Management Accounting Report: Techniques for Putney Enterprise

VerifiedAdded on 2020/07/22

|17

|5159

|35

Report

AI Summary

This report delves into the core concepts of management accounting, differentiating it from financial accounting and emphasizing its role in internal decision-making. It explores various management accounting systems, including cost accounting, inventory management, and job costing systems, highlighting their applications in providing crucial internal data for managers. The report then examines different reporting methods such as budgeting reports, accounts receivable aging reports, job cost reports, and inventory and manufacturing reports. Furthermore, it evaluates the benefits of management accounting systems, particularly in terms of cost reduction, improved cash flow, and enhanced financial returns, and analyzes the integration of management accounting systems and reporting within organizational processes. The report also includes a practical application involving the calculation of costs using marginal and absorption costing to prepare income statements for Putney Enterprise, a UK-based SME. It further explores planning tools used for budgetary control, comparing methods adapted to respond to financial problems, and evaluating the importance of management accounting systems in achieving sustainable success and overcoming financial obstacles. The report concludes with an overview of the key findings and recommendations related to the application of management accounting principles.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Explaining management accounting and essential requirement of different types of

management accounting systems...........................................................................................1

P2 Explaining different methods used for management accounting reporting......................3

M1 Evaluating benefits of management accounting systems and its applications.................4

D1 Critically evaluate how management accounting systems and management accounting

reporting is integrated within organisational processes .........................................................4

TASK 2............................................................................................................................................5

P3 Calculation of cost using correct techniques of cost analysis to prepare an income

statements using marginal and absorption costing.................................................................5

M2 Applying management accounting techniques and financial reporting documents.........8

D2 Interpretation of accurately applicable financial report for Putney Enterprise................8

TASK 3............................................................................................................................................9

P4 Explaining the advantages and disadvantages of planning tools used for budgetary control.

................................................................................................................................................9

M3 Use of various kinds of planning tools in producing adequate budgets for Putney

Enterprise..............................................................................................................................11

TASK 4..........................................................................................................................................11

P5 Comparing methods adapted to respond to financial problems......................................11

M4 Evaluating the importance of management accounting systems in sustainable success and

overcoming financial obstacles............................................................................................12

D3 Analysing Planning tools leads to the sustainable success.............................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Explaining management accounting and essential requirement of different types of

management accounting systems...........................................................................................1

P2 Explaining different methods used for management accounting reporting......................3

M1 Evaluating benefits of management accounting systems and its applications.................4

D1 Critically evaluate how management accounting systems and management accounting

reporting is integrated within organisational processes .........................................................4

TASK 2............................................................................................................................................5

P3 Calculation of cost using correct techniques of cost analysis to prepare an income

statements using marginal and absorption costing.................................................................5

M2 Applying management accounting techniques and financial reporting documents.........8

D2 Interpretation of accurately applicable financial report for Putney Enterprise................8

TASK 3............................................................................................................................................9

P4 Explaining the advantages and disadvantages of planning tools used for budgetary control.

................................................................................................................................................9

M3 Use of various kinds of planning tools in producing adequate budgets for Putney

Enterprise..............................................................................................................................11

TASK 4..........................................................................................................................................11

P5 Comparing methods adapted to respond to financial problems......................................11

M4 Evaluating the importance of management accounting systems in sustainable success and

overcoming financial obstacles............................................................................................12

D3 Analysing Planning tools leads to the sustainable success.............................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting is that process which will be enabling all managers of any firm

whether big or small to access the information or data related to company. This will be telling

how the managers are going to decide over investment proposals which are coming to them or to

company. Management accounting enable managers who are been involved within decision

making procedure that how will they exact data from which source and then how would they be

using that particular data. Both type of financial and non financial information should be

included within this system of accounting and then reporting it to higher level of managers. The

present report is specifically based on management accounting, how this is different from

financial accounting. The report will also be covering what are all type of different reporting

methods that are been employed by managers of company. The company which report would be

covering is a SME enterprise of UK i.e., Putney Enterprise and at the end report will be covering

different methods which are adopted financial problems.

TASK 1

P1 Explaining management accounting and essential requirement of different types of

management accounting systems.

Management accounting is basically concern with production of data so that managers

could use that information for their internal purpose and then making important decision making.

All types of information which are been involved within this system is based on internal form

and there are various management accounting systems which are been employed. Each and every

system would be designed on bases of their information and need of management which will be

helping in decision making. The very basic and common type of management accounting

systems that are used would be as under stated:

Cost accounting system-

This type of accounting system which is also called as product costing system is based on

frameworks so that cost of each and every department or products could be estimated up to their

profitability. Other than taking out profits of all products or working cost accounting is also

helping to take out inventory valuation and then controlling of cost so that there is lesser amount

of waste (Hopper and Bui, 2016). This system will also be having two different type of

accounting systems namely job order cost and process costing. Once the total cost of whole

1

Management accounting is that process which will be enabling all managers of any firm

whether big or small to access the information or data related to company. This will be telling

how the managers are going to decide over investment proposals which are coming to them or to

company. Management accounting enable managers who are been involved within decision

making procedure that how will they exact data from which source and then how would they be

using that particular data. Both type of financial and non financial information should be

included within this system of accounting and then reporting it to higher level of managers. The

present report is specifically based on management accounting, how this is different from

financial accounting. The report will also be covering what are all type of different reporting

methods that are been employed by managers of company. The company which report would be

covering is a SME enterprise of UK i.e., Putney Enterprise and at the end report will be covering

different methods which are adopted financial problems.

