Management Accounting Report: Evaluating Financial Systems and Reports

VerifiedAdded on 2023/01/19

|24

|6993

|27

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its systems, techniques, and practical applications within the context of ABC Ltd, a medium-sized manufacturing company. It begins by defining management accounting and its role in financial decision-making, followed by an examination of various management accounting systems such as cost accounting, price optimization, job costing, and inventory management systems. The report then delves into the different methods used in management accounting reports, including budget reports, performance reports, inventory management reports, and accounts receivable reports. It also explores the benefits of these systems, evaluating the integration between accounting systems, reports, and organizational processes. Furthermore, the report analyzes cost analysis techniques, planning tools, and their application in forecasting budgets. Finally, it compares how organizations solve financial problems using accounting systems, emphasizing the role of management accounting in achieving sustainable success. The report concludes with a summary of the key findings and insights, supported by relevant references.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and accounting systems.................................................................1

P2. Methods in management accounting reports.........................................................................3

M1. Benefits of management accounting systems......................................................................5

D1. Evaluating integration between accounting systems as well as reports with organisational

processes......................................................................................................................................6

TASK 2............................................................................................................................................6

P3. Calculation of costs by using cost analysis techniques.........................................................6

M2. Usage of appropriate techniques in order to produce financial reporting documents........10

D2. Financial reports to interpret business operational activities..............................................11

TASK 3..........................................................................................................................................11

P4. Distinct Kinds of planning tools..........................................................................................11

M3. Planning tools with application in order to prepare as well as forecasting budgets...........15

TASK 4..........................................................................................................................................16

P5. Comparison showing the ways organisations solve financial problems with the use of

accounting systems....................................................................................................................16

M4. Responding of management accounting towards financial problems for sustainable

success........................................................................................................................................18

D3. Planning tools usage to respond towards solving financial problems so to lead the

organisation towards sustainable success..................................................................................18

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and accounting systems.................................................................1

P2. Methods in management accounting reports.........................................................................3

M1. Benefits of management accounting systems......................................................................5

D1. Evaluating integration between accounting systems as well as reports with organisational

processes......................................................................................................................................6

TASK 2............................................................................................................................................6

P3. Calculation of costs by using cost analysis techniques.........................................................6

M2. Usage of appropriate techniques in order to produce financial reporting documents........10

D2. Financial reports to interpret business operational activities..............................................11

TASK 3..........................................................................................................................................11

P4. Distinct Kinds of planning tools..........................................................................................11

M3. Planning tools with application in order to prepare as well as forecasting budgets...........15

TASK 4..........................................................................................................................................16

P5. Comparison showing the ways organisations solve financial problems with the use of

accounting systems....................................................................................................................16

M4. Responding of management accounting towards financial problems for sustainable

success........................................................................................................................................18

D3. Planning tools usage to respond towards solving financial problems so to lead the

organisation towards sustainable success..................................................................................18

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

INTRODUCTION

Management accounting helps accountants to emphasise towards numerous events that

occurs in financial year while performing business activities (Bennett and James, 2017). By

using management accounting, financial department presents accounting information to

managers so that policies can be framed to attain main goals. Management Accounting performs

a main role in organisations now a days and thus stakeholders in the organisation need to know

how to generate and use excellent accounting information systems. It is used for assisting daily

operations along with performing managerial functions. It describes accounting techniques,

methods together with systems with ability as well as specialised information to minimise losses

addition to maximising profits. In today's company setting, company intends to monitor market

data that extends further than the price-based data supplied by traditional financial accounting

data from historical general ledger systems like Cost volume profit, budgetary control, cash

budget, marginal costing and absorption costing to make applicable management accounting

reports for informed decision making. To develop understanding about management accounting,

selected organisation ABC limited which is a medium sized manufacturing company. To

promote their different departments require to understand of different business activities and

apply all the appropriate systems and reports. The present report involves information related

with management accounting together with its accounting systems, reports addition to

techniques. It further includes distinct planning tools and comparison between two organisations

in the manner accounting systems are adopted to respond towards financial problems.

TASK 1

P1. Management accounting and accounting systems.

Management accounting: The concept that comprises procedures to analyse costs as

well as activities in order to construct financial reports together with maintaining records that

aids in decision making to attain organisational goals is characterised to management accounting.

It is mainly used for keeping records, financial planning, analysing sales trends, performance

management, controlling expenses and to make decisions (Brewer, Garrison and Noreen, 2015).

In context to ABC Ltd Company, managers uses it for systematic management planning together

with formulating strategic decisions.

1

Management accounting helps accountants to emphasise towards numerous events that

occurs in financial year while performing business activities (Bennett and James, 2017). By

using management accounting, financial department presents accounting information to

managers so that policies can be framed to attain main goals. Management Accounting performs

a main role in organisations now a days and thus stakeholders in the organisation need to know

how to generate and use excellent accounting information systems. It is used for assisting daily

operations along with performing managerial functions. It describes accounting techniques,

methods together with systems with ability as well as specialised information to minimise losses

addition to maximising profits. In today's company setting, company intends to monitor market

data that extends further than the price-based data supplied by traditional financial accounting

data from historical general ledger systems like Cost volume profit, budgetary control, cash

budget, marginal costing and absorption costing to make applicable management accounting

reports for informed decision making. To develop understanding about management accounting,

selected organisation ABC limited which is a medium sized manufacturing company. To

promote their different departments require to understand of different business activities and

apply all the appropriate systems and reports. The present report involves information related

with management accounting together with its accounting systems, reports addition to

techniques. It further includes distinct planning tools and comparison between two organisations

in the manner accounting systems are adopted to respond towards financial problems.

TASK 1

P1. Management accounting and accounting systems.

Management accounting: The concept that comprises procedures to analyse costs as

well as activities in order to construct financial reports together with maintaining records that

aids in decision making to attain organisational goals is characterised to management accounting.

