MGMT 500: Management Accounting Report, Excite Entertainment Ltd

VerifiedAdded on 2023/01/13

|16

|4155

|1

Report

AI Summary

This report provides a detailed analysis of management accounting principles and their application within Excite Entertainment Ltd, a UK-based entertainment and leisure company. The report begins by contrasting management accounting with financial accounting, highlighting their distinct aims and information requirements. It then delves into various management accounting systems, including cost accounting, inventory management, and job costing, outlining their benefits and relevance to the company's operations. The report further explores different types of managerial accounting reports, such as performance, budget, and accounts receivable aging reports, and explains the importance of accurate, relevant, and up-to-date information. The integration of management accounting systems and reports with operational processes is also discussed. The report includes calculations using both absorption costing and marginal costing methods, comparing their impact on profit statements. Additionally, the report examines budgeting techniques, break-even analysis, and standard costing, including variable analysis. Sensitivity analysis and the assumptions underlying break-even point analysis are also addressed. The report concludes with a summary of the key findings and recommendations for Excite Entertainment Ltd.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

SECTION A.....................................................................................................................................1

(a) Comparison between MA and financial accounting.........................................................1

(b) Cost accounting system....................................................................................................2

(c) Inventory management system..........................................................................................2

(d) Job costing system............................................................................................................2

(e) Benefits of above mentioned accounting systems............................................................2

SECTION B.....................................................................................................................................3

(a) Different types of managerial accounting reports.............................................................3

(b) Why information should be accurate, relevant and up to date..........................................3

(c) How MAS and MA reports integrated with operational process......................................4

TASK 2............................................................................................................................................4

Calculation using Absorption Costing or Marginal Costing Method.....................................4

TASK 3............................................................................................................................................6

PART A...........................................................................................................................................6

Budgeting...............................................................................................................................6

Break even analysis................................................................................................................7

Standard costing.....................................................................................................................7

Variable analysis....................................................................................................................8

TASK 4............................................................................................................................................8

PART B............................................................................................................................................8

Contribution margin...............................................................................................................8

Break even point.....................................................................................................................9

Units to achieve......................................................................................................................9

Sensitivity analysis.................................................................................................................9

Assumption of break-even point analysis.............................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

SECTION A.....................................................................................................................................1

(a) Comparison between MA and financial accounting.........................................................1

(b) Cost accounting system....................................................................................................2

(c) Inventory management system..........................................................................................2

(d) Job costing system............................................................................................................2

(e) Benefits of above mentioned accounting systems............................................................2

SECTION B.....................................................................................................................................3

(a) Different types of managerial accounting reports.............................................................3

(b) Why information should be accurate, relevant and up to date..........................................3

(c) How MAS and MA reports integrated with operational process......................................4

TASK 2............................................................................................................................................4

Calculation using Absorption Costing or Marginal Costing Method.....................................4

TASK 3............................................................................................................................................6

PART A...........................................................................................................................................6

Budgeting...............................................................................................................................6

Break even analysis................................................................................................................7

Standard costing.....................................................................................................................7

Variable analysis....................................................................................................................8

TASK 4............................................................................................................................................8

PART B............................................................................................................................................8

Contribution margin...............................................................................................................8

Break even point.....................................................................................................................9

Units to achieve......................................................................................................................9

Sensitivity analysis.................................................................................................................9

Assumption of break-even point analysis.............................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION

Management accounting is regarded as the method of formulating managerial reports as

well as accounts which facilitates relevant and on time statistical data to managers for making

the long term and short term decisions. This finds evaluate, examine, interprets as well as

communicates information for enabling an entities to meet their objectives (What is Management

Accounting and its Importance, 2020). As per the given scenario, the undertaken organisation for

this report is Excite Entertainment Ltd. Which operates into entertainment as well as leisure

sector within United Kingdom. The topic which is going to covered in this report are differences

among financial and management accounting, cost accounting system and its benefits, many

kinds of managerial accounting reports and preparation of financial reports using costing

techniques. Apart from this, comparison among three planning tools and ways in which

management accounting system is applied are also discussed in this report.

TASK 1

SECTION A

(a) Comparison between MA and financial accounting.

As management accounting is differ from the financial accounting (Akhmetshin and

Osadchy, 2015). As financial accounting facilitates information to internal and external

stakeholder of organisation so, comparison among both accounting are discussed below:

Basis Management accounting Financial accounting

Aim The aim of management accounting

is to formulate internal report so that

firm's managers may develop

effective decisions.

The aim of Financial accounting is

to formulate financial statement for

expanding information related to

monetary position to stakeholders.

Information It depends upon two kinds of

information which is related to

statistical and non statistical aspects.

It only depends upon the financial

information.

1

Management accounting is regarded as the method of formulating managerial reports as

well as accounts which facilitates relevant and on time statistical data to managers for making

the long term and short term decisions. This finds evaluate, examine, interprets as well as

communicates information for enabling an entities to meet their objectives (What is Management

Accounting and its Importance, 2020). As per the given scenario, the undertaken organisation for

this report is Excite Entertainment Ltd. Which operates into entertainment as well as leisure

sector within United Kingdom. The topic which is going to covered in this report are differences

among financial and management accounting, cost accounting system and its benefits, many

kinds of managerial accounting reports and preparation of financial reports using costing

techniques. Apart from this, comparison among three planning tools and ways in which

management accounting system is applied are also discussed in this report.

TASK 1

SECTION A

(a) Comparison between MA and financial accounting.

As management accounting is differ from the financial accounting (Akhmetshin and

Osadchy, 2015). As financial accounting facilitates information to internal and external

stakeholder of organisation so, comparison among both accounting are discussed below:

Basis Management accounting Financial accounting

Aim The aim of management accounting

is to formulate internal report so that

firm's managers may develop

effective decisions.

The aim of Financial accounting is

to formulate financial statement for

expanding information related to

monetary position to stakeholders.

Information It depends upon two kinds of

information which is related to

statistical and non statistical aspects.

It only depends upon the financial

information.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(b) Cost accounting system

This is regarded as the type of management accounting system that is in respect for

developing future projection spendings as well as managing whole costs. It is crucial for entities

to use this into its practices so that variance and exact cost may be calculated. In absence of

respective accounting system, this become tough for them to overcome from unfavourable

variances. Moreover, it is not only restricted to this within it the standard and direct costs are also

managed effectively. So, this is being used into Excite Entertainment Ltd with an intent to

manage cost of various practices regarding conducting any events.

