Management Accounting Report: Decision Making for Imda Tech (2024)

VerifiedAdded on 2020/01/07

|16

|4373

|144

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, focusing on their application within Imda Tech, a company specializing in chargers and electronic gadgets. The report delves into the meaning and importance of management accounting, differentiating it from financial accounting and emphasizing its role in strategic decision-making. It examines various management accounting systems, including cost accounting, inventory management, and job costing, and their practical applications. The core of the report analyzes costing methods, comparing absorption and marginal costing through detailed calculations and reconciliation statements. Furthermore, it explores different budgeting types, their advantages and disadvantages, and the budgetary process. The report also investigates pricing strategies and the balance scorecard approach, detailing its implementation and significance in addressing financial problems and enhancing financial governance. The report concludes by summarizing the key findings and highlighting the importance of these tools in driving success for Imda Tech. The report includes tables illustrating calculations for costing methods and a reconciliation statement, enhancing the understanding of the concepts discussed.

Management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION.........................................................................................................................................4

TASK 1..........................................................................................................................................................4

(A). (i) Management accounting meaning and difference between financial and management

accounting..................................................................................................................................................4

(ii) Importance of management accounting information as a decision-making tool.................................5

(B) Explain various types of management accounting system & its application......................................6

TASK 2..........................................................................................................................................................7

(1). Absorption costing..............................................................................................................................7

(2). Marginal costing..................................................................................................................................8

TASK 3..........................................................................................................................................................9

(A) Different types of budgets and their advantage and disadvantages.....................................................9

(B) Budgetary process..............................................................................................................................11

(C) Pricing strategies................................................................................................................................12

TASK 4........................................................................................................................................................13

(A). Explaining the balance score card approach & describing its implementation................................13

(I) Use of BSC to respond financial problems.........................................................................................13

(II) Significance of BSC to improve financial governance & development of effective strategies........14

CONCLUSION............................................................................................................................................14

REFERENCES............................................................................................................................................15

INTRODUCTION.........................................................................................................................................4

TASK 1..........................................................................................................................................................4

(A). (i) Management accounting meaning and difference between financial and management

accounting..................................................................................................................................................4

(ii) Importance of management accounting information as a decision-making tool.................................5

(B) Explain various types of management accounting system & its application......................................6

TASK 2..........................................................................................................................................................7

(1). Absorption costing..............................................................................................................................7

(2). Marginal costing..................................................................................................................................8

TASK 3..........................................................................................................................................................9

(A) Different types of budgets and their advantage and disadvantages.....................................................9

(B) Budgetary process..............................................................................................................................11

(C) Pricing strategies................................................................................................................................12

TASK 4........................................................................................................................................................13

(A). Explaining the balance score card approach & describing its implementation................................13

(I) Use of BSC to respond financial problems.........................................................................................13

(II) Significance of BSC to improve financial governance & development of effective strategies........14

CONCLUSION............................................................................................................................................14

REFERENCES............................................................................................................................................15

Table of figures

Table 1 Calculation of profit or loss under Absorption costing...................................................................7

Table 2Calculation of unit cost under absorption costing............................................................................8

Table 3 Calculation of profit or loss under marginal costing.......................................................................8

Table 4Calculation of unit cost under marginal costing...............................................................................9

Table 5 Reconcilation statement..................................................................................................................9

Table 1 Calculation of profit or loss under Absorption costing...................................................................7

Table 2Calculation of unit cost under absorption costing............................................................................8

Table 3 Calculation of profit or loss under marginal costing.......................................................................8

Table 4Calculation of unit cost under marginal costing...............................................................................9

Table 5 Reconcilation statement..................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Now-a-days with the internationalized of the operations and tough rivalry period, it becomes too

complex for the managers to make prudent decisions on a urgent basis or in very short period. This

challenges arise the need of managers to be well-equipped with the extra ordinary & exceptional

managerial skills, so that, immediate decisions can be made for arriving success. The present report aims

at finding out the critical importance of managerial accounting tools like costing, balance scorecard

approach and budgeting framework to gain succcess for Imda Tech which is engaging in production and

delivery of special charger for the phones & other carrying electronic gadgets.

TASK 1

(A). (i) Management accounting meaning and difference between financial and management

accounting

Managerial accounting is a framework that managers use to make business decisions

regarding their day-to-day functioning, operations and regular course of actions. In the global

corporate scenario, managers are highly concerned towards their future performance and thereby

use current information and business performance to make variety of decisions in operational

areas in highly fluctuating environment. Unlike it,

Management accounting Financial accounting

Meanining CIMA (Chartered Institute of

Management Accounting) has

defined management accounting as a

process which comprises

identifying, measurement,

accumulation, evaluation, analysis

and communication to the managers

to aid in successful & effective

corporate planning (Simons, 2013).

Financial accounting is a process

which is concerned with

preparation of Imda Tech’s

annual financial reports for the

objective of financial

reporting(Pratt, 2013).

