Management Accounting and Business Strategies: Divine Denim Report

VerifiedAdded on 2022/09/26

|18

|2330

|23

Report

AI Summary

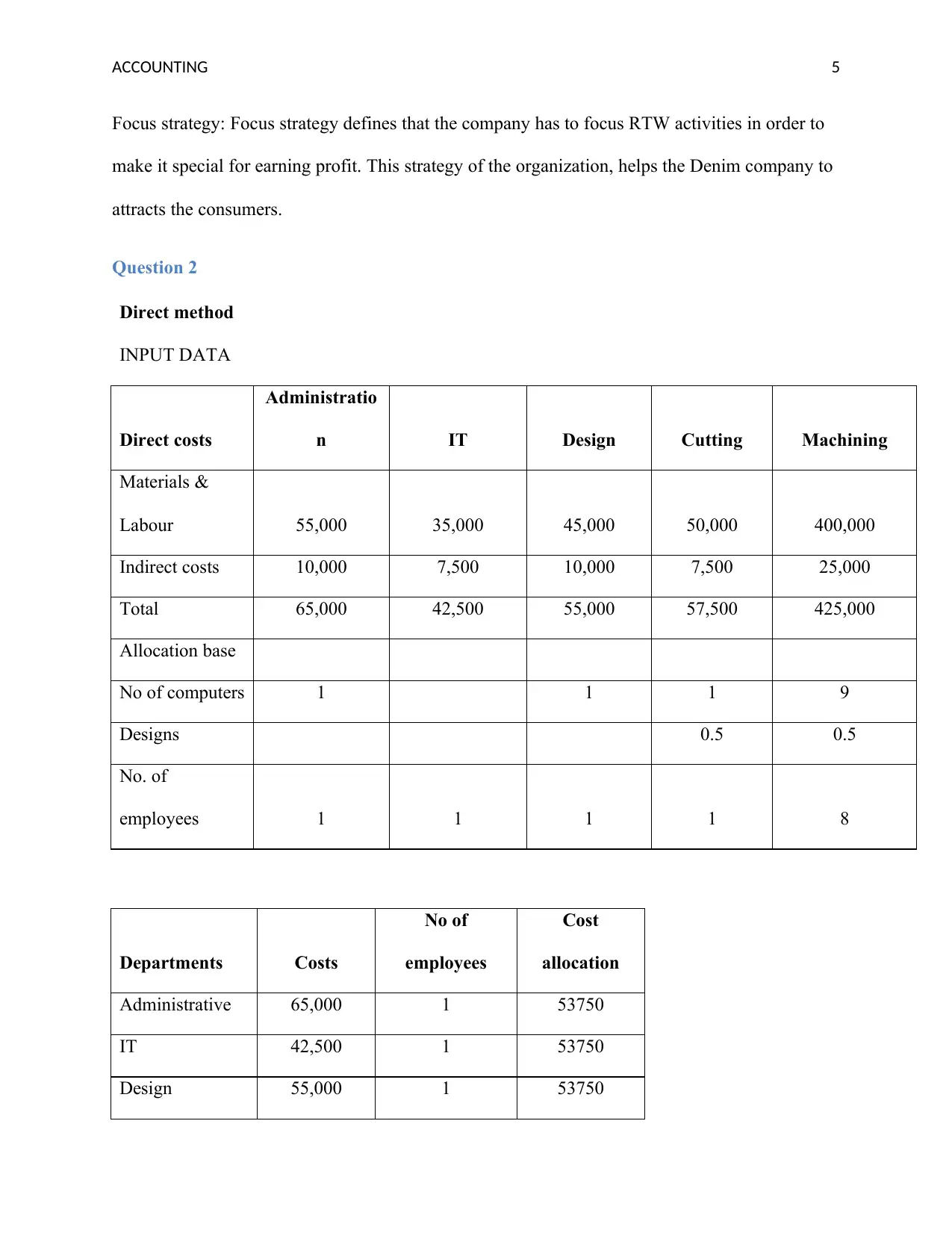

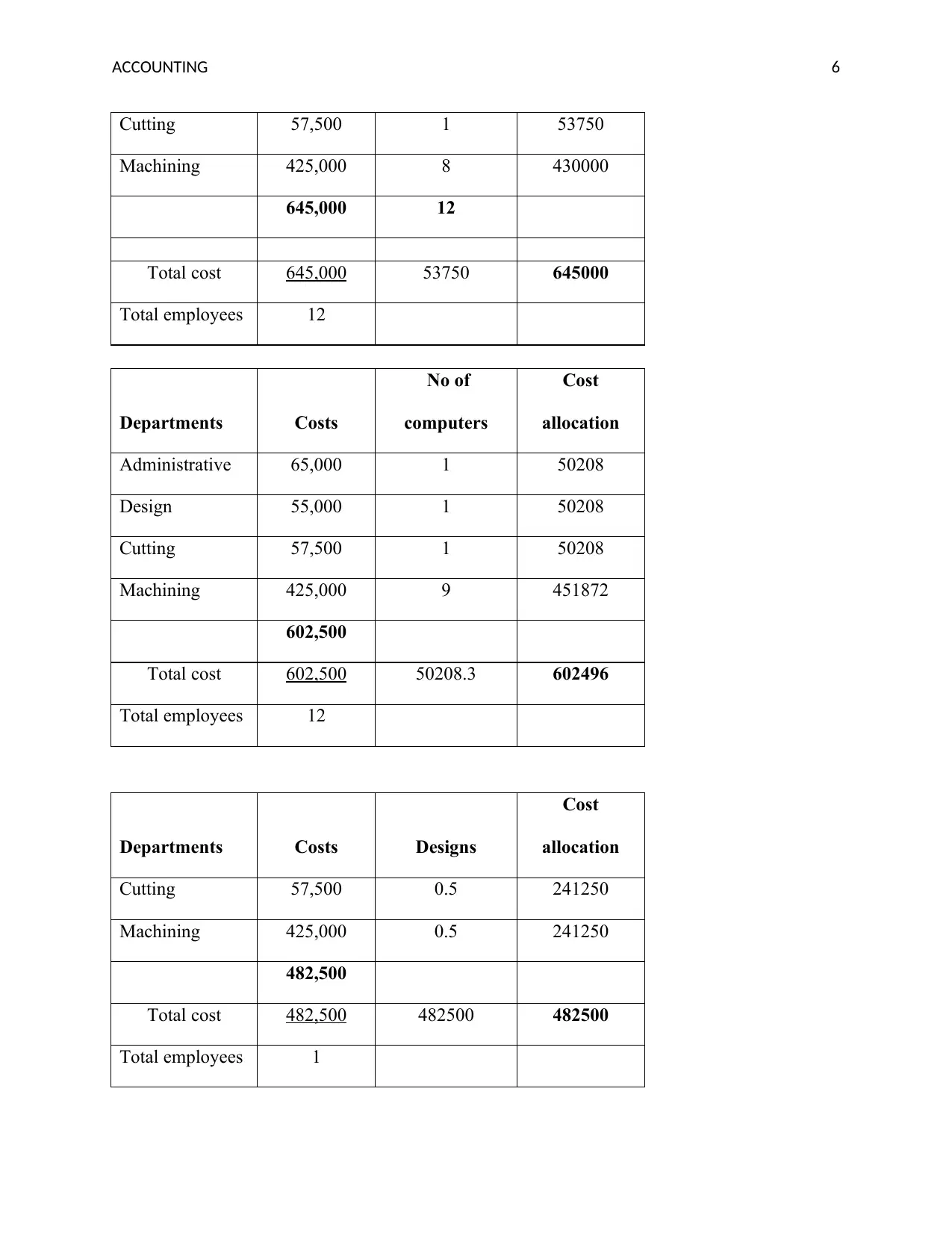

