Management Accounting Report: Role and Function, Financial Analysis

VerifiedAdded on 2022/10/13

|10

|3349

|18

Report

AI Summary

This report delves into the multifaceted world of management accounting, elucidating its core role and functions within organizations. Part 1 explores the essential requirements of different management accounting systems, including inventory management, cost accounting, job costing, and price optimization, and the benefits of these systems, and how they are applied. It also examines various reporting methods such as budget reports, cost reports, and performance reports. Part 2 analyzes key planning tools like benchmarking, activity-based costing, and break-even analysis. Furthermore, the report includes a financial analysis of JB Hi-Fi Group Pty Ltd based on their 2017 and 2018 financial statements. The report provides a comprehensive overview of management accounting principles and practices.

MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 1- REPORT ON ROLE AND FUNCTION OF MANAGEMENT ACCOUNTS

DEPARTMENT

Part 1

A. Management accounting and the essential requirement of different types of

management accounting systems

Management Accounting

Management accounting, also known as the “cost accounting” or the “managerial

accounting” denotes a process of evaluation of the business costs and operations of an entity.

The said analysis aid in the preparation of the internal financial accounts, records and reports

to aid the management of the enterprise in the policy formulation and implementation for the

achievement of the business objectives. Thus, the management accounting enables the

managers of the enterprise to gain a better understanding of the financial and costing data to

translate the same into useful information for management and varied range of stakeholders

within an organization.

Essential requirement of different types of management accounting systems

The essential requirement of different types of the management accounting systems is

provided in the following segment. Inventory management system is aimed at controlling and

overseeing the various aspects of the inventory of an enterprise. This involves the control

over the ordering, use, and storage of constituents of the raw material, consumables, goods

and supplies to be used in the production as well as the units of the finished goods (Drury,

2015). The inventory management is required in an enterprise for maintaining the adequate

inventory levels by the reduction in the overstock and understock situations and gain an

accurate understanding of present inventory levels. The cost accounting system is

necessitated to compute the actual cost of the products by taking into account the inputs costs

at various stages of the operations arising out of the production processes and the fixed costs

of the entity. The analytical tools such as the operating costing, standard costing and marginal

costing enable the better understanding of the cost function. The next accounting system is

that of the job costing by which the manufacturing costs comprised of direct materials, direct

labor, and direct overhead; is allocated to the respective item or batch of the products. Thus,

the significance lies in the ability to quote the price depending on the relevant costs involved.

The last type of accounting system is the Price optimization system. The process of price

DEPARTMENT

Part 1

A. Management accounting and the essential requirement of different types of

management accounting systems

Management Accounting

Management accounting, also known as the “cost accounting” or the “managerial

accounting” denotes a process of evaluation of the business costs and operations of an entity.

The said analysis aid in the preparation of the internal financial accounts, records and reports

to aid the management of the enterprise in the policy formulation and implementation for the

achievement of the business objectives. Thus, the management accounting enables the

managers of the enterprise to gain a better understanding of the financial and costing data to

translate the same into useful information for management and varied range of stakeholders

within an organization.

Essential requirement of different types of management accounting systems

The essential requirement of different types of the management accounting systems is

provided in the following segment. Inventory management system is aimed at controlling and

overseeing the various aspects of the inventory of an enterprise. This involves the control

over the ordering, use, and storage of constituents of the raw material, consumables, goods

and supplies to be used in the production as well as the units of the finished goods (Drury,

2015). The inventory management is required in an enterprise for maintaining the adequate

inventory levels by the reduction in the overstock and understock situations and gain an

accurate understanding of present inventory levels. The cost accounting system is

necessitated to compute the actual cost of the products by taking into account the inputs costs

at various stages of the operations arising out of the production processes and the fixed costs

of the entity. The analytical tools such as the operating costing, standard costing and marginal

costing enable the better understanding of the cost function. The next accounting system is

that of the job costing by which the manufacturing costs comprised of direct materials, direct

labor, and direct overhead; is allocated to the respective item or batch of the products. Thus,

the significance lies in the ability to quote the price depending on the relevant costs involved.

The last type of accounting system is the Price optimization system. The process of price

optimization is aimed at determining the consumers’ reaction to various prices for the goods

and services by the application of mathematical analysis. Thus, the said accounting system

aids the company in the maximization of the operating profit, quick selling of the products by

fixation of the best price possible (Edmonds and Olds, 2013).

B. Different methods used for types of management accounting reporting

An organisation’s performance can be monitored by the preparation of various accounting

reports on the periodical basis that give useful insights about the internal functioning and

operations of the enterprise. It must be noted that the significance of the information

presented lies in the relevance, reliability, accuracy and the timeliness of the data presented

therein. In addition, the said information must be presented correctly that is free from the

errors and must be understandable by the users of the reports. The information can be

presented in different forms as listed below.

