Detailed Management Accounting Report: Excite Entertainment Limited

VerifiedAdded on 2023/01/19

|16

|4563

|47

Report

AI Summary

This report delves into the core principles of management accounting, offering a comparative analysis with financial accounting, and highlighting the significance of Management Accounting Systems (MAS). It uses Excite Entertainment Limited as a case study, examining various MAS such as cost accounting, inventory management, and job costing systems, along with their benefits. The report further explores different types of managerial reports including inventory, performance, accounts receivable ageing, and cost accounting reports, emphasizing the importance of accurate and relevant information. Additionally, it covers the absorption and marginal costing methods, outlining their advantages and disadvantages, providing a comprehensive overview of key management accounting concepts and techniques.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

TASK 2............................................................................................................................................7

TASK 3..........................................................................................................................................11

TASK 4..........................................................................................................................................12

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

TASK 2............................................................................................................................................7

TASK 3..........................................................................................................................................11

TASK 4..........................................................................................................................................12

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

The management accounting a way of guiding managers of business entities in order to

take corrective actions and steps (Oldroyd, 2017). Under this accounting monetary and non

monetary data are utilised for preparation of reports as well as these reports are prepared as

accordance of need of companies. In the report a company is selected that is Excite entertainment

limited. It is located in UK and operates in entertainment aspect. The project report covers

various MAS and MA reports. As well as two income statements are prepared by use of give

data. In addition, planning tools are also covered under the budget. Further, role of MAS in

sorting monetary issues is covered in the project report.

TASK 1

Section A

(a) Comparison between MA and Financial accounting.

Management accounting – It can be defined as a kind of accounting approach that is associated

with process of recording companies financial and non financial transactions in a systematic

manner. The purpose of recording these transactions is to produce internal managerial reports

which can be used at important decision level.

Financial accounting – This accounting is completely variant from above accounting. It is a type

of accounting which is linked with procedure of collecting monetary informations with an

objective of preparing monetary reports (Busco and Quattrone, 2015). These reports are being

used by both internal and external aspects for own purposes.

Difference :

Basis MA Financial accounting

Publication of

reports

The MA reports are prepared and

presented to internal users specially

for managers and board of directors.

While in this accounting, monetary

reports are presented to all

stakeholders who are linked with

companies.

The management accounting a way of guiding managers of business entities in order to

take corrective actions and steps (Oldroyd, 2017). Under this accounting monetary and non

monetary data are utilised for preparation of reports as well as these reports are prepared as

accordance of need of companies. In the report a company is selected that is Excite entertainment

limited. It is located in UK and operates in entertainment aspect. The project report covers

various MAS and MA reports. As well as two income statements are prepared by use of give

data. In addition, planning tools are also covered under the budget. Further, role of MAS in

sorting monetary issues is covered in the project report.

TASK 1

Section A

(a) Comparison between MA and Financial accounting.

Management accounting – It can be defined as a kind of accounting approach that is associated

with process of recording companies financial and non financial transactions in a systematic

manner. The purpose of recording these transactions is to produce internal managerial reports

which can be used at important decision level.

Financial accounting – This accounting is completely variant from above accounting. It is a type

of accounting which is linked with procedure of collecting monetary informations with an

objective of preparing monetary reports (Busco and Quattrone, 2015). These reports are being

used by both internal and external aspects for own purposes.

Difference :

Basis MA Financial accounting

Publication of

reports

The MA reports are prepared and

presented to internal users specially

for managers and board of directors.

While in this accounting, monetary

reports are presented to all

stakeholders who are linked with

companies.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Format of

preparing reports

There is no any specific format by

which reports can be prepared. Most

of the organisations, produce these

reports as per own suitability and

understanding.

On the other hand, in this accounting

it is necessary for companies to

prepare the monetary reports as

according to international financial

reporting standards.

Nature of

information

which is used

Under this accounting, both monetary

and non monetary information are

utilised by accountants for

preparation of reports.

In this, only monetary information is

applied for producing reports by

accountants.

Various types of MAS:

(b) Cost accounting system – This is an accounting system which is integrated with the

systematic process of gathering information about monetary aspects of different functions and

activities. On the basis of all collected data regards to cost of various aspects finance managers

of companies make corrective projection of futuristic expenditures. In addition, this accounting

system is widely used in those organisations wherein large number of monetary transactions are

done on regular interval. In the above chosen business entity Excite entertainment limited

company, their finance managers trace the usage of their monetary resources in different kind of

operations. It overall helps in making an effective control over expenditures.

