Management Accounting Report: Systems, Costing, Budgeting, Analysis

VerifiedAdded on 2023/01/12

|20

|5158

|46

Report

AI Summary

This report analyzes management accounting practices within Cream Ltd., covering various systems like inventory management, job order costing, price optimization, and cost accounting. It delves into different methods of reporting, including inventory management, accounts receivable, budget, and performance reports. The report includes cost analysis techniques, such as marginal and absorption costing, along with income statement calculations and variance analysis. It further explains budgetary control, planning tools, and their advantages and disadvantages. Finally, it compares organizations based on their use of management accounting to address financial issues, providing a comprehensive overview of the subject.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Explanation of different types of systems of management accounting along with their

essential requirements..................................................................................................................1

P2 Explanation of various methods that are used for reporting of management accounting......3

TASK 2............................................................................................................................................4

P3 Calculation of costs using cost analysis techniques and formulating of income statement

under absorption and marginal costing........................................................................................4

TASK 3..........................................................................................................................................10

P4 Explanation of budgetary control along with description of planning tools and advantages

and disadvantages of all of them...............................................................................................10

TASK 4..........................................................................................................................................13

P5 Comparison of organisations on the basis of use of management accounting to respond

financial issues...........................................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Explanation of different types of systems of management accounting along with their

essential requirements..................................................................................................................1

P2 Explanation of various methods that are used for reporting of management accounting......3

TASK 2............................................................................................................................................4

P3 Calculation of costs using cost analysis techniques and formulating of income statement

under absorption and marginal costing........................................................................................4

TASK 3..........................................................................................................................................10

P4 Explanation of budgetary control along with description of planning tools and advantages

and disadvantages of all of them...............................................................................................10

TASK 4..........................................................................................................................................13

P5 Comparison of organisations on the basis of use of management accounting to respond

financial issues...........................................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Managerial Accounting is a larger and more diverse concept or notion that all managing

personnel need to recognize so they can then enhance the profitability of the entity they operate

with. It is a strategy that lets the inner interested parties establish whether or not the organization

is working efficiently (Cooper, Ezzamel and Qu, 2017). With the aid of it

all details/information concerning business practice is reported. This is crucial for all firms to

ensure that they devote importance to this in attempt to fulfil all the established targets and goals.

Maim ultimate objective of this study is to elucidate the core aspects of MA and its application

within the business for the structured execution of procedures in context of Cream ltd.

The project-report addresses a wide variety of topics like understanding management

accounting, including systems and key reports, applying multiple cost analysis approaches to

compile a firm's income statement. Aside from this, study also addresses different forms of

forecasting methods used in financial monitoring and operational analysis depending on use of

management accounting.

TASK 1

P1 Explanation of different types of systems of management accounting along with their

essential requirements

Managers utilize a common framework in all enterprises to evaluate whether the attempts

they make to improve organizational performance impact positively or adversely. It is

recognized as management accounting and supports company's performance review by all inner

interested parties (Hopper and Bui, 2016). The management accounting is utilized in Cream

Limited to aid the management team in evaluating the corporation's actual growth. Employees

also decide with the aid of it that enterprise in which they operate does or does not offer them

with success in the coming years. When aiming to accomplish all of long-term business targets,

it is very critical for the management teams to making sure they use it because it can help them

in measuring and managing company results.

Many corporate entities use multiple forms of MA systems to ensure that the expected

tasks are executed in a coordinated way or not. This is valuable for management teams to use

various sorts of structures to carry out all of activities appropriately. Management at Cream

Limited is giving attention to multiple forms of them, like cost accounting system, price

1

Managerial Accounting is a larger and more diverse concept or notion that all managing

personnel need to recognize so they can then enhance the profitability of the entity they operate

with. It is a strategy that lets the inner interested parties establish whether or not the organization

is working efficiently (Cooper, Ezzamel and Qu, 2017). With the aid of it

all details/information concerning business practice is reported. This is crucial for all firms to

ensure that they devote importance to this in attempt to fulfil all the established targets and goals.

Maim ultimate objective of this study is to elucidate the core aspects of MA and its application

within the business for the structured execution of procedures in context of Cream ltd.

The project-report addresses a wide variety of topics like understanding management

accounting, including systems and key reports, applying multiple cost analysis approaches to

compile a firm's income statement. Aside from this, study also addresses different forms of

forecasting methods used in financial monitoring and operational analysis depending on use of

management accounting.

