Advanced Management Accounting Report: Factors & Stakeholders

VerifiedAdded on 2022/11/14

|10

|2377

|67

Report

AI Summary

This report delves into advanced management accounting, exploring the purpose and presentation of financial data from the perspective of various stakeholders. It examines the significance of financial data for stakeholders, including suppliers, creditors, media, consumers, the public, and government, as well as internal stakeholders like shareholders, employees, and managers. The report further evaluates the impact of changing external and internal factors on management accounting practices. Internal factors such as organizational structure, size, strategy, and business line are discussed, along with external factors like environmental uncertainty and market competition. The analysis highlights how these factors influence the adoption of management accounting practices, emphasizing the need for adaptation to maintain competitiveness and achieve favorable outcomes. The report references several academic sources to support its findings.

Running Head: ADVANCED MANAGEMENT ACCOUNTING

ADVANCED MANAGEMENT ACCOUNTING

ADVANCED MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED MANAGEMENT ACCOUNTING 2

Table of Contents

Management Accounting...........................................................................................................2

P1: Analyse the purpose and presentation of financial data from the perspective of different

stakeholders................................................................................................................................2

P5: Evaluate how external and internal factors changing the business environment impact

upon the management accounting..............................................................................................4

References..................................................................................................................................8

Table of Contents

Management Accounting...........................................................................................................2

P1: Analyse the purpose and presentation of financial data from the perspective of different

stakeholders................................................................................................................................2

P5: Evaluate how external and internal factors changing the business environment impact

upon the management accounting..............................................................................................4

References..................................................................................................................................8

ADVANCED MANAGEMENT ACCOUNTING 3

Management Accounting

P1: Analyse the purpose and presentation of financial data from the perspective of

different stakeholders

The financial data of the organization is gathered by considering the annual report. The

organization has the mandate to offer the financial data to its different stakeholder at the time

of reporting period. The financial report is the organization report to its comprehensive

transactions as well as events to publish and offered to the needed parties (Rensburg & Botha,

2014). Moreover, the annual report is a tool that assists to the organization to comprehend

the transaction that has been completed during the period. There are certain causes that could

mandate to the firm or effective comprehend their financial inflows and outflow and make an

effective financial decision. On behalf of 150, 151, 152 and 153 acts could mandate to the

organization for preparing the financial contents and financial statement for making the

record of finance transaction. Furthermore, it is stated that the stakeholder of the company

requires financial information for completing many activities. Through this, the stakeholders

could be needed to comprehend how the organization process is working. It is evaluated that

the stakeholders could also comprehend the amount of profit that has been obtained by the

firm. The financial data could be effective for comprehending the tactical and strategic policy

of the organization. It is stated that financial information could also lead to making a decision

in the context of top management. It is stated that the audit procedure could be effective for

evaluating the weakness and strengths of the management and supports to get higher

competitive advantages. It is examined that the financial requirement could lead to the firm

for operating the business process and get a favorable outcome (Cooper, 2017).

Significance of financial data to Stakeholders

The financial data could play an imperative role in the firm as it assists to operate the

business process and make an effective financial decision. There are different kinds of

Management Accounting

P1: Analyse the purpose and presentation of financial data from the perspective of

different stakeholders

The financial data of the organization is gathered by considering the annual report. The

organization has the mandate to offer the financial data to its different stakeholder at the time

of reporting period. The financial report is the organization report to its comprehensive

transactions as well as events to publish and offered to the needed parties (Rensburg & Botha,

2014). Moreover, the annual report is a tool that assists to the organization to comprehend

the transaction that has been completed during the period. There are certain causes that could

mandate to the firm or effective comprehend their financial inflows and outflow and make an

effective financial decision. On behalf of 150, 151, 152 and 153 acts could mandate to the

organization for preparing the financial contents and financial statement for making the

record of finance transaction. Furthermore, it is stated that the stakeholder of the company

requires financial information for completing many activities. Through this, the stakeholders

could be needed to comprehend how the organization process is working. It is evaluated that

the stakeholders could also comprehend the amount of profit that has been obtained by the

firm. The financial data could be effective for comprehending the tactical and strategic policy

of the organization. It is stated that financial information could also lead to making a decision

in the context of top management. It is stated that the audit procedure could be effective for

evaluating the weakness and strengths of the management and supports to get higher

competitive advantages. It is examined that the financial requirement could lead to the firm

for operating the business process and get a favorable outcome (Cooper, 2017).

