Management Accounting Systems and Techniques Report

VerifiedAdded on 2022/12/28

|17

|4199

|35

Report

AI Summary

This report delves into the realm of management accounting, providing a comprehensive analysis of its systems and techniques. It begins by defining management accounting and exploring its essential requirements, followed by an examination of various reporting methods, including budgetary reports, account receivable aging reports, cost reports, and performance reports. The report then proceeds to calculate costs using marginal and absorption costing methods, preparing income statements and conducting break-even analysis. Furthermore, it explains the advantages and disadvantages of different planning tools used for budgetary control, such as cash flow budgets. Finally, it discusses how organizations adapt management accounting systems to address financial challenges, offering insights into strategic decision-making and organizational performance. The report uses the case study of Connect Catering Services, a small to medium enterprise (SME) to explain key concepts and techniques.

Management

Accounting System and

Techniques

Accounting System and

Techniques

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................4

P1: Explain management accounting and give the essential requirements of different types of

management accounting systems................................................................................................4

P2: Explain different methods used for management accounting reporting...............................5

TASK 2............................................................................................................................................6

P3: Calculate cost using appropriate techniques of cost analysis to prepare an Income

Statement using Marginal and Absorption Costs........................................................................6

TASK 3..........................................................................................................................................12

P4: Explain the advantages and disadvantages of different types of planning tools used for

budgetary control......................................................................................................................12

TASK 4..........................................................................................................................................14

P5: Compare how organisations are adapting management accounting systems to respond to

financial problems.....................................................................................................................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................4

P1: Explain management accounting and give the essential requirements of different types of

management accounting systems................................................................................................4

P2: Explain different methods used for management accounting reporting...............................5

TASK 2............................................................................................................................................6

P3: Calculate cost using appropriate techniques of cost analysis to prepare an Income

Statement using Marginal and Absorption Costs........................................................................6

TASK 3..........................................................................................................................................12

P4: Explain the advantages and disadvantages of different types of planning tools used for

budgetary control......................................................................................................................12

TASK 4..........................................................................................................................................14

P5: Compare how organisations are adapting management accounting systems to respond to

financial problems.....................................................................................................................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

INTRODUCTION

Management accounting is a branch of accounting, that provides financial information to

the organisation so that they can make managerial decision. Management accounting is a

procedure of identifying, analysing, interpretation and communicating the information that leads

in achieving organisational goals (Campos and et. al, 2019). It uses all the functions of

management including planning, organising, staffing, direction and control. This accounting

provides information which is useful for the organisation. The objective of management

accounting is to use statistical data and take an accurate decision. Generally, it is used for

internal purpose and it is not regulated by any law.

Management Accounting helps the organisation to take important decisions related to the

functionality and management. This may include decisions like price determination, number of

units to be sold in order to earn profit or how much of a bonus can the company afford to give its

employees. This facilitates the business to run smoothly with extensive opportunities of growth

and expansion.

Management accounting is a combination of Management and Accounting, management

is an art of getting things done through people by motivating and influencing them in the right

direction on the other hand accounting is a process of identifying, recording, analysing and

presenting data in an effective way (Wen, 2020). Management accounting is accounting of such

data which can make people do the required task and take important planning decisions.

Connect Catering Services is a SME and a family owned business located at Oxfordshire.

The enterprise provides catering services. Connect Catering feels that the implementation of the

management accounting systems along with financial accounting systems would enable them to

strengthen its decision making which will help the enterprise to survive in the long run and in

this competitive market. In this report various management accounting system which are

essential while making organisational decisions. Various techniques of cost determination are

used and explained.

Management accounting is a branch of accounting, that provides financial information to

the organisation so that they can make managerial decision. Management accounting is a

procedure of identifying, analysing, interpretation and communicating the information that leads

in achieving organisational goals (Campos and et. al, 2019). It uses all the functions of

management including planning, organising, staffing, direction and control. This accounting

provides information which is useful for the organisation. The objective of management

accounting is to use statistical data and take an accurate decision. Generally, it is used for

internal purpose and it is not regulated by any law.

Management Accounting helps the organisation to take important decisions related to the

functionality and management. This may include decisions like price determination, number of

units to be sold in order to earn profit or how much of a bonus can the company afford to give its

employees. This facilitates the business to run smoothly with extensive opportunities of growth

and expansion.

Management accounting is a combination of Management and Accounting, management

is an art of getting things done through people by motivating and influencing them in the right

direction on the other hand accounting is a process of identifying, recording, analysing and

presenting data in an effective way (Wen, 2020). Management accounting is accounting of such

data which can make people do the required task and take important planning decisions.

Connect Catering Services is a SME and a family owned business located at Oxfordshire.

The enterprise provides catering services. Connect Catering feels that the implementation of the

management accounting systems along with financial accounting systems would enable them to

strengthen its decision making which will help the enterprise to survive in the long run and in

this competitive market. In this report various management accounting system which are

essential while making organisational decisions. Various techniques of cost determination are

used and explained.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 1

P1: Explain management accounting and give the essential requirements of different types

of management accounting systems.

Here management accounting system will be used to analyse the situation of Connect

Catering Services. Management accounting will enable Connect Catering Services to get

organisational reports and these reports will help it to make necessary changes and take required

decisions in the organisation itself and the management.

Management Accounting will provide the organisation with information about

manufacturing of services which will further help in preparing budgets which will aid in

improvement of management (VYSOCHAN and HYK, 2020).

