Management Accounting Report: Costing Methods and Budgeting Strategies

VerifiedAdded on 2019/12/18

|17

|5249

|210

Report

AI Summary

This report delves into the core concepts of management accounting, exploring its significance for businesses like Imda Tech (UK) Limited. It differentiates between management and financial accounting, highlighting the role of management accounting in decision-making, product costing, and budgeting. The report analyzes various management accounting systems, including cost accounting and inventory management. Furthermore, it examines costing methods, comparing marginal and absorption costing through income statements, and discusses different types of budgets along with their respective advantages and disadvantages. The report also touches upon pricing strategies and the balance scorecard approach, providing a comprehensive overview of management accounting practices and their practical application in a business context.

MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

a)..................................................................................................................................................4

i) Define management accounting and different between management and financial accounting

.....................................................................................................................................................4

ii Importance of management accounting information................................................................6

b) Different types of management accounting systems...............................................................7

TASK 2............................................................................................................................................8

Costing methods..........................................................................................................................8

TASK 3..........................................................................................................................................10

(a)Different type of budgets and their advantages as well as disadvantages.............................10

© Pricing strategies....................................................................................................................13

TASK 4..........................................................................................................................................13

a) Balance score card approach.................................................................................................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

a)..................................................................................................................................................4

i) Define management accounting and different between management and financial accounting

.....................................................................................................................................................4

ii Importance of management accounting information................................................................6

b) Different types of management accounting systems...............................................................7

TASK 2............................................................................................................................................8

Costing methods..........................................................................................................................8

TASK 3..........................................................................................................................................10

(a)Different type of budgets and their advantages as well as disadvantages.............................10

© Pricing strategies....................................................................................................................13

TASK 4..........................................................................................................................................13

a) Balance score card approach.................................................................................................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

It is essential for each and every business enterprise to record their transactions in day to

day operations. Thus, for such purpose business requires to undertake management accounting

concept and provide financial information to other stakeholders. Business appoint accountants to

record financial transactions so that information could be recorded in a timely manner. However,

it also proves to be very efficient tool and thus results in directing and controlling the actions of

business (Otley and Emmanuel, 2013). It has been assessed that there has been great difference

lies in management and financial accounting. They both are different from each other.

Management accounting is considered as the decision making tool that provides different

information regarding purchase or sell, product costing and budgeting etc. While, financial

accounting is prepared in relation manage orecord financial information so that shareholders

could be given best information regarding investment (Fullerton, Kennedy and Widener, 2013).

Present study has been prepared in relation to Imda Tech (UK) Limited in relation to manage

their accounting information which results in achieving desired goals and objectives. Report

analyses the income statement which is developed on the basis of Marginal and Absorption

costing techniques. Also, it discusses the advantages and disadvantages of different types of

budget.

TASK 1

a)

i) Define management accounting and different between management and financial accounting

The concept of management accounting is considered as the process through which

crucial information could be identified, analyzed, measured and interpret the financial data so

that desired results could be attained. Hence, manager of Imda Tech Limited needs to make their

day to day transactions of business which results firm to carry out their functions in an effective

way. Main purpose of preparing such accounting system is helping firm to look forward and

execute internal affairs so that success can be attained (Bhimani and et. al., 2013). Management

accounting is crucial part of business and thus helps them to improve their corporate brand

image. There also lies tough competition and thus Imda needs to prepare good budget so that

It is essential for each and every business enterprise to record their transactions in day to

day operations. Thus, for such purpose business requires to undertake management accounting

concept and provide financial information to other stakeholders. Business appoint accountants to

record financial transactions so that information could be recorded in a timely manner. However,

it also proves to be very efficient tool and thus results in directing and controlling the actions of

business (Otley and Emmanuel, 2013). It has been assessed that there has been great difference

lies in management and financial accounting. They both are different from each other.

Management accounting is considered as the decision making tool that provides different

information regarding purchase or sell, product costing and budgeting etc. While, financial

accounting is prepared in relation manage orecord financial information so that shareholders

could be given best information regarding investment (Fullerton, Kennedy and Widener, 2013).

Present study has been prepared in relation to Imda Tech (UK) Limited in relation to manage

their accounting information which results in achieving desired goals and objectives. Report

analyses the income statement which is developed on the basis of Marginal and Absorption

costing techniques. Also, it discusses the advantages and disadvantages of different types of

budget.

TASK 1

a)

i) Define management accounting and different between management and financial accounting

The concept of management accounting is considered as the process through which

crucial information could be identified, analyzed, measured and interpret the financial data so

that desired results could be attained. Hence, manager of Imda Tech Limited needs to make their

day to day transactions of business which results firm to carry out their functions in an effective

way. Main purpose of preparing such accounting system is helping firm to look forward and

execute internal affairs so that success can be attained (Bhimani and et. al., 2013). Management

accounting is crucial part of business and thus helps them to improve their corporate brand

image. There also lies tough competition and thus Imda needs to prepare good budget so that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

financial decisions could be made accordingly. It results in preparing an effective income and