Significance of financial data to Stakeholders

The financial data could play an imperative role in the firm as it assists to operate the

business process and make an effective financial decision. There are different kinds of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADVANCED MANAGEMENT ACCOUNTING 4

stakeholders that are considered by a firm named external and internal stakeholders. It is

examined that the Suppliers and Trade creditors, Medias, Consumers, Public, and

Government are known as the external stakeholder of the firm that is known as the external

stakeholders. It is examined that shareholders, employees, and directors & managers were

known as the internal stakeholders (Gonzalez-Zapata & Heeks, 2015). The directors and

managers of the firm in diverse time as well as in the diverse level. It is evaluated that the

director, as well as executives of the firm, are having certain kinds of decision making a

reliable matter. It is evaluated that the stakeholder could be effective in making the

investment as well as report appreciation decision. The stakeholders could be capable to

comprehend policies of dividend policies. It could be effective to know the operation of the

business. It could also be effective in making effective business decisions. The shareholder of

the firm could also evaluate the investment decision before purchasing the share of a firm as

it could be possible by collecting the financial information. The shareholders could take the

fair decision in the context of investment return and operate the business effectively. It could

be effective for gaining the understanding of the organizational acts. The shareholder could

compare the benefits of investment with their competitive industries. It could lead to the

shareholder for getting a favorable outcome. It is stated that employees could comprehend the

profitability as well as the stability of the organization (De Massis & Kotlar, 2014). It could

be effective for the attainment of the organizational task. It could be effective for

comprehending towards retirement advantages, remuneration, as well as the opportunity of

employment. It could increase the security of a job with the recent organization. It could be

effective for sharing the fairness of wages as they get by the company according to its

earnings. It could be effective for operating the business operation for the firm. It is stated

that the government could support to get the accurate taxes as well as amounts of the firm on

due dates. It is examined that the government benefaction could lead to improve the business.

stakeholders that are considered by a firm named external and internal stakeholders. It is

examined that the Suppliers and Trade creditors, Medias, Consumers, Public, and

Government are known as the external stakeholder of the firm that is known as the external

stakeholders. It is examined that shareholders, employees, and directors & managers were

known as the internal stakeholders (Gonzalez-Zapata & Heeks, 2015). The directors and

managers of the firm in diverse time as well as in the diverse level. It is evaluated that the

director, as well as executives of the firm, are having certain kinds of decision making a

reliable matter. It is evaluated that the stakeholder could be effective in making the

investment as well as report appreciation decision. The stakeholders could be capable to

comprehend policies of dividend policies. It could be effective to know the operation of the

business. It could also be effective in making effective business decisions. The shareholder of

the firm could also evaluate the investment decision before purchasing the share of a firm as

it could be possible by collecting the financial information. The shareholders could take the

fair decision in the context of investment return and operate the business effectively. It could

be effective for gaining the understanding of the organizational acts. The shareholder could

compare the benefits of investment with their competitive industries. It could lead to the

shareholder for getting a favorable outcome. It is stated that employees could comprehend the

profitability as well as the stability of the organization (De Massis & Kotlar, 2014). It could

be effective for the attainment of the organizational task. It could be effective for

comprehending towards retirement advantages, remuneration, as well as the opportunity of

employment. It could increase the security of a job with the recent organization. It could be

effective for sharing the fairness of wages as they get by the company according to its

earnings. It could be effective for operating the business operation for the firm. It is stated

that the government could support to get the accurate taxes as well as amounts of the firm on

due dates. It is examined that the government benefaction could lead to improve the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED MANAGEMENT ACCOUNTING 5

It is examined that shareholder could be capable to get the non-financial and financial support

in the projects of government developments. The owner of the firm could also be

shareholders of the firm as they could be mandated to have a decision in the context of

financial decision. It could also be effective for operating the business process and support to

make a decision effectively. The financial data could be effective to determine the rules and

regulation of the firm and make the decision accordingly (Crowther, 2018). The consumers

could also comprehend the financial data of the origination to know the cost structure of

goods. It could be effective for the firm to get a reliable outcome. They could also be capable

to assure the stability of the firm. It could be effective for making a financial decision and

increase the possibilities of getting a positive outcome. The consumer could also be effective

for comprehending the CSR cultures to perform by the firm. The consumer could also be

capable to evaluate the profitability of the firm to gain the competitiveness of a firm. It could

lead to getting a reliable outcome.

