Comprehensive Management Accounting Report: Herbert Johnson Ltd

VerifiedAdded on 2021/02/20

|17

|4080

|23

Report

AI Summary

This report analyzes management accounting practices, focusing on Herbert Johnson Ltd. It begins with an introduction to management accounting, differentiating it from financial accounting, and exploring various systems like inventory management and cost accounting. The report then delves into management accounting reporting, detailing features of financial data and different report types. Cost and costing methods, including marginal and absorption costing, are examined, alongside budgetary control and planning tools. Financial problems and governance are addressed, highlighting the characteristics and skills of an effective management accountant. The report covers topics such as cost analysis, cost-volume-profit analysis, flexible budgeting, and the preparation of income statements using both marginal and absorption costing methods. Furthermore, the report examines various types of budgets, including capital and operating budgets, and discusses pricing strategies and SWOT analysis, providing a comprehensive overview of management accounting principles and their practical application.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Management Accounting System:..........................................................................................3

Management Accounting:......................................................................................................3

Management Accounting Systems:........................................................................................4

Benefits of management accounting systems:........................................................................5

P2 Management Accounting Reporting:......................................................................................5

Features of Financial Data:.....................................................................................................5

Different types of reports .......................................................................................................6

TASK 2............................................................................................................................................6

P3 Cost and Costing Methods:.....................................................................................................6

Cost: .......................................................................................................................................6

Income statement using marginal costing..............................................................................8

Income statement using Absorption Costing........................................................................10

TASK 3..........................................................................................................................................11

P4 Budgetary control and Planning tools:.................................................................................11

Budget: ................................................................................................................................11

Pricing Strategies:.................................................................................................................12

Common Costing Systems:..................................................................................................13

SWOT Analysis:...................................................................................................................13

TASK 4..........................................................................................................................................14

P5 Financial Problems and Financial Governance:...................................................................14

Financial Problems...............................................................................................................14

Financial Governance:..........................................................................................................15

Characteristics and Skills of effective management accountant:.........................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Management Accounting System:..........................................................................................3

Management Accounting:......................................................................................................3

Management Accounting Systems:........................................................................................4

Benefits of management accounting systems:........................................................................5

P2 Management Accounting Reporting:......................................................................................5

Features of Financial Data:.....................................................................................................5

Different types of reports .......................................................................................................6

TASK 2............................................................................................................................................6

P3 Cost and Costing Methods:.....................................................................................................6

Cost: .......................................................................................................................................6

Income statement using marginal costing..............................................................................8

Income statement using Absorption Costing........................................................................10

TASK 3..........................................................................................................................................11

P4 Budgetary control and Planning tools:.................................................................................11

Budget: ................................................................................................................................11

Pricing Strategies:.................................................................................................................12

Common Costing Systems:..................................................................................................13

SWOT Analysis:...................................................................................................................13

TASK 4..........................................................................................................................................14

P5 Financial Problems and Financial Governance:...................................................................14

Financial Problems...............................................................................................................14

Financial Governance:..........................................................................................................15

Characteristics and Skills of effective management accountant:.........................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

Business activities and operations are more diverse and complex nowadays and cost

accounting method is not enough to calculate little costs. The economic and business world

needs a effective system which can help in managing, assessing and controlling overall internal

business processes. For this purpose, the method or framework that has been developed is

management accounting that is also known as managerial accounting (Mistry, Sharma and Low,

2014).

Herbert Johnson (Hatters) which is a hat and caps manufacturing company situated in

Bond Street, London founded by Herbert Lewis Johnson in 1889 has been chosen to prepare this

report. This report will discuss about various management accounting systems management

accounting reports. It also involves understanding of different types of casts and costing

methods, budgets and planning tools and financial problems. Further, it describes financial

governance and characteristics and skills of managerial accountant.

TASK 1

P1 Management Accounting System:

Management Accounting:

Although there is not any specific definition for management accounting but in simple

words, it can be defined as a framework or overall process of collecting, filtering, classifying,

recording and reporting financial and non-financial data in such a manner that administration of a

firm can plan its strategies and make the decisions in an effective manner so that organizational

objectives and goals can be achieved successfully (Trigo, Belfo and Estébanez, 2016).

Managerial accounting concept was evolved at the beginning of nineteenth century to manage

and control the internal structure and components of the organizations. Management accounting

has some significant differences from financial accounting which are given below:

Management Accounting Financial Accounting

Data and information used and presented by

this accounting framework may be financial or

non-financial.

Financial accounting system always use and

provide financial data and information.

Business activities and operations are more diverse and complex nowadays and cost

accounting method is not enough to calculate little costs. The economic and business world

needs a effective system which can help in managing, assessing and controlling overall internal

business processes. For this purpose, the method or framework that has been developed is

management accounting that is also known as managerial accounting (Mistry, Sharma and Low,

2014).

Herbert Johnson (Hatters) which is a hat and caps manufacturing company situated in

Bond Street, London founded by Herbert Lewis Johnson in 1889 has been chosen to prepare this

report. This report will discuss about various management accounting systems management

accounting reports. It also involves understanding of different types of casts and costing

methods, budgets and planning tools and financial problems. Further, it describes financial

governance and characteristics and skills of managerial accountant.

