Analysis of Management Accounting Practices for IMDA Ltd Report

VerifiedAdded on 2019/12/18

|14

|3664

|403

Report

AI Summary

This report delves into the realm of management accounting (MA) practices, emphasizing their critical role in business survival and effective decision-making. It analyzes the case of IMDA Ltd, highlighting the significance of MA in contrast to financial accounting, and explores various MA practices such as cost accounting, inventory management, job costing, and price optimization. The report examines costing methods, including absorption and marginal costing, providing detailed calculations and income statements. Furthermore, it discusses budgeting techniques, including master and operating budgets, and their respective advantages and disadvantages. The report concludes by emphasizing the importance of MA in forecasting, decision-making, and overall firm sustainability, providing a comprehensive overview of MA principles and their practical application within a business context. Access more past papers and solved assignments on Desklib.

MANAGEMENT

ACCONUTING

ACCONUTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK.1............................................................................................................................................3

A).................................................................................................................................................3

1..............................................................................................................................................3

2..............................................................................................................................................4

B).................................................................................................................................................5

TASK. 2...........................................................................................................................................6

TASK. 3...........................................................................................................................................9

TASK. 4.........................................................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

TASK.1............................................................................................................................................3

A).................................................................................................................................................3

1..............................................................................................................................................3

2..............................................................................................................................................4

B).................................................................................................................................................5

TASK. 2...........................................................................................................................................6

TASK. 3...........................................................................................................................................9

TASK. 4.........................................................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

MA practice is must for the business survival. There has been seen that the company

which does not follow in their business the MA practices, are not run for a long run. There are so

many bodies who specially trained the individual to practically apply MA practices in the

business. However, MA activities are applied almost all the companies for their betterment. MA

activities assist the management for practising within the organisation(Granlund, 2011). IMDA

Limited while applying MA practices in their business, did not apply effectively. That is the

main cause why Imda Ltd did not take decision effectively. MA practises requires special

interest individuals,like CPA, CA, ACCA etc.

TASK.1

A).

1.

MA practices are the one which reports to the management about the organisation's internal

activities. MA is the procedure is to determine the data, measuring of them, analyse them in a

better way and and communicating those data within the organisation for attainment of the

organisational goals and objectives. This is also named as “cost accounting”. MA assists the

managers of IMDA Ltd for making the decisions in order to attain the objectives. On the other

hands, financial accounting is the the accounting which provides the reports to the outsiders or

special interest group people about the organisation's finance related informations so that such

outsiders would able to take their investment decisions. MA use the informations which are

connected to the cost of the product or service(Fullerton, Kennedy and Widener, 2013). While

financial accounting, is connected to the financial statements of the organisation. MA helps the

managers to make the plans or strategies for the betterment of organisation. MA is the broad

concept then finance accounting, as it covers finance related matters within itself. MA is the

internal process which is implemented for business transactions. While finance accounting is

used to sum all the accounting information into financial statements of the company.

BASIS OF DIFFERENCE MA FINANCIAL ACCOUNTING

Aggregation It reports at more detailed

level. Like- profits by

It reports on outcomes of an

MA practice is must for the business survival. There has been seen that the company

which does not follow in their business the MA practices, are not run for a long run. There are so

many bodies who specially trained the individual to practically apply MA practices in the

business. However, MA activities are applied almost all the companies for their betterment. MA

activities assist the management for practising within the organisation(Granlund, 2011). IMDA

Limited while applying MA practices in their business, did not apply effectively. That is the

main cause why Imda Ltd did not take decision effectively. MA practises requires special

interest individuals,like CPA, CA, ACCA etc.

TASK.1

A).

1.

MA practices are the one which reports to the management about the organisation's internal

activities. MA is the procedure is to determine the data, measuring of them, analyse them in a

better way and and communicating those data within the organisation for attainment of the

organisational goals and objectives. This is also named as “cost accounting”. MA assists the

managers of IMDA Ltd for making the decisions in order to attain the objectives. On the other

hands, financial accounting is the the accounting which provides the reports to the outsiders or

special interest group people about the organisation's finance related informations so that such

outsiders would able to take their investment decisions. MA use the informations which are

connected to the cost of the product or service(Fullerton, Kennedy and Widener, 2013). While

financial accounting, is connected to the financial statements of the organisation. MA helps the

managers to make the plans or strategies for the betterment of organisation. MA is the broad

concept then finance accounting, as it covers finance related matters within itself. MA is the

internal process which is implemented for business transactions. While finance accounting is

used to sum all the accounting information into financial statements of the company.