P5: Evaluate how external and internal factors changing the business environment

impact upon the management accounting

The fundamental role of an accounting system is to manage the organizational structure. The

literature demonstrates that there are different factors of contingency which may influence the

organizational structure such as strategy, structure, production technology, as well as,

environmental vagueness. The purpose of this investigation is to depict that integration

related to management accounting practices is a concern of harmonization between internal

as well as, external factor of management accounting practices and companies. In this way,

the contingency model could be adopted for assessing the external contingency components

that illustrate the implementing of business accounting practice at the different development

level.

Internal Factors

It is examined that shareholder could be capable to get the non-financial and financial support

in the projects of government developments. The owner of the firm could also be

shareholders of the firm as they could be mandated to have a decision in the context of

financial decision. It could also be effective for operating the business process and support to

make a decision effectively. The financial data could be effective to determine the rules and

regulation of the firm and make the decision accordingly (Crowther, 2018). The consumers

could also comprehend the financial data of the origination to know the cost structure of

goods. It could be effective for the firm to get a reliable outcome. They could also be capable

to assure the stability of the firm. It could be effective for making a financial decision and

increase the possibilities of getting a positive outcome. The consumer could also be effective

for comprehending the CSR cultures to perform by the firm. The consumer could also be

capable to evaluate the profitability of the firm to gain the competitiveness of a firm. It could

lead to getting a reliable outcome.

P5: Evaluate how external and internal factors changing the business environment

impact upon the management accounting

The fundamental role of an accounting system is to manage the organizational structure. The

literature demonstrates that there are different factors of contingency which may influence the

organizational structure such as strategy, structure, production technology, as well as,

environmental vagueness. The purpose of this investigation is to depict that integration

related to management accounting practices is a concern of harmonization between internal

as well as, external factor of management accounting practices and companies. In this way,

the contingency model could be adopted for assessing the external contingency components

that illustrate the implementing of business accounting practice at the different development

level.