TASK 1

P1 Explanation of different types of systems of management accounting along with their

essential requirements

Managers utilize a common framework in all enterprises to evaluate whether the attempts

they make to improve organizational performance impact positively or adversely. It is

recognized as management accounting and supports company's performance review by all inner

interested parties (Hopper and Bui, 2016). The management accounting is utilized in Cream

Limited to aid the management team in evaluating the corporation's actual growth. Employees

also decide with the aid of it that enterprise in which they operate does or does not offer them

with success in the coming years. When aiming to accomplish all of long-term business targets,

it is very critical for the management teams to making sure they use it because it can help them

in measuring and managing company results.

Many corporate entities use multiple forms of MA systems to ensure that the expected

tasks are executed in a coordinated way or not. This is valuable for management teams to use

various sorts of structures to carry out all of activities appropriately. Management at Cream

Limited is giving attention to multiple forms of them, like cost accounting system, price

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

optimization, inventory management system and job orders costing. With the aid of both of

them, management develop internal reports to evaluate organizations 'individual performance.

All these are outlined in detailed in Cream Limited's context as below:

Inventory management system: In majority of corporations, management are using it to retain

accurate information on the goods/inventories that they use to manufacture products sold to end

users. In Creams Limited, all products demanded by buyers are manufactured by maintaining all

the materials as per their preferences (Hall, 2016). It lets management ensure they have all goods

or materials they need to make final product. There are multiple types of inventory valuation

approaches for the managing of inventories within enterprise. All of these are listed as below:

AVCO (Average Cost Method): Here in this technique, average cost is assessed to

value the cost of closing inventory.

FIFO (First in First Out): Whereas under this, cost of closing stock is assessed based on

concept that items bought on first place is sold first place in defined sequence.

LIFO (Last in First Out): While, under this technique closing stock is valued depending

on the concept that latest/recent purchased goods are sold at first place.

Essential requirement- This accounting system is mandatory for Creams limited in order to

track quantity of goods sold and purchased during a particular time frame. As above

mentioned company deals in selling of chocolates, draughts then it is essential for them to

manage stored level of inventories as well as to control cost of different items by help of

various methods.

Job order costing system: This is one of key principal systems utilized in all businesses

carrying out multiple kinds of businesses. This is primarily intended to record information

specifically for all activities (Hirsch, Seubert, and Sohn, 2015). Within Creams Limited, the

needs for all customers are reported clearly within order to satisfy all of their demands. The

business is thus able to fulfil its lengthy-term goals, like better customer satisfaction. This

directs executives to ensure that all operations can be carried out on a customer-specific

basis. For Creams Limited, job ordering costing system is a valuable mechanism, as it

enables to fulfil all of customers 'requirements properly. In addition, achieving company

targets like higher earnings and more satisfied consumers/customers it is also beneficial.

2

them, management develop internal reports to evaluate organizations 'individual performance.

All these are outlined in detailed in Cream Limited's context as below:

Inventory management system: In majority of corporations, management are using it to retain

accurate information on the goods/inventories that they use to manufacture products sold to end

users. In Creams Limited, all products demanded by buyers are manufactured by maintaining all

the materials as per their preferences (Hall, 2016). It lets management ensure they have all goods

or materials they need to make final product. There are multiple types of inventory valuation

approaches for the managing of inventories within enterprise. All of these are listed as below:

AVCO (Average Cost Method): Here in this technique, average cost is assessed to

value the cost of closing inventory.

FIFO (First in First Out): Whereas under this, cost of closing stock is assessed based on

concept that items bought on first place is sold first place in defined sequence.

LIFO (Last in First Out): While, under this technique closing stock is valued depending

on the concept that latest/recent purchased goods are sold at first place.

Essential requirement- This accounting system is mandatory for Creams limited in order to

track quantity of goods sold and purchased during a particular time frame. As above

mentioned company deals in selling of chocolates, draughts then it is essential for them to

manage stored level of inventories as well as to control cost of different items by help of

various methods.

Job order costing system: This is one of key principal systems utilized in all businesses

carrying out multiple kinds of businesses. This is primarily intended to record information

specifically for all activities (Hirsch, Seubert, and Sohn, 2015). Within Creams Limited, the

needs for all customers are reported clearly within order to satisfy all of their demands. The

business is thus able to fulfil its lengthy-term goals, like better customer satisfaction. This

directs executives to ensure that all operations can be carried out on a customer-specific

basis. For Creams Limited, job ordering costing system is a valuable mechanism, as it

enables to fulfil all of customers 'requirements properly. In addition, achieving company

targets like higher earnings and more satisfied consumers/customers it is also beneficial.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Essential requirement- It is essential for companies to measure of cost of job or number of

employees employed in order to perform different kinds of tasks. In above Creams limited, this

accounting system is necessary for them to find out cost of each or individual unit of production.

