Management Accounting Report: Systems, Benefits, and Applications

VerifiedAdded on 2023/01/12

|14

|3454

|35

Report

AI Summary

This report on management accounting provides a comprehensive overview of the subject, focusing on the application of professional skills in preparing financial information for managerial decision-making. It examines management accounting systems, including inventory management, cost accounting, and price optimization, detailing their benefits and applications within a manufacturing concern, GSQ Limited. The report also covers management accounting reporting, such as inventory management reports, budgeting reports, performance reports, and cost reports, highlighting their role in effective business operations. Furthermore, it explores costing techniques like marginal costing and absorption costing, comparing their advantages and disadvantages. The report also delves into the integration of management accounting systems with reporting systems and how management accounting aids in resolving financial issues, offering insights into planning tools and their impact on organizational performance. The report concludes with detailed financial statements using both marginal and absorption costing methods.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

INTRODUTION..............................................................................................................................1

REPORT..........................................................................................................................................1

Management accounting systems with its benefits and applications...........................................1

Benefits and application of management accounting systems....................................................3

Management Accounting reporting.............................................................................................4

Integration of management accounting systems with the reporting systems of management

accounting....................................................................................................................................5

Management accounting costing techniques...............................................................................5

Different types of planning tools used by organisation with their advantages and

disadvantages...............................................................................................................................6

Management accounting adapted by companies in resolving financial issues............................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

TABLE OF CONTENTS................................................................................................................2

INTRODUTION..............................................................................................................................1

REPORT..........................................................................................................................................1

Management accounting systems with its benefits and applications...........................................1

Benefits and application of management accounting systems....................................................3

Management Accounting reporting.............................................................................................4

Integration of management accounting systems with the reporting systems of management

accounting....................................................................................................................................5

Management accounting costing techniques...............................................................................5

Different types of planning tools used by organisation with their advantages and

disadvantages...............................................................................................................................6

Management accounting adapted by companies in resolving financial issues............................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUTION

Management accounting can be defined as the method of gathering, analysing, interpreting

and preparation of financial reports used by the management in decision making. This is the

process involving use of financial information and the resources in decision making by th

managers. Management provides information and prepares report that is essential for the internal

users of the management. Present report is based on GSQ limited a manufacturing concern.

Report will cover management accounting systems, reports used in management accounting and

costing techniques used in management accounting. It will also cover the management

accounting costing techniques used for recording closing stock. It will also provide about the

planning tools used by MA and how MA systems help in solving the financial issues of an entity.

REPORT

Management accounting systems with its benefits and applications.

Management Accounting

Management accounting refers to the application of professional language & skills in

preparation of the accounting information in manner for assisting the management in formulation

of the policies as well as in planning and controlling the operation of undertaking. MA provides

information for the internal management of the company unlike the financial accounting that is

useful for external users of the company.

Management accounting systems

Management accounting systems are used by enterprise for effective management of the

operation of the organisations.

Inventory management system

Inventory management system refers to the system used by management for recording all

the transactions related to the inventory. Entity have different inventory such as capital assets,

raw materials, work in progress and the finished goods. Inventory system with the collaboration

of advance software has become very useful for the management in having proper record and

information of all the inventory of the enterprise (Turner and et.al., 2017). It keeps information

of all the inventory movements from raw material to finished goods.

Just-in-time – This is the inventory systems used by enterprise for having inventory on the spot

as and when required. This prevents company to overstock and save its storage costs,

1

Management accounting can be defined as the method of gathering, analysing, interpreting

and preparation of financial reports used by the management in decision making. This is the

process involving use of financial information and the resources in decision making by th

managers. Management provides information and prepares report that is essential for the internal

users of the management. Present report is based on GSQ limited a manufacturing concern.

Report will cover management accounting systems, reports used in management accounting and

costing techniques used in management accounting. It will also cover the management

accounting costing techniques used for recording closing stock. It will also provide about the

planning tools used by MA and how MA systems help in solving the financial issues of an entity.

REPORT

Management accounting systems with its benefits and applications.

Management Accounting

Management accounting refers to the application of professional language & skills in

preparation of the accounting information in manner for assisting the management in formulation

of the policies as well as in planning and controlling the operation of undertaking. MA provides

information for the internal management of the company unlike the financial accounting that is

useful for external users of the company.

Management accounting systems

Management accounting systems are used by enterprise for effective management of the

operation of the organisations.

Inventory management system

Inventory management system refers to the system used by management for recording all

the transactions related to the inventory. Entity have different inventory such as capital assets,

raw materials, work in progress and the finished goods. Inventory system with the collaboration

of advance software has become very useful for the management in having proper record and

information of all the inventory of the enterprise (Turner and et.al., 2017). It keeps information

of all the inventory movements from raw material to finished goods.

Just-in-time – This is the inventory systems used by enterprise for having inventory on the spot

as and when required. This prevents company to overstock and save its storage costs,

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Material requisition planning – In this method of inventory management company used to

analyse the requirements of inventory based in its previous trends and stores inventory

accordingly.

Cost accounting

Cost accounting is one of the most important management accounting systems used by

the enterprise for recording all the information related to the cost of products and services. Cost

accounting is used by the entity for calculating the cost of products or services. This is essential

for the business to assess the costing of every product for deciding its prices and the profit

margins. Cost accounting also involves comparison of the budgeted and actual figures to identify

the variances in the process. This helps company to take measures and steps for reducing the

variances and improving the performance of company. Cost accounting systems are very

essential for the business enterprise to control its costs.