(c) Inventory management system – In the context of this competitive business environment only

those companies can sustain who manage their costs and inventories in an effective manner

(Grace, Phillips and Shimpi, 2015). So basically, stock management system can be defined as

an accounting system that combines with the manufacturing department of companies and keeps

the detailed record about how much quantity of material are bought and how much quantity is

being used for production. By assessing useful information about stock, the production manager

of companies can trace daily consumption of material in manufacturing process and as per it

control total storage cost. In the aspect of above Excite entertainment limited company, their

managers of stock collect important data about how much number of gadgets are used in

organising events. As well as assess the requirement of purchasing new equipments.

preparing reports

There is no any specific format by

which reports can be prepared. Most

of the organisations, produce these

reports as per own suitability and

understanding.

On the other hand, in this accounting

it is necessary for companies to

prepare the monetary reports as

according to international financial

reporting standards.

Nature of

information

which is used

Under this accounting, both monetary

and non monetary information are

utilised by accountants for

preparation of reports.

In this, only monetary information is

applied for producing reports by

accountants.

Various types of MAS:

(b) Cost accounting system – This is an accounting system which is integrated with the

systematic process of gathering information about monetary aspects of different functions and

activities. On the basis of all collected data regards to cost of various aspects finance managers

of companies make corrective projection of futuristic expenditures. In addition, this accounting

system is widely used in those organisations wherein large number of monetary transactions are

done on regular interval. In the above chosen business entity Excite entertainment limited

company, their finance managers trace the usage of their monetary resources in different kind of

operations. It overall helps in making an effective control over expenditures.

(c) Inventory management system – In the context of this competitive business environment only

those companies can sustain who manage their costs and inventories in an effective manner

(Grace, Phillips and Shimpi, 2015). So basically, stock management system can be defined as

an accounting system that combines with the manufacturing department of companies and keeps

the detailed record about how much quantity of material are bought and how much quantity is

being used for production. By assessing useful information about stock, the production manager

of companies can trace daily consumption of material in manufacturing process and as per it

control total storage cost. In the aspect of above Excite entertainment limited company, their

managers of stock collect important data about how much number of gadgets are used in

organising events. As well as assess the requirement of purchasing new equipments.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(d) Job costing system – It is a type of accounting system that is associated with process of

accumulating cost of each produced output. The significance of this accounting system is that

due to information of each units' cost managers can focus on investing those units which are

profitable for them. It is essentially needed by organisations in the case when more then one

units are produced. In the aspect of above Excite entertainment limited company, their managers

are using this accounting system in order to gather information about each job's cost separately

that involves in the process of managing any kind of events or functions. As well as their finance

manager can become able to focus on those activities that are leading as cause of higher cost.

(e) Benefits of above described MAS.

Name of MAS Role for the business activities and operations

Cost accounting system This accounting system is related with process of predicting future

costs of operations and activities (Smith, 2015). In the aspect of

above chosen business entity Excite entertainment limited they are

getting advantage from this accounting system by minimising

unwanted expenditures.

Inventory management

system

This accounting system acts effectively by coordination of

production department. Such as in the context of above Excite

entertainment limited company, their event manager gather

information about total number of equipments and gadgets are used

in events and functions.

Job costing system This is an accounting system which computes each produced

outputs cost. In the above Excite entertainment limited company,

their managers calculate each individual activities' cost which

engage in process of organising any event.

Section B

(a) Various kind of managerial reports

MA reports – The term MA reports can be defined as those written document which include

information about monetary and non monetary aspects. These reports are prepared and published

accumulating cost of each produced output. The significance of this accounting system is that

due to information of each units' cost managers can focus on investing those units which are

profitable for them. It is essentially needed by organisations in the case when more then one

units are produced. In the aspect of above Excite entertainment limited company, their managers

are using this accounting system in order to gather information about each job's cost separately

that involves in the process of managing any kind of events or functions. As well as their finance

manager can become able to focus on those activities that are leading as cause of higher cost.

(e) Benefits of above described MAS.

Name of MAS Role for the business activities and operations

Cost accounting system This accounting system is related with process of predicting future

costs of operations and activities (Smith, 2015). In the aspect of

above chosen business entity Excite entertainment limited they are

getting advantage from this accounting system by minimising

unwanted expenditures.

Inventory management

system

This accounting system acts effectively by coordination of

production department. Such as in the context of above Excite

entertainment limited company, their event manager gather

information about total number of equipments and gadgets are used

in events and functions.

Job costing system This is an accounting system which computes each produced

outputs cost. In the above Excite entertainment limited company,

their managers calculate each individual activities' cost which

engage in process of organising any event.