TASK 1

P1 Explaining management accounting and essential requirement of different types of

management accounting systems.

Management accounting is basically concern with production of data so that managers

could use that information for their internal purpose and then making important decision making.

All types of information which are been involved within this system is based on internal form

and there are various management accounting systems which are been employed. Each and every

system would be designed on bases of their information and need of management which will be

helping in decision making. The very basic and common type of management accounting

systems that are used would be as under stated:

Cost accounting system-

This type of accounting system which is also called as product costing system is based on

frameworks so that cost of each and every department or products could be estimated up to their

profitability. Other than taking out profits of all products or working cost accounting is also

helping to take out inventory valuation and then controlling of cost so that there is lesser amount

of waste (Hopper and Bui, 2016). This system will also be having two different type of

accounting systems namely job order cost and process costing. Once the total cost of whole

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company is been identified managers will be carrying out allocation of those cost to various

departments and products of firm. This allocation which is done by cost accountants would either

be based on activity based or traditional costing systems.

Inventory management system-

All the stock or raw material which is been used by company in carrying or producing

end used products or finished goods are called as inventory. This will not only including raw

material but also the equipments or tools or methods that are used to produce or manufacture

finished goods. So it is essential for company that they are controlling bad use and wasting of

that inventory which is very much important and integral part of company (Pemsel and

Wiewiora, 2013). This management of inventory could be done by using effective technology,

better use of bar code printers or also with efficient staff or employees.

This will be working as to see how inventory could be tracked by incoming and outgoing

from warehouse and then effectively controlling that flow of stock. One of the main aim of this

system of management would be mentioned ot as what is current inventory level that could be

required by company. That would be between minimum and maximum level of inventory which

would be best suited so that chance of misplacement or wastage becomes minimum.

Job costing system-

This could be defined to as process of accumulation of all type of information based on

proper allocation of each and every job, service or production specified activity and then

allocation of cost accordingly. Products and service that are been produced within organisation

or company will be based on what and how much amount would be cost of manufacturing goods

and services. Job costing technique would also be used to inform about what could b a specified

cost over particular job so that this would be informed to customer better known to as client of

company. There are particularly three types of information that are been used in this job costing

system namely direct material, direct labour and overhead cost.

Price Optimisation System-

Under this system of management accounting technique various level of price that are

there at different level of demand of that particular product in market. These informations are

then combined so that data on inventory or cost at various levels are suggested and this will then

2

departments and products of firm. This allocation which is done by cost accountants would either

be based on activity based or traditional costing systems.

Inventory management system-

All the stock or raw material which is been used by company in carrying or producing

end used products or finished goods are called as inventory. This will not only including raw

material but also the equipments or tools or methods that are used to produce or manufacture

finished goods. So it is essential for company that they are controlling bad use and wasting of

that inventory which is very much important and integral part of company (Pemsel and

Wiewiora, 2013). This management of inventory could be done by using effective technology,

better use of bar code printers or also with efficient staff or employees.

This will be working as to see how inventory could be tracked by incoming and outgoing

from warehouse and then effectively controlling that flow of stock. One of the main aim of this

system of management would be mentioned ot as what is current inventory level that could be

required by company. That would be between minimum and maximum level of inventory which

would be best suited so that chance of misplacement or wastage becomes minimum.

Job costing system-

This could be defined to as process of accumulation of all type of information based on

proper allocation of each and every job, service or production specified activity and then

allocation of cost accordingly. Products and service that are been produced within organisation

or company will be based on what and how much amount would be cost of manufacturing goods

and services. Job costing technique would also be used to inform about what could b a specified

cost over particular job so that this would be informed to customer better known to as client of

company. There are particularly three types of information that are been used in this job costing

system namely direct material, direct labour and overhead cost.

Price Optimisation System-

Under this system of management accounting technique various level of price that are

there at different level of demand of that particular product in market. These informations are

then combined so that data on inventory or cost at various levels are suggested and this will then

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

be improving price and profits of firm. It is also having three of important factors which would

be defined to as price strategy, value of that product for customer and company and then

technique that are to be used by management that would be effecting proficiency of firm.

P2 Explaining different methods used for management accounting reporting.

Management accounting would be used to inform mangers about how much would

company be spending, what is their budget and what is actual cost of all production or working

of firm. However, one more important factor which is been associated with this type of reporting

function could be reporting of all these informations or data which they would be collecting.

Reporting includes very important activity of manager so that they could inform to higher level

of management that what could be estimated expenditure by company in coming or present year.

As this factor of year or particular period for which it would be calculated is very much essential

as generally all cost or profits are estimated only for specified time period (Nuhu and et.al.,

2017). There are different type of techniques which are been employed for reporting purpose by

management which are explained as under:

Budgeting report-

Budgets are very much important for all type of organisation which are working within

market which would be including estimated cost, price and profits of firm throughout particular

time period. So reporting budgets that are been prepared by managers would be very much

important and then they are reported to higher level management. This is very good and effective

technique been implemented within company which helps in estimating profits, firm's

performance and then controlling of cost so that there are no excessive wastage of fund or

money.