Direct Costing

This is the method in which organisations only considers variable costs associated with

the products. This includes direct costs such as materials, labour and overheads. Fixed costs are

not considered in this costing method.

Standard costing

It refers costing in which standards are decided for every cost and process before the start

of production process. At the end of production process actual costs are compared with the

standard for identifying the variances.

Price Optimisation

Price Optimisation refers to the systems in which organisation decided the prices of their

product and services. It is a process which involves mathematical analysis and calculation. It

helps the organisation in identifying the demand of its product at different level of prices. There

is a direct impact of the prices on the demand of product (Bui and De Villiers, 2017).

Organisations using the price optimisation analyses the demand of its products and services and

decide the prices that are most optimum for product. They are decided after keeping in view the

objective of organisation.

Job Costing System

This is the process of management accounting that calculates the cost of each job

separately. In job costing system management identify the costs of producing every job related

2

analyse the requirements of inventory based in its previous trends and stores inventory

accordingly.

Cost accounting

Cost accounting is one of the most important management accounting systems used by

the enterprise for recording all the information related to the cost of products and services. Cost

accounting is used by the entity for calculating the cost of products or services. This is essential

for the business to assess the costing of every product for deciding its prices and the profit

margins. Cost accounting also involves comparison of the budgeted and actual figures to identify

the variances in the process. This helps company to take measures and steps for reducing the

variances and improving the performance of company. Cost accounting systems are very

essential for the business enterprise to control its costs.

Direct Costing

This is the method in which organisations only considers variable costs associated with

the products. This includes direct costs such as materials, labour and overheads. Fixed costs are

not considered in this costing method.

Standard costing

It refers costing in which standards are decided for every cost and process before the start

of production process. At the end of production process actual costs are compared with the

standard for identifying the variances.

Price Optimisation

Price Optimisation refers to the systems in which organisation decided the prices of their

product and services. It is a process which involves mathematical analysis and calculation. It

helps the organisation in identifying the demand of its product at different level of prices. There

is a direct impact of the prices on the demand of product (Bui and De Villiers, 2017).

Organisations using the price optimisation analyses the demand of its products and services and

decide the prices that are most optimum for product. They are decided after keeping in view the

objective of organisation.

Job Costing System

This is the process of management accounting that calculates the cost of each job

separately. In job costing system management identify the costs of producing every job related

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

with the product. This system is not concerned with the process but with each job. It considers

information related to raw materials, labour and other overheads. This is used by enterprises

having different process to manufacture a product.

