Management Accounting Report: Marginal & Absorption Costing Methods

VerifiedAdded on 2022/12/01

|12

|1351

|483

Report

AI Summary

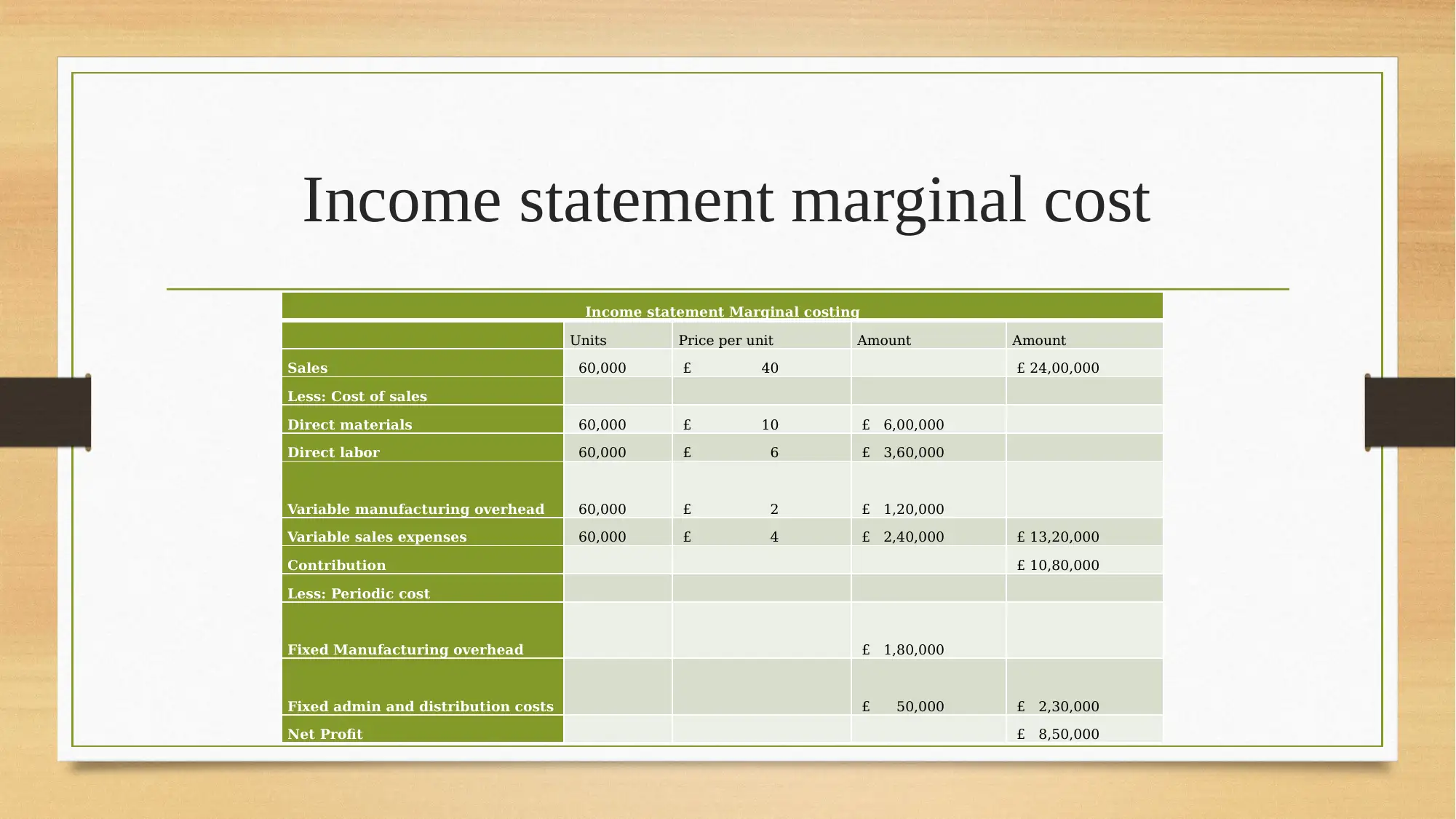

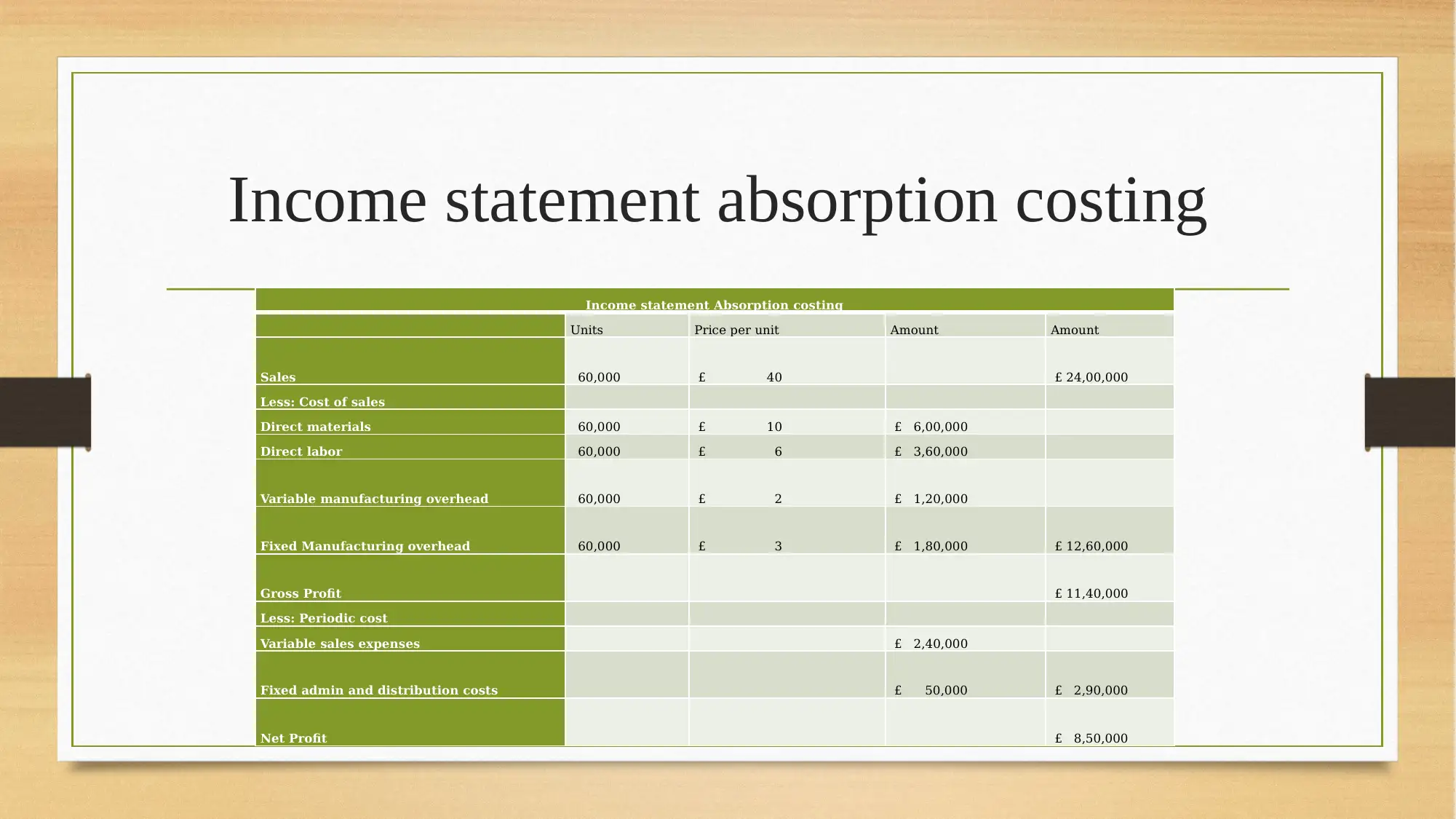

This report delves into the core concepts of management accounting, using Jeloa Limited as a case study. It explores cost analysis, including direct, indirect, fixed, and variable costs, and examines flexible budgeting and cost variance analysis. The report clarifies marginal and absorption costing methods, detailing their applications through income statements. It also covers valuation methods like LIFO and FIFO and discusses the collection and management of overhead costs. The conclusion emphasizes the role of management accounting in decision-making and financial sustainability, highlighting the importance of techniques such as KPI and Benchmarking.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.