BTEC Level 4 HND Unit 5: Management Accounting Report on Vinamilk

VerifiedAdded on 2022/01/19

|14

|3916

|316

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its definition, roles, and comparison with financial accounting. It explores various management accounting systems such as cost accounting, inventory management, job costing, and price optimization, offering detailed explanations and examples. The report also delves into different methods used for management accounting reporting, including budget reports, accounts receivable aging reports, job cost reports, and inventory reports. A significant portion of the report analyzes how organizations adapt their management accounting systems to address financial challenges, using Vietnam Dairy Products Joint-Stock Company (Vinamilk) as a case study. The report concludes by summarizing the key findings and emphasizing the practical application of management accounting principles in a real-world business context. The report examines Vinamilk's financial performance and strategies, highlighting the importance of effective management accounting in achieving organizational goals.

ASSIGNMENT 1 FRONT SHEET

Qualification BTEC Level 4 HND Diploma in Business

Unit number and title Unit 5: Management Accounting (489)

Submission date December 16, 2021 Date received (1st December 16, 2021

submission)

Re-submission date Date received (2nd

submission)

Student name Bui Minh Phi Student ID BDBF200006

Class BA16101 Assessor name Vu Thi Quynh Anh

Student declaration

I certify that the assignment submission is entirely my own work and I fully understand the consequences of plagiarism. I

understand that making a false declaration is a form of malpractice.

Student’s signature:

Phi

Grading grid

P1 P2 P5 M1 M4 D1 D3

Qualification BTEC Level 4 HND Diploma in Business

Unit number and title Unit 5: Management Accounting (489)

Submission date December 16, 2021 Date received (1st December 16, 2021

submission)

Re-submission date Date received (2nd

submission)

Student name Bui Minh Phi Student ID BDBF200006

Class BA16101 Assessor name Vu Thi Quynh Anh

Student declaration

I certify that the assignment submission is entirely my own work and I fully understand the consequences of plagiarism. I

understand that making a false declaration is a form of malpractice.

Student’s signature:

Phi

Grading grid

P1 P2 P5 M1 M4 D1 D3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Summative Feedbacks: Resubmission Feedbacks:

Grade: Assessor Signature: Date:

Internal Verifier’s Comments:

Signature & Date:

Grade: Assessor Signature: Date:

Internal Verifier’s Comments:

Signature & Date:

Contents

1. Introduction......................................................................................................................................4

2. Management accounting...................................................................................................................4

2.1. Definition of Management accounting........................................................................................4

2.2. Roles of Management accounting...............................................................................................5

2.2.1. Stewardship Accounting.......................................................................................................5

2.2.2. Long-term and Short-Term Planning.....................................................................................5

2.2.3. Developing Management Information System (MIS).............................................................5

2.2.4. Maintaining Optimum Capital Structure...............................................................................5

2.2.5. Participating in Management Process...................................................................................5

2.2.6. Controlling............................................................................................................................6

2.2.7. Decision-Making...................................................................................................................6

2.3. Comparison of Financial accounting and Management accounting..............................................6

2.4. Different types of MA systems....................................................................................................7

2.4.1. Cost accounting system........................................................................................................7

2.4.2. Inventory management system............................................................................................7

2.4.3. Job costing system................................................................................................................8

2.4.4. Price optimization system.....................................................................................................9

2.5. Different methods used for management accounting reporting..................................................9

2.5.1. Budget report.......................................................................................................................9

2.5.2. Accounts Receivable Aging Reports....................................................................................10

2.5.3. Job cost reports..................................................................................................................10

2.5.4. Inventory and Manufacturing report..................................................................................11

3. How organizations are adapting their management accounting Systems to deal with financial

problems.............................................................................................................................................11

4. Conclusion.......................................................................................................................................13

References..........................................................................................................................................13

1. Introduction......................................................................................................................................4

2. Management accounting...................................................................................................................4

2.1. Definition of Management accounting........................................................................................4

2.2. Roles of Management accounting...............................................................................................5

2.2.1. Stewardship Accounting.......................................................................................................5

2.2.2. Long-term and Short-Term Planning.....................................................................................5

2.2.3. Developing Management Information System (MIS).............................................................5

2.2.4. Maintaining Optimum Capital Structure...............................................................................5

2.2.5. Participating in Management Process...................................................................................5

2.2.6. Controlling............................................................................................................................6

2.2.7. Decision-Making...................................................................................................................6

2.3. Comparison of Financial accounting and Management accounting..............................................6

2.4. Different types of MA systems....................................................................................................7

2.4.1. Cost accounting system........................................................................................................7

2.4.2. Inventory management system............................................................................................7

2.4.3. Job costing system................................................................................................................8

2.4.4. Price optimization system.....................................................................................................9

2.5. Different methods used for management accounting reporting..................................................9

2.5.1. Budget report.......................................................................................................................9

