Management Accounting: Costing, Budgeting, and Reporting

VerifiedAdded on 2022/12/14

|23

|5628

|398

Homework Assignment

AI Summary

This management accounting report begins with an introduction to the field, defining its role in aiding managerial decision-making through the analysis of financial information. It then delves into the essential requirements of various management accounting systems, emphasizing their importance in effective business management, planning, and control. The report highlights the benefits of these systems, such as improved decision-making, accurate information, and strategic management. The main body of the report is divided into two parts. Part 1 discusses the importance of management accounting systems and reporting, including inventory management, job costing, and price optimization. Part 2 focuses on costing methods, with detailed calculations using both absorption and marginal costing techniques. The report includes a comparative analysis of the merits and demerits of both costing methods. Furthermore, it covers various types of budgeting and explores how companies utilize management accounting systems to evaluate financial performance. The report concludes by summarizing the key findings and the overall significance of management accounting in business operations.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Part 1................................................................................................................................................3

Section 1......................................................................................................................................3

1.1................................................................................................................................................3

1.2................................................................................................................................................4

1.3................................................................................................................................................5

1.4................................................................................................................................................6

Section 2......................................................................................................................................7

2.1................................................................................................................................................7

2.2................................................................................................................................................9

2.3..............................................................................................................................................10

2.4..............................................................................................................................................12

Part 2..............................................................................................................................................14

Section 3....................................................................................................................................14

3.1..............................................................................................................................................14

3.2..............................................................................................................................................15

Section 4....................................................................................................................................16

4.1..............................................................................................................................................16

4.2..............................................................................................................................................17

4.3..............................................................................................................................................18

4.4..............................................................................................................................................18

CONCLUSION..............................................................................................................................20

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Part 1................................................................................................................................................3

Section 1......................................................................................................................................3

1.1................................................................................................................................................3

1.2................................................................................................................................................4

1.3................................................................................................................................................5

1.4................................................................................................................................................6

Section 2......................................................................................................................................7

2.1................................................................................................................................................7

2.2................................................................................................................................................9

2.3..............................................................................................................................................10

2.4..............................................................................................................................................12

Part 2..............................................................................................................................................14

Section 3....................................................................................................................................14

3.1..............................................................................................................................................14

3.2..............................................................................................................................................15

Section 4....................................................................................................................................16

4.1..............................................................................................................................................16

4.2..............................................................................................................................................17

4.3..............................................................................................................................................18

4.4..............................................................................................................................................18

CONCLUSION..............................................................................................................................20

REFERENCES................................................................................................................................1

INTRODUCTION

Management accounting is being defined as the practice or branch of accounting which

assist manager in taking decision for betterment and growth of the business. This involves the

process of analysing and interpreting the financial information in order to take effective decision

for the betterment of the business. The purpose of management accounting is that it supplies

financial information to required parties and this assists them in managing operations of business

in such a manner that it yields profit and growth for company. The present study will start by

discussing about MA and essential requirements of different types of the management

accounting system. Further it will highlight the different methods of management accounting

reporting along with benefits of these systems. Moreover the next section will discuss the

calculation based on the marginal and absorption costing and their merits and demerits. Along

with this different types of budget will be prepared based on the information provided. Further in

the end the comparison of the fact that how companies make use of management accounting

system in order to deal with financial performances will be highlighted.

MAIN BODY

Part 1

Section 1

1.1

Management accounting is defined as that branch of accounting which deals with

analysis and evaluation of financial information so that managers can take proper decision for the

betterment of company. For any organization it is very important that they have proper

management accounting system as this will assist them in managing the business in proper and

effective manner. this will guide the employees that how the decisions are taken based on the

financial information of the company and for development of the business and its operations. In

order to make the company successful the most essential requirement is that the business must

have effective management accounting system. This is pertaining to the fact that when the MA

system will be effective then complete and effective analysis will take place of the whole

business (Zyznarska-Dworczak, 2018). Thus, this will result in successful and effective decision

making for the betterment of the company. The major importance and prerequisite of

management accounting are as follows-

Management accounting is being defined as the practice or branch of accounting which

assist manager in taking decision for betterment and growth of the business. This involves the

process of analysing and interpreting the financial information in order to take effective decision

for the betterment of the business. The purpose of management accounting is that it supplies

financial information to required parties and this assists them in managing operations of business

in such a manner that it yields profit and growth for company. The present study will start by

discussing about MA and essential requirements of different types of the management

accounting system. Further it will highlight the different methods of management accounting

reporting along with benefits of these systems. Moreover the next section will discuss the

calculation based on the marginal and absorption costing and their merits and demerits. Along

with this different types of budget will be prepared based on the information provided. Further in

the end the comparison of the fact that how companies make use of management accounting

system in order to deal with financial performances will be highlighted.

MAIN BODY

Part 1

Section 1

1.1

Management accounting is defined as that branch of accounting which deals with

analysis and evaluation of financial information so that managers can take proper decision for the

betterment of company. For any organization it is very important that they have proper

management accounting system as this will assist them in managing the business in proper and

effective manner. this will guide the employees that how the decisions are taken based on the

financial information of the company and for development of the business and its operations. In

order to make the company successful the most essential requirement is that the business must

have effective management accounting system. This is pertaining to the fact that when the MA

system will be effective then complete and effective analysis will take place of the whole

business (Zyznarska-Dworczak, 2018). Thus, this will result in successful and effective decision

making for the betterment of the company. The major importance and prerequisite of

management accounting are as follows-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The major importance of using different types of management accounting systems is that

this assists in effective decision making (Quinn and et.al., 2018). The reason pertaining to this

fact is that when management accountants evaluate the financial performance and other aspect of

the companies then this reflects that they will take effective decisions. Hence, this will assist

managers in taking proper and in- depth decision for the development and growth of the

company.