BASIS OF DIFFERENCE MA FINANCIAL ACCOUNTING

Aggregation It reports at more detailed

level. Like- profits by

It reports on outcomes of an

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

products,product line. whole business.

Efficiency It reports on particularly, what

is causing issues and how to

fix them.

It reports on the profitability.

System It is totally concerned in the

location of bottleneck

operations.

It gives on attention to the

entire system which an

organisation for producing

profits

Time period It issue reports in order to

make budgets and forecasts.

It relates to the financial

results which an organisation

has already attained.

Valuation MA does not concern to the

assets and liabilities of the

company.

Financial accounting find out

an adequate valuation about

assets and liabilities.

2.

MA refers to the procedures for making management reports which could able to provides

proper financial and other related informations to the managers for making the short term and

long term decisions.

The MA plays crucial part in the IMDA Ltd. These are as follows:

1. For assisting the future forecasting: MA assist in forecasting the future of the

company. That will also supports for framing the decisions.

2. Assisting in make or buy decisions: with the help of MA, company would get to

know about the product that whether it needs to produce the product or buy form

the sub contractor at a cheaper rate than the cost of production(Otley and

Emmanuel, 2013).

3. Estimating cash flow: Forecasting and impacts of cash flow is must. MA assist in

knowing the forecasting of cash flow, like- how much capital is needed in the

future(Hiebl, 2014). MA covers designing of budgets and managers of the cited

Efficiency It reports on particularly, what

is causing issues and how to

fix them.

It reports on the profitability.

System It is totally concerned in the

location of bottleneck

operations.

It gives on attention to the

entire system which an

organisation for producing

profits

Time period It issue reports in order to

make budgets and forecasts.

It relates to the financial

results which an organisation

has already attained.

Valuation MA does not concern to the

assets and liabilities of the

company.

Financial accounting find out

an adequate valuation about

assets and liabilities.

2.

MA refers to the procedures for making management reports which could able to provides

proper financial and other related informations to the managers for making the short term and

long term decisions.

The MA plays crucial part in the IMDA Ltd. These are as follows:

1. For assisting the future forecasting: MA assist in forecasting the future of the

company. That will also supports for framing the decisions.

2. Assisting in make or buy decisions: with the help of MA, company would get to

know about the product that whether it needs to produce the product or buy form

the sub contractor at a cheaper rate than the cost of production(Otley and

Emmanuel, 2013).

3. Estimating cash flow: Forecasting and impacts of cash flow is must. MA assist in

knowing the forecasting of cash flow, like- how much capital is needed in the

future(Hiebl, 2014). MA covers designing of budgets and managers of the cited

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company implement this information to determines how to allocate capital for

producing the projected revenues.

4. Assessment of rate of return: MA practices in the firm helps to analyse the future

rate of return. If there are two or more investment opportunities are given, then

select the most profitable out of them.

Therefore, these are the ways through which MA helps the managers to make the efficient

decisions for the firm sustainability purpose.

B).

The MA practises helps the managers to collect and analyse the information through which they

could make an effective plans for the firm sustainability purposes. MA assists in knowing the

cost of the products. There are so many accounting tools such as, traditional cost accounting,

lean accounting, etc. which assess the cost of the product in different ways. If the company does

not follow MA practices within their business, then the cost of the product rises and reduce the

margin cost.

Cost accounting system: Cost accounting is a procedure through which company gets

to know about the cost of product with the help of measuring the input costs and fixed costs like

depreciation of capital employed(Zimmerman and Yahya-Zadeh, 2011). Cost accounting assist

to measures and record cost ,then compare input outcome to output or real outcomes to assist

firm management in assessing financial performance. However, there are almost four kinds of

cost accounting system. Which are namely standard cost accounting, activity based accounting,

lean accounting and marginal costing.

Standard costing implements ratios to compare effective implementation of labour and material

to manufacture product or services(Ward, 2012). Measuring these variance is known as variance

analysis.

Activity based costing gather the overheads from firm's each division and assign them to specific

cost objects such as, services, customers or product.

Lean accounting does not only concerned to limit the cost but also assist in making the decision

within the firm.

Inventory management system: This is the continuous procedures of moving product

into or out of firm's locations. Firm handle their stock on regular basis as they place fresh order

for goods and ship orders out of consumers. With the help of this system, company manages

producing the projected revenues.

