Management Accounting Report: Jeffrey & Sons Ltd Analysis

VerifiedAdded on 2020/01/21

|20

|4735

|64

Report

AI Summary

This Management Accounting report provides a comprehensive analysis of various cost concepts and their practical application within Jeffrey & Son’s Ltd. The report begins with a detailed description of cost classification, including direct and indirect costs, costs based on nature, and functional and behavioral costs. It then demonstrates the computation of job costs using job costing and exquisite costs through absorption costing. The report further includes the preparation and analysis of a cost report for September, highlighting variance analysis and the use of performance indicators to identify areas for improvement. The report also covers budgetary procedures, including the preparation of purchase, production, and cash budgets. Finally, the report concludes with a variance analysis and an operational reconciliation statement, offering recommendations for cost reduction and quality enhancement.

Management

Accounting

1

Accounting

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Table of Contents.............................................................................................................................2

Index of Tables................................................................................................................................3

Introduction......................................................................................................................................4

Task 1...............................................................................................................................................4

1.1 Description of cost classification...........................................................................................4

1.2 Computation of job cost by considering method of job costing............................................5

1.3 Computation of exquisite cost by using absorption costing technique..................................6

1.4 Analysis of cost data of exquisite..........................................................................................9

Task 2.............................................................................................................................................10

2.1 Preparation and analysis of cost report of September month..............................................10

2.2 Use of performance indicators in order to identify potential areas of improvement...........11

2.3 Recommendations for cost reduction and enhancement is quality and value.....................12

Task 3.............................................................................................................................................13

3.1 Nature and purpose of budgetary procedure........................................................................13

3.2 Selection of suitable method for the preparation of budgetary statements..........................13

3.3 Purchase and production budget..........................................................................................13

3.4 Cash budget..........................................................................................................................14

Task 4.............................................................................................................................................17

4.1 Variance analysis.................................................................................................................17

4.2 Operational reconciliation statement...................................................................................18

4.3 Report of variance analysis..................................................................................................19

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

2

Table of Contents.............................................................................................................................2

Index of Tables................................................................................................................................3

Introduction......................................................................................................................................4

Task 1...............................................................................................................................................4

1.1 Description of cost classification...........................................................................................4

1.2 Computation of job cost by considering method of job costing............................................5

1.3 Computation of exquisite cost by using absorption costing technique..................................6

1.4 Analysis of cost data of exquisite..........................................................................................9

Task 2.............................................................................................................................................10

2.1 Preparation and analysis of cost report of September month..............................................10

2.2 Use of performance indicators in order to identify potential areas of improvement...........11

2.3 Recommendations for cost reduction and enhancement is quality and value.....................12

Task 3.............................................................................................................................................13

3.1 Nature and purpose of budgetary procedure........................................................................13

3.2 Selection of suitable method for the preparation of budgetary statements..........................13

3.3 Purchase and production budget..........................................................................................13

3.4 Cash budget..........................................................................................................................14

Task 4.............................................................................................................................................17

4.1 Variance analysis.................................................................................................................17

4.2 Operational reconciliation statement...................................................................................18

4.3 Report of variance analysis..................................................................................................19

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

2

INDEX OF TABLES

Table 1: Statement showing total and unit cost of Job 444.............................................................4

Table 2: Allocation Criteria of cost ...............................................................................................5

Table 3: Allocation of cost of support departments on the basis of machine hours........................7

Table 4: Statement showing computation of exquisite....................................................................7

Table 5: Statement showing computation of exquisite....................................................................8

Table 6: Cost report of September...................................................................................................9

Table 7: Production budget (in units)...........................................................................................12

Table 8: Material purchase budget in amount................................................................................12

Table 9: Cash budget.....................................................................................................................12

3

Table 1: Statement showing total and unit cost of Job 444.............................................................4

Table 2: Allocation Criteria of cost ...............................................................................................5

Table 3: Allocation of cost of support departments on the basis of machine hours........................7

Table 4: Statement showing computation of exquisite....................................................................7

Table 5: Statement showing computation of exquisite....................................................................8

Table 6: Cost report of September...................................................................................................9

Table 7: Production budget (in units)...........................................................................................12

Table 8: Material purchase budget in amount................................................................................12

Table 9: Cash budget.....................................................................................................................12

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is a procedure used for the analysis and interpretation of

information collected through cost and financial accounting. Objective of this subject is to assist

managerial person in making viable decisions in order to attain aims and objectives of business

in an effective manner (Dekker, 2015). Present project report is focused on evaluation of various

cost concepts by considering information of Jeffrey & Son’s Ltd. In this report, theoretical

description and practical application will be provided regarding cost computation, budget and

variance analysis.

TASK 1

1.1 Description of cost classification

Cost is an amount paid or payable by business in order to obtain product or service.

Classification of cost can be done of the basis of following factors:

Basis Description Example

Element This classification is based on cost

objective. On this basis, cost is classified

into direct and indirect cost. Direct cost

is incurred for the production activities

which are necessary for business

(Fullerton, Kennedy and Widener,

2014). Further, indirect is incurred to

attain economic benefit in order to

enhance efficiency and profitability of

business.

Example of direct cost is purchase of raw

material and indirect cost is amount

incurred on selling and distribution

expenses.

Nature By considering nature of expenses, cost

is classified into material, labour and

overhead.

Material cost includes amount incurred

on variables required for production such

as raw material (Suomala, Lyly-

Yrjänäinen and Lukka, 2014). Labour

cost includes wages and overhead

4

Management accounting is a procedure used for the analysis and interpretation of

information collected through cost and financial accounting. Objective of this subject is to assist

managerial person in making viable decisions in order to attain aims and objectives of business

in an effective manner (Dekker, 2015). Present project report is focused on evaluation of various

cost concepts by considering information of Jeffrey & Son’s Ltd. In this report, theoretical

description and practical application will be provided regarding cost computation, budget and

variance analysis.

TASK 1

1.1 Description of cost classification

Cost is an amount paid or payable by business in order to obtain product or service.

Classification of cost can be done of the basis of following factors:

Basis Description Example

Element This classification is based on cost

objective. On this basis, cost is classified

into direct and indirect cost. Direct cost

is incurred for the production activities

which are necessary for business

(Fullerton, Kennedy and Widener,

2014). Further, indirect is incurred to

attain economic benefit in order to

enhance efficiency and profitability of

business.

Example of direct cost is purchase of raw

material and indirect cost is amount

incurred on selling and distribution

expenses.

Nature By considering nature of expenses, cost

is classified into material, labour and

overhead.

