Management Accounting Report: Systems, Budgeting, and Analysis (2020)

VerifiedAdded on 2023/01/11

|14

|4484

|32

Report

AI Summary

This report delves into the core principles of management accounting (MA), exploring its systems and techniques, and their significance in informed decision-making for business organizations. It highlights the benefits of MA systems, such as job costing, price optimization, and inventory management, and their impact on operational efficiency. The report further examines various MA reports, including inventory control, debtors analysis, break-even analysis, and master budget reports, detailing their importance in performance evaluation and financial planning. A cash budget for Lets Grow Ltd. for the next six months is presented, along with an analysis of its cash position, and planning tools for ensuring budgetary control are discussed. Finally, the report compares different approaches to adopting MA systems within organizations, concluding with a synthesis of key findings and recommendations.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

LO1..................................................................................................................................................3

Management accounting (MA) system and it benefits...............................................................3

Management accounting (MA) reports and its usefulness..........................................................6

LO2..................................................................................................................................................8

Cash budget for the next 6 months ending in August 2020........................................................8

LO3..................................................................................................................................................8

Planning tools for ensuring budgetary control............................................................................8

LO 4...............................................................................................................................................11

Compare the ways organization used to adopt MA system......................................................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................3

LO1..................................................................................................................................................3

Management accounting (MA) system and it benefits...............................................................3

Management accounting (MA) reports and its usefulness..........................................................6

LO2..................................................................................................................................................8

Cash budget for the next 6 months ending in August 2020........................................................8

LO3..................................................................................................................................................8

Planning tools for ensuring budgetary control............................................................................8

LO 4...............................................................................................................................................11

Compare the ways organization used to adopt MA system......................................................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting (MA) is mainly the process through which the business

organization identifies, measures and analyses the important accounting information for

effective and improved decision making. It is used by the internal team of management

for the purpose of taking crucial business decisions such as business expansion, for

which requires a complete analysis for before taking any decision as it affects the future

prospects of the business. This reports presents about the fundamental aspects of

management accounting, its systems and techniques which are useful for business

organizations. It also covers the various types of tools which can be used by the

business entity for facing various financial problems that may come across. Also, the

cash budget for the Lets Grow Ltd which will be helpful in determining it current cash

position.

LO1

Management accounting (MA) system and it benefits

MA is also known as managerial accounting which is the process used in

determining and analysing the costs and the business operation for the purpose of

preparing the relevant reports which are mainly used for the internal financial reporting

(Singhvi and BODHANWALA, 2018) . It also provides help to the management taking

effective decision with respect to strategic planning and implementation. In simple

terms, it is the process of transformation data into useful information to be used by

internal management team.

The management accounting system are the system which is deployed in an

organization which provides assistance in meeting the varied business needs. An

effective MA system will meet the needs of the business organization and it includes

budgeting, cost analysis, trend analysis etc.

Essential requirements of good MA system

Following are the few essential requirements of a good MA system.

Reliable: The data provided under MA system should be stable and consistent

with the data gathering process. The progress towards the performance should reveal

the actual changes instead of variation of the data gathering process and methods. The

Management accounting (MA) is mainly the process through which the business

organization identifies, measures and analyses the important accounting information for

effective and improved decision making. It is used by the internal team of management

for the purpose of taking crucial business decisions such as business expansion, for

which requires a complete analysis for before taking any decision as it affects the future

prospects of the business. This reports presents about the fundamental aspects of

management accounting, its systems and techniques which are useful for business

organizations. It also covers the various types of tools which can be used by the

business entity for facing various financial problems that may come across. Also, the

cash budget for the Lets Grow Ltd which will be helpful in determining it current cash

position.

LO1

Management accounting (MA) system and it benefits

MA is also known as managerial accounting which is the process used in

determining and analysing the costs and the business operation for the purpose of

preparing the relevant reports which are mainly used for the internal financial reporting

(Singhvi and BODHANWALA, 2018) . It also provides help to the management taking

effective decision with respect to strategic planning and implementation. In simple

terms, it is the process of transformation data into useful information to be used by

internal management team.

The management accounting system are the system which is deployed in an

organization which provides assistance in meeting the varied business needs. An

effective MA system will meet the needs of the business organization and it includes

budgeting, cost analysis, trend analysis etc.

Essential requirements of good MA system

Following are the few essential requirements of a good MA system.

