Management Accounting Report: Analyzing Vitacoco's Financials

VerifiedAdded on 2021/10/06

|126

|39645

|53

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application to Vitacoco, a coconut water producer. The report begins with an overview of management accounting, its roles, and principles, including cost accounting, inventory management, and price optimization systems. It differentiates between management and financial accounting, highlighting the qualitative characteristics of useful financial information. The report then delves into various management accounting reports, such as accounts receivable aging and cost accounting reports, and critically evaluates the impact of management accounting systems. It explores budgetary control as a planning tool, examining different types of budgets and analyzing planning tools like the Balanced Scorecard and Porter's Five Forces. Furthermore, the report discusses financial governance, benchmarks, and financial and non-financial KPIs. It analyzes financial problems faced by organizations and provides insights into how Vitacoco can adapt its management accounting systems to respond to financial challenges and achieve sustainable success, incorporating the characteristics and skills of effective management accountants and information systems. The report concludes with a detailed evaluation of accounting planning tools and their role in solving financial problems and leading Vitacoco to sustainable growth.

Zun Thet Hmu San

UB-05-19

AUGUST 28, 2020

UB-05-19

AUGUST 28, 2020

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

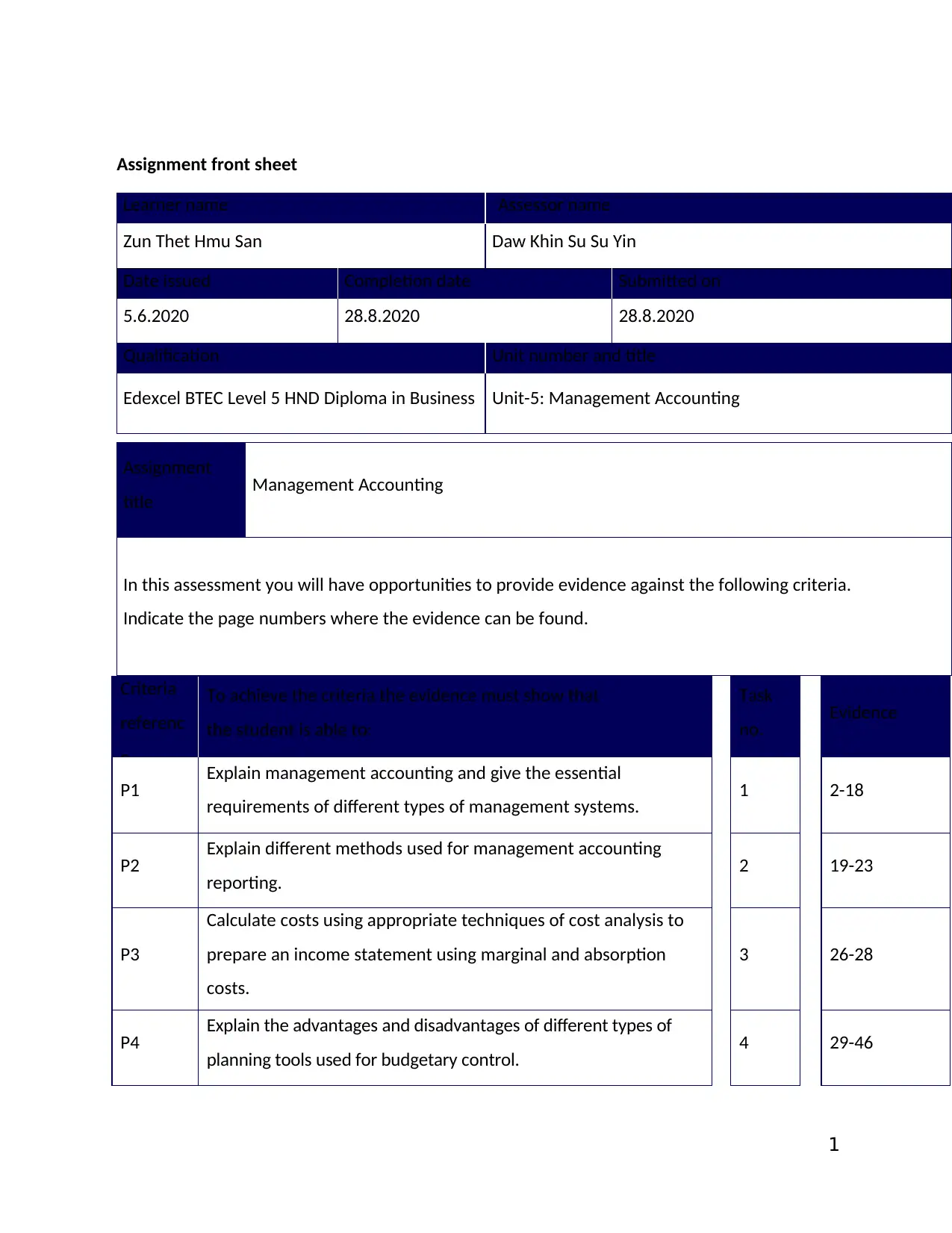

Assignment front sheet

Learner name Assessor name

Zun Thet Hmu San Daw Khin Su Su Yin

Date issued Completion date Submitted on

5.6.2020 28.8.2020 28.8.2020

Qualification Unit number and title

Edexcel BTEC Level 5 HND Diploma in Business Unit-5: Management Accounting

Assignment

title Management Accounting

In this assessment you will have opportunities to provide evidence against the following criteria.