Material cost includes amount incurred

on variables required for production such

as raw material (Suomala, Lyly-

Yrjänäinen and Lukka, 2014). Labour

cost includes wages and overhead

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

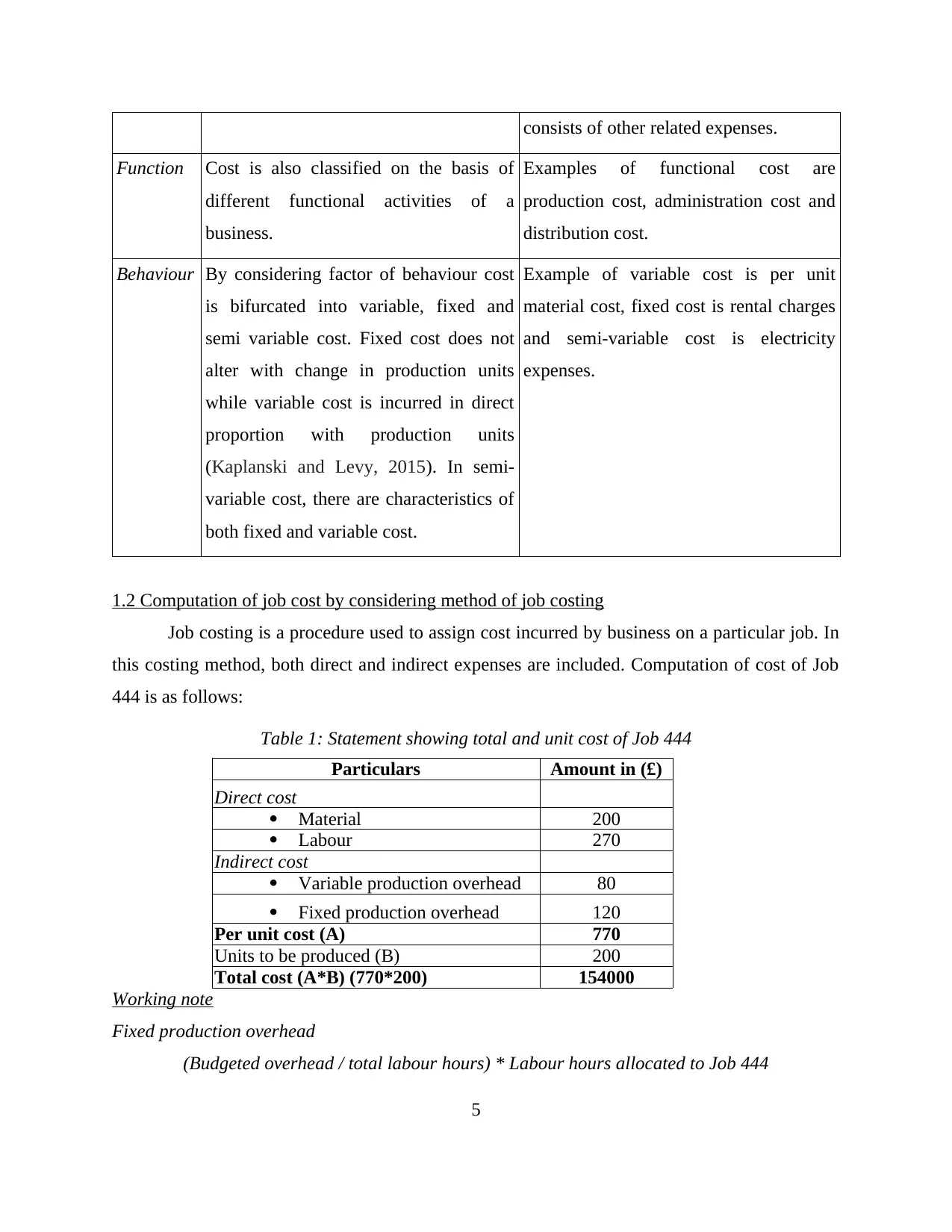

consists of other related expenses.

Function Cost is also classified on the basis of

different functional activities of a

business.

Examples of functional cost are

production cost, administration cost and

distribution cost.

Behaviour By considering factor of behaviour cost

is bifurcated into variable, fixed and

semi variable cost. Fixed cost does not

alter with change in production units

while variable cost is incurred in direct

proportion with production units

(Kaplanski and Levy, 2015). In semi-

variable cost, there are characteristics of

both fixed and variable cost.

Example of variable cost is per unit

material cost, fixed cost is rental charges

and semi-variable cost is electricity

expenses.

1.2 Computation of job cost by considering method of job costing

Job costing is a procedure used to assign cost incurred by business on a particular job. In

this costing method, both direct and indirect expenses are included. Computation of cost of Job

444 is as follows:

Table 1: Statement showing total and unit cost of Job 444

Particulars Amount in (£)

Direct cost

Material 200

Labour 270

Indirect cost

Variable production overhead 80

Fixed production overhead 120

Per unit cost (A) 770

Units to be produced (B) 200

Total cost (A*B) (770*200) 154000

Working note

Fixed production overhead

(Budgeted overhead / total labour hours) * Labour hours allocated to Job 444

5

Function Cost is also classified on the basis of

different functional activities of a

business.

Examples of functional cost are

production cost, administration cost and

distribution cost.

Behaviour By considering factor of behaviour cost

is bifurcated into variable, fixed and

semi variable cost. Fixed cost does not

alter with change in production units

while variable cost is incurred in direct

proportion with production units

(Kaplanski and Levy, 2015). In semi-

variable cost, there are characteristics of

both fixed and variable cost.

Example of variable cost is per unit

material cost, fixed cost is rental charges

and semi-variable cost is electricity

expenses.

1.2 Computation of job cost by considering method of job costing

Job costing is a procedure used to assign cost incurred by business on a particular job. In

this costing method, both direct and indirect expenses are included. Computation of cost of Job

444 is as follows:

Table 1: Statement showing total and unit cost of Job 444

Particulars Amount in (£)