Reliable: The data provided under MA system should be stable and consistent

with the data gathering process. The progress towards the performance should reveal

the actual changes instead of variation of the data gathering process and methods. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

data should be easily made available either through manually, automated or through

others systems and records.

Accurate: The data gathered under the MA system should be accurate should

be able to serve the intended use and should be gathered only once even if it is having

multiple usage. All the relevant data should be captured at the point of activity.

Timely: It is very essential to record all the relevant data in a timely manager and

as quickly as possible and should make available as and when it is required within the

required time frame (Wisna, 2018). The data should provide quickly and frequently for

meeting the business requirements for influencing the organizations decisions.

Relevant: The another crucial aspect to be considered while implementing the

MA system is that it should be relevant to the changing needs of the business. The data

which is being available should meet the purpose and requirement for which it is

gathered otherwise it will be of no use. A periodic review is required for the changing

needs.

Types of management accounting system

There are various forms of MA systems which is being utilized for the meeting

the various needs of the business. This need varies from one organization to another.

The various forms of MA system are stated below.

Job Costing system

It is mainly used for assigning and accumulating the costs in respect to the

production of the single unit of the product. It is mostly useful when the various items

are being produced which different from one another and each having a significant cost

(Weinman Jr, AT&T Intellectual Property II LP, 2019). This system requires a separate

job cost record of each of its items. It provides complete details about the direct material

and labour which is had been used in real and the amount assigned as the production

overheads.

Benefits:

It provides complete detail about the costs which is being used through the

process of production.

others systems and records.

Accurate: The data gathered under the MA system should be accurate should

be able to serve the intended use and should be gathered only once even if it is having

multiple usage. All the relevant data should be captured at the point of activity.

Timely: It is very essential to record all the relevant data in a timely manager and

as quickly as possible and should make available as and when it is required within the

required time frame (Wisna, 2018). The data should provide quickly and frequently for

meeting the business requirements for influencing the organizations decisions.

Relevant: The another crucial aspect to be considered while implementing the

MA system is that it should be relevant to the changing needs of the business. The data

which is being available should meet the purpose and requirement for which it is

gathered otherwise it will be of no use. A periodic review is required for the changing

needs.

Types of management accounting system

There are various forms of MA systems which is being utilized for the meeting

the various needs of the business. This need varies from one organization to another.

The various forms of MA system are stated below.

Job Costing system

It is mainly used for assigning and accumulating the costs in respect to the

production of the single unit of the product. It is mostly useful when the various items

are being produced which different from one another and each having a significant cost

(Weinman Jr, AT&T Intellectual Property II LP, 2019). This system requires a separate

job cost record of each of its items. It provides complete details about the direct material

and labour which is had been used in real and the amount assigned as the production

overheads.

Benefits:

It provides complete detail about the costs which is being used through the

process of production.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This system is also used in determining and measuring the profitability

associated with each job undertaken and also help in taking future decisions with

respect to whether to take the job next time or not. It also helps in avoiding the situation of duplication of work because it can be

used in estimating the cost of the similar job. The price of the job is dependent

upon the price of the previous job which is taken as a base.

Price Optimization system

It is the another form of MA system which is being used by the business

organization with the purpose of determining the price of the product. It is used for

finding out the sweet spot or in other words, the maximum price at which the customers

are willing to pay (Harsha, Subramanian and Ettl, 2019). The organizations up and

down their supply chain with the core objective of optimizing the price of their products

which can be useful in optimizing the price of the product which will help in selling the

product as quickly as possible at the right price for making a good amount of profit.

Benefits:

Price optimization assists the companies in focussing on the key areas like sales,

conversion rate and so forth. It helps in growth and expansion of the business.

This system has completely reduced the manual work and has also reduced the

possibility of any human errors. Also, the prediction which are done with it are

more precise and has huge influence over the business. It helps in regularizing the price of the product as per the changing market trends

and the willingness of the customers to pay.

Inventory Management System

It is the tool which is being used by the business organization with the objective

of tracking the movement of goods from one process to another across the entire supply

chain. It helps in optimizing the entire system from the time of placing the order and the

delivery of the same to the end customers (Henderson and et.al, 2018). It monitors the

complete journey of the material transforming into a product. It helps in ensuring that the

right amount of inventory is available at the right time.

