Management Accounting: Report, Analysis, and Financial Reporting

VerifiedAdded on 2022/12/26

|29

|4421

|90

Report

AI Summary

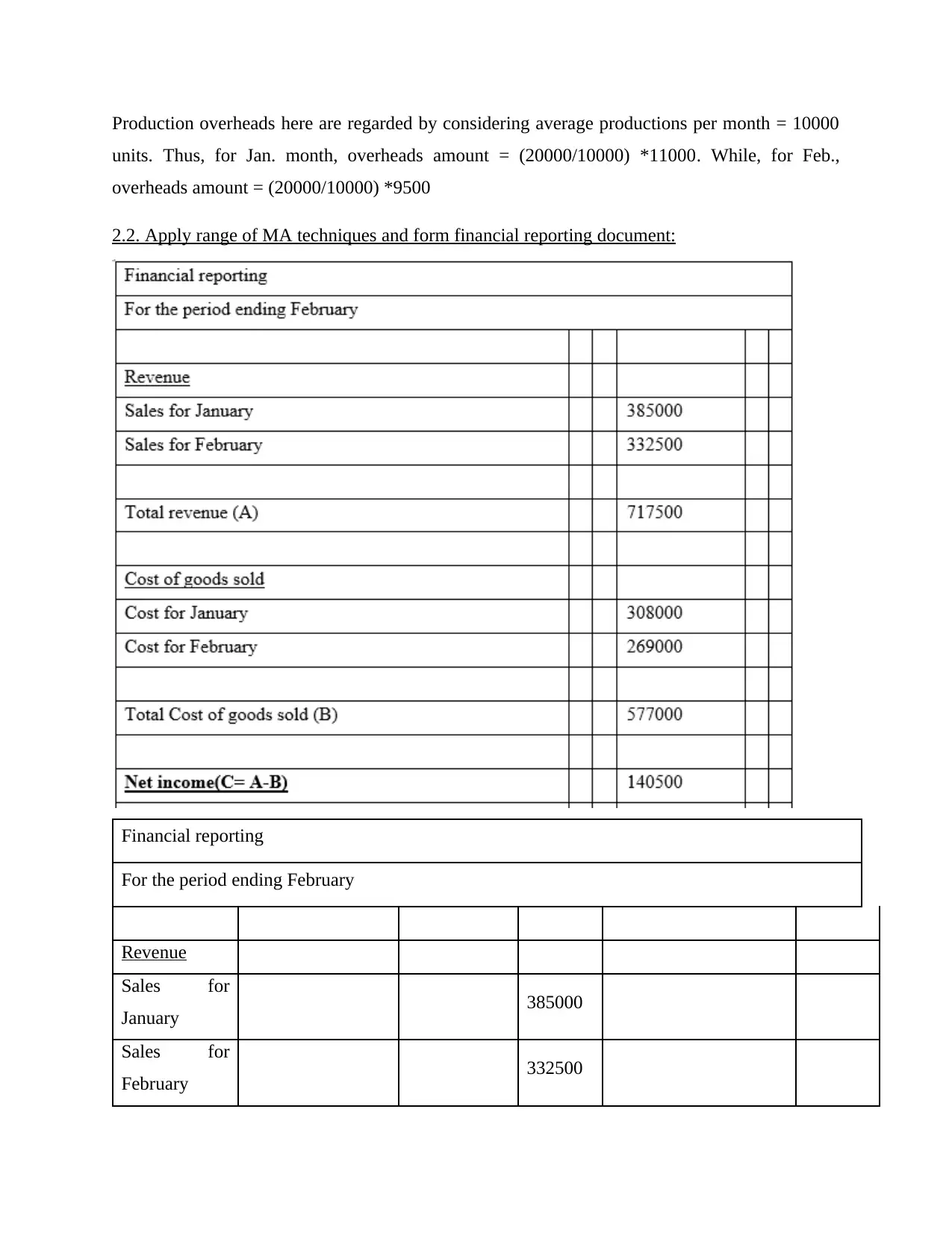

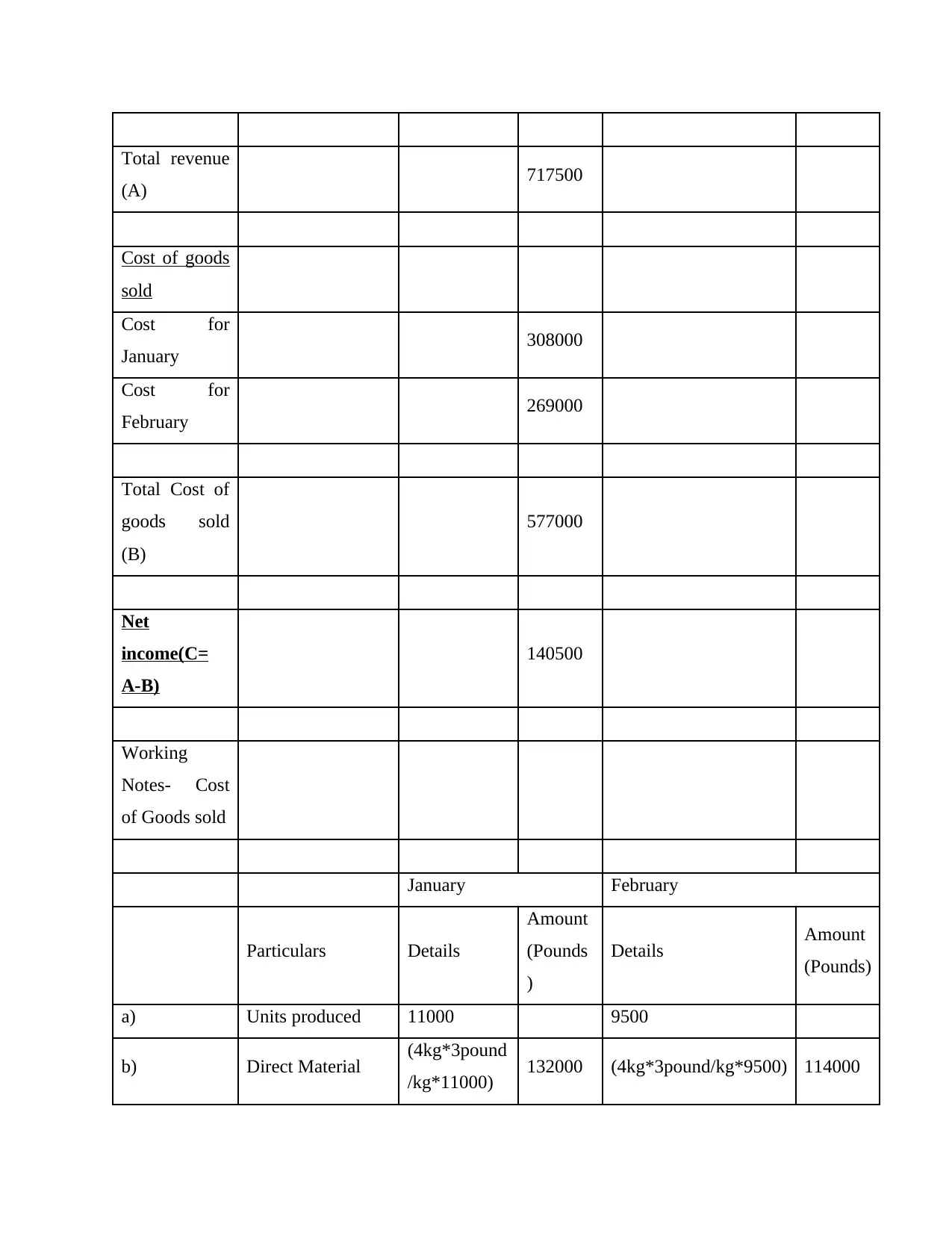

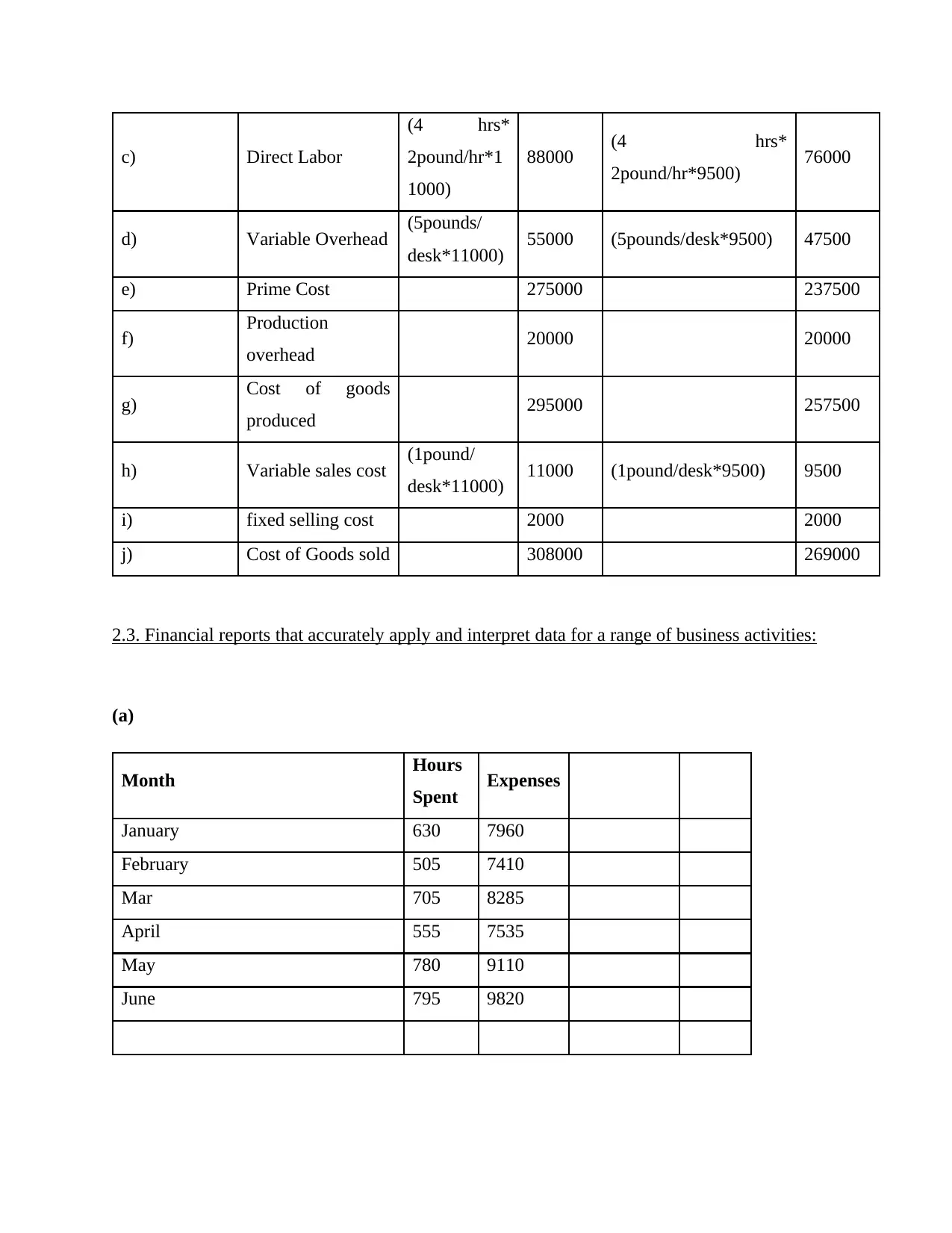

This report delves into the core concepts of management accounting, encompassing its systems, applications, and integration within organizational processes. It begins by defining management accounting and its significance in providing crucial information to managers for effective decision-making. The report explores various management accounting systems, including inventory management, job costing, and price optimization, detailing their key features and benefits. It then critically evaluates the integration of these systems within organizational frameworks. The report presents financial reporting documents, including income statements and cost of goods sold calculations, along with detailed analyses using techniques like high-low method, FIFO, LIFO, and weighted average costing. Finally, it covers break-even analysis and profit calculations, providing a comprehensive overview of management accounting principles and their practical application in business scenarios.

1 out of 29

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.