2.5.2. Accounts Receivable Aging Reports....................................................................................10

2.5.3. Job cost reports..................................................................................................................10

2.5.4. Inventory and Manufacturing report..................................................................................11

3. How organizations are adapting their management accounting Systems to deal with financial

problems.............................................................................................................................................11

4. Conclusion.......................................................................................................................................13

References..........................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Vietnam Dairy Products

Joint– Stock Company

1. Introduction

Vietnam Dairy Products Joint- Stock Company is currently the leading enterprise in the dairy

industry in Vietnam. The brand has been around for 40 years, it has become the most

mentioned national brand in the field of nutritional milk. Looking back on 2020, it was a really

tough first year for any business. However, to complete the tasks in 2020, the Board of

Directors and all employees have done their best. They have achieved many achievements and

are well received and trusted by partners and customers. Vinamilk‘s business results in

2020 achieved as follows:

o Total revenue in 2020: 59,723 billion VND, up 5.9% over the same period in 2019

and complete 100% of the year plan.

o Profit after tax in 2020: 11,236 billion VND, complete 105% of the year plan.

I’m a member of the Financial Governance committee of Vietnam Dairy Products Joint-

Stock Company. Our committee has to prepare an annual report for the shareholders’

meeting and I am in charge of writing this time.

2. Management accounting

2.1. Definition of Management accounting

Management accounting is the identification, measurement, analysis, interpretation and

communication of financial information to managers so that they can pursue organizational

goals. It differs from financial accounting because the intended purpose of management

accounting is to assist a company's internal users in making informed business decisions.

(Managerial Accounting Definition, 2021)

Joint– Stock Company

1. Introduction

Vietnam Dairy Products Joint- Stock Company is currently the leading enterprise in the dairy

industry in Vietnam. The brand has been around for 40 years, it has become the most

mentioned national brand in the field of nutritional milk. Looking back on 2020, it was a really

tough first year for any business. However, to complete the tasks in 2020, the Board of

Directors and all employees have done their best. They have achieved many achievements and

are well received and trusted by partners and customers. Vinamilk‘s business results in

2020 achieved as follows:

o Total revenue in 2020: 59,723 billion VND, up 5.9% over the same period in 2019

and complete 100% of the year plan.

o Profit after tax in 2020: 11,236 billion VND, complete 105% of the year plan.

I’m a member of the Financial Governance committee of Vietnam Dairy Products Joint-

Stock Company. Our committee has to prepare an annual report for the shareholders’

meeting and I am in charge of writing this time.

2. Management accounting

2.1. Definition of Management accounting

Management accounting is the identification, measurement, analysis, interpretation and

communication of financial information to managers so that they can pursue organizational

goals. It differs from financial accounting because the intended purpose of management

accounting is to assist a company's internal users in making informed business decisions.

(Managerial Accounting Definition, 2021)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.2. Roles of Management accounting

2.2.1. Stewardship Accounting

Management accountants will have a role in designing the framework of cost and financial

accounts and preparing reports for the company to make regular financial and operating

decisions.

2.2.2. Long-term and Short-Term Planning

Management accounting plays an important role in forecasting upcoming business and

economic events so that the company can make future plans including long-term planning,

strategic management accounting, building corporate strategy, market research, etc.

2.2.3. Developing Management Information System (MIS)

Periodic reports and long-term decision-making reports are communicated to managers at

all levels to take corrective actions at the right time. At the same time, management

accountants can also use these reports to make important decisions.

2.2.4. Maintaining Optimum Capital Structure

Management accounting has a key role in raising capital and their application. The MA must

decide on maintaining the right mix of debt and equity. Raising capital through debt is

cheaper because of the tax advantages.

However, this is very risky because interest must be paid on the debt whether or not the

company is fully profitable. Therefore, management accountants must maintain an optimal

capital structure and give due consideration to the theories of cost of capital, leverage, and

business viability on equity.

2.2.5. Participating in Management Process

Management accounting occupies an important position in the organization. The MA performs

the staff function and also has authority over the accountants and other employees

2.2.1. Stewardship Accounting

Management accountants will have a role in designing the framework of cost and financial

accounts and preparing reports for the company to make regular financial and operating

decisions.

2.2.2. Long-term and Short-Term Planning

Management accounting plays an important role in forecasting upcoming business and

economic events so that the company can make future plans including long-term planning,

strategic management accounting, building corporate strategy, market research, etc.

2.2.3. Developing Management Information System (MIS)

Periodic reports and long-term decision-making reports are communicated to managers at

all levels to take corrective actions at the right time. At the same time, management

accountants can also use these reports to make important decisions.

2.2.4. Maintaining Optimum Capital Structure

Management accounting has a key role in raising capital and their application. The MA must

decide on maintaining the right mix of debt and equity. Raising capital through debt is

cheaper because of the tax advantages.