Accounts receivable ageing report-

This will be based on receivable of firm which are covering part of creditors who are part

of organisation and their amount is still outstanding or pending. This report will also be including

all those account receivable which are over aged and need to be expended over certain time

period. Report will be including various segregation of amount receivable, for how much time

this is been outstanding and what are future chance of getting them back. After this segregation

accountant would also be easily having knowledge about how good is receivable policy of

3

be defined to as price strategy, value of that product for customer and company and then

technique that are to be used by management that would be effecting proficiency of firm.

P2 Explaining different methods used for management accounting reporting.

Management accounting would be used to inform mangers about how much would

company be spending, what is their budget and what is actual cost of all production or working

of firm. However, one more important factor which is been associated with this type of reporting

function could be reporting of all these informations or data which they would be collecting.

Reporting includes very important activity of manager so that they could inform to higher level

of management that what could be estimated expenditure by company in coming or present year.

As this factor of year or particular period for which it would be calculated is very much essential

as generally all cost or profits are estimated only for specified time period (Nuhu and et.al.,

2017). There are different type of techniques which are been employed for reporting purpose by

management which are explained as under:

Budgeting report-

Budgets are very much important for all type of organisation which are working within

market which would be including estimated cost, price and profits of firm throughout particular

time period. So reporting budgets that are been prepared by managers would be very much

important and then they are reported to higher level management. This is very good and effective

technique been implemented within company which helps in estimating profits, firm's

performance and then controlling of cost so that there are no excessive wastage of fund or

money.

Accounts receivable ageing report-

This will be based on receivable of firm which are covering part of creditors who are part

of organisation and their amount is still outstanding or pending. This report will also be including

all those account receivable which are over aged and need to be expended over certain time

period. Report will be including various segregation of amount receivable, for how much time

this is been outstanding and what are future chance of getting them back. After this segregation

accountant would also be easily having knowledge about how good is receivable policy of

3

company and what all things need to be changed within organisation (Types of Management

accounting Reports. 2017). All the aged bad debts or outstanding amount of company would be

known to them so that they are able to reduce these debts and then maintain liquidity within

organisation.

Job cost reports-

This is another type of report which is been prepared by accountants of firm that would

be covering all sorts of expenses, cost and then how many profits the firm would be incurring

from different departments. As the name clearly suggest that this is report which is based on

various departments or job and then their costing so that accountant could make out relevant

profits of firm (Messner, 2016). This report would be evaluating whole and total cost of firm and

especially in that project which is running currently so that wastage could be lowered down and

project could be made more profitable.

Inventory and manufacturing reports-

This type of report is majorly made and prepared by those companies which are wholly

based on manufacturing or production of product the service based organisation are not required

to prepare inventory and manufacturing report. As this report would be including all inventory,

raw materials, labour cost, overhead cost of firm and also would be including wastage part of

firm. Thus, would also be including any opportunity which is been taken as per part of employee

or particular department of the firm so that improvement if any could be easily be implemented.

M1 Evaluating benefits of management accounting systems and its applications.

Management accounting is the best way to review the organisation actual position ui

terms of finance. This helps managers to take decision for investment and guide them to take

effective decision making process (Lock, 2014). This helps to keep the management on tract as

per the organisation objectives and goals. This helps to reduce the expenses of the business and

give better way to work. It also helps to improve cash flow, business decision and increase

financial returns as well.

4

accounting Reports. 2017). All the aged bad debts or outstanding amount of company would be

known to them so that they are able to reduce these debts and then maintain liquidity within

organisation.

Job cost reports-

This is another type of report which is been prepared by accountants of firm that would

be covering all sorts of expenses, cost and then how many profits the firm would be incurring

from different departments. As the name clearly suggest that this is report which is based on

various departments or job and then their costing so that accountant could make out relevant

profits of firm (Messner, 2016). This report would be evaluating whole and total cost of firm and

especially in that project which is running currently so that wastage could be lowered down and

project could be made more profitable.

Inventory and manufacturing reports-

This type of report is majorly made and prepared by those companies which are wholly

based on manufacturing or production of product the service based organisation are not required

to prepare inventory and manufacturing report. As this report would be including all inventory,

raw materials, labour cost, overhead cost of firm and also would be including wastage part of

firm. Thus, would also be including any opportunity which is been taken as per part of employee

or particular department of the firm so that improvement if any could be easily be implemented.

M1 Evaluating benefits of management accounting systems and its applications.

Management accounting is the best way to review the organisation actual position ui

terms of finance. This helps managers to take decision for investment and guide them to take

effective decision making process (Lock, 2014). This helps to keep the management on tract as

per the organisation objectives and goals. This helps to reduce the expenses of the business and

give better way to work. It also helps to improve cash flow, business decision and increase

financial returns as well.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

D1 Critically evaluate how management accounting systems and management accounting

reporting is integrated within organisational processes

Management accounting and managing reporting both the term is plays crucial role in the

organisation. It helps manager to check the requirement in the organization in terms of resources

and raw material etc. furthermore, sometimes due to this whole process manager takes much

time to make all those managing reporting system (Joshi and Li, 2016). Through which they fail

to focus on the other activities. Moreover, management accounting is the best way to determine

the actual needs in the organization.