(c) Inventory management system

This is regarded as accounting system which is associated with methods of managing as

well as controlling several types of inventory quantity such as raw material, development of

goods and others (Borker, 2016). This depends upon some stock valuation techniques that are

FIFO, LIFO and many more. This is crucial for firm as it aids them to keep inventory level

updated on regular basis in order to identify how much inventory is utilised for producing goods

as well as how much raw materials quantity is there in warehouse. So, Excite Entertainment Ltd

event manager may use this system for tracking various musical instruments availability.

(d) Job costing system

This is define as a kind of accounting system which is related with computing job cots

individually. It is essential for entities to understand how much cost have been incurred in

accomplishing any specific activities. In job accounting system, many kinds of costs are

computed like direct material cots, labour cost and others. Such as within Excite Entertainment

Ltd., this respective system is used with an intent of facilitating detailed data to its finance

department regarding job costs.

(e) Benefits of above mentioned accounting systems

The above mentioned management accounting system have various benefits which is

described below: Cost accounting system: It is an accounting system which depends upon computing as

well as managing whole expenses (Osadchy and Akhmetshin, 2015). For this within

Excite Entertainment Ltd, its finance manager perform relevant assumptions regarding

future cost as well as keeping control over unnecessary expenses.

2

This is regarded as the type of management accounting system that is in respect for

developing future projection spendings as well as managing whole costs. It is crucial for entities

to use this into its practices so that variance and exact cost may be calculated. In absence of

respective accounting system, this become tough for them to overcome from unfavourable

variances. Moreover, it is not only restricted to this within it the standard and direct costs are also

managed effectively. So, this is being used into Excite Entertainment Ltd with an intent to

manage cost of various practices regarding conducting any events.

(c) Inventory management system

This is regarded as accounting system which is associated with methods of managing as

well as controlling several types of inventory quantity such as raw material, development of

goods and others (Borker, 2016). This depends upon some stock valuation techniques that are

FIFO, LIFO and many more. This is crucial for firm as it aids them to keep inventory level

updated on regular basis in order to identify how much inventory is utilised for producing goods

as well as how much raw materials quantity is there in warehouse. So, Excite Entertainment Ltd

event manager may use this system for tracking various musical instruments availability.

(d) Job costing system

This is define as a kind of accounting system which is related with computing job cots

individually. It is essential for entities to understand how much cost have been incurred in

accomplishing any specific activities. In job accounting system, many kinds of costs are

computed like direct material cots, labour cost and others. Such as within Excite Entertainment

Ltd., this respective system is used with an intent of facilitating detailed data to its finance

department regarding job costs.

(e) Benefits of above mentioned accounting systems

The above mentioned management accounting system have various benefits which is

described below: Cost accounting system: It is an accounting system which depends upon computing as

well as managing whole expenses (Osadchy and Akhmetshin, 2015). For this within

Excite Entertainment Ltd, its finance manager perform relevant assumptions regarding

future cost as well as keeping control over unnecessary expenses.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inventory management system: This depends upon the usages of several methods of

inventory valuation for updating as well as tacking raw materials utilisation. Excite

Entertainment Ltd use this system for facilitating vital data to its manager related to

whole material quantity which is stored into its warehouses.

Job costing system: It is associated with computing job costs individually. Within Excite

Entertainment Ltd, its manager utilise this accounting system for managing as well as

tracking job costs in more efficacious way.

SECTION B

(a) Different types of managerial accounting reports.

Managerial accounting reporting is regarded as the procedures to develop report which is

comply through whole firms for analysing exact business performance. So, into Excite

Entertainment Ltd, its manager are some reports that are discussed below: Performance report: In this the data related to performance of every prospect in involved.

The aim of formulating this report is to assists managers for taking appropriate steps

regarding staff progress and promotion based on its exact performance (Gunarathne and

et. al, 2016). Budget report: Within this managerial report, data related to approximated as well as

exact monetary results is involved. So, Excite Entertainment Ltd. Formulate respective

report in order to manage financial performance.

Account receivable ageing report: This is considered as the managerial report that

involves data related to overall debtors or clients whose payment is due. Within Excite

Entertainment Ltd, its accounts manager prepare respective report in order to track those

consumer whose payment is not yet cleared.

(b) Why information should be accurate, relevant and up to date.

It is vital for all companies to keep their monetary data relevant, updated and accurate.

This is because in case information is accurate then it becomes simple for its accountants t

formulate financial statements (Butler and Ghosh, 2015). Moreover, there have to be relevancy

of monetary information with firms transactions in order make effective internal decisions.

Similarly, this is essential to to represent the monetary data at specified duration so that

stakeholder may have knowledge regarding entities performance.

3

inventory valuation for updating as well as tacking raw materials utilisation. Excite

Entertainment Ltd use this system for facilitating vital data to its manager related to

whole material quantity which is stored into its warehouses.

Job costing system: It is associated with computing job costs individually. Within Excite

Entertainment Ltd, its manager utilise this accounting system for managing as well as

tracking job costs in more efficacious way.

SECTION B

(a) Different types of managerial accounting reports.

Managerial accounting reporting is regarded as the procedures to develop report which is

comply through whole firms for analysing exact business performance. So, into Excite

Entertainment Ltd, its manager are some reports that are discussed below: Performance report: In this the data related to performance of every prospect in involved.

The aim of formulating this report is to assists managers for taking appropriate steps

regarding staff progress and promotion based on its exact performance (Gunarathne and

et. al, 2016). Budget report: Within this managerial report, data related to approximated as well as

exact monetary results is involved. So, Excite Entertainment Ltd. Formulate respective

report in order to manage financial performance.

Account receivable ageing report: This is considered as the managerial report that

involves data related to overall debtors or clients whose payment is due. Within Excite

Entertainment Ltd, its accounts manager prepare respective report in order to track those

consumer whose payment is not yet cleared.

(b) Why information should be accurate, relevant and up to date.

It is vital for all companies to keep their monetary data relevant, updated and accurate.

This is because in case information is accurate then it becomes simple for its accountants t

formulate financial statements (Butler and Ghosh, 2015). Moreover, there have to be relevancy

of monetary information with firms transactions in order make effective internal decisions.

Similarly, this is essential to to represent the monetary data at specified duration so that

stakeholder may have knowledge regarding entities performance.

3

(c) How MAS and MA reports integrated with operational process.

The operative procedures of Excite Entertainment Ltd have been incorporated with

management accounting system like inventory, cost and others. It is so as its finance section may

able to control as well as trace the whole cost and its production section are also related to

inventory management system so that materials quantity can be managed effectively. Similarly,

the reports of management accounting are also integrated to its enterprise procedures.