Direct cost

Material 200

Labour 270

Indirect cost

Variable production overhead 80

Fixed production overhead 120

Per unit cost (A) 770

Units to be produced (B) 200

Total cost (A*B) (770*200) 154000

Working note

Fixed production overhead

(Budgeted overhead / total labour hours) * Labour hours allocated to Job 444

5

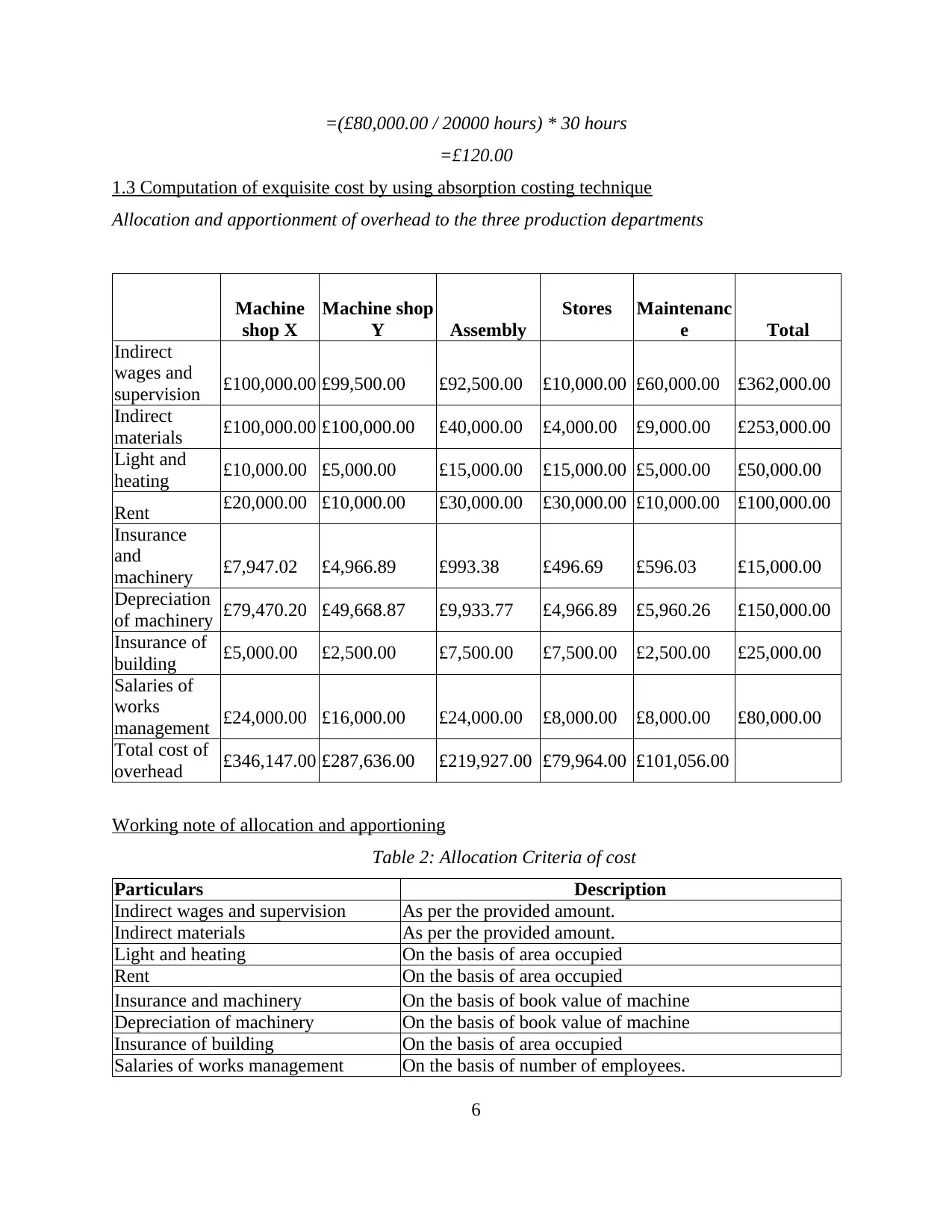

=(£80,000.00 / 20000 hours) * 30 hours

=£120.00

1.3 Computation of exquisite cost by using absorption costing technique

Allocation and apportionment of overhead to the three production departments

Machine

shop X

Machine shop

Y Assembly

Stores Maintenanc

e Total

Indirect

wages and

supervision £100,000.00 £99,500.00 £92,500.00 £10,000.00 £60,000.00 £362,000.00

Indirect

materials £100,000.00 £100,000.00 £40,000.00 £4,000.00 £9,000.00 £253,000.00

Light and

heating £10,000.00 £5,000.00 £15,000.00 £15,000.00 £5,000.00 £50,000.00

Rent £20,000.00 £10,000.00 £30,000.00 £30,000.00 £10,000.00 £100,000.00

Insurance

and

machinery £7,947.02 £4,966.89 £993.38 £496.69 £596.03 £15,000.00

Depreciation

of machinery £79,470.20 £49,668.87 £9,933.77 £4,966.89 £5,960.26 £150,000.00

Insurance of

building £5,000.00 £2,500.00 £7,500.00 £7,500.00 £2,500.00 £25,000.00

Salaries of

works

management £24,000.00 £16,000.00 £24,000.00 £8,000.00 £8,000.00 £80,000.00

Total cost of

overhead £346,147.00 £287,636.00 £219,927.00 £79,964.00 £101,056.00

Working note of allocation and apportioning

Table 2: Allocation Criteria of cost

Particulars Description

Indirect wages and supervision As per the provided amount.

Indirect materials As per the provided amount.

Light and heating On the basis of area occupied

Rent On the basis of area occupied

Insurance and machinery On the basis of book value of machine

Depreciation of machinery On the basis of book value of machine

Insurance of building On the basis of area occupied

Salaries of works management On the basis of number of employees.

6

=£120.00

1.3 Computation of exquisite cost by using absorption costing technique

Allocation and apportionment of overhead to the three production departments

Machine

shop X

Machine shop

Y Assembly

Stores Maintenanc

e Total

Indirect

wages and

supervision £100,000.00 £99,500.00 £92,500.00 £10,000.00 £60,000.00 £362,000.00

Indirect

materials £100,000.00 £100,000.00 £40,000.00 £4,000.00 £9,000.00 £253,000.00

Light and

heating £10,000.00 £5,000.00 £15,000.00 £15,000.00 £5,000.00 £50,000.00

Rent £20,000.00 £10,000.00 £30,000.00 £30,000.00 £10,000.00 £100,000.00

Insurance

and

machinery £7,947.02 £4,966.89 £993.38 £496.69 £596.03 £15,000.00

Depreciation

of machinery £79,470.20 £49,668.87 £9,933.77 £4,966.89 £5,960.26 £150,000.00

Insurance of

building £5,000.00 £2,500.00 £7,500.00 £7,500.00 £2,500.00 £25,000.00

Salaries of

works

management £24,000.00 £16,000.00 £24,000.00 £8,000.00 £8,000.00 £80,000.00

Total cost of

overhead £346,147.00 £287,636.00 £219,927.00 £79,964.00 £101,056.00

Working note of allocation and apportioning

Table 2: Allocation Criteria of cost

Particulars Description

Indirect wages and supervision As per the provided amount.

Indirect materials As per the provided amount.