It is mainly used for keeping records, financial planning, analysing sales trends, performance

management, controlling expenses and to make decisions (Brewer, Garrison and Noreen, 2015).

In context to ABC Ltd Company, managers uses it for systematic management planning together

with formulating strategic decisions.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management accounting systems: These are described to the systems that helps

managers to measure price level, observing statistical information and evaluating business

operations so to make decisions. These are confidential as well as aids to provide guidelines so

that overall efficiency and productivity are improved for betterment of an organisation. In ABC

Ltd Company, following management accounting systems are used to record and maintain

information related to actual performance of company. Detailed description of the systems are as

follows:

Cost accounting system: It is defined as the framework that is applied by accountants to

approximate cost of distinct products for purpose of profitability analysis, controlling costs

addition to inventory valuation. It is a kind of accounting that helps production department of

ABC Ltd Company to analyse and identify cost that are associated with meal kit boxes so that

ices are set accordingly to attain profitability (Busco and Quattrone, 2015). The system is

essentially required at the company as to reduce costs, controlling materials, recording

production transactions as well as maintaining profitable status.

Price optimisation system: With the use of mathematical analysis, price optimisation

system is used to determine perception of market towards prices of organisational products.

Under the system, administrators of ABC Ltd Company carefully understands customer

perceptions in order to set appropriate prices for distinct meal boxes that results in generating

more revenue. The essential requirement of the system is to determine prices that results in

maximising operating profits. This system mainly applied by the organisation to set effective

price structure in which price provide products to the customers. It helps to understand the

perception of customer regarding to different price of the products.

Job costing system: Another accounting system is job costing system in which

manufacturing costs are allocated to individual jobs or specific product. It encompasses

procedures to accumulate information on costs associated with specific service or job. By using

job order costing, production managers of ABC Ltd company calculates profits by collecting

costs as well as controls operational efficiencies. The system helps in providing accurate

valuation in context to work in progress. The system is essentially required at company as to

accumulate reliable estimates about direct information labour, overhead addition to direct

material.

2

managers to measure price level, observing statistical information and evaluating business

operations so to make decisions. These are confidential as well as aids to provide guidelines so

that overall efficiency and productivity are improved for betterment of an organisation. In ABC

Ltd Company, following management accounting systems are used to record and maintain

information related to actual performance of company. Detailed description of the systems are as

follows:

Cost accounting system: It is defined as the framework that is applied by accountants to

approximate cost of distinct products for purpose of profitability analysis, controlling costs

addition to inventory valuation. It is a kind of accounting that helps production department of

ABC Ltd Company to analyse and identify cost that are associated with meal kit boxes so that

ices are set accordingly to attain profitability (Busco and Quattrone, 2015). The system is

essentially required at the company as to reduce costs, controlling materials, recording

production transactions as well as maintaining profitable status.

Price optimisation system: With the use of mathematical analysis, price optimisation

system is used to determine perception of market towards prices of organisational products.

Under the system, administrators of ABC Ltd Company carefully understands customer

perceptions in order to set appropriate prices for distinct meal boxes that results in generating

more revenue. The essential requirement of the system is to determine prices that results in

maximising operating profits. This system mainly applied by the organisation to set effective

price structure in which price provide products to the customers. It helps to understand the

perception of customer regarding to different price of the products.

Job costing system: Another accounting system is job costing system in which

manufacturing costs are allocated to individual jobs or specific product. It encompasses

procedures to accumulate information on costs associated with specific service or job. By using

job order costing, production managers of ABC Ltd company calculates profits by collecting

costs as well as controls operational efficiencies. The system helps in providing accurate

valuation in context to work in progress. The system is essentially required at company as to

accumulate reliable estimates about direct information labour, overhead addition to direct

material.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inventory management system: The system which is aggregation of barcode scanners,

technological devices, desktop software along with barcode printers in order to streamline

management of inventory at workplace. Using such system, the management of ABC Ltd

Company tracks inventory positions so to eliminate any overstock or under stock conditions. By

effectively tracking quantities across warehouses, managers are capable to make inventory

decisions in efficient manner. Such system is further classified into LIFO, FIFO together with

Weighted average methods. Essential requirements of the system at the company is to record,

manage and track inventory materials together with reducing shortages, improving timely

delivery as well as maintaining surplus stock (Charifzadeh and Taschner, 2017).

Thus, all the elaborated accounting systems are used by ABC Ltd Company managers as

to analyse performances and formulating strategies accordingly so to achieve higher profits.

P2. Methods in management accounting reports.

Management accounting reporting plays valuable function in protecting business and

analysing its performance. Such reports are prepared as per the requirements in the bookkeeping

period. These reports provides significant information about various transactions or activities

addition to making profits. It is crucial for management team to adopt appropriate methods for

preparation of distinct reports after analysing gains and expenditures made by company. In

context to ABC Ltd Company, distinct accounting reports are prepared by departmental heads

with the objective to track operational activities and recording them so to submit the same to top

managers. Certain methods that are adopted by departmental heads of selected company to

generate accounting reports are the following:

Budget reports: One of the fundamental report is budget report a it helps in

understanding as well as controlling costs so to measure business performances. Using budget

report, actual results are compared with pre established budget in order to determine the

expenses. Budgetary report is used by administrators to determine the use of monetary resources

in effective manner. The activities of ABC Ltd Company such as production, marketing and

sales are recorded in such report. By considering the budget reports, all the transactions are

performed within set budgetary amounts so that measuring performance becomes easy for

departmental heads and managers.

