University Management Accounting Report: Concepts and Applications

VerifiedAdded on 2021/04/24

|16

|1850

|31

Report

AI Summary

This report on management accounting delves into several key aspects of the field. It begins by exploring the concept of Panopticism in relation to management accounting, highlighting its role in monitoring and surveillance of transactions. The report then outlines the three primary functions of management accounting: planning, organizing, and controlling, providing detailed explanations and examples for each. It touches upon the use of checklists, drawing an interesting analogy to a rock band's concert rider. The report also includes a discussion of perpetual inventory systems and the treatment of overtime costs. The assignment further incorporates manufacturing and income statements in both normal and formula views, as well as journal entries and ledger postings. Finally, it provides a comprehensive reference list of relevant academic sources.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

MANAGEMENT ACCOUNTING

Table of Contents

Answer to Question No 1................................................................................................................2

Answer to Question No 2................................................................................................................3

Answer to Question No 3................................................................................................................5

Answer to Question No 4:...............................................................................................................6

Normal View:..............................................................................................................................6

Manufacturing Statement:.......................................................................................................6

Income Statement:...................................................................................................................7

Formula View:.............................................................................................................................8

Manufacturing Statement:.......................................................................................................8

Income Statement:...................................................................................................................9

Answer to Question No 5..............................................................................................................10

Answer to Question No 6:.............................................................................................................10

Answer to Question No 7:.............................................................................................................11

Answer to Question No 8:.............................................................................................................11

Requirement a:...........................................................................................................................11

Requirement b:...........................................................................................................................11

Requirement c:...........................................................................................................................12

Reference List................................................................................................................................14

MANAGEMENT ACCOUNTING

Table of Contents

Answer to Question No 1................................................................................................................2

Answer to Question No 2................................................................................................................3

Answer to Question No 3................................................................................................................5

Answer to Question No 4:...............................................................................................................6

Normal View:..............................................................................................................................6

Manufacturing Statement:.......................................................................................................6

Income Statement:...................................................................................................................7

Formula View:.............................................................................................................................8

Manufacturing Statement:.......................................................................................................8

Income Statement:...................................................................................................................9

Answer to Question No 5..............................................................................................................10

Answer to Question No 6:.............................................................................................................10

Answer to Question No 7:.............................................................................................................11

Answer to Question No 8:.............................................................................................................11

Requirement a:...........................................................................................................................11

Requirement b:...........................................................................................................................11

Requirement c:...........................................................................................................................12

Reference List................................................................................................................................14

2

MANAGEMENT ACCOUNTING

Answer to Question No 1

Panopticism is a social or a communal theory named after Panopticon, which was created

by a French philosopher Michel Foucault. The panopticon addresses to an experimental

laboratory associated with power within which the behaviour can be changed or modified and

panopticon is looked upon as the sign of disciplinary society of surveillance. It is known as the

role of the disciplinary process like in a prison and explains the function of the discipline as an

equipment of power (Soltani et al., 2014). It is an ever visible inmate and recommends that it is

an object of information and is not a topic of communication.

For instance, panoptic theory has extensive ranging effects for surveillance in the digital

age and therefore it is seen that surveillance have an effective cultural allure. The rising visible

data that is made accessible to the companies and the individuals from the technologies of new

mining has led to proliferation of data surveillance which can be explained as the medium of

surveillance that looks to single out any specific kind of transaction with the help of routine

algorithmic production.

In accordance to definition that is given on Panopticism, is seen that this process has a

key role to play in the process of management accounting because in Panopticism leads to proper

monitoring and surveillance of all the transactions that are taking place and the surveillance of

each and every transaction details thereby keeping track of all the transactions and eliminating

the chances of any kind of error.