TASK 1

P1 Management Accounting System:

Management Accounting:

Although there is not any specific definition for management accounting but in simple

words, it can be defined as a framework or overall process of collecting, filtering, classifying,

recording and reporting financial and non-financial data in such a manner that administration of a

firm can plan its strategies and make the decisions in an effective manner so that organizational

objectives and goals can be achieved successfully (Trigo, Belfo and Estébanez, 2016).

Managerial accounting concept was evolved at the beginning of nineteenth century to manage

and control the internal structure and components of the organizations. Management accounting

has some significant differences from financial accounting which are given below:

Management Accounting Financial Accounting

Data and information used and presented by

this accounting framework may be financial or

non-financial.

Financial accounting system always use and

provide financial data and information.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Internal stakeholders such as managers,

owners, board members are the users of

management accounting data.

Financial accounting provides its data for the

use of external stakeholders such as

shareholders, government, investors,

competitors, etc.

Managerial accounting do not follow any

specific formulas or formats in preparing and

recording the data.

Financial accounting is abide with legal

compliances to follow a pre-described format

for presentation of data and information.

Management Accounting Systems:

Managerial accounting system can be described as a technique that is used to manage the

internal functioning of an organization with the help of available financial as well as non-

financial data and information. Management accounting system for assessing different

departments and activities is developed by Herbert Johnson Ltd so that the management of the

company can manage and record the status of each and every activity. Various managerial

accounting system followed by the selected company are presented as under:

Inventory Management System: Inventory management system is primarily introduced

to identify the status of stocked goods whether it is raw or finished. This system helps the

management of the respective company in monitoring and recording every movement in the

stock. Manufacturing firms such as Herbert Johnson Ltd uses latest inventory management

system software to trace even the single unit of their production (Thomas, 2016).

Cost Accounting System: Cost accounting system is a method to trace and record the cost

that has been incurred at the various stages of production. This costing system helps the

management of chosen firm for identifying various direct and indirect costs of production so that

all the cost can be assigned to their specific cost centres and actual cost of inventory can be

calculated.

Price Optimisation System: Price optimisation system has been developed to identify the

price of the business offerings that customers wants to pay willingly. This system provides help

in understanding the customers' behaviour towards different rice range for various products and

services. The administration of the selected firm is capable to evaluate the maximum price for a

product which is profitable for the firm as well as affordable for the customers.

owners, board members are the users of

management accounting data.

Financial accounting provides its data for the

use of external stakeholders such as

shareholders, government, investors,

competitors, etc.

Managerial accounting do not follow any

specific formulas or formats in preparing and

recording the data.

Financial accounting is abide with legal

compliances to follow a pre-described format

for presentation of data and information.

Management Accounting Systems:

Managerial accounting system can be described as a technique that is used to manage the

internal functioning of an organization with the help of available financial as well as non-

financial data and information. Management accounting system for assessing different

departments and activities is developed by Herbert Johnson Ltd so that the management of the

company can manage and record the status of each and every activity. Various managerial

accounting system followed by the selected company are presented as under:

Inventory Management System: Inventory management system is primarily introduced

to identify the status of stocked goods whether it is raw or finished. This system helps the

management of the respective company in monitoring and recording every movement in the

stock. Manufacturing firms such as Herbert Johnson Ltd uses latest inventory management

system software to trace even the single unit of their production (Thomas, 2016).

Cost Accounting System: Cost accounting system is a method to trace and record the cost

that has been incurred at the various stages of production. This costing system helps the

management of chosen firm for identifying various direct and indirect costs of production so that

all the cost can be assigned to their specific cost centres and actual cost of inventory can be

calculated.

Price Optimisation System: Price optimisation system has been developed to identify the

price of the business offerings that customers wants to pay willingly. This system provides help

in understanding the customers' behaviour towards different rice range for various products and

services. The administration of the selected firm is capable to evaluate the maximum price for a

product which is profitable for the firm as well as affordable for the customers.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