Light and heating On the basis of area occupied

Rent On the basis of area occupied

Insurance and machinery On the basis of book value of machine

Depreciation of machinery On the basis of book value of machine

Insurance of building On the basis of area occupied

Salaries of works management On the basis of number of employees.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

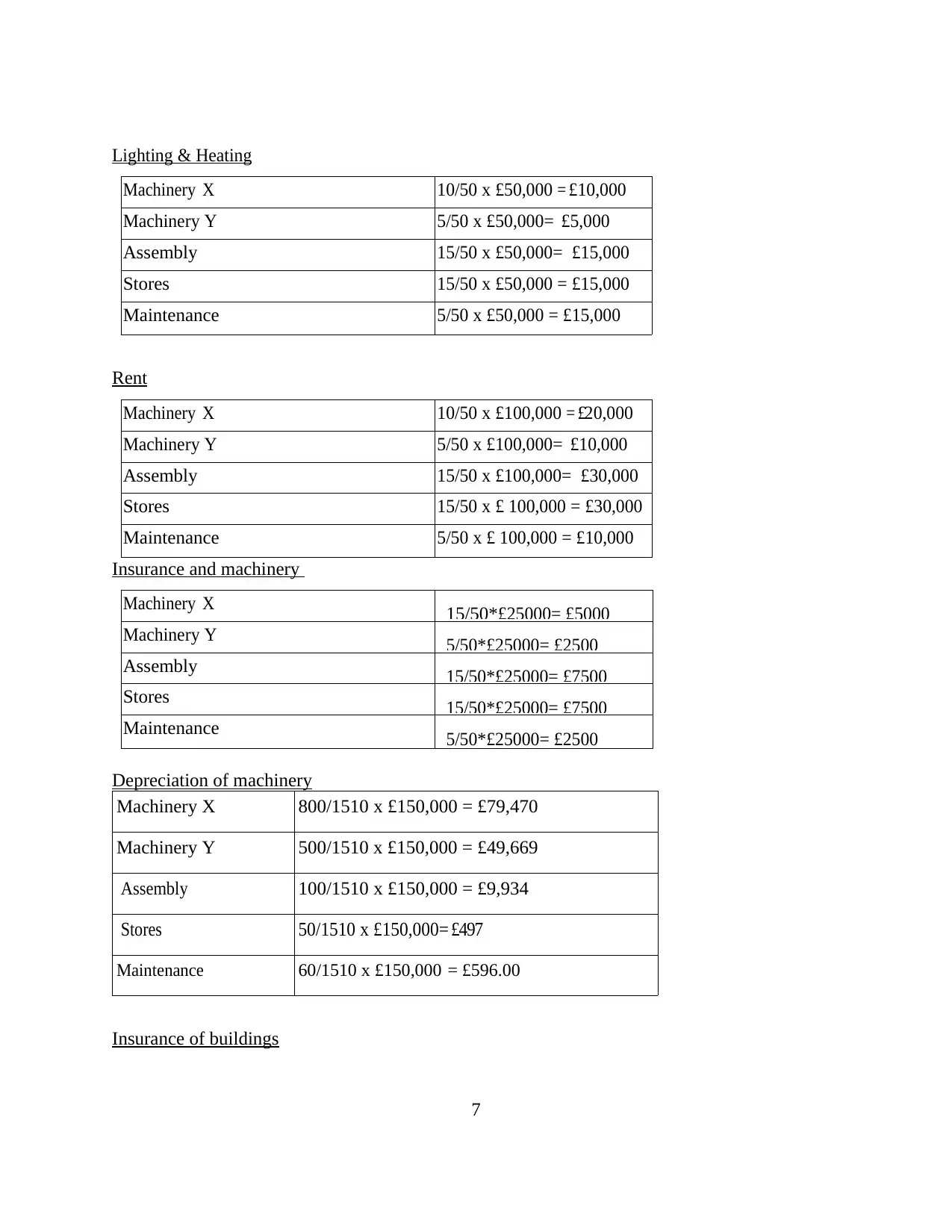

Lighting & Heating

Machinery X 10/50 x £50,000 = £10,000

Machinery Y 5/50 x £50,000= £5,000

Assembly 15/50 x £50,000= £15,000

Stores 15/50 x £50,000 = £15,000

Maintenance 5/50 x £50,000 = £15,000

Rent

Machinery X 10/50 x £100,000 = £20,000

Machinery Y 5/50 x £100,000= £10,000

Assembly 15/50 x £100,000= £30,000

Stores 15/50 x £ 100,000 = £30,000

Maintenance 5/50 x £ 100,000 = £10,000

Insurance and machinery

Machinery X 15/50*£25000= £5000

Machinery Y 5/50*£25000= £2500

Assembly 15/50*£25000= £7500

Stores 15/50*£25000= £7500

Maintenance 5/50*£25000= £2500

Depreciation of machinery

Machinery X 800/1510 x £150,000 = £79,470

Machinery Y 500/1510 x £150,000 = £49,669

Assembly 100/1510 x £150,000 = £9,934

Stores 50/1510 x £150,000= £497

Maintenance 60/1510 x £150,000 = £596.00

Insurance of buildings

7

Machinery X 10/50 x £50,000 = £10,000

Machinery Y 5/50 x £50,000= £5,000

Assembly 15/50 x £50,000= £15,000

Stores 15/50 x £50,000 = £15,000

Maintenance 5/50 x £50,000 = £15,000

Rent

Machinery X 10/50 x £100,000 = £20,000

Machinery Y 5/50 x £100,000= £10,000

Assembly 15/50 x £100,000= £30,000

Stores 15/50 x £ 100,000 = £30,000

Maintenance 5/50 x £ 100,000 = £10,000

Insurance and machinery

Machinery X 15/50*£25000= £5000

Machinery Y 5/50*£25000= £2500

Assembly 15/50*£25000= £7500

Stores 15/50*£25000= £7500

Maintenance 5/50*£25000= £2500

Depreciation of machinery

Machinery X 800/1510 x £150,000 = £79,470

Machinery Y 500/1510 x £150,000 = £49,669

Assembly 100/1510 x £150,000 = £9,934

Stores 50/1510 x £150,000= £497