Performance reports: It is prepared with the aim to keep record of organisational

performances in distinct time frame. Using performance reports, managers of any entity provides

3

technological devices, desktop software along with barcode printers in order to streamline

management of inventory at workplace. Using such system, the management of ABC Ltd

Company tracks inventory positions so to eliminate any overstock or under stock conditions. By

effectively tracking quantities across warehouses, managers are capable to make inventory

decisions in efficient manner. Such system is further classified into LIFO, FIFO together with

Weighted average methods. Essential requirements of the system at the company is to record,

manage and track inventory materials together with reducing shortages, improving timely

delivery as well as maintaining surplus stock (Charifzadeh and Taschner, 2017).

Thus, all the elaborated accounting systems are used by ABC Ltd Company managers as

to analyse performances and formulating strategies accordingly so to achieve higher profits.

P2. Methods in management accounting reports.

Management accounting reporting plays valuable function in protecting business and

analysing its performance. Such reports are prepared as per the requirements in the bookkeeping

period. These reports provides significant information about various transactions or activities

addition to making profits. It is crucial for management team to adopt appropriate methods for

preparation of distinct reports after analysing gains and expenditures made by company. In

context to ABC Ltd Company, distinct accounting reports are prepared by departmental heads

with the objective to track operational activities and recording them so to submit the same to top

managers. Certain methods that are adopted by departmental heads of selected company to

generate accounting reports are the following:

Budget reports: One of the fundamental report is budget report a it helps in

understanding as well as controlling costs so to measure business performances. Using budget

report, actual results are compared with pre established budget in order to determine the

expenses. Budgetary report is used by administrators to determine the use of monetary resources

in effective manner. The activities of ABC Ltd Company such as production, marketing and

sales are recorded in such report. By considering the budget reports, all the transactions are

performed within set budgetary amounts so that measuring performance becomes easy for

departmental heads and managers.

Performance reports: It is prepared with the aim to keep record of organisational

performances in distinct time frame. Using performance reports, managers of any entity provides

3

bonus together with incentives to work force as per the efforts that are made by them towards

accomplishing business objectives (Cooper, 2017). It benefits administrators of Guosto Company

to analyse performances of employees and determine which individual is performing well

addition to which one not. High performers are awarded more where as under performers are

provided more training programs. Performance accounting reports provides in depth information

about business workings and its capacity.

Inventory management report: Organisations manufactures physical products and

inventory management reports plays important function in centralising data associated on

inventory costs or other overheads that are involved in providing raw material as well as

production processes. Such report is a customized report that involves information about

supplier, location and product. This report all over the information such as how much raw

material come in the firm and on which date and how much take for the manufacturing

procedure. So with the help of this report take detailed information about the raw material and

understand how to take help from this report. It provides detailed information how much material

remain in the warehouse and in which stage require more material for further procedure.

Account receivable report: The report that is used to record credit sales as well as

analysing due payments in the accounting period. It is generally opted by the entities that

performs operations in credit terms and record all credit transaction in systematic manner along

with date, creditors name and amount (Eterno and Silverman, 2017). Reason behind preparing

account receivable report at ABC Ltd company is to list out unused credit memos together with

unpaid customer invoices as to determine nature of invoices that are overdue for payments. It is

used by top management of the company to ascertain effectiveness of collection as well as credit

functions. Selected organisation uses accounting software system in order to reconfigure report

in context to distinct data ranges.

Thus, the above stated management accounting reports are used by administrators of

ABC Ltd Company in order to manage inventory, knowing performances, working within set

budget as well as recording details of unpaid customers. All these reports helps in maintaining

efficiency together with formulating appropriate decisions so to grab opportunities.

M1. Benefits of management accounting systems

Management accounting with benefits: There are defined the different benefits of the

particular system that help to conduct the business activities smoothly and easily take decision

4

accomplishing business objectives (Cooper, 2017). It benefits administrators of Guosto Company

to analyse performances of employees and determine which individual is performing well

addition to which one not. High performers are awarded more where as under performers are

provided more training programs. Performance accounting reports provides in depth information

about business workings and its capacity.

Inventory management report: Organisations manufactures physical products and

inventory management reports plays important function in centralising data associated on

inventory costs or other overheads that are involved in providing raw material as well as

production processes. Such report is a customized report that involves information about

supplier, location and product. This report all over the information such as how much raw

material come in the firm and on which date and how much take for the manufacturing

procedure. So with the help of this report take detailed information about the raw material and

understand how to take help from this report. It provides detailed information how much material

remain in the warehouse and in which stage require more material for further procedure.

Account receivable report: The report that is used to record credit sales as well as

analysing due payments in the accounting period. It is generally opted by the entities that

performs operations in credit terms and record all credit transaction in systematic manner along

with date, creditors name and amount (Eterno and Silverman, 2017). Reason behind preparing

account receivable report at ABC Ltd company is to list out unused credit memos together with

unpaid customer invoices as to determine nature of invoices that are overdue for payments. It is

used by top management of the company to ascertain effectiveness of collection as well as credit

functions. Selected organisation uses accounting software system in order to reconfigure report

in context to distinct data ranges.

Thus, the above stated management accounting reports are used by administrators of

ABC Ltd Company in order to manage inventory, knowing performances, working within set

budget as well as recording details of unpaid customers. All these reports helps in maintaining

efficiency together with formulating appropriate decisions so to grab opportunities.

