Management Accounting Analysis: UCK Furniture Budgeting and Financials

VerifiedAdded on 2023/01/12

|10

|2572

|66

Report

AI Summary

This report delves into the application of management accounting principles, specifically focusing on UCK Furniture. It begins with an introduction to management accounting, emphasizing its role in providing financial and quantitative information for decision-making, contrasting it with financial accounting's historical perspective. The main body of the report explores budgeting, defining its purpose and types, including cash, master, and flexible budgets, with their respective advantages and disadvantages. It provides a practical example of cash budget preparation. The report further examines how management accounting systems, such as inventory and cost management, help organizations address financial problems, and analyzes how these systems can enhance financial performance. The analysis includes key financial ratios like Return on Capital Employed, asset turnover and operating profit margin, to evaluate the performance of different divisions within UCK Furniture. Planning tools like budgetary control and ratio analysis are also evaluated in reducing financial issues. The conclusion summarizes the key findings and the importance of management accounting in achieving sustainable success. The report emphasizes the use of these techniques to improve operational efficiency and financial outcomes.

Management

Accounting

1

Accounting

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

PART 2............................................................................................................................................3

3.1 Explain purpose of budget and prepare different budget.......................................................3

4.1 Compare how organization following management accounting systems to resolve their

financial problem.........................................................................................................................8

4.2 Analyse how management accounting can improve the financial performance of both

companies to achieve the sustainable success.............................................................................8

4.3 Evaluate the planning tools used in management accounting to reduce the financial issues

to achieve success........................................................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

2

MAIN BODY..................................................................................................................................3

PART 2............................................................................................................................................3

3.1 Explain purpose of budget and prepare different budget.......................................................3

4.1 Compare how organization following management accounting systems to resolve their

financial problem.........................................................................................................................8

4.2 Analyse how management accounting can improve the financial performance of both

companies to achieve the sustainable success.............................................................................8

4.3 Evaluate the planning tools used in management accounting to reduce the financial issues

to achieve success........................................................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

2

INTRODUCTION

Management accounting includes the planning and adequate delivery of financial and

quantitative information to business executives so they can make day to day and short term

strategic decisions (Dierynck and Labro, 2018). In a variety of aspects, knowledge found in

management accounting varies considerably from that of financial accounting. Although reports

on financial statements appear to be focused on historical evidence, reports on the management

are largely forward thinking. This report is based on UCK furniture which adopts several

management accounting techniques to improve their operational efficiency and the purpose of

budgeting that how it is beneficial for the organizations.

MAIN BODY

PART 2

3.1 Explain purpose of budget and prepare different budget

Budget is a structured forecast revenue and expenditure document focused on projected

expectations and goals. In certain words, a plan is a report made by management to forecast

revenues and expenditures for the upcoming year that is based on their business objectives. Lots

of various types of budgets vary from short and long-term to agency specific. Management

should create a budget for whatever. The main thing to remember is that these plans are actually

just the potential expectations and strategies written down in financial form by the management

for the company.

Purpose of budget: Budgeting purposes are for allocating, organizing, arranging,

managing and empowering capital. It is also an essential method for decision-making, market

performance reporting and revenue and expense forecasting (Gomez-Conde And et.al., 2019).

Valuable resources are handled effectively, through proper budgeting. Below mention some

specific purpose help the managers of UCK furniture to produce budget and perform effectively

to maximise the productivity as well as profitability. All are as follow:

Budget is an instrument for the planning and execution of short-range plans.

This is a tool to convey certain plans to the managers of the accountability centre.

Budget is a way to motivate managers to accomplish their goals at the centres of

responsibility.

Controlling ongoing operations is a standard.

3

Management accounting includes the planning and adequate delivery of financial and

quantitative information to business executives so they can make day to day and short term

strategic decisions (Dierynck and Labro, 2018). In a variety of aspects, knowledge found in

management accounting varies considerably from that of financial accounting. Although reports

on financial statements appear to be focused on historical evidence, reports on the management

are largely forward thinking. This report is based on UCK furniture which adopts several

management accounting techniques to improve their operational efficiency and the purpose of

budgeting that how it is beneficial for the organizations.

MAIN BODY

PART 2

3.1 Explain purpose of budget and prepare different budget

Budget is a structured forecast revenue and expenditure document focused on projected

expectations and goals. In certain words, a plan is a report made by management to forecast

revenues and expenditures for the upcoming year that is based on their business objectives. Lots

of various types of budgets vary from short and long-term to agency specific. Management

should create a budget for whatever. The main thing to remember is that these plans are actually

just the potential expectations and strategies written down in financial form by the management

for the company.