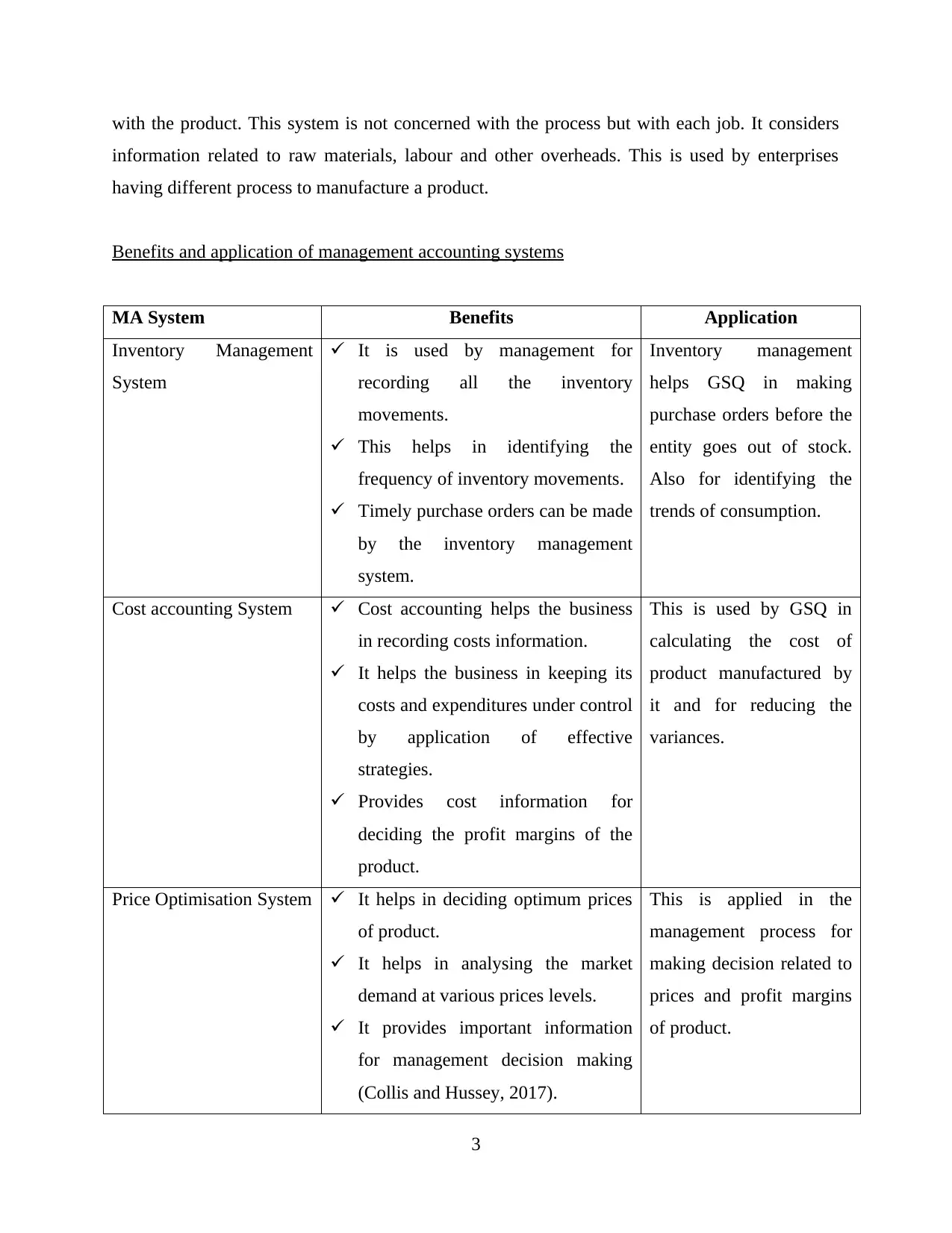

Benefits and application of management accounting systems

MA System Benefits Application

Inventory Management

System

It is used by management for

recording all the inventory

movements.

This helps in identifying the

frequency of inventory movements.

Timely purchase orders can be made

by the inventory management

system.

Inventory management

helps GSQ in making

purchase orders before the

entity goes out of stock.

Also for identifying the

trends of consumption.

Cost accounting System Cost accounting helps the business

in recording costs information.

It helps the business in keeping its

costs and expenditures under control

by application of effective

strategies.

Provides cost information for

deciding the profit margins of the

product.

This is used by GSQ in

calculating the cost of

product manufactured by

it and for reducing the

variances.

Price Optimisation System It helps in deciding optimum prices

of product.

It helps in analysing the market

demand at various prices levels.

It provides important information

for management decision making

(Collis and Hussey, 2017).

This is applied in the

management process for

making decision related to

prices and profit margins

of product.

3

information related to raw materials, labour and other overheads. This is used by enterprises

having different process to manufacture a product.

Benefits and application of management accounting systems

MA System Benefits Application

Inventory Management

System

It is used by management for

recording all the inventory

movements.

This helps in identifying the

frequency of inventory movements.

Timely purchase orders can be made

by the inventory management

system.

Inventory management

helps GSQ in making

purchase orders before the

entity goes out of stock.

Also for identifying the

trends of consumption.

Cost accounting System Cost accounting helps the business

in recording costs information.

It helps the business in keeping its

costs and expenditures under control

by application of effective

strategies.

Provides cost information for

deciding the profit margins of the

product.

This is used by GSQ in

calculating the cost of

product manufactured by

it and for reducing the

variances.

Price Optimisation System It helps in deciding optimum prices

of product.

It helps in analysing the market

demand at various prices levels.

It provides important information

for management decision making

(Collis and Hussey, 2017).

This is applied in the

management process for

making decision related to

prices and profit margins

of product.

3

Job Costing System It helps business to identify cost of

each job.

It provides detailed cost information

for deciding the profit margins.

This is applied by GSQ in

specific orders related to

the product for giving

costing information to the

consumers.

Management Accounting reporting.

Reporting is an important part for effective management of the business operations.

There are various management reports that helps the business to make decisions.

Inventory management reports

This report is prepared by the management for having the information related to the

inventory. It consists of information related to inventory purchased, consumed and output

produced. This provides the company information to make decisions related to the purchases as

well as to take promotions for the product. It contains trends of inventory movements of raw

materials and finished goods for placing the purchase orders after analysing the movements. The

report is based on information provided by the inventory management system. It enables the

company in preventing its storage cost by making orders on the basis of requirement.

Budgeting Report

Budgeting report is prepared by the organisation for planning the business operations.

Budget could be defined as the report that is prepared on the forecasts made over the incomes

and expenditures of company. Budgets are prepared over by the business based on it previous

budgets. Managers make adjustment related to the inflations, market condition, consumer

behaviour etc for preparing budgets for current year. Budget report helps the business enterprise

in keeping its expenditures. This provides the departments with specified resources on the

budgets prepared. They help the business in making effective allocation of the resources among

the various department and keeping the expenses under control.

Performance report

Performance report contains the information related to the performance of organisation

during the specific period. It gives the company essential information related to the performance

of various department, products and services. This helps the company in identifying the

productive operations of enterprise. Performance report helps the business enterprise in

4

each job.

It provides detailed cost information

for deciding the profit margins.

This is applied by GSQ in

specific orders related to

the product for giving

costing information to the

consumers.

Management Accounting reporting.

Reporting is an important part for effective management of the business operations.

There are various management reports that helps the business to make decisions.

Inventory management reports

This report is prepared by the management for having the information related to the

inventory. It consists of information related to inventory purchased, consumed and output

produced. This provides the company information to make decisions related to the purchases as

well as to take promotions for the product. It contains trends of inventory movements of raw

materials and finished goods for placing the purchase orders after analysing the movements. The

report is based on information provided by the inventory management system. It enables the

company in preventing its storage cost by making orders on the basis of requirement.

Budgeting Report

Budgeting report is prepared by the organisation for planning the business operations.