Budget Reports: The preparation and presentation of the various budgets is one of the

most crucial exercise of the internal managerial function. The preparation of the

budgets is done with the aid of application of data of the budgets of prior years and

the same is further adjusted in accordance with the future forecast of the expected

business environment (Nishimura, 2013).

Cost Reports: The costs of items manufactured is calculated and presented in the said

reports. The cost is comprised of the price of raw material, costs, labor plus any

additional direct cost. The cost per unit is determined by dividing the total costs by the

units of goods produced and summarized into the cost report. Thus, the costs of

various goods and services is compared to each other as well as against the selling

prices.

Accounts Receivable Aging Reports: The said report is a crucial aid for the cost

managers for the evaluation of the cash flow position in the company. The report aids

in the identification of the problems with the collections process of the entity.

Accordingly, the credit policy of the company is amended to maintain the flow of the

cash in entity.

Performance reports: The actual revenues and expenditures of an enterprise are

compared to the budgeted figures for a respective period. The resulting differences are

and the reasons for the differences are recorded in the performance report. The

frequency of the performance report can be quarterly or monthly, depending on the

and services by the application of mathematical analysis. Thus, the said accounting system

aids the company in the maximization of the operating profit, quick selling of the products by

fixation of the best price possible (Edmonds and Olds, 2013).

B. Different methods used for types of management accounting reporting

An organisation’s performance can be monitored by the preparation of various accounting

reports on the periodical basis that give useful insights about the internal functioning and

operations of the enterprise. It must be noted that the significance of the information

presented lies in the relevance, reliability, accuracy and the timeliness of the data presented

therein. In addition, the said information must be presented correctly that is free from the

errors and must be understandable by the users of the reports. The information can be

presented in different forms as listed below.

Budget Reports: The preparation and presentation of the various budgets is one of the

most crucial exercise of the internal managerial function. The preparation of the

budgets is done with the aid of application of data of the budgets of prior years and

the same is further adjusted in accordance with the future forecast of the expected

business environment (Nishimura, 2013).

Cost Reports: The costs of items manufactured is calculated and presented in the said

reports. The cost is comprised of the price of raw material, costs, labor plus any

additional direct cost. The cost per unit is determined by dividing the total costs by the

units of goods produced and summarized into the cost report. Thus, the costs of

various goods and services is compared to each other as well as against the selling

prices.

Accounts Receivable Aging Reports: The said report is a crucial aid for the cost

managers for the evaluation of the cash flow position in the company. The report aids

in the identification of the problems with the collections process of the entity.

Accordingly, the credit policy of the company is amended to maintain the flow of the

cash in entity.

Performance reports: The actual revenues and expenditures of an enterprise are

compared to the budgeted figures for a respective period. The resulting differences are

and the reasons for the differences are recorded in the performance report. The

frequency of the performance report can be quarterly or monthly, depending on the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

discretion of the management. The performance report is further studied at the time of

the formulation of the new budgets (Horngreen, Sunden, Stratton, Burstalher, and

Schatzberg, 2013). Hence, it can be stated that the performances reports aid the cost

managers of an enterprise in planning for the increment in the costs and the upcoming

demands in production.

C. Benefits of the management accounting systems and their application within an

organizational context.

Benefits of the management accounting systems

The following segment is descriptive of the benefits of the management accounting systems

to an enterprise. The first key purpose is the formulation of the financial strategies with the

aid of the various managerial accounting tools such as the sales forecasts, job-costing

techniques, budgets, study of the overheads and others. The business strategies in relation to

the fixation of price of a product, purchasing of a capital equipment and reduction of the

operating costs are formulated with the aid of the techniques of management accounting

(Mohammad, 2016). The second key purpose served by the management accounting is the

monitoring of the expenses of the enterprise. The cost accountants of the company formulate

a number of budgets such as the static, flexible or rolling budgets together with various

periodical and ad hoc reports. The budgets and the reports aid the department heads of the

enterprise to keep an oversight over the respective departmental expenses and overhead,

thereby enabling the business run on run as cost efficient business. The improvement in the

cash flow position of an enterprise can be reached with the aid of the budget preparations and

undertaking the activities on the same lines. The senior leader formulates the master budget

which is further bifurcated into the smaller departmental budgets. The third significance of

the management accounting systems can be stated to be the maintenance of the profitability

by the use of the techniques such as the break even analysis and the variance analysis. Thus, a

systematic framework is provided by the management accounting systems for the better

management of the differences from expected costs.