Purpose/objecctive To devise solid plans, formulate

organizational strategies and

effective decisions for meeting out

To measure the performane of

the entity by finding out the

profitability and financial status

Now-a-days with the internationalized of the operations and tough rivalry period, it becomes too

complex for the managers to make prudent decisions on a urgent basis or in very short period. This

challenges arise the need of managers to be well-equipped with the extra ordinary & exceptional

managerial skills, so that, immediate decisions can be made for arriving success. The present report aims

at finding out the critical importance of managerial accounting tools like costing, balance scorecard

approach and budgeting framework to gain succcess for Imda Tech which is engaging in production and

delivery of special charger for the phones & other carrying electronic gadgets.

TASK 1

(A). (i) Management accounting meaning and difference between financial and management

accounting

Managerial accounting is a framework that managers use to make business decisions

regarding their day-to-day functioning, operations and regular course of actions. In the global

corporate scenario, managers are highly concerned towards their future performance and thereby

use current information and business performance to make variety of decisions in operational

areas in highly fluctuating environment. Unlike it,

Management accounting Financial accounting

Meanining CIMA (Chartered Institute of

Management Accounting) has

defined management accounting as a

process which comprises

identifying, measurement,

accumulation, evaluation, analysis

and communication to the managers

to aid in successful & effective

corporate planning (Simons, 2013).

Financial accounting is a process

which is concerned with

preparation of Imda Tech’s

annual financial reports for the

objective of financial

reporting(Pratt, 2013).

Purpose/objecctive To devise solid plans, formulate

organizational strategies and

effective decisions for meeting out

To measure the performane of

the entity by finding out the

profitability and financial status

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

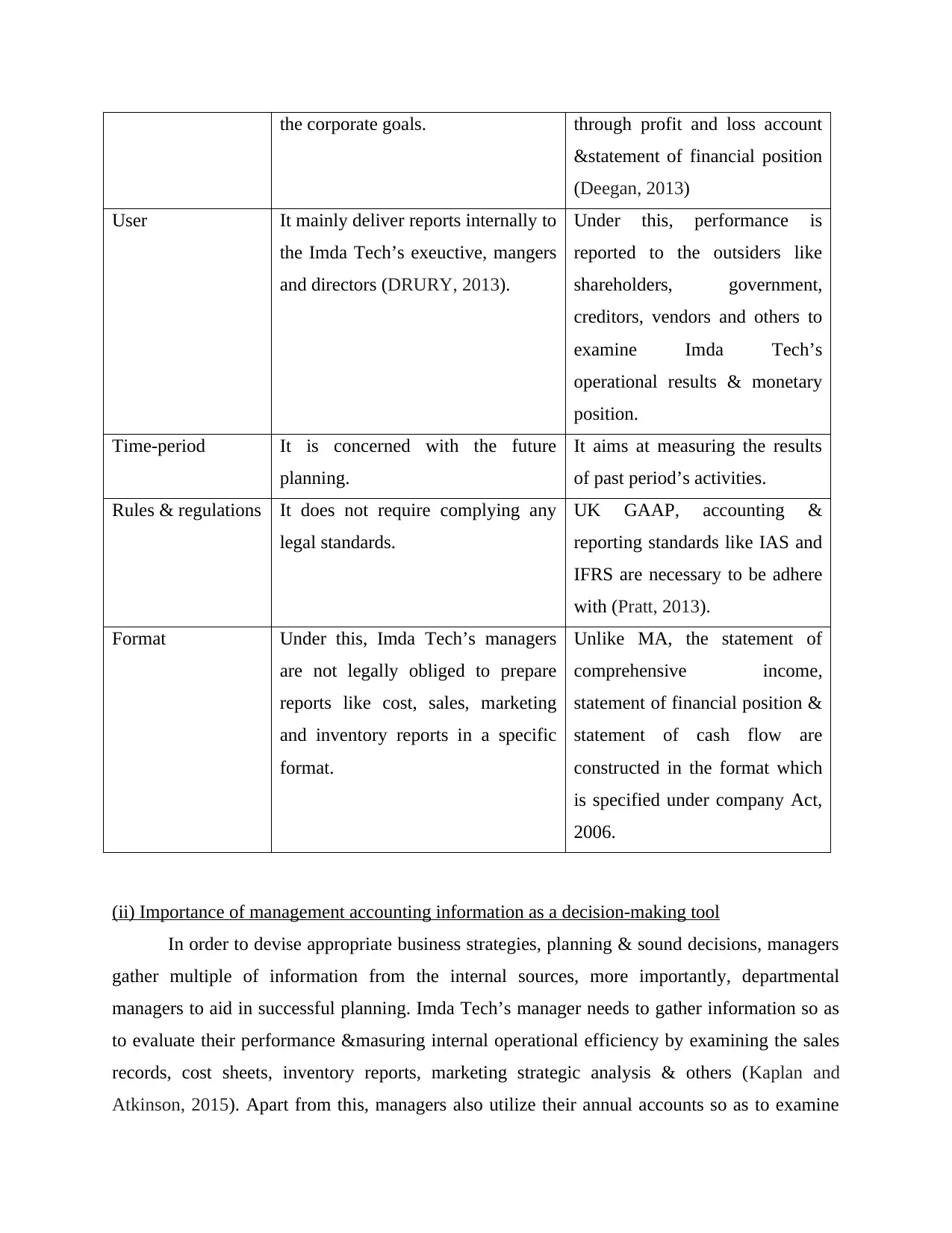

the corporate goals. through profit and loss account

&statement of financial position

(Deegan, 2013)

User It mainly deliver reports internally to

the Imda Tech’s exeuctive, mangers

and directors (DRURY, 2013).