Indicate the page numbers where the evidence can be found.

Criteria

referenc

e

To achieve the criteria the evidence must show that

the student is able to:

Task

no. Evidence

P1 Explain management accounting and give the essential

requirements of different types of management systems. 1 2-18

P2 Explain different methods used for management accounting

reporting. 2 19-23

P3

Calculate costs using appropriate techniques of cost analysis to

prepare an income statement using marginal and absorption

costs.

3 26-28

P4 Explain the advantages and disadvantages of different types of

planning tools used for budgetary control. 4 29-46

1

Learner name Assessor name

Zun Thet Hmu San Daw Khin Su Su Yin

Date issued Completion date Submitted on

5.6.2020 28.8.2020 28.8.2020

Qualification Unit number and title

Edexcel BTEC Level 5 HND Diploma in Business Unit-5: Management Accounting

Assignment

title Management Accounting

In this assessment you will have opportunities to provide evidence against the following criteria.

Indicate the page numbers where the evidence can be found.

Criteria

referenc

e

To achieve the criteria the evidence must show that

the student is able to:

Task

no. Evidence

P1 Explain management accounting and give the essential

requirements of different types of management systems. 1 2-18

P2 Explain different methods used for management accounting

reporting. 2 19-23

P3

Calculate costs using appropriate techniques of cost analysis to

prepare an income statement using marginal and absorption

costs.

3 26-28

P4 Explain the advantages and disadvantages of different types of

planning tools used for budgetary control. 4 29-46

1

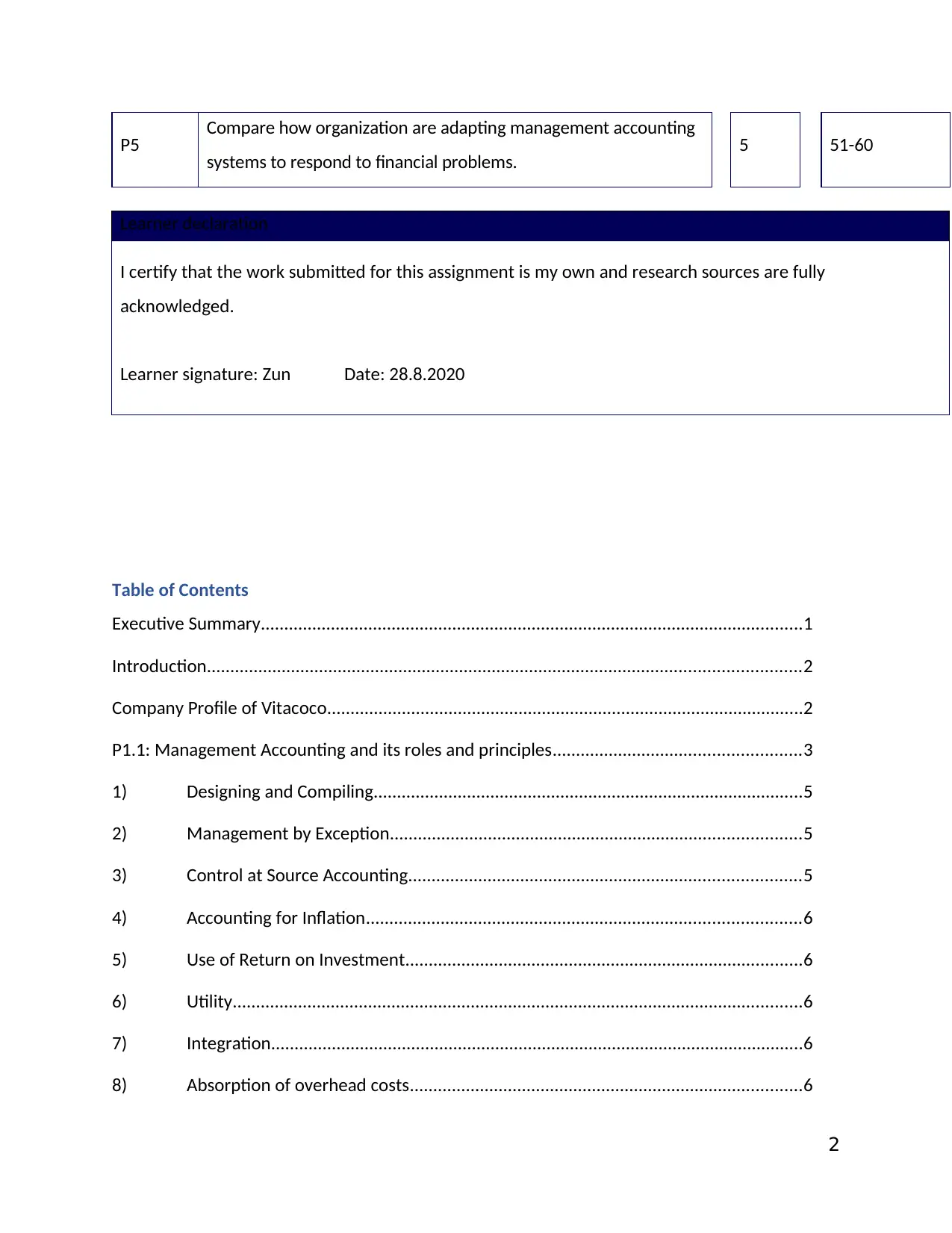

P5 Compare how organization are adapting management accounting

systems to respond to financial problems. 5 51-60

Table of Contents

Executive Summary....................................................................................................................1