Application of the management accounting systems within an organizational context

It is imperative to note that during the implementation of the management accounting

systems, there is no mandatory requirement of the compliance with the national accounting

standards. The management accounting systems can be tailored by the cost managers

the formulation of the new budgets (Horngreen, Sunden, Stratton, Burstalher, and

Schatzberg, 2013). Hence, it can be stated that the performances reports aid the cost

managers of an enterprise in planning for the increment in the costs and the upcoming

demands in production.

C. Benefits of the management accounting systems and their application within an

organizational context.

Benefits of the management accounting systems

The following segment is descriptive of the benefits of the management accounting systems

to an enterprise. The first key purpose is the formulation of the financial strategies with the

aid of the various managerial accounting tools such as the sales forecasts, job-costing

techniques, budgets, study of the overheads and others. The business strategies in relation to

the fixation of price of a product, purchasing of a capital equipment and reduction of the

operating costs are formulated with the aid of the techniques of management accounting

(Mohammad, 2016). The second key purpose served by the management accounting is the

monitoring of the expenses of the enterprise. The cost accountants of the company formulate

a number of budgets such as the static, flexible or rolling budgets together with various

periodical and ad hoc reports. The budgets and the reports aid the department heads of the

enterprise to keep an oversight over the respective departmental expenses and overhead,

thereby enabling the business run on run as cost efficient business. The improvement in the

cash flow position of an enterprise can be reached with the aid of the budget preparations and

undertaking the activities on the same lines. The senior leader formulates the master budget

which is further bifurcated into the smaller departmental budgets. The third significance of

the management accounting systems can be stated to be the maintenance of the profitability

by the use of the techniques such as the break even analysis and the variance analysis. Thus, a

systematic framework is provided by the management accounting systems for the better

management of the differences from expected costs.

Application of the management accounting systems within an organizational context

It is imperative to note that during the implementation of the management accounting

systems, there is no mandatory requirement of the compliance with the national accounting

standards. The management accounting systems can be tailored by the cost managers

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

according to the management’s need of the requisite information and the company’s business

operations. The effective implementation of the management accounting systems lead to

several advantages to the enterprises and are aimed at improving the operations and overall

profitability of the enterprise. A competitive advantage can be achieved by the efficient

development of the cost allocation processes in the management accounting function of an

organisation.

D. Integration of the management accounting systems and management accounting

reporting within organisational processes

The integration of the management accounting reports and the organisational processes is

explained as follows. The integration between the organisational activities and the budget

reports makes a pathway for the control over the activities and expenses of the entity and thus

aids the entity in the better achievement of the business objectives. The job cost reports when

integrated in the system of an entity leads to not only the overall reduction in the cost of the

products but also facilitates the entity in the pricing strategies for the future price fixations

(Levitan and Baxendale, 2012). The accounts receivable reports when integrated in the

systems of the entity would facilitate the management towards the timely collection of the

accounts receivable and thus would prevent the entity from the liquidity crunch as the cash

flow balance is maintained. The better management of the inventory levels can be attained by

the integration of the various processes such as the sales orders, picking, packaging, and

shipping of products with the inventory management system of the enterprise. The benefits of

the inventory accuracy and the consequent improvement in the company workflow are the

key achievements from the said integration.

Part 2

Analysis of the planning tools

Benchmarking

Benchmarking denotes the process of the measurement of the performance of a company in

context of the products, services, or any of the processes. The said measurement and

evaluation is done against the respective figures of those of another business which is

performing to the best of its level in the industry. The aim of the benchmarking exercise is the

efficient identification of the internal opportunities in an enterprise that would lead to the

improvement in various financial, costing and the management variables. The companies

with superior performances are studied, the processes, policies and the means of control are

operations. The effective implementation of the management accounting systems lead to

several advantages to the enterprises and are aimed at improving the operations and overall

profitability of the enterprise. A competitive advantage can be achieved by the efficient

development of the cost allocation processes in the management accounting function of an

organisation.

D. Integration of the management accounting systems and management accounting

reporting within organisational processes

The integration of the management accounting reports and the organisational processes is

explained as follows. The integration between the organisational activities and the budget

reports makes a pathway for the control over the activities and expenses of the entity and thus

aids the entity in the better achievement of the business objectives. The job cost reports when

integrated in the system of an entity leads to not only the overall reduction in the cost of the

products but also facilitates the entity in the pricing strategies for the future price fixations

(Levitan and Baxendale, 2012). The accounts receivable reports when integrated in the

systems of the entity would facilitate the management towards the timely collection of the

accounts receivable and thus would prevent the entity from the liquidity crunch as the cash

flow balance is maintained. The better management of the inventory levels can be attained by

the integration of the various processes such as the sales orders, picking, packaging, and

shipping of products with the inventory management system of the enterprise. The benefits of

the inventory accuracy and the consequent improvement in the company workflow are the

key achievements from the said integration.