TASK 2

Calculation using Absorption Costing or Marginal Costing Method

Basically, there are two costing techniques such as marginal and absorption. Both of

them are discussed below:

Marginal costing:

It is regarded as costing techniques which undertake the cost into various ways as in this

fixed cost is allotted as period cost. Where as the variable cost is delegated as unit cost (Tan,

2016). With the help of this Excite Entertainment Ltd can able to distinguished several kinds of

cost which is incurred as well as utilised that for formulation of financial statement. Advantage: It can be understandable and used in simple. Moreover, this contributes into

effectual cost control as it distinguish overall cost within variable and fixed cost. Thus,

through concentrating upon whole potential upon variable cost as it control the cost

effectively.

Disadvantage: Also, it have some disadvantage as this is computed on unrealistic

assumption in which whole cost is categorised in variable and fixed cost. Moreover, it is

unrealistic into the situation of production level variation.

Absorption costing:

This is regarded as the type of costing technique where whole kinds of cost are absorbed

in accomplished way at the time of formulating financial statements (Edmonds and et. al., 2015).

Within this, the variable as well as fixed cost are taken as product cost. Advantage: This is helpful to understand the role of fixed manufacturing cost into product

analysis as well as using effectual policy related to pricing.

Disadvantage: It is not effective for producing flexible budgets as due to lack of

differences among fixed and non fixed cost.

4

The operative procedures of Excite Entertainment Ltd have been incorporated with

management accounting system like inventory, cost and others. It is so as its finance section may

able to control as well as trace the whole cost and its production section are also related to

inventory management system so that materials quantity can be managed effectively. Similarly,

the reports of management accounting are also integrated to its enterprise procedures.

TASK 2

Calculation using Absorption Costing or Marginal Costing Method

Basically, there are two costing techniques such as marginal and absorption. Both of

them are discussed below:

Marginal costing:

It is regarded as costing techniques which undertake the cost into various ways as in this

fixed cost is allotted as period cost. Where as the variable cost is delegated as unit cost (Tan,

2016). With the help of this Excite Entertainment Ltd can able to distinguished several kinds of

cost which is incurred as well as utilised that for formulation of financial statement. Advantage: It can be understandable and used in simple. Moreover, this contributes into

effectual cost control as it distinguish overall cost within variable and fixed cost. Thus,

through concentrating upon whole potential upon variable cost as it control the cost

effectively.

Disadvantage: Also, it have some disadvantage as this is computed on unrealistic

assumption in which whole cost is categorised in variable and fixed cost. Moreover, it is

unrealistic into the situation of production level variation.

Absorption costing:

This is regarded as the type of costing technique where whole kinds of cost are absorbed

in accomplished way at the time of formulating financial statements (Edmonds and et. al., 2015).

Within this, the variable as well as fixed cost are taken as product cost. Advantage: This is helpful to understand the role of fixed manufacturing cost into product

analysis as well as using effectual policy related to pricing.

Disadvantage: It is not effective for producing flexible budgets as due to lack of

differences among fixed and non fixed cost.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

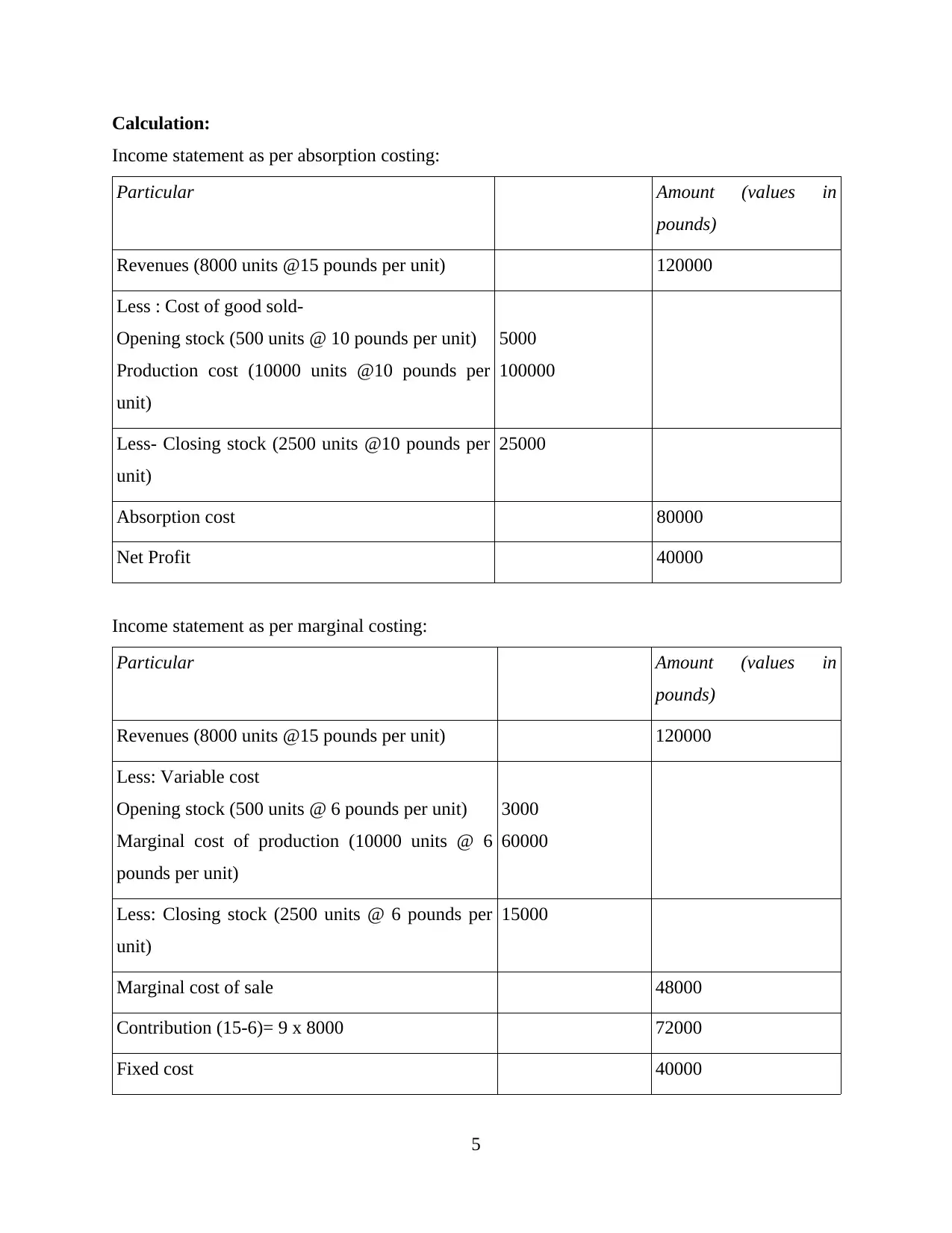

Calculation:

Income statement as per absorption costing:

Particular Amount (values in

pounds)

Revenues (8000 units @15 pounds per unit) 120000

Less : Cost of good sold-

Opening stock (500 units @ 10 pounds per unit)

Production cost (10000 units @10 pounds per

unit)

5000

100000

Less- Closing stock (2500 units @10 pounds per

unit)

25000

Absorption cost 80000

Net Profit 40000

Income statement as per marginal costing:

Particular Amount (values in

pounds)

Revenues (8000 units @15 pounds per unit) 120000

Less: Variable cost

Opening stock (500 units @ 6 pounds per unit)

Marginal cost of production (10000 units @ 6

pounds per unit)

3000

60000

Less: Closing stock (2500 units @ 6 pounds per

unit)

15000

Marginal cost of sale 48000

Contribution (15-6)= 9 x 8000 72000

Fixed cost 40000

5

Income statement as per absorption costing:

Particular Amount (values in

pounds)

Revenues (8000 units @15 pounds per unit) 120000

Less : Cost of good sold-

Opening stock (500 units @ 10 pounds per unit)

Production cost (10000 units @10 pounds per

unit)

5000

100000

Less- Closing stock (2500 units @10 pounds per

unit)

25000

Absorption cost 80000

Net Profit 40000

Income statement as per marginal costing:

Particular Amount (values in

pounds)

Revenues (8000 units @15 pounds per unit) 120000

Less: Variable cost

Opening stock (500 units @ 6 pounds per unit)

Marginal cost of production (10000 units @ 6

pounds per unit)

3000

60000

Less: Closing stock (2500 units @ 6 pounds per

unit)

15000

Marginal cost of sale 48000

Contribution (15-6)= 9 x 8000 72000

Fixed cost 40000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

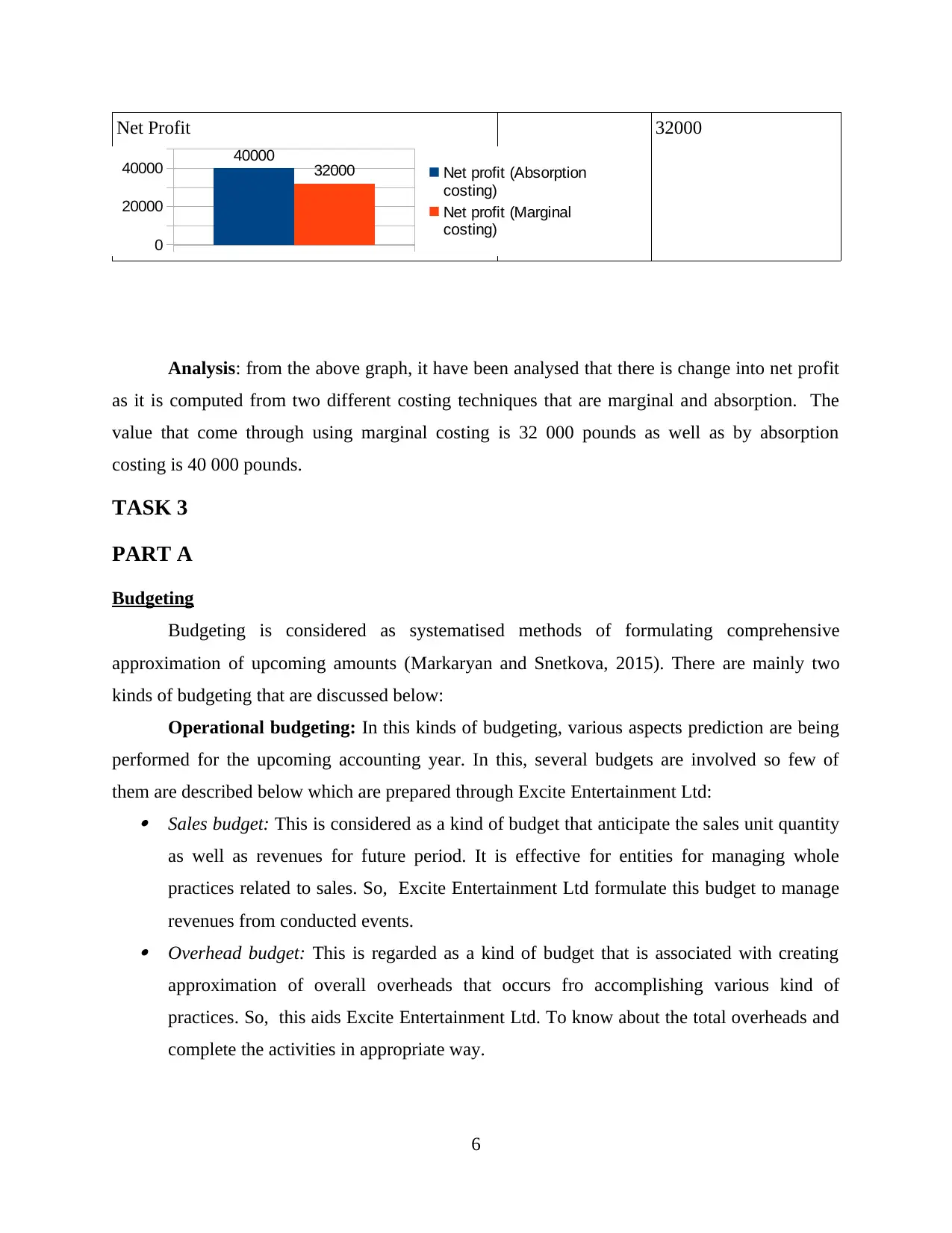

Net Profit 32000

Analysis: from the above graph, it have been analysed that there is change into net profit

as it is computed from two different costing techniques that are marginal and absorption. The

value that come through using marginal costing is 32 000 pounds as well as by absorption

costing is 40 000 pounds.