Purpose of budget: Budgeting purposes are for allocating, organizing, arranging,

managing and empowering capital. It is also an essential method for decision-making, market

performance reporting and revenue and expense forecasting (Gomez-Conde And et.al., 2019).

Valuable resources are handled effectively, through proper budgeting. Below mention some

specific purpose help the managers of UCK furniture to produce budget and perform effectively

to maximise the productivity as well as profitability. All are as follow:

Budget is an instrument for the planning and execution of short-range plans.

This is a tool to convey certain plans to the managers of the accountability centre.

Budget is a way to motivate managers to accomplish their goals at the centres of

responsibility.

Controlling ongoing operations is a standard.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The budget acts as a framework for evaluating the success of accountability centres and

their administrators.

Above mention budgeting purpose help the UCK’s managers to estimate income and

expenditure according to the operational activities. It is also beneficial to evaluating overall

performance of the company in comparison to last year performance or with their competitors.

Different types of budget along with advantage or disadvantage:

Cash budget: Cash budget is a plan or schedule for forecasted cash collections and

payments over the year. Other money inflows and outflows involve income received, expenses

charged, and refunds and payments for loans. In other words, capital budgeting is a projected

future financial situation forecast of the business. Management creates the cash budget after the

budgets for revenues, acquisitions, and capital expenses have already been made. Such forecasts

must be made in advance of the cash budget to accurately predict how the cash will be impacted

over the time. For example, manager of UCK furniture needs to have an estimation of revenue so

it can determine how often cash will be gathered over the era. Management using the cash

budget to control a company's cash flows.

Advantage: There are also benefits of using cash budgeting. This method helps to assess

whether cash balances are adequate to meet daily obligations and if the necessary criteria for

stability and cash balance specified by banking or internal company regulations are preserved

(Laela And et.al., 2018). It also lets an organization decide whether it holds too much money that

could otherwise be invested in productive things. Companies that lend from banks have to track

their ratio of cash coverage and plan a cash budget is the first phase in measuring that ratio.

Disadvantage: Cash budgets can trigger errors, too. Cash inflows aren't efficient. Cash

inflows arising from bond transactions, penalties, asset sales, or other one-off, semi-sustainable

operation do not generally reflect credible additional revenue sources. Decreased cash flow not

need always be a cause of concern. At times, selling goods with long credit terms will lead to a

much greater long-term profit that would cover more than the cost associated with receiving

short-term loans to fulfil immediate obligations. To interpret the data, managerial assessment is

required.

Master budget: The master budget consists of the accumulation of all low-level budgets

generated by the different functioning areas of a organization. It also requires budget accounts,

4

their administrators.

Above mention budgeting purpose help the UCK’s managers to estimate income and

expenditure according to the operational activities. It is also beneficial to evaluating overall

performance of the company in comparison to last year performance or with their competitors.

Different types of budget along with advantage or disadvantage:

Cash budget: Cash budget is a plan or schedule for forecasted cash collections and

payments over the year. Other money inflows and outflows involve income received, expenses

charged, and refunds and payments for loans. In other words, capital budgeting is a projected

future financial situation forecast of the business. Management creates the cash budget after the

budgets for revenues, acquisitions, and capital expenses have already been made. Such forecasts

must be made in advance of the cash budget to accurately predict how the cash will be impacted

over the time. For example, manager of UCK furniture needs to have an estimation of revenue so

it can determine how often cash will be gathered over the era. Management using the cash

budget to control a company's cash flows.

Advantage: There are also benefits of using cash budgeting. This method helps to assess

whether cash balances are adequate to meet daily obligations and if the necessary criteria for

stability and cash balance specified by banking or internal company regulations are preserved

(Laela And et.al., 2018). It also lets an organization decide whether it holds too much money that

could otherwise be invested in productive things. Companies that lend from banks have to track

their ratio of cash coverage and plan a cash budget is the first phase in measuring that ratio.

Disadvantage: Cash budgets can trigger errors, too. Cash inflows aren't efficient. Cash

inflows arising from bond transactions, penalties, asset sales, or other one-off, semi-sustainable

operation do not generally reflect credible additional revenue sources. Decreased cash flow not

need always be a cause of concern. At times, selling goods with long credit terms will lead to a

much greater long-term profit that would cover more than the cost associated with receiving

short-term loans to fulfil immediate obligations. To interpret the data, managerial assessment is

required.