Part 2

Analysis of the planning tools

Benchmarking

Benchmarking denotes the process of the measurement of the performance of a company in

context of the products, services, or any of the processes. The said measurement and

evaluation is done against the respective figures of those of another business which is

performing to the best of its level in the industry. The aim of the benchmarking exercise is the

efficient identification of the internal opportunities in an enterprise that would lead to the

improvement in various financial, costing and the management variables. The companies

with superior performances are studied, the processes, policies and the means of control are

identified that lead to such a superior performance in the industry. Further the gaps are filled

in the processes and policies of the own company by implementing the significant changes.

The policy changes may be on the lines of the amendments in the product’s features to make

it matching and competitive to a competitor’s goods, change the product mix, or changing the

scope of services offered, change in the technology and others. The company can further

install a customer relationship management (CRM) system to serve the customers better.

The Activity-based costing (ABC) refers to a methodology by which the overheads of the

production process are allocated more precisely and accurately to the items that actually use

the respective said overhead. The said managerial planning tool is used by the costing

managers for reduction of the overhead costs in a targeted manner. It is imperative to note

that the Activity-based costing technique produces the best results in the complex

environments, comprised of numerous machines and products. The complex environment is

further characterised by the interdependent processes that are tangled with each other. It must

also be noted that in a business environment where the production processes are abbreviated

and streamlined with each other, the said planning tool would not give much efficient results.

A break-even analysis is a financial planning tool which aids the entity in the determination

of the stage at which a new product or a service, will be profitable. In simple words it can be

stated that is a financial calculation done by the managers to compute the number of products

or services that must be sold by the company in order to cover the costs of the production

(particularly the associated fixed costs). The Break-even point refers to a situation where the

entity earns a zero profit and incurs zero amount of losses as well because all the associated

costs including the fixed costs such as the rent, salaries have been covered.

Break-even analysis is aids in the evaluation of the relation between the variable cost, fixed

cost and revenue. It is significant to note that usually a company that has lower amount of

fixed costs will have a low break-even point in terms of the sale and vice versa.

in the processes and policies of the own company by implementing the significant changes.

The policy changes may be on the lines of the amendments in the product’s features to make

it matching and competitive to a competitor’s goods, change the product mix, or changing the

scope of services offered, change in the technology and others. The company can further

install a customer relationship management (CRM) system to serve the customers better.

The Activity-based costing (ABC) refers to a methodology by which the overheads of the

production process are allocated more precisely and accurately to the items that actually use

the respective said overhead. The said managerial planning tool is used by the costing

managers for reduction of the overhead costs in a targeted manner. It is imperative to note

that the Activity-based costing technique produces the best results in the complex

environments, comprised of numerous machines and products. The complex environment is

further characterised by the interdependent processes that are tangled with each other. It must

also be noted that in a business environment where the production processes are abbreviated

and streamlined with each other, the said planning tool would not give much efficient results.

A break-even analysis is a financial planning tool which aids the entity in the determination

of the stage at which a new product or a service, will be profitable. In simple words it can be

stated that is a financial calculation done by the managers to compute the number of products

or services that must be sold by the company in order to cover the costs of the production

(particularly the associated fixed costs). The Break-even point refers to a situation where the

entity earns a zero profit and incurs zero amount of losses as well because all the associated

costs including the fixed costs such as the rent, salaries have been covered.

Break-even analysis is aids in the evaluation of the relation between the variable cost, fixed

cost and revenue. It is significant to note that usually a company that has lower amount of

fixed costs will have a low break-even point in terms of the sale and vice versa.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2-

Memo

To: The Finance Manager, JB Hi-Fi Group Pty Ltd.

From: Senior Financial Consultant, XYZ Company.

Date: 31 July 2019

Regarding: Financial Analysis of the entity based on the financial statements of year

2017 and 2018.

Dear Sir,

In order to understand the context of the financial analysis, it is firstly imperative to

understand the technique which has been used for the said analysis and the interpretation of

the results. In the wake of the numerous corporate collapses, complex global business

environment and the need of the transparent presentation of the financial results, the conduct

of the financial analysis is imperative to get the useful insights about the financial health of

an enterprise. The said financial analysis would aid the management of the entity to identify

the gaps and the crucial areas, the successful variables and thus would aid in the future policy

formulations (Higgins, 2012).