Under this, performance is

reported to the outsiders like

shareholders, government,

creditors, vendors and others to

examine Imda Tech’s

operational results & monetary

position.

Time-period It is concerned with the future

planning.

It aims at measuring the results

of past period’s activities.

Rules & regulations It does not require complying any

legal standards.

UK GAAP, accounting &

reporting standards like IAS and

IFRS are necessary to be adhere

with (Pratt, 2013).

Format Under this, Imda Tech’s managers

are not legally obliged to prepare

reports like cost, sales, marketing

and inventory reports in a specific

format.

Unlike MA, the statement of

comprehensive income,

statement of financial position &

statement of cash flow are

constructed in the format which

is specified under company Act,

2006.

(ii) Importance of management accounting information as a decision-making tool

In order to devise appropriate business strategies, planning & sound decisions, managers

gather multiple of information from the internal sources, more importantly, departmental

managers to aid in successful planning. Imda Tech’s manager needs to gather information so as

to evaluate their performance &masuring internal operational efficiency by examining the sales

records, cost sheets, inventory reports, marketing strategic analysis & others (Kaplan and

Atkinson, 2015). Apart from this, managers also utilize their annual accounts so as to examine

&statement of financial position

(Deegan, 2013)

User It mainly deliver reports internally to

the Imda Tech’s exeuctive, mangers

and directors (DRURY, 2013).

Under this, performance is

reported to the outsiders like

shareholders, government,

creditors, vendors and others to

examine Imda Tech’s

operational results & monetary

position.

Time-period It is concerned with the future

planning.

It aims at measuring the results

of past period’s activities.

Rules & regulations It does not require complying any

legal standards.

UK GAAP, accounting &

reporting standards like IAS and

IFRS are necessary to be adhere

with (Pratt, 2013).

Format Under this, Imda Tech’s managers

are not legally obliged to prepare

reports like cost, sales, marketing

and inventory reports in a specific

format.

Unlike MA, the statement of

comprehensive income,

statement of financial position &

statement of cash flow are

constructed in the format which

is specified under company Act,

2006.

(ii) Importance of management accounting information as a decision-making tool

In order to devise appropriate business strategies, planning & sound decisions, managers

gather multiple of information from the internal sources, more importantly, departmental

managers to aid in successful planning. Imda Tech’s manager needs to gather information so as

to evaluate their performance &masuring internal operational efficiency by examining the sales

records, cost sheets, inventory reports, marketing strategic analysis & others (Kaplan and

Atkinson, 2015). Apart from this, managers also utilize their annual accounts so as to examine

their business profitability & financial status like solvency & liquidity position. All these

information are really excruciatingly important for the purpose of making solid planning &

decisions. It enable managers in finding out the areas where firm did not performed well such as

high cost, inefficient operation, poor sales, declined rturn and others as a result, decisions can be

make to combat hurdles and bring improvement. Apart from this, one of the important

information tool for the Imda Tech’s executive and policy makers is budget which is a document

that provide information about the target income & expenses that it has supposed to collect or

expected to incur. It sets a target or bechmark with which actual results are compared for

variance analysis. With the help of it, they can create better plans for sales maximization & cost-

curtailmentt with the aim of driving success.

(B) Explain various types of management accounting system & its application

There are number of tools which Imda Tech’s managers can use for the purpose of

making sound quaity of decisions that are explained underneath:

Cost Accounting system:This is a system that is allows Imda Tech to trace the resources

that has been consumed by it in the manufacturing & distribution of goods & services to the

consumers. Under this, Imda Tech can accumulate the costs incurred in various functions which

are the results of its manufacturing activities and thereby the total cost can be determined. It

assist the business entity in monitoring & controlling the business progress, evaluate the cost

related data over the period and implement tighten control over the operational procedure to

reduce the cost with the aim of driving larger return (Ellul and et.al., 2015).

Inventory management system:It is a computer-based application software that is used

to track the level of stock available in Imda Tech along with the goods ordering and its deliveries

as well. Imda Tech can also implement the system to create the work order, material bill & other

production-related reports. With this, they can keep their eye overr the stock through regularly

supervising the flow of goods from production division to wareouse and at point of sale (POS).

With this, procurement department can place purchase order on right demand so that sufficient

quantity of goods can be procured right time before reaching danger level.