4. Assessment of rate of return: MA practices in the firm helps to analyse the future

rate of return. If there are two or more investment opportunities are given, then

select the most profitable out of them.

Therefore, these are the ways through which MA helps the managers to make the efficient

decisions for the firm sustainability purpose.

B).

The MA practises helps the managers to collect and analyse the information through which they

could make an effective plans for the firm sustainability purposes. MA assists in knowing the

cost of the products. There are so many accounting tools such as, traditional cost accounting,

lean accounting, etc. which assess the cost of the product in different ways. If the company does

not follow MA practices within their business, then the cost of the product rises and reduce the

margin cost.

Cost accounting system: Cost accounting is a procedure through which company gets

to know about the cost of product with the help of measuring the input costs and fixed costs like

depreciation of capital employed(Zimmerman and Yahya-Zadeh, 2011). Cost accounting assist

to measures and record cost ,then compare input outcome to output or real outcomes to assist

firm management in assessing financial performance. However, there are almost four kinds of

cost accounting system. Which are namely standard cost accounting, activity based accounting,

lean accounting and marginal costing.

Standard costing implements ratios to compare effective implementation of labour and material

to manufacture product or services(Ward, 2012). Measuring these variance is known as variance

analysis.

Activity based costing gather the overheads from firm's each division and assign them to specific

cost objects such as, services, customers or product.

Lean accounting does not only concerned to limit the cost but also assist in making the decision

within the firm.

Inventory management system: This is the continuous procedures of moving product

into or out of firm's locations. Firm handle their stock on regular basis as they place fresh order

for goods and ship orders out of consumers. With the help of this system, company manages

their stock at an optimum level. If the company does not do the proper inventory management it

cannot satiate the whole clients.

Job Costing system: It incorporates the route towards collecting data about the cost

related with a specific manufacturing work (Macintosh and Quattrone, 2010). This information

may be required in remembering the true objective to display the cost information to a customer

under agreements where cost can be reimbursed.

Price optimising system: Value Optimization Models are logical model which register

how request shift at different value levels, then join that data with information on expenses and

stock levels to endorse value that could improve benefits. This model could be implemented to

tailor pricing for customer division by replicating how focused customers will respond to value

changes with data driven situations.

TASK. 2

The profits of the company could be determined by various methods of MA. The IMDA Ltd is a

manufacturing company whose main aim is to produce the more specific charger for the

mobile(Lukka and Modell, 2010). So that the net profits can be determined by way of absorption

costing method or marginal costing methods.

Absorption costing: Under this costing method, various costs which are related to the different

types of product procedure are absorbed on a cost of the good. Through absorption costing, the

cited company is able to evaluate the inventory of a firm. Estimation is the chief component of

MA.