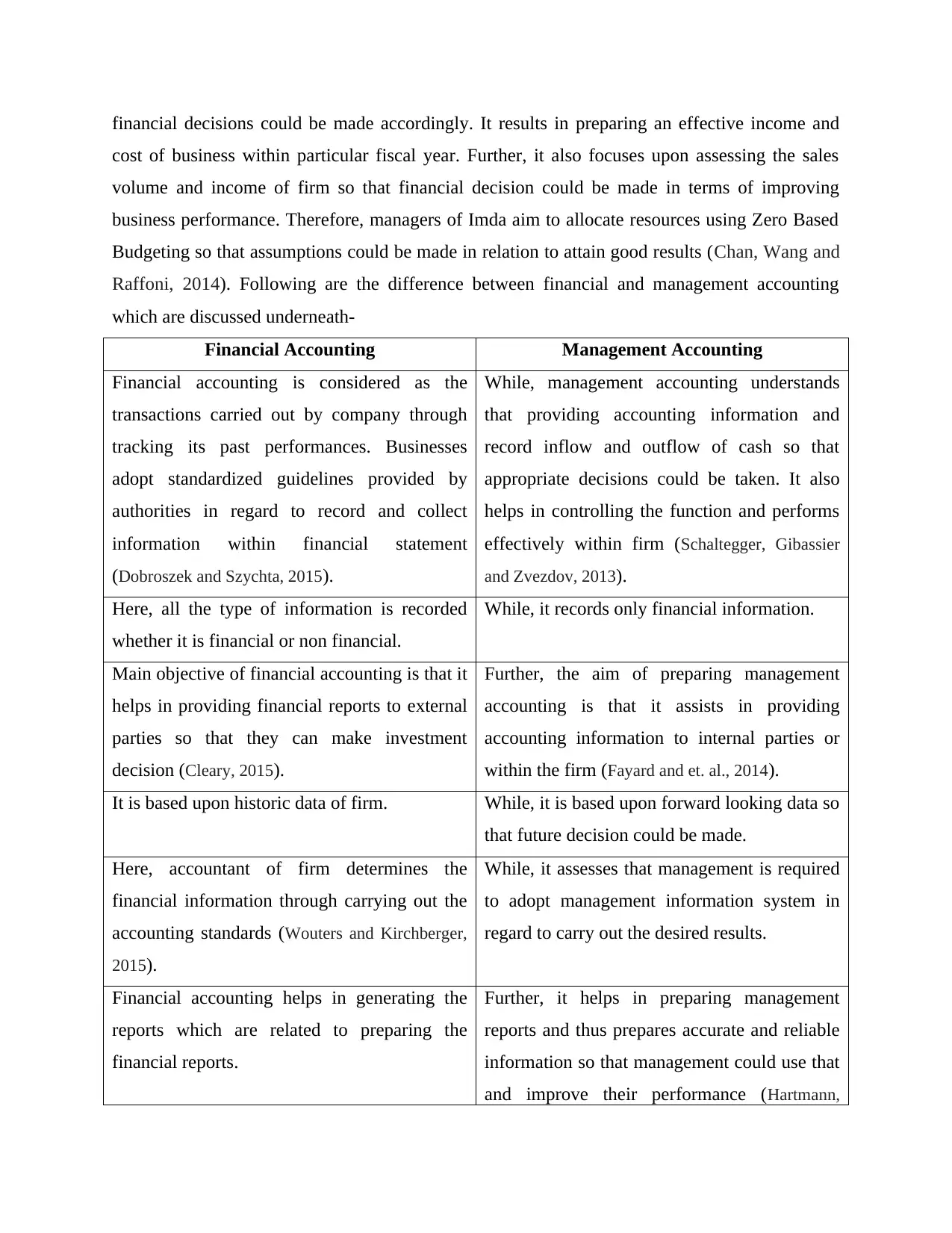

cost of business within particular fiscal year. Further, it also focuses upon assessing the sales

volume and income of firm so that financial decision could be made in terms of improving

business performance. Therefore, managers of Imda aim to allocate resources using Zero Based

Budgeting so that assumptions could be made in relation to attain good results (Chan, Wang and

Raffoni, 2014). Following are the difference between financial and management accounting

which are discussed underneath-

Financial Accounting Management Accounting

Financial accounting is considered as the

transactions carried out by company through

tracking its past performances. Businesses

adopt standardized guidelines provided by

authorities in regard to record and collect

information within financial statement

(Dobroszek and Szychta, 2015).

While, management accounting understands

that providing accounting information and

record inflow and outflow of cash so that

appropriate decisions could be taken. It also

helps in controlling the function and performs

effectively within firm (Schaltegger, Gibassier

and Zvezdov, 2013).

Here, all the type of information is recorded

whether it is financial or non financial.

While, it records only financial information.

Main objective of financial accounting is that it

helps in providing financial reports to external

parties so that they can make investment

decision (Cleary, 2015).

Further, the aim of preparing management

accounting is that it assists in providing

accounting information to internal parties or

within the firm (Fayard and et. al., 2014).

It is based upon historic data of firm. While, it is based upon forward looking data so

that future decision could be made.

Here, accountant of firm determines the

financial information through carrying out the

accounting standards (Wouters and Kirchberger,

2015).