M1. Benefits of management accounting systems

Management accounting with benefits: There are defined the different benefits of the

particular system that help to conduct the business activities smoothly and easily take decision

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

regarding to business. For this purpose require to understand the benefits of the system that

discussed below:

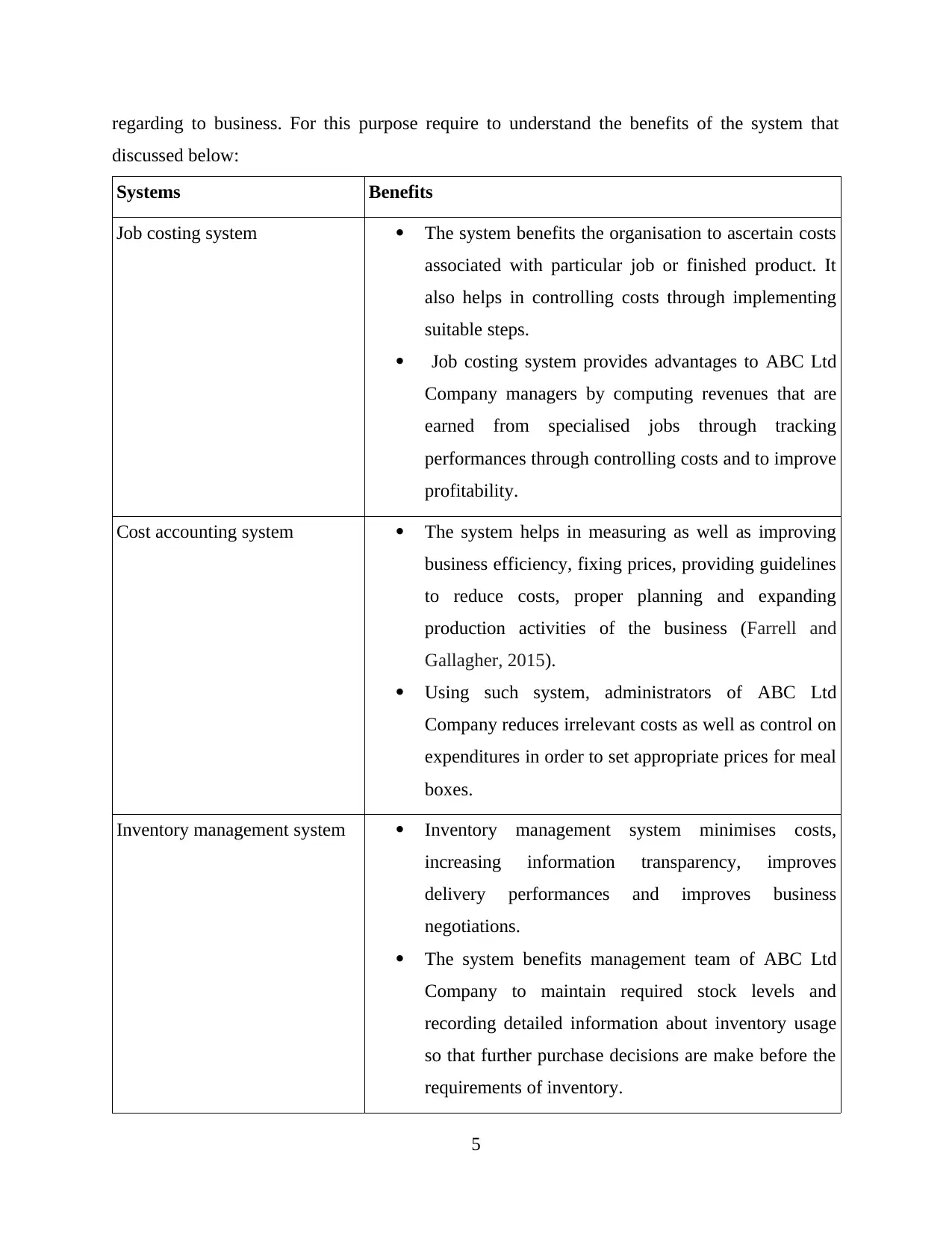

Systems Benefits

Job costing system The system benefits the organisation to ascertain costs

associated with particular job or finished product. It

also helps in controlling costs through implementing

suitable steps.

Job costing system provides advantages to ABC Ltd

Company managers by computing revenues that are

earned from specialised jobs through tracking

performances through controlling costs and to improve

profitability.

Cost accounting system The system helps in measuring as well as improving

business efficiency, fixing prices, providing guidelines

to reduce costs, proper planning and expanding

production activities of the business (Farrell and

Gallagher, 2015).

Using such system, administrators of ABC Ltd

Company reduces irrelevant costs as well as control on

expenditures in order to set appropriate prices for meal

boxes.

Inventory management system Inventory management system minimises costs,

increasing information transparency, improves

delivery performances and improves business

negotiations.

The system benefits management team of ABC Ltd

Company to maintain required stock levels and

recording detailed information about inventory usage

so that further purchase decisions are make before the

requirements of inventory.

5

discussed below:

Systems Benefits

Job costing system The system benefits the organisation to ascertain costs

associated with particular job or finished product. It

also helps in controlling costs through implementing

suitable steps.

Job costing system provides advantages to ABC Ltd

Company managers by computing revenues that are

earned from specialised jobs through tracking

performances through controlling costs and to improve

profitability.

Cost accounting system The system helps in measuring as well as improving

business efficiency, fixing prices, providing guidelines

to reduce costs, proper planning and expanding

production activities of the business (Farrell and

Gallagher, 2015).

Using such system, administrators of ABC Ltd

Company reduces irrelevant costs as well as control on

expenditures in order to set appropriate prices for meal

boxes.

Inventory management system Inventory management system minimises costs,

increasing information transparency, improves

delivery performances and improves business

negotiations.

