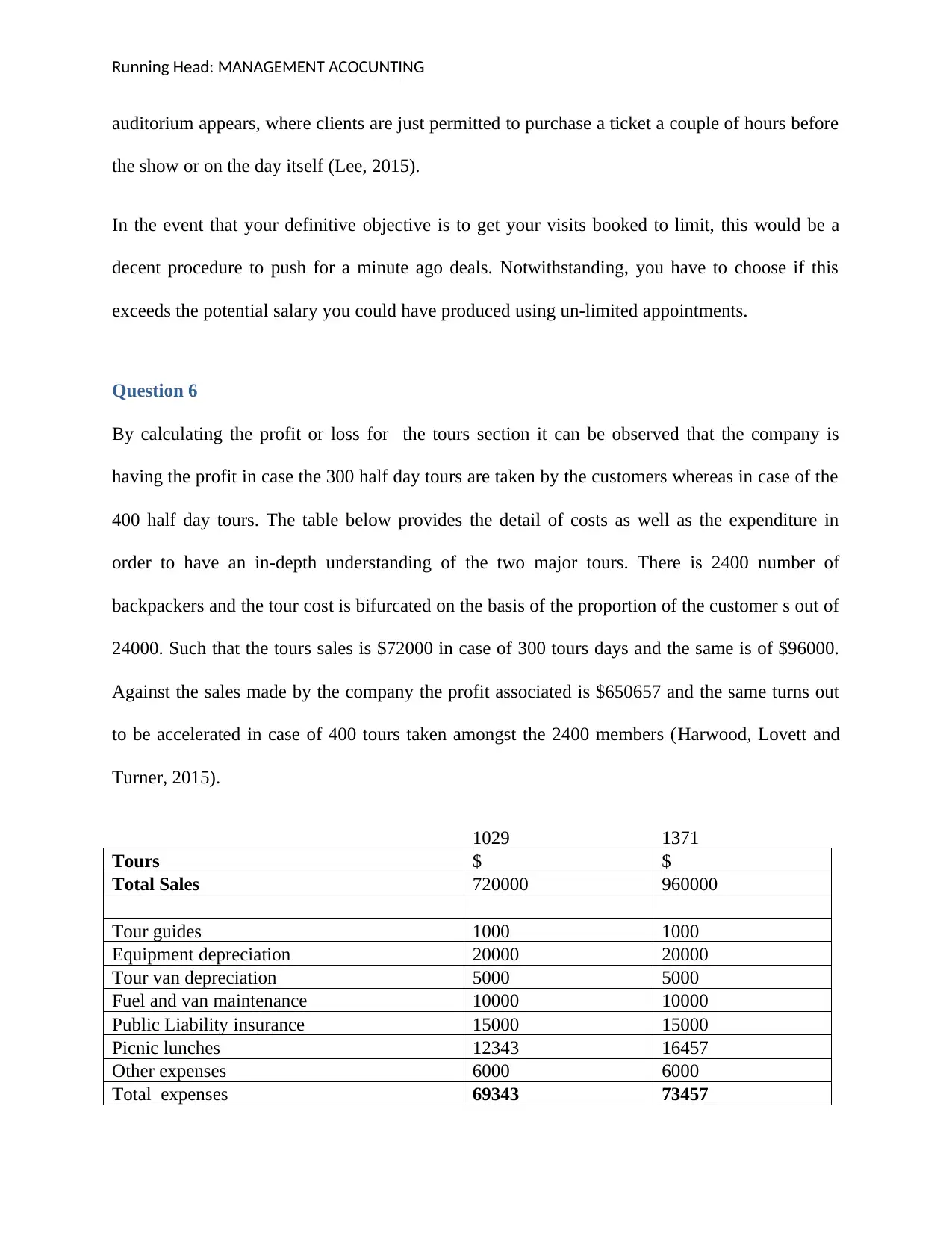

Question 6

By calculating the profit or loss for the tours section it can be observed that the company is

having the profit in case the 300 half day tours are taken by the customers whereas in case of the

400 half day tours. The table below provides the detail of costs as well as the expenditure in

order to have an in-depth understanding of the two major tours. There is 2400 number of

backpackers and the tour cost is bifurcated on the basis of the proportion of the customer s out of

24000. Such that the tours sales is $72000 in case of 300 tours days and the same is of $96000.

Against the sales made by the company the profit associated is $650657 and the same turns out

to be accelerated in case of 400 tours taken amongst the 2400 members (Harwood, Lovett and

Turner, 2015).