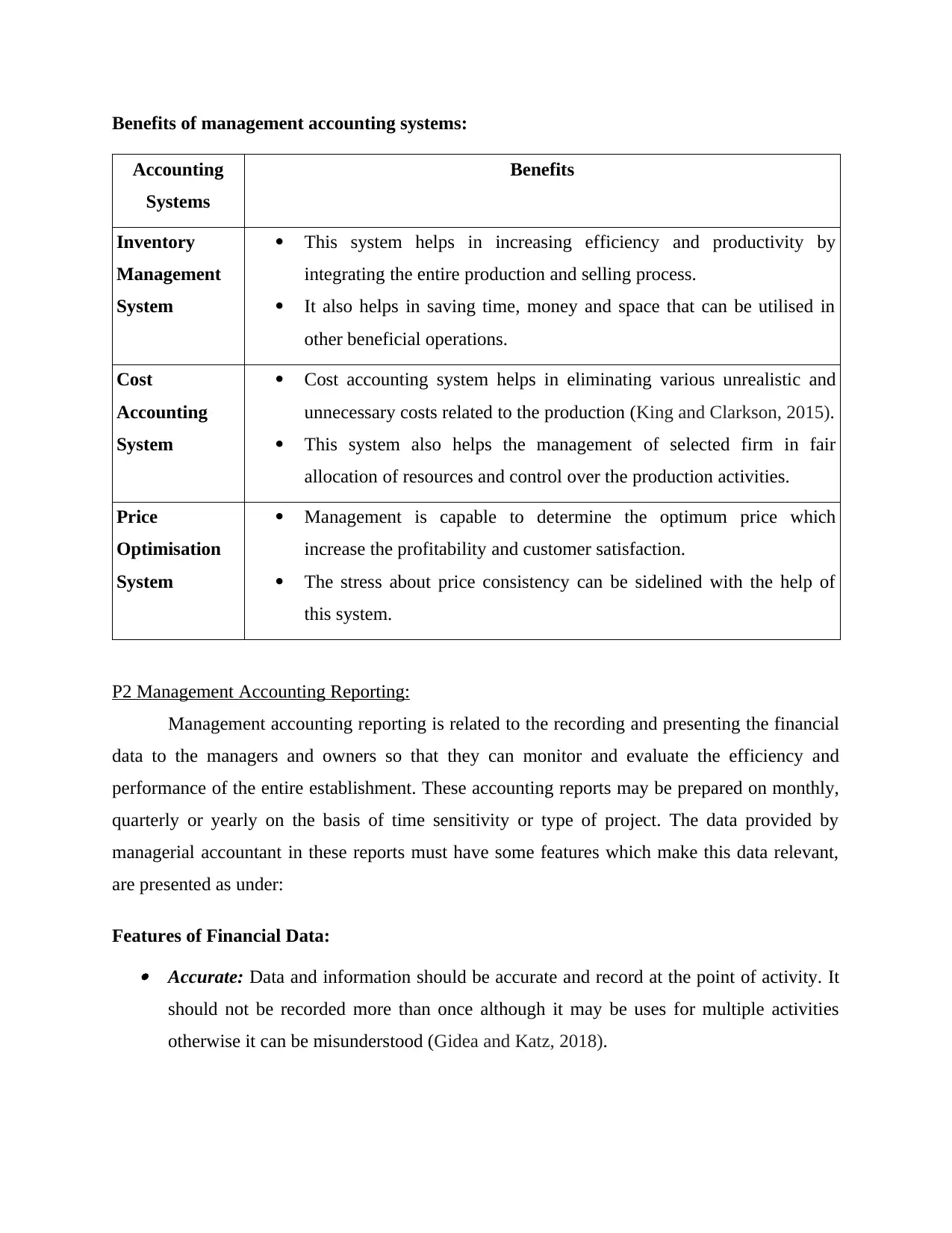

Benefits of management accounting systems:

Accounting

Systems

Benefits

Inventory

Management

System

This system helps in increasing efficiency and productivity by

integrating the entire production and selling process.

It also helps in saving time, money and space that can be utilised in

other beneficial operations.

Cost

Accounting

System

Cost accounting system helps in eliminating various unrealistic and

unnecessary costs related to the production (King and Clarkson, 2015).

This system also helps the management of selected firm in fair

allocation of resources and control over the production activities.

Price

Optimisation

System

Management is capable to determine the optimum price which

increase the profitability and customer satisfaction.

The stress about price consistency can be sidelined with the help of

this system.

P2 Management Accounting Reporting:

Management accounting reporting is related to the recording and presenting the financial

data to the managers and owners so that they can monitor and evaluate the efficiency and

performance of the entire establishment. These accounting reports may be prepared on monthly,

quarterly or yearly on the basis of time sensitivity or type of project. The data provided by

managerial accountant in these reports must have some features which make this data relevant,

are presented as under:

Features of Financial Data: Accurate: Data and information should be accurate and record at the point of activity. It

should not be recorded more than once although it may be uses for multiple activities

otherwise it can be misunderstood (Gidea and Katz, 2018).

Accounting

Systems

Benefits

Inventory

Management

System

This system helps in increasing efficiency and productivity by

integrating the entire production and selling process.

It also helps in saving time, money and space that can be utilised in

other beneficial operations.

Cost

Accounting

System

Cost accounting system helps in eliminating various unrealistic and

unnecessary costs related to the production (King and Clarkson, 2015).

This system also helps the management of selected firm in fair

allocation of resources and control over the production activities.

Price

Optimisation

System

Management is capable to determine the optimum price which

increase the profitability and customer satisfaction.

The stress about price consistency can be sidelined with the help of

this system.

P2 Management Accounting Reporting:

Management accounting reporting is related to the recording and presenting the financial

data to the managers and owners so that they can monitor and evaluate the efficiency and

performance of the entire establishment. These accounting reports may be prepared on monthly,

quarterly or yearly on the basis of time sensitivity or type of project. The data provided by

managerial accountant in these reports must have some features which make this data relevant,

are presented as under:

Features of Financial Data: Accurate: Data and information should be accurate and record at the point of activity. It

should not be recorded more than once although it may be uses for multiple activities

otherwise it can be misunderstood (Gidea and Katz, 2018).

Relevant: Data recorded in the reports should be relevant to the purpose for which it is

being provided. For this, it is necessary to review the requirements periodically so that

management can make effective decisions.