While, it assesses that management is required

to adopt management information system in

regard to carry out the desired results.

Financial accounting helps in generating the

reports which are related to preparing the

financial reports.

Further, it helps in preparing management

reports and thus prepares accurate and reliable

information so that management could use that

and improve their performance (Hartmann,

cost of business within particular fiscal year. Further, it also focuses upon assessing the sales

volume and income of firm so that financial decision could be made in terms of improving

business performance. Therefore, managers of Imda aim to allocate resources using Zero Based

Budgeting so that assumptions could be made in relation to attain good results (Chan, Wang and

Raffoni, 2014). Following are the difference between financial and management accounting

which are discussed underneath-

Financial Accounting Management Accounting

Financial accounting is considered as the

transactions carried out by company through

tracking its past performances. Businesses

adopt standardized guidelines provided by

authorities in regard to record and collect

information within financial statement

(Dobroszek and Szychta, 2015).

While, management accounting understands

that providing accounting information and

record inflow and outflow of cash so that

appropriate decisions could be taken. It also

helps in controlling the function and performs

effectively within firm (Schaltegger, Gibassier

and Zvezdov, 2013).

Here, all the type of information is recorded

whether it is financial or non financial.

While, it records only financial information.

Main objective of financial accounting is that it

helps in providing financial reports to external

parties so that they can make investment

decision (Cleary, 2015).

Further, the aim of preparing management

accounting is that it assists in providing

accounting information to internal parties or

within the firm (Fayard and et. al., 2014).

It is based upon historic data of firm. While, it is based upon forward looking data so

that future decision could be made.

Here, accountant of firm determines the

financial information through carrying out the

accounting standards (Wouters and Kirchberger,

2015).

While, it assesses that management is required

to adopt management information system in

regard to carry out the desired results.

Financial accounting helps in generating the

reports which are related to preparing the

financial reports.

Further, it helps in preparing management

reports and thus prepares accurate and reliable

information so that management could use that

and improve their performance (Hartmann,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Perego and Young, 2013).

It helps in preparing financial or annual reports

at the end of accounting year for the use of

external stakeholders.

While, the management report generates

monthly and weekly records so that

improvement within department could be

carried out (Hiebl and et. al., 2013).

Here, the report shows the income statement or

balance sheet and profit and loss account

(Alsharari, Dixon and Youssef, 2015).

It indicates the sales revenue, availability of cash,

account payable and inventory etc.

ii Importance of management accounting information

The Imda tech limited makes use of management accounting information as tool for

decision making that offers several benefits which are enumerated in the manner as under:

Make or buy decision: The management accounting information that is being utilized by the

cited business wherein the manager of purchase department effectively develops decision

regarding making or buying of the goods (Taipaleenmäki, 2014). This is possible through

making comparison of the most suitable cost that describes the difference between the several

options of decisions. The manager can develop decision wherein it decides upon whether to

make purchase or develop parts related with production.

Product costing: It is regarded as the management accounting information that is utilized

towards measuring the cost of goods. It assists them in gaining knowledge in relation with the

cost of the product that is required for the small business. It acts as an aid for them in making

determination of the price at which the product can be sold so that break-even point can be

attained. This is being utilized by the manager of production of Imda tech limited towards setting

the price of the goods so that they are able to know its profitability before making allocation of

the resources within the production (Bebbington, Unerman and O'Dwyer, 2014).

Budgets: The management accounting is majorly being utilized by the small organization in

order to make preparation of the budgets. This acts as an aid for the purchase department in

making plan with respect to purchase and sales of the goods. Beside this it can also be utilized

towards motivating the staff workers as well as direct management (Otley and Emmanuel, 2013).

The manager of finance is able to gain knowledge regarding the sales expected over the period of

budgeting as well as sales figures towards showing the data related within costing in order to

measure the cash flows.

It helps in preparing financial or annual reports

at the end of accounting year for the use of

external stakeholders.

While, the management report generates

monthly and weekly records so that

improvement within department could be

carried out (Hiebl and et. al., 2013).

Here, the report shows the income statement or

balance sheet and profit and loss account

(Alsharari, Dixon and Youssef, 2015).

It indicates the sales revenue, availability of cash,

account payable and inventory etc.

ii Importance of management accounting information

The Imda tech limited makes use of management accounting information as tool for

decision making that offers several benefits which are enumerated in the manner as under:

Make or buy decision: The management accounting information that is being utilized by the

cited business wherein the manager of purchase department effectively develops decision

regarding making or buying of the goods (Taipaleenmäki, 2014). This is possible through

making comparison of the most suitable cost that describes the difference between the several

options of decisions. The manager can develop decision wherein it decides upon whether to

make purchase or develop parts related with production.

Product costing: It is regarded as the management accounting information that is utilized

towards measuring the cost of goods. It assists them in gaining knowledge in relation with the

cost of the product that is required for the small business. It acts as an aid for them in making

determination of the price at which the product can be sold so that break-even point can be

attained. This is being utilized by the manager of production of Imda tech limited towards setting

the price of the goods so that they are able to know its profitability before making allocation of

the resources within the production (Bebbington, Unerman and O'Dwyer, 2014).