Budget could be defined as the report that is prepared on the forecasts made over the incomes

and expenditures of company. Budgets are prepared over by the business based on it previous

budgets. Managers make adjustment related to the inflations, market condition, consumer

behaviour etc for preparing budgets for current year. Budget report helps the business enterprise

in keeping its expenditures. This provides the departments with specified resources on the

budgets prepared. They help the business in making effective allocation of the resources among

the various department and keeping the expenses under control.

Performance report

Performance report contains the information related to the performance of organisation

during the specific period. It gives the company essential information related to the performance

of various department, products and services. This helps the company in identifying the

productive operations of enterprise. Performance report helps the business enterprise in

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

identifying the ability of company in achieving its targeted objectives. Management based on the

performance report makes effective improvement strategies for increasing the productivity and

efficiency of the process. It is also essential for rewarding and providing incentives to the

employees who are performing well in enterprise.

Cost Reports

Cost report contains all the information related to the cost associated with the product in

detailed manner. It provides information related to the variable costs and fixed costs in producing

a product. Cost report are important for managers in decisions making related to the cost of

product, and deciding the prices after appropriate profit margins (Chiwamit, Modell and

Scapens, 2017). Cost reports also provide the management in carrying out the cost analysis and

setting standard for each new period. After the end of period standard cost are compared within

the actual costs. Variances are identified by the management and on the basis of this corrective

measures are taken. This helps the business in reducing the cost by implementing cost efficient

strategies in the business.

Integration of management accounting systems with the reporting systems of management

accounting.

Management accounting is a broad concept consisting of various tools and techniques for

effective management of the enterprise. MA accounting systems are the system with the use of

which managers keep proper record of all the transaction and events related to the different

activities and operation. On the other MA accounting reports are prepared by the organisation for

having complete information related to the outcomes of the management systems. Management

accounting systems and reporting together helps the management to maintain effective control

over its operations. For example the cost accounting systems provide the information related to

the actual costs incurred in the production process and cost report provide information related to

the variances incurred between actual and standards cost. This enables the company to identify

areas of improvements and to take corrective steps for increasing productivity.

Management accounting costing techniques

Marginal Costing

5

performance report makes effective improvement strategies for increasing the productivity and

efficiency of the process. It is also essential for rewarding and providing incentives to the

employees who are performing well in enterprise.

Cost Reports

Cost report contains all the information related to the cost associated with the product in

detailed manner. It provides information related to the variable costs and fixed costs in producing

a product. Cost report are important for managers in decisions making related to the cost of

product, and deciding the prices after appropriate profit margins (Chiwamit, Modell and

Scapens, 2017). Cost reports also provide the management in carrying out the cost analysis and

setting standard for each new period. After the end of period standard cost are compared within

the actual costs. Variances are identified by the management and on the basis of this corrective

measures are taken. This helps the business in reducing the cost by implementing cost efficient

strategies in the business.

Integration of management accounting systems with the reporting systems of management

accounting.

Management accounting is a broad concept consisting of various tools and techniques for

effective management of the enterprise. MA accounting systems are the system with the use of

which managers keep proper record of all the transaction and events related to the different

activities and operation. On the other MA accounting reports are prepared by the organisation for

having complete information related to the outcomes of the management systems. Management

accounting systems and reporting together helps the management to maintain effective control

over its operations. For example the cost accounting systems provide the information related to

the actual costs incurred in the production process and cost report provide information related to

the variances incurred between actual and standards cost. This enables the company to identify

areas of improvements and to take corrective steps for increasing productivity.