Maintenance 60/1510 x £150,000 = £596.00

Insurance of buildings

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

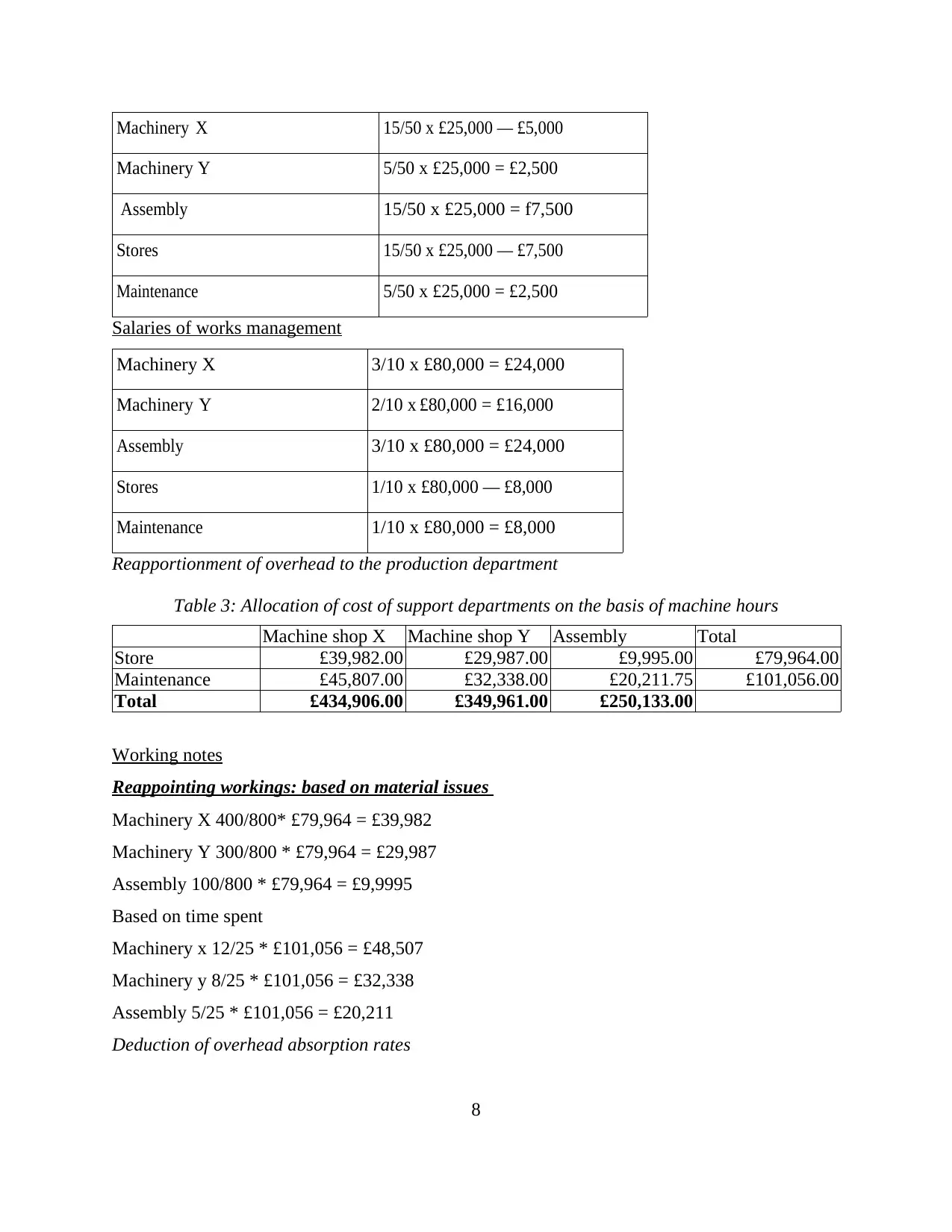

Machinery X 15/50 x £25,000 — £5,000

Machinery Y 5/50 x £25,000 = £2,500

Assembly 15/50 x £25,000 = f7,500

Stores 15/50 x £25,000 — £7,500

Maintenance 5/50 x £25,000 = £2,500

Salaries of works management

Machinery X 3/10 x £80,000 = £24,000

Machinery Y 2/10 x £80,000 = £16,000

Assembly 3/10 x £80,000 = £24,000

Stores 1/10 x £80,000 — £8,000

Maintenance 1/10 x £80,000 = £8,000

Reapportionment of overhead to the production department

Table 3: Allocation of cost of support departments on the basis of machine hours

Machine shop X Machine shop Y Assembly Total

Store £39,982.00 £29,987.00 £9,995.00 £79,964.00

Maintenance £45,807.00 £32,338.00 £20,211.75 £101,056.00

Total £434,906.00 £349,961.00 £250,133.00

Working notes

Reappointing workings: based on material issues

Machinery X 400/800* £79,964 = £39,982

Machinery Y 300/800 * £79,964 = £29,987

Assembly 100/800 * £79,964 = £9,9995

Based on time spent

Machinery x 12/25 * £101,056 = £48,507

Machinery y 8/25 * £101,056 = £32,338

Assembly 5/25 * £101,056 = £20,211

Deduction of overhead absorption rates

8

Machinery Y 5/50 x £25,000 = £2,500

Assembly 15/50 x £25,000 = f7,500

Stores 15/50 x £25,000 — £7,500

Maintenance 5/50 x £25,000 = £2,500

Salaries of works management

Machinery X 3/10 x £80,000 = £24,000

Machinery Y 2/10 x £80,000 = £16,000

Assembly 3/10 x £80,000 = £24,000

Stores 1/10 x £80,000 — £8,000

Maintenance 1/10 x £80,000 = £8,000

Reapportionment of overhead to the production department

Table 3: Allocation of cost of support departments on the basis of machine hours

Machine shop X Machine shop Y Assembly Total

Store £39,982.00 £29,987.00 £9,995.00 £79,964.00

Maintenance £45,807.00 £32,338.00 £20,211.75 £101,056.00

Total £434,906.00 £349,961.00 £250,133.00

Working notes

Reappointing workings: based on material issues