Along with this MA systems are also of importance as this assists the companies in doing

proper planning for the organization. This is pertaining to the act that with help of the financial

performance analysis the managers can predict the future performance and plan strategies in

accordance to the financial performance of the company.

In addition to this another major prerequisite for the proper use of management

accounting system within companies is that this assists in controlling different business

operations. The reason underlying this fact is that when the manager analyses the financial

performance then they come to know the areas in which company is lacking and the areas

wherein company is good. Hence, they can decide for the strategies to control the areas at which

company is not much effective and try to improve those. Along with this company can try to

manage and maintain the areas in which company is good and always try to improve those areas.

Furthermore, proper use of MA systems will assist the company in having good strategic

management. This is pertaining to the fact that when the company is going to evaluate each and

every aspect of the business then they will come to know complete business working and they

will be in position to effectively manage the business and its different strategies.

Moreover, another important prerequisite of MA systems is that this assists managers and

decision makers to make effective budgets. This is pertaining to the fact that when managers

know that how much cost is applicable to which product and how much profit can be generated.

Then in that case these managers can easily predict the cost and income and an estimated budget

can be prepared (Fleischman and McLean, 2020). This budget will be helpful for the business as

this will assist the other employees to know the limit in which they have to perform the task and

make their products and services.

1.2

Management accounting reporting are the documents which are helpful to the company to

record the relevant data and information. These reports are assistive to the companies as they can

this assists in effective decision making (Quinn and et.al., 2018). The reason pertaining to this

fact is that when management accountants evaluate the financial performance and other aspect of

the companies then this reflects that they will take effective decisions. Hence, this will assist

managers in taking proper and in- depth decision for the development and growth of the

company.

Along with this MA systems are also of importance as this assists the companies in doing

proper planning for the organization. This is pertaining to the act that with help of the financial

performance analysis the managers can predict the future performance and plan strategies in

accordance to the financial performance of the company.

In addition to this another major prerequisite for the proper use of management

accounting system within companies is that this assists in controlling different business

operations. The reason underlying this fact is that when the manager analyses the financial

performance then they come to know the areas in which company is lacking and the areas

wherein company is good. Hence, they can decide for the strategies to control the areas at which

company is not much effective and try to improve those. Along with this company can try to

manage and maintain the areas in which company is good and always try to improve those areas.

Furthermore, proper use of MA systems will assist the company in having good strategic

management. This is pertaining to the fact that when the company is going to evaluate each and

every aspect of the business then they will come to know complete business working and they

will be in position to effectively manage the business and its different strategies.

Moreover, another important prerequisite of MA systems is that this assists managers and

decision makers to make effective budgets. This is pertaining to the fact that when managers

know that how much cost is applicable to which product and how much profit can be generated.

Then in that case these managers can easily predict the cost and income and an estimated budget

can be prepared (Fleischman and McLean, 2020). This budget will be helpful for the business as

this will assist the other employees to know the limit in which they have to perform the task and

make their products and services.

1.2

Management accounting reporting are the documents which are helpful to the company to

record the relevant data and information. These reports are assistive to the companies as they can

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

view this information and facts and figures later whenever there is requirement. These reporting

are guidance to the manager in taking effective decision as this records all the past data and

future decision are taken by analysing the past records and performance only (Doktoralina and

Apollo, 2019). Hence, he different types of the management accounting reports which are used

by the companies are as follows-

Inventory management system- it is a type of report which is being used by the

companies in order to record all the data and information relating to inventory which is coming

within the company. Along with this every little detail of allocation of the inventory to different

types of product is also being recorded and this assist in proper decision making. The reason

beneath this is the fact that these records can be analysed and compared with the current rates

and quantity and then in accordance to the requirement the inventory can be ordered.

Job costing system- this is another type of report which is prepared wherein the job

costing method is being applicable. The reason pertaining to the fact is that this is a type of

system which involves dividing the activities on the basis of different jobs present in the

company. Under this system or report all the cost is being allocated on the basis of the job and

the profit of every job is being individually presented. Hence, this report is of relevance to the

company as this provides information to the manager that every job involves how much cost and

with that how much profit can be generated. Thus, the manager can allocate cost to that

particular job on that basis only.

Price optimisation- this price optimisation is a mathematical tool which assist company

and manager in calculating that how the demand of the product varied at different price levels.

This system or report is helpful in deciding the fact that earlier how the demand of product

fluctuated with changes in price level. This is pertaining to the fact that this will guide the

decision takers that at what price they must sell their product so that demand will not vary and

consumer will like the rates.

1.3

The use of different management accounting system is very beneficial and helpful for the

companies (Drury, 2018). This is pertaining to the fact that these systems like job costing,

inventory management, price optimisation and others assist companies in taking better and

effective decision. The major benefits of using these systems are as follows-

are guidance to the manager in taking effective decision as this records all the past data and

future decision are taken by analysing the past records and performance only (Doktoralina and

Apollo, 2019). Hence, he different types of the management accounting reports which are used

by the companies are as follows-

Inventory management system- it is a type of report which is being used by the

companies in order to record all the data and information relating to inventory which is coming

within the company. Along with this every little detail of allocation of the inventory to different

types of product is also being recorded and this assist in proper decision making. The reason

beneath this is the fact that these records can be analysed and compared with the current rates

and quantity and then in accordance to the requirement the inventory can be ordered.