As per our discussion regarding the conduct of the financial analysis of the

organisation with respect to the various financial variables, the results and observations are

presented as follows. In order to understand the financial interpretations, it is imperative to

understand the technique used for the said evaluation. The computation of various ratios on

the lines of profitability ratios, liquidity ratios, solvency ratios, market prospect ratios and

others; aid in the evaluation of operational efficiency, cash flow position, ability to repay the

debts and overall financial status of the business of an entity (Fridson and Alvarez, 2011). It

must be noted that the ratio computation is the most popular technique as it further enables

the intra firm and inter firm comparison over the years. As a result, anyone can track the

progress of the activities of a company over a concerned period of time. The financial

analysis has led to the following observations.

Memo

To: The Finance Manager, JB Hi-Fi Group Pty Ltd.

From: Senior Financial Consultant, XYZ Company.

Date: 31 July 2019

Regarding: Financial Analysis of the entity based on the financial statements of year

2017 and 2018.

Dear Sir,

In order to understand the context of the financial analysis, it is firstly imperative to

understand the technique which has been used for the said analysis and the interpretation of

the results. In the wake of the numerous corporate collapses, complex global business

environment and the need of the transparent presentation of the financial results, the conduct

of the financial analysis is imperative to get the useful insights about the financial health of

an enterprise. The said financial analysis would aid the management of the entity to identify

the gaps and the crucial areas, the successful variables and thus would aid in the future policy

formulations (Higgins, 2012).

As per our discussion regarding the conduct of the financial analysis of the

organisation with respect to the various financial variables, the results and observations are

presented as follows. In order to understand the financial interpretations, it is imperative to

understand the technique used for the said evaluation. The computation of various ratios on

the lines of profitability ratios, liquidity ratios, solvency ratios, market prospect ratios and

others; aid in the evaluation of operational efficiency, cash flow position, ability to repay the

debts and overall financial status of the business of an entity (Fridson and Alvarez, 2011). It

must be noted that the ratio computation is the most popular technique as it further enables

the intra firm and inter firm comparison over the years. As a result, anyone can track the

progress of the activities of a company over a concerned period of time. The financial

analysis has led to the following observations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Working capital ratios

The working capital ratios or the liquidity ratios are the most popular set of ratios and

describe the efficiency of the liquidity position, and the operational efficiency of an entity.

The ideal current ratio of an entity is 2:1. It is significant to note that the higher the current

ratio, quick ratio and the cash ratio, the better it is (Saleem & Rehman, 2011). The ratios lead

to the understanding of a company’s capacity utilise the short term assets for the payment of

the short term loans of entity.

WORKING CAPITAL RATIOS 2017 2018

Current Ratio (Cash and Short Term Marketable Securities /

Current Liabilities)

1.32 1.32

Cash Ratio (Current Assets / Current Liabilities) 0.08 0.08

The table above depicts two key ratios of the entity JB Hi Fi. It is evident that there is not

much gap between the current assets and the current liabilities of the enterprise, as the current

ratio is quite on the lower side. The reason for such a low current ratio can be attributed to the

mounting trade payables as against the very low balance of cash and trade receivables. It is

recommended to the entity to arrange cash for the payment of the mounting current liabilities

as the liquidity position does not look very sound.

Profitability Ratios

The profitability ratios such as the net profit ratio, gross profit ration, return on income

describe the capability of the business activities to generate earnings (Velnampy & Niresh,

2012). Accordingly, the trends in the revenues, together with the insights about the operating

costs, and shareholders' equity can be gained with the aid of the said group of ratios.

The key profitability ratios of the entity JB Hi Fi are calculated and presented as follows.

PROFITABILITY RATIOS 2017 2018

Gross profit margin (Gross Profit/Sales) 21.87% 21.45%

Net profit margin (Net income/Sales) 3% 3%

The working capital ratios or the liquidity ratios are the most popular set of ratios and

describe the efficiency of the liquidity position, and the operational efficiency of an entity.

The ideal current ratio of an entity is 2:1. It is significant to note that the higher the current

ratio, quick ratio and the cash ratio, the better it is (Saleem & Rehman, 2011). The ratios lead

to the understanding of a company’s capacity utilise the short term assets for the payment of

the short term loans of entity.

WORKING CAPITAL RATIOS 2017 2018

Current Ratio (Cash and Short Term Marketable Securities /

Current Liabilities)

1.32 1.32

Cash Ratio (Current Assets / Current Liabilities) 0.08 0.08

The table above depicts two key ratios of the entity JB Hi Fi. It is evident that there is not

much gap between the current assets and the current liabilities of the enterprise, as the current

ratio is quite on the lower side. The reason for such a low current ratio can be attributed to the

mounting trade payables as against the very low balance of cash and trade receivables. It is

recommended to the entity to arrange cash for the payment of the mounting current liabilities

as the liquidity position does not look very sound.