The system benefits management team of ABC Ltd

Company to maintain required stock levels and

recording detailed information about inventory usage

so that further purchase decisions are make before the

requirements of inventory.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

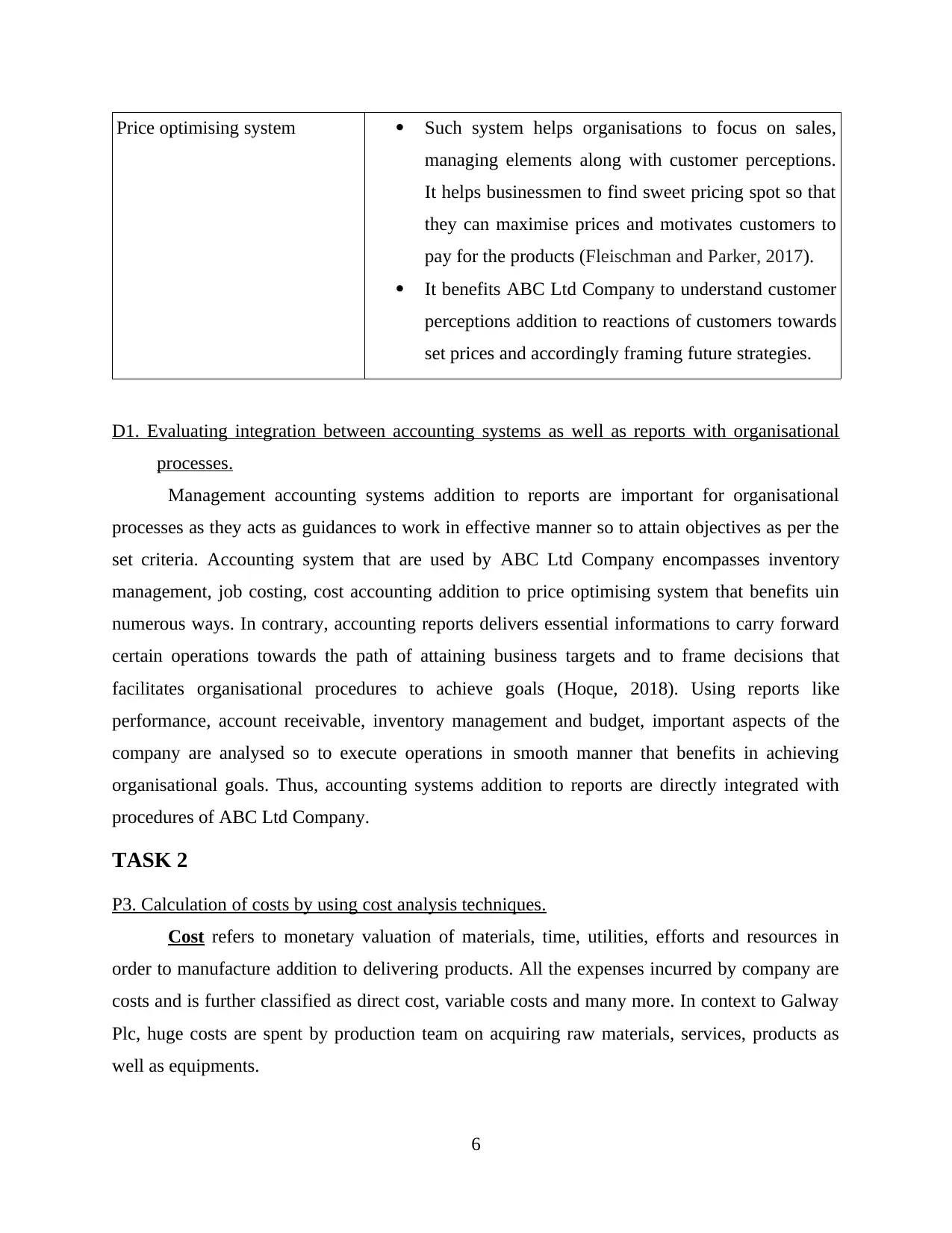

Price optimising system Such system helps organisations to focus on sales,

managing elements along with customer perceptions.

It helps businessmen to find sweet pricing spot so that

they can maximise prices and motivates customers to

pay for the products (Fleischman and Parker, 2017).

It benefits ABC Ltd Company to understand customer

perceptions addition to reactions of customers towards

set prices and accordingly framing future strategies.

D1. Evaluating integration between accounting systems as well as reports with organisational

processes.

Management accounting systems addition to reports are important for organisational

processes as they acts as guidances to work in effective manner so to attain objectives as per the

set criteria. Accounting system that are used by ABC Ltd Company encompasses inventory

management, job costing, cost accounting addition to price optimising system that benefits uin

numerous ways. In contrary, accounting reports delivers essential informations to carry forward

certain operations towards the path of attaining business targets and to frame decisions that

facilitates organisational procedures to achieve goals (Hoque, 2018). Using reports like

performance, account receivable, inventory management and budget, important aspects of the

company are analysed so to execute operations in smooth manner that benefits in achieving

organisational goals. Thus, accounting systems addition to reports are directly integrated with

procedures of ABC Ltd Company.

TASK 2

P3. Calculation of costs by using cost analysis techniques.

Cost refers to monetary valuation of materials, time, utilities, efforts and resources in

order to manufacture addition to delivering products. All the expenses incurred by company are

costs and is further classified as direct cost, variable costs and many more. In context to Galway

Plc, huge costs are spent by production team on acquiring raw materials, services, products as

well as equipments.

6

managing elements along with customer perceptions.

It helps businessmen to find sweet pricing spot so that

they can maximise prices and motivates customers to

pay for the products (Fleischman and Parker, 2017).

It benefits ABC Ltd Company to understand customer

perceptions addition to reactions of customers towards

set prices and accordingly framing future strategies.

D1. Evaluating integration between accounting systems as well as reports with organisational

processes.

Management accounting systems addition to reports are important for organisational

processes as they acts as guidances to work in effective manner so to attain objectives as per the

set criteria. Accounting system that are used by ABC Ltd Company encompasses inventory

management, job costing, cost accounting addition to price optimising system that benefits uin

numerous ways. In contrary, accounting reports delivers essential informations to carry forward

certain operations towards the path of attaining business targets and to frame decisions that

facilitates organisational procedures to achieve goals (Hoque, 2018). Using reports like

performance, account receivable, inventory management and budget, important aspects of the

company are analysed so to execute operations in smooth manner that benefits in achieving

organisational goals. Thus, accounting systems addition to reports are directly integrated with

procedures of ABC Ltd Company.