Management accounting costing techniques

Marginal Costing

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

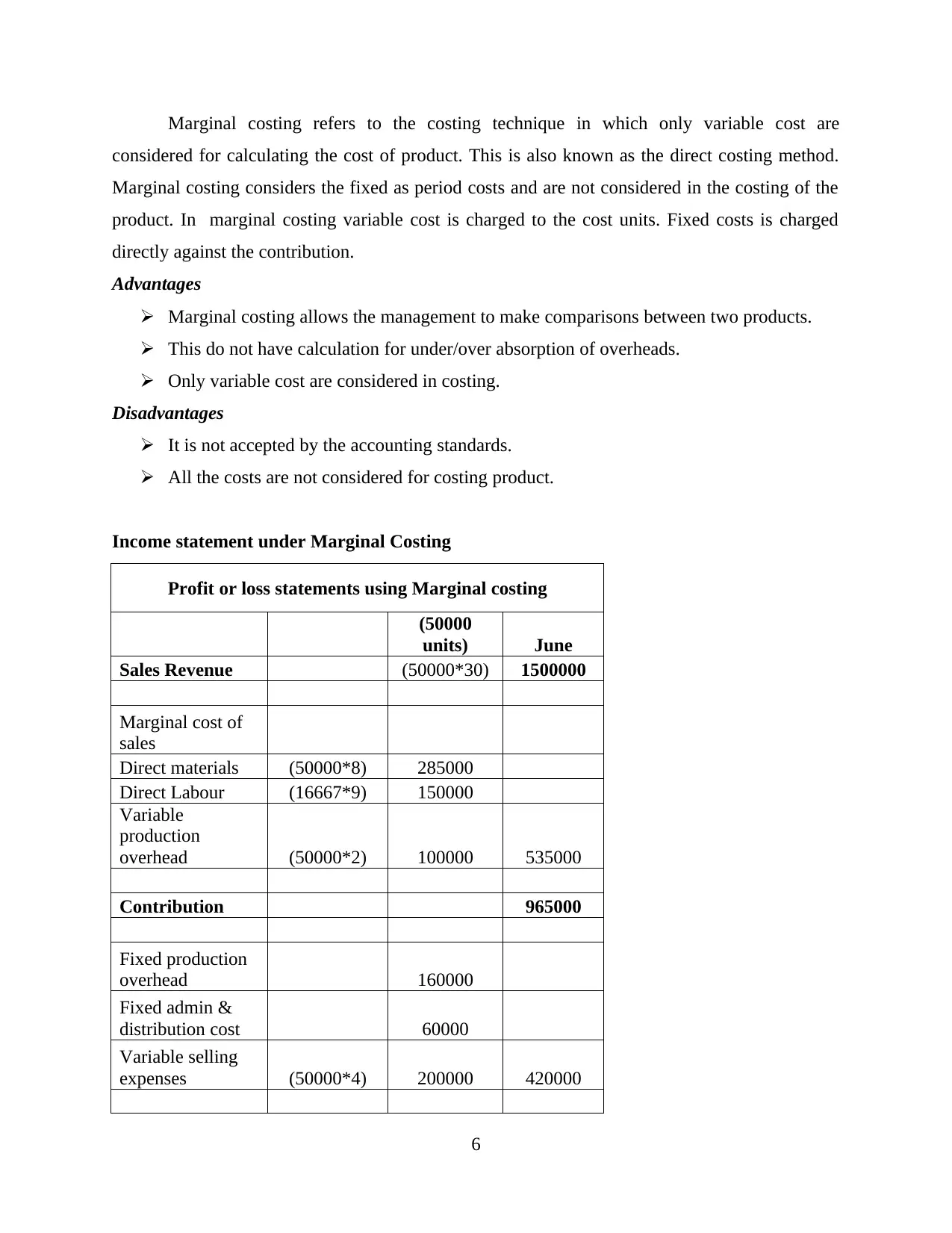

Marginal costing refers to the costing technique in which only variable cost are

considered for calculating the cost of product. This is also known as the direct costing method.

Marginal costing considers the fixed as period costs and are not considered in the costing of the

product. In marginal costing variable cost is charged to the cost units. Fixed costs is charged

directly against the contribution.

Advantages

Marginal costing allows the management to make comparisons between two products.

This do not have calculation for under/over absorption of overheads.

Only variable cost are considered in costing.

Disadvantages

It is not accepted by the accounting standards.

All the costs are not considered for costing product.

Income statement under Marginal Costing

Profit or loss statements using Marginal costing

(50000

units) June

Sales Revenue (50000*30) 1500000

Marginal cost of

sales

Direct materials (50000*8) 285000

Direct Labour (16667*9) 150000

Variable

production

overhead (50000*2) 100000 535000

Contribution 965000

Fixed production

overhead 160000

Fixed admin &

distribution cost 60000

Variable selling

expenses (50000*4) 200000 420000

6

considered for calculating the cost of product. This is also known as the direct costing method.

Marginal costing considers the fixed as period costs and are not considered in the costing of the

product. In marginal costing variable cost is charged to the cost units. Fixed costs is charged

directly against the contribution.

Advantages

Marginal costing allows the management to make comparisons between two products.

This do not have calculation for under/over absorption of overheads.

Only variable cost are considered in costing.

Disadvantages

It is not accepted by the accounting standards.

All the costs are not considered for costing product.