Profitability Ratios

The profitability ratios such as the net profit ratio, gross profit ration, return on income

describe the capability of the business activities to generate earnings (Velnampy & Niresh,

2012). Accordingly, the trends in the revenues, together with the insights about the operating

costs, and shareholders' equity can be gained with the aid of the said group of ratios.

The key profitability ratios of the entity JB Hi Fi are calculated and presented as follows.

PROFITABILITY RATIOS 2017 2018

Gross profit margin (Gross Profit/Sales) 21.87% 21.45%

Net profit margin (Net income/Sales) 3% 3%

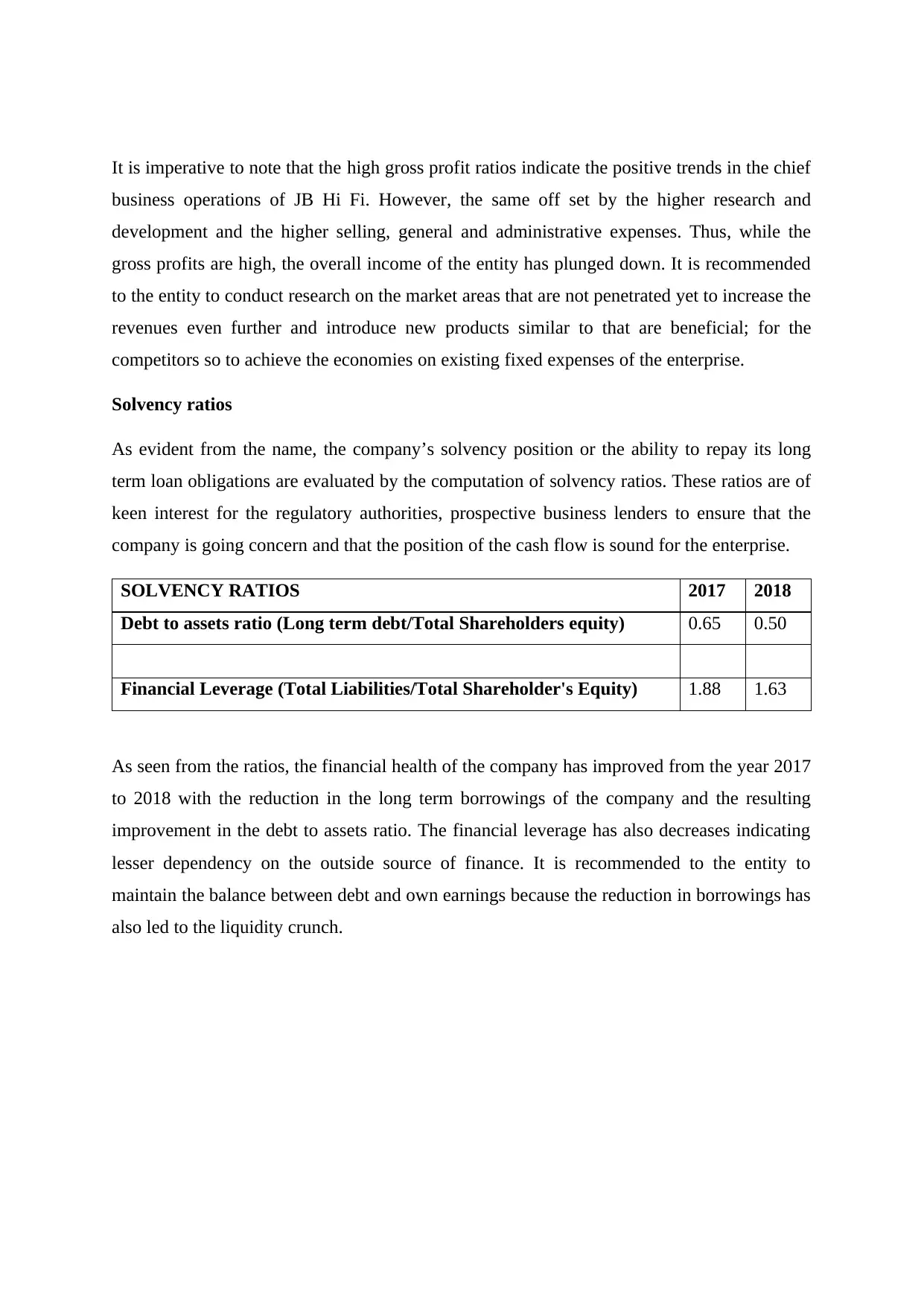

It is imperative to note that the high gross profit ratios indicate the positive trends in the chief

business operations of JB Hi Fi. However, the same off set by the higher research and

development and the higher selling, general and administrative expenses. Thus, while the

gross profits are high, the overall income of the entity has plunged down. It is recommended

to the entity to conduct research on the market areas that are not penetrated yet to increase the

revenues even further and introduce new products similar to that are beneficial; for the

competitors so to achieve the economies on existing fixed expenses of the enterprise.