Section B

(a) Various kind of managerial reports

MA reports – The term MA reports can be defined as those written document which include

information about monetary and non monetary aspects. These reports are prepared and published

to internal department of companies such as managers, board of directors, employees and many

more. The accountant of Excite entertainment limited company, produce different kinds of

reports which are mentioned below :

Inventory reports – Under these reports information regards to available commodities in

stores, is included. Basically, the stock reports are needed to be updated on a daily basis

because in business entities materials are utilised for production and prepared products

for selling. In the absence of this report, it can be difficult for companies to manage their

all materials and production process. In the aspect of above Excite entertainment limited

company, their event planners utilise important information about used equipments in

different functions and events.

Performance report – It is a kind of report which is helpful for managers in order to check

progress of different aspects (Sithole, Abeysekera and Paas, 2017). Mainly, in this report

information of actual and estimated outputs is included. As well as by utilising key

informations through this report, managers become able to trace the variances of different

aspects. In addition, by help of this report managers can decide about promotion and

growth of their employees. In the context of above Excite entertainment limited

company, their event managers get information about compared outcome of estimated

and actual revenues.

Account receivable ageing report – This is a type of report that contains information

about total debt amount of debtors who are liable to make payment to the company. As

accordance of this report, the finance managers of business entities can focus on those

debtors who are not making payment on time. In addition, it becomes easier for

companies to prepare cash budget because of information regards to total cash that is

needed to be collect from debtors. Same as in the aspect of above Excite entertainment

limited company, their managers make a systematic plan to collect debt amount from

those debtors who are making delay in payment of organised events.

Cost accounting report – This is a report which consists information about estimated and

actual cost of various operations (Burritt and Christ, 2017). Basically, it is prepared by

integration of cost accounting system because information. By assessing useful

information through this report, managers of companies easily highlight those activities

which become cause of monetary lose. In the aspect of above Excite entertainment

more. The accountant of Excite entertainment limited company, produce different kinds of

reports which are mentioned below :

Inventory reports – Under these reports information regards to available commodities in

stores, is included. Basically, the stock reports are needed to be updated on a daily basis

because in business entities materials are utilised for production and prepared products

for selling. In the absence of this report, it can be difficult for companies to manage their

all materials and production process. In the aspect of above Excite entertainment limited

company, their event planners utilise important information about used equipments in

different functions and events.

Performance report – It is a kind of report which is helpful for managers in order to check

progress of different aspects (Sithole, Abeysekera and Paas, 2017). Mainly, in this report

information of actual and estimated outputs is included. As well as by utilising key

informations through this report, managers become able to trace the variances of different

aspects. In addition, by help of this report managers can decide about promotion and

growth of their employees. In the context of above Excite entertainment limited

company, their event managers get information about compared outcome of estimated

and actual revenues.

Account receivable ageing report – This is a type of report that contains information

about total debt amount of debtors who are liable to make payment to the company. As

accordance of this report, the finance managers of business entities can focus on those

debtors who are not making payment on time. In addition, it becomes easier for

companies to prepare cash budget because of information regards to total cash that is

needed to be collect from debtors. Same as in the aspect of above Excite entertainment

limited company, their managers make a systematic plan to collect debt amount from

those debtors who are making delay in payment of organised events.

Cost accounting report – This is a report which consists information about estimated and

actual cost of various operations (Burritt and Christ, 2017). Basically, it is prepared by

integration of cost accounting system because information. By assessing useful

information through this report, managers of companies easily highlight those activities

which become cause of monetary lose. In the aspect of above Excite entertainment

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

limited company, their event planners are using this report for calculating cost of each

activities which occur in process of organising different events and functions.

So these are the key MA reports.

(b) Why information should be accurate and relevant to user.

This is important that accounting information should be accurate and understandable so

that managers can relay on that in order to take important decisions. Below some characteristics

of good information are demonstrated that are as follows such as :

Accuracy – It is one of the important characteristics of accounting information that it

should be accurate because if information will not be correct then it can be difficult for

managers to take corrective actions.

Relevancy – In addition, the accounting information should be relevant to business

transactions (Christopher, 2016). This is so because if information will not be relevant

then it can be difficult for businesses to create competitive strategies.

Reliable and up to date – As well as accounting information should be reliable and

updated because financial transactions are done day by day in companies. Thus, it is

important to keep updated to accounting informations.

Presentation of data on time – Apart from these characteristics, another important

characteristics of accounting information is that it should be presented to stakeholders on

right time whenever managers need.

Hence, these are the main characteristics of good accounting information.

TASK 2

Section (A)

Absorption and marginal costing method:

There are mainly two kinds of costing techniques which are used by accountants in order

to produce income statements at the end of year that are as follows :

Absorption costing – It is a type of method of preparation of income statement in that both fixed

and flexible costs are assigned as cost of product. As well as absorbed in fully manner during

activities which occur in process of organising different events and functions.