Job costing system- this is another type of report which is prepared wherein the job

costing method is being applicable. The reason pertaining to the fact is that this is a type of

system which involves dividing the activities on the basis of different jobs present in the

company. Under this system or report all the cost is being allocated on the basis of the job and

the profit of every job is being individually presented. Hence, this report is of relevance to the

company as this provides information to the manager that every job involves how much cost and

with that how much profit can be generated. Thus, the manager can allocate cost to that

particular job on that basis only.

Price optimisation- this price optimisation is a mathematical tool which assist company

and manager in calculating that how the demand of the product varied at different price levels.

This system or report is helpful in deciding the fact that earlier how the demand of product

fluctuated with changes in price level. This is pertaining to the fact that this will guide the

decision takers that at what price they must sell their product so that demand will not vary and

consumer will like the rates.

1.3

The use of different management accounting system is very beneficial and helpful for the

companies (Drury, 2018). This is pertaining to the fact that these systems like job costing,

inventory management, price optimisation and others assist companies in taking better and

effective decision. The major benefits of using these systems are as follows-

The major benefit is that with help of these systems the managers are able to have

updated information. This is pertaining to the fact that when the company and manager analyses

the past information then only then they can analyse what is currently going on (Speckbacher,

2017). The reason to this is that when the person will compare the present and past information

then only they can realise that whether the data has been upgraded or being degraded and

accordingly they have to take the decisions.

In addition to this another benefit of using this variety of MA systems is accuracy of

information. The underlying reason for this is that when the manager is able to compare the

current facts and figures with past then they can identify the trends in both the data that is

whether it is increasing or decreasing. The reason pertaining to this fact is that when both past

and present record will have same trend then it can be stated that the data is accurate and

decisions are taken in correct manner.

1.4

As per the views of the Endenich and Trapp (2020) both management accounting system

and reports are very essential for the success of the company. When both the system and reports

are integrated together then this provides a wider base to manager at time of taking the decisions.

Hence, this will always result in the better evaluation and effective decision making. On the

other side, Abernethy and Wallis (2019) argues that in case there is not proper integration and

coordination among system and report then there are possibilities that there is mismatch within

the information and this can affect performance of company.

For the success of the company it is very important for them to record and manage all the

different types of reports. The reason behind their importance is that this will provide a wider

database to the managers of company at time of taking decision. Along with this when the past

data is being recorded within the reports then this can be compared with the present data. In

addition to this the present data in reports can also be compared with the data of competitors and

the present position within highly competitive market can also be analysed and evaluated

(Cooper, Ezzamel and Qu, 2017). As a result of this, it will assist company in more effective and

efficient decision making and will improve the performance of the company in comparison to its

competitors.

updated information. This is pertaining to the fact that when the company and manager analyses

the past information then only then they can analyse what is currently going on (Speckbacher,

2017). The reason to this is that when the person will compare the present and past information

then only they can realise that whether the data has been upgraded or being degraded and

accordingly they have to take the decisions.

In addition to this another benefit of using this variety of MA systems is accuracy of

information. The underlying reason for this is that when the manager is able to compare the

current facts and figures with past then they can identify the trends in both the data that is

whether it is increasing or decreasing. The reason pertaining to this fact is that when both past

and present record will have same trend then it can be stated that the data is accurate and

decisions are taken in correct manner.

1.4

As per the views of the Endenich and Trapp (2020) both management accounting system

and reports are very essential for the success of the company. When both the system and reports

are integrated together then this provides a wider base to manager at time of taking the decisions.

Hence, this will always result in the better evaluation and effective decision making. On the

other side, Abernethy and Wallis (2019) argues that in case there is not proper integration and

coordination among system and report then there are possibilities that there is mismatch within

the information and this can affect performance of company.

For the success of the company it is very important for them to record and manage all the

different types of reports. The reason behind their importance is that this will provide a wider

database to the managers of company at time of taking decision. Along with this when the past

data is being recorded within the reports then this can be compared with the present data. In

addition to this the present data in reports can also be compared with the data of competitors and

the present position within highly competitive market can also be analysed and evaluated

(Cooper, Ezzamel and Qu, 2017). As a result of this, it will assist company in more effective and

efficient decision making and will improve the performance of the company in comparison to its