Price optimisation system: This MA system for handling all products sold by a company

focuses primarily on establishing the correct price. Creams Ltd. managers evaluate that they are

able to draw significant numbers of consumers by pricing all their goods. The company profits

from assessing customers 'reactions to prices they plan to pay on all products they sell. Creams

Limited includes this, as managers can maximize profits by establishing the correct price for any

item they sell. This system could also assist the corporation in its evaluation by setting

acceptable prices for all of the products sold by entity to fulfil all its objectives.

Essential requirement- It is compulsory for Creams limited in order to set prices of their different

bakery products at a level on which customers can be satisfied. This is being done in accordance

of analysis of market trends like change in demand of products, customers’ perception about

product and many more.

Cost accounting system: This is another major method/system of management accounting

utilized mainly to assess costs of all activities carried out by an organisation in order to achieve

all its corporate targets. Within Creams Limited, managers evaluate all of the costs actually

required to meet all of the predefined objectives. Through implementing it, management is

knowledgeable of all costs of the activities. Creams Limited uses the cost accounting system

because it can enable administrators to assess actual costs of all operations carried out within

entity (Järvenpää and Länsiluoto, 2016).

Essential requirement- This accounting system is essential for Creams limited for keeping cost of

different types of operations and activities at a level on which they cannot bear any loss. It

becomes possible because under this cost of production is measured and compared with

estimated amount of cost.

P2 Explanation of various methods that are used for reporting of management accounting

In the present business scenario, the specific process for producing internal documents and

analyses, recognized as management accounting reporting, is practiced in most organisations. It

is important to be concentrated in order to evaluate the company performs favourably or

negatively (Šiška, 2016). The managers always take into account in Creams Restricted to ensure

3

employees employed in order to perform different kinds of tasks. In above Creams limited, this

accounting system is necessary for them to find out cost of each or individual unit of production.

Price optimisation system: This MA system for handling all products sold by a company

focuses primarily on establishing the correct price. Creams Ltd. managers evaluate that they are

able to draw significant numbers of consumers by pricing all their goods. The company profits

from assessing customers 'reactions to prices they plan to pay on all products they sell. Creams

Limited includes this, as managers can maximize profits by establishing the correct price for any

item they sell. This system could also assist the corporation in its evaluation by setting

acceptable prices for all of the products sold by entity to fulfil all its objectives.

Essential requirement- It is compulsory for Creams limited in order to set prices of their different

bakery products at a level on which customers can be satisfied. This is being done in accordance

of analysis of market trends like change in demand of products, customers’ perception about

product and many more.

Cost accounting system: This is another major method/system of management accounting

utilized mainly to assess costs of all activities carried out by an organisation in order to achieve

all its corporate targets. Within Creams Limited, managers evaluate all of the costs actually

required to meet all of the predefined objectives. Through implementing it, management is

knowledgeable of all costs of the activities. Creams Limited uses the cost accounting system

because it can enable administrators to assess actual costs of all operations carried out within

entity (Järvenpää and Länsiluoto, 2016).

Essential requirement- This accounting system is essential for Creams limited for keeping cost of

different types of operations and activities at a level on which they cannot bear any loss. It

becomes possible because under this cost of production is measured and compared with

estimated amount of cost.

P2 Explanation of various methods that are used for reporting of management accounting

In the present business scenario, the specific process for producing internal documents and

analyses, recognized as management accounting reporting, is practiced in most organisations. It

is important to be concentrated in order to evaluate the company performs favourably or

negatively (Šiška, 2016). The managers always take into account in Creams Restricted to ensure

3

they achieve all the company targets. There are different approaches used to collect financial

reports from the administration. They all are listed below:

Inventory management report: It is relevant to the reporting of all the items which an entity

requires to conduct all the organizational activities. A study is produced by management in

Creams Limited to determine whether they have adequate products to sell consumers

various goods as per their specifications. This is helpful for the company, because it will

help to deliver products on schedule in order to avoid the risk of dis-satisfied buyers.

Account receivable report: This is primarily linked to tracking the data of these buyers that can

make potential purchases and purchase products on credit. In Creams Limited, management

does this to retain accurate details about the sum owing and would be collected by the

consumers in the meantime on a deadline. It is helpful to the agency since it will aid to

evaluate the real exemption that would be issued in the future.

Budget report: This is primarily linked to the reports made by companies to distribute funds

according to their specifications to all branches so manager can conduct all their activities.