Commonly used Management Accounting Systems are:

Cost Accounting System: It is one of the important system of management

accounting system. This system consists of various accounting techniques by

which the business can find cost of certain tasks and projects, with this they can

compare their profits with their costs and take necessary decisions and plan

accordingly. In context to Connect Caters Services, the company uses Cost

Accounting System with which they are able to manage all their relevant cost like

that of raw material, processes and of distribution of products.

Inventory Management System: This system has techniques that help the

management to maintain the level of stock. This system involves the process of

stocking and restocking the organisation's inventory so as to increase overall

sales as stock will be available when needed (Guo, 2019). Connect Caters

Services uses this system with its various techniques to manage inventory.

Techniques may include LIFO, FIFO, JIT and ABC analysis.

Job Costing System: Job costing system is a type of management accounting

system which is generally used by manufacturers (of goods and services both)

because accountant can easily estimate the cost of performing a every job. This

system will help the accountant in assessment of costs of every department

separately (de Lautour, 2019). The organisation assesses the cost required for

every job and running business activities. This information is of crucial use for

the managers to formulate trading strategies.

P1: Explain management accounting and give the essential requirements of different types

of management accounting systems.

Here management accounting system will be used to analyse the situation of Connect

Catering Services. Management accounting will enable Connect Catering Services to get

organisational reports and these reports will help it to make necessary changes and take required

decisions in the organisation itself and the management.

Management Accounting will provide the organisation with information about

manufacturing of services which will further help in preparing budgets which will aid in

improvement of management (VYSOCHAN and HYK, 2020).

Commonly used Management Accounting Systems are:

Cost Accounting System: It is one of the important system of management

accounting system. This system consists of various accounting techniques by

which the business can find cost of certain tasks and projects, with this they can

compare their profits with their costs and take necessary decisions and plan

accordingly. In context to Connect Caters Services, the company uses Cost

Accounting System with which they are able to manage all their relevant cost like

that of raw material, processes and of distribution of products.

Inventory Management System: This system has techniques that help the

management to maintain the level of stock. This system involves the process of

stocking and restocking the organisation's inventory so as to increase overall

sales as stock will be available when needed (Guo, 2019). Connect Caters

Services uses this system with its various techniques to manage inventory.

Techniques may include LIFO, FIFO, JIT and ABC analysis.

Job Costing System: Job costing system is a type of management accounting

system which is generally used by manufacturers (of goods and services both)

because accountant can easily estimate the cost of performing a every job. This

system will help the accountant in assessment of costs of every department

separately (de Lautour, 2019). The organisation assesses the cost required for

every job and running business activities. This information is of crucial use for

the managers to formulate trading strategies.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P2: Explain different methods used for management accounting reporting.

Management accounting reporting will aid the accountant to represent management

accounting information in an operative form which helps in taking important strategic decisions

for the smooth working of the organisation. This helps in highlighting the profitable operations

of the business so that they are easily visible to the stakeholders. This segment has various

techniques like inventory report, budgetary report, job costs report, account receivable ageing

report.

Budgetary Reports: Budget reports are important in measuring performance of a

company. Basically, budget reports are made for small companies but they are also used

in large-scale organisations as per the department. They are made on the basis of past

experiences and have power to give insight of future unfavourable situations. Budgets

are prepared on the basis of current expenditure and costs as compared to expected costs

and expenditure. Accounting reports that are related to budgets help managers to provide

with insight of more ways to earn profit, lowers cost and gives a chance of negotiation

with suppliers and stakeholders (Alam, Ranasinghe and Wickramasinghe, 2019). It will

enable Connect Cater Services to evaluate current performance with the expected

performance. With the budget report Connect Caters estimates the value of expected

profit and filter out activities that can become the cause of failure in achieving so. It also

helps in analysing new opportunities which are there in the market and also which will

arrive in the near future.

Account Receivable Ageing Report: Businesses that are dependent on credit sales have

account receivable ageing reports of great significance. It helps management in

identifying those account receivables who continue turning into bad debts and also helps

in finding problems in the process of collection. If it is found that there are many

defaulters then there is a need of regulating the policies of credit sales. It will help the

management to keep surveillance on the credit period of debtors and also the cash inflow

and outflow of the business. This will aid the enterprise to take decisions like that of

increasing or decreasing the credit period. Connect Cater Services forms policies that

will enable them in collecting amount from their debtors in time and with less Bad

Debts.

Management accounting reporting will aid the accountant to represent management

accounting information in an operative form which helps in taking important strategic decisions

for the smooth working of the organisation. This helps in highlighting the profitable operations

of the business so that they are easily visible to the stakeholders. This segment has various

techniques like inventory report, budgetary report, job costs report, account receivable ageing

report.

Budgetary Reports: Budget reports are important in measuring performance of a

company. Basically, budget reports are made for small companies but they are also used

in large-scale organisations as per the department. They are made on the basis of past

experiences and have power to give insight of future unfavourable situations. Budgets

are prepared on the basis of current expenditure and costs as compared to expected costs

and expenditure. Accounting reports that are related to budgets help managers to provide

with insight of more ways to earn profit, lowers cost and gives a chance of negotiation

with suppliers and stakeholders (Alam, Ranasinghe and Wickramasinghe, 2019). It will

enable Connect Cater Services to evaluate current performance with the expected

performance. With the budget report Connect Caters estimates the value of expected

profit and filter out activities that can become the cause of failure in achieving so. It also

helps in analysing new opportunities which are there in the market and also which will

arrive in the near future.