TASK 2

P3 Calculation of cost using correct techniques of cost analysis to prepare an income statements

using marginal and absorption costing.

Cost would be the actual expenditure which is ascertained by company if thy are

producing any one or more products (Hopper and Bui, 2016). The value of money that could be

based on evaluating material, resources and then labour which would be employed at that portion

of production. Which would be including all kinds of cost like fixed and variable, historical and

replacement and opportunity cost as well. Fixed cost is that type of cost which company would

be incurring at all time whether they are working or operating or not cost like that of water and

electricity bills would be incurring at all times. Whereas, variable cost is that type of cost which

is incurring only at times when company is been in working and the time when they are

operating like that of cost of producing per unit of product. In order to determine cost there are

majorly two types of costing methods that are been used namely marginal and absorption

costing. Both these type of method would be determining cost in their own way

Marginal costing: this is that type of method that could be covering major part that is the

decision making process all variable cost should be charged as per cost of unit and then fixed of

time period would be written off in full manner (Hiebl, 2014). This is the most simple and

efficient method of calculating cost which would be including all effects that profits of firm are

having due ot level of production or output when they are changing. Putney Enterprise which

the is including this method of costing will be taking out marginal cost.

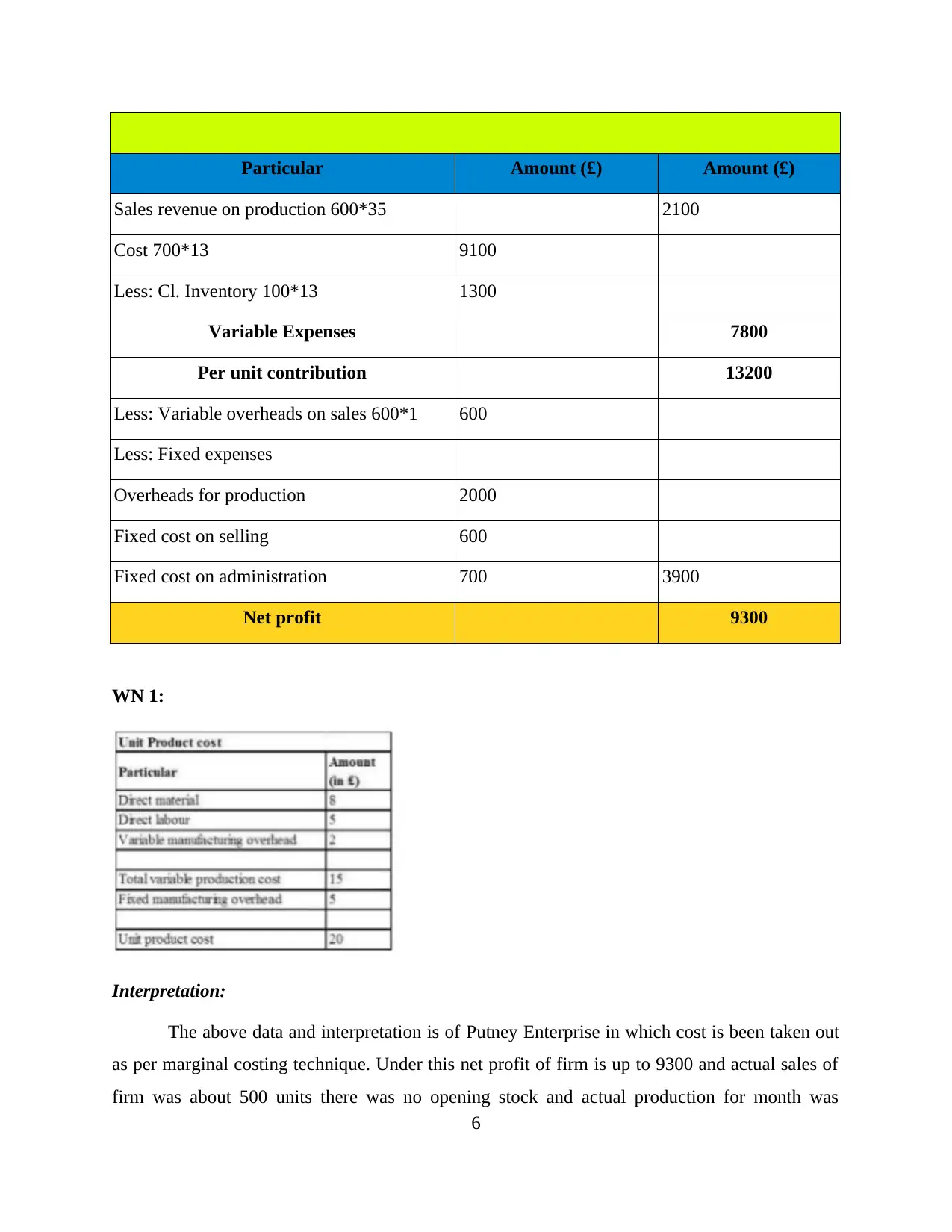

Income statements of Putney Enterprise on basis of Marginal costing

5

reporting is integrated within organisational processes

Management accounting and managing reporting both the term is plays crucial role in the

organisation. It helps manager to check the requirement in the organization in terms of resources

and raw material etc. furthermore, sometimes due to this whole process manager takes much

time to make all those managing reporting system (Joshi and Li, 2016). Through which they fail

to focus on the other activities. Moreover, management accounting is the best way to determine

the actual needs in the organization.