Creams Limited still requires this study to ensure that scheduled events are carried out in the

same budget that was already agreed on for them. It is advantageous for the company

because the required funds will be distributed to the divisions to fulfil all their tasks with the

aid of this report.

Performance report: This report is created in most organizations for the reason of evaluating the

overall output of the entire company and its workforce (van Helden and Uddin, 2016). Creams

Limited's president frequently formulates it in order to assess the entity's success and evaluate

whether workers are making sufficient attempts to lead to company development. This is good

for the company and it will enable the management to offer the workers incentives and rewards

due to their success.

TASK 2

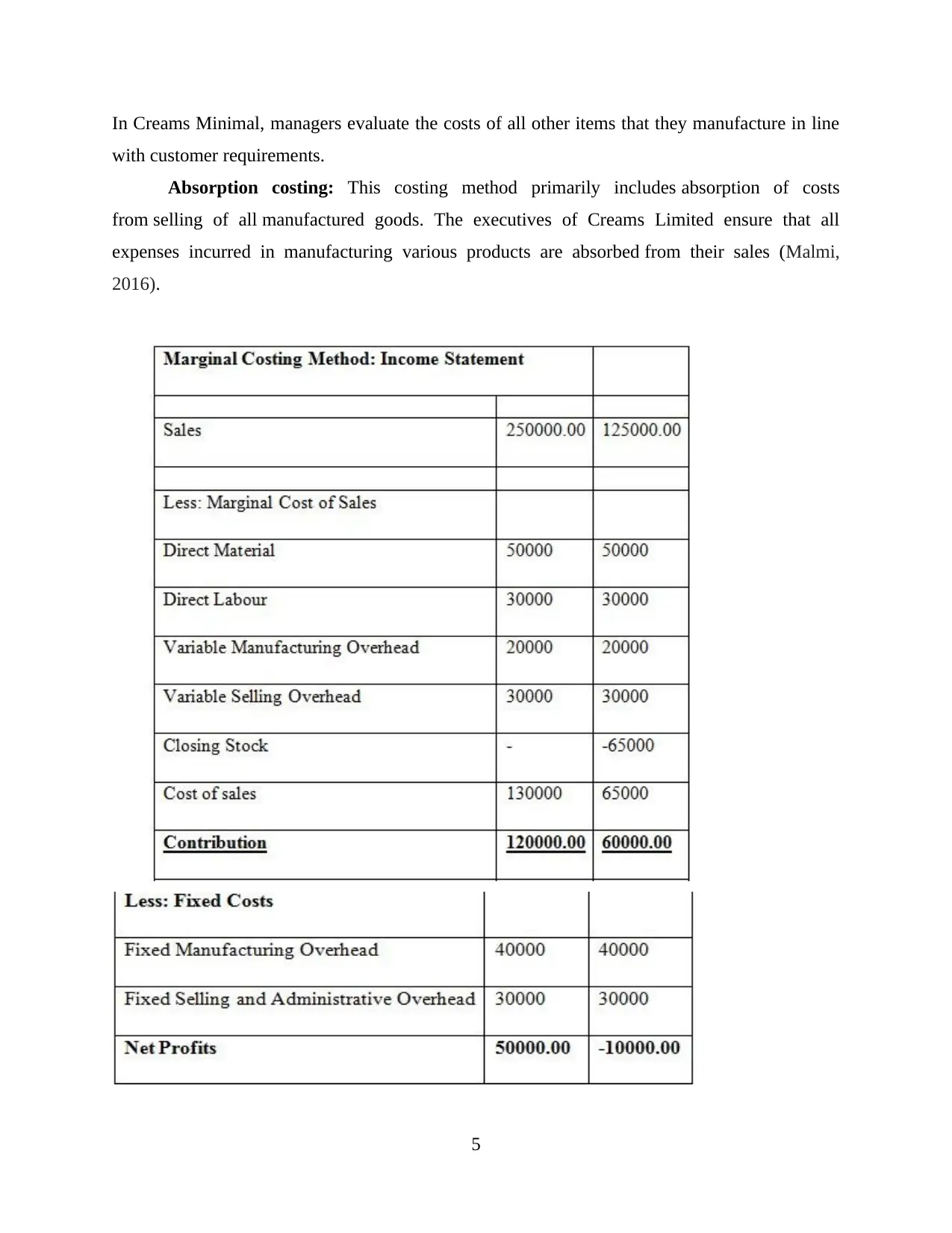

P3 Calculation of costs using cost analysis techniques and formulating of income statement

under absorption and marginal costing

Marginal costing: It could be described as costing method that organisations use to

calculate cost for each added unit, together with predetermined units produced, by the enterprise.