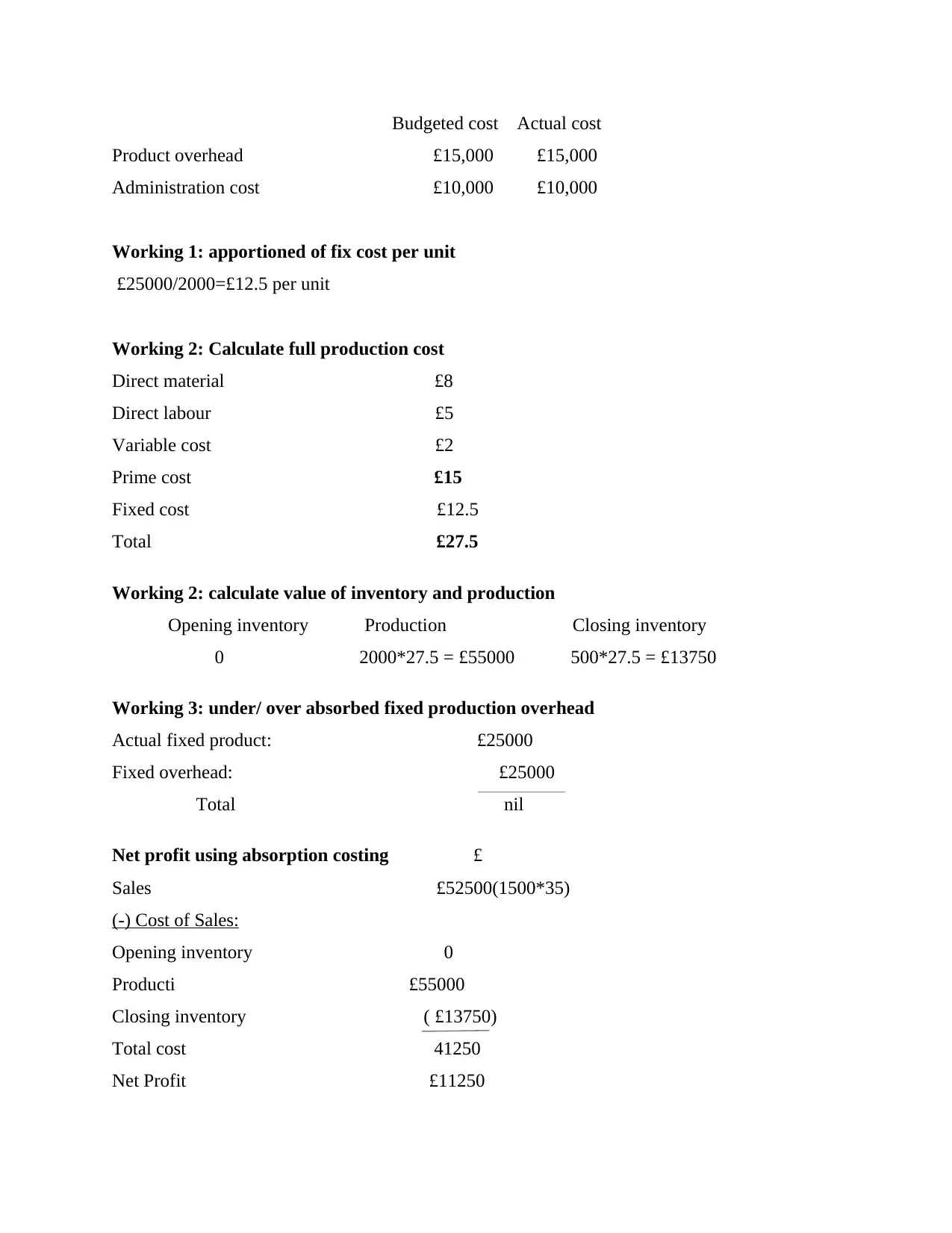

Income Statement as per absorption costing :

Selling price £35

Unit costs

Direct Labour £5

Direct Material £8

Variable Product overhead £2

Variable sales overhead £5.25

Budgeted product for the period is 3000 units

Actual product for the September is 2000 units

Fixed costs for the month are given below

cannot satiate the whole clients.

Job Costing system: It incorporates the route towards collecting data about the cost

related with a specific manufacturing work (Macintosh and Quattrone, 2010). This information

may be required in remembering the true objective to display the cost information to a customer

under agreements where cost can be reimbursed.

Price optimising system: Value Optimization Models are logical model which register

how request shift at different value levels, then join that data with information on expenses and

stock levels to endorse value that could improve benefits. This model could be implemented to

tailor pricing for customer division by replicating how focused customers will respond to value

changes with data driven situations.

TASK. 2

The profits of the company could be determined by various methods of MA. The IMDA Ltd is a

manufacturing company whose main aim is to produce the more specific charger for the

mobile(Lukka and Modell, 2010). So that the net profits can be determined by way of absorption

costing method or marginal costing methods.

Absorption costing: Under this costing method, various costs which are related to the different

types of product procedure are absorbed on a cost of the good. Through absorption costing, the

cited company is able to evaluate the inventory of a firm. Estimation is the chief component of

MA.

Income Statement as per absorption costing :

Selling price £35

Unit costs

Direct Labour £5

Direct Material £8

Variable Product overhead £2

Variable sales overhead £5.25

Budgeted product for the period is 3000 units

Actual product for the September is 2000 units

Fixed costs for the month are given below

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Budgeted cost Actual cost

Product overhead £15,000 £15,000

Administration cost £10,000 £10,000

Working 1: apportioned of fix cost per unit

£25000/2000=£12.5 per unit

Working 2: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Prime cost £15

Fixed cost £12.5

Total £27.5

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2000*27.5 = £55000 500*27.5 = £13750

Working 3: under/ over absorbed fixed production overhead

Actual fixed product: £25000

Fixed overhead: £25000

Total nil

Net profit using absorption costing £

Sales £52500(1500*35)

(-) Cost of Sales:

Opening inventory 0

Producti £55000

Closing inventory ( £13750)