competitors.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Section 2

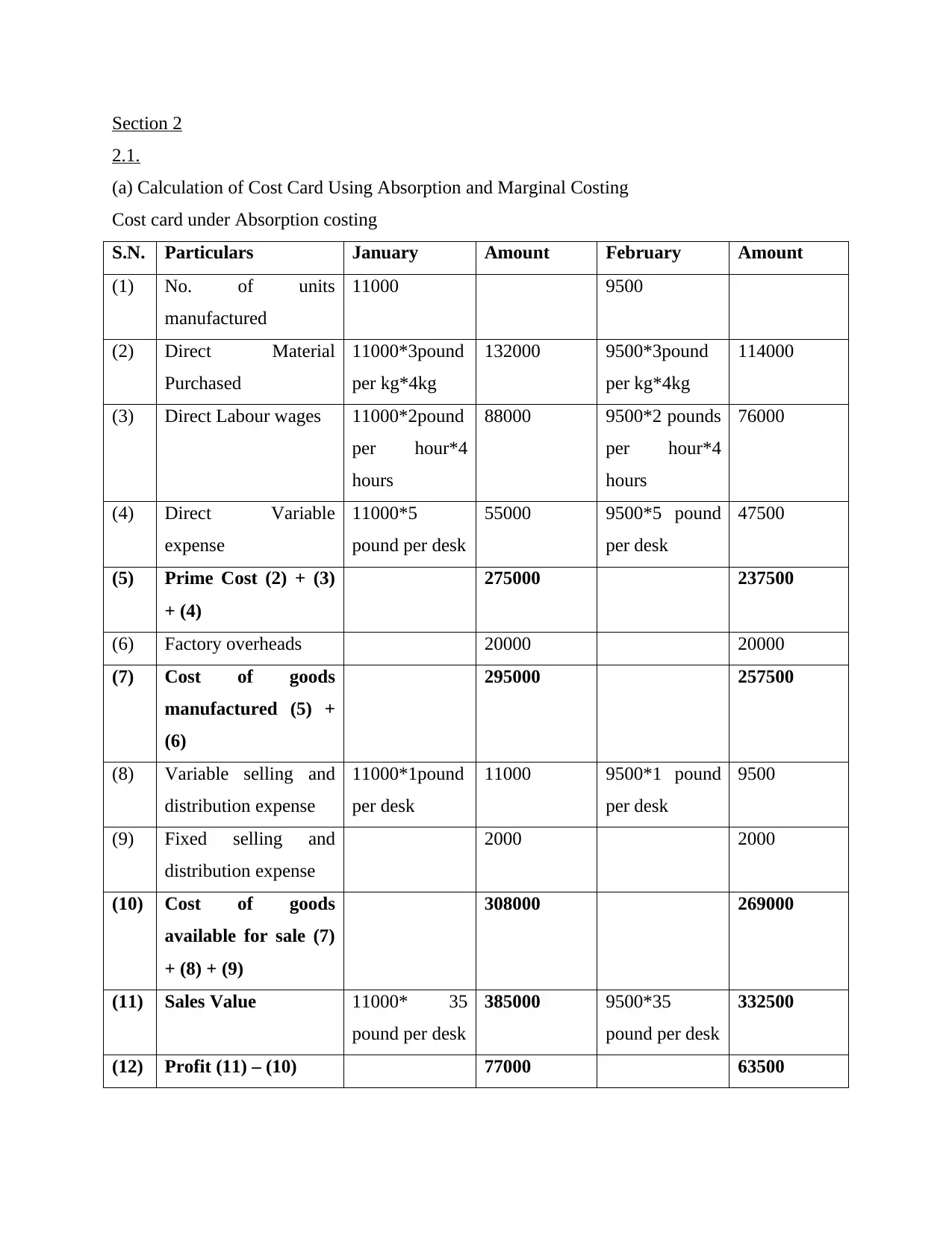

2.1.

(a) Calculation of Cost Card Using Absorption and Marginal Costing

Cost card under Absorption costing

S.N. Particulars January Amount February Amount

(1) No. of units

manufactured

11000 9500

(2) Direct Material

Purchased

11000*3pound

per kg*4kg

132000 9500*3pound

per kg*4kg

114000

(3) Direct Labour wages 11000*2pound

per hour*4

hours

88000 9500*2 pounds

per hour*4

hours

76000

(4) Direct Variable

expense

11000*5

pound per desk

55000 9500*5 pound

per desk

47500

(5) Prime Cost (2) + (3)

+ (4)

275000 237500

(6) Factory overheads 20000 20000

(7) Cost of goods

manufactured (5) +

(6)

295000 257500

(8) Variable selling and

distribution expense

11000*1pound

per desk

11000 9500*1 pound

per desk

9500

(9) Fixed selling and

distribution expense

2000 2000

(10) Cost of goods

available for sale (7)

+ (8) + (9)

308000 269000

(11) Sales Value 11000* 35

pound per desk

385000 9500*35

pound per desk

332500

(12) Profit (11) – (10) 77000 63500

2.1.

(a) Calculation of Cost Card Using Absorption and Marginal Costing

Cost card under Absorption costing

S.N. Particulars January Amount February Amount

(1) No. of units

manufactured

11000 9500

(2) Direct Material

Purchased

11000*3pound

per kg*4kg

132000 9500*3pound

per kg*4kg

114000

(3) Direct Labour wages 11000*2pound

per hour*4

hours

88000 9500*2 pounds

per hour*4

hours

76000

(4) Direct Variable

expense

11000*5

pound per desk

55000 9500*5 pound

per desk

47500

(5) Prime Cost (2) + (3)

+ (4)

275000 237500

(6) Factory overheads 20000 20000

(7) Cost of goods

manufactured (5) +

(6)

295000 257500

(8) Variable selling and

distribution expense

11000*1pound

per desk

11000 9500*1 pound

per desk

9500

(9) Fixed selling and

distribution expense

2000 2000

(10) Cost of goods

available for sale (7)

+ (8) + (9)

308000 269000

(11) Sales Value 11000* 35

pound per desk

385000 9500*35

pound per desk

332500

(12) Profit (11) – (10) 77000 63500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