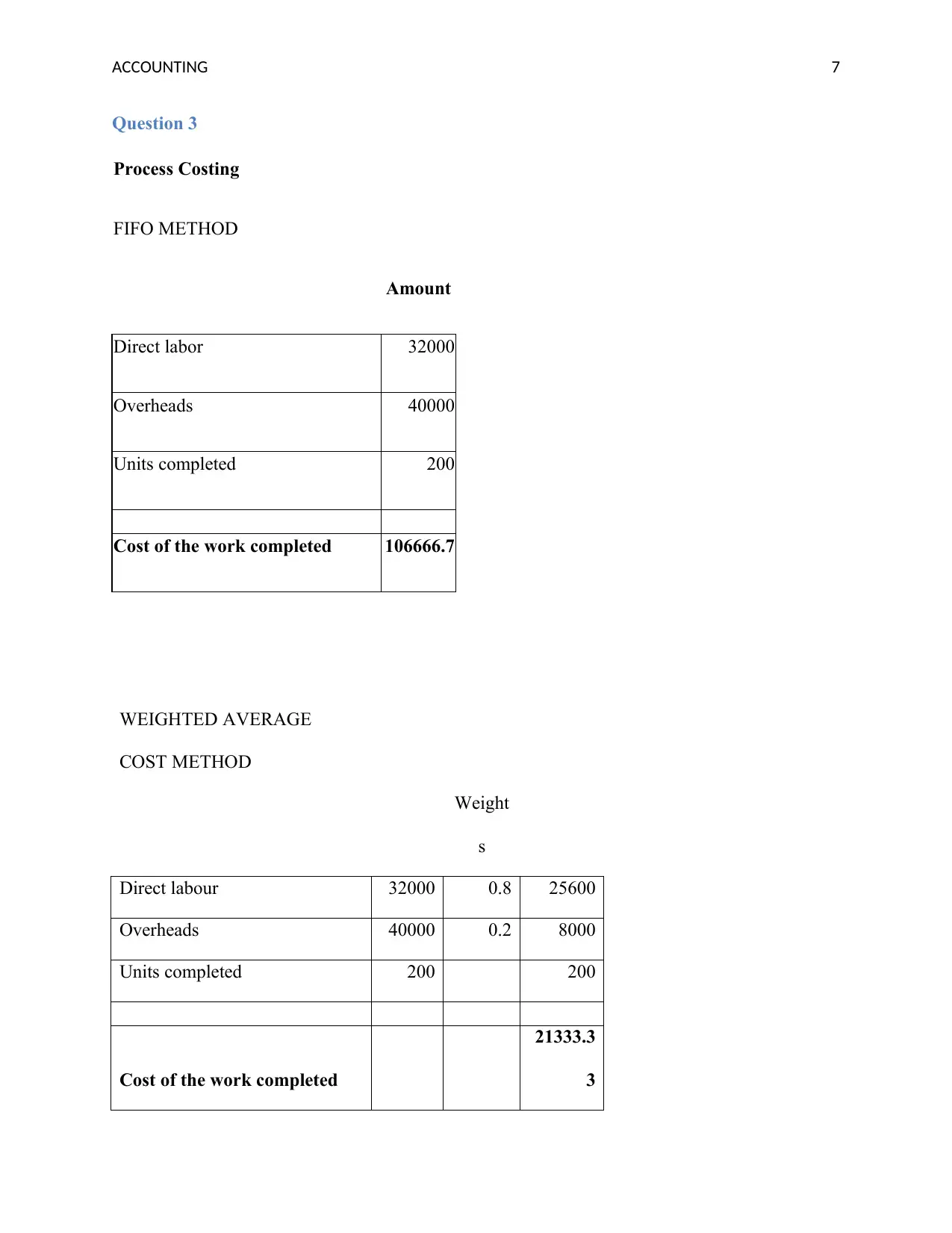

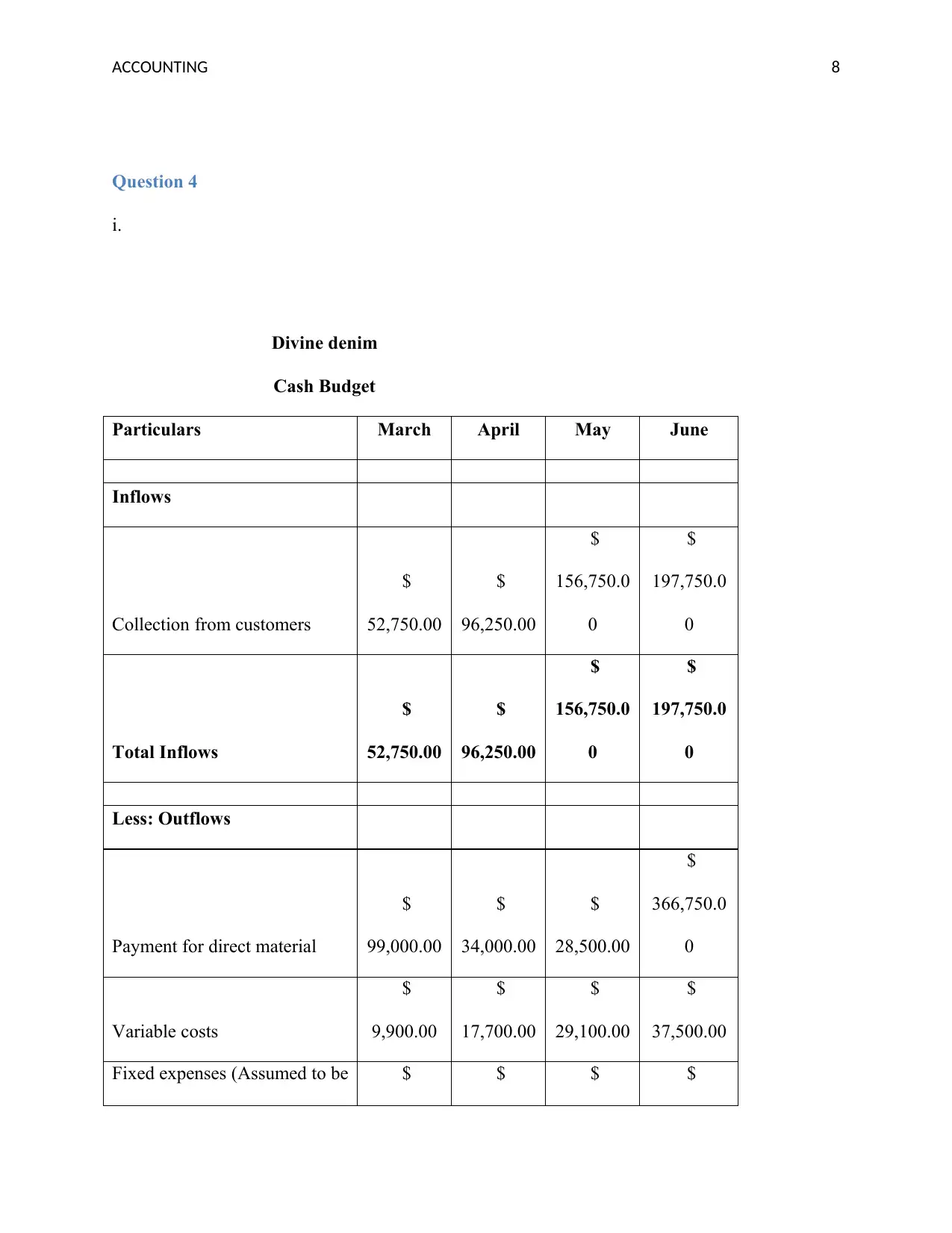

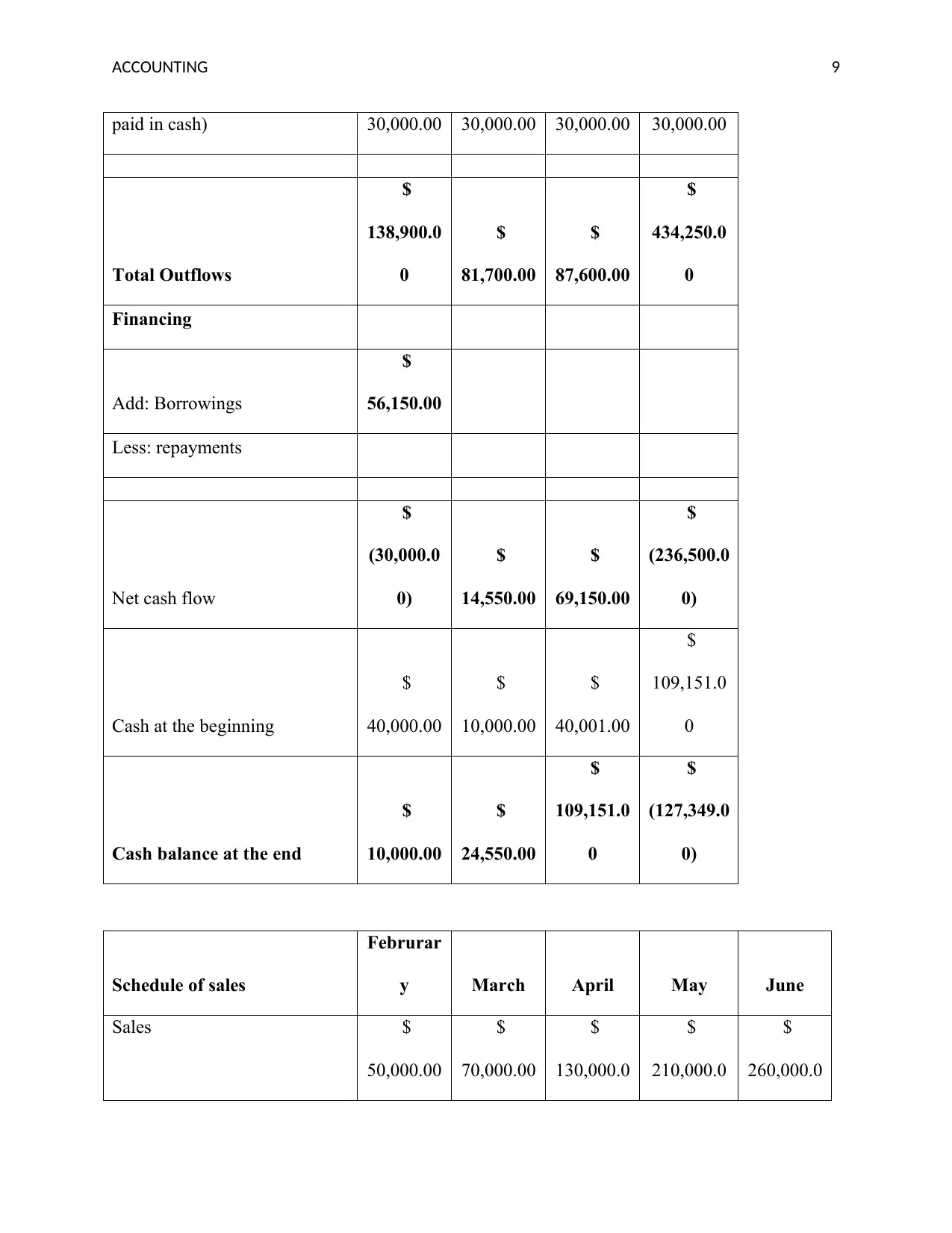

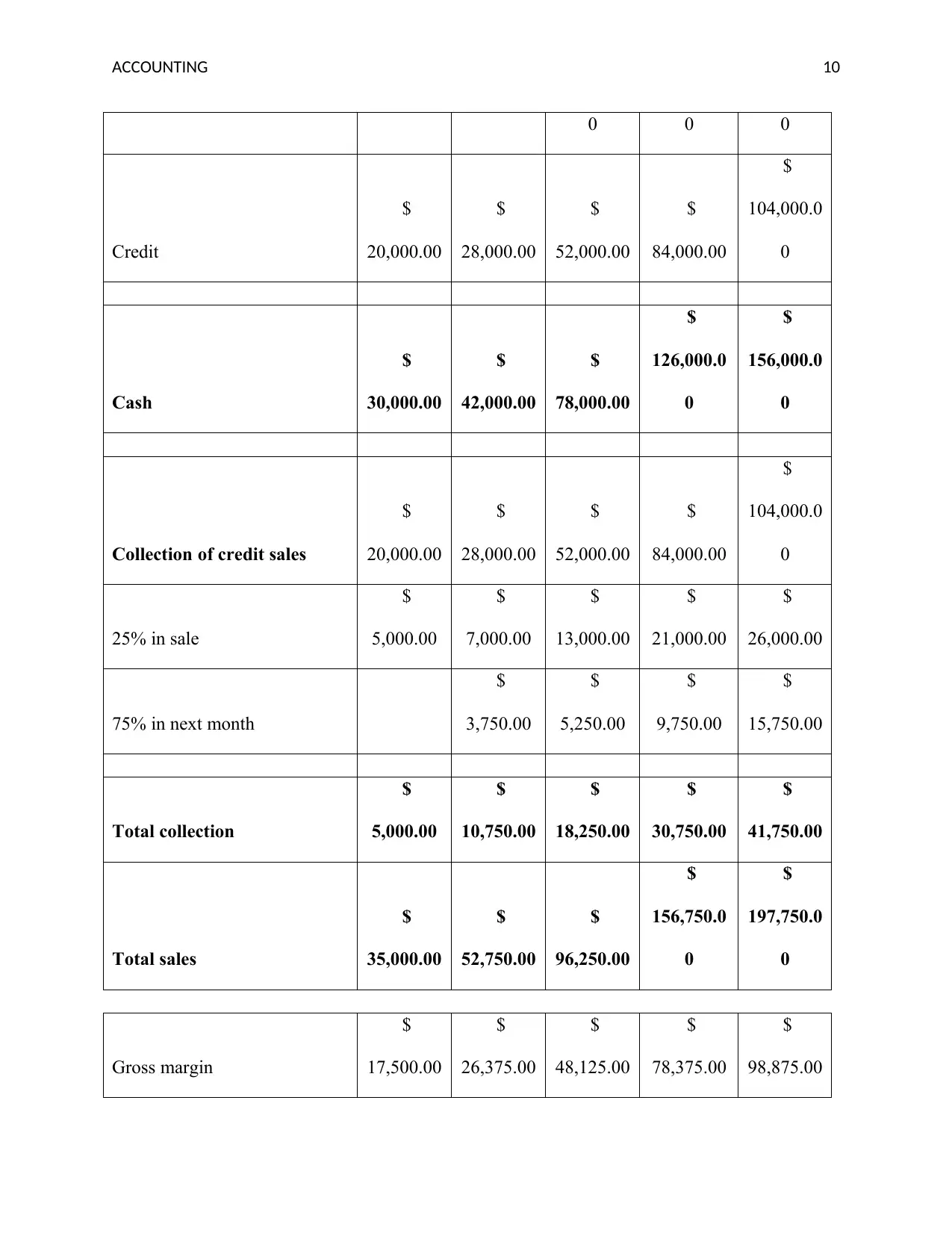

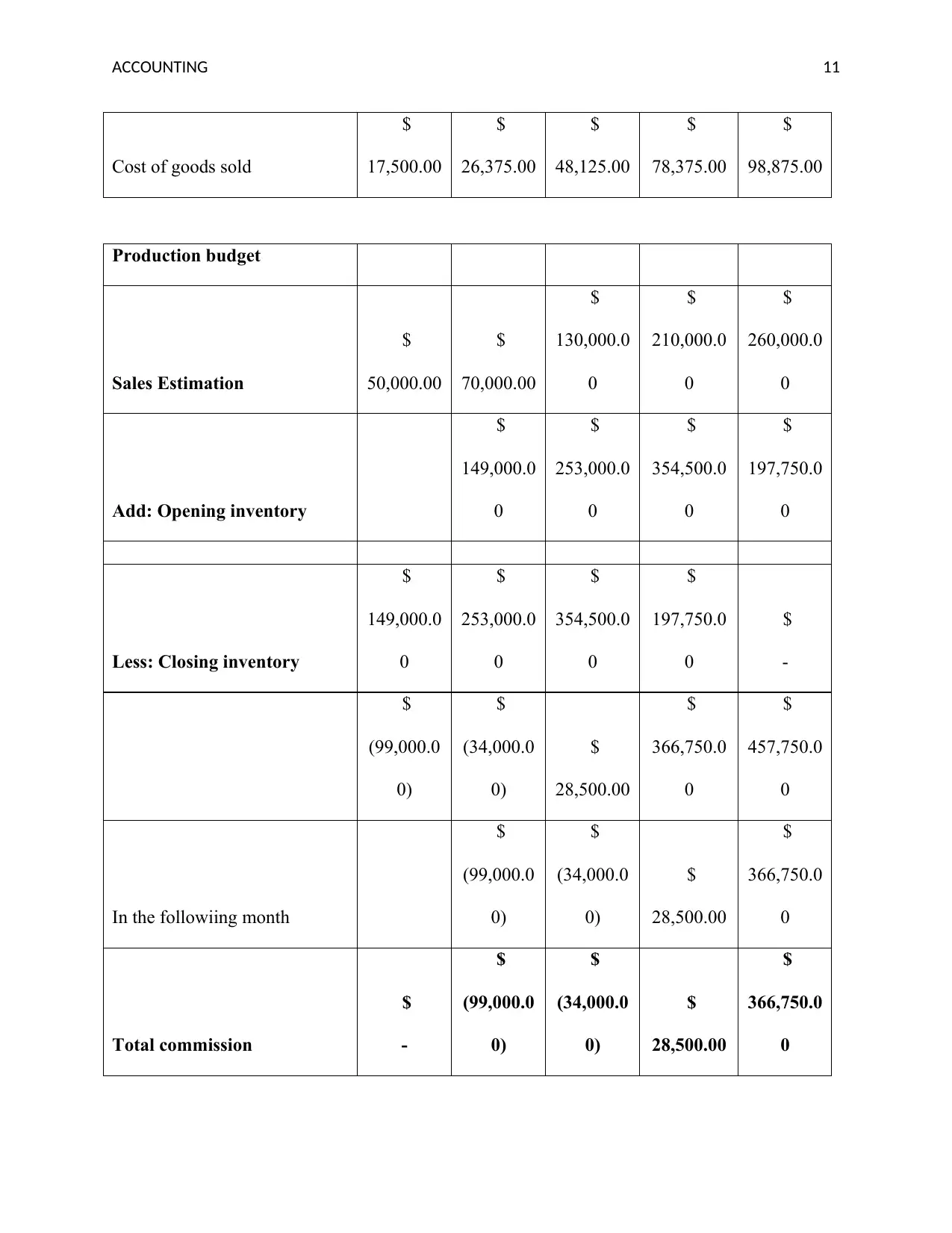

This report provides a comprehensive analysis of Divine Denim, a growing company specializing in designer denim jeans and jackets. The report begins with a business background, outlining the company's operations and expansion into Ready-to-Wear (RTW) clothing. It then applies Porter's Five Forces framework to assess the competitive environment, evaluating the threat of new entrants, bargaining power of buyers and suppliers, threat of competitors, and the threat of substitutes. The analysis highlights the impact of these forces on Divine Denim's business and examines how the company can use cost leadership, differentiation, and focus strategies to gain a competitive advantage. The report continues with a detailed examination of direct and indirect costs, allocation methods, process costing using FIFO and weighted average methods, and a cash budget. The cash budget includes inflows, outflows, and financing requirements, along with a schedule of sales and production budgets. Finally, the report connects the cost leadership strategy to the company's budgeting process, showing how it helps control expenses and increase sales.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.