Solvency ratios

As evident from the name, the company’s solvency position or the ability to repay its long

term loan obligations are evaluated by the computation of solvency ratios. These ratios are of

keen interest for the regulatory authorities, prospective business lenders to ensure that the

company is going concern and that the position of the cash flow is sound for the enterprise.

SOLVENCY RATIOS 2017 2018

Debt to assets ratio (Long term debt/Total Shareholders equity) 0.65 0.50

Financial Leverage (Total Liabilities/Total Shareholder's Equity) 1.88 1.63

As seen from the ratios, the financial health of the company has improved from the year 2017

to 2018 with the reduction in the long term borrowings of the company and the resulting

improvement in the debt to assets ratio. The financial leverage has also decreases indicating

lesser dependency on the outside source of finance. It is recommended to the entity to

maintain the balance between debt and own earnings because the reduction in borrowings has

also led to the liquidity crunch.

business operations of JB Hi Fi. However, the same off set by the higher research and

development and the higher selling, general and administrative expenses. Thus, while the

gross profits are high, the overall income of the entity has plunged down. It is recommended

to the entity to conduct research on the market areas that are not penetrated yet to increase the

revenues even further and introduce new products similar to that are beneficial; for the

competitors so to achieve the economies on existing fixed expenses of the enterprise.

Solvency ratios

As evident from the name, the company’s solvency position or the ability to repay its long

term loan obligations are evaluated by the computation of solvency ratios. These ratios are of

keen interest for the regulatory authorities, prospective business lenders to ensure that the

company is going concern and that the position of the cash flow is sound for the enterprise.

SOLVENCY RATIOS 2017 2018

Debt to assets ratio (Long term debt/Total Shareholders equity) 0.65 0.50

Financial Leverage (Total Liabilities/Total Shareholder's Equity) 1.88 1.63

As seen from the ratios, the financial health of the company has improved from the year 2017

to 2018 with the reduction in the long term borrowings of the company and the resulting

improvement in the debt to assets ratio. The financial leverage has also decreases indicating

lesser dependency on the outside source of finance. It is recommended to the entity to

maintain the balance between debt and own earnings because the reduction in borrowings has

also led to the liquidity crunch.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