Introduction...............................................................................................................................2

Company Profile of Vitacoco......................................................................................................2

P1.1: Management Accounting and its roles and principles.....................................................3

1) Designing and Compiling............................................................................................5

2) Management by Exception........................................................................................5

3) Control at Source Accounting....................................................................................5

4) Accounting for Inflation.............................................................................................6

5) Use of Return on Investment.....................................................................................6

6) Utility..........................................................................................................................6

7) Integration..................................................................................................................6

8) Absorption of overhead costs....................................................................................6

2

Learner declaration

I certify that the work submitted for this assignment is my own and research sources are fully

acknowledged.

Learner signature: Zun Date: 28.8.2020

systems to respond to financial problems. 5 51-60

Table of Contents

Executive Summary....................................................................................................................1

Introduction...............................................................................................................................2

Company Profile of Vitacoco......................................................................................................2

P1.1: Management Accounting and its roles and principles.....................................................3

1) Designing and Compiling............................................................................................5

2) Management by Exception........................................................................................5

3) Control at Source Accounting....................................................................................5

4) Accounting for Inflation.............................................................................................6

5) Use of Return on Investment.....................................................................................6

6) Utility..........................................................................................................................6

7) Integration..................................................................................................................6

8) Absorption of overhead costs....................................................................................6

2

Learner declaration

I certify that the work submitted for this assignment is my own and research sources are fully

acknowledged.

Learner signature: Zun Date: 28.8.2020

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9) Utilization of Resources.............................................................................................6

10) Controllable and Uncontrollable costs..................................................................6

11) Forward-Looking Approach....................................................................................7

12) Appropriate means................................................................................................7

13) Personal contacts...................................................................................................7

P1.2: Management Accounting Systems with their benefits....................................................7

Cost Accounting System.............................................................................................................7

Classification of Costs.................................................................................................................7

Benefits and Limitations of Cost Accounting System..............................................................10

Inventory Management System...............................................................................................11

Price-Optimizing System..........................................................................................................12

Pricing Policies..........................................................................................................................12

Management Accounting Systems in Vitacoco........................................................................13

Cost Accounting System...........................................................................................................13

Inventory Management System...............................................................................................14

Price Optimizing System..........................................................................................................14

P2.1: Differences between Management Accounting and Financial Accounting....................15

P2.2: Qualitative Characteristics of useful financial information............................................16

Relevant...................................................................................................................................16

Reliable.....................................................................................................................................16

Understandable........................................................................................................................16

Comparability...........................................................................................................................17

Consistency..............................................................................................................................17

P2.3: Types of Management Accounting Reports with their benefits.....................................17

3

10) Controllable and Uncontrollable costs..................................................................6

11) Forward-Looking Approach....................................................................................7

12) Appropriate means................................................................................................7

13) Personal contacts...................................................................................................7

P1.2: Management Accounting Systems with their benefits....................................................7

Cost Accounting System.............................................................................................................7

Classification of Costs.................................................................................................................7

Benefits and Limitations of Cost Accounting System..............................................................10

Inventory Management System...............................................................................................11

Price-Optimizing System..........................................................................................................12

Pricing Policies..........................................................................................................................12

Management Accounting Systems in Vitacoco........................................................................13

Cost Accounting System...........................................................................................................13

Inventory Management System...............................................................................................14

Price Optimizing System..........................................................................................................14

P2.1: Differences between Management Accounting and Financial Accounting....................15

P2.2: Qualitative Characteristics of useful financial information............................................16

Relevant...................................................................................................................................16

Reliable.....................................................................................................................................16

Understandable........................................................................................................................16

Comparability...........................................................................................................................17

Consistency..............................................................................................................................17

P2.3: Types of Management Accounting Reports with their benefits.....................................17