Account Receivable Ageing Report: Businesses that are dependent on credit sales have

account receivable ageing reports of great significance. It helps management in

identifying those account receivables who continue turning into bad debts and also helps

in finding problems in the process of collection. If it is found that there are many

defaulters then there is a need of regulating the policies of credit sales. It will help the

management to keep surveillance on the credit period of debtors and also the cash inflow

and outflow of the business. This will aid the enterprise to take decisions like that of

increasing or decreasing the credit period. Connect Cater Services forms policies that

will enable them in collecting amount from their debtors in time and with less Bad

Debts.

Cost Reports: Procurement of raw materials, labours, overheads are the costs for a

company. The total of these costs are divided by the amount of the produce. The cost

report has the information about the cost of items with the selling prices of the product.

Through this report companies decide upon the profit margins for their products. It will

help the manager to evaluate critical expenditure areas, and have a systematic analysis of

total costs involved in specific projects. Connect Caters' department of management

makes report to identifying the reason of excessive cash outflow or costs which are not

beneficial for the business.

Performance Reports: These are the reports that are made to review the performance of

an organisation and the workforce of a company. In large-scale organisations

performance reports of departments are also made (Rauscher and Zielke, 2019). These

reports are made to make decisions for the future of the company. Exceptional workers

who achieve targets on time and even exceed their goals are appreciated for their

performance in the organisation and under performers are given warning and also

motivation to work effectively. Connect Cater Services form performance report to

identify departments which are not working effectively and efficiently.

TASK 2

P3: Calculate cost using appropriate techniques of cost analysis to prepare an Income

Statement using Marginal and Absorption Costs.

company. The total of these costs are divided by the amount of the produce. The cost

report has the information about the cost of items with the selling prices of the product.

Through this report companies decide upon the profit margins for their products. It will

help the manager to evaluate critical expenditure areas, and have a systematic analysis of

total costs involved in specific projects. Connect Caters' department of management

makes report to identifying the reason of excessive cash outflow or costs which are not

beneficial for the business.

Performance Reports: These are the reports that are made to review the performance of

an organisation and the workforce of a company. In large-scale organisations

performance reports of departments are also made (Rauscher and Zielke, 2019). These

reports are made to make decisions for the future of the company. Exceptional workers

who achieve targets on time and even exceed their goals are appreciated for their

performance in the organisation and under performers are given warning and also

motivation to work effectively. Connect Cater Services form performance report to

identify departments which are not working effectively and efficiently.

TASK 2

P3: Calculate cost using appropriate techniques of cost analysis to prepare an Income

Statement using Marginal and Absorption Costs.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

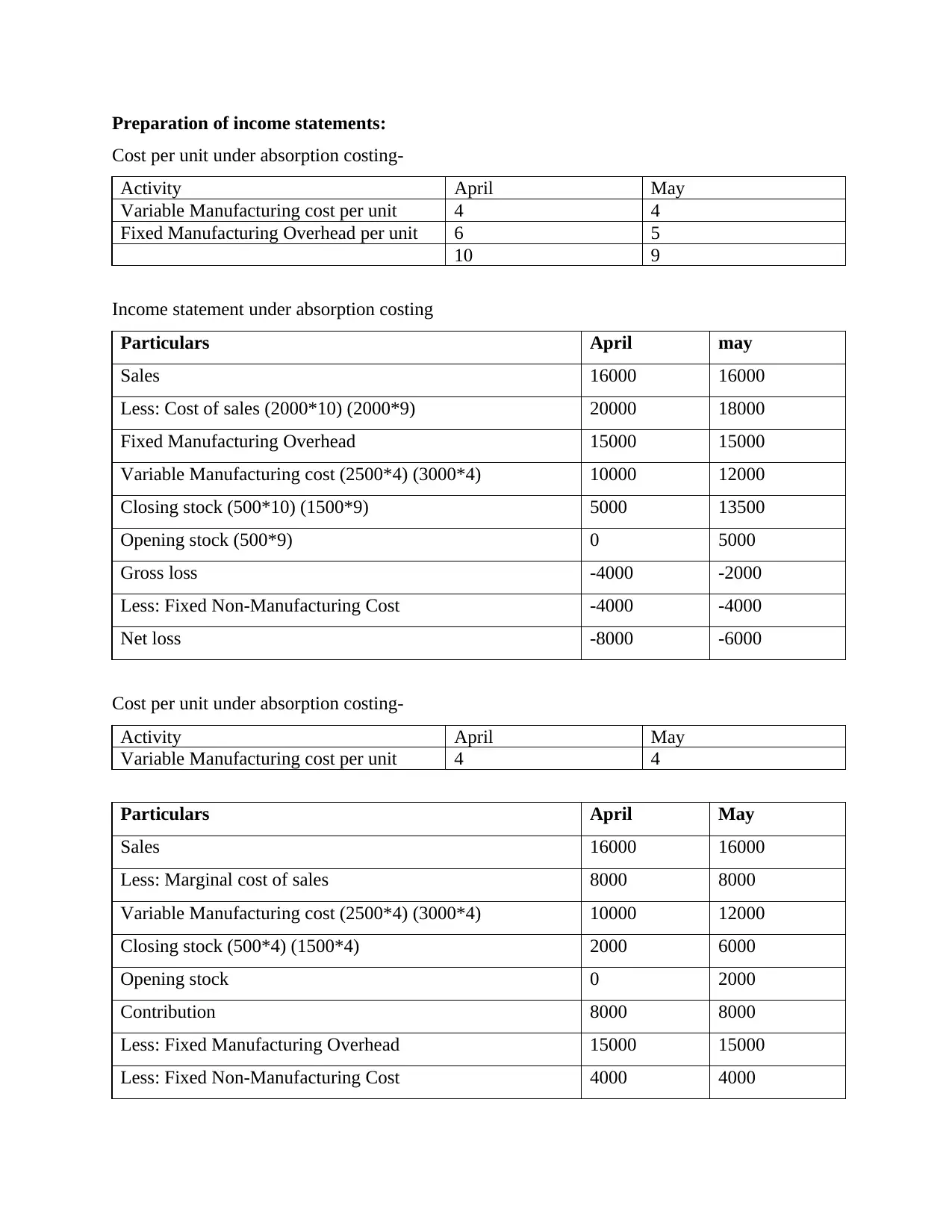

Preparation of income statements:

Cost per unit under absorption costing-

Activity April May

Variable Manufacturing cost per unit 4 4

Fixed Manufacturing Overhead per unit 6 5

10 9

Income statement under absorption costing

Particulars April may

Sales 16000 16000

Less: Cost of sales (2000*10) (2000*9) 20000 18000

Fixed Manufacturing Overhead 15000 15000

Variable Manufacturing cost (2500*4) (3000*4) 10000 12000

Closing stock (500*10) (1500*9) 5000 13500

Opening stock (500*9) 0 5000

Gross loss -4000 -2000

Less: Fixed Non-Manufacturing Cost -4000 -4000

Net loss -8000 -6000

Cost per unit under absorption costing-

Activity April May

Variable Manufacturing cost per unit 4 4

Particulars April May

Sales 16000 16000

Less: Marginal cost of sales 8000 8000

Variable Manufacturing cost (2500*4) (3000*4) 10000 12000

Closing stock (500*4) (1500*4) 2000 6000

Opening stock 0 2000

Contribution 8000 8000

Less: Fixed Manufacturing Overhead 15000 15000

Less: Fixed Non-Manufacturing Cost 4000 4000

Cost per unit under absorption costing-

Activity April May

Variable Manufacturing cost per unit 4 4

Fixed Manufacturing Overhead per unit 6 5

10 9

Income statement under absorption costing

Particulars April may

Sales 16000 16000

Less: Cost of sales (2000*10) (2000*9) 20000 18000

Fixed Manufacturing Overhead 15000 15000

Variable Manufacturing cost (2500*4) (3000*4) 10000 12000

Closing stock (500*10) (1500*9) 5000 13500

Opening stock (500*9) 0 5000

Gross loss -4000 -2000

Less: Fixed Non-Manufacturing Cost -4000 -4000

Net loss -8000 -6000

Cost per unit under absorption costing-

Activity April May

Variable Manufacturing cost per unit 4 4

Particulars April May

Sales 16000 16000

Less: Marginal cost of sales 8000 8000

Variable Manufacturing cost (2500*4) (3000*4) 10000 12000

Closing stock (500*4) (1500*4) 2000 6000

Opening stock 0 2000

Contribution 8000 8000

Less: Fixed Manufacturing Overhead 15000 15000

Less: Fixed Non-Manufacturing Cost 4000 4000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