Benefits:

associated with each job undertaken and also help in taking future decisions with

respect to whether to take the job next time or not. It also helps in avoiding the situation of duplication of work because it can be

used in estimating the cost of the similar job. The price of the job is dependent

upon the price of the previous job which is taken as a base.

Price Optimization system

It is the another form of MA system which is being used by the business

organization with the purpose of determining the price of the product. It is used for

finding out the sweet spot or in other words, the maximum price at which the customers

are willing to pay (Harsha, Subramanian and Ettl, 2019). The organizations up and

down their supply chain with the core objective of optimizing the price of their products

which can be useful in optimizing the price of the product which will help in selling the

product as quickly as possible at the right price for making a good amount of profit.

Benefits:

Price optimization assists the companies in focussing on the key areas like sales,

conversion rate and so forth. It helps in growth and expansion of the business.

This system has completely reduced the manual work and has also reduced the

possibility of any human errors. Also, the prediction which are done with it are

more precise and has huge influence over the business. It helps in regularizing the price of the product as per the changing market trends

and the willingness of the customers to pay.

Inventory Management System

It is the tool which is being used by the business organization with the objective

of tracking the movement of goods from one process to another across the entire supply

chain. It helps in optimizing the entire system from the time of placing the order and the

delivery of the same to the end customers (Henderson and et.al, 2018). It monitors the

complete journey of the material transforming into a product. It helps in ensuring that the

right amount of inventory is available at the right time.

Benefits:

This system helps in reducing the inaccuracies as most of the task is automated

which leads to reduction the human error.

It provides relevant reports which can be used by the organization in taking more

relevant and intelligent business decisions.

It helps in exercising control over the stock by ensuring that the company has not

over stocked the products or in the situation of out of stock. This results into cost

saving with respect to unnecessary management of overstocked inventory and

wastage and spoilage.

Management accounting (MA) reports and its usefulness

Management Accounting report

The MA reports generated by the various MA system helps Lets Grow Ltd in

monitoring and evaluating the performance of the business which can be prepared

frequently for a specific period (Ma and Gong, 2019). It is prepared as per the

requirement of the business each of it serving the various business needs. The various

types of MA reports are stated below which can be used by Lets Grow Ltd.

Inventory control report

This report is useful in determining the amount of inventory the company is

currently having in comparison to the inventory it requires for carrying its business

activities (Handojo and et.al, 2020). It provides details about raw material, work in

progress and the finished goods.

Importance

This report is useful in determining the level of inventory the company is having

based on which the reorder time of it is estimated. It used for ensuring that the business

never goes out of stock or is over stocked. Also, it is useful in mitigating the

unnecessary costs associated with managing the additional inventory.

Debtors analysis report

This report provides the complete details about the amount to be paid by the

customers for the goods purchased on credit (Date and Acts, 2016). It provides break

up of all the details with the due balance and the due date of each. It is also useful in

determining any bad debts in time.

Importance

which leads to reduction the human error.

It provides relevant reports which can be used by the organization in taking more

relevant and intelligent business decisions.

It helps in exercising control over the stock by ensuring that the company has not

over stocked the products or in the situation of out of stock. This results into cost

saving with respect to unnecessary management of overstocked inventory and

wastage and spoilage.

Management accounting (MA) reports and its usefulness

Management Accounting report

The MA reports generated by the various MA system helps Lets Grow Ltd in

monitoring and evaluating the performance of the business which can be prepared

frequently for a specific period (Ma and Gong, 2019). It is prepared as per the

requirement of the business each of it serving the various business needs. The various

types of MA reports are stated below which can be used by Lets Grow Ltd.

Inventory control report

This report is useful in determining the amount of inventory the company is

currently having in comparison to the inventory it requires for carrying its business

activities (Handojo and et.al, 2020). It provides details about raw material, work in

progress and the finished goods.

Importance

This report is useful in determining the level of inventory the company is having

based on which the reorder time of it is estimated. It used for ensuring that the business

never goes out of stock or is over stocked. Also, it is useful in mitigating the

unnecessary costs associated with managing the additional inventory.

Debtors analysis report

This report provides the complete details about the amount to be paid by the

customers for the goods purchased on credit (Date and Acts, 2016). It provides break

up of all the details with the due balance and the due date of each. It is also useful in

determining any bad debts in time.