Budgets: The management accounting is majorly being utilized by the small organization in

order to make preparation of the budgets. This acts as an aid for the purchase department in

making plan with respect to purchase and sales of the goods. Beside this it can also be utilized

towards motivating the staff workers as well as direct management (Otley and Emmanuel, 2013).

The manager of finance is able to gain knowledge regarding the sales expected over the period of

budgeting as well as sales figures towards showing the data related within costing in order to

measure the cash flows.

b) Different types of management accounting systems

Management accounting system is being used in regard to carry out effective information

so that crucial decision could be made. Hence, it is essential for Imda Tech Limited uses crucial

accounting information that helps business to carry out desired results. It is as follows-

Cost accounting system- Such framework is used by Imda in regard to make estimation

about cost of its products for the purpose of valuing inventory, profitability analysis and

controlling cost. It also helps cited firm manufacturing department to estimate the reliable

cost of products so that they are able to identify the products that are providing them

profits or not (Klemstine and Maher, 2014). Also, such method is being used for

preparing the financial statements so that Imda could estimate the closing inventory, WIP

and finished stock etc.

Inventory management system- Further, it is another tool that helps firm to identify the

management accounting system so that it could be used in order to make inventory for

the aim of maintaining the stock level. Also, such element helps in assessing the supply

chain management and thus involves different elements such as controlling and directing

the order stock so that Imda could deliver the goods to target market. Moreover,

management accountant helps in storing the daily transactions so that inventory could be

managed in an effective way (Gibassier, 2017). Further, it also facilitates firm to take

new orders from customers and thus enable them to maintain track of inventory, orders

etc. Imda also uses different software in regard to maintain their inventory and also

manage their stock in regard to minimize the wastage of resources.

Job costing system- It is another system of management accounting information so that it

results in carrying out job costing and thus carry out effective procedure so that best

information could be obtained in relation to cost and carry out effective manufacturing of

products by Imda. Also, it is being used in regard to track cost of raw material so that it

is being used in regard to carry out the job. Here, three types of information is being used

such as direct material, labour and overhead expenses etc. All these could be used for the

aim of tracking of cost and revenue so that they are being able to produce standardized

Management accounting system is being used in regard to carry out effective information

so that crucial decision could be made. Hence, it is essential for Imda Tech Limited uses crucial

accounting information that helps business to carry out desired results. It is as follows-

Cost accounting system- Such framework is used by Imda in regard to make estimation

about cost of its products for the purpose of valuing inventory, profitability analysis and

controlling cost. It also helps cited firm manufacturing department to estimate the reliable

cost of products so that they are able to identify the products that are providing them

profits or not (Klemstine and Maher, 2014). Also, such method is being used for

preparing the financial statements so that Imda could estimate the closing inventory, WIP

and finished stock etc.

Inventory management system- Further, it is another tool that helps firm to identify the

management accounting system so that it could be used in order to make inventory for

the aim of maintaining the stock level. Also, such element helps in assessing the supply

chain management and thus involves different elements such as controlling and directing

the order stock so that Imda could deliver the goods to target market. Moreover,

management accountant helps in storing the daily transactions so that inventory could be

managed in an effective way (Gibassier, 2017). Further, it also facilitates firm to take

new orders from customers and thus enable them to maintain track of inventory, orders

etc. Imda also uses different software in regard to maintain their inventory and also

manage their stock in regard to minimize the wastage of resources.

Job costing system- It is another system of management accounting information so that it

results in carrying out job costing and thus carry out effective procedure so that best

information could be obtained in relation to cost and carry out effective manufacturing of

products by Imda. Also, it is being used in regard to track cost of raw material so that it

is being used in regard to carry out the job. Here, three types of information is being used

such as direct material, labour and overhead expenses etc. All these could be used for the

aim of tracking of cost and revenue so that they are being able to produce standardized

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

reports of profitability in regard to carry out job (Klychova, Faskhutdinova and Sadrieva,

2014).