However, this is very risky because interest must be paid on the debt whether or not the

company is fully profitable. Therefore, management accountants must maintain an optimal

capital structure and give due consideration to the theories of cost of capital, leverage, and

business viability on equity.

2.2.5. Participating in Management Process

Management accounting occupies an important position in the organization. The MA performs

the staff function and also has authority over the accountants and other employees

in its office. It educates executives about the need for control information and how to use

it. It also transmits relevant information from the same stakeholders and reports in clear

form to management and sometimes to external interested parties.

2.2.6. Controlling

Management accountants analyze accounts and prepare reports such as standard costs,

budgets, analysis and interpretation of variance, cash and fund flow analysis, liquidity

management, performance reviews and responsibility accounting, etc. to control.

2.2.7. Decision-Making

Management accounting provides the information needed by management in making short

term decisions such as optimal product mix, make-or-buy, product pricing, product

discontinuation, etc. and long-term decisions such as capital budgeting, investment

appraisal, project financing, etc.

However, the work of management accountants is limited to providing the necessary

information in a comprehensive and reliable form to management for decision-making

purposes. But the actual decision-making responsibility rests with management. In other

words, neither management accounting nor internal accounting reports can make decisions

for the management.

2.3. Comparison of Financial accounting and Management accounting

There are two differences between financial accounting and management accounting:

o Management accounting is presented to the company's internal community, while

financial accounting is presented to external audiences. In other words, financial

accounting is important for current and potential investors, while management

accounting is essential for managers to make current and future financial decisions

for the business.

o Management accounting can be based on estimates because most managers don't

have time to get exact numbers at the time they need to make a decision, whereas

it. It also transmits relevant information from the same stakeholders and reports in clear

form to management and sometimes to external interested parties.

2.2.6. Controlling

Management accountants analyze accounts and prepare reports such as standard costs,

budgets, analysis and interpretation of variance, cash and fund flow analysis, liquidity

management, performance reviews and responsibility accounting, etc. to control.

2.2.7. Decision-Making

Management accounting provides the information needed by management in making short

term decisions such as optimal product mix, make-or-buy, product pricing, product

discontinuation, etc. and long-term decisions such as capital budgeting, investment

appraisal, project financing, etc.

However, the work of management accountants is limited to providing the necessary

information in a comprehensive and reliable form to management for decision-making

purposes. But the actual decision-making responsibility rests with management. In other

words, neither management accounting nor internal accounting reports can make decisions

for the management.

2.3. Comparison of Financial accounting and Management accounting

There are two differences between financial accounting and management accounting:

o Management accounting is presented to the company's internal community, while

financial accounting is presented to external audiences. In other words, financial

accounting is important for current and potential investors, while management

accounting is essential for managers to make current and future financial decisions

for the business.

o Management accounting can be based on estimates because most managers don't

have time to get exact numbers at the time they need to make a decision, whereas

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

financial accounting is precise and must be done. Comply with Generally Accepted

Accounting Principles (GAAP)