Importance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Preparing this report will help the organization in carrying out the effective

planning process with respect to collecting the due amount on time. It will be useful in

analysing the present and the future cash flow position of the business and also based

on it the relevant decisions related to credit policy can be taken.

Break even analysis report

It is a very important report which is being prepared by the businesses with the

objective of knowing the point at which the business will be in no profit no loss situation

(Rizki and Sukoco, 2019). It helps in determining the amount of sales at which the

company would be able to achieve maximum profits. Break even analysis is also useful

in determining the price of the product in order to achieve the desired profits.

Importance

This report is basically useful for the business organization which are looking for

expansing their business or introducing the new product in the market and its impact

over the profits of the organization. More importantly, this report is useful in establishing

the relationship with change in profits with respect to change in price of the product in

the long run. A bifurcation of costs is done into fixed and the variable cost which helps in

determining the impact of each these costs on the profits.

Master budget report

The master budget report is the compilation of all the lower budgets which states

about the functional areas of the organization and it also includes the forecasted

financial statements, cash budget and a complete financial plan (Bužinskienė, 2019).

This report is being used by the management for directing the business activities.

Importance

This budget provides an assistance to the organization taking relevant business

decisions based on the information gathered on various aspects and departments of the

organization. It assists in meeting the long and short term outcome of the business. It

also helps in meeting the financial requirements of the business in order to enhance its

position.

The MA system and reporting is very important for the business organization

since the MA report provides information on different business requirements whereas

planning process with respect to collecting the due amount on time. It will be useful in

analysing the present and the future cash flow position of the business and also based

on it the relevant decisions related to credit policy can be taken.

Break even analysis report

It is a very important report which is being prepared by the businesses with the

objective of knowing the point at which the business will be in no profit no loss situation

(Rizki and Sukoco, 2019). It helps in determining the amount of sales at which the

company would be able to achieve maximum profits. Break even analysis is also useful

in determining the price of the product in order to achieve the desired profits.

Importance

This report is basically useful for the business organization which are looking for

expansing their business or introducing the new product in the market and its impact

over the profits of the organization. More importantly, this report is useful in establishing

the relationship with change in profits with respect to change in price of the product in

the long run. A bifurcation of costs is done into fixed and the variable cost which helps in

determining the impact of each these costs on the profits.

Master budget report

The master budget report is the compilation of all the lower budgets which states

about the functional areas of the organization and it also includes the forecasted

financial statements, cash budget and a complete financial plan (Bužinskienė, 2019).

This report is being used by the management for directing the business activities.

Importance

This budget provides an assistance to the organization taking relevant business

decisions based on the information gathered on various aspects and departments of the

organization. It assists in meeting the long and short term outcome of the business. It

also helps in meeting the financial requirements of the business in order to enhance its

position.

The MA system and reporting is very important for the business organization

since the MA report provides information on different business requirements whereas

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the MA system is mainly used to provide the qualitative information to the business. The

integration of the two results in effective managerial decision making process.