Income statement under Marginal Costing

Profit or loss statements using Marginal costing

(50000

units) June

Sales Revenue (50000*30) 1500000

Marginal cost of

sales

Direct materials (50000*8) 285000

Direct Labour (16667*9) 150000

Variable

production

overhead (50000*2) 100000 535000

Contribution 965000

Fixed production

overhead 160000

Fixed admin &

distribution cost 60000

Variable selling

expenses (50000*4) 200000 420000

6

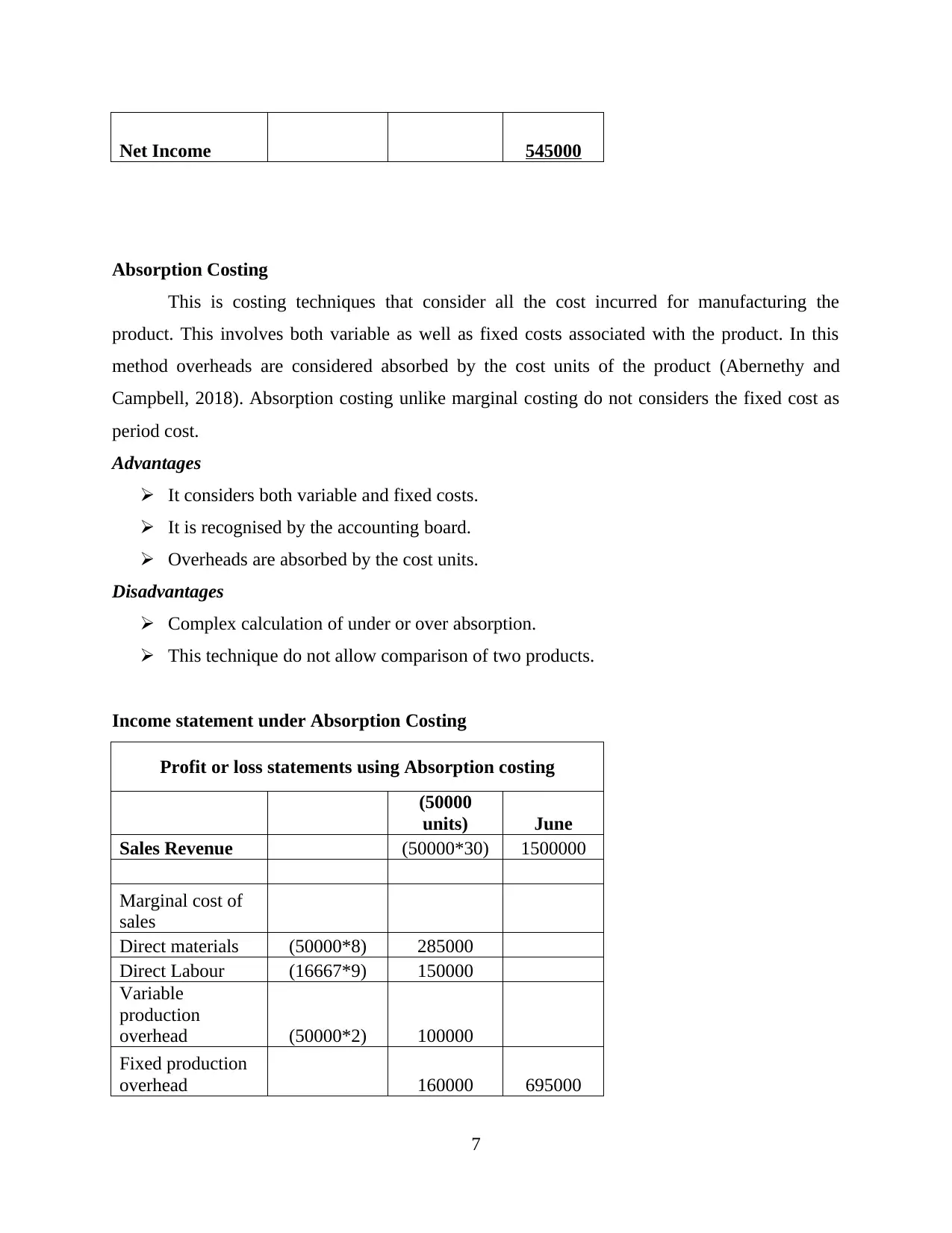

Net Income 545000

Absorption Costing

This is costing techniques that consider all the cost incurred for manufacturing the

product. This involves both variable as well as fixed costs associated with the product. In this

method overheads are considered absorbed by the cost units of the product (Abernethy and

Campbell, 2018). Absorption costing unlike marginal costing do not considers the fixed cost as

period cost.

Advantages

It considers both variable and fixed costs.

It is recognised by the accounting board.

Overheads are absorbed by the cost units.

Disadvantages

Complex calculation of under or over absorption.

This technique do not allow comparison of two products.

Income statement under Absorption Costing

Profit or loss statements using Absorption costing

(50000

units) June

Sales Revenue (50000*30) 1500000

Marginal cost of

sales

Direct materials (50000*8) 285000

Direct Labour (16667*9) 150000

Variable

production

overhead (50000*2) 100000

Fixed production

overhead 160000 695000

7

Absorption Costing

This is costing techniques that consider all the cost incurred for manufacturing the

product. This involves both variable as well as fixed costs associated with the product. In this

method overheads are considered absorbed by the cost units of the product (Abernethy and

Campbell, 2018). Absorption costing unlike marginal costing do not considers the fixed cost as

period cost.

Advantages

It considers both variable and fixed costs.

It is recognised by the accounting board.

Overheads are absorbed by the cost units.

Disadvantages

Complex calculation of under or over absorption.

This technique do not allow comparison of two products.