4

reports from the administration. They all are listed below:

Inventory management report: It is relevant to the reporting of all the items which an entity

requires to conduct all the organizational activities. A study is produced by management in

Creams Limited to determine whether they have adequate products to sell consumers

various goods as per their specifications. This is helpful for the company, because it will

help to deliver products on schedule in order to avoid the risk of dis-satisfied buyers.

Account receivable report: This is primarily linked to tracking the data of these buyers that can

make potential purchases and purchase products on credit. In Creams Limited, management

does this to retain accurate details about the sum owing and would be collected by the

consumers in the meantime on a deadline. It is helpful to the agency since it will aid to

evaluate the real exemption that would be issued in the future.

Budget report: This is primarily linked to the reports made by companies to distribute funds

according to their specifications to all branches so manager can conduct all their activities.

Creams Limited still requires this study to ensure that scheduled events are carried out in the

same budget that was already agreed on for them. It is advantageous for the company

because the required funds will be distributed to the divisions to fulfil all their tasks with the

aid of this report.

Performance report: This report is created in most organizations for the reason of evaluating the

overall output of the entire company and its workforce (van Helden and Uddin, 2016). Creams

Limited's president frequently formulates it in order to assess the entity's success and evaluate

whether workers are making sufficient attempts to lead to company development. This is good

for the company and it will enable the management to offer the workers incentives and rewards

due to their success.

TASK 2

P3 Calculation of costs using cost analysis techniques and formulating of income statement

under absorption and marginal costing

Marginal costing: It could be described as costing method that organisations use to

calculate cost for each added unit, together with predetermined units produced, by the enterprise.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In Creams Minimal, managers evaluate the costs of all other items that they manufacture in line

with customer requirements.

Absorption costing: This costing method primarily includes absorption of costs

from selling of all manufactured goods. The executives of Creams Limited ensure that all

expenses incurred in manufacturing various products are absorbed from their sales (Malmi,

2016).

5

with customer requirements.

Absorption costing: This costing method primarily includes absorption of costs

from selling of all manufactured goods. The executives of Creams Limited ensure that all

expenses incurred in manufacturing various products are absorbed from their sales (Malmi,