TASK 2

Costing methods

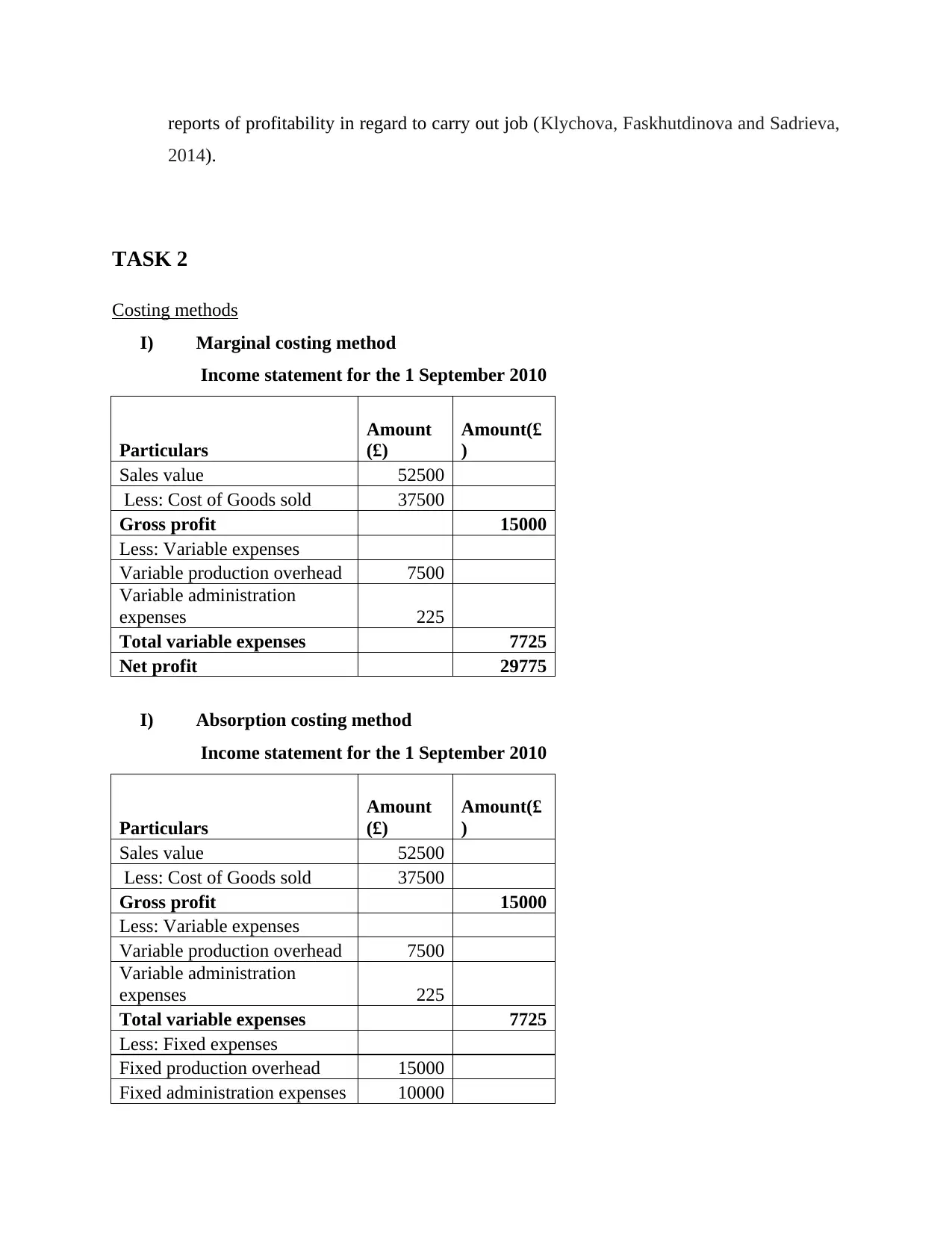

I) Marginal costing method

Income statement for the 1 September 2010

Particulars

Amount

(£)

Amount(£

)

Sales value 52500

Less: Cost of Goods sold 37500

Gross profit 15000

Less: Variable expenses

Variable production overhead 7500

Variable administration

expenses 225

Total variable expenses 7725

Net profit 29775

I) Absorption costing method

Income statement for the 1 September 2010

Particulars

Amount

(£)

Amount(£

)

Sales value 52500

Less: Cost of Goods sold 37500

Gross profit 15000

Less: Variable expenses

Variable production overhead 7500

Variable administration

expenses 225

Total variable expenses 7725

Less: Fixed expenses

Fixed production overhead 15000

Fixed administration expenses 10000

2014).

TASK 2

Costing methods

I) Marginal costing method

Income statement for the 1 September 2010

Particulars

Amount

(£)

Amount(£

)

Sales value 52500

Less: Cost of Goods sold 37500

Gross profit 15000

Less: Variable expenses

Variable production overhead 7500

Variable administration

expenses 225

Total variable expenses 7725

Net profit 29775

I) Absorption costing method

Income statement for the 1 September 2010

Particulars

Amount

(£)

Amount(£

)

Sales value 52500

Less: Cost of Goods sold 37500

Gross profit 15000

Less: Variable expenses

Variable production overhead 7500

Variable administration

expenses 225

Total variable expenses 7725

Less: Fixed expenses

Fixed production overhead 15000

Fixed administration expenses 10000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total fixed expenses 5000

Net profit 24775

Interpretation

Interpretation: Imda tech is one of the well known business firm and for same financial

statement is prepared by using marginal and absorption costing system. Marginal and absorption

costing are the two main methods that are used for costing and profitability of the product. It is

mainly used to compute cost of production. Under both methods first of all cost is measured and

then and then profit on each product line is measured. For the mentioned firm by using marginal

and absorption costing method profit and cost is computed in the tables that are given above.