MANAGEMENT ACCOUNTING

Answer to Question No 1

Panopticism is a social or a communal theory named after Panopticon, which was created

by a French philosopher Michel Foucault. The panopticon addresses to an experimental

laboratory associated with power within which the behaviour can be changed or modified and

panopticon is looked upon as the sign of disciplinary society of surveillance. It is known as the

role of the disciplinary process like in a prison and explains the function of the discipline as an

equipment of power (Soltani et al., 2014). It is an ever visible inmate and recommends that it is

an object of information and is not a topic of communication.

For instance, panoptic theory has extensive ranging effects for surveillance in the digital

age and therefore it is seen that surveillance have an effective cultural allure. The rising visible

data that is made accessible to the companies and the individuals from the technologies of new

mining has led to proliferation of data surveillance which can be explained as the medium of

surveillance that looks to single out any specific kind of transaction with the help of routine

algorithmic production.

In accordance to definition that is given on Panopticism, is seen that this process has a

key role to play in the process of management accounting because in Panopticism leads to proper

monitoring and surveillance of all the transactions that are taking place and the surveillance of

each and every transaction details thereby keeping track of all the transactions and eliminating

the chances of any kind of error.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

MANAGEMENT ACCOUNTING

Answer to Question No 2

The three functions of management accounting are as follows:

Planning

It is the process of constructing the long term and short term actions and plans to gain a

specific end. Management accounting is a closely connected with planning as it provides the data

for the purpose of decision making and because the entire process of budgeting is created around

the reports that are associated to accounting (Otley, 2016). Management accounting assists the

managers in planning by giving out reports which projects the impact of the alternative actions

on the ability of a company to attain their desired objectives and goals. For instance, what are the

products that are to be sold and at what prices? The process of management accounting creates a

data that aids the managers to recognise the products that are more profitable. In the same

manner the impacts of the substitute prices and the efforts of selling can be determined easily by

the management accountant. As a section of the process of budgeting, the management

accountants construct financial statements which are called proforma statements.

Organising

Organising is the process of creating a business framework and allocating the

responsibilities to the employee functioning in the company for gaining the objectives and goals

of the business. The kind of organizational framework is different from one company to the

other. In the process of organising departmentalization can be undertaken by creating divisions

sections and branches (Fullerton et al., 2014).

Organising is in need of clarity about the obligation of the managers and the authority

lines. The several departments and units are interconnected in a hierarchical manner with a

MANAGEMENT ACCOUNTING

Answer to Question No 2

The three functions of management accounting are as follows:

Planning

It is the process of constructing the long term and short term actions and plans to gain a

specific end. Management accounting is a closely connected with planning as it provides the data

for the purpose of decision making and because the entire process of budgeting is created around

the reports that are associated to accounting (Otley, 2016). Management accounting assists the

managers in planning by giving out reports which projects the impact of the alternative actions

on the ability of a company to attain their desired objectives and goals. For instance, what are the

products that are to be sold and at what prices? The process of management accounting creates a

data that aids the managers to recognise the products that are more profitable. In the same

manner the impacts of the substitute prices and the efforts of selling can be determined easily by

the management accountant. As a section of the process of budgeting, the management

accountants construct financial statements which are called proforma statements.

Organising

Organising is the process of creating a business framework and allocating the

responsibilities to the employee functioning in the company for gaining the objectives and goals

of the business. The kind of organizational framework is different from one company to the

other. In the process of organising departmentalization can be undertaken by creating divisions

sections and branches (Fullerton et al., 2014).

Organising is in need of clarity about the obligation of the managers and the authority

lines. The several departments and units are interconnected in a hierarchical manner with a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

MANAGEMENT ACCOUNTING

formal structure of communication in which the data and the instructions are forwarded down to

the lower level management and upwards to the management of the top level.

Management accounting assists the managers in organising by giving out the documents

and the reports that are essential information in order to adjust and regulate the activities and the

operations in accordance to the changing scenario (Maas et al., 2016). For instance, the

documents under the process of management accounting can be constructed on the product lines

on which the managers can take the decision whether to eliminate or add a product line in the

present mix of product. In the same manner, the management accountant can provide the sales

report, production report to the managers for taking appropriate actions about the production and

the sales position.