2016).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

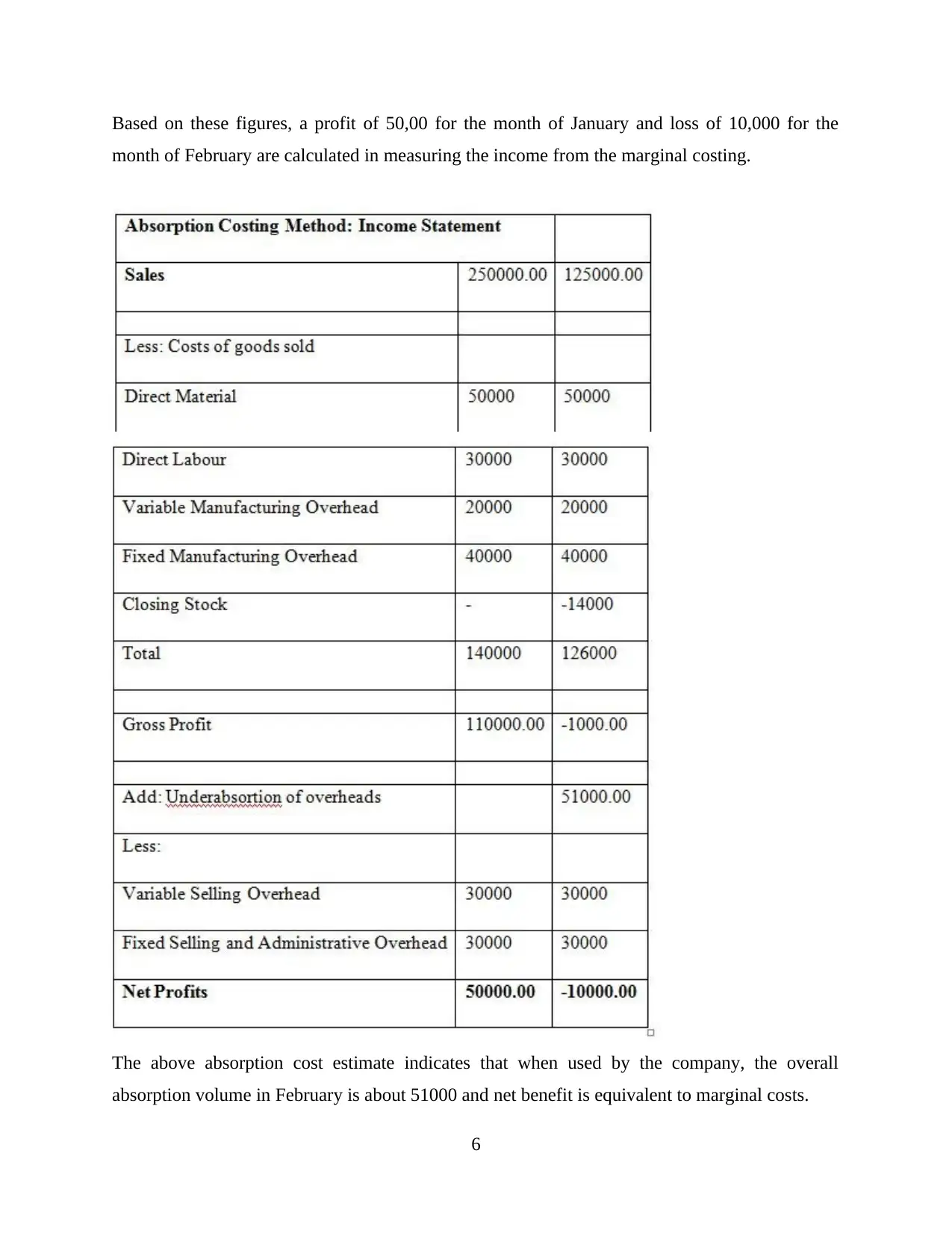

Based on these figures, a profit of 50,00 for the month of January and loss of 10,000 for the

month of February are calculated in measuring the income from the marginal costing.

The above absorption cost estimate indicates that when used by the company, the overall

absorption volume in February is about 51000 and net benefit is equivalent to marginal costs.

6

month of February are calculated in measuring the income from the marginal costing.

The above absorption cost estimate indicates that when used by the company, the overall

absorption volume in February is about 51000 and net benefit is equivalent to marginal costs.