Marginal costing is the method under which only variable expenses are taken in to account in

order to compute cost of production. Fixed costs are not taken in to consideration to compute

fixed cost (Yalcin, 2012). Absorption costing is the method of costing under which both fixed

and variable expenses are taken in to account in order to compute cost of production. It can be

said that both costing methods are different from each other and there is significant importance

of all these methods for the business firms. This is the one of the main reason due to which

different amount of net profit is computed in case of marginal and absorption costing method. It

can be observed from the first table that income statement is prepared by using marginal costing

method and profit computed by using mentioned method is equivalent to £29775. In comparison

to this in case of absorption costing method net profit £24775. It can be said that higher amount

of profit is revealed by the marginal costing method then absorption costing method. This

happened because in case of marginal costing method only variable expenses are taken in to

account. This means that in the calculation process fixed expenses are not taken in to account

and due to this reason higher amount of profit is revealed by the marginal then absorption costing

method. It can be seen from the table that in case of marginal costing method the expenses that

are taken in to account are production and administration expenses. Both these expenses are

added and subtracted from the sales revenue amount and in this way net profit is computed

(Tucke and Parker, 2014). Whereas, in case of absorption costing method both expenses are

taken in to account. It can be observed from the table given above that fixed expenses are taken

in to account namely fixed production, fixed overhead and fixed expenses. It can be said that

both method of costing are effective and in case of both of them costing is done in proper

manner.

Net profit 24775

Interpretation

Interpretation: Imda tech is one of the well known business firm and for same financial

statement is prepared by using marginal and absorption costing system. Marginal and absorption

costing are the two main methods that are used for costing and profitability of the product. It is

mainly used to compute cost of production. Under both methods first of all cost is measured and

then and then profit on each product line is measured. For the mentioned firm by using marginal

and absorption costing method profit and cost is computed in the tables that are given above.

Marginal costing is the method under which only variable expenses are taken in to account in

order to compute cost of production. Fixed costs are not taken in to consideration to compute

fixed cost (Yalcin, 2012). Absorption costing is the method of costing under which both fixed

and variable expenses are taken in to account in order to compute cost of production. It can be

said that both costing methods are different from each other and there is significant importance

of all these methods for the business firms. This is the one of the main reason due to which

different amount of net profit is computed in case of marginal and absorption costing method. It

can be observed from the first table that income statement is prepared by using marginal costing

method and profit computed by using mentioned method is equivalent to £29775. In comparison

to this in case of absorption costing method net profit £24775. It can be said that higher amount

of profit is revealed by the marginal costing method then absorption costing method. This

happened because in case of marginal costing method only variable expenses are taken in to

account. This means that in the calculation process fixed expenses are not taken in to account

and due to this reason higher amount of profit is revealed by the marginal then absorption costing

method. It can be seen from the table that in case of marginal costing method the expenses that

are taken in to account are production and administration expenses. Both these expenses are

added and subtracted from the sales revenue amount and in this way net profit is computed

(Tucke and Parker, 2014). Whereas, in case of absorption costing method both expenses are

taken in to account. It can be observed from the table given above that fixed expenses are taken

in to account namely fixed production, fixed overhead and fixed expenses. It can be said that

both method of costing are effective and in case of both of them costing is done in proper

manner.

TASK 3

(a)Different type of budgets and their advantages as well as disadvantages

Budget refers to the projected statement under which projection is made about the income

and expenses. There are different sort of budget that are prepared by the business firm. Some of

the budgets are explained below.

Incremental budget

Incremental budgeting refers to the budget under which values of the components of the

budget is increased consistently. In the budget there are two sections cash inflow and cash

outflow. In the cash inflow different sources from which funds can be received in the business is

determined. Some of the sources from which cash receipt takes place in the business are sales

revenue and receivables. Apart from this in the cash outflow section various items are included

like sales and administrative expenses etc. From the cash inflow cash outflow amount is

deducted to compute net balance amount. In the incremental budget for each month value of the

components of the budget is increased or decreased by certain percentage (Hülle, Kaspar. and

Möller, 2011). There are number of factors that are considered to determine the growth rate of

different components of the budget. It is very important to select appropriate growth rate for all

elements of the budget because by doing so accurate prediction can be made in the business. On

the basis of accurate prediction good business decisions can be made by the managers. If

estimate of growth rate will be wrong then in that case wrong decisions will be taken by the

managers. Advantages and disadvantages of the incremental budget are given below.

Advantages of incremental budget

One of the main advantages of the incremental budget is that by using same with passage

of time according to expected change that can take place in the business environment

decisions are made by the managers in respect to use of resources in the business. It can

be said that best use and allocation of resources can be made by preparing incremental

budget (Ambe, 2016).

Other main advantage of incremental budget is that by using same flexible decisions can

be made by the managers. Every time with passage of time same decisions are not made

by the managers.

Disadvantage of the incremental budget

(a)Different type of budgets and their advantages as well as disadvantages

Budget refers to the projected statement under which projection is made about the income

and expenses. There are different sort of budget that are prepared by the business firm. Some of

the budgets are explained below.