TASK 2

P3 Calculation of cost using correct techniques of cost analysis to prepare an income statements

using marginal and absorption costing.

Cost would be the actual expenditure which is ascertained by company if thy are

producing any one or more products (Hopper and Bui, 2016). The value of money that could be

based on evaluating material, resources and then labour which would be employed at that portion

of production. Which would be including all kinds of cost like fixed and variable, historical and

replacement and opportunity cost as well. Fixed cost is that type of cost which company would

be incurring at all time whether they are working or operating or not cost like that of water and

electricity bills would be incurring at all times. Whereas, variable cost is that type of cost which

is incurring only at times when company is been in working and the time when they are

operating like that of cost of producing per unit of product. In order to determine cost there are

majorly two types of costing methods that are been used namely marginal and absorption

costing. Both these type of method would be determining cost in their own way

Marginal costing: this is that type of method that could be covering major part that is the

decision making process all variable cost should be charged as per cost of unit and then fixed of

time period would be written off in full manner (Hiebl, 2014). This is the most simple and

efficient method of calculating cost which would be including all effects that profits of firm are

having due ot level of production or output when they are changing. Putney Enterprise which

the is including this method of costing will be taking out marginal cost.

Income statements of Putney Enterprise on basis of Marginal costing

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Particular Amount (£) Amount (£)

Sales revenue on production 600*35 2100

Cost 700*13 9100

Less: Cl. Inventory 100*13 1300

Variable Expenses 7800

Per unit contribution 13200

Less: Variable overheads on sales 600*1 600

Less: Fixed expenses

Overheads for production 2000

Fixed cost on selling 600

Fixed cost on administration 700 3900

Net profit 9300

WN 1:

Interpretation:

The above data and interpretation is of Putney Enterprise in which cost is been taken out

as per marginal costing technique. Under this net profit of firm is up to 9300 and actual sales of

firm was about 500 units there was no opening stock and actual production for month was

6

Sales revenue on production 600*35 2100

Cost 700*13 9100

Less: Cl. Inventory 100*13 1300

Variable Expenses 7800

Per unit contribution 13200

Less: Variable overheads on sales 600*1 600

Less: Fixed expenses

Overheads for production 2000

Fixed cost on selling 600

Fixed cost on administration 700 3900

Net profit 9300

WN 1:

Interpretation:

The above data and interpretation is of Putney Enterprise in which cost is been taken out

as per marginal costing technique. Under this net profit of firm is up to 9300 and actual sales of

firm was about 500 units there was no opening stock and actual production for month was