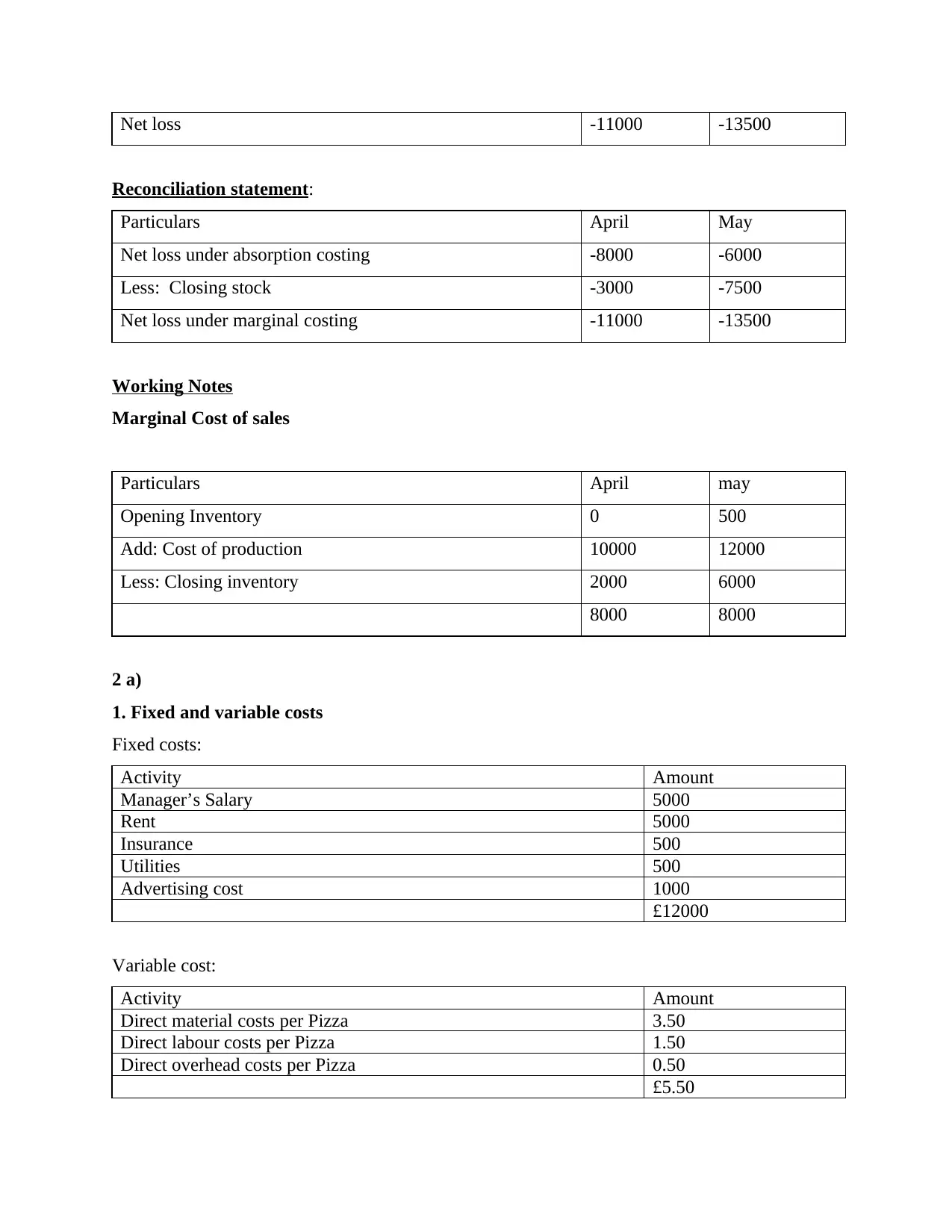

Net loss -11000 -13500

Reconciliation statement:

Particulars April May

Net loss under absorption costing -8000 -6000

Less: Closing stock -3000 -7500

Net loss under marginal costing -11000 -13500

Working Notes

Marginal Cost of sales

Particulars April may

Opening Inventory 0 500

Add: Cost of production 10000 12000

Less: Closing inventory 2000 6000

8000 8000

2 a)

1. Fixed and variable costs

Fixed costs:

Activity Amount

Manager’s Salary 5000

Rent 5000

Insurance 500

Utilities 500

Advertising cost 1000

£12000

Variable cost:

Activity Amount

Direct material costs per Pizza 3.50

Direct labour costs per Pizza 1.50

Direct overhead costs per Pizza 0.50

£5.50

Reconciliation statement:

Particulars April May

Net loss under absorption costing -8000 -6000

Less: Closing stock -3000 -7500

Net loss under marginal costing -11000 -13500

Working Notes

Marginal Cost of sales

Particulars April may

Opening Inventory 0 500

Add: Cost of production 10000 12000

Less: Closing inventory 2000 6000

8000 8000

2 a)

1. Fixed and variable costs

Fixed costs:

Activity Amount

Manager’s Salary 5000

Rent 5000

Insurance 500

Utilities 500

Advertising cost 1000

£12000

Variable cost:

Activity Amount

Direct material costs per Pizza 3.50

Direct labour costs per Pizza 1.50

Direct overhead costs per Pizza 0.50

£5.50

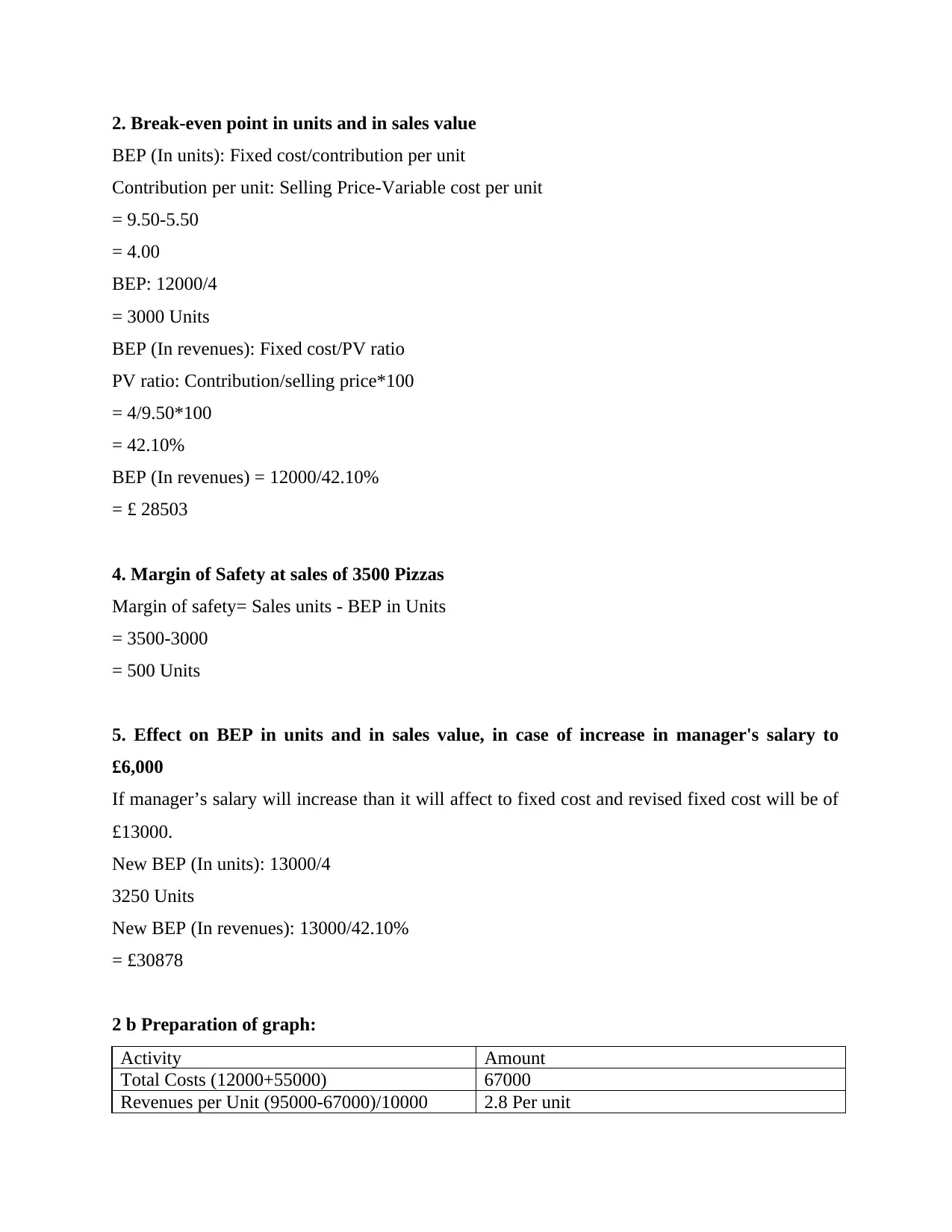

2. Break-even point in units and in sales value

BEP (In units): Fixed cost/contribution per unit

Contribution per unit: Selling Price-Variable cost per unit

= 9.50-5.50

= 4.00

BEP: 12000/4

= 3000 Units

BEP (In revenues): Fixed cost/PV ratio

PV ratio: Contribution/selling price*100

= 4/9.50*100

= 42.10%

BEP (In revenues) = 12000/42.10%

= £ 28503

4. Margin of Safety at sales of 3500 Pizzas

Margin of safety= Sales units - BEP in Units

= 3500-3000

= 500 Units

5. Effect on BEP in units and in sales value, in case of increase in manager's salary to

£6,000

If manager’s salary will increase than it will affect to fixed cost and revised fixed cost will be of

£13000.

New BEP (In units): 13000/4

3250 Units

New BEP (In revenues): 13000/42.10%

= £30878

2 b Preparation of graph:

Activity Amount

Total Costs (12000+55000) 67000

Revenues per Unit (95000-67000)/10000 2.8 Per unit

BEP (In units): Fixed cost/contribution per unit

Contribution per unit: Selling Price-Variable cost per unit

= 9.50-5.50

= 4.00

BEP: 12000/4

= 3000 Units

BEP (In revenues): Fixed cost/PV ratio

PV ratio: Contribution/selling price*100

= 4/9.50*100

= 42.10%

BEP (In revenues) = 12000/42.10%

= £ 28503

4. Margin of Safety at sales of 3500 Pizzas

Margin of safety= Sales units - BEP in Units

= 3500-3000

= 500 Units

5. Effect on BEP in units and in sales value, in case of increase in manager's salary to

£6,000

If manager’s salary will increase than it will affect to fixed cost and revised fixed cost will be of

£13000.

New BEP (In units): 13000/4

3250 Units

New BEP (In revenues): 13000/42.10%

= £30878

2 b Preparation of graph:

Activity Amount

Total Costs (12000+55000) 67000

Revenues per Unit (95000-67000)/10000 2.8 Per unit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