Job costing system:It is also regarded as job order costing that is used to assign the

overheads like production expense i.e. rent, depreication & others to one or more cost pools. In

information are really excruciatingly important for the purpose of making solid planning &

decisions. It enable managers in finding out the areas where firm did not performed well such as

high cost, inefficient operation, poor sales, declined rturn and others as a result, decisions can be

make to combat hurdles and bring improvement. Apart from this, one of the important

information tool for the Imda Tech’s executive and policy makers is budget which is a document

that provide information about the target income & expenses that it has supposed to collect or

expected to incur. It sets a target or bechmark with which actual results are compared for

variance analysis. With the help of it, they can create better plans for sales maximization & cost-

curtailmentt with the aim of driving success.

(B) Explain various types of management accounting system & its application

There are number of tools which Imda Tech’s managers can use for the purpose of

making sound quaity of decisions that are explained underneath:

Cost Accounting system:This is a system that is allows Imda Tech to trace the resources

that has been consumed by it in the manufacturing & distribution of goods & services to the

consumers. Under this, Imda Tech can accumulate the costs incurred in various functions which

are the results of its manufacturing activities and thereby the total cost can be determined. It

assist the business entity in monitoring & controlling the business progress, evaluate the cost

related data over the period and implement tighten control over the operational procedure to

reduce the cost with the aim of driving larger return (Ellul and et.al., 2015).

Inventory management system:It is a computer-based application software that is used

to track the level of stock available in Imda Tech along with the goods ordering and its deliveries

as well. Imda Tech can also implement the system to create the work order, material bill & other

production-related reports. With this, they can keep their eye overr the stock through regularly

supervising the flow of goods from production division to wareouse and at point of sale (POS).

With this, procurement department can place purchase order on right demand so that sufficient

quantity of goods can be procured right time before reaching danger level.

Job costing system:It is also regarded as job order costing that is used to assign the

overheads like production expense i.e. rent, depreication & others to one or more cost pools. In

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the end, the system generates the costs report about every job work that has been completed by

Imda Tech to measure the total costs of each job (DRURY, 2013). Manufacturing department

can use it and report to the other departments like finance to have sufficient fund to incur these

expense for continual operations.

Price optimising system:As its name, the system presents the essential information to

the executives to investigate that to what extent, product-users are price sensitive by assessing

the impact of alteration in delivering’s prices on their demand(Simons, 2013). Setting a right

price through devising an excellent pricing mechanism is the most important benefit that can be

gained by Imda Tech by using the system.

TASK 2

(1). Absorption costing

As per the stated scenario, Imda Tech UK Limited is produced special charger for the

mobile phone and other carry-on-gadgets which cost data has been provided. Absorption costing

is a method that apportion or assigns both the fixed & variable costs to the each unit of output in

order to find out cost each unit, presented below:

Table 1 Calculation of profit or loss under Absorption costing

Particulars Amount

Sales (1500*35) 52500

Less: Cost of production

Direct material (2000*5) 10000

Direct labor (2000*8) 16000

Variable production overheads (2000*2) 4000

Total variable cost of production 30000

Fixed production overheads (2000*5) 10000

Cost of production 40000

Less: Closing stock (40000/2000*500) 10000

Cost of goods sold 30000

Under/Over absorption (1000*5) 5000

Gross profit 17500

Less: Non production overheads

Less: Fixed selling, distribution and administration expense 10000

Variable selling, distribution and administrative expense (15% of

52500) 7875

Imda Tech to measure the total costs of each job (DRURY, 2013). Manufacturing department

can use it and report to the other departments like finance to have sufficient fund to incur these

expense for continual operations.

Price optimising system:As its name, the system presents the essential information to

the executives to investigate that to what extent, product-users are price sensitive by assessing

the impact of alteration in delivering’s prices on their demand(Simons, 2013). Setting a right

price through devising an excellent pricing mechanism is the most important benefit that can be

gained by Imda Tech by using the system.

TASK 2

(1). Absorption costing

As per the stated scenario, Imda Tech UK Limited is produced special charger for the

mobile phone and other carry-on-gadgets which cost data has been provided. Absorption costing

is a method that apportion or assigns both the fixed & variable costs to the each unit of output in

order to find out cost each unit, presented below:

Table 1 Calculation of profit or loss under Absorption costing

Particulars Amount

Sales (1500*35) 52500

Less: Cost of production

Direct material (2000*5) 10000

Direct labor (2000*8) 16000

Variable production overheads (2000*2) 4000

Total variable cost of production 30000

Fixed production overheads (2000*5) 10000

Cost of production 40000

Less: Closing stock (40000/2000*500) 10000

Cost of goods sold 30000

Under/Over absorption (1000*5) 5000

Gross profit 17500

Less: Non production overheads

Less: Fixed selling, distribution and administration expense 10000

Variable selling, distribution and administrative expense (15% of

52500) 7875

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total non-production overheads 17875

Net profitability -375

Table 2Calculation of unit cost under absorption costing

Particulars Absorption costing

Direct labor 5

Direct material 8

Variable production overheads 2

Fixed production overheads 5

Costs per unit 20

From the outcome, it is clear that company incurred a loss of 375 GBP under absorption

costing method. Here, the unit cost of production is derived to 20 each unit.