6

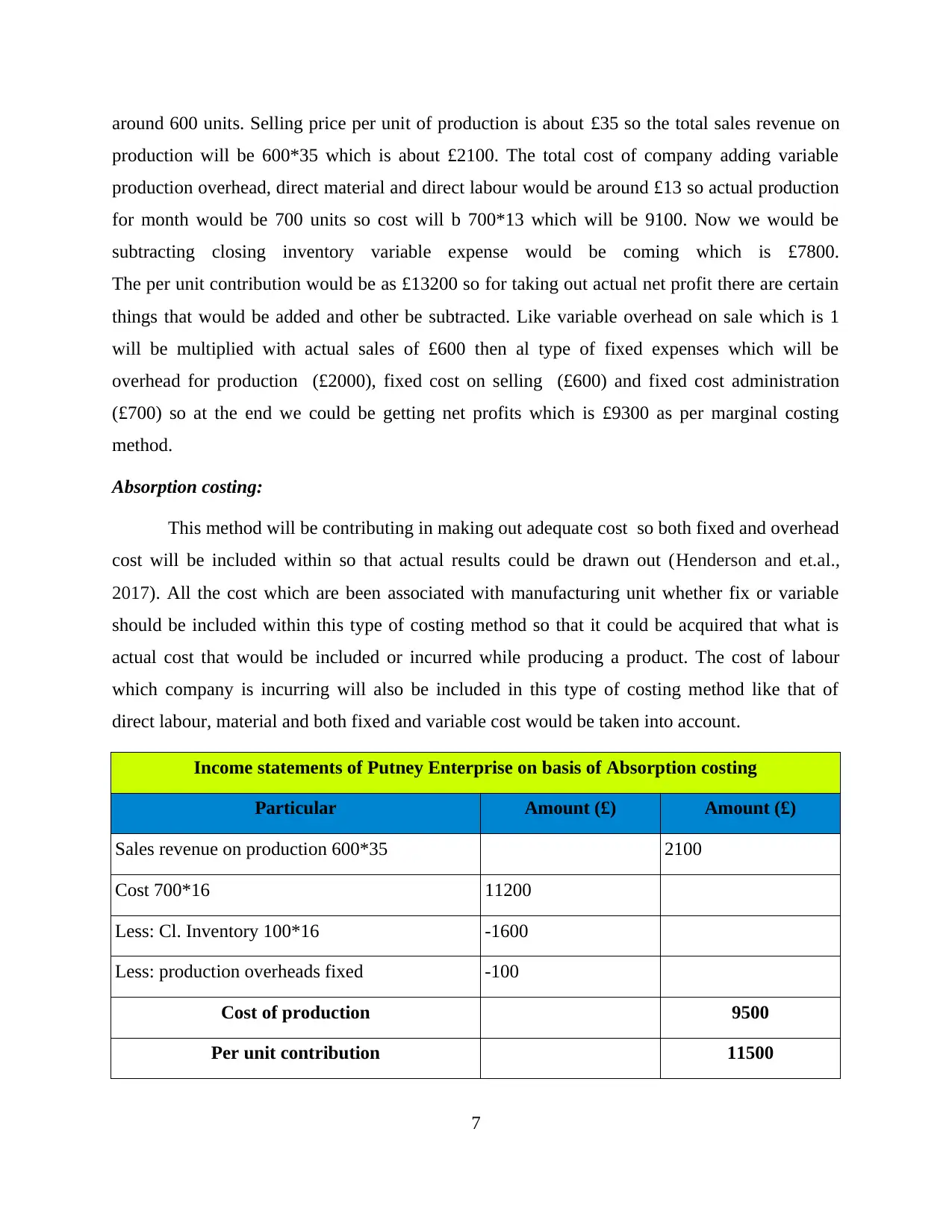

around 600 units. Selling price per unit of production is about £35 so the total sales revenue on

production will be 600*35 which is about £2100. The total cost of company adding variable

production overhead, direct material and direct labour would be around £13 so actual production

for month would be 700 units so cost will b 700*13 which will be 9100. Now we would be

subtracting closing inventory variable expense would be coming which is £7800.

The per unit contribution would be as £13200 so for taking out actual net profit there are certain

things that would be added and other be subtracted. Like variable overhead on sale which is 1

will be multiplied with actual sales of £600 then al type of fixed expenses which will be

overhead for production (£2000), fixed cost on selling (£600) and fixed cost administration

(£700) so at the end we could be getting net profits which is £9300 as per marginal costing

method.

Absorption costing:

This method will be contributing in making out adequate cost so both fixed and overhead

cost will be included within so that actual results could be drawn out (Henderson and et.al.,

2017). All the cost which are been associated with manufacturing unit whether fix or variable

should be included within this type of costing method so that it could be acquired that what is

actual cost that would be included or incurred while producing a product. The cost of labour

which company is incurring will also be included in this type of costing method like that of

direct labour, material and both fixed and variable cost would be taken into account.

Income statements of Putney Enterprise on basis of Absorption costing

Particular Amount (£) Amount (£)

Sales revenue on production 600*35 2100

Cost 700*16 11200

Less: Cl. Inventory 100*16 -1600

Less: production overheads fixed -100

Cost of production 9500

Per unit contribution 11500

7

production will be 600*35 which is about £2100. The total cost of company adding variable

production overhead, direct material and direct labour would be around £13 so actual production

for month would be 700 units so cost will b 700*13 which will be 9100. Now we would be

subtracting closing inventory variable expense would be coming which is £7800.

The per unit contribution would be as £13200 so for taking out actual net profit there are certain

things that would be added and other be subtracted. Like variable overhead on sale which is 1

will be multiplied with actual sales of £600 then al type of fixed expenses which will be

overhead for production (£2000), fixed cost on selling (£600) and fixed cost administration

(£700) so at the end we could be getting net profits which is £9300 as per marginal costing

method.

Absorption costing:

This method will be contributing in making out adequate cost so both fixed and overhead

cost will be included within so that actual results could be drawn out (Henderson and et.al.,

2017). All the cost which are been associated with manufacturing unit whether fix or variable

should be included within this type of costing method so that it could be acquired that what is

actual cost that would be included or incurred while producing a product. The cost of labour

which company is incurring will also be included in this type of costing method like that of

direct labour, material and both fixed and variable cost would be taken into account.

Income statements of Putney Enterprise on basis of Absorption costing

Particular Amount (£) Amount (£)