Internal Factors

ADVANCED MANAGEMENT ACCOUNTING 6

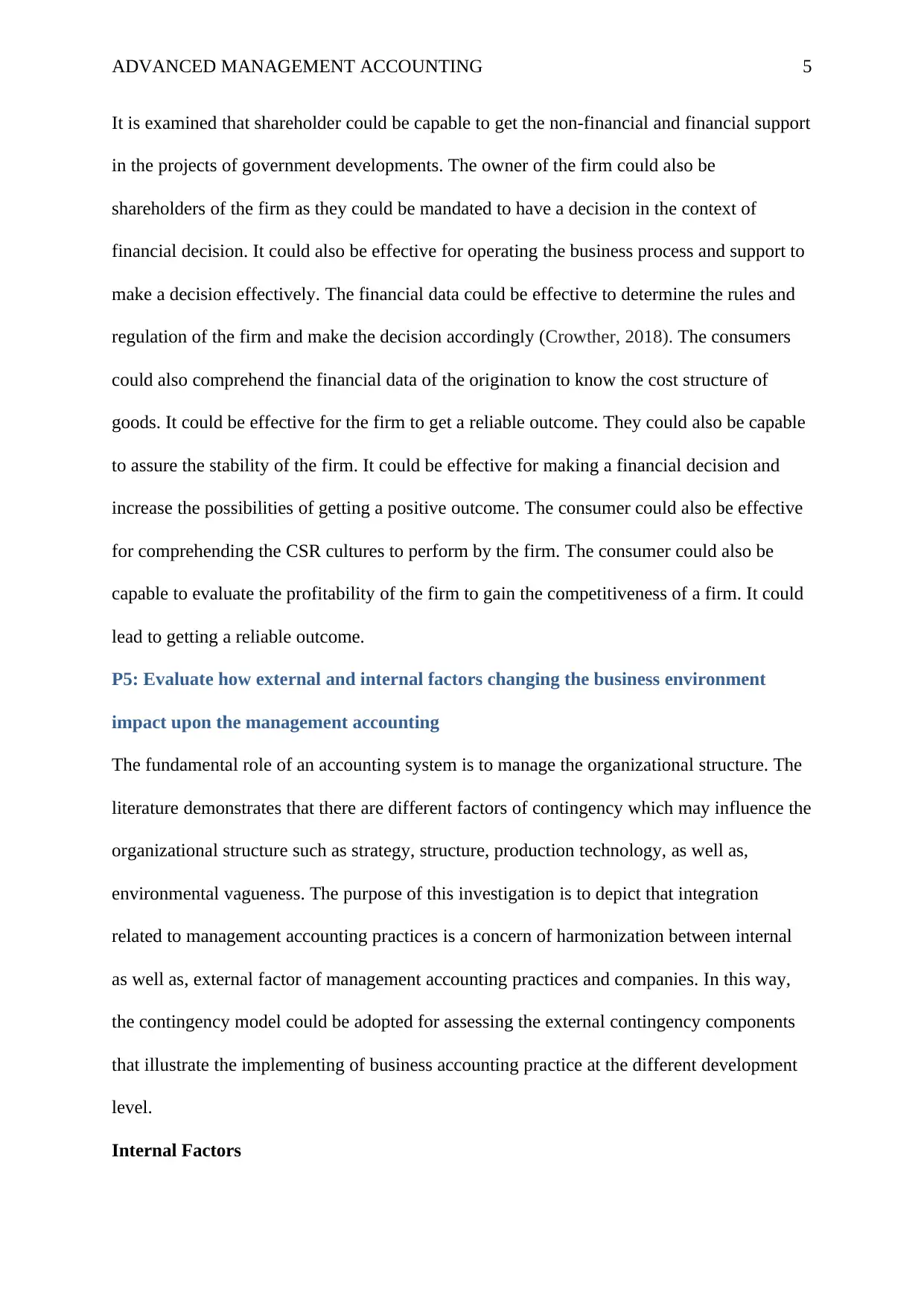

There are different internal factors of firms that are associated with organizational structure,

its pursued strategy, and its size.

(Source: Otley, 2016).

The Organizational Structure

It is evaluated that between the significant structural parameters that have received high

consideration in organizational research are those associated with the definition of the extent

to which, decision-making at the workplace could be centralized or decentralized. It is

addressed that there is a favorable association among management accounting practices, and

decentralization (Otley, 2016).

The Size

The size of the company is a key indicator of its structure. In this way, the smaller

corporation focuses on simpler accounting practices as well as, lower level of difficulty. The

size demonstrates the significant factors related to a structural contingency that justifies and

explains the practice of management control techniques (Appelbaum, et al., 2017).

The Strategy

There are different strategies related to management accounting practices. These strategies

are related to prospectors, defenders, assessor, as well as, reactors. It is also identified that

sophisticated management accounting practices have a more favorable impact on business

performance that implements the prospecting approach as compared to corporations that

implement the defender approaches. A feasible management accounting system can aid

strategic priorities for enhancing performance. Furthermore, competing strategies are also

identified as a mediating variable into contingent association among management accounting

There are different internal factors of firms that are associated with organizational structure,

its pursued strategy, and its size.

(Source: Otley, 2016).

The Organizational Structure

It is evaluated that between the significant structural parameters that have received high

consideration in organizational research are those associated with the definition of the extent

to which, decision-making at the workplace could be centralized or decentralized. It is

addressed that there is a favorable association among management accounting practices, and

decentralization (Otley, 2016).

The Size

The size of the company is a key indicator of its structure. In this way, the smaller

corporation focuses on simpler accounting practices as well as, lower level of difficulty. The

size demonstrates the significant factors related to a structural contingency that justifies and

explains the practice of management control techniques (Appelbaum, et al., 2017).

The Strategy

There are different strategies related to management accounting practices. These strategies

are related to prospectors, defenders, assessor, as well as, reactors. It is also identified that

sophisticated management accounting practices have a more favorable impact on business

performance that implements the prospecting approach as compared to corporations that

implement the defender approaches. A feasible management accounting system can aid

strategic priorities for enhancing performance. Furthermore, competing strategies are also

identified as a mediating variable into contingent association among management accounting

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADVANCED MANAGEMENT ACCOUNTING 7

practices as well as external competition. There is also a difference between competitive

approaches as well as, international outlooks as an explanatory element for differences into

management accounting systems (Sekaran & Bougie, 2016).

The Business Line

The sector related to activity has been focused by different investigators as an explanatory

element, specifically in small and medium companies. But, in the study of 928 Australian

SMEs, there is an indication that industry can impact on the extent of production related to

non-compulsory accounting information for small and medium companies.