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

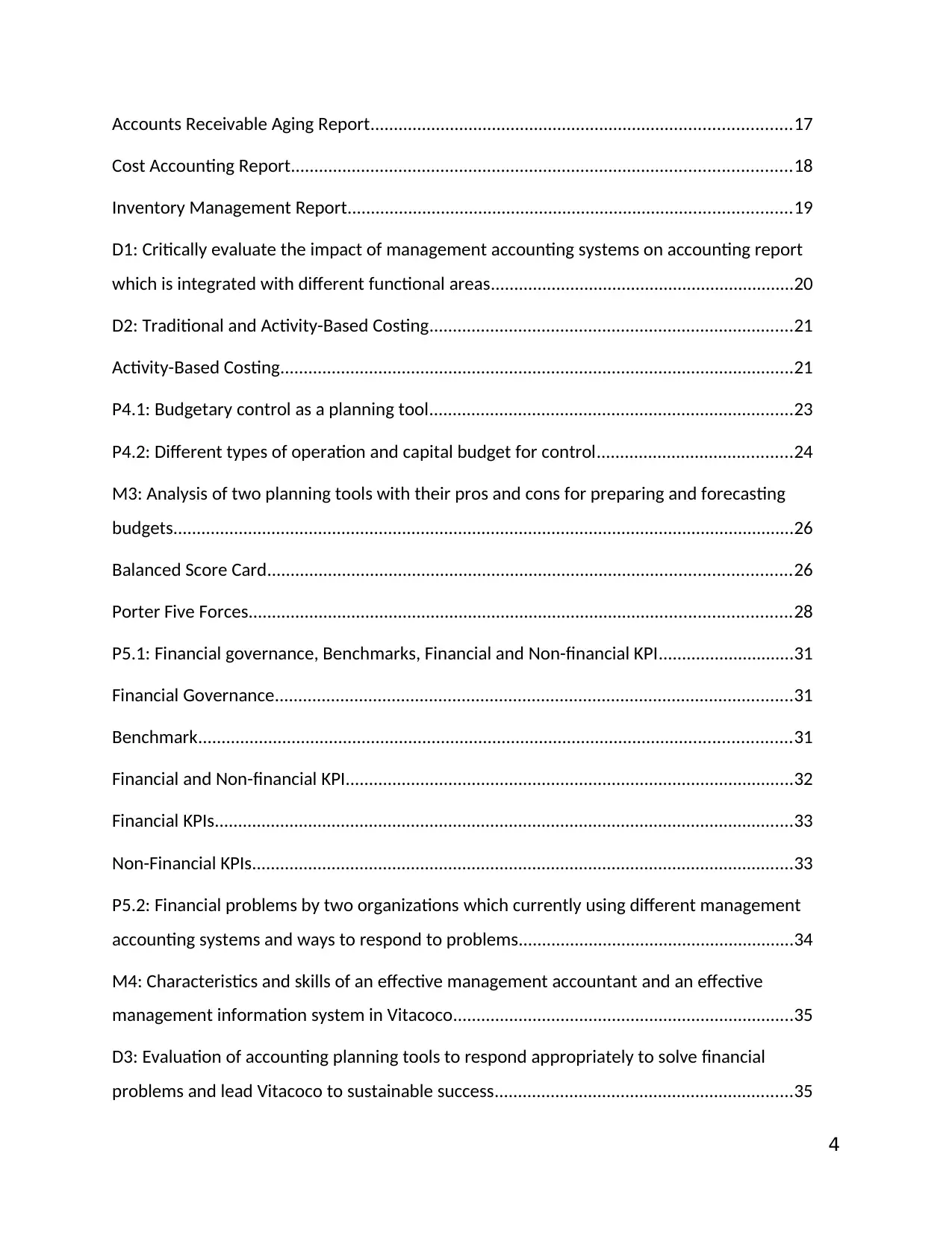

Accounts Receivable Aging Report..........................................................................................17

Cost Accounting Report...........................................................................................................18

Inventory Management Report...............................................................................................19

D1: Critically evaluate the impact of management accounting systems on accounting report

which is integrated with different functional areas.................................................................20

D2: Traditional and Activity-Based Costing..............................................................................21

Activity-Based Costing..............................................................................................................21

P4.1: Budgetary control as a planning tool..............................................................................23

P4.2: Different types of operation and capital budget for control..........................................24

M3: Analysis of two planning tools with their pros and cons for preparing and forecasting

budgets.....................................................................................................................................26

Balanced Score Card................................................................................................................26

Porter Five Forces....................................................................................................................28

P5.1: Financial governance, Benchmarks, Financial and Non-financial KPI.............................31

Financial Governance...............................................................................................................31

Benchmark...............................................................................................................................31

Financial and Non-financial KPI................................................................................................32

Financial KPIs............................................................................................................................33

Non-Financial KPIs....................................................................................................................33

P5.2: Financial problems by two organizations which currently using different management

accounting systems and ways to respond to problems...........................................................34

M4: Characteristics and skills of an effective management accountant and an effective

management information system in Vitacoco.........................................................................35

D3: Evaluation of accounting planning tools to respond appropriately to solve financial

problems and lead Vitacoco to sustainable success................................................................35

4

Cost Accounting Report...........................................................................................................18

Inventory Management Report...............................................................................................19

D1: Critically evaluate the impact of management accounting systems on accounting report

which is integrated with different functional areas.................................................................20

D2: Traditional and Activity-Based Costing..............................................................................21

Activity-Based Costing..............................................................................................................21

P4.1: Budgetary control as a planning tool..............................................................................23

P4.2: Different types of operation and capital budget for control..........................................24

M3: Analysis of two planning tools with their pros and cons for preparing and forecasting

budgets.....................................................................................................................................26

Balanced Score Card................................................................................................................26

Porter Five Forces....................................................................................................................28

P5.1: Financial governance, Benchmarks, Financial and Non-financial KPI.............................31

Financial Governance...............................................................................................................31

Benchmark...............................................................................................................................31

Financial and Non-financial KPI................................................................................................32

Financial KPIs............................................................................................................................33

Non-Financial KPIs....................................................................................................................33

P5.2: Financial problems by two organizations which currently using different management

accounting systems and ways to respond to problems...........................................................34

M4: Characteristics and skills of an effective management accountant and an effective

management information system in Vitacoco.........................................................................35

D3: Evaluation of accounting planning tools to respond appropriately to solve financial

problems and lead Vitacoco to sustainable success................................................................35

4

Conclusion................................................................................................................................36

References................................................................................................................................37

Executive Summary

This report provides comprehensive management figures related to Vitacoco, a coconut water

producer. First, to understand how to work with a management accountant. It explains the

basics of a management accountant and his principles. Appropriate cost analysis methods are

designed to minimize penetration of income statements. Used to explain differences in

reconciliation values due to differences in results for the above costs. Vitacoco recommends

using action-based cost systems instead of traditional cost systems. Five strengths of the

Balance Scorecard and Porter: Vitacoco has budgeted to increase the accuracy and depth of the

project, and has suggested two more. Learn about the financial problems of soft drink makers

Vitacoco and Zico. It is found that project methods should be systematically incorporated to

solve financial problems and that qualified management accountants should be hired.