Total cost 41250

Net Profit £11250

Product overhead £15,000 £15,000

Administration cost £10,000 £10,000

Working 1: apportioned of fix cost per unit

£25000/2000=£12.5 per unit

Working 2: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Prime cost £15

Fixed cost £12.5

Total £27.5

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2000*27.5 = £55000 500*27.5 = £13750

Working 3: under/ over absorbed fixed production overhead

Actual fixed product: £25000

Fixed overhead: £25000

Total nil

Net profit using absorption costing £

Sales £52500(1500*35)

(-) Cost of Sales:

Opening inventory 0

Producti £55000

Closing inventory ( £13750)

Total cost 41250

Net Profit £11250

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

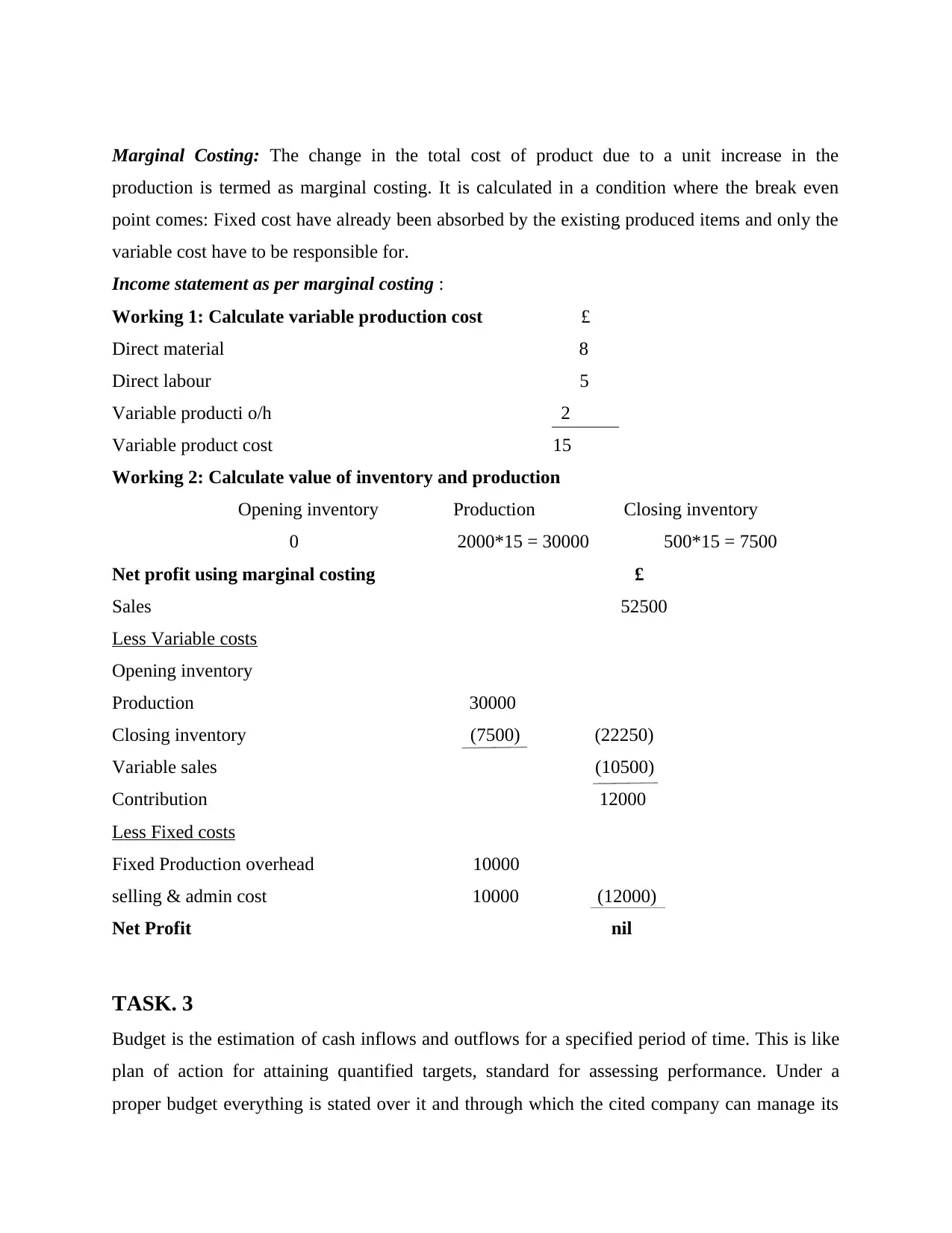

Marginal Costing: The change in the total cost of product due to a unit increase in the

production is termed as marginal costing. It is calculated in a condition where the break even

point comes: Fixed cost have already been absorbed by the existing produced items and only the

variable cost have to be responsible for.