The Type of Business Affiliation

The aspect related to the parent company as well as, its subsidiary has not been combined as a

contextual element in determining the combination of range related to the management

accounting system. In this way, the ability of the parent company is to persuade the kind of

its management accounting system of the subsidiary. Moreover, it is identified that the

company implemented the activity-based costing technique as they are persuaded by the

international parent corporation. In such sense, the company has combined this factor for

studying its effect on integration related to set of management practices of accounting as well

as, their extent is related to sophistication (Goetsch & Davis, 2014).

External Factors

A company cannot simply create for demonstrating the objectives, motivation as well as,

requirements of its members and leadership. It should focus on the constraints that can

impose through its association with the atmosphere. Therefore, the unpredictability of

atmosphere has anticipated implication regarding management accounting practices. Along

with this, accounting practices of companies can perceive low eco-friendly uncertainty.

Environmental Uncertainty

practices as well as external competition. There is also a difference between competitive

approaches as well as, international outlooks as an explanatory element for differences into

management accounting systems (Sekaran & Bougie, 2016).

The Business Line

The sector related to activity has been focused by different investigators as an explanatory

element, specifically in small and medium companies. But, in the study of 928 Australian

SMEs, there is an indication that industry can impact on the extent of production related to

non-compulsory accounting information for small and medium companies.

The Type of Business Affiliation

The aspect related to the parent company as well as, its subsidiary has not been combined as a

contextual element in determining the combination of range related to the management

accounting system. In this way, the ability of the parent company is to persuade the kind of

its management accounting system of the subsidiary. Moreover, it is identified that the

company implemented the activity-based costing technique as they are persuaded by the

international parent corporation. In such sense, the company has combined this factor for

studying its effect on integration related to set of management practices of accounting as well

as, their extent is related to sophistication (Goetsch & Davis, 2014).

External Factors

A company cannot simply create for demonstrating the objectives, motivation as well as,

requirements of its members and leadership. It should focus on the constraints that can

impose through its association with the atmosphere. Therefore, the unpredictability of

atmosphere has anticipated implication regarding management accounting practices. Along

with this, accounting practices of companies can perceive low eco-friendly uncertainty.

Environmental Uncertainty

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED MANAGEMENT ACCOUNTING 8

The environmental uncertainty could be first contingent elements that are addressed for their

impact on designing of the management accounting system. Along with this, while perceived

environmental uncertainties are low, management could be competent for making relatively

feasible prediction across the market (Schaltegger & Burritt, 2017). It is identified that

observed different level of environmental uncertainty implements effective sophisticated

management. These levels are costing as well as, financial control i.e. first level, the offering

of data related to planning and control i.e. second level, declining waste in business resources

i.e. third level, and creating value by optimum utilization of resources i.e. fourth level. Along

with this, external factors are market competition and environmental uncertainty. Internal

factors are size, structure, and business line.

Market Competition

It is addressed that there is an association between intensity related to market rivalry as well

as, utilization of data by top executives. The researcher has tasted the practices of

management accounting as well as, the performance of a business unit (Stubbs & Higgins,

2014). The results indicate that the gain in the intensity of rivalry in the market is related to

increase the managerial practice of management accounting data. In current times, the

company should consider management accounting control system that can offer accurate,

timely as well as, relevant data on a wide range of concerns such as productivity, customer

services, profitability, productivity, customer satisfaction, and quality. Management

accounting control practice can be modified or created to emphasize value-added practices of

a company associated with its rivalry (Epstein, 2018).

The environmental uncertainty could be first contingent elements that are addressed for their

impact on designing of the management accounting system. Along with this, while perceived

environmental uncertainties are low, management could be competent for making relatively

feasible prediction across the market (Schaltegger & Burritt, 2017). It is identified that

observed different level of environmental uncertainty implements effective sophisticated

management. These levels are costing as well as, financial control i.e. first level, the offering

of data related to planning and control i.e. second level, declining waste in business resources

i.e. third level, and creating value by optimum utilization of resources i.e. fourth level. Along

with this, external factors are market competition and environmental uncertainty. Internal

factors are size, structure, and business line.