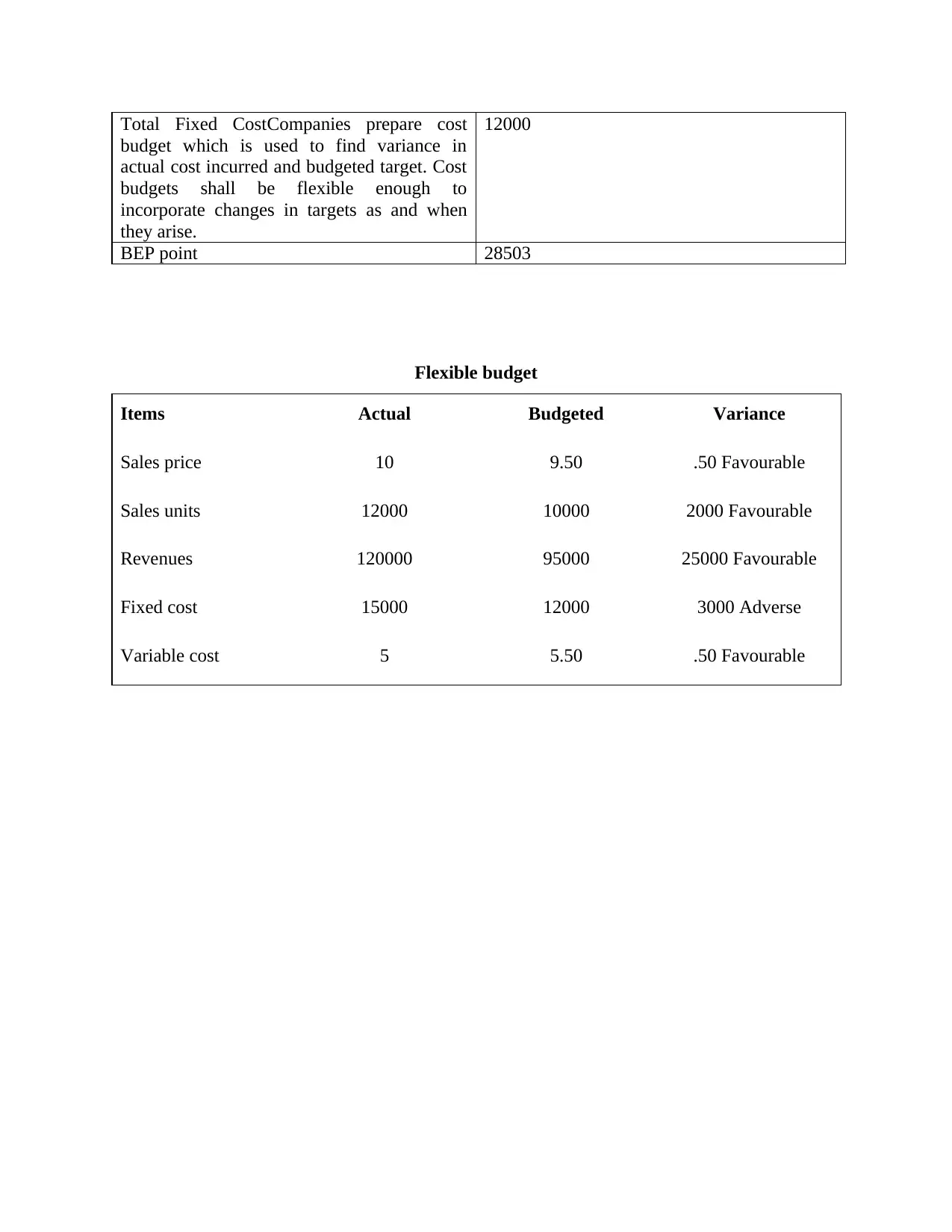

Total Fixed CostCompanies prepare cost

budget which is used to find variance in

actual cost incurred and budgeted target. Cost

budgets shall be flexible enough to

incorporate changes in targets as and when

they arise.

12000

BEP point 28503

Flexible budget

Items Actual Budgeted Variance

Sales price 10 9.50 .50 Favourable

Sales units 12000 10000 2000 Favourable

Revenues 120000 95000 25000 Favourable

Fixed cost 15000 12000 3000 Adverse

Variable cost 5 5.50 .50 Favourable

budget which is used to find variance in

actual cost incurred and budgeted target. Cost

budgets shall be flexible enough to

incorporate changes in targets as and when

they arise.

12000

BEP point 28503

Flexible budget

Items Actual Budgeted Variance

Sales price 10 9.50 .50 Favourable

Sales units 12000 10000 2000 Favourable

Revenues 120000 95000 25000 Favourable

Fixed cost 15000 12000 3000 Adverse

Variable cost 5 5.50 .50 Favourable

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

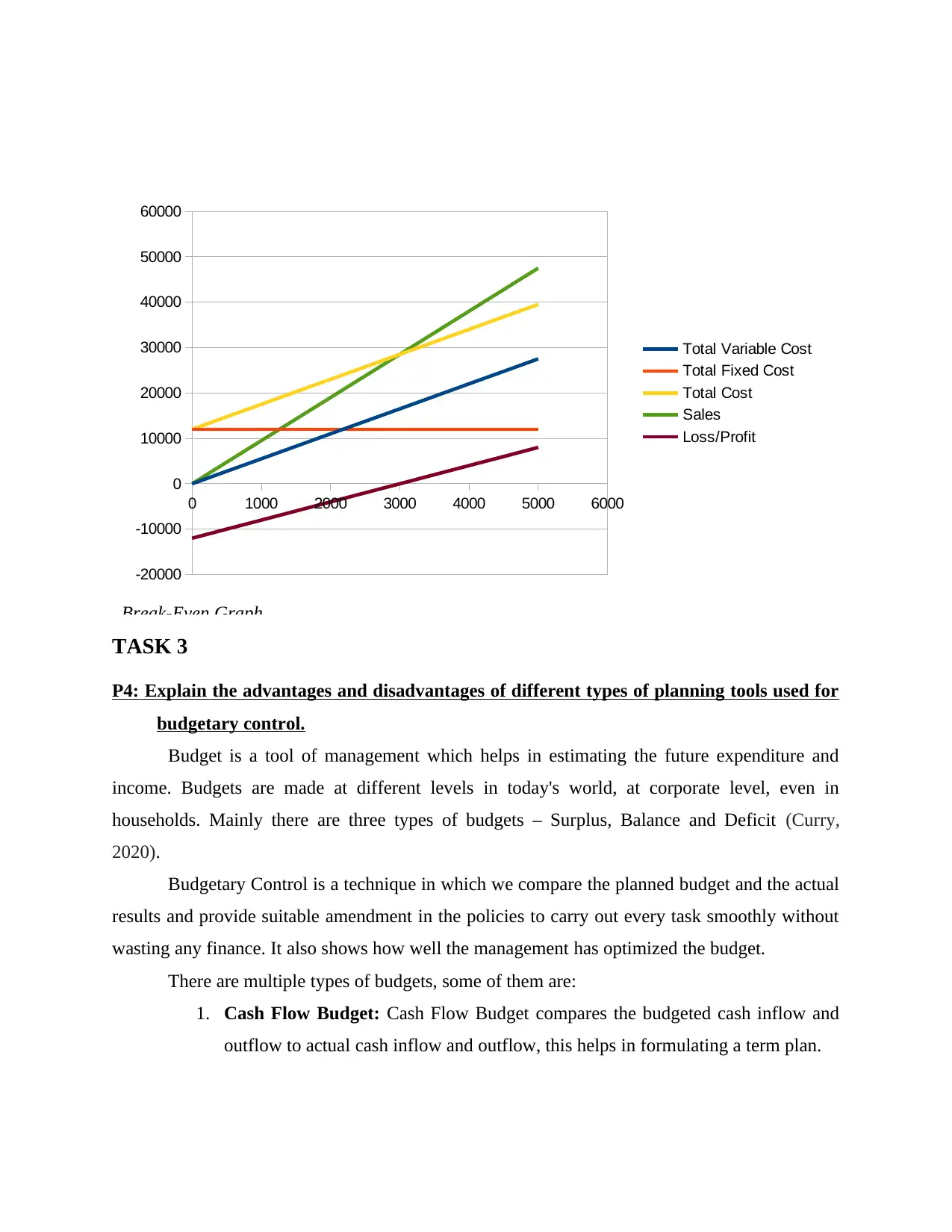

0 1000 2000 3000 4000 5000 6000

-20000

-10000

0

10000

20000

30000

40000

50000

60000

Total Variable Cost

Total Fixed Cost

Total Cost

Sales

Loss/Profit

Break-Even Graph

TASK 3

P4: Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.