Master budget: The master budget consists of the accumulation of all low-level budgets

generated by the different functioning areas of a organization. It also requires budget accounts,

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

cash estimates and a payment plan. Usually the master budget is provided in either a monthly or

quarterly format, and generally covering the entire fiscal year of a corporation. A master budget

is the centrally planned tool used by a management team of UCK furniture to guide a

corporation's operations as well as to assess the success of its different accountability centres. It

is common for the senior management department to review a variety of master budget variations

and implement changes before it reaches a budget which assigns funds to achieve desired

outcomes.

Advantage: Using a master budget has the advantage of being able to recognize

challenges and prepare accordingly (Li, 2018). For example, if one department spends over its

cap, the master budget will show them which causes the business to invest than it earns per

month. To address the issue, by examining at the actual department expenditures, you can

determine which department is spending excessively. You will then either cut the expenses of

that department or make reductions in other departments to free up money to fund the extra cost.

It is harder to detect budget problems by just looking at departmental budgets individually.

Disadvantage: One of the drawbacks to getting a master budget is their lack of detail.

The dollar sums and figures written on both the master budget constitute a cumulative total of all

the expenditures and profits of the divisions. For example, they would not be able to tell how

much of the marketing team spends on a monthly basis because the amount would be applied as

one total of all other department spending.

Flexible budget: It is considered a variable budget, a financial program of projected

revenue and expenditure based on the real current production number. In other words, a flexible

budget using the income and expenditure generated in production as a benchmark and forecasts

how profit and expenditure will adjust based on performance changes. During an accounting

cycle, flexible budgets may also be used to determine the effective areas and ineffective areas of

last-performance. Management of UCK furniture contrasts the budgeted figures closely with the

real performance results to see where business has been improving and where the company needs

further change.

Advantage: The main advantage of such a budget being that it allows the management of

the company to assess the level of production in various consumer and business environments.

This also helps to reclassify the various types of budgeted expenses together with revenue so that

5

quarterly format, and generally covering the entire fiscal year of a corporation. A master budget

is the centrally planned tool used by a management team of UCK furniture to guide a

corporation's operations as well as to assess the success of its different accountability centres. It

is common for the senior management department to review a variety of master budget variations

and implement changes before it reaches a budget which assigns funds to achieve desired

outcomes.

Advantage: Using a master budget has the advantage of being able to recognize

challenges and prepare accordingly (Li, 2018). For example, if one department spends over its

cap, the master budget will show them which causes the business to invest than it earns per

month. To address the issue, by examining at the actual department expenditures, you can

determine which department is spending excessively. You will then either cut the expenses of

that department or make reductions in other departments to free up money to fund the extra cost.

It is harder to detect budget problems by just looking at departmental budgets individually.

Disadvantage: One of the drawbacks to getting a master budget is their lack of detail.

The dollar sums and figures written on both the master budget constitute a cumulative total of all

the expenditures and profits of the divisions. For example, they would not be able to tell how

much of the marketing team spends on a monthly basis because the amount would be applied as

one total of all other department spending.

Flexible budget: It is considered a variable budget, a financial program of projected

revenue and expenditure based on the real current production number. In other words, a flexible

budget using the income and expenditure generated in production as a benchmark and forecasts

how profit and expenditure will adjust based on performance changes. During an accounting

cycle, flexible budgets may also be used to determine the effective areas and ineffective areas of

last-performance. Management of UCK furniture contrasts the budgeted figures closely with the

real performance results to see where business has been improving and where the company needs

further change.

Advantage: The main advantage of such a budget being that it allows the management of

the company to assess the level of production in various consumer and business environments.

This also helps to reclassify the various types of budgeted expenses together with revenue so that

5

executives can better recognize the areas of benefit and therefore behave accordingly. Based on

the activity rates, this budget could be re-casted. It is not stiff.

Disadvantage: It will take time to work out exactly how unpredictable such

unpredictable costs could be and during the budget season, time is always at a premium (Qian,

Hörisch and Schaltegger, 2018). Consequently, a flexible budget might contain just a few

variable cost factors that in the first place diminish the importance of designing a flexible budget.