Trustworthy: The sources from where the data has been conducted must be reliable,

consistent and stable. The methods and approaches for collecting the data should not be

changed as it may effect the assessment of the performance.

There are various types of reports prepared by Herbert Johnson Ltd which help its

management to evaluate the performance of employees as well as the organization which are

described below:

Different types of reports

Performance Report: A performance report is created to evaluate the outcome or

performance of an activity or individual. This report involves comparison between actual

outcomes and standard measurements and try to find out the variances. It also helps in deriving

the reasons behind those deviations and try to fix them if results are adverse in nature.

Accounts Receivable aging report: This report is a critical tool used by those companies

which conduct their business on credit terms. This report provides help in managing cash flow of

the organization by keeping a record of the customers, their owes, interest on late payments, etc.

This report is considered to evaluate and tightening of credit policies and increase debtor

turnover ratio (Takeda and Boyns, 2014).

Inventory management report: These reports are mostly generated by manufacturing and

retail companies such as Herbert Johnson Ltd in order to make their production process more

efficient. The managers of the establishment can compare various production stages and

assembly lines to find out the operations, activities and processes that can be improved.

TASK 2

P3 Cost and Costing Methods:

Cost:

Cost can be defined as the amount or value that has been bared by the manufacturer or

seller in order to sell the business offerings i.e. products and services. It includes all the expenses

being provided. For this, it is necessary to review the requirements periodically so that

management can make effective decisions.

Trustworthy: The sources from where the data has been conducted must be reliable,

consistent and stable. The methods and approaches for collecting the data should not be

changed as it may effect the assessment of the performance.

There are various types of reports prepared by Herbert Johnson Ltd which help its

management to evaluate the performance of employees as well as the organization which are

described below:

Different types of reports

Performance Report: A performance report is created to evaluate the outcome or

performance of an activity or individual. This report involves comparison between actual

outcomes and standard measurements and try to find out the variances. It also helps in deriving

the reasons behind those deviations and try to fix them if results are adverse in nature.

Accounts Receivable aging report: This report is a critical tool used by those companies

which conduct their business on credit terms. This report provides help in managing cash flow of

the organization by keeping a record of the customers, their owes, interest on late payments, etc.

This report is considered to evaluate and tightening of credit policies and increase debtor

turnover ratio (Takeda and Boyns, 2014).

Inventory management report: These reports are mostly generated by manufacturing and

retail companies such as Herbert Johnson Ltd in order to make their production process more

efficient. The managers of the establishment can compare various production stages and

assembly lines to find out the operations, activities and processes that can be improved.

TASK 2

P3 Cost and Costing Methods:

Cost:

Cost can be defined as the amount or value that has been bared by the manufacturer or

seller in order to sell the business offerings i.e. products and services. It includes all the expenses

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and overheads from the purchase of raw material to selling and distribution as well as

administrative charges. There are various types of costs that are mentioned below: Direct cost: A direct cost is the value of cost that can be attributed to the production

process completely such as direct labour, direct material, manufacturing overheads, etc. Indirect cost: The costs which are difficult to assign directly to the production line or

cost objects are known as indirect cost like, depreciation, administrative charges, etc. Fixed cost: A cost or expenses that remains unchanged or do not fluctuate with the

output level of production is called fixed cost. These costs have to be bared even when

there is no production within the firm like Interest, salaries, rent, etc.

Variable cost: The costs that changes or fluctuate with the production level and remains

zero when there is no production are called variable costs such as wages, bonus, etc.

Cost Analysis: Cost analysis is a method of comparing the actual cost with the budgeted

cost or a periodic cost with the another period cost so that disclosing and reporting on conditions

can be improved (Cost variance, 2019).

Cost Volume profit: This analysis method is a tool that evaluate the impact costing have

upon the operating profit. It is also known as break-even analysis which is used to determine the

break-even point of sales and cost structure so that management of the selected firm can make

short-term economic decisions.

Flexible Budgeting: Flexible budgeting is a method of prepare financial plan that flex or

varies according to the organizational requirements. Flexible budget allows the management to

alter the overheads that vary with revenues. This budget is consider as more relevant to the fixed

or static budget because:

Performance of the company can be predicted wit greater accuracy.

Make it easy to evaluate the results of specific department more properly.

Budget for various activities can be altered to indicate changing conditions.

Marginal Costing: Marginal costing is a method that determine the cost of

manufacturing one additional unit of product. This costing method is used to define the

maximum production capability of the organization. This costing method assigned all variable

costs to the production units while all the fixed overheads are set-off from the contribution.

administrative charges. There are various types of costs that are mentioned below: Direct cost: A direct cost is the value of cost that can be attributed to the production

process completely such as direct labour, direct material, manufacturing overheads, etc. Indirect cost: The costs which are difficult to assign directly to the production line or

cost objects are known as indirect cost like, depreciation, administrative charges, etc. Fixed cost: A cost or expenses that remains unchanged or do not fluctuate with the

output level of production is called fixed cost. These costs have to be bared even when

there is no production within the firm like Interest, salaries, rent, etc.

Variable cost: The costs that changes or fluctuate with the production level and remains

zero when there is no production are called variable costs such as wages, bonus, etc.