Budget is a tool of management which helps in estimating the future expenditure and

income. Budgets are made at different levels in today's world, at corporate level, even in

households. Mainly there are three types of budgets – Surplus, Balance and Deficit (Curry,

2020).

Budgetary Control is a technique in which we compare the planned budget and the actual

results and provide suitable amendment in the policies to carry out every task smoothly without

wasting any finance. It also shows how well the management has optimized the budget.

There are multiple types of budgets, some of them are:

1. Cash Flow Budget: Cash Flow Budget compares the budgeted cash inflow and

outflow to actual cash inflow and outflow, this helps in formulating a term plan.

-20000

-10000

0

10000

20000

30000

40000

50000

60000

Total Variable Cost

Total Fixed Cost

Total Cost

Sales

Loss/Profit

Break-Even Graph

TASK 3

P4: Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.

Budget is a tool of management which helps in estimating the future expenditure and

income. Budgets are made at different levels in today's world, at corporate level, even in

households. Mainly there are three types of budgets – Surplus, Balance and Deficit (Curry,

2020).

Budgetary Control is a technique in which we compare the planned budget and the actual

results and provide suitable amendment in the policies to carry out every task smoothly without

wasting any finance. It also shows how well the management has optimized the budget.

There are multiple types of budgets, some of them are:

1. Cash Flow Budget: Cash Flow Budget compares the budgeted cash inflow and

outflow to actual cash inflow and outflow, this helps in formulating a term plan.

Advantage: Cash budgets helps the management in minimising unnecessary expenditure, so the

business is able to manage its finances and use it effectively. Cash flow budget helps predicting

seasonal fluctuations where shortage and surplus cash can be avoided.

Disadvantage: While creating cash flow budget non-financial and non-cash factors are excluded.

When the business has to choose from one of the two financial institution from where it can

incur debt; where one institution may offer low interest rate and other may offer better services.

In cash flow budget non-financial perks are not recorded.

2. Flexible Budget: It is a budget which is flexible and dynamic as per the volume

and activity. In this budget, the budgeted amount changes and varies according to

the situation. This budget is also known as variable budget because it includes

variable factors like variable factor cost rather than static ones (Giovanni and et.

al, 2019).

Advantage: It helps in assessing the efficiency of the departmental head. It control overheads and

help in revaluation of the budget at every level.

Disadvantage: This budget requires skilled workers, therefore it becomes a challenge for the

business to find skilled human resource and it requires a lot of resources. It also depends on the

accounts of the company, if the accounts went wrong the budgets will automatically be faulty.

3. Variance Analysis Report: Variance analysis report shows the difference

between actual and planned budget.

Advantage: It draws attention to areas where actual performance is different from planned

performance so that management can take necessary decisions to amend that. Furthermore it is

helpful in assessing areas where assets are not effectively utilized and areas where adjustments

are necessary.

Disadvantage: It has a major drawback; it takes a long time to examine the effect of the variance

and therefore corrective decisions and actions are delayed.

4. Operational Budget: This budget helps as a financial plan which is designed to

aid the business to meet its debt obligations and sustain growth over time

(Agustia, 2020). Operational budget provides the company with the areas where

cast is needed the most and how the company spends its resources.

business is able to manage its finances and use it effectively. Cash flow budget helps predicting

seasonal fluctuations where shortage and surplus cash can be avoided.

Disadvantage: While creating cash flow budget non-financial and non-cash factors are excluded.

When the business has to choose from one of the two financial institution from where it can

incur debt; where one institution may offer low interest rate and other may offer better services.

In cash flow budget non-financial perks are not recorded.

2. Flexible Budget: It is a budget which is flexible and dynamic as per the volume

and activity. In this budget, the budgeted amount changes and varies according to

the situation. This budget is also known as variable budget because it includes

variable factors like variable factor cost rather than static ones (Giovanni and et.

al, 2019).

Advantage: It helps in assessing the efficiency of the departmental head. It control overheads and

help in revaluation of the budget at every level.

Disadvantage: This budget requires skilled workers, therefore it becomes a challenge for the

business to find skilled human resource and it requires a lot of resources. It also depends on the

accounts of the company, if the accounts went wrong the budgets will automatically be faulty.

3. Variance Analysis Report: Variance analysis report shows the difference

between actual and planned budget.

Advantage: It draws attention to areas where actual performance is different from planned

performance so that management can take necessary decisions to amend that. Furthermore it is

helpful in assessing areas where assets are not effectively utilized and areas where adjustments

are necessary.

Disadvantage: It has a major drawback; it takes a long time to examine the effect of the variance

and therefore corrective decisions and actions are delayed.

4. Operational Budget: This budget helps as a financial plan which is designed to

aid the business to meet its debt obligations and sustain growth over time

(Agustia, 2020). Operational budget provides the company with the areas where

cast is needed the most and how the company spends its resources.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.