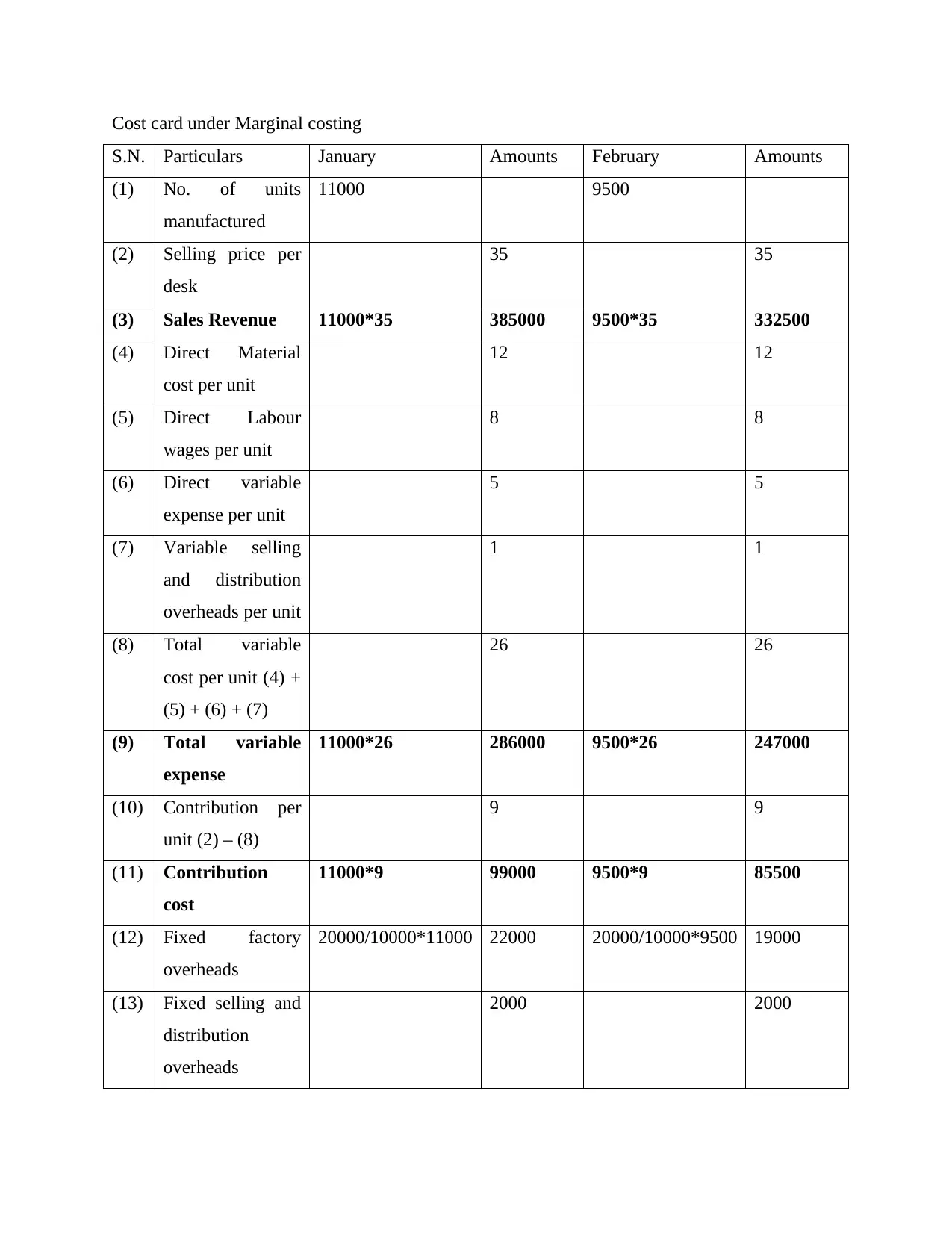

Cost card under Marginal costing

S.N. Particulars January Amounts February Amounts

(1) No. of units

manufactured

11000 9500

(2) Selling price per

desk

35 35

(3) Sales Revenue 11000*35 385000 9500*35 332500

(4) Direct Material

cost per unit

12 12

(5) Direct Labour

wages per unit

8 8

(6) Direct variable

expense per unit

5 5

(7) Variable selling

and distribution

overheads per unit

1 1

(8) Total variable

cost per unit (4) +

(5) + (6) + (7)

26 26

(9) Total variable

expense

11000*26 286000 9500*26 247000

(10) Contribution per

unit (2) – (8)

9 9

(11) Contribution

cost

11000*9 99000 9500*9 85500

(12) Fixed factory

overheads

20000/10000*11000 22000 20000/10000*9500 19000

(13) Fixed selling and

distribution

overheads

2000 2000

S.N. Particulars January Amounts February Amounts

(1) No. of units

manufactured

11000 9500

(2) Selling price per

desk

35 35

(3) Sales Revenue 11000*35 385000 9500*35 332500

(4) Direct Material

cost per unit

12 12

(5) Direct Labour

wages per unit

8 8

(6) Direct variable

expense per unit

5 5

(7) Variable selling

and distribution

overheads per unit

1 1

(8) Total variable

cost per unit (4) +

(5) + (6) + (7)

26 26

(9) Total variable

expense

11000*26 286000 9500*26 247000

(10) Contribution per

unit (2) – (8)