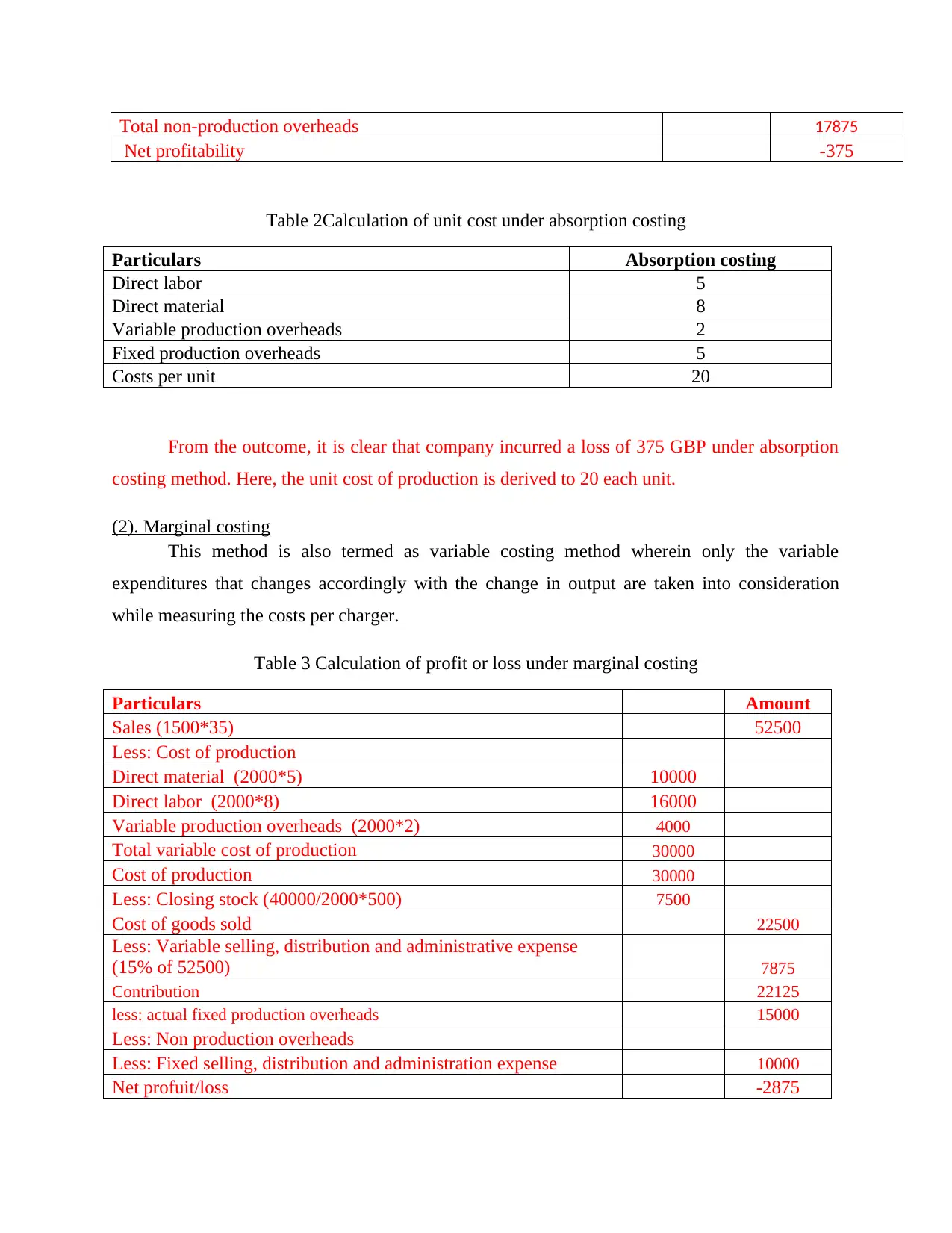

(2). Marginal costing

This method is also termed as variable costing method wherein only the variable

expenditures that changes accordingly with the change in output are taken into consideration

while measuring the costs per charger.

Table 3 Calculation of profit or loss under marginal costing

Particulars Amount

Sales (1500*35) 52500

Less: Cost of production

Direct material (2000*5) 10000

Direct labor (2000*8) 16000

Variable production overheads (2000*2) 4000

Total variable cost of production 30000

Cost of production 30000

Less: Closing stock (40000/2000*500) 7500

Cost of goods sold 22500

Less: Variable selling, distribution and administrative expense

(15% of 52500) 7875

Contribution 22125

less: actual fixed production overheads 15000

Less: Non production overheads

Less: Fixed selling, distribution and administration expense 10000

Net profuit/loss -2875

Net profitability -375

Table 2Calculation of unit cost under absorption costing

Particulars Absorption costing

Direct labor 5

Direct material 8

Variable production overheads 2

Fixed production overheads 5

Costs per unit 20

From the outcome, it is clear that company incurred a loss of 375 GBP under absorption

costing method. Here, the unit cost of production is derived to 20 each unit.

(2). Marginal costing

This method is also termed as variable costing method wherein only the variable

expenditures that changes accordingly with the change in output are taken into consideration

while measuring the costs per charger.