Incremental budget

Incremental budgeting refers to the budget under which values of the components of the

budget is increased consistently. In the budget there are two sections cash inflow and cash

outflow. In the cash inflow different sources from which funds can be received in the business is

determined. Some of the sources from which cash receipt takes place in the business are sales

revenue and receivables. Apart from this in the cash outflow section various items are included

like sales and administrative expenses etc. From the cash inflow cash outflow amount is

deducted to compute net balance amount. In the incremental budget for each month value of the

components of the budget is increased or decreased by certain percentage (Hülle, Kaspar. and

Möller, 2011). There are number of factors that are considered to determine the growth rate of

different components of the budget. It is very important to select appropriate growth rate for all

elements of the budget because by doing so accurate prediction can be made in the business. On

the basis of accurate prediction good business decisions can be made by the managers. If

estimate of growth rate will be wrong then in that case wrong decisions will be taken by the

managers. Advantages and disadvantages of the incremental budget are given below.

Advantages of incremental budget

One of the main advantages of the incremental budget is that by using same with passage

of time according to expected change that can take place in the business environment

decisions are made by the managers in respect to use of resources in the business. It can

be said that best use and allocation of resources can be made by preparing incremental

budget (Ambe, 2016).

Other main advantage of incremental budget is that by using same flexible decisions can

be made by the managers. Every time with passage of time same decisions are not made

by the managers.

Disadvantage of the incremental budget

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The main disadvantage of incremental budget is that in preparation of same one need to

estimate growth rate. It is very difficult task to estimate growth rate of the budget

elements. Businesses managers are department level are not very experienced and they

cannot estimate likely changes in the business environment accurately. Hence, due to

estimation of wrong growth rate wrong prediction can be made in the budget and

improper use of resources can be made in the business.

Fixed budget

Fixed budget refers to the budget under which values of all components of the budget is

fixed and same is not changed even business conditions get changed (Klychova, Faskhutdinova

and Sadrieva, 2014). This means that if business condition becomes worse than in that case at

same rate resources will be used in the business. Fixed budget is prepared by number of business

firms. Advantages and disadvantages of fixed budget are explained below.

Advantages of fixed budget

The main advantage of fixed budget is that it is not time consuming and one can easily

use same by making slight modifications each year in the value of the component of the

budget. Thus, it can be said that no high level of expertise is need to prepare fixed budget.

Department managers do not need to spend lots of time on budget preparation and they

can use that time for performing other activities that are related to their department.

Disadvantages of fixed budget

The main disadvantage of the fixed budget is that according to change in business

conditions values are not changed and due to this reason with change in the situation use

of resource does not get changed in the business.

Zero based budgeting

Zero based budgeting is another method that is used for budgeting. Under this method

past year figures are not taken in to account to prepare budget for the current time period. It can

be said that there is significant importance of the zero based budgeting for the business firms

(Taipaleenmäki, 2014). This is because it is not necessary that past scenario will again repeat in

the future. Advantages and disadvantages of the zero based budgeting are given below.

Advantages of zero based budget

estimate growth rate. It is very difficult task to estimate growth rate of the budget

elements. Businesses managers are department level are not very experienced and they

cannot estimate likely changes in the business environment accurately. Hence, due to

estimation of wrong growth rate wrong prediction can be made in the budget and

improper use of resources can be made in the business.

Fixed budget

Fixed budget refers to the budget under which values of all components of the budget is

fixed and same is not changed even business conditions get changed (Klychova, Faskhutdinova

and Sadrieva, 2014). This means that if business condition becomes worse than in that case at

same rate resources will be used in the business. Fixed budget is prepared by number of business

firms. Advantages and disadvantages of fixed budget are explained below.

Advantages of fixed budget

The main advantage of fixed budget is that it is not time consuming and one can easily

use same by making slight modifications each year in the value of the component of the

budget. Thus, it can be said that no high level of expertise is need to prepare fixed budget.

Department managers do not need to spend lots of time on budget preparation and they

can use that time for performing other activities that are related to their department.

Disadvantages of fixed budget

The main disadvantage of the fixed budget is that according to change in business

conditions values are not changed and due to this reason with change in the situation use

of resource does not get changed in the business.

Zero based budgeting

Zero based budgeting is another method that is used for budgeting. Under this method

past year figures are not taken in to account to prepare budget for the current time period. It can

be said that there is significant importance of the zero based budgeting for the business firms

(Taipaleenmäki, 2014). This is because it is not necessary that past scenario will again repeat in

the future. Advantages and disadvantages of the zero based budgeting are given below.

Advantages of zero based budget

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Budget is prepared in the systematic way by using zero based budgets because past years

figures are not considered. Thus, from starting point values of all components of budget

is determined.

Disadvantages of zero based budget

One of the main disadvantages of zero based budgets is that lengthy process needs to be

followed to prepare zero based budgets. Thus, it is very time consuming to prepare zero

based budgets.