Income statement under Absorption Costing

Profit or loss statements using Absorption costing

(50000

units) June

Sales Revenue (50000*30) 1500000

Marginal cost of

sales

Direct materials (50000*8) 285000

Direct Labour (16667*9) 150000

Variable

production

overhead (50000*2) 100000

Fixed production

overhead 160000 695000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

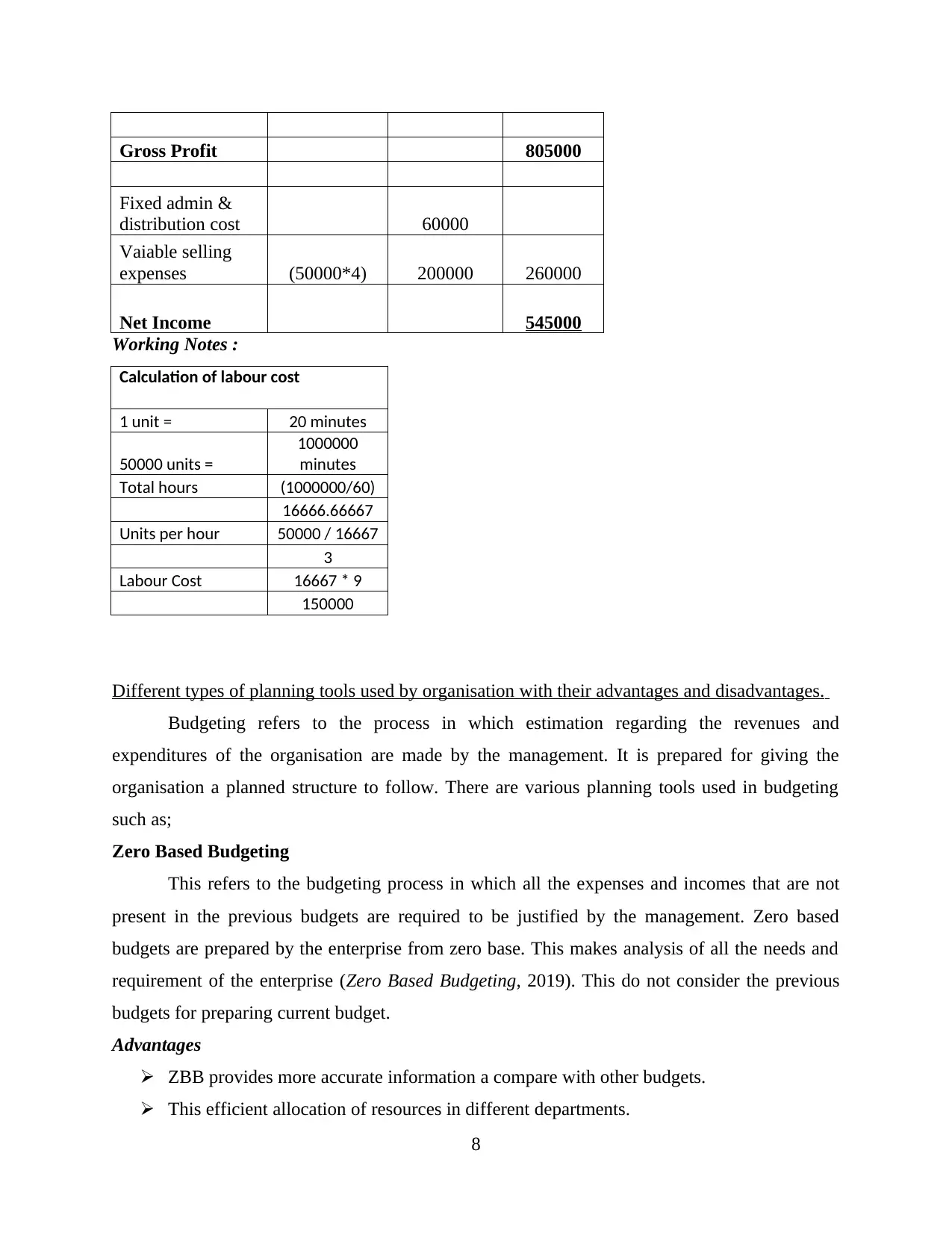

Gross Profit 805000

Fixed admin &

distribution cost 60000

Vaiable selling

expenses (50000*4) 200000 260000

Net Income 545000

Working Notes :

Calculation of labour cost

1 unit = 20 minutes

50000 units =

1000000

minutes

Total hours (1000000/60)

16666.66667

Units per hour 50000 / 16667

3

Labour Cost 16667 * 9

150000

Different types of planning tools used by organisation with their advantages and disadvantages.

Budgeting refers to the process in which estimation regarding the revenues and

expenditures of the organisation are made by the management. It is prepared for giving the

organisation a planned structure to follow. There are various planning tools used in budgeting

such as;

Zero Based Budgeting

This refers to the budgeting process in which all the expenses and incomes that are not

present in the previous budgets are required to be justified by the management. Zero based

budgets are prepared by the enterprise from zero base. This makes analysis of all the needs and

requirement of the enterprise (Zero Based Budgeting, 2019). This do not consider the previous

budgets for preparing current budget.

Advantages

ZBB provides more accurate information a compare with other budgets.

This efficient allocation of resources in different departments.

8

Fixed admin &

distribution cost 60000

Vaiable selling

expenses (50000*4) 200000 260000

Net Income 545000

Working Notes :

Calculation of labour cost

1 unit = 20 minutes

50000 units =

1000000

minutes

Total hours (1000000/60)

16666.66667

Units per hour 50000 / 16667

3

Labour Cost 16667 * 9

150000

Different types of planning tools used by organisation with their advantages and disadvantages.

Budgeting refers to the process in which estimation regarding the revenues and

expenditures of the organisation are made by the management. It is prepared for giving the

organisation a planned structure to follow. There are various planning tools used in budgeting

such as;

Zero Based Budgeting

This refers to the budgeting process in which all the expenses and incomes that are not

present in the previous budgets are required to be justified by the management. Zero based

budgets are prepared by the enterprise from zero base. This makes analysis of all the needs and

requirement of the enterprise (Zero Based Budgeting, 2019). This do not consider the previous

budgets for preparing current budget.

Advantages

ZBB provides more accurate information a compare with other budgets.

This efficient allocation of resources in different departments.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Justification of every line item causes company to consider the inflation and other market

conditions.

Disadvantages.

It is a time consuming process as everything is taken from the fresh.

Explanation of every cost and expenditure is difficult process.

This is costly process as large number of information is searched to prepared ZBB.

Activity based Budgeting

The budget is prepared using the information of activity based costing. This do not

consider the budget of previous years like zero based budget. Budget is prepare after properly

analysing the expenses associated with each activity. This is prepared by the management in

business having number of activities to prepare the product (Rikhardsson, 2017). It is not

prepared based on the operation but over different activities carried out in the process.