Controlling

Controlling is the process of computing, assessing, monitoring and rectifying the actual

result to make sure that the business plans and goals are attained. Control is attained with the

help of gaining feedback (Chenhall, & Moers 2015). Feedback is the data that can be utilised in

order to assess or rectify the steps that is being taken in order to incorporate a plan. Feedback

permits the managers to take decisions to let the activities and the operations to sustain as they

are and take rectifiable decisions to put certain actions back in the agreement with the actual plan

and objectives or do certain re-planning and rearranging at the midstream.

Management accounting is helpful in the control function by manufacturing performance

reports and the control reports which addresses the variances among the actual and the expected

performances. These statements and reports acts as a basis for undertaking essential corrective

measures in order to control the operational process. The utilisation of the performance and

MANAGEMENT ACCOUNTING

formal structure of communication in which the data and the instructions are forwarded down to

the lower level management and upwards to the management of the top level.

Management accounting assists the managers in organising by giving out the documents

and the reports that are essential information in order to adjust and regulate the activities and the

operations in accordance to the changing scenario (Maas et al., 2016). For instance, the

documents under the process of management accounting can be constructed on the product lines

on which the managers can take the decision whether to eliminate or add a product line in the

present mix of product. In the same manner, the management accountant can provide the sales

report, production report to the managers for taking appropriate actions about the production and

the sales position.

Controlling

Controlling is the process of computing, assessing, monitoring and rectifying the actual

result to make sure that the business plans and goals are attained. Control is attained with the

help of gaining feedback (Chenhall, & Moers 2015). Feedback is the data that can be utilised in

order to assess or rectify the steps that is being taken in order to incorporate a plan. Feedback

permits the managers to take decisions to let the activities and the operations to sustain as they

are and take rectifiable decisions to put certain actions back in the agreement with the actual plan

and objectives or do certain re-planning and rearranging at the midstream.

Management accounting is helpful in the control function by manufacturing performance

reports and the control reports which addresses the variances among the actual and the expected

performances. These statements and reports acts as a basis for undertaking essential corrective

measures in order to control the operational process. The utilisation of the performance and

5

MANAGEMENT ACCOUNTING

control statements follows the principle of the management by exemption. In case of the key

differences among the actual and the budgeted outcomes, a manager will generally examine in

order to ascertain what is happening wrong and probably, which units may require assistance.

Answer to Question No 3

Checklists are seen even in the arena of rock and music. There exists a story of the fact

that rocker David Lee Roth’s disreputable case that Van Halen’s agreements with the promoters

of the concerts had a clause that explained that a bowl of M&M’s has to be given at the

backstage, but with every individual brown candy that has been removed, during the forfeiture of

pain of the show; with an entire compensation to the band. Even once, Van Halen actually

followed the same and cancelled the show in Colorado when some brown M&M were found in

the dressing room of Roth. This turned out to be however, not an mad demand and authority of

the mad celebrities but an resourceful trick (Cooper et al., 2017).

MANAGEMENT ACCOUNTING

control statements follows the principle of the management by exemption. In case of the key

differences among the actual and the budgeted outcomes, a manager will generally examine in

order to ascertain what is happening wrong and probably, which units may require assistance.

Answer to Question No 3

Checklists are seen even in the arena of rock and music. There exists a story of the fact

that rocker David Lee Roth’s disreputable case that Van Halen’s agreements with the promoters

of the concerts had a clause that explained that a bowl of M&M’s has to be given at the

backstage, but with every individual brown candy that has been removed, during the forfeiture of

pain of the show; with an entire compensation to the band. Even once, Van Halen actually

followed the same and cancelled the show in Colorado when some brown M&M were found in

the dressing room of Roth. This turned out to be however, not an mad demand and authority of

the mad celebrities but an resourceful trick (Cooper et al., 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

MANAGEMENT ACCOUNTING

Answer to Question No 4:

Normal View:

Manufacturing Statement:

Particulars Amount Amount

($) ($)

Direct Materials:

Raw Materials 1/10/X6 11000

Raw Materials Purchased 842000

Inward Charges on Raw Material 25340

878340

Less: Raw Materials 30/09/X7 26000

Raw Materials to Production 852340

Add: Work in Process 1/10/X6 23000

875340

Less: Work in Process 30/09/X7 15000

Raw Materials in Goods Manufactured 860340

Direct Labor:

Direct Labor 456780

Add: Work in Process 1/10/X6 17000

473780

Less: Work in Process 30/09/X7 11000

Direct Labor in Goods Manufactured 462780

Prime Cost 1323120

Manufacturing Overhead:

Manufactring Expense 370000

Salaries (Factory) 380400

Insurance 9225

Rates 9425

Depreciation on Machinery 12900

781950

Add: Work in Process 1/10/X6 26000

807950

Less: Work in Process 30/09/X7 8000

Manufacturing Overhead in Goods

Manufactured 799950

Cost of Goods Manufactured 2123070

Tendulkar Manufacturing Co.

Manufacturing Statement

for the year ended 30th September 20X7

MANAGEMENT ACCOUNTING

Answer to Question No 4:

Normal View:

Manufacturing Statement:

Particulars Amount Amount

($) ($)

Direct Materials:

Raw Materials 1/10/X6 11000

Raw Materials Purchased 842000

Inward Charges on Raw Material 25340

878340

Less: Raw Materials 30/09/X7 26000

Raw Materials to Production 852340

Add: Work in Process 1/10/X6 23000

875340

Less: Work in Process 30/09/X7 15000

Raw Materials in Goods Manufactured 860340

Direct Labor:

Direct Labor 456780

Add: Work in Process 1/10/X6 17000

473780

Less: Work in Process 30/09/X7 11000

Direct Labor in Goods Manufactured 462780

Prime Cost 1323120

Manufacturing Overhead:

Manufactring Expense 370000

Salaries (Factory) 380400

Insurance 9225

Rates 9425

Depreciation on Machinery 12900

781950

Add: Work in Process 1/10/X6 26000

807950

Less: Work in Process 30/09/X7 8000

Manufacturing Overhead in Goods

Manufactured 799950

Cost of Goods Manufactured 2123070

Tendulkar Manufacturing Co.

Manufacturing Statement

for the year ended 30th September 20X7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGEMENT ACCOUNTING