Income statement as per marginal costing :

Working 1: Calculate variable production cost £

Direct material 8

Direct labour 5

Variable producti o/h 2

Variable product cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £

Sales 52500

Less Variable costs

Opening inventory

Production 30000

Closing inventory (7500) (22250)

Variable sales (10500)

Contribution 12000

Less Fixed costs

Fixed Production overhead 10000

selling & admin cost 10000 (12000)

Net Profit nil

TASK. 3

Budget is the estimation of cash inflows and outflows for a specified period of time. This is like

plan of action for attaining quantified targets, standard for assessing performance. Under a

proper budget everything is stated over it and through which the cited company can manage its

production is termed as marginal costing. It is calculated in a condition where the break even

point comes: Fixed cost have already been absorbed by the existing produced items and only the

variable cost have to be responsible for.

Income statement as per marginal costing :

Working 1: Calculate variable production cost £

Direct material 8

Direct labour 5

Variable producti o/h 2

Variable product cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £

Sales 52500

Less Variable costs

Opening inventory

Production 30000

Closing inventory (7500) (22250)

Variable sales (10500)

Contribution 12000

Less Fixed costs

Fixed Production overhead 10000

selling & admin cost 10000 (12000)

Net Profit nil

TASK. 3

Budget is the estimation of cash inflows and outflows for a specified period of time. This is like

plan of action for attaining quantified targets, standard for assessing performance. Under a

proper budget everything is stated over it and through which the cited company can manage its

entire expenses and also assist in investing entire money and finance in an adequate manner (Li

and et. al., 2012). In an organisation, every departments have their own budgets so that they

could able to manage their department in a better way. Through budget, risk can be reduced or

managed accordingly. However, there are several kinds of budgeting methods which have

advantages and disadvantages as well. These are:

1. Master budget

2. operating budget

3. cash flow budget

4. financial budget

5. static budget

These above mentioned budgets are so popular and supports in allocating entire resources.

1. Master budget: This consists all the factors which come under a financial year.

Master budget assist in providing a whole picture of its financial activity along

with its soundness. Master budget incorporates every one of the components such

as sales, assets, working costs, and earning streams to enable firm to set up their

objectives and targets which they need to accomplish and furthermore helps in

enhancing their performance. The advantages of the master budget have been

mentioned herewith:

a). It helps in making all the useful budgetary plans in a capsule shape which implies it assistance

in planning all the work related exercises budgets into one form (Herzig and et. al., 2012).

b). It helps in detailing all the functional plans at same place which implies it is the summery of

entire spending which is set up for a annual year.

c). It helps in evaluating the entire year profits of the association.

d). It is useful for the top specialist since it helps motel defining the entire spending plan in a

capsule shape in this way, it turn out to be simple for them to compute every exercises in a

legitimate way.

However, master budget contains disadvantages as well which shows why it is not to be followed

within the organisations which are as follows:

and et. al., 2012). In an organisation, every departments have their own budgets so that they

could able to manage their department in a better way. Through budget, risk can be reduced or

managed accordingly. However, there are several kinds of budgeting methods which have

advantages and disadvantages as well. These are:

1. Master budget

2. operating budget

3. cash flow budget

4. financial budget

5. static budget

These above mentioned budgets are so popular and supports in allocating entire resources.

1. Master budget: This consists all the factors which come under a financial year.

Master budget assist in providing a whole picture of its financial activity along

with its soundness. Master budget incorporates every one of the components such

as sales, assets, working costs, and earning streams to enable firm to set up their

objectives and targets which they need to accomplish and furthermore helps in

enhancing their performance. The advantages of the master budget have been

mentioned herewith:

a). It helps in making all the useful budgetary plans in a capsule shape which implies it assistance

in planning all the work related exercises budgets into one form (Herzig and et. al., 2012).

b). It helps in detailing all the functional plans at same place which implies it is the summery of

entire spending which is set up for a annual year.

c). It helps in evaluating the entire year profits of the association.

d). It is useful for the top specialist since it helps motel defining the entire spending plan in a

capsule shape in this way, it turn out to be simple for them to compute every exercises in a

legitimate way.