Advantages

This helps in effectively evaluating the cost drivers in different activities.

This helps in eliminating the unproductive costs and expenses from the budgets.

ABC budget help the business organisation in increasing its productivity and efficiency.

Disadvantages

This requires professional knowledge to understand the functional areas of business.

It is time consuming and expensive process to implement thios budgeting.

It focuses over the short term goals of the business enterprise.

Operating budget

Operating budget refers to the budget which is prepare by the business enterprise for

planning it daily expenses. They are prepared by the organisation based on previous budgets.

Adjustments related to the requirements of current year are made in this budgeting. It involves

forecasting about the revenues and expense essential to carry out the operations of business.

Advantages

This helps business in managing it current expenses.

This helps the organisation to prepare budget analysing the previous trends.

It is easy to prepare and simple to understand and interpret.

Disadvantages

9

conditions.

Disadvantages.

It is a time consuming process as everything is taken from the fresh.

Explanation of every cost and expenditure is difficult process.

This is costly process as large number of information is searched to prepared ZBB.

Activity based Budgeting

The budget is prepared using the information of activity based costing. This do not

consider the budget of previous years like zero based budget. Budget is prepare after properly

analysing the expenses associated with each activity. This is prepared by the management in

business having number of activities to prepare the product (Rikhardsson, 2017). It is not

prepared based on the operation but over different activities carried out in the process.

Advantages

This helps in effectively evaluating the cost drivers in different activities.

This helps in eliminating the unproductive costs and expenses from the budgets.

ABC budget help the business organisation in increasing its productivity and efficiency.

Disadvantages

This requires professional knowledge to understand the functional areas of business.

It is time consuming and expensive process to implement thios budgeting.

It focuses over the short term goals of the business enterprise.

Operating budget

Operating budget refers to the budget which is prepare by the business enterprise for

planning it daily expenses. They are prepared by the organisation based on previous budgets.

Adjustments related to the requirements of current year are made in this budgeting. It involves

forecasting about the revenues and expense essential to carry out the operations of business.

Advantages

This helps business in managing it current expenses.

This helps the organisation to prepare budget analysing the previous trends.

It is easy to prepare and simple to understand and interpret.

Disadvantages

9

It is based on previous budgets therefore the errors or mistakes could be carried forward.

This don not provide accurate information of costs.

Budget is prepared for short term business goals and objectives.

Management accounting adapted by companies in resolving financial issues.

An organisation for carrying out business has to face number of challenges. It is required to

overcome these challenges for the growth and success of the organisation. An organisation

problems related to the scarcity of resources and such other issues.

Management accounting systems.

GSQ faces the problem of increased storage cost of inventory. Inventory management

systems of MA helped the business to reduce its storage by adopting to just- in-time method.

Order is placed on demand and urgent delivery is made eliminating storage cost.

ABC faced the problems of high expenses. It adopted cost accounting systems to control

its expenditures. With use of standard costing specific resources were allocated to each

department for carrying out operation. This helped in identifying the department consuming

highest cost and was reduced by cost effective strategies.

Management accounting tools

Benchmarking helped the GSK in setting objectives for various tasks to be performed by

the organisation. This helped the management in identifying the performance of the departments.

They set realistic and achievable target for boosting motivation.

Key performance indicator is tool used in MA to measure the performance by

identifying the level of success achieved in accomplishing the set objectives (Dearman, Lechner

and Shanklin, 2018). Reasons are identified and corrective measures are taken.

MA planning tools

Zero based budget prepares budgets after analysing all the information related to incomes

and expenses that provides accurate information this reduces the variations in the actual and

budgeted figures.

Activity based budget has helped the business to resolves its issues of increasing costs. It

made budget based on activities involved in the process. Using this company identified the

consumption of resources by each activity and corrective steps to control the cost were taken.

10

This don not provide accurate information of costs.

Budget is prepared for short term business goals and objectives.

Management accounting adapted by companies in resolving financial issues.

An organisation for carrying out business has to face number of challenges. It is required to

overcome these challenges for the growth and success of the organisation. An organisation

problems related to the scarcity of resources and such other issues.

Management accounting systems.

GSQ faces the problem of increased storage cost of inventory. Inventory management

systems of MA helped the business to reduce its storage by adopting to just- in-time method.

Order is placed on demand and urgent delivery is made eliminating storage cost.

ABC faced the problems of high expenses. It adopted cost accounting systems to control

its expenditures. With use of standard costing specific resources were allocated to each

department for carrying out operation. This helped in identifying the department consuming

highest cost and was reduced by cost effective strategies.

Management accounting tools

Benchmarking helped the GSK in setting objectives for various tasks to be performed by

the organisation. This helped the management in identifying the performance of the departments.

They set realistic and achievable target for boosting motivation.

Key performance indicator is tool used in MA to measure the performance by

identifying the level of success achieved in accomplishing the set objectives (Dearman, Lechner

and Shanklin, 2018). Reasons are identified and corrective measures are taken.

MA planning tools

Zero based budget prepares budgets after analysing all the information related to incomes

and expenses that provides accurate information this reduces the variations in the actual and

budgeted figures.

Activity based budget has helped the business to resolves its issues of increasing costs. It

made budget based on activities involved in the process. Using this company identified the

consumption of resources by each activity and corrective steps to control the cost were taken.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.