2.4. Different types of MA systems

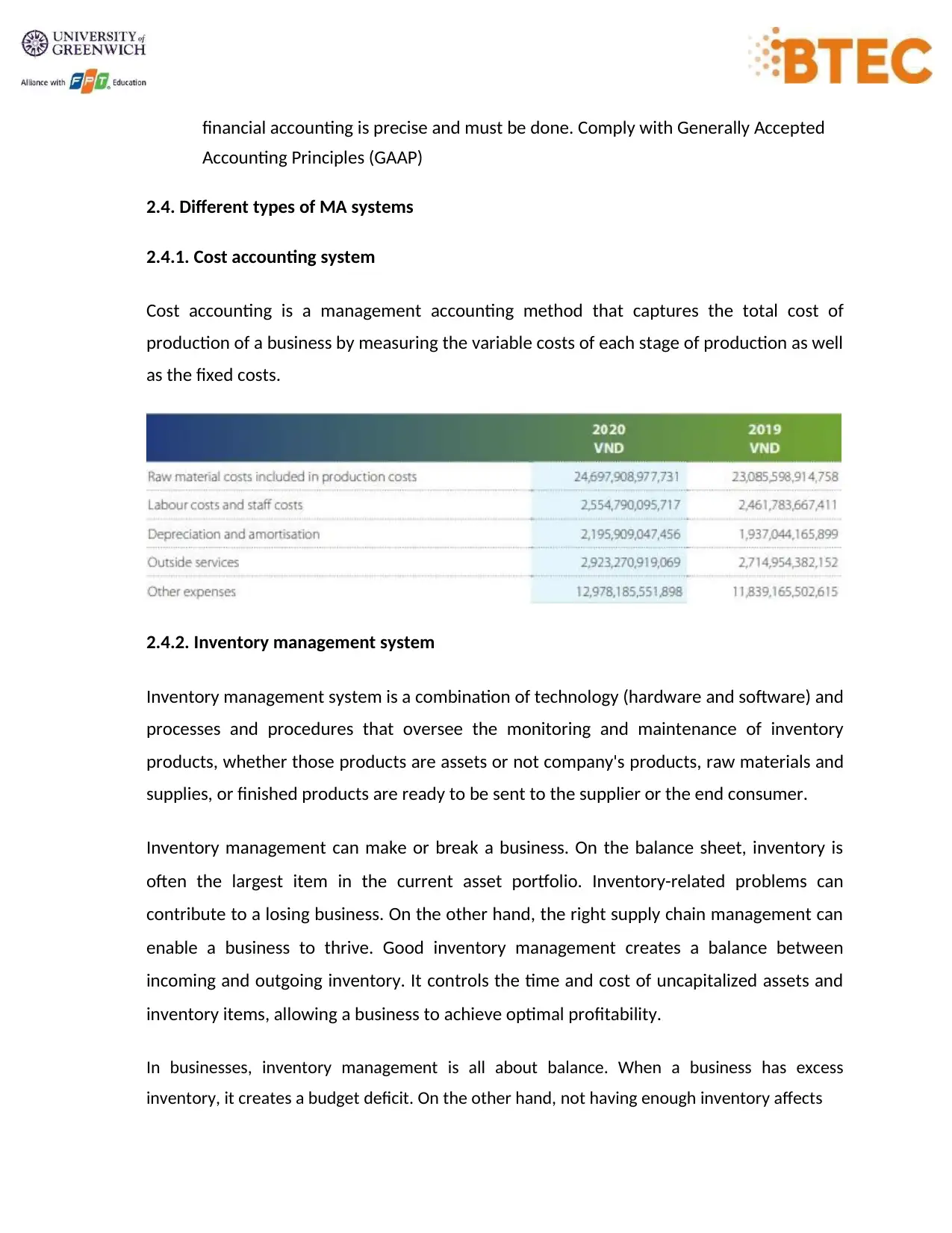

2.4.1. Cost accounting system

Cost accounting is a management accounting method that captures the total cost of

production of a business by measuring the variable costs of each stage of production as well

as the fixed costs.