TASK 2

P3. Calculation of costs by using cost analysis techniques.

Cost refers to monetary valuation of materials, time, utilities, efforts and resources in

order to manufacture addition to delivering products. All the expenses incurred by company are

costs and is further classified as direct cost, variable costs and many more. In context to Galway

Plc, huge costs are spent by production team on acquiring raw materials, services, products as

well as equipments.

6

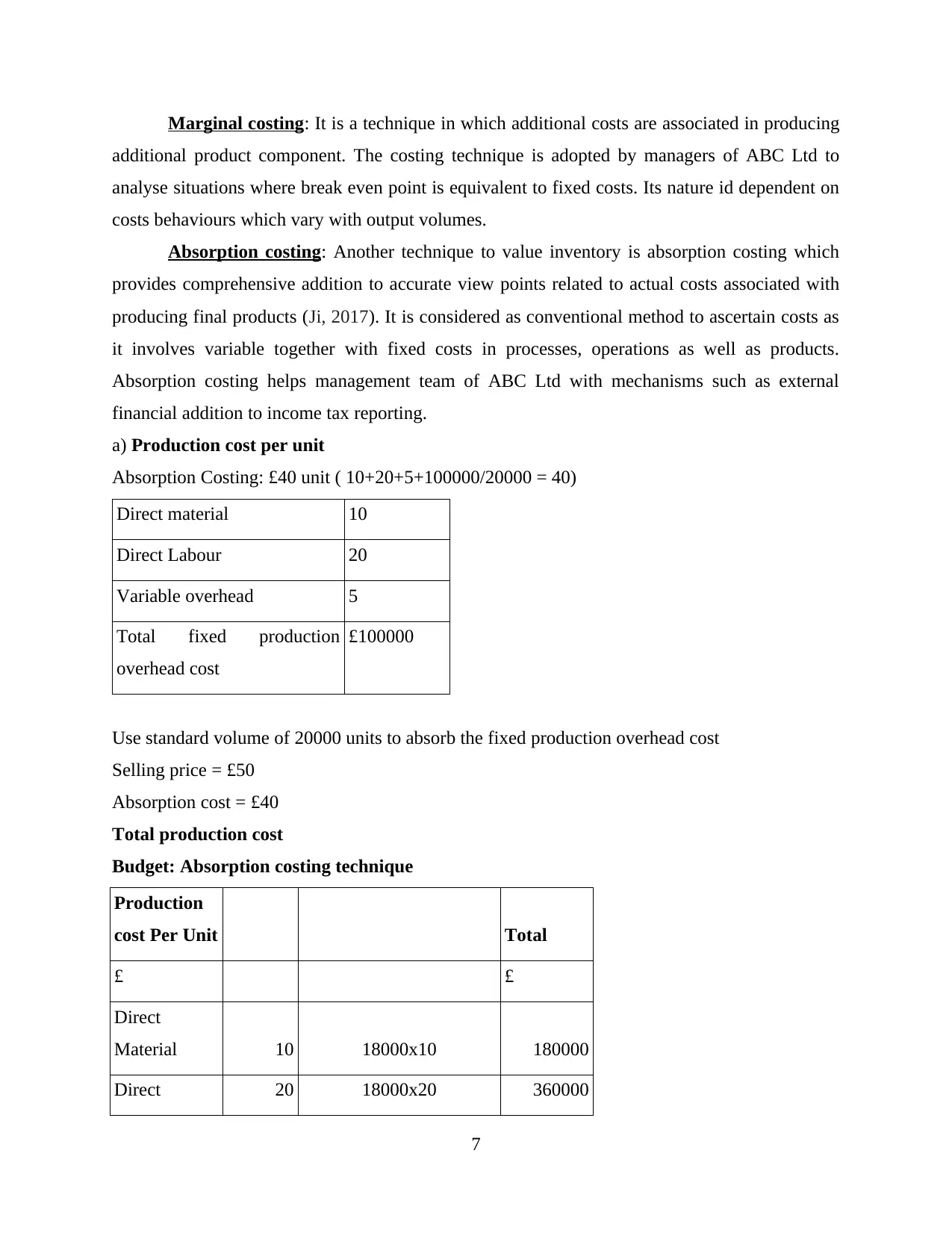

Marginal costing: It is a technique in which additional costs are associated in producing

additional product component. The costing technique is adopted by managers of ABC Ltd to

analyse situations where break even point is equivalent to fixed costs. Its nature id dependent on

costs behaviours which vary with output volumes.

Absorption costing: Another technique to value inventory is absorption costing which

provides comprehensive addition to accurate view points related to actual costs associated with

producing final products (Ji, 2017). It is considered as conventional method to ascertain costs as

it involves variable together with fixed costs in processes, operations as well as products.

Absorption costing helps management team of ABC Ltd with mechanisms such as external

financial addition to income tax reporting.

a) Production cost per unit

Absorption Costing: £40 unit ( 10+20+5+100000/20000 = 40)

Direct material 10

Direct Labour 20

Variable overhead 5

Total fixed production

overhead cost

£100000

Use standard volume of 20000 units to absorb the fixed production overhead cost

Selling price = £50

Absorption cost = £40

Total production cost

Budget: Absorption costing technique

Production

cost Per Unit Total

£ £

Direct

Material 10 18000x10 180000

Direct 20 18000x20 360000

7

additional product component. The costing technique is adopted by managers of ABC Ltd to

analyse situations where break even point is equivalent to fixed costs. Its nature id dependent on

costs behaviours which vary with output volumes.