However, master budget contains disadvantages as well which shows why it is not to be followed

within the organisations which are as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

a) In master budget, their is an absence of specifications. Since it helps in deciding the entire

capacities of spending plans under one roof,it becomes impracticable for the top expert for

directing which office department is spending more and which offers less.

b) It advances the trouble in perusing and composing since it apportions entire budget plans in

one term. Along these lines, it makes an issue in comprehension.

2. Operating budget: It supports in assessing the everyday costs and operations of

the association. This is set up for evaluating the everyday operations costs since it

assist in understanding the clear and fitting report of the entire costs which are

occurring in an association on a continuous basis.

There are some of the operating budget advantages which have been discussed hereunder:

a) Employees salary and fixed overheads are the costs which cannot get dismissed and trimmed

by the organization and it is a beginning stage of the financial budget. Along these lines, working

spending help in dealing with the present costs of a firm. So that their business can work

appropriately.

b) It assists in framing reserves through investing in an adequate project association can gain

benefit and they can deal with their everyday operations appropriately. So, for such kind of

concern organization need to keep up stores for the association.

Each budgeting framework have a few advantages and inconveniences in this way, working

spending disadvantages are:

a) It takes cost in managing entire activities since a separate individuals need to hired for this

thing.

3. Financial budget: This kind of budget is framed for the whole budgetary year with every

single capacity has its different section(Garrison and et. al., 2010). This is one of the best

strategy for planning since it gives and viable review. This procedure is oftenlly adopted by each

company in an efficient manner. The points of interest and disinterest of this modern approach

are:

a) It helps in giving a viable review of the entire money related exercises and capacities in a

legitimate manner.

capacities of spending plans under one roof,it becomes impracticable for the top expert for

directing which office department is spending more and which offers less.

b) It advances the trouble in perusing and composing since it apportions entire budget plans in

one term. Along these lines, it makes an issue in comprehension.

2. Operating budget: It supports in assessing the everyday costs and operations of

the association. This is set up for evaluating the everyday operations costs since it

assist in understanding the clear and fitting report of the entire costs which are

occurring in an association on a continuous basis.

There are some of the operating budget advantages which have been discussed hereunder:

a) Employees salary and fixed overheads are the costs which cannot get dismissed and trimmed

by the organization and it is a beginning stage of the financial budget. Along these lines, working

spending help in dealing with the present costs of a firm. So that their business can work

appropriately.

b) It assists in framing reserves through investing in an adequate project association can gain

benefit and they can deal with their everyday operations appropriately. So, for such kind of

concern organization need to keep up stores for the association.

Each budgeting framework have a few advantages and inconveniences in this way, working

spending disadvantages are:

a) It takes cost in managing entire activities since a separate individuals need to hired for this

thing.

3. Financial budget: This kind of budget is framed for the whole budgetary year with every

single capacity has its different section(Garrison and et. al., 2010). This is one of the best

strategy for planning since it gives and viable review. This procedure is oftenlly adopted by each

company in an efficient manner. The points of interest and disinterest of this modern approach

are:

a) It helps in giving a viable review of the entire money related exercises and capacities in a

legitimate manner.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

b) It helps in making the financial plan adequately justifiable.

c) One of the most drawback financial plan is that it is extensive in nature and this extensiveness

make it hard to peruse it legitimately.

Budget support in assessing every one of the resources appropriately and in a productive way.

This is set up with the reason for making the monetary policies of association(Burritt and et. al.,

2011). Therefore, cited organisation need to utilize steps through which they can get design

budget which is successful in nature and adequate by the firm. Steps including in designing

budgets are:

1. Initially, organization need to accumulate data about the distinctive sources and

ventures on which they need to contribute money. Thus, that they can examine that the amount

they will going to spare and what sum will be spent.

2. Other thing of this progression is to designate all the fundamental variables which help

in making the financial plan, for example, unique sources through which back can be accessible

to them(Bodie, 2013).

3. Alongside that a powerful spending plan incorporates all the month to month costs

with an appropriate rundown.

4. In a proper spending all costs are separate into classifications.

5. Aggregate of month to month salary and costs since it helps in decide the benefit and

loss of business.

6. Make modification revenue driven which implies entire store ought to be appropriately

utilized as a part of a precise way.

7. In the event that in spending organization found that their costs are more than their

sparing than they need to chop down their spending in this way, that they can legitimately

oversee everything.