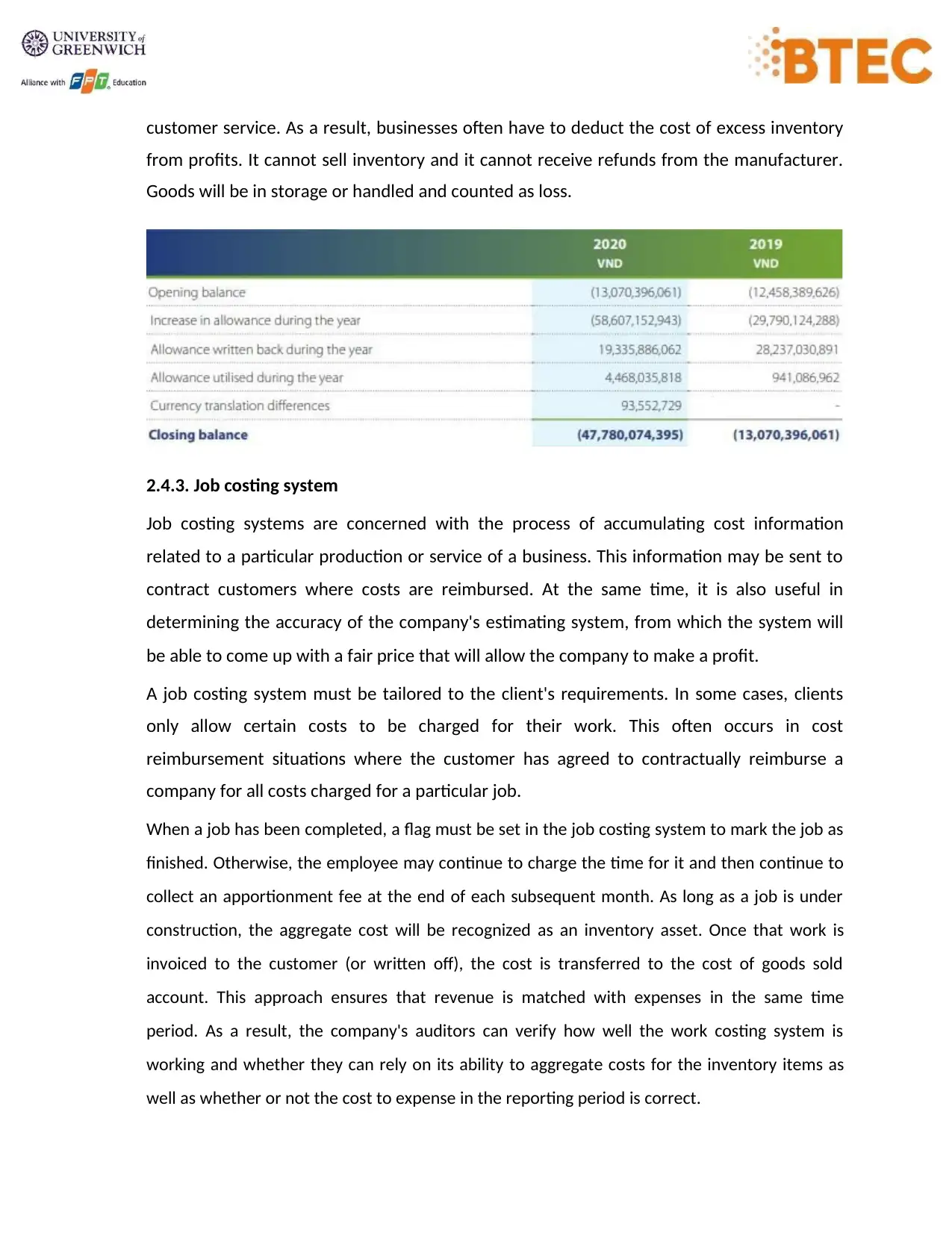

2.4.2. Inventory management system

Inventory management system is a combination of technology (hardware and software) and

processes and procedures that oversee the monitoring and maintenance of inventory

products, whether those products are assets or not company's products, raw materials and

supplies, or finished products are ready to be sent to the supplier or the end consumer.

Inventory management can make or break a business. On the balance sheet, inventory is

often the largest item in the current asset portfolio. Inventory-related problems can

contribute to a losing business. On the other hand, the right supply chain management can

enable a business to thrive. Good inventory management creates a balance between

incoming and outgoing inventory. It controls the time and cost of uncapitalized assets and

inventory items, allowing a business to achieve optimal profitability.

In businesses, inventory management is all about balance. When a business has excess

inventory, it creates a budget deficit. On the other hand, not having enough inventory affects

Accounting Principles (GAAP)

2.4. Different types of MA systems

2.4.1. Cost accounting system

Cost accounting is a management accounting method that captures the total cost of

production of a business by measuring the variable costs of each stage of production as well

as the fixed costs.

2.4.2. Inventory management system

Inventory management system is a combination of technology (hardware and software) and

processes and procedures that oversee the monitoring and maintenance of inventory

products, whether those products are assets or not company's products, raw materials and

supplies, or finished products are ready to be sent to the supplier or the end consumer.

Inventory management can make or break a business. On the balance sheet, inventory is

often the largest item in the current asset portfolio. Inventory-related problems can

contribute to a losing business. On the other hand, the right supply chain management can

enable a business to thrive. Good inventory management creates a balance between

incoming and outgoing inventory. It controls the time and cost of uncapitalized assets and

inventory items, allowing a business to achieve optimal profitability.

In businesses, inventory management is all about balance. When a business has excess

inventory, it creates a budget deficit. On the other hand, not having enough inventory affects

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

customer service. As a result, businesses often have to deduct the cost of excess inventory

from profits. It cannot sell inventory and it cannot receive refunds from the manufacturer.

Goods will be in storage or handled and counted as loss.

2.4.3. Job costing system

Job costing systems are concerned with the process of accumulating cost information

related to a particular production or service of a business. This information may be sent to

contract customers where costs are reimbursed. At the same time, it is also useful in

determining the accuracy of the company's estimating system, from which the system will

be able to come up with a fair price that will allow the company to make a profit.

A job costing system must be tailored to the client's requirements. In some cases, clients

only allow certain costs to be charged for their work. This often occurs in cost

reimbursement situations where the customer has agreed to contractually reimburse a

company for all costs charged for a particular job.

When a job has been completed, a flag must be set in the job costing system to mark the job as

finished. Otherwise, the employee may continue to charge the time for it and then continue to

collect an apportionment fee at the end of each subsequent month. As long as a job is under

construction, the aggregate cost will be recognized as an inventory asset. Once that work is

invoiced to the customer (or written off), the cost is transferred to the cost of goods sold

account. This approach ensures that revenue is matched with expenses in the same time

period. As a result, the company's auditors can verify how well the work costing system is

working and whether they can rely on its ability to aggregate costs for the inventory items as

well as whether or not the cost to expense in the reporting period is correct.

from profits. It cannot sell inventory and it cannot receive refunds from the manufacturer.

Goods will be in storage or handled and counted as loss.

2.4.3. Job costing system

Job costing systems are concerned with the process of accumulating cost information

related to a particular production or service of a business. This information may be sent to

contract customers where costs are reimbursed. At the same time, it is also useful in

determining the accuracy of the company's estimating system, from which the system will

be able to come up with a fair price that will allow the company to make a profit.