Machinery X 400/800* £79,964 = £39,982

Machinery Y 300/800 * £79,964 = £29,987

Assembly 100/800 * £79,964 = £9,9995

Based on time spent

Machinery x 12/25 * £101,056 = £48,507

Machinery y 8/25 * £101,056 = £32,338

Assembly 5/25 * £101,056 = £20,211

Deduction of overhead absorption rates

8

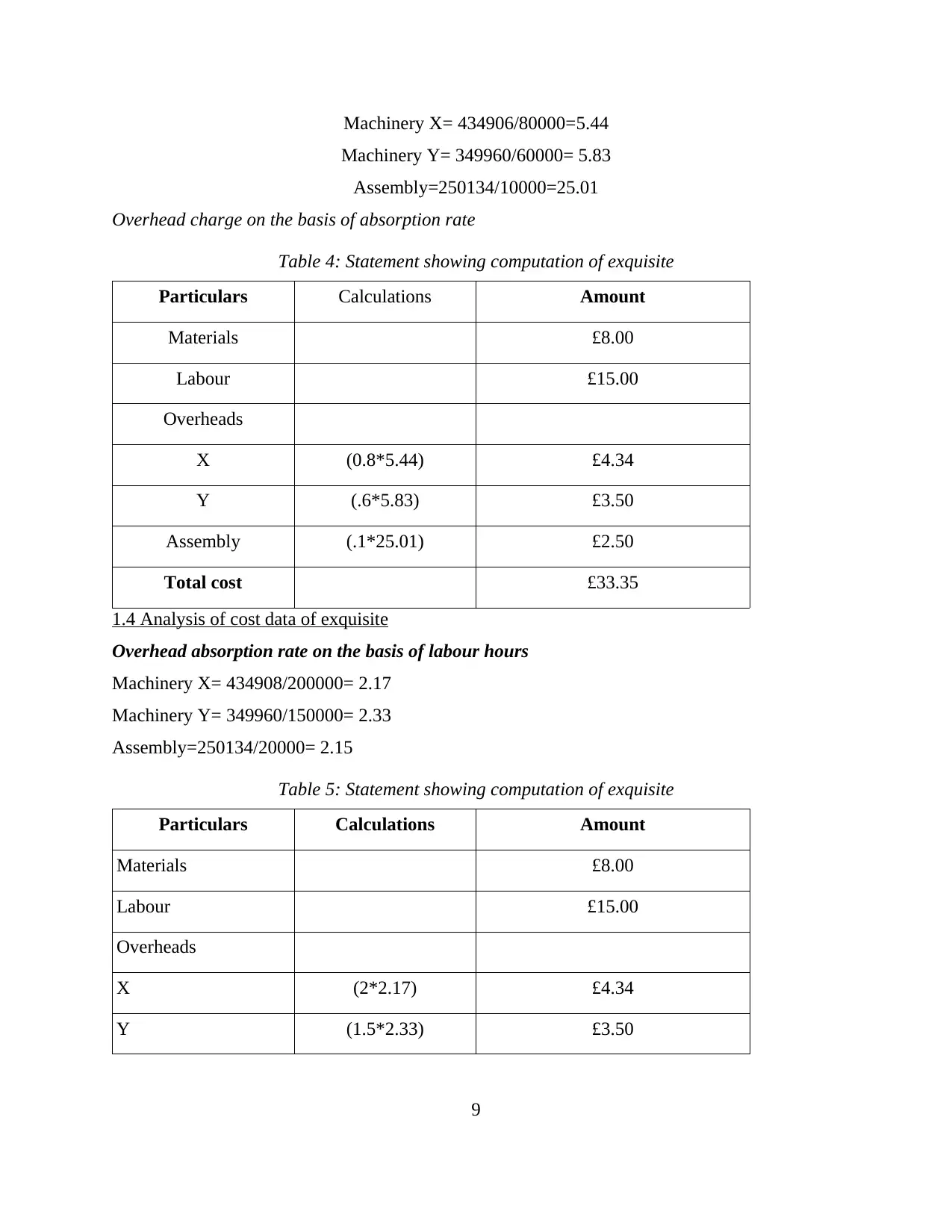

Machinery X= 434906/80000=5.44

Machinery Y= 349960/60000= 5.83

Assembly=250134/10000=25.01

Overhead charge on the basis of absorption rate

Table 4: Statement showing computation of exquisite

Particulars Calculations Amount

Materials £8.00

Labour £15.00

Overheads

X (0.8*5.44) £4.34

Y (.6*5.83) £3.50

Assembly (.1*25.01) £2.50

Total cost £33.35

1.4 Analysis of cost data of exquisite

Overhead absorption rate on the basis of labour hours

Machinery X= 434908/200000= 2.17

Machinery Y= 349960/150000= 2.33

Assembly=250134/20000= 2.15

Table 5: Statement showing computation of exquisite

Particulars Calculations Amount

Materials £8.00

Labour £15.00

Overheads

X (2*2.17) £4.34

Y (1.5*2.33) £3.50

9

Machinery Y= 349960/60000= 5.83

Assembly=250134/10000=25.01

Overhead charge on the basis of absorption rate

Table 4: Statement showing computation of exquisite

Particulars Calculations Amount

Materials £8.00

Labour £15.00

Overheads

X (0.8*5.44) £4.34

Y (.6*5.83) £3.50

Assembly (.1*25.01) £2.50

Total cost £33.35

1.4 Analysis of cost data of exquisite

Overhead absorption rate on the basis of labour hours

Machinery X= 434908/200000= 2.17

Machinery Y= 349960/150000= 2.33

Assembly=250134/20000= 2.15

Table 5: Statement showing computation of exquisite

Particulars Calculations Amount

Materials £8.00

Labour £15.00

Overheads

X (2*2.17) £4.34

Y (1.5*2.33) £3.50

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

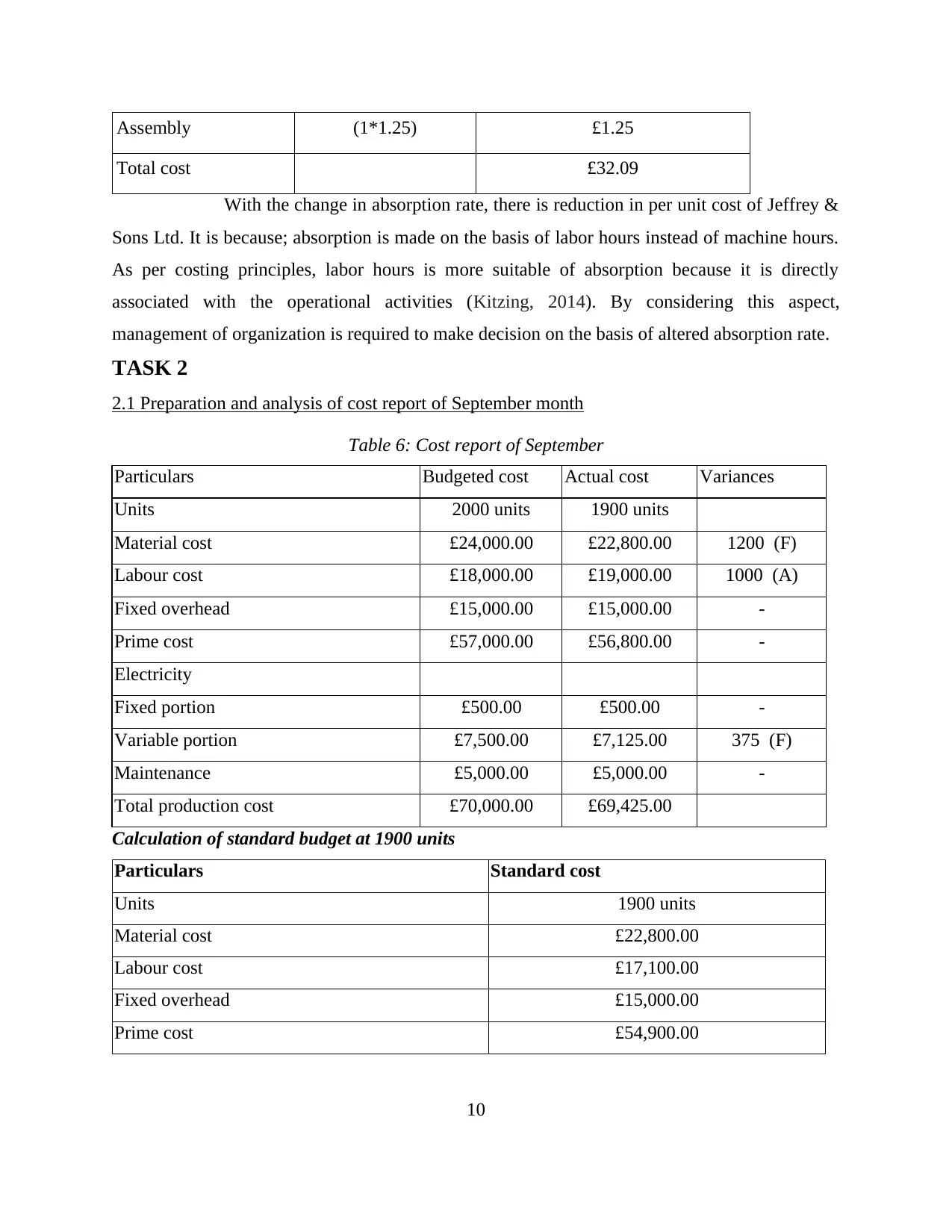

Assembly (1*1.25) £1.25

Total cost £32.09

With the change in absorption rate, there is reduction in per unit cost of Jeffrey &