Introduction

This report provides an overview of the necessary statistical information from executives and

top executives for decision makers. During the past two decades many organizations have

faced dramatic changes in their environment especially in information technology and global

market arena. To succeed in today’s highly competitive environment, to obtain customer

satisfaction is an overriding priority for every business. Therefore, organizations have adopted

new approaches for their management and ways of doing thing. Companies must adopt a

philosophy of continuous improvement that involves a continuous search to reduce costs,

eliminate waste and improve quality and performance of activities that increases customer

value or satisfaction. This philosophy has significant impact on management accounting system

from traditional role-providing information to managers to monitor the activities of employees.

5

References................................................................................................................................37

Executive Summary

This report provides comprehensive management figures related to Vitacoco, a coconut water

producer. First, to understand how to work with a management accountant. It explains the

basics of a management accountant and his principles. Appropriate cost analysis methods are

designed to minimize penetration of income statements. Used to explain differences in

reconciliation values due to differences in results for the above costs. Vitacoco recommends

using action-based cost systems instead of traditional cost systems. Five strengths of the

Balance Scorecard and Porter: Vitacoco has budgeted to increase the accuracy and depth of the

project, and has suggested two more. Learn about the financial problems of soft drink makers

Vitacoco and Zico. It is found that project methods should be systematically incorporated to

solve financial problems and that qualified management accountants should be hired.

Introduction

This report provides an overview of the necessary statistical information from executives and

top executives for decision makers. During the past two decades many organizations have

faced dramatic changes in their environment especially in information technology and global

market arena. To succeed in today’s highly competitive environment, to obtain customer

satisfaction is an overriding priority for every business. Therefore, organizations have adopted

new approaches for their management and ways of doing thing. Companies must adopt a

philosophy of continuous improvement that involves a continuous search to reduce costs,

eliminate waste and improve quality and performance of activities that increases customer

value or satisfaction. This philosophy has significant impact on management accounting system

from traditional role-providing information to managers to monitor the activities of employees.

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Now, Management accounting supports continuous improvements by identifying opportunities

for changes and then providing information to employees to empower them to focus on the

continuous improvement of customer value. Therefore, every organization should have

awareness on role of management accounting in creating values for customer, business and

society. As a new business, Vitacoco needs to adopt appropriate management accounting

systems to streamline operations and increase profits. Budget control is critical to the

effectiveness and efficiency of Vitacoco. It can be enhanced by other planning tools. According

to the report, Vitacoco is facing financial problems. Companies looking to reduce costs

continuously and eliminate waste to improve the quality and performance of businesses that

increase customer value and satisfaction should embrace the concept of sustainable growth.

This concept has a significant impact on the management accounting system. From information

to managers, it examines the performance of traditional staff.

Company profile

Vitacoco produces and distributes coconut water to keep consumers healthy and refreshed.

Vitacoco Coconut Juice contains a variety of nutrients and flavors, and is included in a modern,

convenient packaging that encourages consumers to maintain a healthy diet and maintain a

healthy lifestyle. Vitacoco obtains fresh coconuts and buys its bottles from trusted suppliers and

manufacturers. Vitacoco uses coconut water as a nutrient and sells it in bottles.

Address: No.105/107, Kha-Yae-Bin Road, between Pyi Daung Su Yeik Tha (Halpin) Road and

Road, Manawhari Road, Yangon 11191. Phone: 01 538 895. Email: vitacoco@gmail.com.

LO-1

P-1.1

For through understanding management accounting area, definition, role, principle and

differences from financial and management accounting are disclosed as a introduction.

Management Accounting

That branch of accounting deals with presenting, providing information management such

systematic perform managerial functions an effective, efficient manner (Bhattacharyya, 2011).

Management Accounting is the accounting system for making decisions of the business

enterprise. Management Accounting furnishes the necessary information to assist the business

6

for changes and then providing information to employees to empower them to focus on the

continuous improvement of customer value. Therefore, every organization should have

awareness on role of management accounting in creating values for customer, business and

society. As a new business, Vitacoco needs to adopt appropriate management accounting

systems to streamline operations and increase profits. Budget control is critical to the

effectiveness and efficiency of Vitacoco. It can be enhanced by other planning tools. According

to the report, Vitacoco is facing financial problems. Companies looking to reduce costs

continuously and eliminate waste to improve the quality and performance of businesses that

increase customer value and satisfaction should embrace the concept of sustainable growth.

This concept has a significant impact on the management accounting system. From information

to managers, it examines the performance of traditional staff.

Company profile

Vitacoco produces and distributes coconut water to keep consumers healthy and refreshed.

Vitacoco Coconut Juice contains a variety of nutrients and flavors, and is included in a modern,

convenient packaging that encourages consumers to maintain a healthy diet and maintain a

healthy lifestyle. Vitacoco obtains fresh coconuts and buys its bottles from trusted suppliers and

manufacturers. Vitacoco uses coconut water as a nutrient and sells it in bottles.