Flexible costs can be hard to predict, thus weakening the importance of a flexible budget. For

example, the labour costs can be especially unpredictable

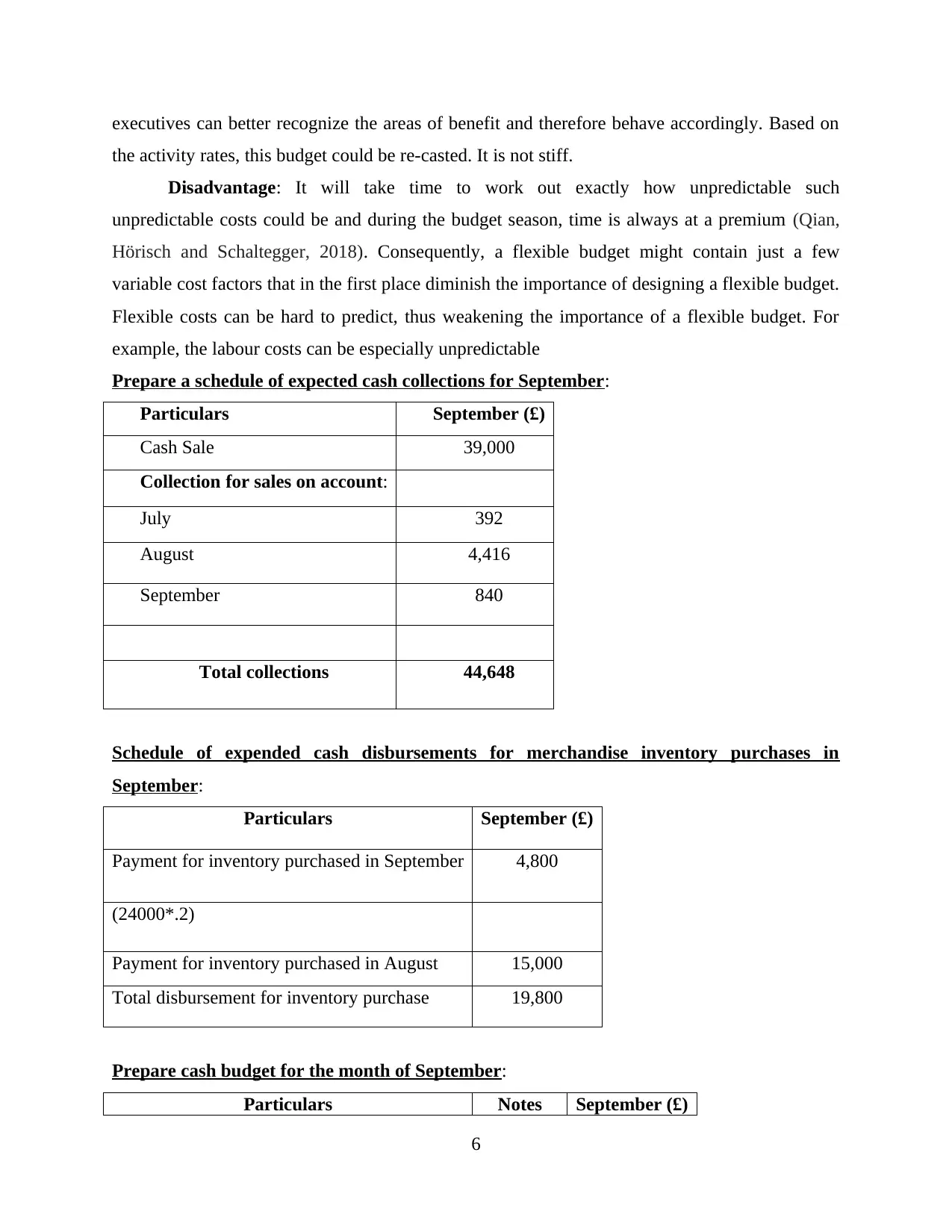

Prepare a schedule of expected cash collections for September:

Particulars September (£)

Cash Sale 39,000

Collection for sales on account:

July 392

August 4,416

September 840

Total collections 44,648

Schedule of expended cash disbursements for merchandise inventory purchases in

September:

Particulars September (£)

Payment for inventory purchased in September 4,800

(24000*.2)