Market Competition

It is addressed that there is an association between intensity related to market rivalry as well

as, utilization of data by top executives. The researcher has tasted the practices of

management accounting as well as, the performance of a business unit (Stubbs & Higgins,

2014). The results indicate that the gain in the intensity of rivalry in the market is related to

increase the managerial practice of management accounting data. In current times, the

company should consider management accounting control system that can offer accurate,

timely as well as, relevant data on a wide range of concerns such as productivity, customer

services, profitability, productivity, customer satisfaction, and quality. Management

accounting control practice can be modified or created to emphasize value-added practices of

a company associated with its rivalry (Epstein, 2018).

ADVANCED MANAGEMENT ACCOUNTING 9

References

Appelbaum, D., Kogan, A., Vasarhelyi, M., & Yan, Z. (2017). Impact of business analytics

and enterprise systems on managerial accounting. International Journal of Accounting

Information Systems, 25, 29-44.

Cooper, S. (2017). Corporate social performance: A stakeholder approach. Routledge.

Crowther, D. (2018). A Social Critique of Corporate Reporting: A Semiotic Analysis of

Corporate Financial and Environmental Reporting: A Semiotic Analysis of Corporate

Financial and Environmental Reporting. Routledge.

De Massis, A., & Kotlar, J. (2014). The case study method in family business research:

Guidelines for a qualitative scholarship. Journal of Family Business Strategy, 5(1),

15-29.

Epstein, M. J. (2018). Making sustainability work: Best practices in managing and measuring

corporate social, environmental and economic impacts. Routledge.

Goetsch, D. L., & Davis, S. B. (2014). Quality management for organizational excellence.

Upper Saddle River, NJ: Pearson.

Gonzalez-Zapata, F., & Heeks, R. (2015). The multiple meanings of open government data:

Understanding different stakeholders and their perspectives. Government Information

Quarterly, 32(4), 441-452.

Otley, D. (2016). The contingency theory of management accounting and control: 1980–

2014. Management accounting research, 31, 45-62.

Rensburg, R., & Botha, E. (2014). Is integrated reporting the silver bullet of financial

communication? A stakeholder perspective from South Africa. Public Relations

Review, 40(2), 144-152.

Schaltegger, S., & Burritt, R. (2017). Contemporary environmental accounting: issues,

concepts, and practice. Routledge.

References

Appelbaum, D., Kogan, A., Vasarhelyi, M., & Yan, Z. (2017). Impact of business analytics

and enterprise systems on managerial accounting. International Journal of Accounting

Information Systems, 25, 29-44.

Cooper, S. (2017). Corporate social performance: A stakeholder approach. Routledge.

Crowther, D. (2018). A Social Critique of Corporate Reporting: A Semiotic Analysis of

Corporate Financial and Environmental Reporting: A Semiotic Analysis of Corporate

Financial and Environmental Reporting. Routledge.

De Massis, A., & Kotlar, J. (2014). The case study method in family business research:

Guidelines for a qualitative scholarship. Journal of Family Business Strategy, 5(1),

15-29.

Epstein, M. J. (2018). Making sustainability work: Best practices in managing and measuring

corporate social, environmental and economic impacts. Routledge.

Goetsch, D. L., & Davis, S. B. (2014). Quality management for organizational excellence.

Upper Saddle River, NJ: Pearson.

Gonzalez-Zapata, F., & Heeks, R. (2015). The multiple meanings of open government data:

Understanding different stakeholders and their perspectives. Government Information

Quarterly, 32(4), 441-452.

Otley, D. (2016). The contingency theory of management accounting and control: 1980–

2014. Management accounting research, 31, 45-62.

Rensburg, R., & Botha, E. (2014). Is integrated reporting the silver bullet of financial

communication? A stakeholder perspective from South Africa. Public Relations

Review, 40(2), 144-152.

Schaltegger, S., & Burritt, R. (2017). Contemporary environmental accounting: issues,

concepts, and practice. Routledge.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADVANCED MANAGEMENT ACCOUNTING 10

Sekaran, U., & Bougie, R. (2016). Research methods for business: A skill building approach.

John Wiley & Sons.

Stubbs, W., & Higgins, C. (2014). Integrated reporting and internal mechanisms of

change. Accounting, Auditing & Accountability Journal, 27(7), 1068-1089.

Sekaran, U., & Bougie, R. (2016). Research methods for business: A skill building approach.

John Wiley & Sons.

Stubbs, W., & Higgins, C. (2014). Integrated reporting and internal mechanisms of

change. Accounting, Auditing & Accountability Journal, 27(7), 1068-1089.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.