Address: No.105/107, Kha-Yae-Bin Road, between Pyi Daung Su Yeik Tha (Halpin) Road and

Road, Manawhari Road, Yangon 11191. Phone: 01 538 895. Email: vitacoco@gmail.com.

LO-1

P-1.1

For through understanding management accounting area, definition, role, principle and

differences from financial and management accounting are disclosed as a introduction.

Management Accounting

That branch of accounting deals with presenting, providing information management such

systematic perform managerial functions an effective, efficient manner (Bhattacharyya, 2011).

Management Accounting is the accounting system for making decisions of the business

enterprise. Management Accounting furnishes the necessary information to assist the business

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

enterprise to make rational decisions through the development of policies, procedures in order

to meet the day to day commitments of the enterprise (Pandikular, 2009).

Internal financial report that helps manage managers' decision-making processes to achieve

business goals. In other words, it is about understanding financial and cost data and turning

that information into useful information for managers and officers within the organization.

The importance of management accounting

Many companies in order to survive in the competitive market, that is associated with rapidly

changing technology, have to using modern methods to work continuously improve quality

control and reduce the cost of their products. In this situation, many companies are changing

their information systems and to avoid traditional systems and move towards long-term view of

management accounting. Customers are looking for higher wages and shareholders are seeking

a greater share and competition takes place to produce better products with better features

and lower prices. Business success depends on how we manage all these factors and other

factors. Management accounting tools have followed the growing trend in recent years. This

process, with the introduction of ABC, ABM, ABB, Target Costing, Kaizen Costing, Back Flash

costing, JIT, TQM and recently started and tools such as ERP, Six Sigma is reached. Growing

economic competition imposes great pressure on managers to make business decisions in order

to maximize financial performance in this matter. To answer this, need a range of management

accounting techniques have been employed by the Company. The heavy competitive

environment prevailing in the world markets, the use of cost management and continuous

improvement of the organization is one of the critical success factors and managers can only

make the right decision about the efficiency of production and operations That have a good

understanding of how to conduct outreach activities and processes. This system, also

identifying and measuring the cost of the basic activities of the organization, to identify non-

value-added activities and introduce activities that improve organizational performance

Roles of Management Accounting

The following functions related with management accountant to reflect the roles of

management accounting (Mohammad, 2016).

Helping Forecast the Future

7

to meet the day to day commitments of the enterprise (Pandikular, 2009).

Internal financial report that helps manage managers' decision-making processes to achieve

business goals. In other words, it is about understanding financial and cost data and turning

that information into useful information for managers and officers within the organization.

The importance of management accounting

Many companies in order to survive in the competitive market, that is associated with rapidly

changing technology, have to using modern methods to work continuously improve quality

control and reduce the cost of their products. In this situation, many companies are changing

their information systems and to avoid traditional systems and move towards long-term view of

management accounting. Customers are looking for higher wages and shareholders are seeking

a greater share and competition takes place to produce better products with better features

and lower prices. Business success depends on how we manage all these factors and other

factors. Management accounting tools have followed the growing trend in recent years. This

process, with the introduction of ABC, ABM, ABB, Target Costing, Kaizen Costing, Back Flash

costing, JIT, TQM and recently started and tools such as ERP, Six Sigma is reached. Growing

economic competition imposes great pressure on managers to make business decisions in order

to maximize financial performance in this matter. To answer this, need a range of management

accounting techniques have been employed by the Company. The heavy competitive

environment prevailing in the world markets, the use of cost management and continuous

improvement of the organization is one of the critical success factors and managers can only

make the right decision about the efficiency of production and operations That have a good

understanding of how to conduct outreach activities and processes. This system, also

identifying and measuring the cost of the basic activities of the organization, to identify non-

value-added activities and introduce activities that improve organizational performance

Roles of Management Accounting

The following functions related with management accountant to reflect the roles of

management accounting (Mohammad, 2016).

Helping Forecast the Future

7

Management accounting report aims to help in planning, monitoring and in determining

decisions on the way forward. Management accounting reports are designed for offering

internal information to management. Information is not just financial, also all kinds of

information. Management accounting performs decision making and focus the future strategies

in organization (Mohammad, 2016).

Helping in Make-or-buy Decisions

Costs and products are in most cases. Management Accounting provides insights that enable

decision making at both operational and strategic levels (Mohammad, 2016).

Forecasting Cash Flows

Management accounting includes the design of budgets and trend curves, and managers use

this information to determine how money and resources are allocated to generate the

expected revenue increase (Mohammad, 2016).

Helping Understand Performance Variances

Management accounting uses analytical techniques to help management make positive

discrepancies and address negative aspects (Mohammad, 2016).

Develop a financial strategy

The Management Accountant is responsible for sales forecasting and forecasting, among other

management accounting tools. These include gross income; Information may also be included

in the Company's financial statements to develop strategies for equity and revenue growth.

Management accountants play an important role in formulating effective financial strategies,

such as purchasing capital or reducing operating costs for running a business.

Explain the financial consequences of the decisions

Managers can explain if senior leaders adjust the capital structure of their company

Concealment of additional debt or stock supplementation. This includes merging with other

companies’ other decisions are made. For example, start a new operation or fire a large

number of personnel. They can explain how budget and financial statements change a

company's time to determine a company's profit or loss. The company is making good business

decisions, but only by digging out the numbers.