9 9

(11) Contribution

cost

11000*9 99000 9500*9 85500

(12) Fixed factory

overheads

20000/10000*11000 22000 20000/10000*9500 19000

(13) Fixed selling and

distribution

overheads

2000 2000

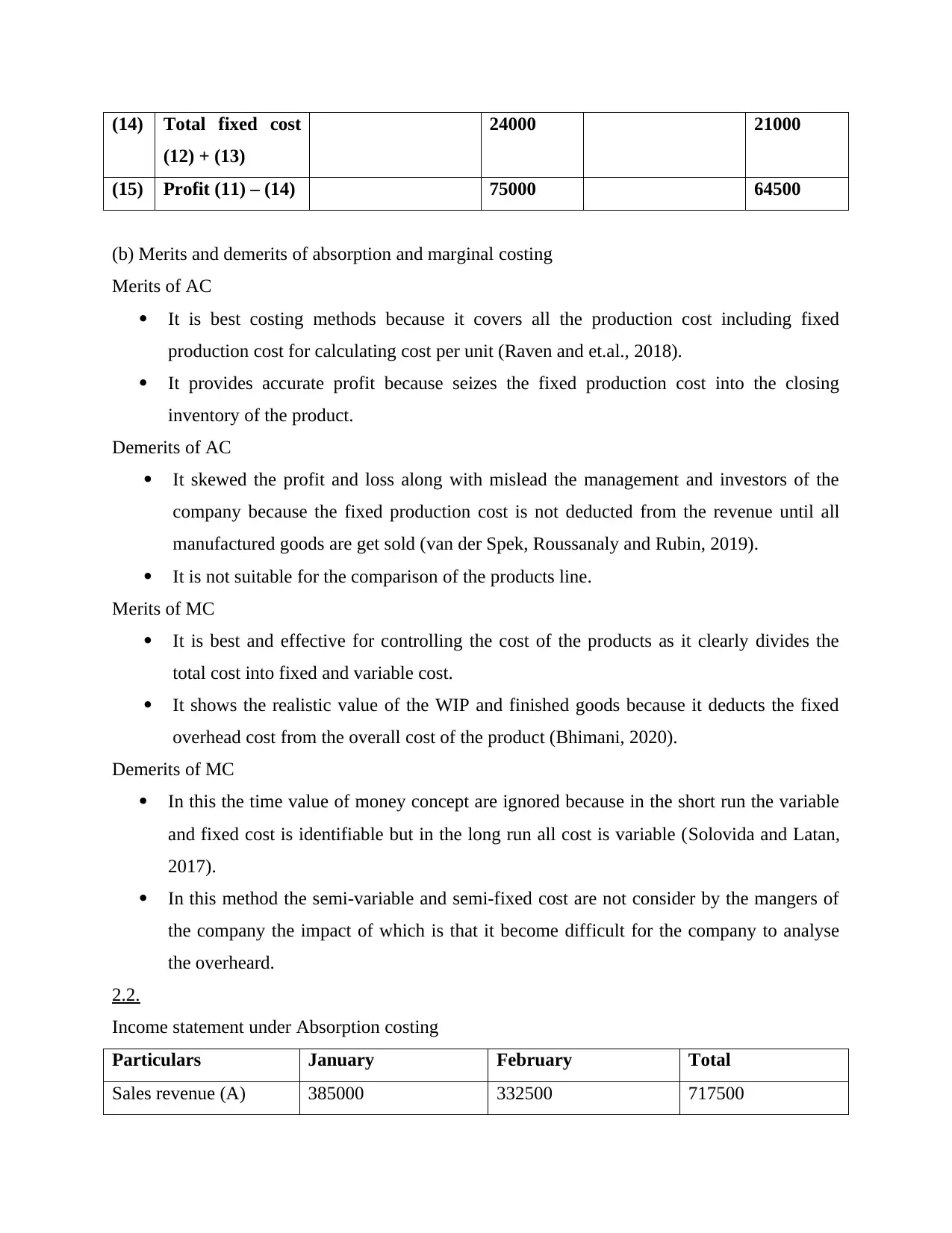

(14) Total fixed cost

(12) + (13)

24000 21000

(15) Profit (11) – (14) 75000 64500

(b) Merits and demerits of absorption and marginal costing

Merits of AC

It is best costing methods because it covers all the production cost including fixed

production cost for calculating cost per unit (Raven and et.al., 2018).

It provides accurate profit because seizes the fixed production cost into the closing

inventory of the product.

Demerits of AC

It skewed the profit and loss along with mislead the management and investors of the

company because the fixed production cost is not deducted from the revenue until all

manufactured goods are get sold (van der Spek, Roussanaly and Rubin, 2019).

It is not suitable for the comparison of the products line.

Merits of MC

It is best and effective for controlling the cost of the products as it clearly divides the

total cost into fixed and variable cost.

It shows the realistic value of the WIP and finished goods because it deducts the fixed

overhead cost from the overall cost of the product (Bhimani, 2020).

Demerits of MC

In this the time value of money concept are ignored because in the short run the variable

and fixed cost is identifiable but in the long run all cost is variable (Solovida and Latan,

2017).

In this method the semi-variable and semi-fixed cost are not consider by the mangers of

the company the impact of which is that it become difficult for the company to analyse

the overheard.