Table 3 Calculation of profit or loss under marginal costing

Particulars Amount

Sales (1500*35) 52500

Less: Cost of production

Direct material (2000*5) 10000

Direct labor (2000*8) 16000

Variable production overheads (2000*2) 4000

Total variable cost of production 30000

Cost of production 30000

Less: Closing stock (40000/2000*500) 7500

Cost of goods sold 22500

Less: Variable selling, distribution and administrative expense

(15% of 52500) 7875

Contribution 22125

less: actual fixed production overheads 15000

Less: Non production overheads

Less: Fixed selling, distribution and administration expense 10000

Net profuit/loss -2875

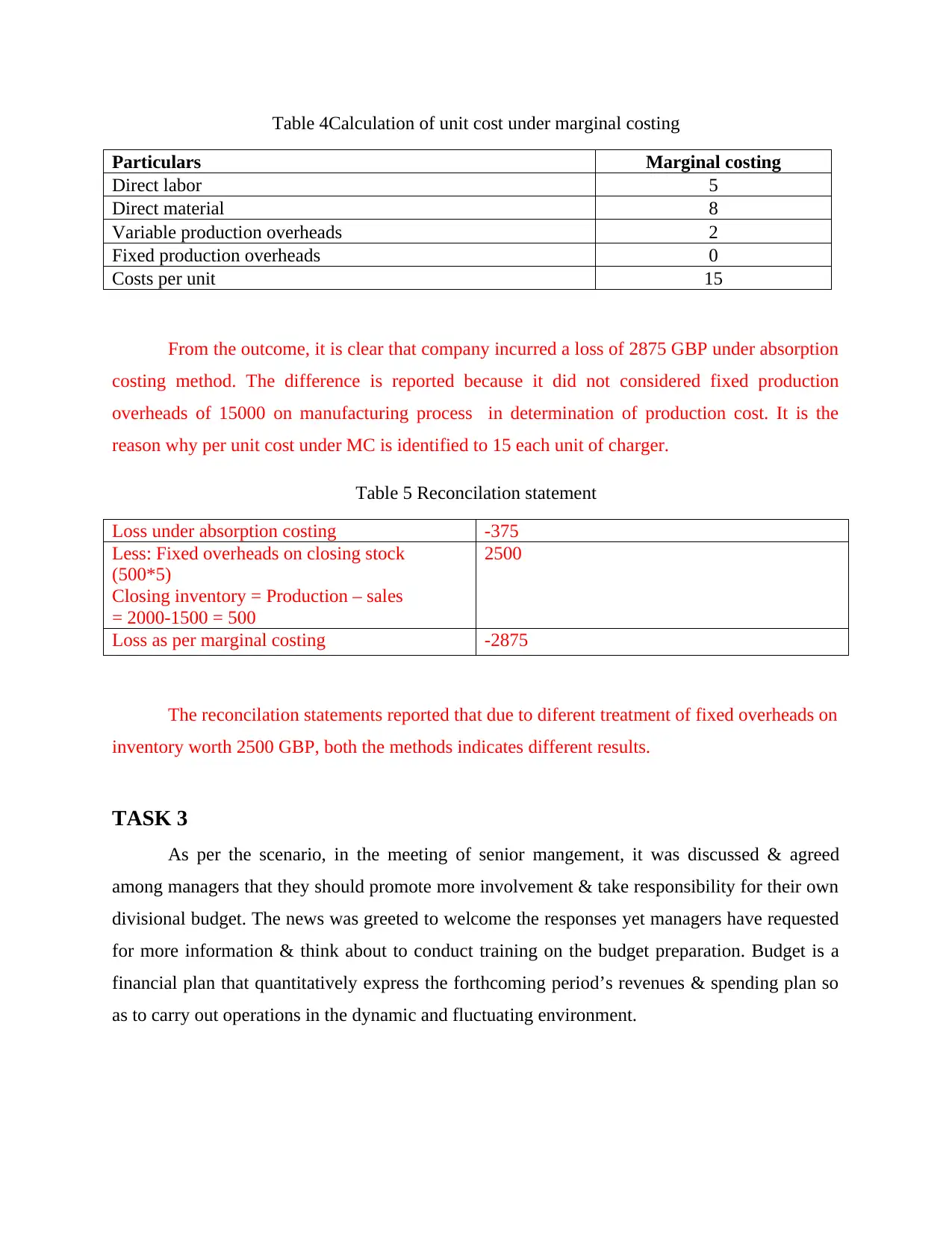

Table 4Calculation of unit cost under marginal costing

Particulars Marginal costing

Direct labor 5

Direct material 8

Variable production overheads 2

Fixed production overheads 0

Costs per unit 15

From the outcome, it is clear that company incurred a loss of 2875 GBP under absorption

costing method. The difference is reported because it did not considered fixed production

overheads of 15000 on manufacturing process in determination of production cost. It is the

reason why per unit cost under MC is identified to 15 each unit of charger.

Table 5 Reconcilation statement

Loss under absorption costing -375

Less: Fixed overheads on closing stock

(500*5)

Closing inventory = Production – sales

= 2000-1500 = 500

2500

Loss as per marginal costing -2875

The reconcilation statements reported that due to diferent treatment of fixed overheads on

inventory worth 2500 GBP, both the methods indicates different results.