A job costing system must be tailored to the client's requirements. In some cases, clients

only allow certain costs to be charged for their work. This often occurs in cost

reimbursement situations where the customer has agreed to contractually reimburse a

company for all costs charged for a particular job.

When a job has been completed, a flag must be set in the job costing system to mark the job as

finished. Otherwise, the employee may continue to charge the time for it and then continue to

collect an apportionment fee at the end of each subsequent month. As long as a job is under

construction, the aggregate cost will be recognized as an inventory asset. Once that work is

invoiced to the customer (or written off), the cost is transferred to the cost of goods sold

account. This approach ensures that revenue is matched with expenses in the same time

period. As a result, the company's auditors can verify how well the work costing system is

working and whether they can rely on its ability to aggregate costs for the inventory items as

well as whether or not the cost to expense in the reporting period is correct.

2.4.4. Price optimization system

Price optimization is the process of finding a pricing sweet spot, or maximising price against

the customers willingness to pay. Companies up and down the supply chain will rightly

dedicate a massive amount of time towards price optimization to ensure that their products

can sell quickly at the right price while still making a decent profit.

The low-cost strategy that is quite familiar to many businesses is one of the pricing

strategies that Vinamilk applies. When applying this strategy, Vinamilk pursues the goal of

outperforming its competitors. In the dairy market with competition from more than 40

businesses and hundreds of milk brands from multinational corporations, Vinamilk creates

products at a lower cost than foreign companies. Therefore, Vinamilk still has a firm

foothold in the turbulent market. The most obvious effect is when the brand's market share

has gradually increased from 17% - 25% - 50% of the national market share.

Not only that, Vinamilk is also very careful with raising product prices because this has a great

impact on the ability of consumers in the context that the income of Vietnamese people is not

equal to many countries in the world. By cutting possible costs, restructuring brands, controlling

retail locations so that sales do not depend on wholesalers, the company has saved a lot of

promotional costs. The phenomena of holding goods, discharging goods, competing on price

and geographically, thanks to the promotional price advantages of big agents have been solved.

This strategy not only increases operational efficiency for the company, but also stabilizes prices

and brings practical benefits to consumers.

2.5. Different methods used for management accounting reporting

2.5.1. Budget report

Budget reports are report that help you see how close the estimated budget was to the actual

financial numbers during a certain accounting period, the period could be a month, quarter or

year. These reports typically serve as the company's financial goals. If a financial report doesn't

reach the goals projected in the budget report, employees can determine which are the

problems that keep them from hitting these projected goals by comparing the two

Price optimization is the process of finding a pricing sweet spot, or maximising price against

the customers willingness to pay. Companies up and down the supply chain will rightly

dedicate a massive amount of time towards price optimization to ensure that their products

can sell quickly at the right price while still making a decent profit.

The low-cost strategy that is quite familiar to many businesses is one of the pricing

strategies that Vinamilk applies. When applying this strategy, Vinamilk pursues the goal of

outperforming its competitors. In the dairy market with competition from more than 40

businesses and hundreds of milk brands from multinational corporations, Vinamilk creates

products at a lower cost than foreign companies. Therefore, Vinamilk still has a firm

foothold in the turbulent market. The most obvious effect is when the brand's market share

has gradually increased from 17% - 25% - 50% of the national market share.

Not only that, Vinamilk is also very careful with raising product prices because this has a great

impact on the ability of consumers in the context that the income of Vietnamese people is not

equal to many countries in the world. By cutting possible costs, restructuring brands, controlling

retail locations so that sales do not depend on wholesalers, the company has saved a lot of

promotional costs. The phenomena of holding goods, discharging goods, competing on price

and geographically, thanks to the promotional price advantages of big agents have been solved.

This strategy not only increases operational efficiency for the company, but also stabilizes prices

and brings practical benefits to consumers.

2.5. Different methods used for management accounting reporting

2.5.1. Budget report

Budget reports are report that help you see how close the estimated budget was to the actual

financial numbers during a certain accounting period, the period could be a month, quarter or

year. These reports typically serve as the company's financial goals. If a financial report doesn't

reach the goals projected in the budget report, employees can determine which are the

problems that keep them from hitting these projected goals by comparing the two

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

reports. These comparision can help employees determine how accurate or reasonable

their financial predictions were for the previous period to adjust the upcoming budget

report and make more realistic future predictions.

In the whole year of 2020, Vinamilk's total consolidated revenue reached VND 59,723

billion, up 5.9% over the same period in 2019 and completing 100% of the year plan.

Consolidated net revenue reached VND 59,636 billion, of which, domestic net revenue

reached VND 50,842 billion, up 6.9% with market share maintained compared to 2019

thanks to appropriate marketing strategy. For the whole year of 2020, consolidated profit

after tax reached VND 11,236 billion, up 6.5% and compared to the same period in 2019,

completing 105% of the year plan.