Absorption costing: Another technique to value inventory is absorption costing which

provides comprehensive addition to accurate view points related to actual costs associated with

producing final products (Ji, 2017). It is considered as conventional method to ascertain costs as

it involves variable together with fixed costs in processes, operations as well as products.

Absorption costing helps management team of ABC Ltd with mechanisms such as external

financial addition to income tax reporting.

a) Production cost per unit

Absorption Costing: £40 unit ( 10+20+5+100000/20000 = 40)

Direct material 10

Direct Labour 20

Variable overhead 5

Total fixed production

overhead cost

£100000

Use standard volume of 20000 units to absorb the fixed production overhead cost

Selling price = £50

Absorption cost = £40

Total production cost

Budget: Absorption costing technique

Production

cost Per Unit Total

£ £

Direct

Material 10 18000x10 180000

Direct 20 18000x20 360000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

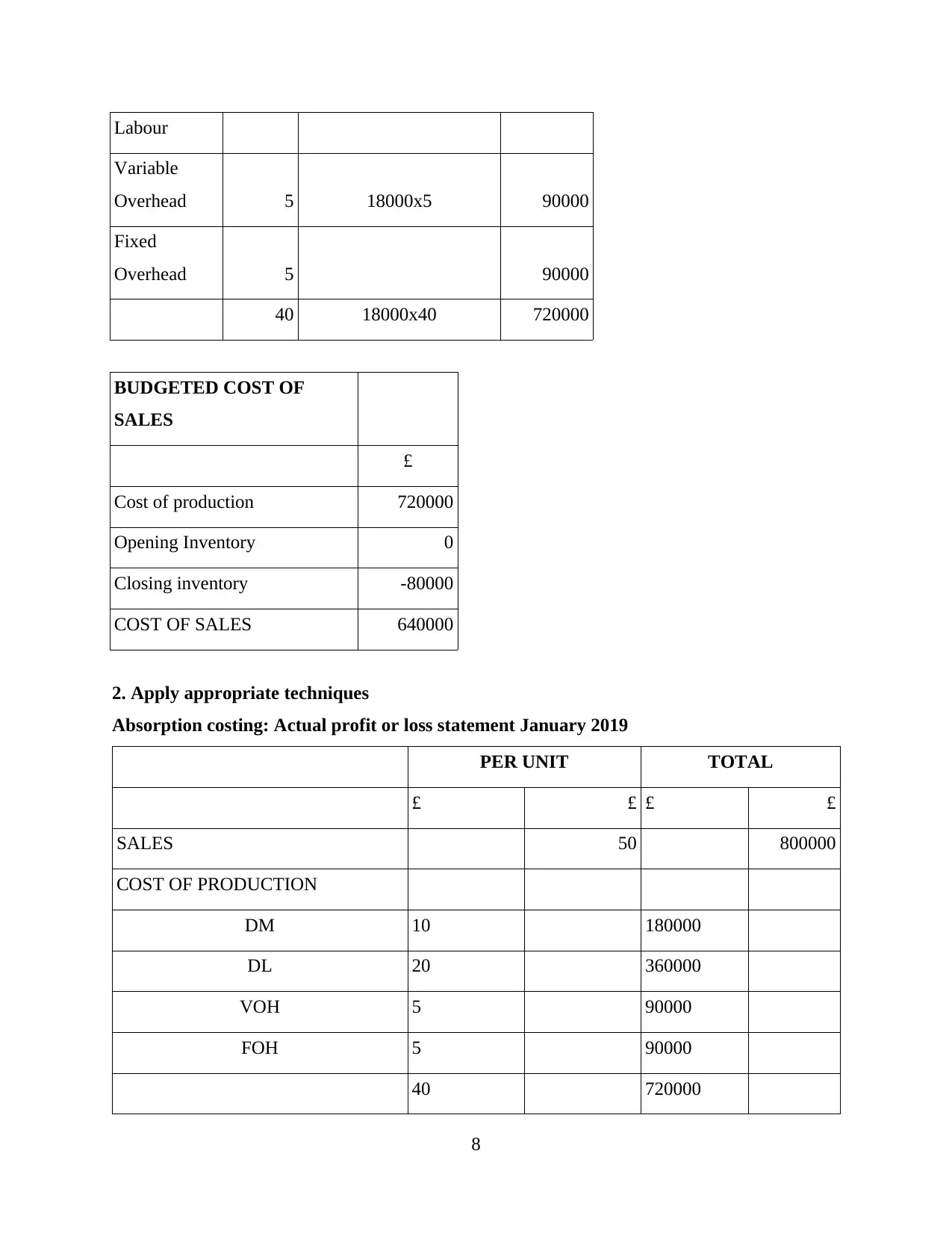

Labour

Variable

Overhead 5 18000x5 90000

Fixed

Overhead 5 90000

40 18000x40 720000

BUDGETED COST OF

SALES

£

Cost of production 720000

Opening Inventory 0

Closing inventory -80000

COST OF SALES 640000

2. Apply appropriate techniques

Absorption costing: Actual profit or loss statement January 2019

PER UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 180000

DL 20 360000

VOH 5 90000

FOH 5 90000

40 720000

8

Variable

Overhead 5 18000x5 90000

Fixed

Overhead 5 90000

40 18000x40 720000

BUDGETED COST OF

SALES

£

Cost of production 720000

Opening Inventory 0

Closing inventory -80000

COST OF SALES 640000

2. Apply appropriate techniques

Absorption costing: Actual profit or loss statement January 2019

PER UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 180000

DL 20 360000

VOH 5 90000

FOH 5 90000

40 720000

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