Sales revenue on production 600*35 2100

Cost 700*16 11200

Less: Cl. Inventory 100*16 -1600

Less: production overheads fixed -100

Cost of production 9500

Per unit contribution 11500

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

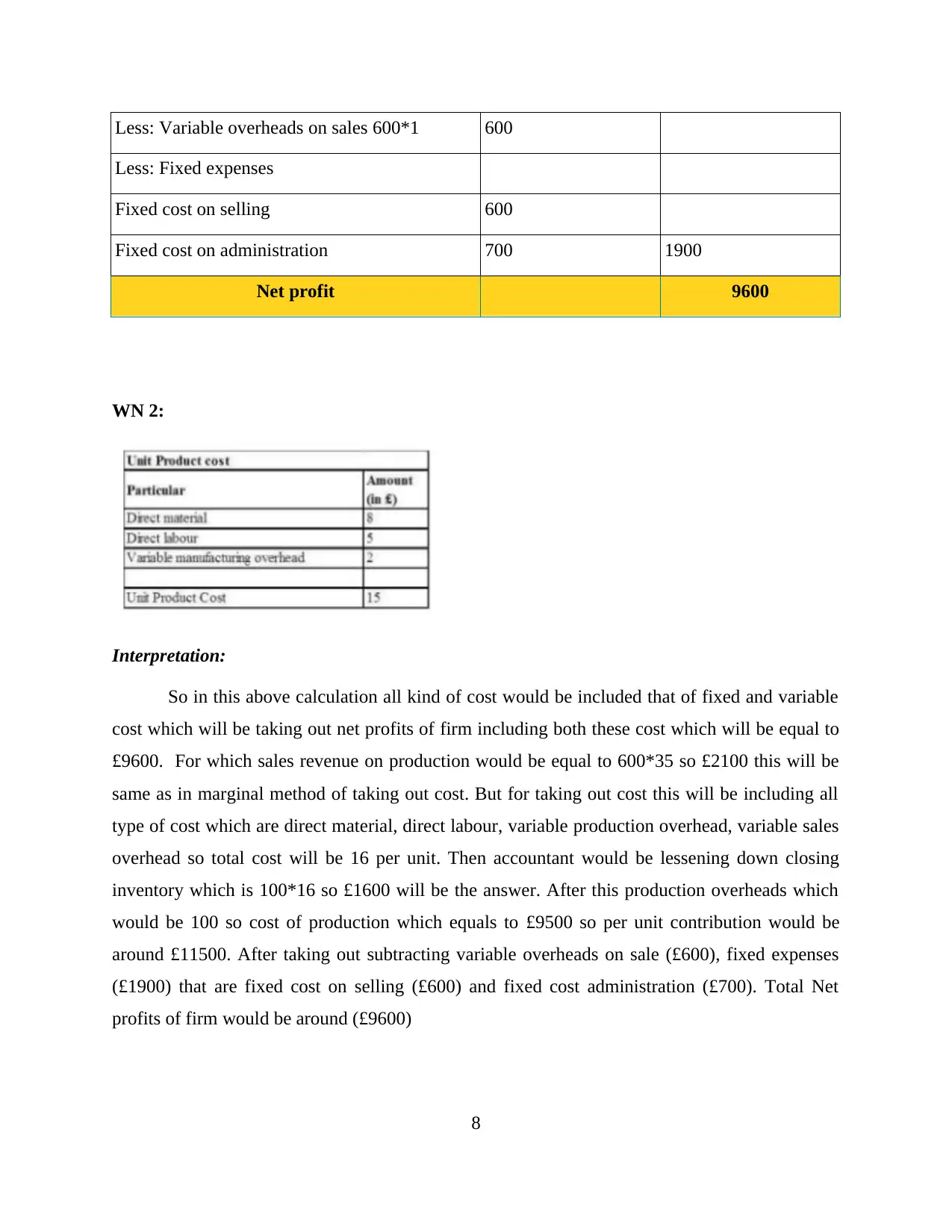

Less: Variable overheads on sales 600*1 600

Less: Fixed expenses

Fixed cost on selling 600

Fixed cost on administration 700 1900

Net profit 9600

WN 2:

Interpretation:

So in this above calculation all kind of cost would be included that of fixed and variable

cost which will be taking out net profits of firm including both these cost which will be equal to

£9600. For which sales revenue on production would be equal to 600*35 so £2100 this will be

same as in marginal method of taking out cost. But for taking out cost this will be including all

type of cost which are direct material, direct labour, variable production overhead, variable sales

overhead so total cost will be 16 per unit. Then accountant would be lessening down closing

inventory which is 100*16 so £1600 will be the answer. After this production overheads which

would be 100 so cost of production which equals to £9500 so per unit contribution would be

around £11500. After taking out subtracting variable overheads on sale (£600), fixed expenses

(£1900) that are fixed cost on selling (£600) and fixed cost administration (£700). Total Net

profits of firm would be around (£9600)

8

Less: Fixed expenses

Fixed cost on selling 600

Fixed cost on administration 700 1900

Net profit 9600

WN 2:

Interpretation:

So in this above calculation all kind of cost would be included that of fixed and variable

cost which will be taking out net profits of firm including both these cost which will be equal to

£9600. For which sales revenue on production would be equal to 600*35 so £2100 this will be

same as in marginal method of taking out cost. But for taking out cost this will be including all

type of cost which are direct material, direct labour, variable production overhead, variable sales

overhead so total cost will be 16 per unit. Then accountant would be lessening down closing

inventory which is 100*16 so £1600 will be the answer. After this production overheads which

would be 100 so cost of production which equals to £9500 so per unit contribution would be

around £11500. After taking out subtracting variable overheads on sale (£600), fixed expenses

(£1900) that are fixed cost on selling (£600) and fixed cost administration (£700). Total Net

profits of firm would be around (£9600)

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

M2 Applying management accounting techniques and financial reporting documents.

Management accounting techniques are the very much helpful to small scale industries to

make proper implementation of funds in order to get the final objectives and goals. This also

helps manager of the company to build innovative ideas at less cost. Besides, it also very much

essential to improve cash flows (Guinea, 2016). These techniques and methods guide manager to

make the effective action plan to make effective management accounting plan and reporting.

D2 Interpretation of accurately applicable financial report for Putney Enterprise

Financial report helps to interpret the company data and helps to determine the actual

position of the company. This financial report helps company to compare with the competitors in

order to determine their position. This is very essential tool to take corrective action plan for the

next financial year to get more sales revenue by enhancing the company product and services.

Moreover, the main objective of the organisation is to get effective sales to get best output

returns.

TASK 3

P4 Explaining the advantages and disadvantages of planning tools used for budgetary control.

In this context is to be focus on advantages and disadvantages for future planing, which is

focus on budget control.