LO2

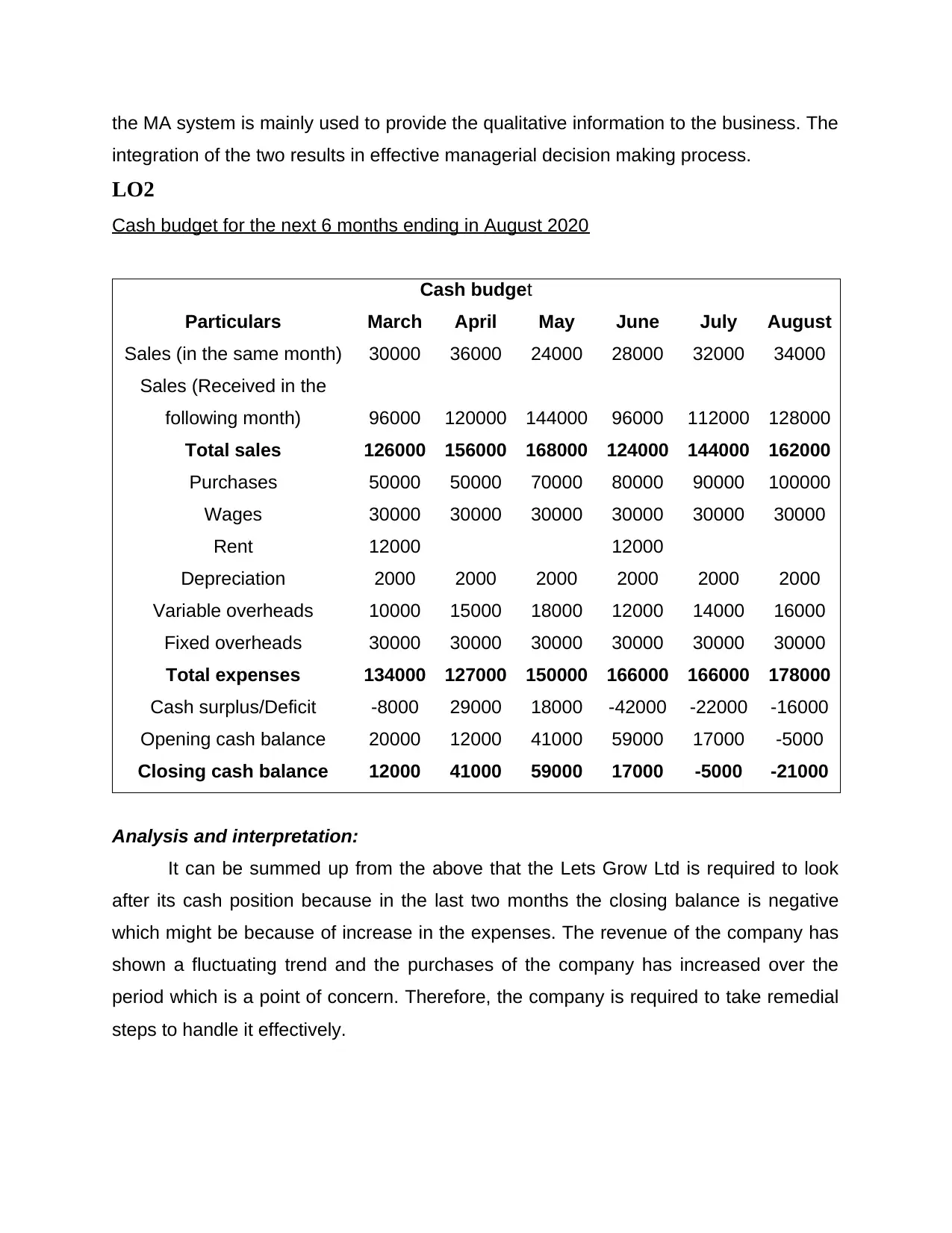

Cash budget for the next 6 months ending in August 2020

Cash budget

Particulars March April May June July August

Sales (in the same month) 30000 36000 24000 28000 32000 34000

Sales (Received in the

following month) 96000 120000 144000 96000 112000 128000

Total sales 126000 156000 168000 124000 144000 162000

Purchases 50000 50000 70000 80000 90000 100000

Wages 30000 30000 30000 30000 30000 30000

Rent 12000 12000

Depreciation 2000 2000 2000 2000 2000 2000

Variable overheads 10000 15000 18000 12000 14000 16000

Fixed overheads 30000 30000 30000 30000 30000 30000

Total expenses 134000 127000 150000 166000 166000 178000

Cash surplus/Deficit -8000 29000 18000 -42000 -22000 -16000

Opening cash balance 20000 12000 41000 59000 17000 -5000

Closing cash balance 12000 41000 59000 17000 -5000 -21000

Analysis and interpretation:

It can be summed up from the above that the Lets Grow Ltd is required to look

after its cash position because in the last two months the closing balance is negative

which might be because of increase in the expenses. The revenue of the company has

shown a fluctuating trend and the purchases of the company has increased over the

period which is a point of concern. Therefore, the company is required to take remedial

steps to handle it effectively.

integration of the two results in effective managerial decision making process.