TASK 3

PART A

Budgeting

Budgeting is considered as systematised methods of formulating comprehensive

approximation of upcoming amounts (Markaryan and Snetkova, 2015). There are mainly two

kinds of budgeting that are discussed below:

Operational budgeting: In this kinds of budgeting, various aspects prediction are being

performed for the upcoming accounting year. In this, several budgets are involved so few of

them are described below which are prepared through Excite Entertainment Ltd: Sales budget: This is considered as a kind of budget that anticipate the sales unit quantity

as well as revenues for future period. It is effective for entities for managing whole

practices related to sales. So, Excite Entertainment Ltd formulate this budget to manage

revenues from conducted events. Overhead budget: This is regarded as a kind of budget that is associated with creating

approximation of overall overheads that occurs fro accomplishing various kind of

practices. So, this aids Excite Entertainment Ltd. To know about the total overheads and

complete the activities in appropriate way.

6

0

20000

40000 40000 32000 Net profit (Absorption

costing)

Net profit (Marginal

costing)

Analysis: from the above graph, it have been analysed that there is change into net profit

as it is computed from two different costing techniques that are marginal and absorption. The

value that come through using marginal costing is 32 000 pounds as well as by absorption

costing is 40 000 pounds.

TASK 3

PART A

Budgeting

Budgeting is considered as systematised methods of formulating comprehensive

approximation of upcoming amounts (Markaryan and Snetkova, 2015). There are mainly two

kinds of budgeting that are discussed below:

Operational budgeting: In this kinds of budgeting, various aspects prediction are being

performed for the upcoming accounting year. In this, several budgets are involved so few of

them are described below which are prepared through Excite Entertainment Ltd: Sales budget: This is considered as a kind of budget that anticipate the sales unit quantity

as well as revenues for future period. It is effective for entities for managing whole

practices related to sales. So, Excite Entertainment Ltd formulate this budget to manage

revenues from conducted events. Overhead budget: This is regarded as a kind of budget that is associated with creating

approximation of overall overheads that occurs fro accomplishing various kind of

practices. So, this aids Excite Entertainment Ltd. To know about the total overheads and

complete the activities in appropriate way.

6

0

20000

40000 40000 32000 Net profit (Absorption

costing)

Net profit (Marginal

costing)

Production budget: It is a kind of budget that is associated with developing anticipation

of overall manufacturing units as well as expenses which may incurs into procedures of

production. So, Excite Entertainment Ltd. Accountant formulate this budget in order to

manage the cost effectively related to entertainment aspects.

Capital Budgeting: It is regarded as a kind of budgeting which is associated with

approximating various kind of project efficiency. This is helpful for that projects which is large

in size (Vasarhelyi, Kogan and Tuttle, 2015). In this, project approximation is being performed

through assistance of many methods like internal rate of return, payback period and others. So,

this assists Excite Entertainment Ltd to examine its project effectiveness with the assistance of

budgeting.

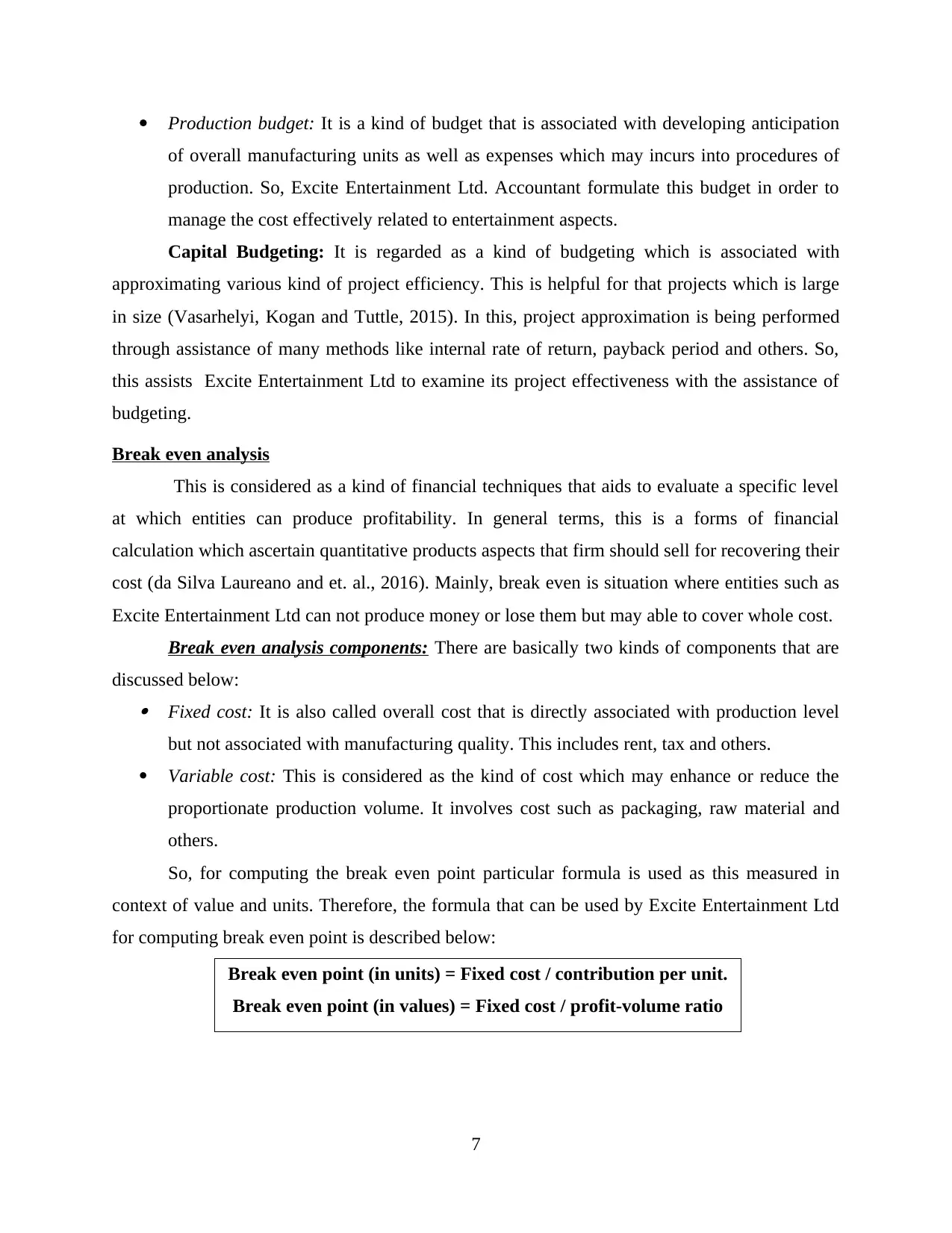

Break even analysis

This is considered as a kind of financial techniques that aids to evaluate a specific level

at which entities can produce profitability. In general terms, this is a forms of financial

calculation which ascertain quantitative products aspects that firm should sell for recovering their

cost (da Silva Laureano and et. al., 2016). Mainly, break even is situation where entities such as

Excite Entertainment Ltd can not produce money or lose them but may able to cover whole cost.