Cost Analysis: Cost analysis is a method of comparing the actual cost with the budgeted

cost or a periodic cost with the another period cost so that disclosing and reporting on conditions

can be improved (Cost variance, 2019).

Cost Volume profit: This analysis method is a tool that evaluate the impact costing have

upon the operating profit. It is also known as break-even analysis which is used to determine the

break-even point of sales and cost structure so that management of the selected firm can make

short-term economic decisions.

Flexible Budgeting: Flexible budgeting is a method of prepare financial plan that flex or

varies according to the organizational requirements. Flexible budget allows the management to

alter the overheads that vary with revenues. This budget is consider as more relevant to the fixed

or static budget because:

Performance of the company can be predicted wit greater accuracy.

Make it easy to evaluate the results of specific department more properly.

Budget for various activities can be altered to indicate changing conditions.

Marginal Costing: Marginal costing is a method that determine the cost of

manufacturing one additional unit of product. This costing method is used to define the

maximum production capability of the organization. This costing method assigned all variable

costs to the production units while all the fixed overheads are set-off from the contribution.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

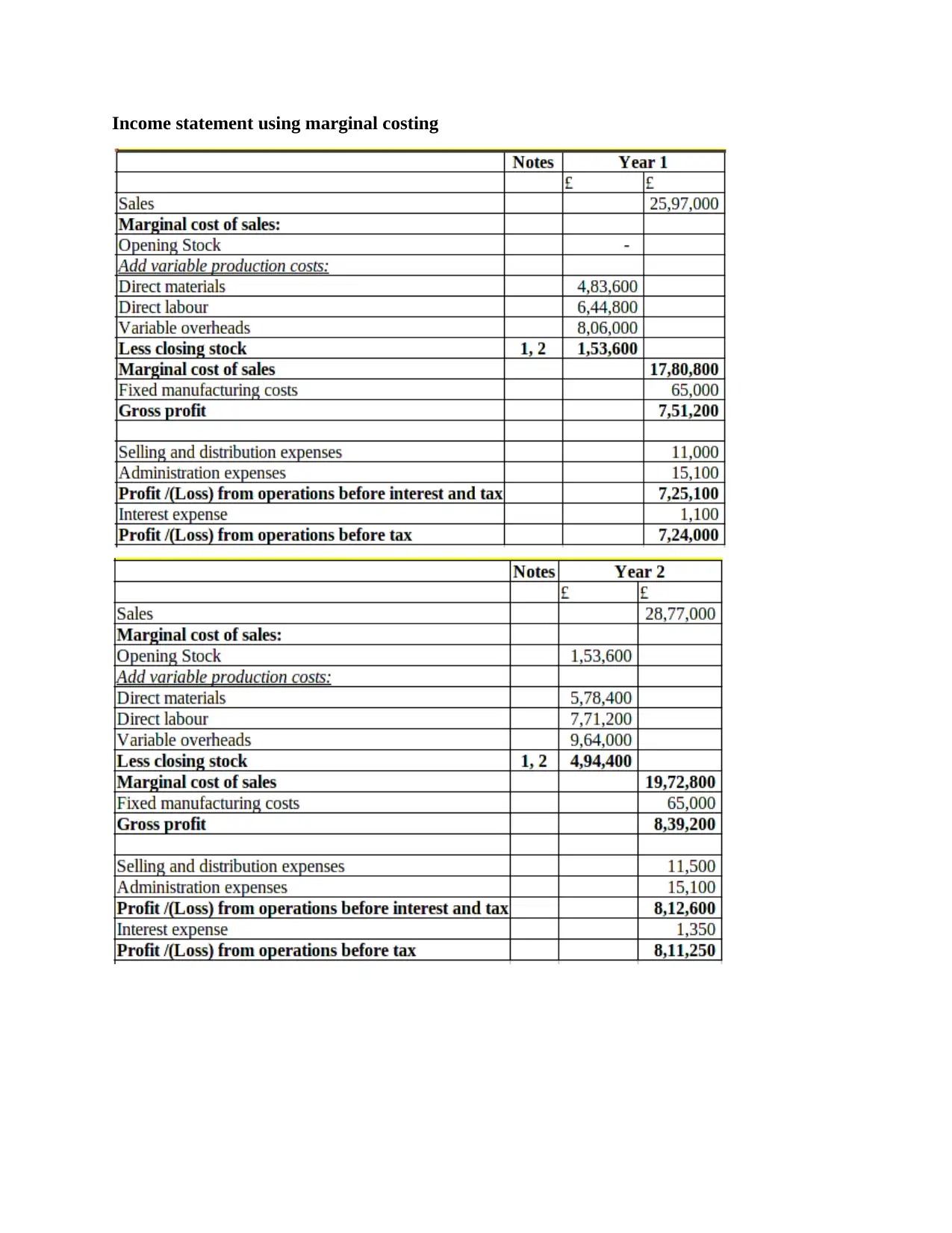

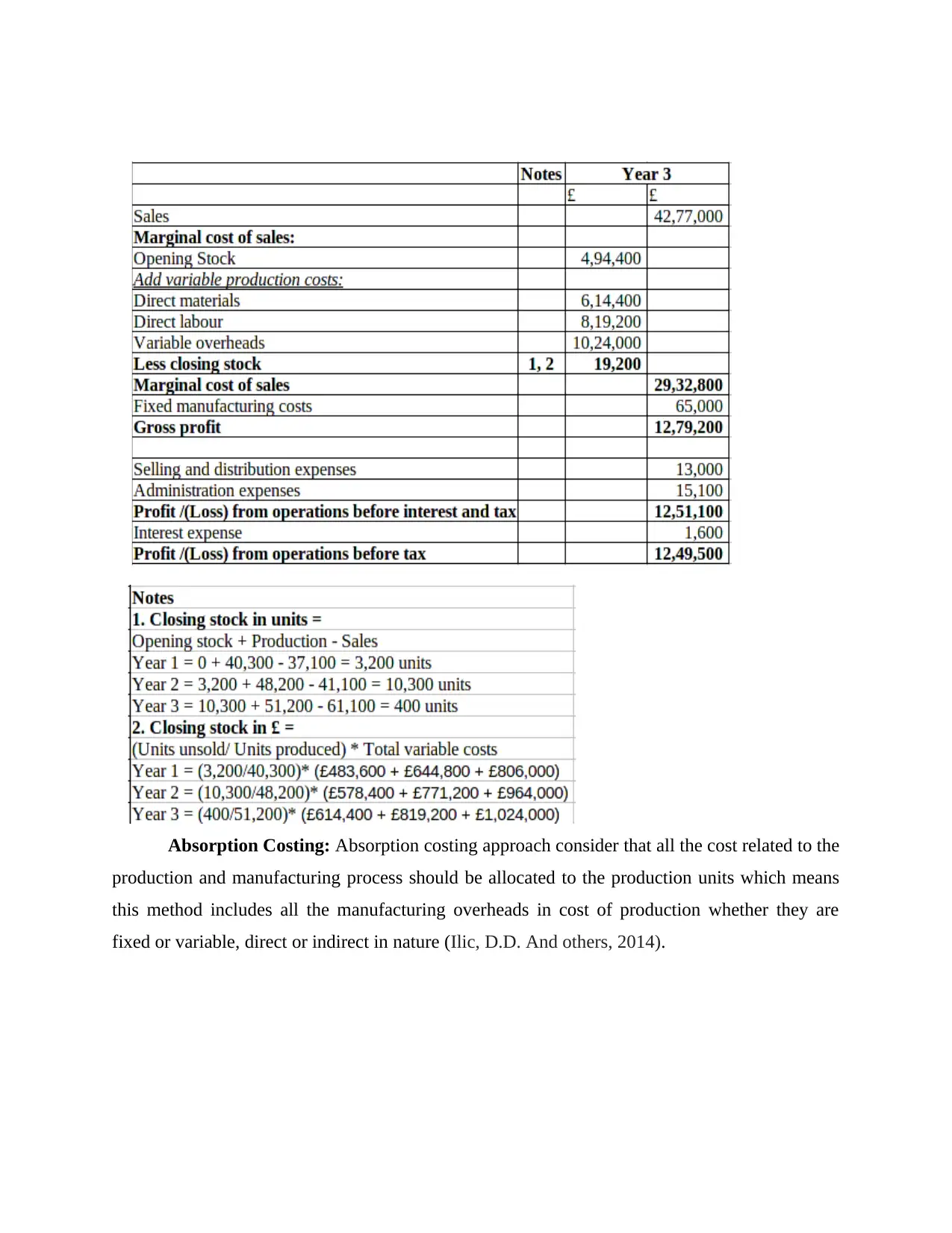

Income statement using marginal costing

Absorption Costing: Absorption costing approach consider that all the cost related to the

production and manufacturing process should be allocated to the production units which means

this method includes all the manufacturing overheads in cost of production whether they are

fixed or variable, direct or indirect in nature (Ilic, D.D. And others, 2014).

production and manufacturing process should be allocated to the production units which means

this method includes all the manufacturing overheads in cost of production whether they are

fixed or variable, direct or indirect in nature (Ilic, D.D. And others, 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