2.5.2. Accounts Receivable Aging Reports

This is a report that categorizes and lists a company's receivables by unpaid customer

invoices. It is a tool commonly used by collections personnel as a metric to determine the

financial health of a company's customers. Reports can be configured to contain contact

information for each customer. The report is also used to determine the effectiveness of

the credit and collection functions by management.

Based on Vinamilk's 2020 annual report, we can see that the receivables from customers in

2020 is VND 5,335,735 million and in 2019 is VND 4,637,582 million. Receivables from

customers in 2020 have increased significantly compared to 2019, which shows that

customers are slow to pay the business. At the same time, Vinamilk's revenue also

increased significantly (as mentioned in the Budget report), so we can see that the policy

that Vinamilk is using has been on the right track.

2.5.3. Job cost reports

This is a report known as a crucial component for running a business in the construction sector

because it will tell construction companies that want to know if their project is within budget. It

continuously tracks the cost of a construction project, giving a company insight into

their financial predictions were for the previous period to adjust the upcoming budget

report and make more realistic future predictions.

In the whole year of 2020, Vinamilk's total consolidated revenue reached VND 59,723

billion, up 5.9% over the same period in 2019 and completing 100% of the year plan.

Consolidated net revenue reached VND 59,636 billion, of which, domestic net revenue

reached VND 50,842 billion, up 6.9% with market share maintained compared to 2019

thanks to appropriate marketing strategy. For the whole year of 2020, consolidated profit

after tax reached VND 11,236 billion, up 6.5% and compared to the same period in 2019,

completing 105% of the year plan.

2.5.2. Accounts Receivable Aging Reports

This is a report that categorizes and lists a company's receivables by unpaid customer

invoices. It is a tool commonly used by collections personnel as a metric to determine the

financial health of a company's customers. Reports can be configured to contain contact

information for each customer. The report is also used to determine the effectiveness of

the credit and collection functions by management.

Based on Vinamilk's 2020 annual report, we can see that the receivables from customers in

2020 is VND 5,335,735 million and in 2019 is VND 4,637,582 million. Receivables from

customers in 2020 have increased significantly compared to 2019, which shows that

customers are slow to pay the business. At the same time, Vinamilk's revenue also

increased significantly (as mentioned in the Budget report), so we can see that the policy

that Vinamilk is using has been on the right track.

2.5.3. Job cost reports

This is a report known as a crucial component for running a business in the construction sector

because it will tell construction companies that want to know if their project is within budget. It

continuously tracks the cost of a construction project, giving a company insight into

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

production efficiency, detecting missing change orders, providing data to estimates in the

future and they may affect the company's bottom line.

2.5.4. Inventory and Manufacturing report

Inventory and manufacturing report will provide manufacturers the information about the

values of sales and product inventory. At the same time, this report can also provide

indicators of economic growth or decline such as sales ratios, how long will the existing

inventories can last under the current sales conditions, and rates of change.

3. How organizations are adapting their management accounting Systems to deal with

financial problems

The COVID-19 epidemic has caused unprecedented difficulties to the economy and the

dairy industry is no exception. Although milk is one of the essential foods in the basket of

goods of Vietnamese consumers, however, the dairy industry grew by negative 6% in 2020

as millions of people were negatively affected by the COVID-19 epidemic- 19 and led to a

decrease in the average income of workers by 2.3% compared to 2019.

To deal with this problem, the digital transformation process has been implemented

quickly, not only at Vinamilk but also in subsidiaries and member companies. At the same

time, a series of other digital transformation projects have been implemented in many

areas of most of Vinamilk's activities such as administration, finance, human resources,

international business and supply chain etc. These tools are an effective arm to help

Vinamilk maintain stability, ensure operational management and performance even when

the business scale is many times larger than the current one.

In particular, management accounting provides information to executives so they can make

important decisions in business operations. The information that management accounting

provides to managers will help them perform the operation, control the organization's

activities and make decisions more quickly. Therefore, executives can make changes based

on the financial statements provided by management accounting to adjust to the actual

situation and development of the company.

future and they may affect the company's bottom line.

2.5.4. Inventory and Manufacturing report

Inventory and manufacturing report will provide manufacturers the information about the

values of sales and product inventory. At the same time, this report can also provide

indicators of economic growth or decline such as sales ratios, how long will the existing

inventories can last under the current sales conditions, and rates of change.

3. How organizations are adapting their management accounting Systems to deal with

financial problems

The COVID-19 epidemic has caused unprecedented difficulties to the economy and the

dairy industry is no exception. Although milk is one of the essential foods in the basket of

goods of Vietnamese consumers, however, the dairy industry grew by negative 6% in 2020

as millions of people were negatively affected by the COVID-19 epidemic- 19 and led to a

decrease in the average income of workers by 2.3% compared to 2019.