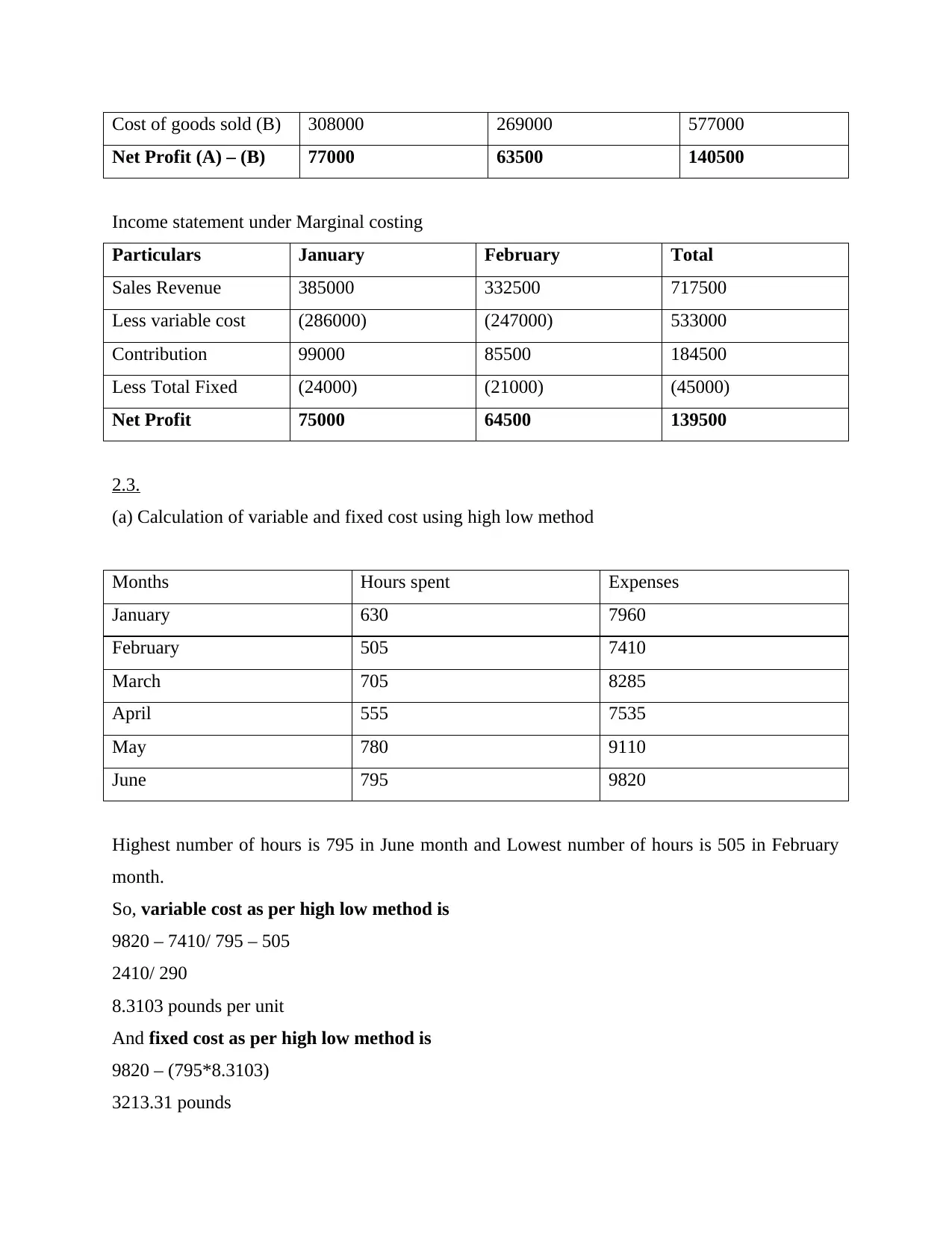

2.2.

Income statement under Absorption costing

Particulars January February Total

Sales revenue (A) 385000 332500 717500

(12) + (13)

24000 21000

(15) Profit (11) – (14) 75000 64500

(b) Merits and demerits of absorption and marginal costing

Merits of AC

It is best costing methods because it covers all the production cost including fixed

production cost for calculating cost per unit (Raven and et.al., 2018).

It provides accurate profit because seizes the fixed production cost into the closing

inventory of the product.

Demerits of AC

It skewed the profit and loss along with mislead the management and investors of the

company because the fixed production cost is not deducted from the revenue until all

manufactured goods are get sold (van der Spek, Roussanaly and Rubin, 2019).

It is not suitable for the comparison of the products line.

Merits of MC

It is best and effective for controlling the cost of the products as it clearly divides the

total cost into fixed and variable cost.

It shows the realistic value of the WIP and finished goods because it deducts the fixed

overhead cost from the overall cost of the product (Bhimani, 2020).

Demerits of MC

In this the time value of money concept are ignored because in the short run the variable

and fixed cost is identifiable but in the long run all cost is variable (Solovida and Latan,

2017).

In this method the semi-variable and semi-fixed cost are not consider by the mangers of

the company the impact of which is that it become difficult for the company to analyse

the overheard.

2.2.

Income statement under Absorption costing

Particulars January February Total

Sales revenue (A) 385000 332500 717500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost of goods sold (B) 308000 269000 577000

Net Profit (A) – (B) 77000 63500 140500

Income statement under Marginal costing

Particulars January February Total

Sales Revenue 385000 332500 717500

Less variable cost (286000) (247000) 533000

Contribution 99000 85500 184500

Less Total Fixed (24000) (21000) (45000)