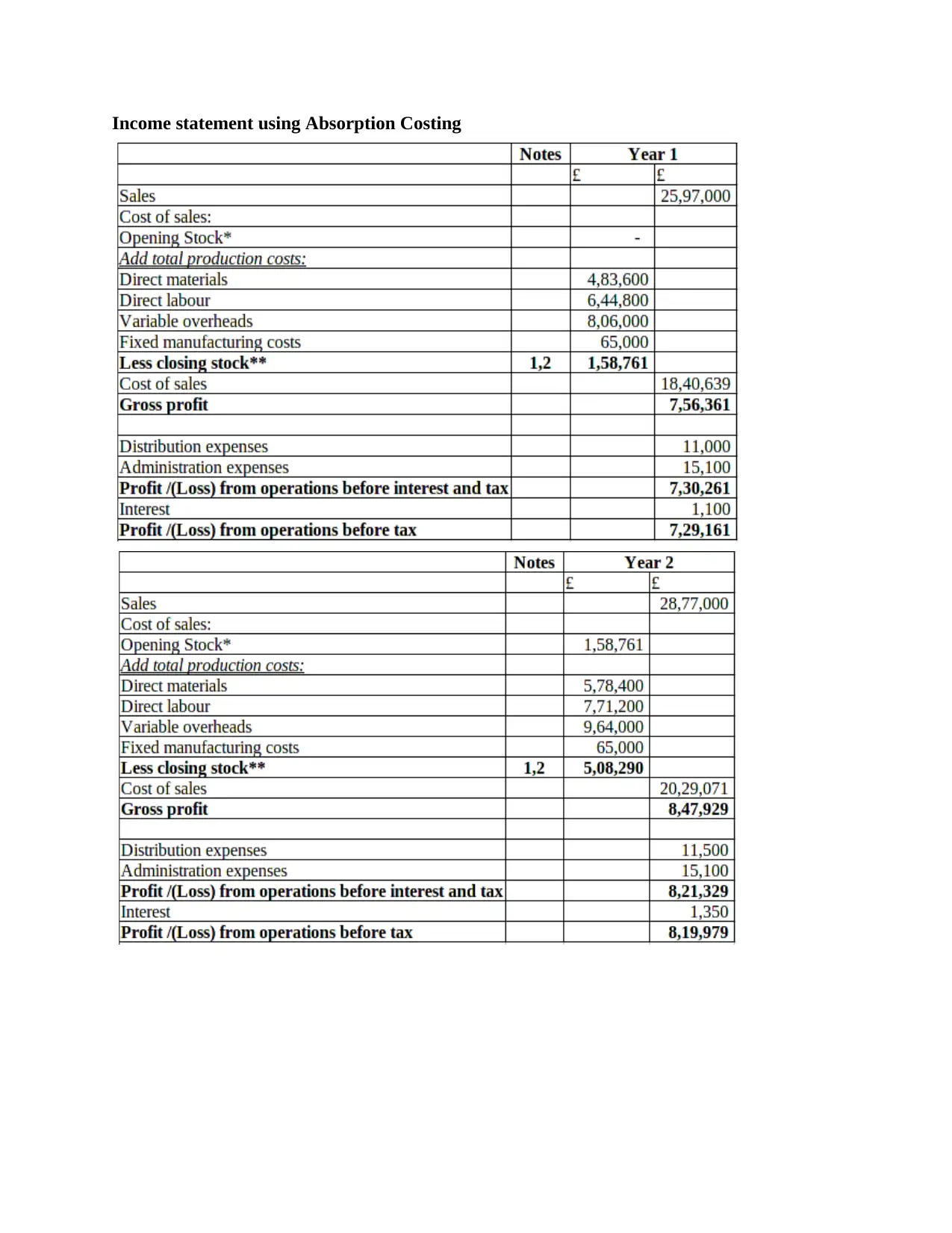

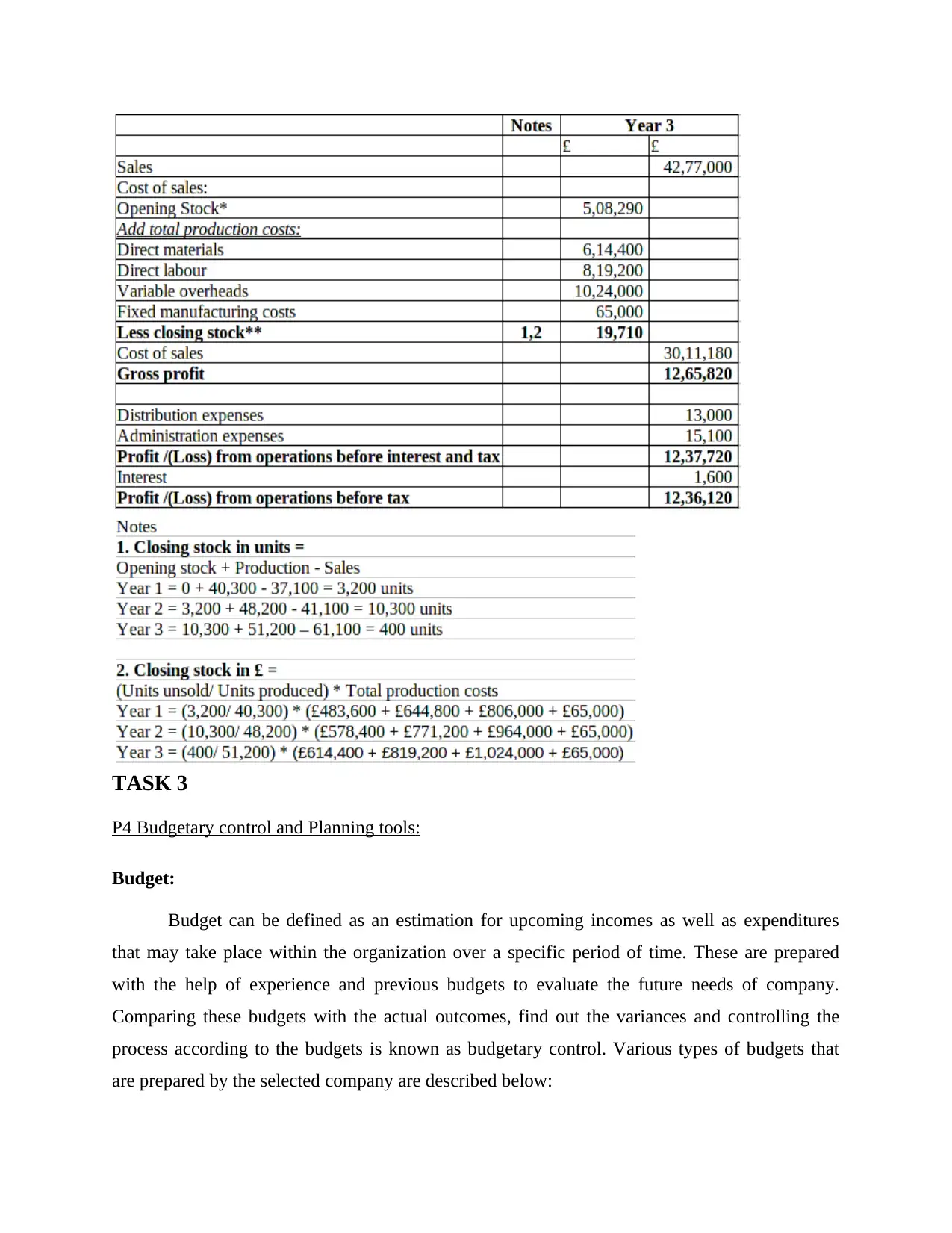

Income statement using Absorption Costing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 3

P4 Budgetary control and Planning tools:

Budget:

Budget can be defined as an estimation for upcoming incomes as well as expenditures

that may take place within the organization over a specific period of time. These are prepared

with the help of experience and previous budgets to evaluate the future needs of company.

Comparing these budgets with the actual outcomes, find out the variances and controlling the

process according to the budgets is known as budgetary control. Various types of budgets that

are prepared by the selected company are described below:

P4 Budgetary control and Planning tools:

Budget:

Budget can be defined as an estimation for upcoming incomes as well as expenditures

that may take place within the organization over a specific period of time. These are prepared

with the help of experience and previous budgets to evaluate the future needs of company.

Comparing these budgets with the actual outcomes, find out the variances and controlling the

process according to the budgets is known as budgetary control. Various types of budgets that

are prepared by the selected company are described below:

Capital Budget: Capital budget is prepared to evaluate the future transactions of the firm

which are related to the capital income and expenditures. This budget includes purchase or sale

of fixed assets, payment of loan or debentures, capital borrowings, etc. this budget helps in

evaluating if an investment plan is profitable for the organization or not.

Operating Budget: A detailed estimation of operational transactions related to the

income and expenditures that are based on estimated sales for a particular period is known as

operating budget. Operating budget is related to the short-term transactions hence it does not

include any capital related income or expense (Bradbury, Pratson and Patiño-Echeverri, 2014).

Zero-based Budget: It is a new approach of preparing budget which develop a budget

without taking any help from previous budgets and calculate all the income and expenditures by

itself. This budget justifies each and every cost and increment in costs and avoid all the cost

which do not have any significance that ultimately reduces the cost of production.

Pricing Strategies:

Pricing: the activity of fixing a value or amount that will be charged for providing a

product or service is known as pricing. Price is the most significant factor that affect the demand

and supply. Other factors that have impact over demand and supply are listed below:

Price fluctuation

market trends

Income and credits

commercial advertisement

Availability of substitutes

seasons

There are some pricing strategies presented below:

Premium pricing: Premium pricing policies are implemented and work in a industry or

segment where strong competitive benefits exists for the organization in the market such as

Gillette in blade industry and Porsche in auto mobile sector.

Economic Pricing: Economic pricing method is used where the organization wants to

build up a strong customer base and for that provide its products and services without frilling in

price and on lowest profit margin like local tea manufacturers (Davcik and Sharma, 2015).

which are related to the capital income and expenditures. This budget includes purchase or sale

of fixed assets, payment of loan or debentures, capital borrowings, etc. this budget helps in

evaluating if an investment plan is profitable for the organization or not.

Operating Budget: A detailed estimation of operational transactions related to the

income and expenditures that are based on estimated sales for a particular period is known as

operating budget. Operating budget is related to the short-term transactions hence it does not

include any capital related income or expense (Bradbury, Pratson and Patiño-Echeverri, 2014).

Zero-based Budget: It is a new approach of preparing budget which develop a budget

without taking any help from previous budgets and calculate all the income and expenditures by

itself. This budget justifies each and every cost and increment in costs and avoid all the cost

which do not have any significance that ultimately reduces the cost of production.

Pricing Strategies:

Pricing: the activity of fixing a value or amount that will be charged for providing a

product or service is known as pricing. Price is the most significant factor that affect the demand

and supply. Other factors that have impact over demand and supply are listed below:

Price fluctuation

market trends

Income and credits

commercial advertisement

Availability of substitutes

seasons

There are some pricing strategies presented below:

Premium pricing: Premium pricing policies are implemented and work in a industry or

segment where strong competitive benefits exists for the organization in the market such as

Gillette in blade industry and Porsche in auto mobile sector.

Economic Pricing: Economic pricing method is used where the organization wants to

build up a strong customer base and for that provide its products and services without frilling in

price and on lowest profit margin like local tea manufacturers (Davcik and Sharma, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.