To deal with this problem, the digital transformation process has been implemented

quickly, not only at Vinamilk but also in subsidiaries and member companies. At the same

time, a series of other digital transformation projects have been implemented in many

areas of most of Vinamilk's activities such as administration, finance, human resources,

international business and supply chain etc. These tools are an effective arm to help

Vinamilk maintain stability, ensure operational management and performance even when

the business scale is many times larger than the current one.

In particular, management accounting provides information to executives so they can make

important decisions in business operations. The information that management accounting

provides to managers will help them perform the operation, control the organization's

activities and make decisions more quickly. Therefore, executives can make changes based

on the financial statements provided by management accounting to adjust to the actual

situation and development of the company.

Vinamilk has been a famous dairy company for a long time, trusted by many people in Vietnam.

This is the brand's biggest advantage during the pandemic, as customers will often tend to

choose low-cost brands that are already familiar with everyday life. Therefore, Vinamilk will be

able to attract a large number of customers during the current pandemic. Besides, Vinamilk also

takes advantage of its nationwide production and distribution system to help ensure stable

production even when some localities have to implement social distancing. Vinamilk is a dairy

product business, so the cost accounting system is used in the manufacturing industry for the

purpose of tracking inventory flows through each production stage. A cost accounting system

will make it easier for businesses to track raw materials, labor costs and total production costs,

from pre-production to the final product. At the end of each month, it will assist in the

inventory check and cost accounting done by the production manager, thereby providing

accurate information about the expenses required by the Board of Directors. to adjust

operations, as well as advise on how to improve Vinamilk's procedures based on cost

effectiveness and capacity. This helps Vinamilk come up with the best policies so that the

company can satisfy both customers and target revenue during the pandemic. As a result, the

business was able to achieve unbelievable revenue with a total consolidated revenue of VND

59,723 billion, up 5.9% over the same period in 2019.

Meanwhile, the complicated situation of the Covid-19 epidemic, affecting the production

and business activities of Vinasoy Company, the consumption of Vinasoy soy milk products

decreased by 10%. With revenue down 130 billion dong, equivalent to 7% year-on-year,

while COGS remained approximately the same period last year, gross profit decreased by

18%. Vinasoy's 3rd quarter gross profit margin shrank to 32%, while the same period

achieved 36%. Accordingly, the company's net profit in the third quarter of 2020 decreased

by 19% over the same period, to more than 233 billion dong. (Fili, 2021)

This shows that Vinasoy has not really applied and effectively used the cost accounting

system. The Covid 19 epidemic is completely inevitable, Vinamilk also suffers, but with the

cheap policy, Vinamilk has made a profit instead of a loss. It is the good application of an

effective cost accounting system that will help the company know the cost of production or

This is the brand's biggest advantage during the pandemic, as customers will often tend to

choose low-cost brands that are already familiar with everyday life. Therefore, Vinamilk will be

able to attract a large number of customers during the current pandemic. Besides, Vinamilk also

takes advantage of its nationwide production and distribution system to help ensure stable

production even when some localities have to implement social distancing. Vinamilk is a dairy

product business, so the cost accounting system is used in the manufacturing industry for the

purpose of tracking inventory flows through each production stage. A cost accounting system

will make it easier for businesses to track raw materials, labor costs and total production costs,

from pre-production to the final product. At the end of each month, it will assist in the

inventory check and cost accounting done by the production manager, thereby providing

accurate information about the expenses required by the Board of Directors. to adjust

operations, as well as advise on how to improve Vinamilk's procedures based on cost

effectiveness and capacity. This helps Vinamilk come up with the best policies so that the

company can satisfy both customers and target revenue during the pandemic. As a result, the

business was able to achieve unbelievable revenue with a total consolidated revenue of VND

59,723 billion, up 5.9% over the same period in 2019.

Meanwhile, the complicated situation of the Covid-19 epidemic, affecting the production

and business activities of Vinasoy Company, the consumption of Vinasoy soy milk products

decreased by 10%. With revenue down 130 billion dong, equivalent to 7% year-on-year,

while COGS remained approximately the same period last year, gross profit decreased by

18%. Vinasoy's 3rd quarter gross profit margin shrank to 32%, while the same period

achieved 36%. Accordingly, the company's net profit in the third quarter of 2020 decreased

by 19% over the same period, to more than 233 billion dong. (Fili, 2021)

This shows that Vinasoy has not really applied and effectively used the cost accounting

system. The Covid 19 epidemic is completely inevitable, Vinamilk also suffers, but with the

cheap policy, Vinamilk has made a profit instead of a loss. It is the good application of an

effective cost accounting system that will help the company know the cost of production or

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.