LO2

Cash budget for the next 6 months ending in August 2020

Cash budget

Particulars March April May June July August

Sales (in the same month) 30000 36000 24000 28000 32000 34000

Sales (Received in the

following month) 96000 120000 144000 96000 112000 128000

Total sales 126000 156000 168000 124000 144000 162000

Purchases 50000 50000 70000 80000 90000 100000

Wages 30000 30000 30000 30000 30000 30000

Rent 12000 12000

Depreciation 2000 2000 2000 2000 2000 2000

Variable overheads 10000 15000 18000 12000 14000 16000

Fixed overheads 30000 30000 30000 30000 30000 30000

Total expenses 134000 127000 150000 166000 166000 178000

Cash surplus/Deficit -8000 29000 18000 -42000 -22000 -16000

Opening cash balance 20000 12000 41000 59000 17000 -5000

Closing cash balance 12000 41000 59000 17000 -5000 -21000

Analysis and interpretation:

It can be summed up from the above that the Lets Grow Ltd is required to look

after its cash position because in the last two months the closing balance is negative

which might be because of increase in the expenses. The revenue of the company has

shown a fluctuating trend and the purchases of the company has increased over the

period which is a point of concern. Therefore, the company is required to take remedial

steps to handle it effectively.

LO3

Planning tools for ensuring budgetary control

The various tools that can be used by Lets Grow Ltd for the purpose of

implementing the budgetary control are described below.

Cash budget

The cash budget is prepared with the aim of determining and evaluating the

various sources of funds along with the application of the same (DeFranco and

Schmidgall, 2017). It used in identifying and analysing the amount of cash the business

is currently having and the future prospects in respect to determining whether the

business is having enough cash to meet its daily cash requirements. Based on this

budget other budgets are prepared as everything is dependent upon cash.

Advantages:

The cash budget will help Lets Grow Ltd in putting focus in the important areas

with respect to cost incurred so that corrective actions can be taken in order to

manage it effectively and avoid the unnecessary expenditure.

It helps in determining the deficit in the budget so that business can make

strategies according to it for increasing the cash balance.

The cash budget depicts the actual liquidity position of the business in respect to

the cash availability. It can be easily understood by anyone has an interest in the budget.

Disadvantages:

The cash budget puts the restriction over the spending of the organization and

this may lead to distortion as changes can be made as per the requirement.

It cannot be considered equivalent to the profits of the organization.

It also takes into account the many unreliable sources through which either cash

inflow and cash outflow, for instance, sales of fixed assets, amount of security

deposit received, legal expenses etc. which are not recurring in nature and this

leads to inaccurate budget. There are chances of altering the cash budget by making huge payment in the

year ending which could have been made earlier causes inaccurate outcome.

Capital budget

Planning tools for ensuring budgetary control

The various tools that can be used by Lets Grow Ltd for the purpose of

implementing the budgetary control are described below.

Cash budget

The cash budget is prepared with the aim of determining and evaluating the

various sources of funds along with the application of the same (DeFranco and

Schmidgall, 2017). It used in identifying and analysing the amount of cash the business

is currently having and the future prospects in respect to determining whether the

business is having enough cash to meet its daily cash requirements. Based on this

budget other budgets are prepared as everything is dependent upon cash.

Advantages:

The cash budget will help Lets Grow Ltd in putting focus in the important areas

with respect to cost incurred so that corrective actions can be taken in order to

manage it effectively and avoid the unnecessary expenditure.

It helps in determining the deficit in the budget so that business can make

strategies according to it for increasing the cash balance.

The cash budget depicts the actual liquidity position of the business in respect to

the cash availability. It can be easily understood by anyone has an interest in the budget.

Disadvantages:

The cash budget puts the restriction over the spending of the organization and

this may lead to distortion as changes can be made as per the requirement.

It cannot be considered equivalent to the profits of the organization.

It also takes into account the many unreliable sources through which either cash

inflow and cash outflow, for instance, sales of fixed assets, amount of security

deposit received, legal expenses etc. which are not recurring in nature and this

leads to inaccurate budget. There are chances of altering the cash budget by making huge payment in the

year ending which could have been made earlier causes inaccurate outcome.

Capital budget

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The capital budget is the statement which provides information about the

estimated capital receipts and expenditures of the business entity. It provides details

about the organizations plan for acquiring or making investment in the capital assets for

the long term perspective (Vlachý, 2020). On the other hand, receipt refers to the

amount which has been received from the public or in the form of borrowings from the

government.

Advantages:

It is completely based on the long term and future opportunities of the business.

The capital budget provides the complete and the exact figures and therefore,

the capital expenditure is required to be incurred within the set limit. Each item is entered into budget after carrying out the proper evaluation and

analysis of it which helps in meeting accuracy.

Disadvantages:

This budget is static nature, therefore, changes cannot be made in between.