6

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

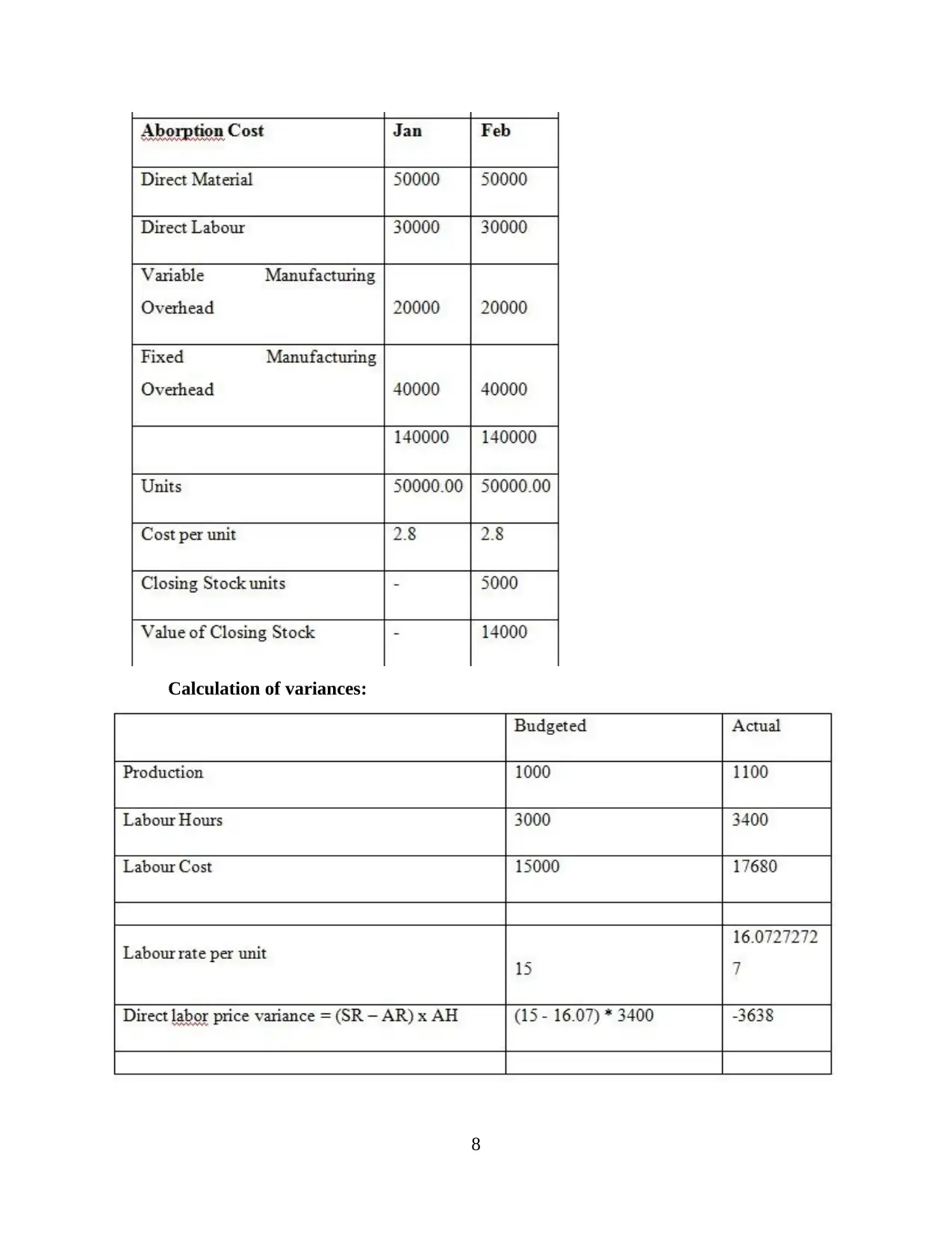

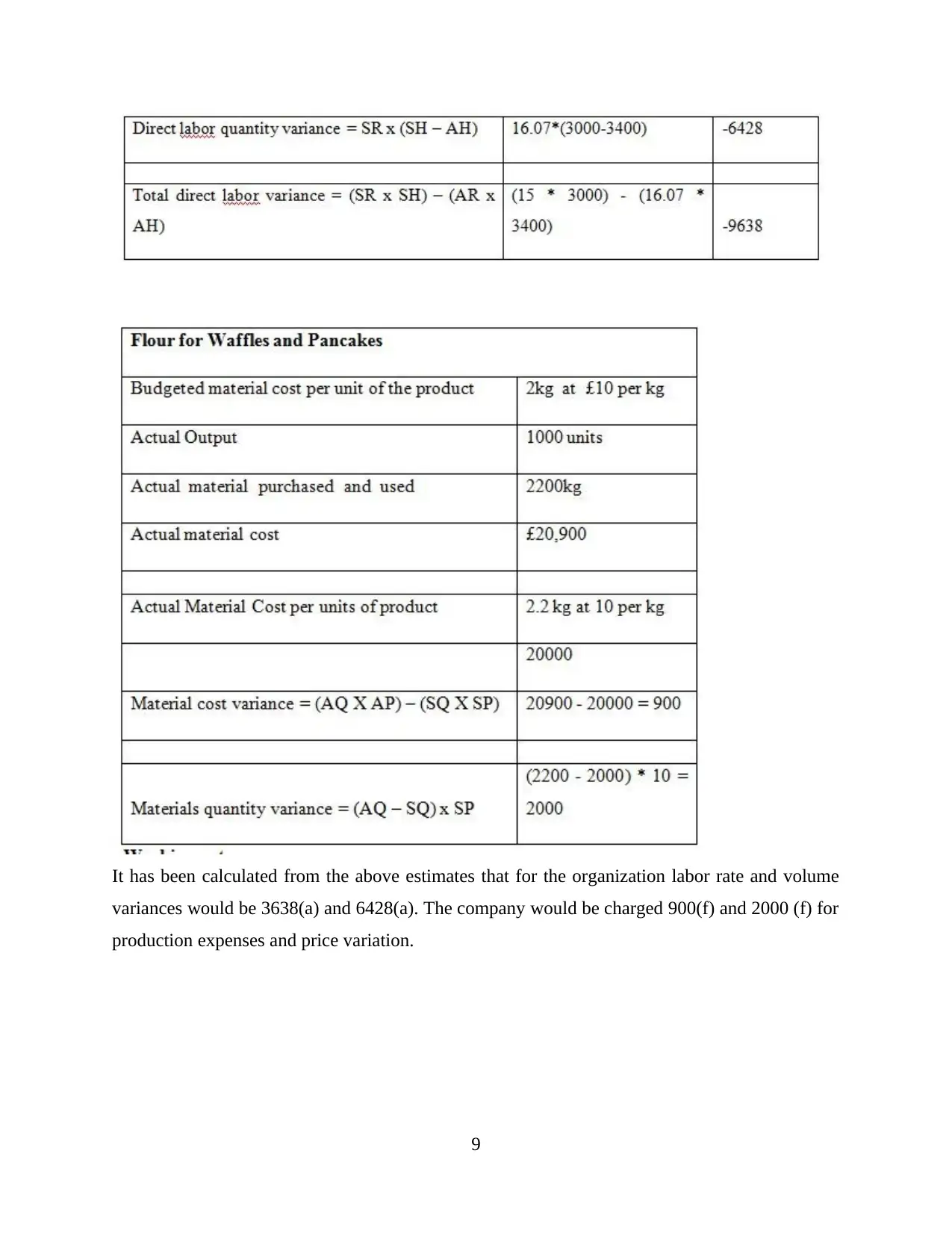

Calculation of variances:

8

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It has been calculated from the above estimates that for the organization labor rate and volume

variances would be 3638(a) and 6428(a). The company would be charged 900(f) and 2000 (f) for

production expenses and price variation.

9

variances would be 3638(a) and 6428(a). The company would be charged 900(f) and 2000 (f) for

production expenses and price variation.

9

TASK 3

P4 Explanation of budgetary control along with description of planning tools and advantages and

disadvantages of all of them

Budgetary control is linked to as the system by which organisations, in order to determine any

variance, arrange their budget for the future and compare it with the actual performance. When

matching the forecast estimates with the actual figures, an organisation's management will easily

detect differences and take immediate corrections. This process guarantees that the budget caps

are acceptable by senior managers at Creams limited. This regulation is necessary because

unnecessary expenditure has a detrimental impact on company income. Budgetary control is

used as a cost reduction mechanism within the organization that involves the fiscal growth,

alignment between various teams, roles and activities, success comparison with expenditures and

the outcomes required to obtain the best costs or losses.

Creams Limited has the key goal to use budgetary management as an efficient

mechanism which is crucial for the company's performance. This leads to increasing business

productivity and performance. Budgeting plays an significant part in organizing and managing,

as it facilitates the allocation of resources that are allocated for the most efficient usage, thereby

maintaining productivity in the business (Quattrone, 2016). A successful budgetary control

mechanism facilitates the preparation of different operations and guarantees that the organisation

operates efficiently and systemically. It often incorporates suggestions from growing layers of

management to plan the budget and promote collaboration between different departments. As an

effective preparation mechanism for financial administration, the job capital and other tools

inside the organization must be sufficiently sufficient. For a successful budgetary control system

certain conditions are required. These involve assistance from the management at upper level,

establishment of a centre of accountability, quantification of an organisation priorities, practical

targets, operational strategies, staff engagement, the scope of all aspects of operation, a reliable

accounting framework, etc. Various types of planning resources are needed for budgetary control

in Creams Limited.

Cost budget- It is a financial plan for the upcoming year with respect to specified company

expenses. It defines all the costs associated with business activities and events. That is the

estimated potential cost that a company may face in the future. This is the most effective method

10

P4 Explanation of budgetary control along with description of planning tools and advantages and

disadvantages of all of them

Budgetary control is linked to as the system by which organisations, in order to determine any

variance, arrange their budget for the future and compare it with the actual performance. When

matching the forecast estimates with the actual figures, an organisation's management will easily

detect differences and take immediate corrections. This process guarantees that the budget caps

are acceptable by senior managers at Creams limited. This regulation is necessary because

unnecessary expenditure has a detrimental impact on company income. Budgetary control is

used as a cost reduction mechanism within the organization that involves the fiscal growth,

alignment between various teams, roles and activities, success comparison with expenditures and

the outcomes required to obtain the best costs or losses.

Creams Limited has the key goal to use budgetary management as an efficient

mechanism which is crucial for the company's performance. This leads to increasing business

productivity and performance. Budgeting plays an significant part in organizing and managing,

as it facilitates the allocation of resources that are allocated for the most efficient usage, thereby

maintaining productivity in the business (Quattrone, 2016). A successful budgetary control

mechanism facilitates the preparation of different operations and guarantees that the organisation

operates efficiently and systemically. It often incorporates suggestions from growing layers of

management to plan the budget and promote collaboration between different departments. As an

effective preparation mechanism for financial administration, the job capital and other tools

inside the organization must be sufficiently sufficient. For a successful budgetary control system

certain conditions are required. These involve assistance from the management at upper level,

establishment of a centre of accountability, quantification of an organisation priorities, practical

targets, operational strategies, staff engagement, the scope of all aspects of operation, a reliable

accounting framework, etc. Various types of planning resources are needed for budgetary control

in Creams Limited.

Cost budget- It is a financial plan for the upcoming year with respect to specified company

expenses. It defines all the costs associated with business activities and events. That is the

estimated potential cost that a company may face in the future. This is the most effective method

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.