1029 1371

Tours $ $

Total Sales 720000 960000

Tour guides 1000 1000

Equipment depreciation 20000 20000

Tour van depreciation 5000 5000

Fuel and van maintenance 10000 10000

Public Liability insurance 15000 15000

Picnic lunches 12343 16457

Other expenses 6000 6000

Total expenses 69343 73457

auditorium appears, where clients are just permitted to purchase a ticket a couple of hours before

the show or on the day itself (Lee, 2015).

In the event that your definitive objective is to get your visits booked to limit, this would be a

decent procedure to push for a minute ago deals. Notwithstanding, you have to choose if this

exceeds the potential salary you could have produced using un-limited appointments.

Question 6

By calculating the profit or loss for the tours section it can be observed that the company is

having the profit in case the 300 half day tours are taken by the customers whereas in case of the

400 half day tours. The table below provides the detail of costs as well as the expenditure in

order to have an in-depth understanding of the two major tours. There is 2400 number of

backpackers and the tour cost is bifurcated on the basis of the proportion of the customer s out of

24000. Such that the tours sales is $72000 in case of 300 tours days and the same is of $96000.

Against the sales made by the company the profit associated is $650657 and the same turns out

to be accelerated in case of 400 tours taken amongst the 2400 members (Harwood, Lovett and

Turner, 2015).

1029 1371

Tours $ $

Total Sales 720000 960000

Tour guides 1000 1000

Equipment depreciation 20000 20000

Tour van depreciation 5000 5000

Fuel and van maintenance 10000 10000

Public Liability insurance 15000 15000

Picnic lunches 12343 16457

Other expenses 6000 6000

Total expenses 69343 73457

Running Head: MANAGEMENT ACOCUNTING

Profit 650657 -34829

The profit that has been earned in the section 1 is$650657, whereas the same is more in case of

the 400 tours which is $886543. In terms of the profitability the business is doing and performing

well. Further, the expenses that have been high and that needs to be controlled are picnic lunches

and the insurance of the liability.

Question 7

In order to improve the profitability of the business there are several recommendations which can

be incorporated by the business in order to have a profitable business. Following are the several

strategies that can be used by the business in order to have a deep analysis. The company must

improve the funding of the money or the financial aspect of the company. One of the

recommendations that can be measured by the most of the other products is the ability to settle

down. For example City/local visits ordinarily keep going for one entire day or less. They pursue

a fixed agenda and will visit regions of enthusiasm for a particular spot, regardless of whether

that is notable, religious or social, refreshments or dinners are frequently included.

Gathering visits likewise pursue a fixed and pre-orchestrated agenda. They frequently just occur

contingent upon the quantity of explorers for example they require a specific number of voyagers

so as to proceed or it turns into a money related expense instead of gainful (Cohen, 2016).

Question 8

There are several strategic variables or say the parameters that are helpful for the companies like

tours and the travel companies. Further the analysis is carried out on the basis of the fact that this

Profit 650657 -34829

The profit that has been earned in the section 1 is$650657, whereas the same is more in case of

the 400 tours which is $886543. In terms of the profitability the business is doing and performing

well. Further, the expenses that have been high and that needs to be controlled are picnic lunches

and the insurance of the liability.

Question 7

In order to improve the profitability of the business there are several recommendations which can

be incorporated by the business in order to have a profitable business. Following are the several

strategies that can be used by the business in order to have a deep analysis. The company must

improve the funding of the money or the financial aspect of the company. One of the

recommendations that can be measured by the most of the other products is the ability to settle

down. For example City/local visits ordinarily keep going for one entire day or less. They pursue

a fixed agenda and will visit regions of enthusiasm for a particular spot, regardless of whether

that is notable, religious or social, refreshments or dinners are frequently included.

Gathering visits likewise pursue a fixed and pre-orchestrated agenda. They frequently just occur

contingent upon the quantity of explorers for example they require a specific number of voyagers

so as to proceed or it turns into a money related expense instead of gainful (Cohen, 2016).

Question 8

There are several strategic variables or say the parameters that are helpful for the companies like

tours and the travel companies. Further the analysis is carried out on the basis of the fact that this

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.