OPENING INVENTORY 0

CLOSING INVENTORY -80000

COST OF SALES -640000

STANDARD PROFIT 160000

ADJ. FOR UNDERABSORPTION -10000

BUDGETED PROFIT 150000

Absorption costing: Budgeted profit or loss statement January 2019

PER UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 190000

DL 20 380000

VOH 5 95000

FOH 5 95000

40 760000

OPENING INVENTORY 0

CLOSING INVENTORY -120000

COST OF SALES 40 -640000

STANDARD PROFIT 10 160000

ADJ. FOR UNDERABSORPTION -5000

BUDGETED PROFIT 155000

9

CLOSING INVENTORY -80000

COST OF SALES -640000

STANDARD PROFIT 160000

ADJ. FOR UNDERABSORPTION -10000

BUDGETED PROFIT 150000

Absorption costing: Budgeted profit or loss statement January 2019

PER UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 190000

DL 20 380000

VOH 5 95000

FOH 5 95000

40 760000

OPENING INVENTORY 0

CLOSING INVENTORY -120000

COST OF SALES 40 -640000

STANDARD PROFIT 10 160000

ADJ. FOR UNDERABSORPTION -5000

BUDGETED PROFIT 155000

9

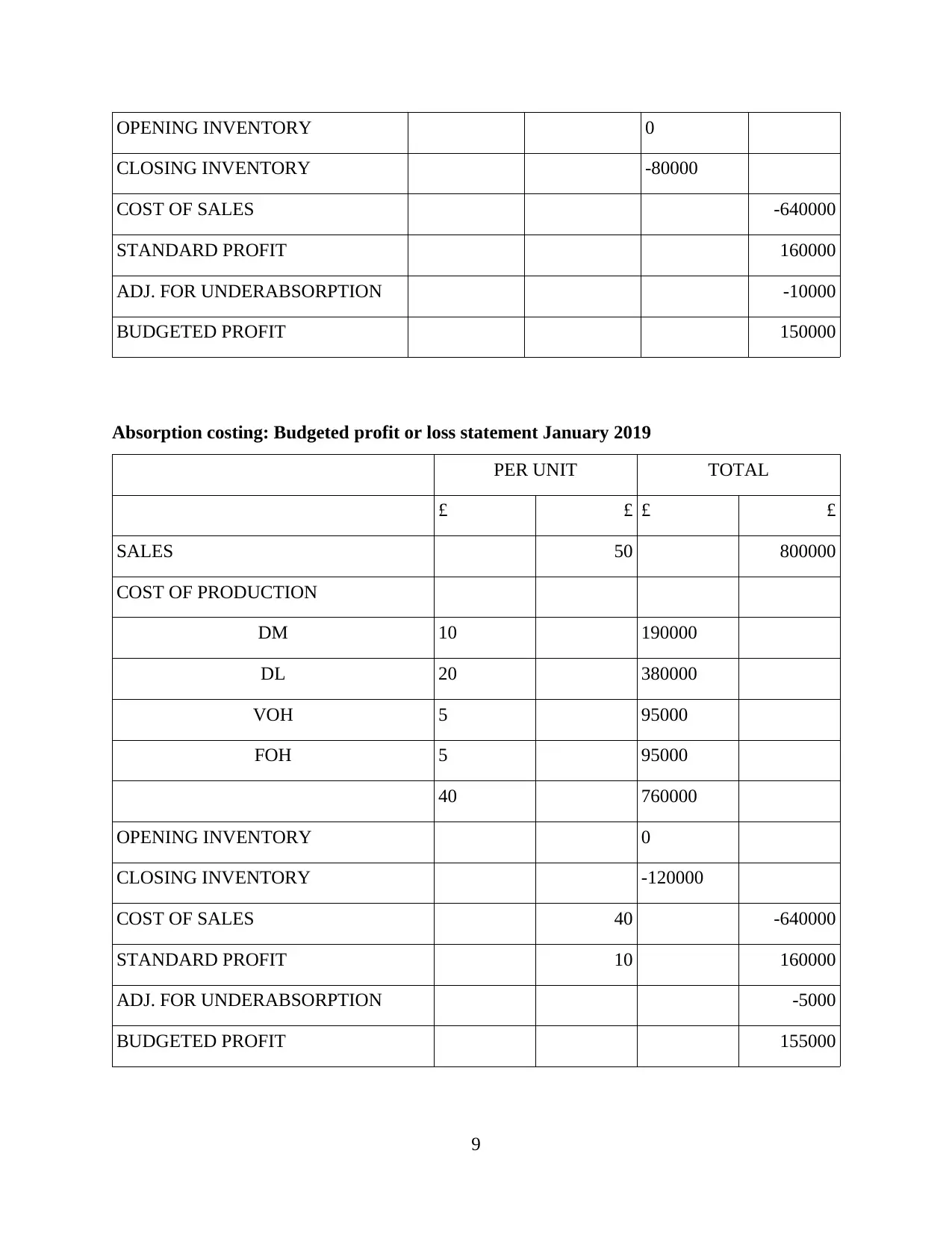

Marginal Costing: Actual Profit or Loss statement January 2019

PER UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 190000

DL 20 380000

VOH 5 95000

FOH 35 665000

OPENING INVENTORY 0

CLOSING INVENTORY -105000

COST OF SALES 35 560000

CONTRIBUTION 15 240000

FOH PRODUCTION -100000

BUDGETED PROFIT 140000

Marginal Costing: Budgeted Profit or Loss statement January 2019

PER UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 180000

DL 20 360000

VOH 5 90000

FOH 35 630000

10

PER UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 190000

DL 20 380000

VOH 5 95000

FOH 35 665000

OPENING INVENTORY 0

CLOSING INVENTORY -105000

COST OF SALES 35 560000

CONTRIBUTION 15 240000

FOH PRODUCTION -100000

BUDGETED PROFIT 140000

Marginal Costing: Budgeted Profit or Loss statement January 2019

PER UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 180000

DL 20 360000

VOH 5 90000

FOH 35 630000

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.