Monitor Expenses

8

decisions on the way forward. Management accounting reports are designed for offering

internal information to management. Information is not just financial, also all kinds of

information. Management accounting performs decision making and focus the future strategies

in organization (Mohammad, 2016).

Helping in Make-or-buy Decisions

Costs and products are in most cases. Management Accounting provides insights that enable

decision making at both operational and strategic levels (Mohammad, 2016).

Forecasting Cash Flows

Management accounting includes the design of budgets and trend curves, and managers use

this information to determine how money and resources are allocated to generate the

expected revenue increase (Mohammad, 2016).

Helping Understand Performance Variances

Management accounting uses analytical techniques to help management make positive

discrepancies and address negative aspects (Mohammad, 2016).

Develop a financial strategy

The Management Accountant is responsible for sales forecasting and forecasting, among other

management accounting tools. These include gross income; Information may also be included

in the Company's financial statements to develop strategies for equity and revenue growth.

Management accountants play an important role in formulating effective financial strategies,

such as purchasing capital or reducing operating costs for running a business.

Explain the financial consequences of the decisions

Managers can explain if senior leaders adjust the capital structure of their company

Concealment of additional debt or stock supplementation. This includes merging with other

companies’ other decisions are made. For example, start a new operation or fire a large

number of personnel. They can explain how budget and financial statements change a

company's time to determine a company's profit or loss. The company is making good business

decisions, but only by digging out the numbers.

Monitor Expenses

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Create a flexible budget with other reports that allow supervisors and department heads to

review costs. This is important. This is because operating costs directly affect bottom-line

profits. Management Accountants can choose the best budgeting method by meeting the

needs of stakeholders. Help the company as much as you can. Stakeholders can create special

reports to make it easier for stakeholders to understand any cost to their department or

organization.

Maintain Profitability

Accountants need to make their business more profitable. It can be used to make a lot of

money, including analyzing breaches. With this type of analysis, accountants compare sales and

costs to determine which company is violating. With sales in mind, management can focus on

production factors as well as other factors that affect profitability. This will help determine the

sales target and overhead cost. In addition, you can manage accounts. Examine direct and

indirect production costs by helping to improve the company's cost structure. Accountants

need to make their business more profitable. It can be used to make a lot of money, including

analyzing breaches. With this type of analysis, accountants compare sales and costs to

determine which company is violating. With sales in mind, management can focus on

production factors as well as other factors that affect profitability. This will help determine the

sales target and overhead cost. In addition, you can manage accounts. Examine direct and

indirect production costs by helping to improve the company's cost structure.

Principles of Management Accounting

1. Designing and Compiling

Statistical information; Documentation Other evidence of past or future results is designed to

meet the needs of each business and / or problem. It must be collected. This means that the

management accounting system needs to present relevant information. Then solve the

problem. Also, adjust the accounting information to meet management requirements (Money

Matters All Management Articles, 2019).

Designed to meet the needs of business and / or specific problems, along with other evidence

of current or future outcomes. Compliance means that the management accounting system is

9

review costs. This is important. This is because operating costs directly affect bottom-line

profits. Management Accountants can choose the best budgeting method by meeting the

needs of stakeholders. Help the company as much as you can. Stakeholders can create special

reports to make it easier for stakeholders to understand any cost to their department or

organization.

Maintain Profitability

Accountants need to make their business more profitable. It can be used to make a lot of

money, including analyzing breaches. With this type of analysis, accountants compare sales and

costs to determine which company is violating. With sales in mind, management can focus on

production factors as well as other factors that affect profitability. This will help determine the

sales target and overhead cost. In addition, you can manage accounts. Examine direct and

indirect production costs by helping to improve the company's cost structure. Accountants

need to make their business more profitable. It can be used to make a lot of money, including

analyzing breaches. With this type of analysis, accountants compare sales and costs to

determine which company is violating. With sales in mind, management can focus on

production factors as well as other factors that affect profitability. This will help determine the

sales target and overhead cost. In addition, you can manage accounts. Examine direct and

indirect production costs by helping to improve the company's cost structure.

Principles of Management Accounting

1. Designing and Compiling

Statistical information; Documentation Other evidence of past or future results is designed to

meet the needs of each business and / or problem. It must be collected. This means that the

management accounting system needs to present relevant information. Then solve the

problem. Also, adjust the accounting information to meet management requirements (Money

Matters All Management Articles, 2019).

Designed to meet the needs of business and / or specific problems, along with other evidence

of current or future outcomes. Compliance means that the management accounting system is

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

required to submit relevant information. Then you can solve the problem. In addition,

accounting data can be modified and audited to meet management requirements.

2. Management by Exception

Rules apply to exceptions when information is submitted to management. This means adhering

to budget control and cost standards. In this way, the actual performance is compared to a

predefined task to detect fraud. Only the worst scams can be properly reported to be

mismanaged. This way, the management will have more time to read the information (Money

Matters All Management Articles, 2019). Management rules are strictly adhered to when

managing information management. This means adhering to the cost standards of the budget

control system and the management accounting system. In this way, it compares to a

predefined one to find the actual performance deviations. Only serious misrepresentations are

misrepresented by management. This allows management to spend less time reading

information and more time to take action. Accept a predetermined amount of overhead costs.