Break even analysis components: There are basically two kinds of components that are

discussed below: Fixed cost: It is also called overall cost that is directly associated with production level

but not associated with manufacturing quality. This includes rent, tax and others.

Variable cost: This is considered as the kind of cost which may enhance or reduce the

proportionate production volume. It involves cost such as packaging, raw material and

others.

So, for computing the break even point particular formula is used as this measured in

context of value and units. Therefore, the formula that can be used by Excite Entertainment Ltd

for computing break even point is described below:

Break even point (in units) = Fixed cost / contribution per unit.

Break even point (in values) = Fixed cost / profit-volume ratio

7

of overall manufacturing units as well as expenses which may incurs into procedures of

production. So, Excite Entertainment Ltd. Accountant formulate this budget in order to

manage the cost effectively related to entertainment aspects.

Capital Budgeting: It is regarded as a kind of budgeting which is associated with

approximating various kind of project efficiency. This is helpful for that projects which is large

in size (Vasarhelyi, Kogan and Tuttle, 2015). In this, project approximation is being performed

through assistance of many methods like internal rate of return, payback period and others. So,

this assists Excite Entertainment Ltd to examine its project effectiveness with the assistance of

budgeting.

Break even analysis

This is considered as a kind of financial techniques that aids to evaluate a specific level

at which entities can produce profitability. In general terms, this is a forms of financial

calculation which ascertain quantitative products aspects that firm should sell for recovering their

cost (da Silva Laureano and et. al., 2016). Mainly, break even is situation where entities such as

Excite Entertainment Ltd can not produce money or lose them but may able to cover whole cost.

Break even analysis components: There are basically two kinds of components that are

discussed below: Fixed cost: It is also called overall cost that is directly associated with production level

but not associated with manufacturing quality. This includes rent, tax and others.

Variable cost: This is considered as the kind of cost which may enhance or reduce the

proportionate production volume. It involves cost such as packaging, raw material and

others.

So, for computing the break even point particular formula is used as this measured in

context of value and units. Therefore, the formula that can be used by Excite Entertainment Ltd

for computing break even point is described below:

Break even point (in units) = Fixed cost / contribution per unit.

Break even point (in values) = Fixed cost / profit-volume ratio

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Standard costing

It is regarded as a kind of technique where cost of several aspects is approximated. As per

this, it becomes simple for firms to compare the actual cost. It is so as based on approximated

cost, Excite Entertainment Ltd finance manager can perform comparison of exact cost. This

have few benefits such as:

It aids respective organisation to do managerial planning as well as make effectual

decisions.

It is more reasonable and appropriate for inventory evaluation.

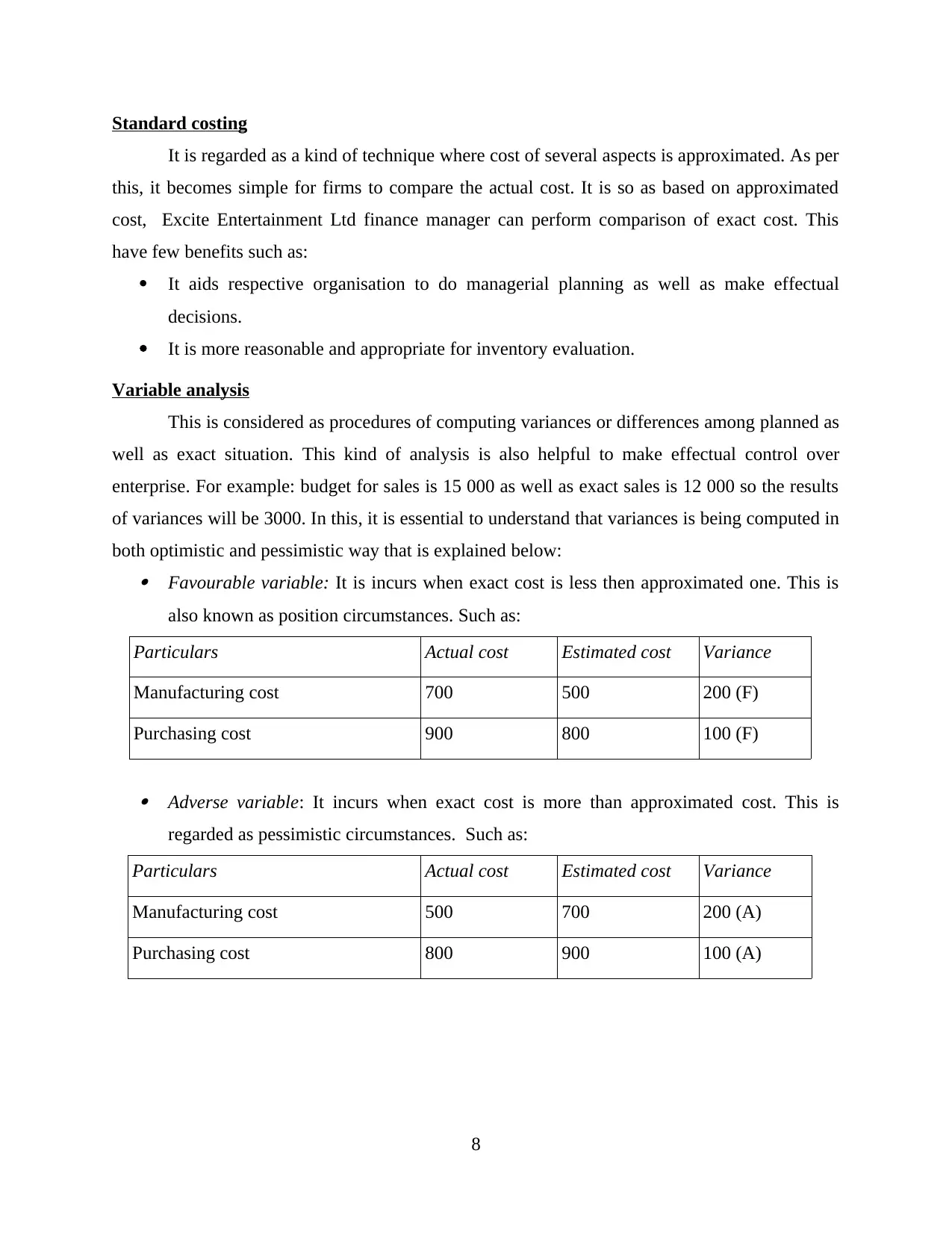

Variable analysis

This is considered as procedures of computing variances or differences among planned as

well as exact situation. This kind of analysis is also helpful to make effectual control over

enterprise. For example: budget for sales is 15 000 as well as exact sales is 12 000 so the results

of variances will be 3000. In this, it is essential to understand that variances is being computed in

both optimistic and pessimistic way that is explained below: Favourable variable: It is incurs when exact cost is less then approximated one. This is

also known as position circumstances. Such as:

Particulars Actual cost Estimated cost Variance

Manufacturing cost 700 500 200 (F)

Purchasing cost 900 800 100 (F)

Adverse variable: It incurs when exact cost is more than approximated cost. This is

regarded as pessimistic circumstances. Such as:

Particulars Actual cost Estimated cost Variance

Manufacturing cost 500 700 200 (A)

Purchasing cost 800 900 100 (A)

8

It is regarded as a kind of technique where cost of several aspects is approximated. As per

this, it becomes simple for firms to compare the actual cost. It is so as based on approximated

cost, Excite Entertainment Ltd finance manager can perform comparison of exact cost. This

have few benefits such as:

It aids respective organisation to do managerial planning as well as make effectual

decisions.

It is more reasonable and appropriate for inventory evaluation.

Variable analysis

This is considered as procedures of computing variances or differences among planned as

well as exact situation. This kind of analysis is also helpful to make effectual control over

enterprise. For example: budget for sales is 15 000 as well as exact sales is 12 000 so the results

of variances will be 3000. In this, it is essential to understand that variances is being computed in

both optimistic and pessimistic way that is explained below: Favourable variable: It is incurs when exact cost is less then approximated one. This is

also known as position circumstances. Such as:

Particulars Actual cost Estimated cost Variance

Manufacturing cost 700 500 200 (F)

Purchasing cost 900 800 100 (F)

Adverse variable: It incurs when exact cost is more than approximated cost. This is

regarded as pessimistic circumstances. Such as:

Particulars Actual cost Estimated cost Variance

Manufacturing cost 500 700 200 (A)

Purchasing cost 800 900 100 (A)

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 4

PART B

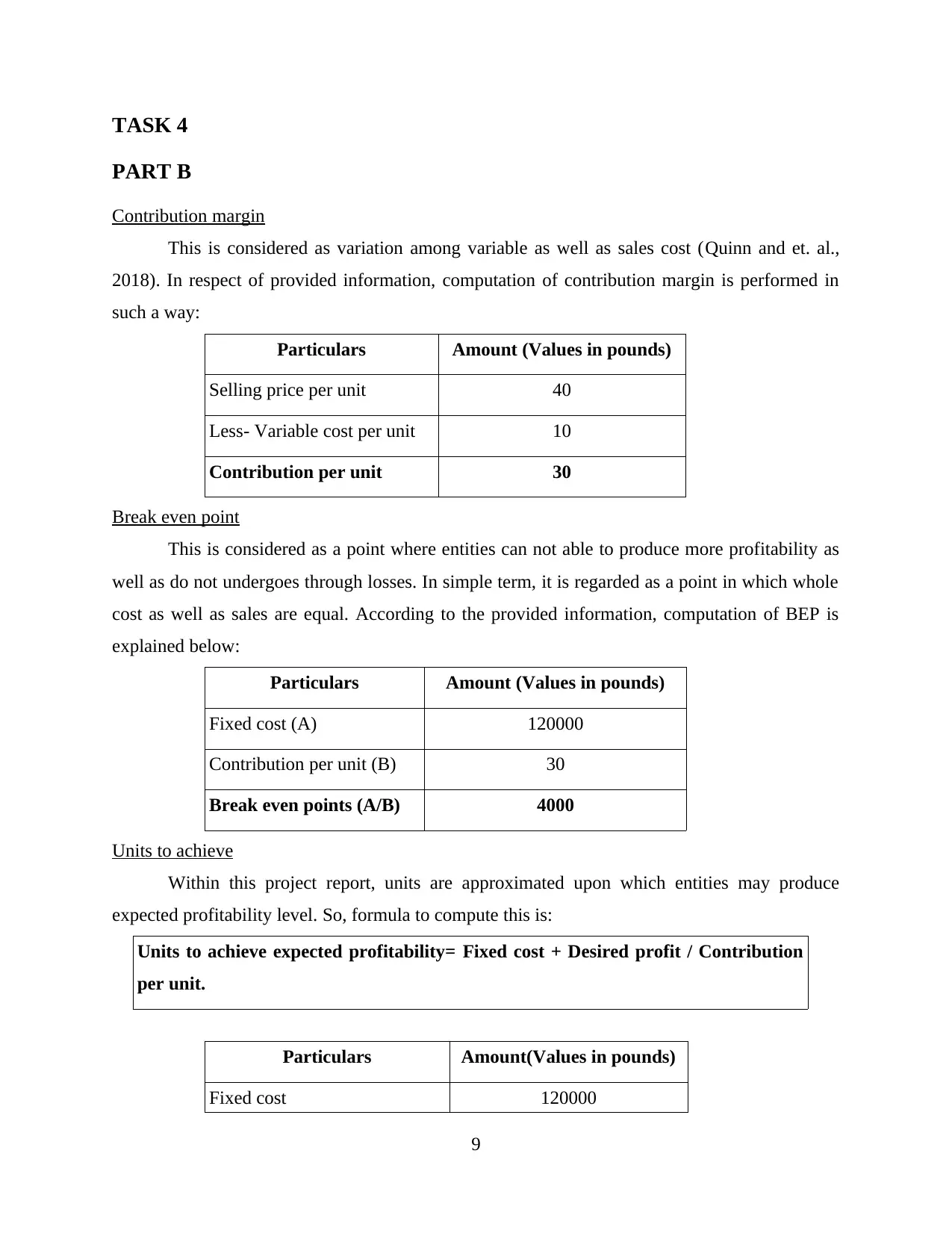

Contribution margin

This is considered as variation among variable as well as sales cost (Quinn and et. al.,

2018). In respect of provided information, computation of contribution margin is performed in

such a way:

Particulars Amount (Values in pounds)

Selling price per unit 40

Less- Variable cost per unit 10

Contribution per unit 30

Break even point

This is considered as a point where entities can not able to produce more profitability as

well as do not undergoes through losses. In simple term, it is regarded as a point in which whole

cost as well as sales are equal. According to the provided information, computation of BEP is

explained below:

Particulars Amount (Values in pounds)

Fixed cost (A) 120000

Contribution per unit (B) 30

Break even points (A/B) 4000

Units to achieve

Within this project report, units are approximated upon which entities may produce

expected profitability level. So, formula to compute this is:

Units to achieve expected profitability= Fixed cost + Desired profit / Contribution

per unit.