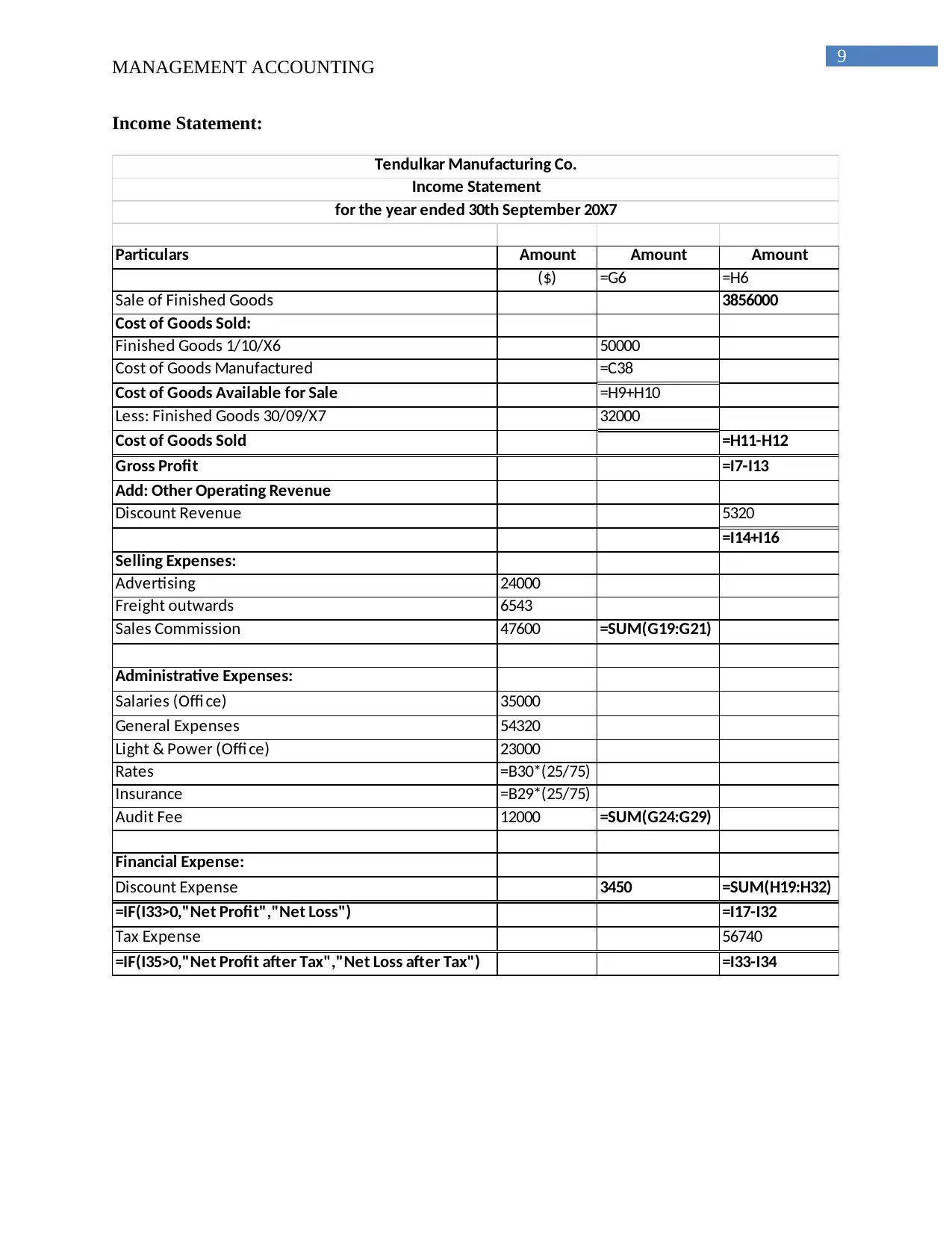

Income Statement:

Particulars Amount Amount Amount

($) ($) ($)

Sale of Finished Goods 3856000

Cost of Goods Sold:

Finished Goods 1/10/X6 50000

Cost of Goods Manufactured 2123070

Cost of Goods Available for Sale 2173070

Less: Finished Goods 30/09/X7 32000

Cost of Goods Sold 2141070

Gross Profit 1714930

Add: Other Operating Revenue

Discount Revenue 5320

1720250

Selling Expenses:

Advertising 24000

Freight outwards 6543

Sales Commission 47600 78143

Administrative Expenses:

Salaries (Offi ce) 35000

General Expenses 54320

Light & Power (Offi ce) 23000

Rates 3142

Insurance 3075

Audit Fee 12000 130537

Financial Expense:

Discount Expense 3450 212130

Net Profit 1508120

Tax Expense 56740

Net Profit after Tax 1451380

Tendulkar Manufacturing Co.

Income Statement

for the year ended 30th September 20X7

MANAGEMENT ACCOUNTING

Income Statement:

Particulars Amount Amount Amount

($) ($) ($)

Sale of Finished Goods 3856000

Cost of Goods Sold:

Finished Goods 1/10/X6 50000

Cost of Goods Manufactured 2123070

Cost of Goods Available for Sale 2173070

Less: Finished Goods 30/09/X7 32000

Cost of Goods Sold 2141070

Gross Profit 1714930

Add: Other Operating Revenue

Discount Revenue 5320

1720250

Selling Expenses:

Advertising 24000

Freight outwards 6543

Sales Commission 47600 78143

Administrative Expenses:

Salaries (Offi ce) 35000

General Expenses 54320

Light & Power (Offi ce) 23000

Rates 3142

Insurance 3075

Audit Fee 12000 130537

Financial Expense:

Discount Expense 3450 212130

Net Profit 1508120

Tax Expense 56740

Net Profit after Tax 1451380

Tendulkar Manufacturing Co.