Sons Ltd. It is because; absorption is made on the basis of labor hours instead of machine hours.

As per costing principles, labor hours is more suitable of absorption because it is directly

associated with the operational activities (Kitzing, 2014). By considering this aspect,

management of organization is required to make decision on the basis of altered absorption rate.

TASK 2

2.1 Preparation and analysis of cost report of September month

Table 6: Cost report of September

Particulars Budgeted cost Actual cost Variances

Units 2000 units 1900 units

Material cost £24,000.00 £22,800.00 1200 (F)

Labour cost £18,000.00 £19,000.00 1000 (A)

Fixed overhead £15,000.00 £15,000.00 -

Prime cost £57,000.00 £56,800.00 -

Electricity

Fixed portion £500.00 £500.00 -

Variable portion £7,500.00 £7,125.00 375 (F)

Maintenance £5,000.00 £5,000.00 -

Total production cost £70,000.00 £69,425.00

Calculation of standard budget at 1900 units

Particulars Standard cost

Units 1900 units

Material cost £22,800.00

Labour cost £17,100.00

Fixed overhead £15,000.00

Prime cost £54,900.00

10

Total cost £32.09

With the change in absorption rate, there is reduction in per unit cost of Jeffrey &

Sons Ltd. It is because; absorption is made on the basis of labor hours instead of machine hours.

As per costing principles, labor hours is more suitable of absorption because it is directly

associated with the operational activities (Kitzing, 2014). By considering this aspect,

management of organization is required to make decision on the basis of altered absorption rate.

TASK 2

2.1 Preparation and analysis of cost report of September month

Table 6: Cost report of September

Particulars Budgeted cost Actual cost Variances

Units 2000 units 1900 units

Material cost £24,000.00 £22,800.00 1200 (F)

Labour cost £18,000.00 £19,000.00 1000 (A)

Fixed overhead £15,000.00 £15,000.00 -

Prime cost £57,000.00 £56,800.00 -

Electricity

Fixed portion £500.00 £500.00 -

Variable portion £7,500.00 £7,125.00 375 (F)

