Management Accounting Report: Comparison of Costing Methods

VerifiedAdded on 2021/05/31

|8

|1208

|55

Report

AI Summary

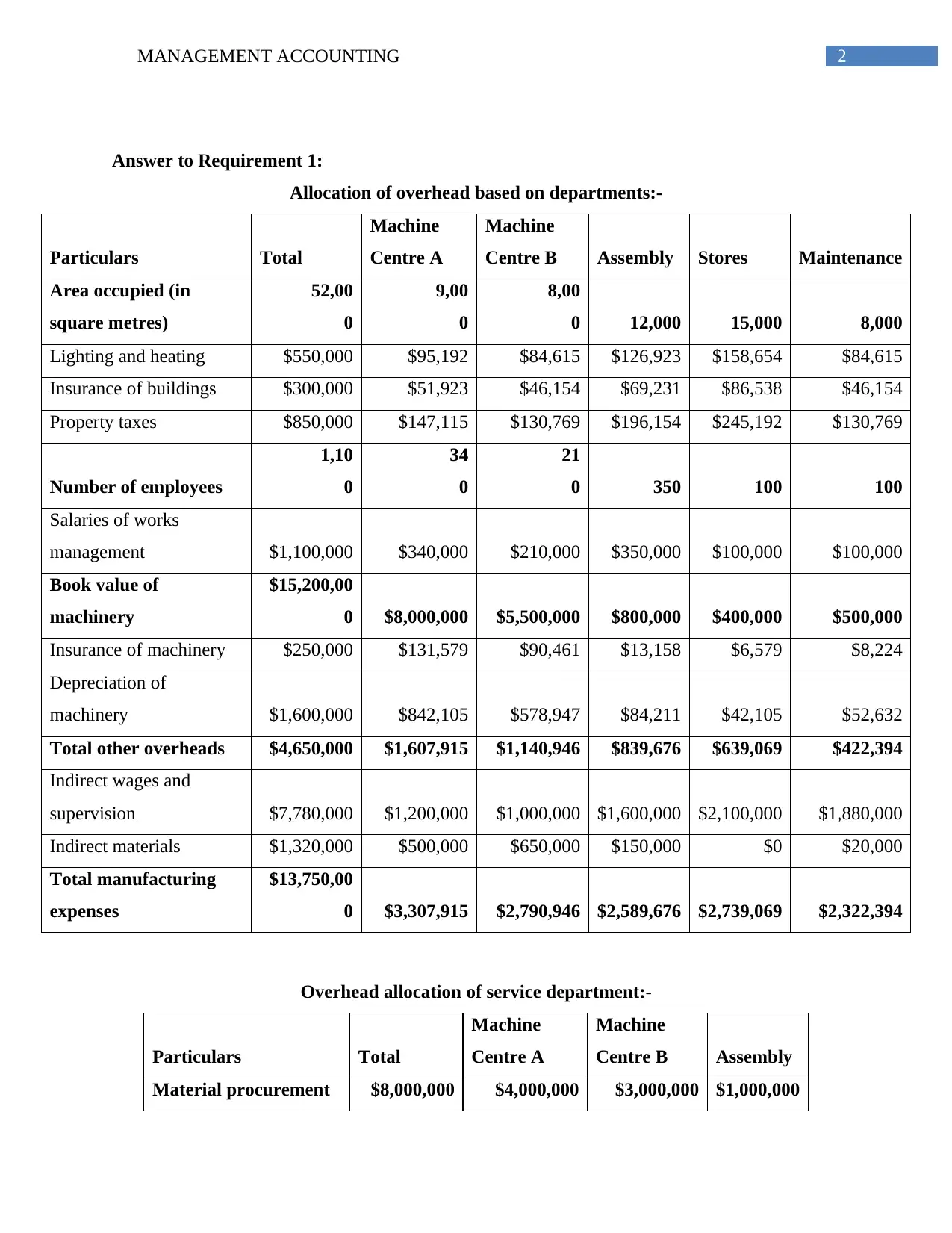

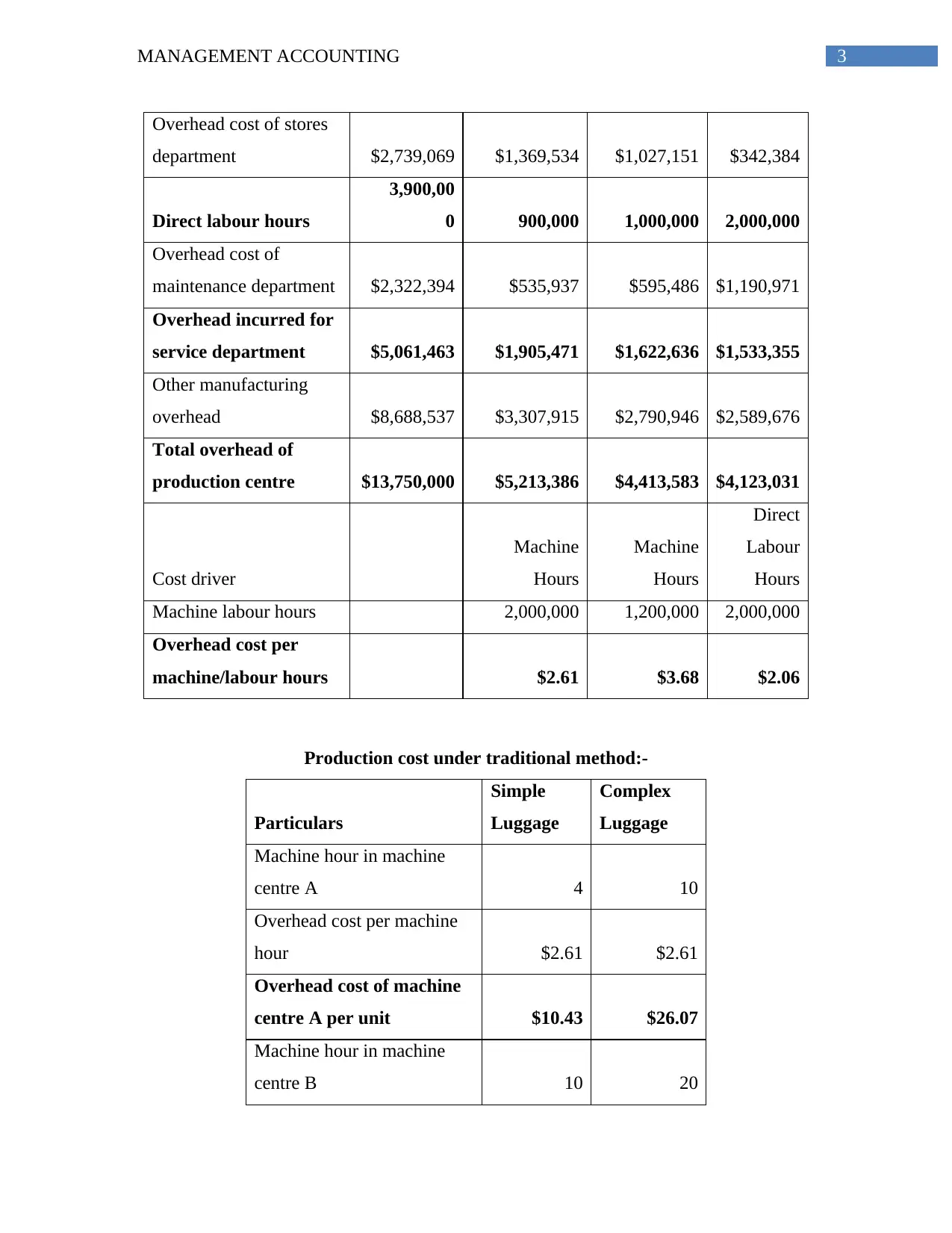

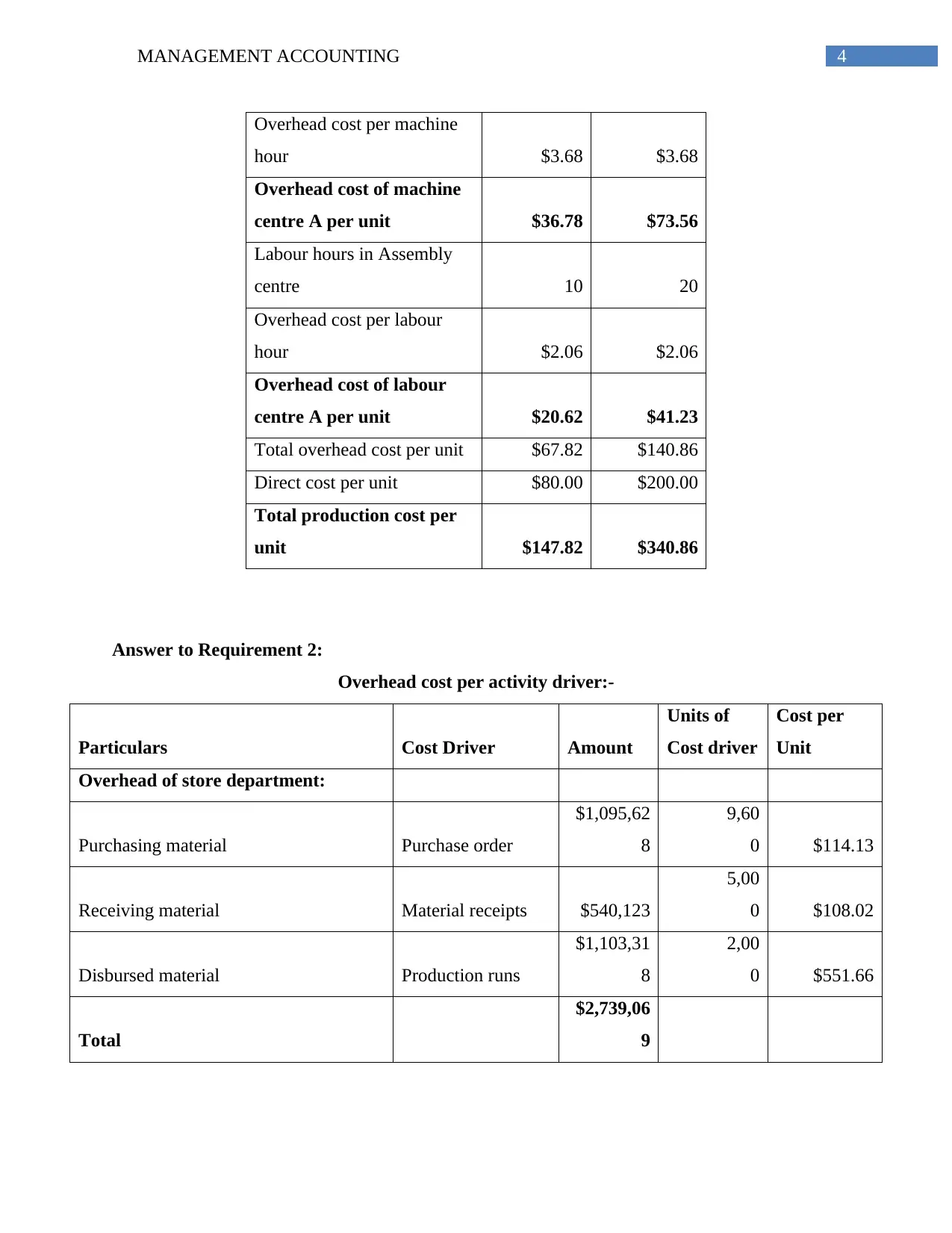