Income Statement

for the year ended 30th September 20X7

8

MANAGEMENT ACCOUNTING

Formula View:

Manufacturing Statement:

Particulars Amount Amount

($) =B6

Direct Materials:

Raw Materials 1/10/X6 11000

Raw Materials Purchased 842000

Inward Charges on Raw Material 25340

=SUM(B8:B10)

Less: Raw Materials 30/09/X7 26000

Raw Materials to Production =B11-B12

Add: Work in Process 1/10/X6 23000

=B13+B14

Less: Work in Process 30/09/X7 15000

Raw Materials in Goods Manufactured =B15-B16

Direct Labor:

Direct Labor 456780

Add: Work in Process 1/10/X6 17000

=B20+B21

Less: Work in Process 30/09/X7 11000

Direct Labor in Goods Manufactured =B22-B23

Prime Cost =C17+C24

Manufacturing Overhead:

Manufactring Expense 370000

Salaries (Factory) =367800+12600

Insurance =(16000-3700)*75%

Rates =12567*75%

Depreciation on Machinery 12900

=SUM(B27:B31)

Add: Work in Process 1/10/X6 26000

=B32+B33

Less: Work in Process 30/09/X7 8000

Manufacturing Overhead in Goods Manufactured =B34-B35

Cost of Goods Manufactured =C25+C36

Tendulkar Manufacturing Co.

Manufacturing Statement

for the year ended 30th September 20X7

MANAGEMENT ACCOUNTING

Formula View:

Manufacturing Statement:

Particulars Amount Amount

($) =B6

Direct Materials:

Raw Materials 1/10/X6 11000

Raw Materials Purchased 842000

Inward Charges on Raw Material 25340

=SUM(B8:B10)

Less: Raw Materials 30/09/X7 26000

Raw Materials to Production =B11-B12

Add: Work in Process 1/10/X6 23000

=B13+B14

Less: Work in Process 30/09/X7 15000

Raw Materials in Goods Manufactured =B15-B16

Direct Labor:

Direct Labor 456780

Add: Work in Process 1/10/X6 17000

=B20+B21

Less: Work in Process 30/09/X7 11000

Direct Labor in Goods Manufactured =B22-B23

Prime Cost =C17+C24

Manufacturing Overhead:

Manufactring Expense 370000

Salaries (Factory) =367800+12600

Insurance =(16000-3700)*75%

Rates =12567*75%

Depreciation on Machinery 12900

=SUM(B27:B31)

Add: Work in Process 1/10/X6 26000

=B32+B33

Less: Work in Process 30/09/X7 8000

Manufacturing Overhead in Goods Manufactured =B34-B35

Cost of Goods Manufactured =C25+C36

Tendulkar Manufacturing Co.

Manufacturing Statement

for the year ended 30th September 20X7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

MANAGEMENT ACCOUNTING

Income Statement:

Particulars Amount Amount Amount

($) =G6 =H6

Sale of Finished Goods 3856000

Cost of Goods Sold:

Finished Goods 1/10/X6 50000

Cost of Goods Manufactured =C38

Cost of Goods Available for Sale =H9+H10

Less: Finished Goods 30/09/X7 32000

Cost of Goods Sold =H11-H12

Gross Profit =I7-I13

Add: Other Operating Revenue

Discount Revenue 5320

=I14+I16

Selling Expenses:

Advertising 24000

Freight outwards 6543

Sales Commission 47600 =SUM(G19:G21)

Administrative Expenses:

Salaries (Offi ce) 35000

General Expenses 54320

Light & Power (Offi ce) 23000

Rates =B30*(25/75)

Insurance =B29*(25/75)

Audit Fee 12000 =SUM(G24:G29)

Financial Expense:

Discount Expense 3450 =SUM(H19:H32)

=IF(I33>0,"Net Profit","Net Loss") =I17-I32

Tax Expense 56740

=IF(I35>0,"Net Profit after Tax","Net Loss after Tax") =I33-I34

Tendulkar Manufacturing Co.