Payment for inventory purchased in August 15,000

Total disbursement for inventory purchase 19,800

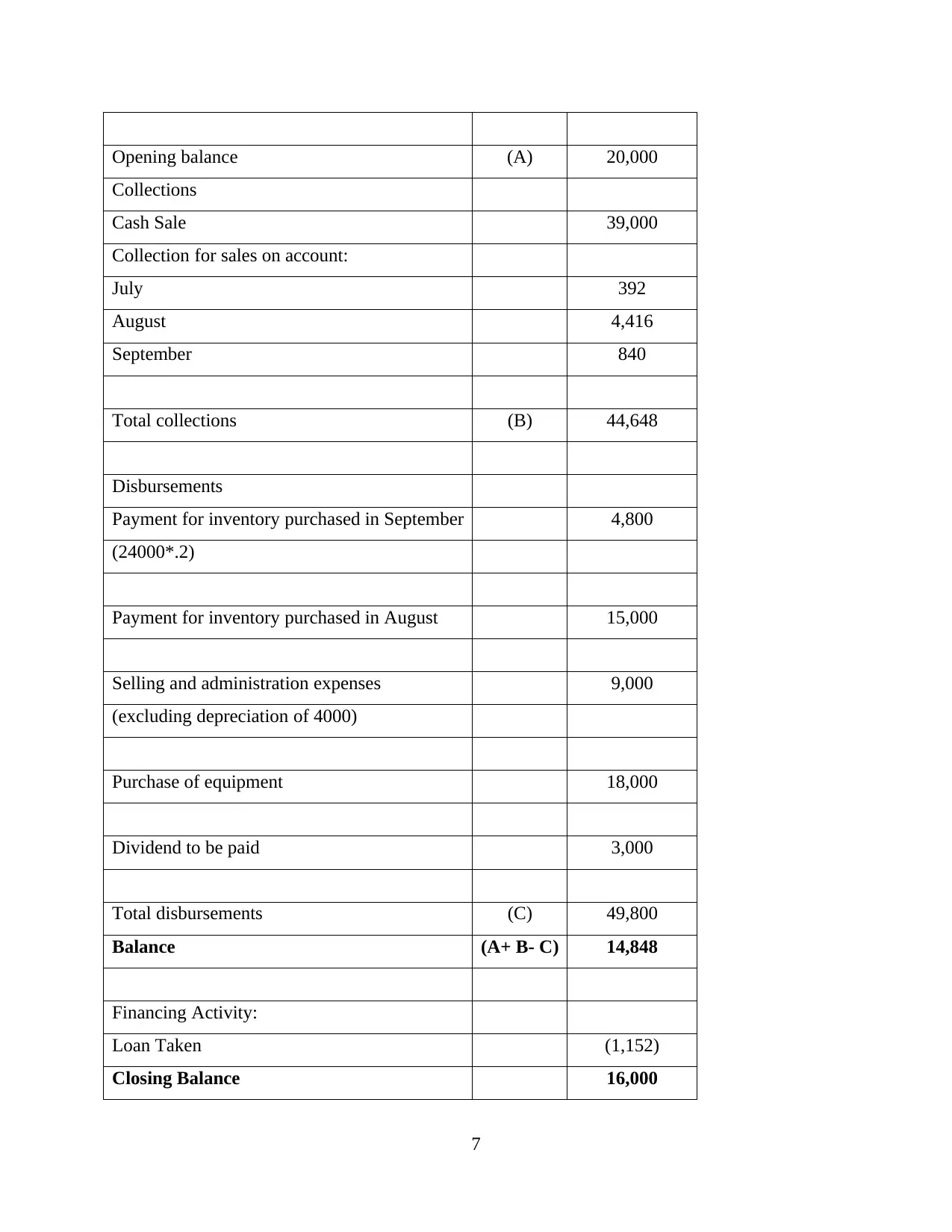

Prepare cash budget for the month of September:

Particulars Notes September (£)

6

the activity rates, this budget could be re-casted. It is not stiff.

Disadvantage: It will take time to work out exactly how unpredictable such

unpredictable costs could be and during the budget season, time is always at a premium (Qian,

Hörisch and Schaltegger, 2018). Consequently, a flexible budget might contain just a few

variable cost factors that in the first place diminish the importance of designing a flexible budget.

Flexible costs can be hard to predict, thus weakening the importance of a flexible budget. For

example, the labour costs can be especially unpredictable

Prepare a schedule of expected cash collections for September:

Particulars September (£)

Cash Sale 39,000

Collection for sales on account:

July 392

August 4,416

September 840

Total collections 44,648

Schedule of expended cash disbursements for merchandise inventory purchases in

September:

Particulars September (£)

Payment for inventory purchased in September 4,800

(24000*.2)

Payment for inventory purchased in August 15,000

Total disbursement for inventory purchase 19,800

Prepare cash budget for the month of September:

Particulars Notes September (£)

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Opening balance (A) 20,000

Collections

Cash Sale 39,000

Collection for sales on account:

July 392

August 4,416

September 840

Total collections (B) 44,648

Disbursements

Payment for inventory purchased in September 4,800

(24000*.2)

Payment for inventory purchased in August 15,000

Selling and administration expenses 9,000

(excluding depreciation of 4000)

Purchase of equipment 18,000

Dividend to be paid 3,000

Total disbursements (C) 49,800

Balance (A+ B- C) 14,848

Financing Activity:

Loan Taken (1,152)

Closing Balance 16,000

7

Collections

Cash Sale 39,000

Collection for sales on account:

July 392

August 4,416

September 840

Total collections (B) 44,648

Disbursements

Payment for inventory purchased in September 4,800

(24000*.2)

Payment for inventory purchased in August 15,000

Selling and administration expenses 9,000

(excluding depreciation of 4000)

Purchase of equipment 18,000

Dividend to be paid 3,000

Total disbursements (C) 49,800

Balance (A+ B- C) 14,848

Financing Activity:

Loan Taken (1,152)

Closing Balance 16,000

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4.1 Compare how organization following management accounting systems to resolve their

financial problem

Organizations are following several management accounting systems such as inventory,

cost management, job costing, price optimization etc. to help tackle financial problems

(Rikhardsson and Yigitbasioglu, 2018). It is impossible to recognize financial issues by using the

management accounting methods. Clearly, it is not possible to come up with approaches to

financial issues when issues themselves cannot be described. Using management accounting

strategies, UCK furniture is able to recognize areas of risk due to which financial troubles occur

appropriately and correctly. Not only this, management accounting also allows to quickly and

efficiently address those problems.

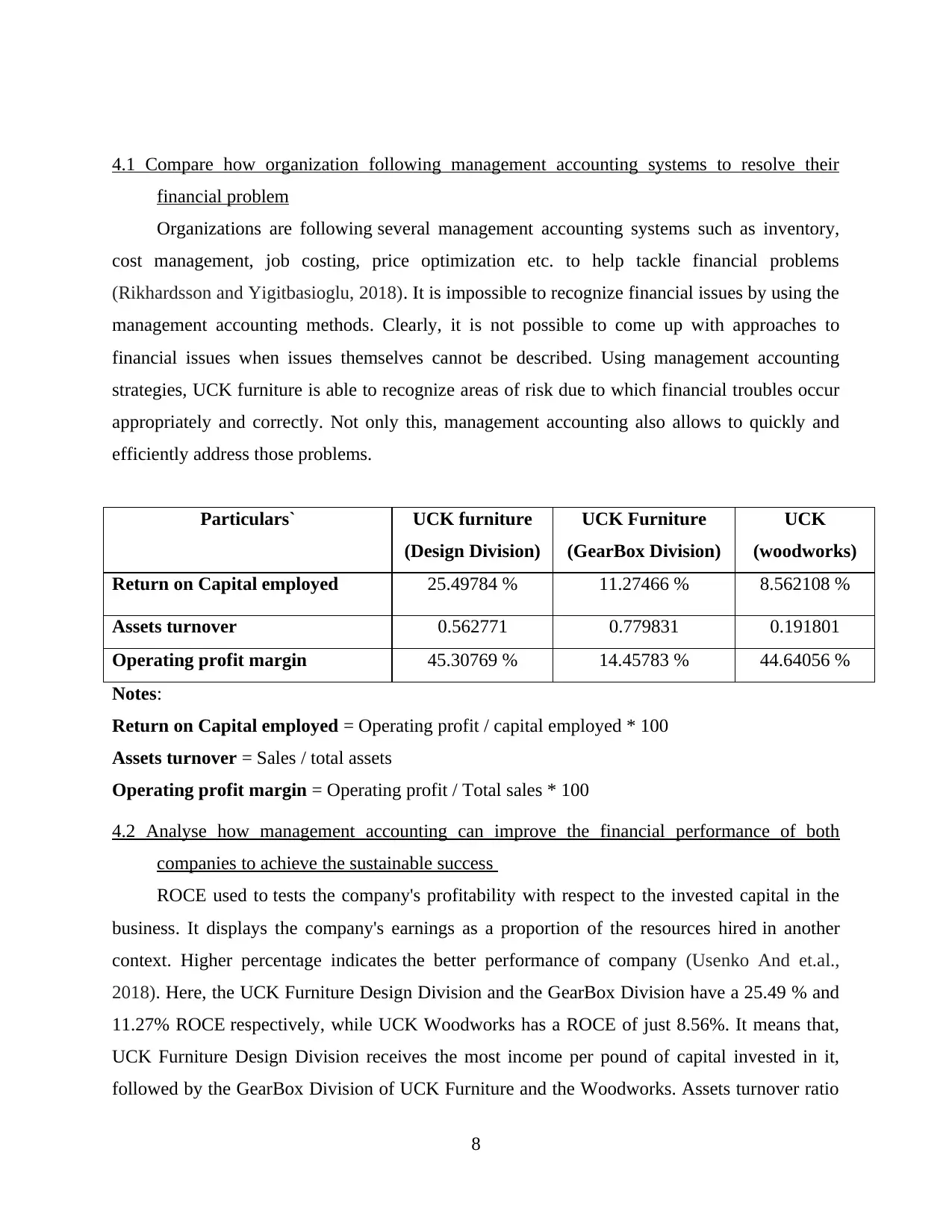

Particulars` UCK furniture

(Design Division)