Maintenance £5,000.00 £5,000.00 -

Total production cost £70,000.00 £69,425.00

Calculation of standard budget at 1900 units

Particulars Standard cost

Units 1900 units

Material cost £22,800.00

Labour cost £17,100.00

Fixed overhead £15,000.00

Prime cost £54,900.00

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

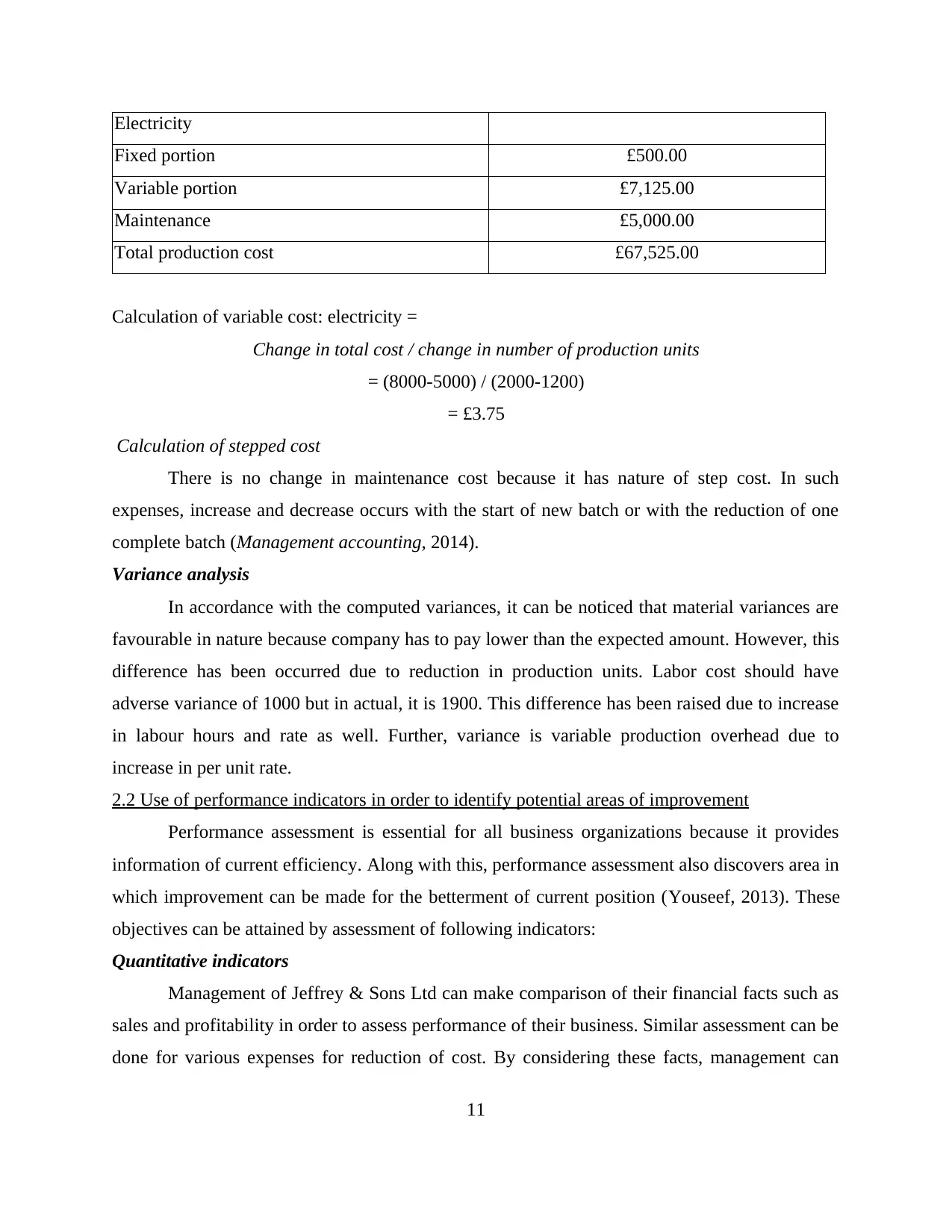

Electricity

Fixed portion £500.00

Variable portion £7,125.00

Maintenance £5,000.00

Total production cost £67,525.00

Calculation of variable cost: electricity =

Change in total cost / change in number of production units

= (8000-5000) / (2000-1200)

= £3.75

Calculation of stepped cost

There is no change in maintenance cost because it has nature of step cost. In such

expenses, increase and decrease occurs with the start of new batch or with the reduction of one

complete batch (Management accounting, 2014).

Variance analysis

In accordance with the computed variances, it can be noticed that material variances are

favourable in nature because company has to pay lower than the expected amount. However, this

difference has been occurred due to reduction in production units. Labor cost should have

adverse variance of 1000 but in actual, it is 1900. This difference has been raised due to increase

in labour hours and rate as well. Further, variance is variable production overhead due to

increase in per unit rate.

2.2 Use of performance indicators in order to identify potential areas of improvement

Performance assessment is essential for all business organizations because it provides

information of current efficiency. Along with this, performance assessment also discovers area in

which improvement can be made for the betterment of current position (Youseef, 2013). These

objectives can be attained by assessment of following indicators:

Quantitative indicators

Management of Jeffrey & Sons Ltd can make comparison of their financial facts such as

sales and profitability in order to assess performance of their business. Similar assessment can be

done for various expenses for reduction of cost. By considering these facts, management can

11

Fixed portion £500.00

Variable portion £7,125.00

Maintenance £5,000.00

Total production cost £67,525.00

Calculation of variable cost: electricity =

Change in total cost / change in number of production units

= (8000-5000) / (2000-1200)

= £3.75

Calculation of stepped cost

There is no change in maintenance cost because it has nature of step cost. In such

expenses, increase and decrease occurs with the start of new batch or with the reduction of one

complete batch (Management accounting, 2014).

Variance analysis

In accordance with the computed variances, it can be noticed that material variances are

favourable in nature because company has to pay lower than the expected amount. However, this

difference has been occurred due to reduction in production units. Labor cost should have

adverse variance of 1000 but in actual, it is 1900. This difference has been raised due to increase

in labour hours and rate as well. Further, variance is variable production overhead due to

increase in per unit rate.

2.2 Use of performance indicators in order to identify potential areas of improvement

Performance assessment is essential for all business organizations because it provides

information of current efficiency. Along with this, performance assessment also discovers area in

which improvement can be made for the betterment of current position (Youseef, 2013). These

objectives can be attained by assessment of following indicators:

Quantitative indicators

Management of Jeffrey & Sons Ltd can make comparison of their financial facts such as

sales and profitability in order to assess performance of their business. Similar assessment can be

done for various expenses for reduction of cost. By considering these facts, management can

11

identify the costs which are continuously increasing and areas which are providing declining

revenue.

Qualitative indicators

Qualitative indicators comprises of customer feedback and satisfaction level. For this,

management of company can make policy of consideration for customer reviews on provided

product and services (Wildavsky, 2006). In this manner, organization can determine areas where

customers are facing maximum issues.

2.3 Recommendations for cost reduction and enhancement is quality and value

In order to make cost reduction and value enhancement, management of Jeffrey & Sons

Ltd can make use of following recommendations: Kaizen costing: This costing approach assists in reduction of wastage in production

process. Kaizen costing is focused on reduction of expenses which are not able to provide

economic advantage to the business (Keown, 2005). Total quality management (TQM): This method integrates entire operational activities in

order to enhance its quality for covering loopholes of the operational process. By the

applicability of this method, management of company can solve their quality issue in

order to provide better product and services to the customers. Stock management: In order to reduce storage and order cost, company can make use of

techniques such as just in time purchase and EOQ. With these methods, they will place

optimum order to reduce wastage of material and prevention of issues of stock out

(Kastantin, 2005).

Other: In addition to above described factors, management audit can be conducted to

monitor and control the performance of subordinates.

TASK 3

3.1 Nature and purpose of budgetary procedure

Budget is a statement showing revenues and costs of future period. It provides financial

framework on the basis of which decisions are taken by managerial parties. In addition to this, it

also assists in monitoring of performance by making comparison of actual values with the

budgeted figures (Budget, Budgeting Process, and Variances, 2016). Budgets are prepared on the

basis of estimation. It determines forecasted revenues and expenditures by considering market

12

revenue.

Qualitative indicators

Qualitative indicators comprises of customer feedback and satisfaction level. For this,

management of company can make policy of consideration for customer reviews on provided

product and services (Wildavsky, 2006). In this manner, organization can determine areas where

customers are facing maximum issues.

2.3 Recommendations for cost reduction and enhancement is quality and value

In order to make cost reduction and value enhancement, management of Jeffrey & Sons

Ltd can make use of following recommendations: Kaizen costing: This costing approach assists in reduction of wastage in production

process. Kaizen costing is focused on reduction of expenses which are not able to provide

economic advantage to the business (Keown, 2005). Total quality management (TQM): This method integrates entire operational activities in

order to enhance its quality for covering loopholes of the operational process. By the

applicability of this method, management of company can solve their quality issue in

order to provide better product and services to the customers. Stock management: In order to reduce storage and order cost, company can make use of

techniques such as just in time purchase and EOQ. With these methods, they will place

optimum order to reduce wastage of material and prevention of issues of stock out

(Kastantin, 2005).

Other: In addition to above described factors, management audit can be conducted to

monitor and control the performance of subordinates.

TASK 3

3.1 Nature and purpose of budgetary procedure

Budget is a statement showing revenues and costs of future period. It provides financial

framework on the basis of which decisions are taken by managerial parties. In addition to this, it

also assists in monitoring of performance by making comparison of actual values with the

budgeted figures (Budget, Budgeting Process, and Variances, 2016). Budgets are prepared on the

basis of estimation. It determines forecasted revenues and expenditures by considering market

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.