Even a minor error in depicting the capital expenditure might cause a huge loss

for the company as it mainly involves huge amount.

It cannot be used for the short term business requirements.

Flexible budget

This budget is also known as variable budget as it provides complete financial

plan in respect to the revenue and expenditure of the business which is based upon the

actual business outcomes (Maher, Fakhar and Karimi, 2018). Taking actual production,

it determines and estimates how the revenue and expenditure will change when there is

a change in the level of output, because of this reason it called variable budget.

Advantages:

It can be prepared for multiple level of activity unlike static budget which prepares

for only one level only.

This can be used in effectively comparing the actual output with the budgeted

output and cost with the set standards. This tool is useful in exercising cost control as it reacts to the changing situations.

Disadvantages:

estimated capital receipts and expenditures of the business entity. It provides details

about the organizations plan for acquiring or making investment in the capital assets for

the long term perspective (Vlachý, 2020). On the other hand, receipt refers to the

amount which has been received from the public or in the form of borrowings from the

government.

Advantages:

It is completely based on the long term and future opportunities of the business.

The capital budget provides the complete and the exact figures and therefore,

the capital expenditure is required to be incurred within the set limit. Each item is entered into budget after carrying out the proper evaluation and

analysis of it which helps in meeting accuracy.

Disadvantages:

This budget is static nature, therefore, changes cannot be made in between.

Even a minor error in depicting the capital expenditure might cause a huge loss

for the company as it mainly involves huge amount.

It cannot be used for the short term business requirements.

Flexible budget

This budget is also known as variable budget as it provides complete financial

plan in respect to the revenue and expenditure of the business which is based upon the

actual business outcomes (Maher, Fakhar and Karimi, 2018). Taking actual production,

it determines and estimates how the revenue and expenditure will change when there is

a change in the level of output, because of this reason it called variable budget.

Advantages:

It can be prepared for multiple level of activity unlike static budget which prepares

for only one level only.

This can be used in effectively comparing the actual output with the budgeted

output and cost with the set standards. This tool is useful in exercising cost control as it reacts to the changing situations.

Disadvantages:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It might show variation in the result and also does not provide details about the

causes of such variance.

There are situations when it shows unfavourable budget which has negative

influence over the investors and the consumers.

This budget requires highly skilled personnel which are lacking in the industry

because of which it is difficult for the companies in utilizing it.

LO 4

Compare the ways organization used to adopt MA system

Financial problems

Financial problem refers to inadequate cash flows in the business, where

expenses are higher than the income of company. Business is not having enough

resources to make payments to the suppliers and creditors. It affects the growth of

business and its working. Lack of resources, delay in collections from the debtors and

such other issues are the financial problems that organisations face. Company runs in a

dynamic environment and is required to face the challenges effectively for achieving

growth and success. Companies use different tools like key performance indicators,

benchmarking and corporate governance for resolving these financial issues.

Balance scorecard – It is described as framework for implementing and

managing the strategy. The vision is linked the strategic objectives, targets, measures

and the initiatives. Balance score card are used for measuring the financial performance

and goals related with all parts in organisation. Lets grow ltd uses balance score card

for reviewing its performance in the specific period. The issue of inadequate cash flows

faced by the company is used for making effective utilisation of resources (Syahdan,

Munawaroh and Akbar, 2018). Lets Grow made budgets for the specific departments

and activities of the organisation to keep them under control. The extent to which

company was able to achieve the targets was measured using the balance score cards

where the scores were given to different department. It helped the company to identify

the areas with lowest scores and made the management to focus over department to

reduce the variances.

Key Performance Indicators – It refers to the measurable value demonstrating

how effectively the company is achieving its business objectives. The KPI's are used at

causes of such variance.

There are situations when it shows unfavourable budget which has negative

influence over the investors and the consumers.

This budget requires highly skilled personnel which are lacking in the industry

because of which it is difficult for the companies in utilizing it.

LO 4

Compare the ways organization used to adopt MA system

Financial problems

Financial problem refers to inadequate cash flows in the business, where

expenses are higher than the income of company. Business is not having enough

resources to make payments to the suppliers and creditors. It affects the growth of

business and its working. Lack of resources, delay in collections from the debtors and

such other issues are the financial problems that organisations face. Company runs in a

dynamic environment and is required to face the challenges effectively for achieving

growth and success. Companies use different tools like key performance indicators,

benchmarking and corporate governance for resolving these financial issues.