Incremental budgeting: In this context such kind of budgeting control method is to be focus on

earlier year execution is to be taken inferior and after that additive amount of money area unit

enclosed for the fresh disbursal year. In additive planning the asset appellation count on the

earliest long time (Grabner and Moers, 2013). This is help to little improvement in current

spending plan for future. On the other hand, actual year’s disbursal plan is interpreted as the

basal to get at the ready one time period from now fiscal plan and plus are allotted similarly. In

this way, such kind of plan is to be focus on incremental plan for future time period are as

follows:

Steady change: In this context is to be focus on as a year ago financial plan is to be taken and

this is exceeding dependable disbursal plan from unitary period to different. Additive

disbursement plan permit uninterrupted alteration in Putney Enterprise.

Preference:

Downrightness as in this last year's spending configuration is taken as the base so this is

essential and easy to understand as the bookkeeper unquestionably considers the most recent

9

Management accounting techniques are the very much helpful to small scale industries to

make proper implementation of funds in order to get the final objectives and goals. This also

helps manager of the company to build innovative ideas at less cost. Besides, it also very much

essential to improve cash flows (Guinea, 2016). These techniques and methods guide manager to

make the effective action plan to make effective management accounting plan and reporting.

D2 Interpretation of accurately applicable financial report for Putney Enterprise

Financial report helps to interpret the company data and helps to determine the actual

position of the company. This financial report helps company to compare with the competitors in

order to determine their position. This is very essential tool to take corrective action plan for the

next financial year to get more sales revenue by enhancing the company product and services.

Moreover, the main objective of the organisation is to get effective sales to get best output

returns.

TASK 3

P4 Explaining the advantages and disadvantages of planning tools used for budgetary control.

In this context is to be focus on advantages and disadvantages for future planing, which is

focus on budget control.

Incremental budgeting: In this context such kind of budgeting control method is to be focus on

earlier year execution is to be taken inferior and after that additive amount of money area unit

enclosed for the fresh disbursal year. In additive planning the asset appellation count on the

earliest long time (Grabner and Moers, 2013). This is help to little improvement in current

spending plan for future. On the other hand, actual year’s disbursal plan is interpreted as the

basal to get at the ready one time period from now fiscal plan and plus are allotted similarly. In

this way, such kind of plan is to be focus on incremental plan for future time period are as

follows:

Steady change: In this context is to be focus on as a year ago financial plan is to be taken and

this is exceeding dependable disbursal plan from unitary period to different. Additive

disbursement plan permit uninterrupted alteration in Putney Enterprise.

Preference:

Downrightness as in this last year's spending configuration is taken as the base so this is

essential and easy to understand as the bookkeeper unquestionably considers the most recent

9

year's cash related course of action. So this budgetary course of action is likewise simple to

emerge from others and most clear with put a little while later.

Zero base budgeting:

Zero based costing is the path toward arranging in which differing costs are legitimized

expected for all new period (Drake, Roulstone and Thornock, 2016). It is started from a Zero

based and all the limit inside an affiliation is destitute down with its needs and costs.

Central focuses:

For the most part help the firm available for use of cash related enunciation for the

expenses and moreover make open a projection of fitting resources for the execution that ought

to be competent.

Hindrances:

Expensive and complex Zero based costing has a lot of cost pool and as needs be can be

additional compound than normal thing.

Versatility each one of the movements can be seen doubtlessly and new approach in like manner

can be executed quickly. So incremental arranging is versatile to execute.

Avoid battle the issues and strife between the workplaces are constrained as there are a similar

spending gets ready for them. It is less difficult to keep each one of the divisions on a

comparative level to keep up a vital separation from conflicts among them.

Deterrents

No inspiring powers it doesn't offer labourers to be innovative so with no headway they don't get

the stimuli from organization.

Development based arranging

In this kind of arranging structure all the fiscal recompense is apportioned on the bases of

activities in the affiliation and Activity based costing is an accounting suggests which help

recognize the activities which a firm execute and assigns abnormal cost to things (Collier, 2015).

It sees the relationship among the costs, activities and things.

10

emerge from others and most clear with put a little while later.

Zero base budgeting:

Zero based costing is the path toward arranging in which differing costs are legitimized

expected for all new period (Drake, Roulstone and Thornock, 2016). It is started from a Zero

based and all the limit inside an affiliation is destitute down with its needs and costs.

Central focuses:

For the most part help the firm available for use of cash related enunciation for the

expenses and moreover make open a projection of fitting resources for the execution that ought

to be competent.

Hindrances:

Expensive and complex Zero based costing has a lot of cost pool and as needs be can be

additional compound than normal thing.

Versatility each one of the movements can be seen doubtlessly and new approach in like manner

can be executed quickly. So incremental arranging is versatile to execute.

Avoid battle the issues and strife between the workplaces are constrained as there are a similar

spending gets ready for them. It is less difficult to keep each one of the divisions on a

comparative level to keep up a vital separation from conflicts among them.

Deterrents

No inspiring powers it doesn't offer labourers to be innovative so with no headway they don't get

the stimuli from organization.

Development based arranging

In this kind of arranging structure all the fiscal recompense is apportioned on the bases of

activities in the affiliation and Activity based costing is an accounting suggests which help

recognize the activities which a firm execute and assigns abnormal cost to things (Collier, 2015).

It sees the relationship among the costs, activities and things.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.