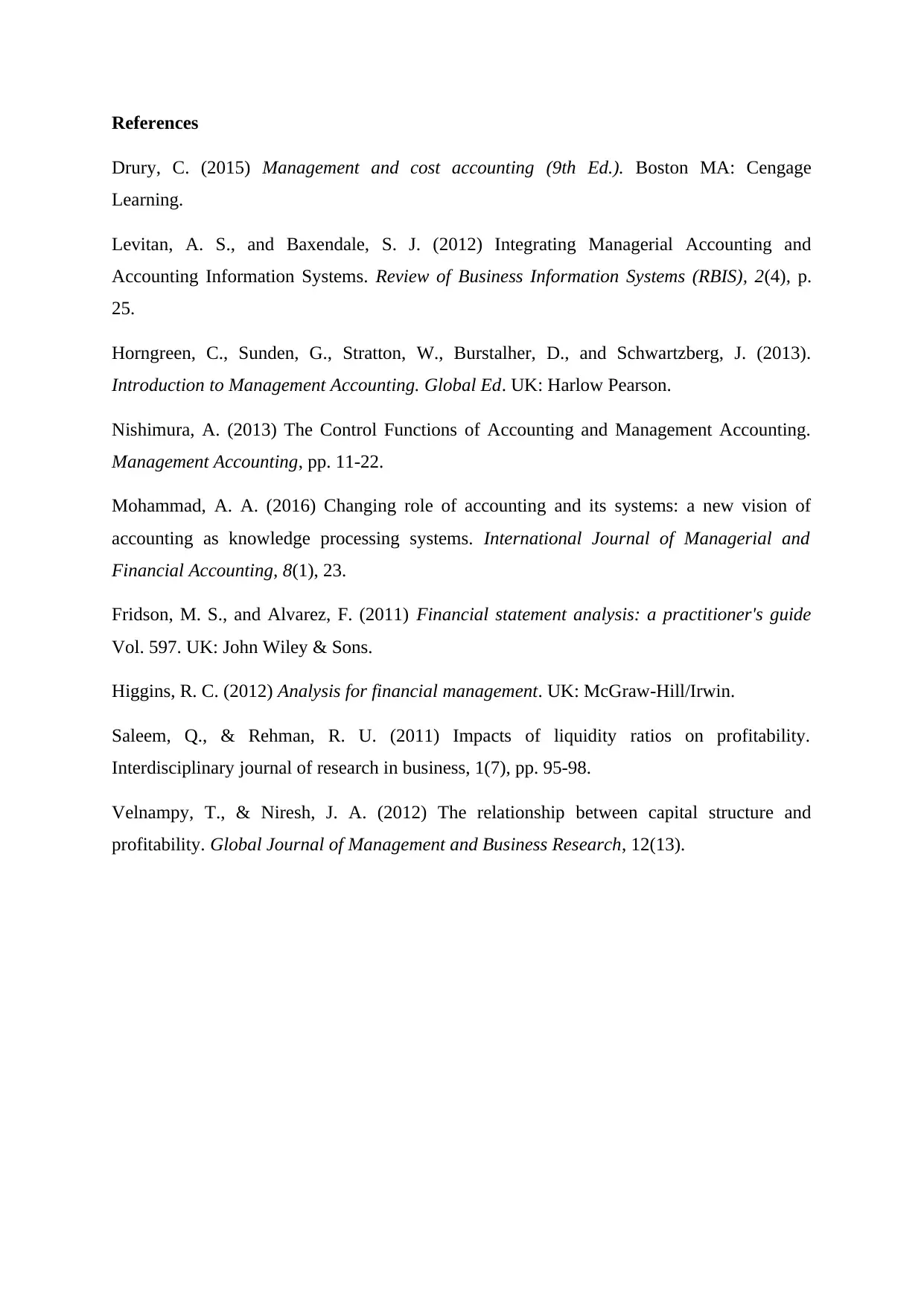

References

Drury, C. (2015) Management and cost accounting (9th Ed.). Boston MA: Cengage

Learning.

Levitan, A. S., and Baxendale, S. J. (2012) Integrating Managerial Accounting and

Accounting Information Systems. Review of Business Information Systems (RBIS), 2(4), p.

25.

Horngreen, C., Sunden, G., Stratton, W., Burstalher, D., and Schwartzberg, J. (2013).

Introduction to Management Accounting. Global Ed. UK: Harlow Pearson.

Nishimura, A. (2013) The Control Functions of Accounting and Management Accounting.

Management Accounting, pp. 11-22.

Mohammad, A. A. (2016) Changing role of accounting and its systems: a new vision of

accounting as knowledge processing systems. International Journal of Managerial and

Financial Accounting, 8(1), 23.

Fridson, M. S., and Alvarez, F. (2011) Financial statement analysis: a practitioner's guide

Vol. 597. UK: John Wiley & Sons.

Higgins, R. C. (2012) Analysis for financial management. UK: McGraw-Hill/Irwin.

Saleem, Q., & Rehman, R. U. (2011) Impacts of liquidity ratios on profitability.

Interdisciplinary journal of research in business, 1(7), pp. 95-98.

Velnampy, T., & Niresh, J. A. (2012) The relationship between capital structure and

profitability. Global Journal of Management and Business Research, 12(13).

Drury, C. (2015) Management and cost accounting (9th Ed.). Boston MA: Cengage

Learning.

Levitan, A. S., and Baxendale, S. J. (2012) Integrating Managerial Accounting and

Accounting Information Systems. Review of Business Information Systems (RBIS), 2(4), p.

25.

Horngreen, C., Sunden, G., Stratton, W., Burstalher, D., and Schwartzberg, J. (2013).

Introduction to Management Accounting. Global Ed. UK: Harlow Pearson.

Nishimura, A. (2013) The Control Functions of Accounting and Management Accounting.

Management Accounting, pp. 11-22.

Mohammad, A. A. (2016) Changing role of accounting and its systems: a new vision of

accounting as knowledge processing systems. International Journal of Managerial and

Financial Accounting, 8(1), 23.

Fridson, M. S., and Alvarez, F. (2011) Financial statement analysis: a practitioner's guide

Vol. 597. UK: John Wiley & Sons.

Higgins, R. C. (2012) Analysis for financial management. UK: McGraw-Hill/Irwin.

Saleem, Q., & Rehman, R. U. (2011) Impacts of liquidity ratios on profitability.

Interdisciplinary journal of research in business, 1(7), pp. 95-98.

Velnampy, T., & Niresh, J. A. (2012) The relationship between capital structure and

profitability. Global Journal of Management and Business Research, 12(13).

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.