Balance scorecard – It is described as framework for implementing and

managing the strategy. The vision is linked the strategic objectives, targets, measures

and the initiatives. Balance score card are used for measuring the financial performance

and goals related with all parts in organisation. Lets grow ltd uses balance score card

for reviewing its performance in the specific period. The issue of inadequate cash flows

faced by the company is used for making effective utilisation of resources (Syahdan,

Munawaroh and Akbar, 2018). Lets Grow made budgets for the specific departments

and activities of the organisation to keep them under control. The extent to which

company was able to achieve the targets was measured using the balance score cards

where the scores were given to different department. It helped the company to identify

the areas with lowest scores and made the management to focus over department to

reduce the variances.

Key Performance Indicators – It refers to the measurable value demonstrating

how effectively the company is achieving its business objectives. The KPI's are used at

different levels by organization for evaluating success in reaching targets. Lets Grow set

targets to be achieved in the specific period related with the sales, production and other

such like targets for achieving the success. Standards are set by the organization

related to the different targets that are to be achieved in specific time frame. At the end

of the period company identifies the distance from the set standards. Measures are

taken by the organization for reducing the areas that are affecting the organisations to

reach their objectives. It helps Lets grew in resolving the financial issues faced related

to different departments.

Corporate Governance – It refers to different rules, laws or processes through

which the business are regulated, operated or controlled. Term also encompasses

internal as well as external factors which are affecting interest of the stakeholders

including customers, suppliers, shareholders and management. All the strategies and

improvement steps are required to be monitored and controlled by organisation

(Yermack, 2017). Corporate governance involves establishing strong internal controls in

various processes where it could identify the wastage and other inefficiencies faced by

the departments. Lets grow has established new controls and processes for making the

management to identify the issues at initial stage so that adequate steps could be taken

immediately for reducing the errors and issues.

Benchmarking — It is the performance measuring tool which is used for

evaluating the performance of the business organization against the competitor within

the same industry. The competitor considered is to be best in the industry. This helps in

identifying the strength, weaknesses and opportunities of the business in comparison to

the competitors (Beyer, Löwe and Wendler, 2019). The comparison is based on the

processes, technology which is being used and what difference it is creating in the

organization. This assist the business entity in understanding its cost structure along

with the internal processes. It encourages team work and establishing proper

coordination. Thus, it helps in evaluating the weakness of the organization so the

remedial actions can be taken to reduce it.

Different organization adopt different types of MA system with the objective to

overcome the various financial problems it faces. There is a comparative analysis of the

two organization is given below.

targets to be achieved in the specific period related with the sales, production and other

such like targets for achieving the success. Standards are set by the organization

related to the different targets that are to be achieved in specific time frame. At the end

of the period company identifies the distance from the set standards. Measures are

taken by the organization for reducing the areas that are affecting the organisations to

reach their objectives. It helps Lets grew in resolving the financial issues faced related

to different departments.

Corporate Governance – It refers to different rules, laws or processes through

which the business are regulated, operated or controlled. Term also encompasses

internal as well as external factors which are affecting interest of the stakeholders

including customers, suppliers, shareholders and management. All the strategies and

improvement steps are required to be monitored and controlled by organisation

(Yermack, 2017). Corporate governance involves establishing strong internal controls in

various processes where it could identify the wastage and other inefficiencies faced by

the departments. Lets grow has established new controls and processes for making the

management to identify the issues at initial stage so that adequate steps could be taken

immediately for reducing the errors and issues.

Benchmarking — It is the performance measuring tool which is used for

evaluating the performance of the business organization against the competitor within

the same industry. The competitor considered is to be best in the industry. This helps in

identifying the strength, weaknesses and opportunities of the business in comparison to

the competitors (Beyer, Löwe and Wendler, 2019). The comparison is based on the

processes, technology which is being used and what difference it is creating in the

organization. This assist the business entity in understanding its cost structure along

with the internal processes. It encourages team work and establishing proper

coordination. Thus, it helps in evaluating the weakness of the organization so the

remedial actions can be taken to reduce it.

Different organization adopt different types of MA system with the objective to

overcome the various financial problems it faces. There is a comparative analysis of the

two organization is given below.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.