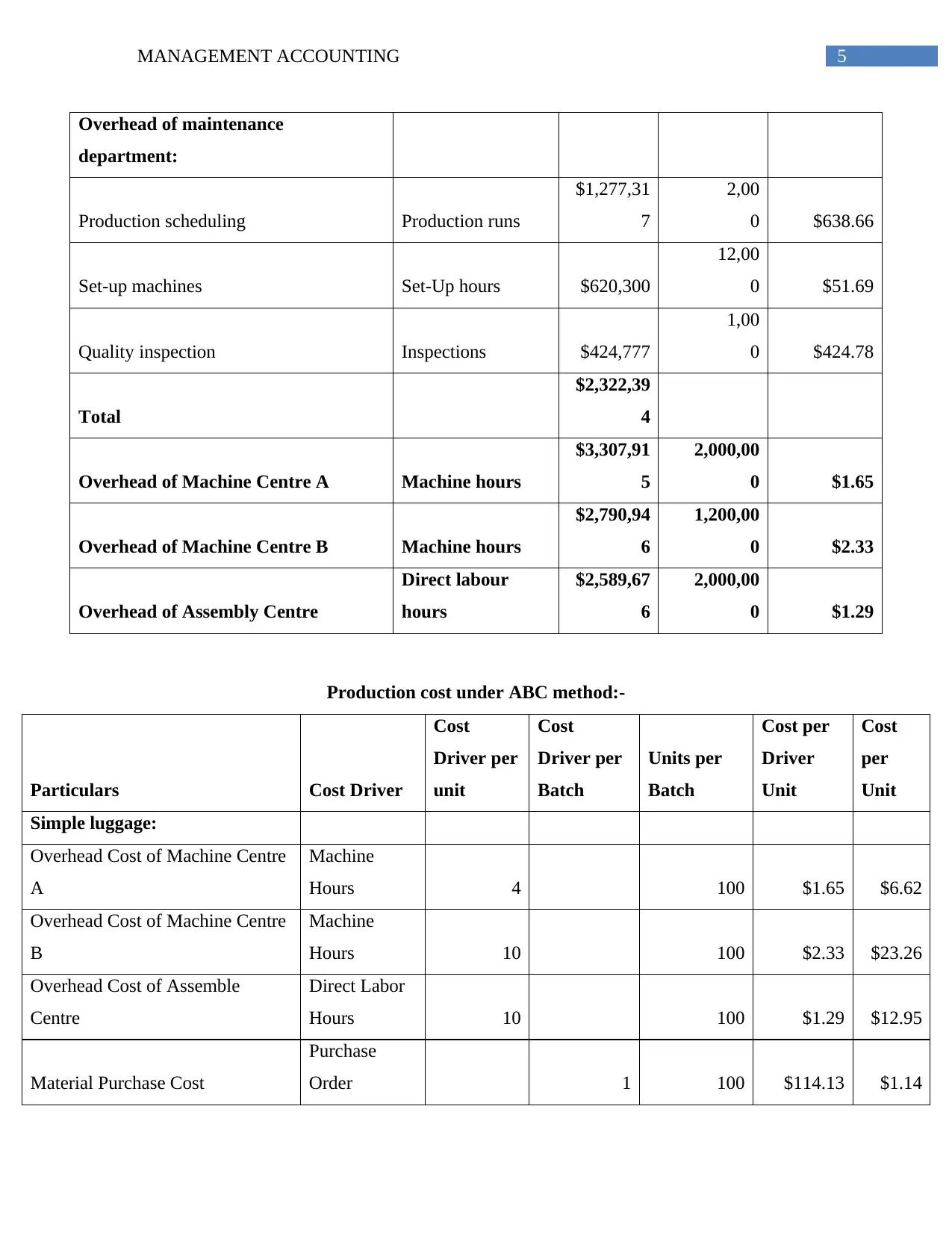

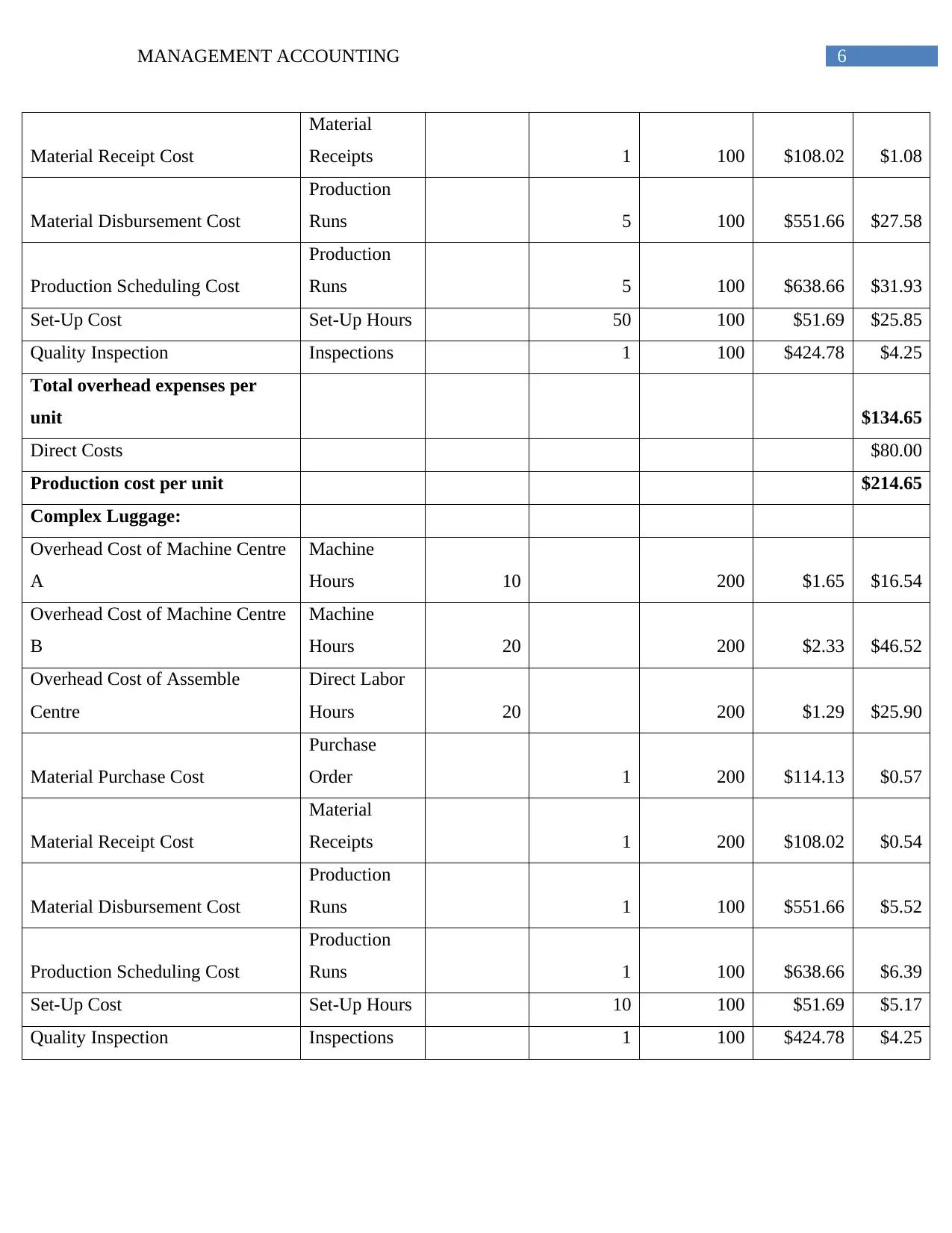

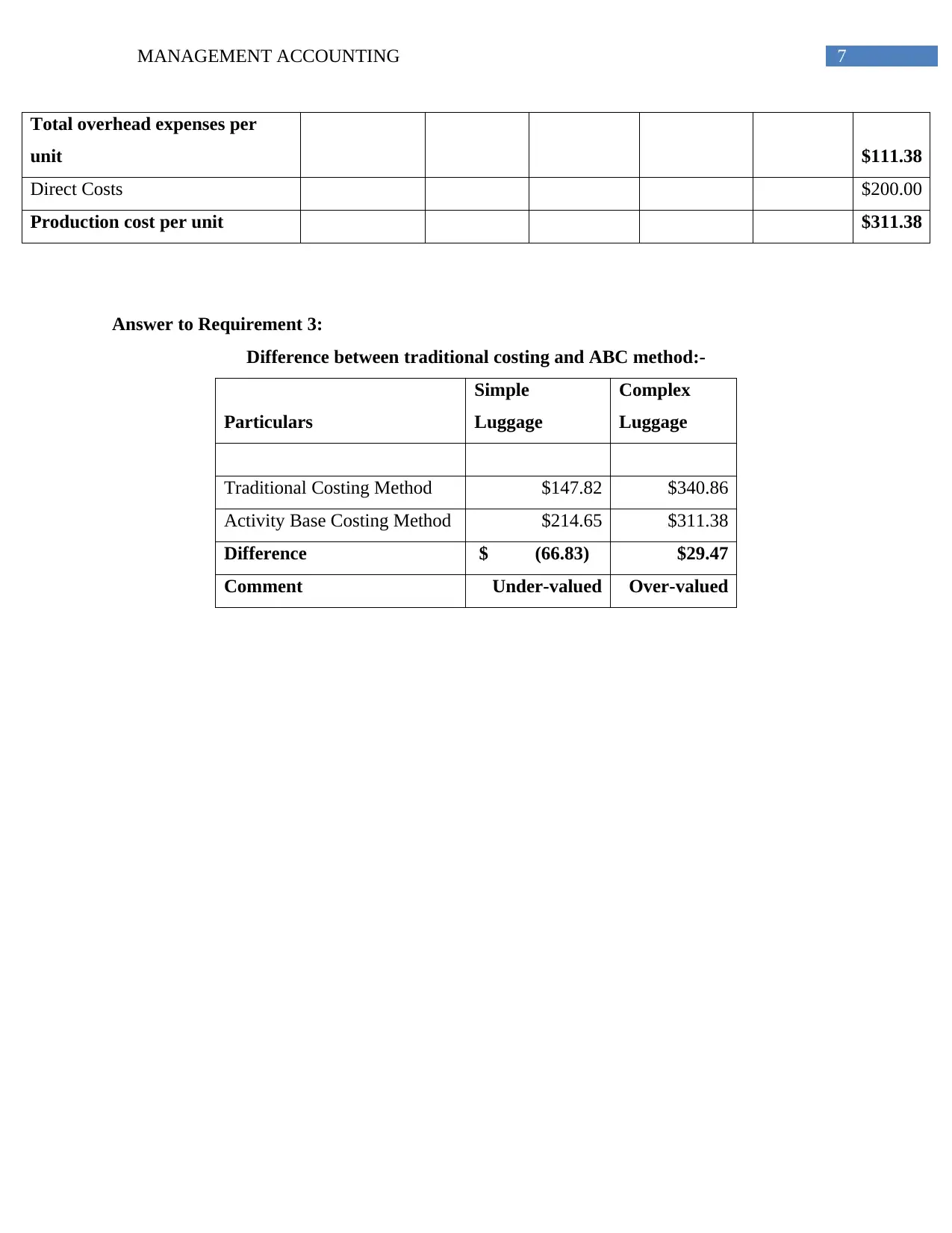

This report provides a detailed analysis of management accounting principles, focusing on cost allocation and the comparison between traditional costing and activity-based costing (ABC). The report begins by allocating overhead costs across different departments based on various cost drivers such as area occupied, number of employees, and machine hours. It then delves into the traditional costing method, calculating the production cost per unit for both simple and complex luggage. Subsequently, the report transitions to the ABC method, identifying activity drivers and calculating overhead costs per unit for different activities within the store and maintenance departments. Finally, it compares the results of the traditional costing and ABC methods, highlighting the differences in cost allocation and the impact on the valuation of simple and complex luggage. The report concludes with a discussion of the advantages and disadvantages of each method, along with relevant bibliographical references.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.