Indirect costs are combined with indirect costs. Therefore, the method or method chosen to

absorb the overheads should automatically give the most effective results. The cost of

controlling a resource accountant is best determined by the resources that control the resource

accountant. Provides quantitative and qualitative information on the use and use of services,

such as vehicles. In this way, employees-controlled goods and services cannot be said to be

profitable unless the capital is kept in check for inflation. This means that the value of money is

not stable. Therefore, it is necessary to assess the value of capital from the actual financial

statements recalculated by the relevant business owners. In this way the inflation rate is taken

into account to determine the true success of the economic impact.

3. Control at Source Accounting

Cost control is best controlled by resource control where they occur. Details of individual skills

and product issues. Power repair and maintenance; The use and utilization of services such as

motor vehicles are constituted by quantitative and qualitative information. In this way,

employees and staff are encouraged. Control of equipment and services (Money Matters All

Management Articles, 2019).

4. Accounting for Inflation

10

accounting data can be modified and audited to meet management requirements.

2. Management by Exception

Rules apply to exceptions when information is submitted to management. This means adhering

to budget control and cost standards. In this way, the actual performance is compared to a

predefined task to detect fraud. Only the worst scams can be properly reported to be

mismanaged. This way, the management will have more time to read the information (Money

Matters All Management Articles, 2019). Management rules are strictly adhered to when

managing information management. This means adhering to the cost standards of the budget

control system and the management accounting system. In this way, it compares to a

predefined one to find the actual performance deviations. Only serious misrepresentations are

misrepresented by management. This allows management to spend less time reading

information and more time to take action. Accept a predetermined amount of overhead costs.

Indirect costs are combined with indirect costs. Therefore, the method or method chosen to

absorb the overheads should automatically give the most effective results. The cost of

controlling a resource accountant is best determined by the resources that control the resource

accountant. Provides quantitative and qualitative information on the use and use of services,

such as vehicles. In this way, employees-controlled goods and services cannot be said to be

profitable unless the capital is kept in check for inflation. This means that the value of money is

not stable. Therefore, it is necessary to assess the value of capital from the actual financial

statements recalculated by the relevant business owners. In this way the inflation rate is taken

into account to determine the true success of the economic impact.

3. Control at Source Accounting

Cost control is best controlled by resource control where they occur. Details of individual skills

and product issues. Power repair and maintenance; The use and utilization of services such as

motor vehicles are constituted by quantitative and qualitative information. In this way,

employees and staff are encouraged. Control of equipment and services (Money Matters All

Management Articles, 2019).

4. Accounting for Inflation

10

Capital cannot be bought without proper capital. This means that the value of money is volatile.

Therefore, it is necessary to assess the true value given by the business owners by recalculating.

In this way the inflation rate is taken into account to determine the true success of the

economic impact (Money Matters All Management Articles, 2019).

5. Use of Return on Investment

The return on investment is not called another investment. Profitability indicates the impact of

the business. The capital used for this purpose is calculated at the actual monetary value

(Money Matters All Management Articles, 2019).

6. Utility

Management accounting systems and templates should be used only if they have a useful

purpose (Money Matters All Management Articles, 2019).

7. Integration

This means integrating all the necessary information related to management so that they can

be used most effectively at the same time to provide accounting services at the least cost

(Money Matters All Management Articles, 2019).

8. Absorption of Overhead Costs

Anyone with a pre-determined fee will be charged an additional service charge. Indirect costs

are combined with indirect costs. Therefore, the method or method chosen to absorb

overheads should achieve the desired results in the same way (Money Matters All Management

Articles, 2019).

9. Utilization of Resources

Available resources should be used effectively. The reason is that some resources are only

available for a reason and some resources are scarce all year round. Therefore, the accounting

system should make sure that the appropriate use (Money Matters All Management Articles,

2019).

10. Controllable and Uncontrollable Costs

Based on cost control, cost control and two types of control are assigned. There is no sense in

taking steps to control costs that are out of control. Therefore, management accounting

11

Therefore, it is necessary to assess the true value given by the business owners by recalculating.

In this way the inflation rate is taken into account to determine the true success of the

economic impact (Money Matters All Management Articles, 2019).

5. Use of Return on Investment

The return on investment is not called another investment. Profitability indicates the impact of

the business. The capital used for this purpose is calculated at the actual monetary value

(Money Matters All Management Articles, 2019).

6. Utility

Management accounting systems and templates should be used only if they have a useful

purpose (Money Matters All Management Articles, 2019).

7. Integration

This means integrating all the necessary information related to management so that they can

be used most effectively at the same time to provide accounting services at the least cost

(Money Matters All Management Articles, 2019).

8. Absorption of Overhead Costs

Anyone with a pre-determined fee will be charged an additional service charge. Indirect costs

are combined with indirect costs. Therefore, the method or method chosen to absorb

overheads should achieve the desired results in the same way (Money Matters All Management

Articles, 2019).

9. Utilization of Resources

Available resources should be used effectively. The reason is that some resources are only

available for a reason and some resources are scarce all year round. Therefore, the accounting

system should make sure that the appropriate use (Money Matters All Management Articles,

2019).

10. Controllable and Uncontrollable Costs

Based on cost control, cost control and two types of control are assigned. There is no sense in

taking steps to control costs that are out of control. Therefore, management accounting

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 126

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.