Income Statement

for the year ended 30th September 20X7

MANAGEMENT ACCOUNTING

Income Statement:

Particulars Amount Amount Amount

($) =G6 =H6

Sale of Finished Goods 3856000

Cost of Goods Sold:

Finished Goods 1/10/X6 50000

Cost of Goods Manufactured =C38

Cost of Goods Available for Sale =H9+H10

Less: Finished Goods 30/09/X7 32000

Cost of Goods Sold =H11-H12

Gross Profit =I7-I13

Add: Other Operating Revenue

Discount Revenue 5320

=I14+I16

Selling Expenses:

Advertising 24000

Freight outwards 6543

Sales Commission 47600 =SUM(G19:G21)

Administrative Expenses:

Salaries (Offi ce) 35000

General Expenses 54320

Light & Power (Offi ce) 23000

Rates =B30*(25/75)

Insurance =B29*(25/75)

Audit Fee 12000 =SUM(G24:G29)

Financial Expense:

Discount Expense 3450 =SUM(H19:H32)

=IF(I33>0,"Net Profit","Net Loss") =I17-I32

Tax Expense 56740

=IF(I35>0,"Net Profit after Tax","Net Loss after Tax") =I33-I34

Tendulkar Manufacturing Co.

Income Statement

for the year ended 30th September 20X7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

MANAGEMENT ACCOUNTING

Answer to Question No 5

(a) If a perpetual inventory system is utilised for the recording of the movement of the raw

materials, there is no need to undertake a physical stock take because of the fact that

perpetual system upgrades the records of the inventory as the organization makes use of

the raw materials or sell the products to their consumers (Messner, 2016). For instance, in

a store, when the consumers buys a product, the cash register deducts automatically the

product from the records of the inventory but in case of a manufacturing company, the

work order process deducts the raw materials from the records of the inventory when the

manufacturing department initiates the order. The perpetual system subtracts the finished

product from the system when the customers order the product from the facility.

(b) Overtime is the value or the amount that is paid for the extra hours worked over the

normal wage rate. Overtime amount is treated as an indirect labour cost and therefore is

treated in the manufacturing overhead. This is due to the fact that the overtime that is

worked in not within the actual working hour of the employee and the worker is working

additionally over their actual working hour (Chiwamit et al., 2017). This payment is an

overhead for the company as this is an additional payment over the direct labour cost that

is estimated by the company. This amount has to be paid by cutting down any other

expense source and thereby it is treated as an overhead.

Answer to Question No 6:

Dr. Cr.

Date Particulars Amount Date Particulars Amount

01-Apr To, Balance b/d 60000 30-Apr By,Work-in-Process A/c. 60000

30-Apr Accounts Payable A/c. 80000 30-Apr By, Manufacturing Overhead A/c. 30000

30-Apr By,Balance c/d. 50000

140000 140000

Material Control A/c.

MANAGEMENT ACCOUNTING

Answer to Question No 5

(a) If a perpetual inventory system is utilised for the recording of the movement of the raw

materials, there is no need to undertake a physical stock take because of the fact that

perpetual system upgrades the records of the inventory as the organization makes use of

the raw materials or sell the products to their consumers (Messner, 2016). For instance, in

a store, when the consumers buys a product, the cash register deducts automatically the

product from the records of the inventory but in case of a manufacturing company, the

work order process deducts the raw materials from the records of the inventory when the

manufacturing department initiates the order. The perpetual system subtracts the finished

product from the system when the customers order the product from the facility.