TASK 3

As per the scenario, in the meeting of senior mangement, it was discussed & agreed

among managers that they should promote more involvement & take responsibility for their own

divisional budget. The news was greeted to welcome the responses yet managers have requested

for more information & think about to conduct training on the budget preparation. Budget is a

financial plan that quantitatively express the forthcoming period’s revenues & spending plan so

as to carry out operations in the dynamic and fluctuating environment.

Particulars Marginal costing

Direct labor 5

Direct material 8

Variable production overheads 2

Fixed production overheads 0

Costs per unit 15

From the outcome, it is clear that company incurred a loss of 2875 GBP under absorption

costing method. The difference is reported because it did not considered fixed production

overheads of 15000 on manufacturing process in determination of production cost. It is the

reason why per unit cost under MC is identified to 15 each unit of charger.

Table 5 Reconcilation statement

Loss under absorption costing -375

Less: Fixed overheads on closing stock

(500*5)

Closing inventory = Production – sales

= 2000-1500 = 500

2500

Loss as per marginal costing -2875

The reconcilation statements reported that due to diferent treatment of fixed overheads on

inventory worth 2500 GBP, both the methods indicates different results.

TASK 3

As per the scenario, in the meeting of senior mangement, it was discussed & agreed

among managers that they should promote more involvement & take responsibility for their own

divisional budget. The news was greeted to welcome the responses yet managers have requested

for more information & think about to conduct training on the budget preparation. Budget is a

financial plan that quantitatively express the forthcoming period’s revenues & spending plan so

as to carry out operations in the dynamic and fluctuating environment.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(A) Different types of budgets and their advantage and disadvantages

There are different types of budgetary planning mechansim which might be adopted by

the Imda Tech in budget formulation that are presented here as under:

Top-down approach:As name implies, under this method, only high level managerial

authority who comprises board members, directors, executives and others decides targets by their

own thoughts and projection (Kramer and Hartmann, 2014). They do not welcome the other

middle and lower level members in the budget creation process and after designing the budget,

they make resource allocating plans to distribute resources to the Imda Tech’s divisions for the

continual of regular course of activities. Advantage:

Top management set out their capital requirement and creates the best spending plan with

the better control over the financing activities.

It puts accountability on the top-level managers so as to set budget and create prudent

financial planning & decisions.

It is a quick way of budget designing because middle and lower level members are not

being invited by the top level hence, they do not need to put a lot of time in making

projection about the future.

Disadvantage:

Departmental managers are more knowledged about their divisional functioning,

therefore, budget designed without involvingg them may questioned the reliability &

authenticity of the budget.

The decisions of allocation of resources are made by top managers, whilst they are not

very much aware about the resource need of the divisions. Thus, ineffective distribution

may leads to cause hurdles (West, Prendergast and Shi, 2015).

It is not useful in boosting staff morale and their productivity because they are

unwelcomed in the budget designing procedure.

Participative budgeting:Unlike the top-down budgeting, participative budgeting, as name

implies, involves all the divisional staff of Imda Tech to present their projections so as to create a

valid and reliable budgte. It involves the participation of every member in the budget, so that,

There are different types of budgetary planning mechansim which might be adopted by

the Imda Tech in budget formulation that are presented here as under:

Top-down approach:As name implies, under this method, only high level managerial

authority who comprises board members, directors, executives and others decides targets by their

own thoughts and projection (Kramer and Hartmann, 2014). They do not welcome the other

middle and lower level members in the budget creation process and after designing the budget,

they make resource allocating plans to distribute resources to the Imda Tech’s divisions for the

continual of regular course of activities. Advantage:

Top management set out their capital requirement and creates the best spending plan with

the better control over the financing activities.

It puts accountability on the top-level managers so as to set budget and create prudent

financial planning & decisions.

It is a quick way of budget designing because middle and lower level members are not

being invited by the top level hence, they do not need to put a lot of time in making

projection about the future.

Disadvantage:

Departmental managers are more knowledged about their divisional functioning,

therefore, budget designed without involvingg them may questioned the reliability &

authenticity of the budget.

The decisions of allocation of resources are made by top managers, whilst they are not

very much aware about the resource need of the divisions. Thus, ineffective distribution

may leads to cause hurdles (West, Prendergast and Shi, 2015).

It is not useful in boosting staff morale and their productivity because they are

unwelcomed in the budget designing procedure.

Participative budgeting:Unlike the top-down budgeting, participative budgeting, as name

implies, involves all the divisional staff of Imda Tech to present their projections so as to create a

valid and reliable budgte. It involves the participation of every member in the budget, so that,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

more realistic projection of revenues & spending plan can be developed (Clinton and Hunton,

2015).

Advantage:

As managers of the division are well aware with their departmenal functioning, thus, they

can give accurate information about possible risk and challenges and helps in creating a

right plan.

It boost staff morale because they are invited & welcome by Imda Tech’s top authority

which helps in making prudent planning.