UCK Furniture

(GearBox Division)

UCK

(woodworks)

Return on Capital employed 25.49784 % 11.27466 % 8.562108 %

Assets turnover 0.562771 0.779831 0.191801

Operating profit margin 45.30769 % 14.45783 % 44.64056 %

Notes:

Return on Capital employed = Operating profit / capital employed * 100

Assets turnover = Sales / total assets

Operating profit margin = Operating profit / Total sales * 100

4.2 Analyse how management accounting can improve the financial performance of both

companies to achieve the sustainable success

ROCE used to tests the company's profitability with respect to the invested capital in the

business. It displays the company's earnings as a proportion of the resources hired in another

context. Higher percentage indicates the better performance of company (Usenko And et.al.,

2018). Here, the UCK Furniture Design Division and the GearBox Division have a 25.49 % and

11.27% ROCE respectively, while UCK Woodworks has a ROCE of just 8.56%. It means that,

UCK Furniture Design Division receives the most income per pound of capital invested in it,

followed by the GearBox Division of UCK Furniture and the Woodworks. Assets turnover ratio

8

financial problem

Organizations are following several management accounting systems such as inventory,

cost management, job costing, price optimization etc. to help tackle financial problems

(Rikhardsson and Yigitbasioglu, 2018). It is impossible to recognize financial issues by using the

management accounting methods. Clearly, it is not possible to come up with approaches to

financial issues when issues themselves cannot be described. Using management accounting

strategies, UCK furniture is able to recognize areas of risk due to which financial troubles occur

appropriately and correctly. Not only this, management accounting also allows to quickly and

efficiently address those problems.

Particulars` UCK furniture

(Design Division)

UCK Furniture

(GearBox Division)

UCK

(woodworks)

Return on Capital employed 25.49784 % 11.27466 % 8.562108 %

Assets turnover 0.562771 0.779831 0.191801

Operating profit margin 45.30769 % 14.45783 % 44.64056 %

Notes:

Return on Capital employed = Operating profit / capital employed * 100

Assets turnover = Sales / total assets

Operating profit margin = Operating profit / Total sales * 100

4.2 Analyse how management accounting can improve the financial performance of both

companies to achieve the sustainable success

ROCE used to tests the company's profitability with respect to the invested capital in the

business. It displays the company's earnings as a proportion of the resources hired in another

context. Higher percentage indicates the better performance of company (Usenko And et.al.,

2018). Here, the UCK Furniture Design Division and the GearBox Division have a 25.49 % and

11.27% ROCE respectively, while UCK Woodworks has a ROCE of just 8.56%. It means that,

UCK Furniture Design Division receives the most income per pound of capital invested in it,

followed by the GearBox Division of UCK Furniture and the Woodworks. Assets turnover ratio

8

is an measure of the revenue a corporation will produce per unit of total assets. Here, the UCK

Furniture GearBox Division has the highest asset turnover ratio at 0.7798 and the UCK Furniture

Design Division at 0.5627 and the UCK Woodworks at 0.1918 respectively. This means that

GearBox Division of UCK Furniture will produce maximum revenue per unit of its properties.

The operating profit margin is the amount of income a firm earns from sales. The highest

operating profit margin for UCK Woodworks is 44.64 percent, followed by the UCK Furniture

Design Division is 45.30 percent and the UCK Furniture GearBox Division is 14.46 percent.

That means UCK Woodworks will gain the full profit from its revenues.

4.3 Evaluate the planning tools used in management accounting to reduce the financial issues to

achieve success

Budgetary control relates to the procedure by which managers contrast budget forecasts with

real results then assess and attempt to limit the differences between projections and real

revenues. It helps tackle problems that create inconsistencies between real data and expected

values. Ratio analysis is a very important method of management accounting (Weetman, 2019).

There are several ratios such as acid test, current ratio, equity ratio, asset turnover ratio, debt

coverage ratio etc., are measured and evaluated to determine overall growth and to evaluate the

corrective steps to be taken to boost negative ratios. Each planning technique used in

management accounting also allows financial statements to be improved and financial issues

removed to achieve success. In addition, ratio analysis of project estimation, calculation, and

costing methods help to minimize financial challenges and improve management accounting

performance.