(b) Process of preparing budget Update budget assumptions: In preparing budget first step is to update the budget

assumptions. Format of budget is always followed same but assumptions are changed

with change in the situation (Bebbington, Unerman and O'Dwyer, 2014). According to

change in assumption values of different components of the budget are changed by the

managers. According to budget entire planning is done in respect to use of resources. Review bottlenecks: In this stage bottlenecks that were prepared in earlier budget are

reviewed and accordingly for the new budget bottlenecks are determined which further

are used to measure firm performance. Available funding: Amount of fund that are available in the business are also considered

while preparing budget. According to available fund allocation is made among different

business activities. In this way best use of fund is made in the business. Obtain revenue forecast: In this stage budget forecast is obtained from the finance

manager (What are steps in preparing budget, 2017). In this phase finance manager

makes estimation about the rate at which revenue may grow in the business in the

upcoming time period. Thus, it is important stage of budget preparation Obtain department budget: On the basis of overall forecast of cash flows department

budget is prepared by the managers which include all income and expenditures of the

specific department. Update the budget model: In this stage budget model that is prepared earlier is updated

and in this department budgets are taken in to consideration to update the budget model Review the budget: After preparation of final budget same is reviewed and it is ensured

that all projections are made accurately. By doing so it is ensured that accurate decisions

will be taken by the managers.

figures are not considered. Thus, from starting point values of all components of budget

is determined.

Disadvantages of zero based budget

One of the main disadvantages of zero based budgets is that lengthy process needs to be

followed to prepare zero based budgets. Thus, it is very time consuming to prepare zero

based budgets.

(b) Process of preparing budget Update budget assumptions: In preparing budget first step is to update the budget

assumptions. Format of budget is always followed same but assumptions are changed

with change in the situation (Bebbington, Unerman and O'Dwyer, 2014). According to

change in assumption values of different components of the budget are changed by the

managers. According to budget entire planning is done in respect to use of resources. Review bottlenecks: In this stage bottlenecks that were prepared in earlier budget are

reviewed and accordingly for the new budget bottlenecks are determined which further

are used to measure firm performance. Available funding: Amount of fund that are available in the business are also considered

while preparing budget. According to available fund allocation is made among different

business activities. In this way best use of fund is made in the business. Obtain revenue forecast: In this stage budget forecast is obtained from the finance

manager (What are steps in preparing budget, 2017). In this phase finance manager

makes estimation about the rate at which revenue may grow in the business in the

upcoming time period. Thus, it is important stage of budget preparation Obtain department budget: On the basis of overall forecast of cash flows department

budget is prepared by the managers which include all income and expenditures of the

specific department. Update the budget model: In this stage budget model that is prepared earlier is updated

and in this department budgets are taken in to consideration to update the budget model Review the budget: After preparation of final budget same is reviewed and it is ensured

that all projections are made accurately. By doing so it is ensured that accurate decisions

will be taken by the managers.

© Pricing strategies

There are different sort of pricing strategies that are prepared by the business firms. Some

of these pricing strategies are explained below. Market skimming strategy: Market skimming strategy is one under which at high price

product is sold in the market. It must be noted that this pricing strategy is followed in the

monopoly market. Due to less competitors firm easily sale product at high price and earn

high profit in business. Price penetration strategy: Price penetration strategy is one under which at low price

product is sold in the market. It is the one of the most important strategy because under

same in order to survive in the market firm sold its product at low price in the market. Competition based pricing: Competition based pricing is one under which by

considering price that is charged by the competitor’s price of the product is determined

and at that price product is sold in the market.

TASK 4

a) Balance score card approach

Earlier the business make use of traditional methods in order to make evaluation of the past

years performance but today there is presence of several tools that assist in measuring

performance of the firm. Balance scorecard approach is considered as approach that is being

utilized by the firm for measurement of the whole performance. It makes evaluation of working

based upon the four criteria that includes financial, internal process, customers as well as

learning or growth. It makes evaluation of the business efforts for making future enhancement in

the firm (Fullerton, Kennedy and Widener, 2013). This not only lays emphasis over the financial

performance of Balance scorecard approach but also takes into account non financial perspective

as well.

Financial perspective: Balance score card approach pays greater attention over the cash

flow, sales, growth, income as well as equity. In case cash flow increases then such

implies that business has attained the profitability and has made sound performance

within the financial year (Bhimani and et. al., 2013).

There are different sort of pricing strategies that are prepared by the business firms. Some

of these pricing strategies are explained below. Market skimming strategy: Market skimming strategy is one under which at high price

product is sold in the market. It must be noted that this pricing strategy is followed in the

monopoly market. Due to less competitors firm easily sale product at high price and earn

high profit in business. Price penetration strategy: Price penetration strategy is one under which at low price

product is sold in the market. It is the one of the most important strategy because under

same in order to survive in the market firm sold its product at low price in the market. Competition based pricing: Competition based pricing is one under which by

considering price that is charged by the competitor’s price of the product is determined

and at that price product is sold in the market.

TASK 4

a) Balance score card approach

Earlier the business make use of traditional methods in order to make evaluation of the past

years performance but today there is presence of several tools that assist in measuring

performance of the firm. Balance scorecard approach is considered as approach that is being

utilized by the firm for measurement of the whole performance. It makes evaluation of working

based upon the four criteria that includes financial, internal process, customers as well as

learning or growth. It makes evaluation of the business efforts for making future enhancement in

the firm (Fullerton, Kennedy and Widener, 2013). This not only lays emphasis over the financial

performance of Balance scorecard approach but also takes into account non financial perspective

as well.

Financial perspective: Balance score card approach pays greater attention over the cash

flow, sales, growth, income as well as equity. In case cash flow increases then such

implies that business has attained the profitability and has made sound performance

within the financial year (Bhimani and et. al., 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.