Net Profit 75000 64500 139500

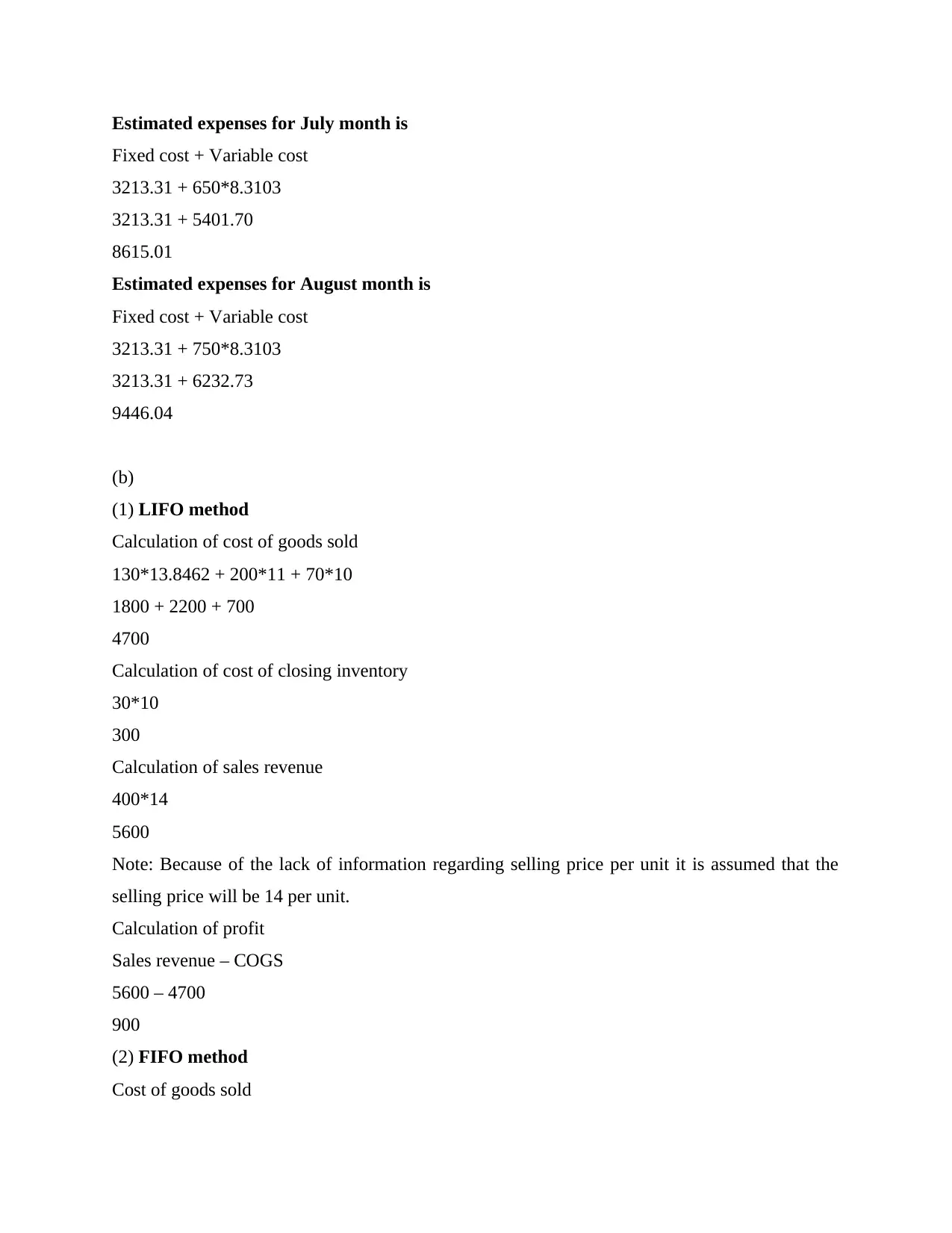

2.3.

(a) Calculation of variable and fixed cost using high low method

Months Hours spent Expenses

January 630 7960

February 505 7410

March 705 8285

April 555 7535

May 780 9110

June 795 9820

Highest number of hours is 795 in June month and Lowest number of hours is 505 in February

month.

So, variable cost as per high low method is

9820 – 7410/ 795 – 505

2410/ 290

8.3103 pounds per unit

And fixed cost as per high low method is

9820 – (795*8.3103)

3213.31 pounds

Net Profit (A) – (B) 77000 63500 140500

Income statement under Marginal costing

Particulars January February Total

Sales Revenue 385000 332500 717500

Less variable cost (286000) (247000) 533000

Contribution 99000 85500 184500

Less Total Fixed (24000) (21000) (45000)

Net Profit 75000 64500 139500

2.3.

(a) Calculation of variable and fixed cost using high low method

Months Hours spent Expenses

January 630 7960

February 505 7410

March 705 8285

April 555 7535

May 780 9110

June 795 9820

Highest number of hours is 795 in June month and Lowest number of hours is 505 in February

month.

So, variable cost as per high low method is

9820 – 7410/ 795 – 505

2410/ 290

8.3103 pounds per unit

And fixed cost as per high low method is

9820 – (795*8.3103)

3213.31 pounds

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Estimated expenses for July month is

Fixed cost + Variable cost

3213.31 + 650*8.3103

3213.31 + 5401.70

8615.01

Estimated expenses for August month is

Fixed cost + Variable cost

3213.31 + 750*8.3103

3213.31 + 6232.73

9446.04

(b)

(1) LIFO method

Calculation of cost of goods sold

130*13.8462 + 200*11 + 70*10

1800 + 2200 + 700

4700

Calculation of cost of closing inventory

30*10

300

Calculation of sales revenue

400*14

5600

Note: Because of the lack of information regarding selling price per unit it is assumed that the

selling price will be 14 per unit.

Calculation of profit

Sales revenue – COGS

5600 – 4700

900

(2) FIFO method

Cost of goods sold

Fixed cost + Variable cost

3213.31 + 650*8.3103

3213.31 + 5401.70

8615.01

Estimated expenses for August month is

Fixed cost + Variable cost

3213.31 + 750*8.3103

3213.31 + 6232.73

9446.04

(b)

(1) LIFO method

Calculation of cost of goods sold

130*13.8462 + 200*11 + 70*10

1800 + 2200 + 700

4700

Calculation of cost of closing inventory

30*10

300

Calculation of sales revenue

400*14

5600

Note: Because of the lack of information regarding selling price per unit it is assumed that the

selling price will be 14 per unit.

Calculation of profit

Sales revenue – COGS

5600 – 4700

900

(2) FIFO method

Cost of goods sold

100*10 + 200*11 + 100* 13.8462

1000 + 2200 + 1385

4585

Cost of closing inventory

30*13.8462

415

Sales revenue

400*14

5700

Profit

5700 – 4585

1115

(3) AVCO method

Cost of goods sold

400*11.6279

4651

Cost of closing inventory

30*11.6279

349

Sales revenue

400*14

5700

Profit

5700 – 4651

1049

2.4.

(a) Calculation of Break-even point

Formula in terms of unit

Fixed cost/ (selling price per unit) – (Variable cost per unit)

£2,000,000/ £300 - £200

1000 + 2200 + 1385

4585

Cost of closing inventory

30*13.8462

415

Sales revenue

400*14

5700

Profit

5700 – 4585

1115

(3) AVCO method

Cost of goods sold

400*11.6279

4651

Cost of closing inventory

30*11.6279

349

Sales revenue

400*14

5700

Profit

5700 – 4651

1049

2.4.

(a) Calculation of Break-even point

Formula in terms of unit

Fixed cost/ (selling price per unit) – (Variable cost per unit)

£2,000,000/ £300 - £200

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.