CONCLUSION

From the above analysis it has been evaluated that, management accounting systems and

techniques are essential for the organizations because it helps in facing financial issues that

organizations face during the business operations. By using several accounting techniques such

as budgetary control, ratio analysis, marginal or absorption costing make business able to

improve financial performance and get success to achieve desired goals & objectives.

9

Furniture GearBox Division has the highest asset turnover ratio at 0.7798 and the UCK Furniture

Design Division at 0.5627 and the UCK Woodworks at 0.1918 respectively. This means that

GearBox Division of UCK Furniture will produce maximum revenue per unit of its properties.

The operating profit margin is the amount of income a firm earns from sales. The highest

operating profit margin for UCK Woodworks is 44.64 percent, followed by the UCK Furniture

Design Division is 45.30 percent and the UCK Furniture GearBox Division is 14.46 percent.

That means UCK Woodworks will gain the full profit from its revenues.

4.3 Evaluate the planning tools used in management accounting to reduce the financial issues to

achieve success

Budgetary control relates to the procedure by which managers contrast budget forecasts with

real results then assess and attempt to limit the differences between projections and real

revenues. It helps tackle problems that create inconsistencies between real data and expected

values. Ratio analysis is a very important method of management accounting (Weetman, 2019).

There are several ratios such as acid test, current ratio, equity ratio, asset turnover ratio, debt

coverage ratio etc., are measured and evaluated to determine overall growth and to evaluate the

corrective steps to be taken to boost negative ratios. Each planning technique used in

management accounting also allows financial statements to be improved and financial issues

removed to achieve success. In addition, ratio analysis of project estimation, calculation, and

costing methods help to minimize financial challenges and improve management accounting

performance.

CONCLUSION

From the above analysis it has been evaluated that, management accounting systems and

techniques are essential for the organizations because it helps in facing financial issues that

organizations face during the business operations. By using several accounting techniques such

as budgetary control, ratio analysis, marginal or absorption costing make business able to

improve financial performance and get success to achieve desired goals & objectives.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books & Journals

Dierynck, B. and Labro, E., 2018. Management accounting information properties and

operations management. Foundations and Trends® in Technology, Information and

Operations Management. 12(1). pp.1-114.

Gomez-Conde, J. And et.al., 2019. Environmental innovation practices and operational

performance. The joint effects of management accounting and control systems and

environmental training. Accounting, Auditing & Accountability Journal.

Laela, S. F. And et.al., 2018. Management accounting-strategy coalignment in Islamic

banking. International Journal of Islamic and Middle Eastern Finance and Management.

Li, W. S., 2018. Strategic Management Accounting. Management for Professionals.

Qian, W., Hörisch, J. and Schaltegger, S., 2018. Environmental management accounting and its

effects on carbon management and disclosure quality. Journal of Cleaner

Production. 174. pp.1608-1619.

Rikhardsson, P. and Yigitbasioglu, O., 2018. Business intelligence & analytics in management

accounting research: Status and future focus. International Journal of Accounting

Information Systems. 29. pp.37-58.

Usenko, L. N. And et.al., 2018. Formation of an integrated accounting and analytical

management system for value analysis purposes.

Weetman, P., 2019. Financial and management accounting. Pearson UK.

10

Books & Journals

Dierynck, B. and Labro, E., 2018. Management accounting information properties and

operations management. Foundations and Trends® in Technology, Information and

Operations Management. 12(1). pp.1-114.

Gomez-Conde, J. And et.al., 2019. Environmental innovation practices and operational

performance. The joint effects of management accounting and control systems and

environmental training. Accounting, Auditing & Accountability Journal.

Laela, S. F. And et.al., 2018. Management accounting-strategy coalignment in Islamic

banking. International Journal of Islamic and Middle Eastern Finance and Management.

Li, W. S., 2018. Strategic Management Accounting. Management for Professionals.

Qian, W., Hörisch, J. and Schaltegger, S., 2018. Environmental management accounting and its

effects on carbon management and disclosure quality. Journal of Cleaner

Production. 174. pp.1608-1619.

Rikhardsson, P. and Yigitbasioglu, O., 2018. Business intelligence & analytics in management

accounting research: Status and future focus. International Journal of Accounting

Information Systems. 29. pp.37-58.

Usenko, L. N. And et.al., 2018. Formation of an integrated accounting and analytical

management system for value analysis purposes.

Weetman, P., 2019. Financial and management accounting. Pearson UK.

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.