Particulars Amount(Values in pounds)

Fixed cost 120000

9

PART B

Contribution margin

This is considered as variation among variable as well as sales cost (Quinn and et. al.,

2018). In respect of provided information, computation of contribution margin is performed in

such a way:

Particulars Amount (Values in pounds)

Selling price per unit 40

Less- Variable cost per unit 10

Contribution per unit 30

Break even point

This is considered as a point where entities can not able to produce more profitability as

well as do not undergoes through losses. In simple term, it is regarded as a point in which whole

cost as well as sales are equal. According to the provided information, computation of BEP is

explained below:

Particulars Amount (Values in pounds)

Fixed cost (A) 120000

Contribution per unit (B) 30

Break even points (A/B) 4000

Units to achieve

Within this project report, units are approximated upon which entities may produce

expected profitability level. So, formula to compute this is:

Units to achieve expected profitability= Fixed cost + Desired profit / Contribution

per unit.

Particulars Amount(Values in pounds)

Fixed cost 120000

9

Desired profit 90000

Contribution per unit 30

Units to attain desired profit 7000 units

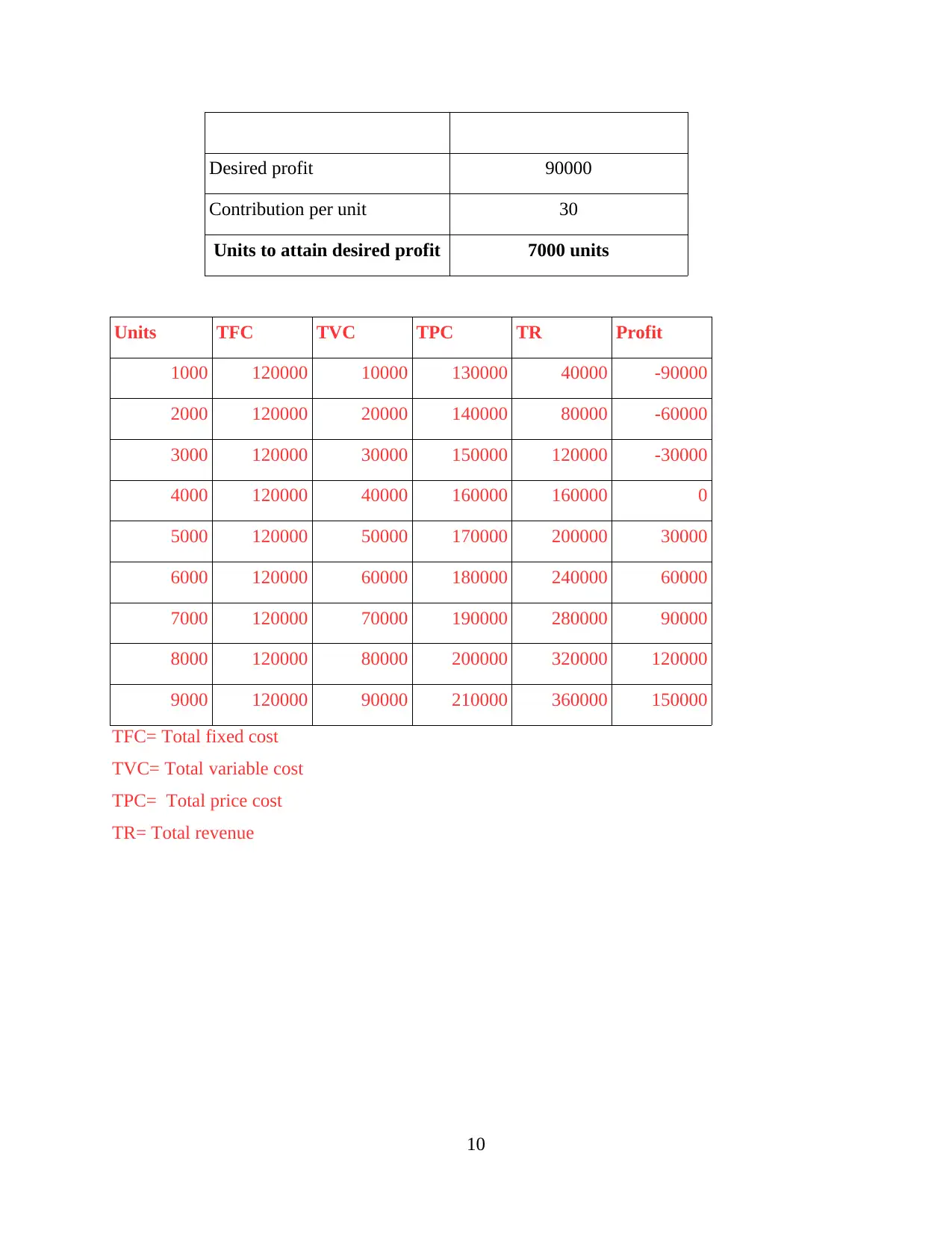

Units TFC TVC TPC TR Profit

1000 120000 10000 130000 40000 -90000

2000 120000 20000 140000 80000 -60000

3000 120000 30000 150000 120000 -30000

4000 120000 40000 160000 160000 0

5000 120000 50000 170000 200000 30000

6000 120000 60000 180000 240000 60000

7000 120000 70000 190000 280000 90000

8000 120000 80000 200000 320000 120000

9000 120000 90000 210000 360000 150000

TFC= Total fixed cost

TVC= Total variable cost

TPC= Total price cost

TR= Total revenue

10

Contribution per unit 30

Units to attain desired profit 7000 units

Units TFC TVC TPC TR Profit

1000 120000 10000 130000 40000 -90000

2000 120000 20000 140000 80000 -60000

3000 120000 30000 150000 120000 -30000

4000 120000 40000 160000 160000 0

5000 120000 50000 170000 200000 30000

6000 120000 60000 180000 240000 60000

7000 120000 70000 190000 280000 90000

8000 120000 80000 200000 320000 120000

9000 120000 90000 210000 360000 150000

TFC= Total fixed cost

TVC= Total variable cost

TPC= Total price cost

TR= Total revenue

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.