TASK. 4

Balance scorecard is the procedure of keep up the key planning and administration framework

which assist administration for staying a legitimate vision and methodology of an association.

c) One of the most drawback financial plan is that it is extensive in nature and this extensiveness

make it hard to peruse it legitimately.

Budget support in assessing every one of the resources appropriately and in a productive way.

This is set up with the reason for making the monetary policies of association(Burritt and et. al.,

2011). Therefore, cited organisation need to utilize steps through which they can get design

budget which is successful in nature and adequate by the firm. Steps including in designing

budgets are:

1. Initially, organization need to accumulate data about the distinctive sources and

ventures on which they need to contribute money. Thus, that they can examine that the amount

they will going to spare and what sum will be spent.

2. Other thing of this progression is to designate all the fundamental variables which help

in making the financial plan, for example, unique sources through which back can be accessible

to them(Bodie, 2013).

3. Alongside that a powerful spending plan incorporates all the month to month costs

with an appropriate rundown.

4. In a proper spending all costs are separate into classifications.

5. Aggregate of month to month salary and costs since it helps in decide the benefit and

loss of business.

6. Make modification revenue driven which implies entire store ought to be appropriately

utilized as a part of a precise way.

7. In the event that in spending organization found that their costs are more than their

sparing than they need to chop down their spending in this way, that they can legitimately

oversee everything.

TASK. 4

Balance scorecard is the procedure of keep up the key planning and administration framework

which assist administration for staying a legitimate vision and methodology of an association.

Furthermore, BS approach helps management in recuperating from all the outside and inner

elements. Balance scorecard is the most important process which is utilized by the organization's

management to examine firm's execution and also aides in keep up key administration

framework. This technique is one of the compelling way.

Imda tech endures lost £1.5 million and from recuperating from that they are required to

utilize this procedure since it helps firm in keep up its execution alongside their representative's

(Baldvinsdottir, Mitchell and Nørreklit, 2010). Likewise balance scorecard approach helps the

cited company for making methodology in this way, that they can dissect every one of the

variables and execute the methodologies as per manner.

An organization can distinguish its budgetary issue with help of this approach. IMDA Ltd also

incorporate all their central goal and dreams. It demonstrates the sum-up of blend money related

and non-monetary things. Like by utilizing this approach, This approach helps the cited firm in

tackling out its budgetary problem.

This scorecard demonstrates the procedures which are figure by the IMDA Ltd. It helps in

recalling all elements on consistent schedule by the administration. Thus, that they need to deal

with such variable and execute every single via BS system through which they can recuperate

their loss of £1.5 million.

CONCLUSION

Form the above report, it has been find that the IMDA Ltd need to make their decisions

effectively by applying the effective management practices. There are so many tools which have

been applied in the firm, MA officers are the proper individuals who apply such tools. MA

officers also find the errors so that they are able to make the decisions in a prudent manner. It

also been point out that the company figure out the income statements by way of absorption

costing or marginal costing methodology.

elements. Balance scorecard is the most important process which is utilized by the organization's

management to examine firm's execution and also aides in keep up key administration

framework. This technique is one of the compelling way.

Imda tech endures lost £1.5 million and from recuperating from that they are required to

utilize this procedure since it helps firm in keep up its execution alongside their representative's

(Baldvinsdottir, Mitchell and Nørreklit, 2010). Likewise balance scorecard approach helps the

cited company for making methodology in this way, that they can dissect every one of the

variables and execute the methodologies as per manner.

An organization can distinguish its budgetary issue with help of this approach. IMDA Ltd also

incorporate all their central goal and dreams. It demonstrates the sum-up of blend money related

and non-monetary things. Like by utilizing this approach, This approach helps the cited firm in

tackling out its budgetary problem.

This scorecard demonstrates the procedures which are figure by the IMDA Ltd. It helps in

recalling all elements on consistent schedule by the administration. Thus, that they need to deal

with such variable and execute every single via BS system through which they can recuperate

their loss of £1.5 million.

CONCLUSION

Form the above report, it has been find that the IMDA Ltd need to make their decisions

effectively by applying the effective management practices. There are so many tools which have

been applied in the firm, MA officers are the proper individuals who apply such tools. MA

officers also find the errors so that they are able to make the decisions in a prudent manner. It

also been point out that the company figure out the income statements by way of absorption

costing or marginal costing methodology.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.