(b) Overtime is the value or the amount that is paid for the extra hours worked over the

normal wage rate. Overtime amount is treated as an indirect labour cost and therefore is

treated in the manufacturing overhead. This is due to the fact that the overtime that is

worked in not within the actual working hour of the employee and the worker is working

additionally over their actual working hour (Chiwamit et al., 2017). This payment is an

overhead for the company as this is an additional payment over the direct labour cost that

is estimated by the company. This amount has to be paid by cutting down any other

expense source and thereby it is treated as an overhead.

Answer to Question No 6:

Dr. Cr.

Date Particulars Amount Date Particulars Amount

01-Apr To, Balance b/d 60000 30-Apr By,Work-in-Process A/c. 60000

30-Apr Accounts Payable A/c. 80000 30-Apr By, Manufacturing Overhead A/c. 30000

30-Apr By,Balance c/d. 50000

140000 140000

Material Control A/c.

11

MANAGEMENT ACCOUNTING

Journal Entry:

Dr. Cr.

Date Particulars Amount Amount

30-Apr Manufacturing Overhead A/c……Dr. 30000

To, Material Control A/c. 30000

Answer to Question No 7:

Dr. Cr.

Date Particulars Amount Date Particulars Amount

01-Jul To, Bank A/c. 40000 01-Jul By, Balance b/d. 18000

31-Jul By, WIP Control A/c. 50000

31-Jul To, Balance c/d. 50000 By, Overhead Control A/c. 22000

90000 90000

Accrued Payroll A/c.

Answer to Question No 8:

Requirement a:

Period

Nos. of

Days

Gross Payroll

per day

Accrued

Payroll

1/09 to 3/09 3 $8,000 $24,000

4/09 to 10/09 5 $8,000 $40,000

11/09 to 17/09 5 $8,000 $40,000

18/09 to 24/09 5 $8,000 $40,000

25/09 to 30/09 4 $8,000 $32,000

Total Amount credited

to Accrued Payroll 22 $1,76,000

Requirement b:

Period

Accrued

Payroll Payment Balance

1/09 to 3/09 $24,000 $24,000 $0

4/09 to 10/09 $40,000 $40,000 $0

11/09 to 17/09 $40,000 $40,000 $0

18/09 to 24/09 $40,000 $40,000 $0

25/09 to 30/09 $32,000 $0 $32,000

Month End Balance in

Accrued Payroll $32,000

MANAGEMENT ACCOUNTING

Journal Entry:

Dr. Cr.

Date Particulars Amount Amount

30-Apr Manufacturing Overhead A/c……Dr. 30000

To, Material Control A/c. 30000

Answer to Question No 7:

Dr. Cr.

Date Particulars Amount Date Particulars Amount

01-Jul To, Bank A/c. 40000 01-Jul By, Balance b/d. 18000

31-Jul By, WIP Control A/c. 50000

31-Jul To, Balance c/d. 50000 By, Overhead Control A/c. 22000

90000 90000

Accrued Payroll A/c.

Answer to Question No 8:

Requirement a:

Period

Nos. of

Days

Gross Payroll

per day

Accrued

Payroll

1/09 to 3/09 3 $8,000 $24,000

4/09 to 10/09 5 $8,000 $40,000

11/09 to 17/09 5 $8,000 $40,000

18/09 to 24/09 5 $8,000 $40,000

25/09 to 30/09 4 $8,000 $32,000

Total Amount credited

to Accrued Payroll 22 $1,76,000

Requirement b:

Period

Accrued

Payroll Payment Balance

1/09 to 3/09 $24,000 $24,000 $0

4/09 to 10/09 $40,000 $40,000 $0

11/09 to 17/09 $40,000 $40,000 $0

18/09 to 24/09 $40,000 $40,000 $0

25/09 to 30/09 $32,000 $0 $32,000

Month End Balance in

Accrued Payroll $32,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.