It provides a platform to the business staff to come up and discuss issues so that it can be

resolved with right planning & good quality of decisions (Heinle, Ross and Saouma,

2013).

Drawbacks:

It takes a very lengthy time in the budget development, in which, all the members are

devoted theirr time and efforts in projectin future.

It can also bring issues in resource allocation system because every manager will try to

benefit themselves by allocating more resources.

Budgetary slack may exists where revenues are maintaingg at less level and spending is

decided at very high to have positive variances (Mahlendorf, Schäffer and Skiba, 2015).

(B) Budgetary process

The process of budgeting comprises number of stages that are required to be followed by

the Imda Tech in building their budget, it is a continuous process that is enumerated underneath:

Setting assumptions: Initially, Imda Tech’s mangers needs to decide assumptions that it

will follow in sales projection, cost trends and other estimation.

Funding requirement: Afterwards, company has to assess their funding requirement so

as to give adequate attention to the available fund for the future projects.

2015).

Advantage:

As managers of the division are well aware with their departmenal functioning, thus, they

can give accurate information about possible risk and challenges and helps in creating a

right plan.

It boost staff morale because they are invited & welcome by Imda Tech’s top authority

which helps in making prudent planning.

It provides a platform to the business staff to come up and discuss issues so that it can be

resolved with right planning & good quality of decisions (Heinle, Ross and Saouma,

2013).

Drawbacks:

It takes a very lengthy time in the budget development, in which, all the members are

devoted theirr time and efforts in projectin future.

It can also bring issues in resource allocation system because every manager will try to

benefit themselves by allocating more resources.

Budgetary slack may exists where revenues are maintaingg at less level and spending is

decided at very high to have positive variances (Mahlendorf, Schäffer and Skiba, 2015).

(B) Budgetary process

The process of budgeting comprises number of stages that are required to be followed by

the Imda Tech in building their budget, it is a continuous process that is enumerated underneath:

Setting assumptions: Initially, Imda Tech’s mangers needs to decide assumptions that it

will follow in sales projection, cost trends and other estimation.

Funding requirement: Afterwards, company has to assess their funding requirement so

as to give adequate attention to the available fund for the future projects.

Forecasting of revenue and expenses: Thereafter, entity needs to anticipate the amount

of total income which is supposed to be acquired and possible expenses which it expect to incur

in the forthcoming years (Budgeting process, 2015).

Approve: The prepared budgeted statement is communicated to the Imda Tech’s

committee who are accountable to judge the validation of the budget for the approval. The

budget committee also may suggest to make some changes or alteration which perfectly match

the market enviromment(Kramer and Hartmann, 2014).

Communication: Lastly, it is communicated to all the divisional manager who are liable

to carry operations accordingly with the aim of achieving the set goals.

(C) Pricing strategies

Pricing decisions is one of the effective & highly important decisions which is required to

be taken by the Imda Tech’s managers. Fixing a right price helps to manage customer base and

attract high amount of consumers so that it will drive large sales value & yield or vice-versa.

Various techniques of the pricing strategies are presented below:

Cost-plus-pricing: Cost is the important element of price decisions, in this. Imda Tech’s

managers must find out the cost for each unit of the output and add a desired or targeted profit

margin per unit so as to set a right price (Dumas, 2013). It is helpful for the business becase it

cover all the costs and drive return also.

Price = Cost + desired return

= 150 + (150*20%)

= 150 + 30

= 180

Competitive pricing: This pricing method suggests a business to consider the prices of their

competitors when deciding their own prices for the goods and services. It is because, in the

competitive era, none of the entity can neglect their competitors prices so as to set their own

prices after comparison their own offerings & competitor goods as well (Vardakas, Zorba and

of total income which is supposed to be acquired and possible expenses which it expect to incur

in the forthcoming years (Budgeting process, 2015).

Approve: The prepared budgeted statement is communicated to the Imda Tech’s

committee who are accountable to judge the validation of the budget for the approval. The

budget committee also may suggest to make some changes or alteration which perfectly match

the market enviromment(Kramer and Hartmann, 2014).

Communication: Lastly, it is communicated to all the divisional manager who are liable

to carry operations accordingly with the aim of achieving the set goals.

(C) Pricing strategies

Pricing decisions is one of the effective & highly important decisions which is required to

be taken by the Imda Tech’s managers. Fixing a right price helps to manage customer base and

attract high amount of consumers so that it will drive large sales value & yield or vice-versa.

Various techniques of the pricing strategies are presented below:

Cost-plus-pricing: Cost is the important element of price decisions, in this. Imda Tech’s

managers must find out the cost for each unit of the output and add a desired or targeted profit

margin per unit so as to set a right price (Dumas, 2013). It is helpful for the business becase it

cover all the costs and drive return also.

Price = Cost + desired return

= 150 + (150*20%)

= 150 + 30

= 180

Competitive pricing: This pricing method suggests a business to consider the prices of their

competitors when deciding their own prices for the goods and services. It is because, in the

competitive era, none of the entity can neglect their competitors prices so as to set their own

prices after comparison their own offerings & competitor goods as well (Vardakas, Zorba and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.