So these are the key MA reports.

(b) Why information should be accurate and relevant to user.

This is important that accounting information should be accurate and understandable so

that managers can relay on that in order to take important decisions. Below some characteristics

of good information are demonstrated that are as follows such as :

Accuracy – It is one of the important characteristics of accounting information that it

should be accurate because if information will not be correct then it can be difficult for

managers to take corrective actions.

Relevancy – In addition, the accounting information should be relevant to business

transactions (Christopher, 2016). This is so because if information will not be relevant

then it can be difficult for businesses to create competitive strategies.

Reliable and up to date – As well as accounting information should be reliable and

updated because financial transactions are done day by day in companies. Thus, it is

important to keep updated to accounting informations.

Presentation of data on time – Apart from these characteristics, another important

characteristics of accounting information is that it should be presented to stakeholders on

right time whenever managers need.

Hence, these are the main characteristics of good accounting information.

TASK 2

Section (A)

Absorption and marginal costing method:

There are mainly two kinds of costing techniques which are used by accountants in order

to produce income statements at the end of year that are as follows :

Absorption costing – It is a type of method of preparation of income statement in that both fixed

and flexible costs are assigned as cost of product. As well as absorbed in fully manner during

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

computation of cost. This method has some drawbacks and benefits that are demonstrated below

such as :

Advantages -

Tracks profit in an accurate manner – It is one of the important benefit of this method that

in this profits are calculated in a corrective manner. Basically, by help of it businesses

can view an accurate picture of profits in front of stakeholders.

Accounts for all production costs – Along with the above benefit, another importance of

this technique is that under it all types of costs are absorbed. As well as accountants

become able to keep record of different costs such as direct material, rents, salaries &

wages and many more.

Disadvantages :

Does not help in improvement of efficiency – Basically, this costing technique does not

help in the aspect of enhancing efficiency (Webb and Chaffer, 2016). It is so because in

the case when fixed cost is higher then this may become difficult to find out variation in

cost. Due to this, it becomes tough for managerial aspects to take crucial decisions in

order to improve operational efficiency. Not useful for comparison of product lines – By implementation of this costing technique

for preparation of income statements, companies can not compare their profits at different

lines of product.

Marginal costing – This is a costing technique in which both costs are assigned in different

manner such as fixed cost as period cost. On the other hand, flexible cost as unit cost. Same as

the above method, it also has some limitations and benefits that are as follows :

Advantages -

Constant in nature – In the short time period, the variable cost flex time to time but in

long time period the marginal cost remain same.

Better control over cost – As well as by help of this method, companies can become able

to keep an effective control over cost. It is so because under this, both costs are

categorised separately and fixed cost is excluded from total production cost.

Disadvantages -

such as :

Advantages -

Tracks profit in an accurate manner – It is one of the important benefit of this method that

in this profits are calculated in a corrective manner. Basically, by help of it businesses

can view an accurate picture of profits in front of stakeholders.

Accounts for all production costs – Along with the above benefit, another importance of

this technique is that under it all types of costs are absorbed. As well as accountants

become able to keep record of different costs such as direct material, rents, salaries &

wages and many more.

Disadvantages :

Does not help in improvement of efficiency – Basically, this costing technique does not

help in the aspect of enhancing efficiency (Webb and Chaffer, 2016). It is so because in

the case when fixed cost is higher then this may become difficult to find out variation in

cost. Due to this, it becomes tough for managerial aspects to take crucial decisions in

order to improve operational efficiency. Not useful for comparison of product lines – By implementation of this costing technique

for preparation of income statements, companies can not compare their profits at different

lines of product.

Marginal costing – This is a costing technique in which both costs are assigned in different

manner such as fixed cost as period cost. On the other hand, flexible cost as unit cost. Same as

the above method, it also has some limitations and benefits that are as follows :

Advantages -

Constant in nature – In the short time period, the variable cost flex time to time but in

long time period the marginal cost remain same.

Better control over cost – As well as by help of this method, companies can become able

to keep an effective control over cost. It is so because under this, both costs are

categorised separately and fixed cost is excluded from total production cost.

Disadvantages -

Time element is ignored – One of the key drawback of this method is that under it, time

elements are ignored. This is so because in long time period, all types of costs varies at

different levels but in marginal costing method it is not considered.

Unrealistic assumption – Under this costing method, it is assumed that selling price will

remain constant at various production stage (Cooper, 2017). In the aspect of practical life

of businesses, it is not possible.

So as per the above critical evaluation, this can be guided to managers of Excite entertainment

limited company that they should apply absorption costing.

In the aspect of given data profit and loss account are prepared by help of both costing methods :

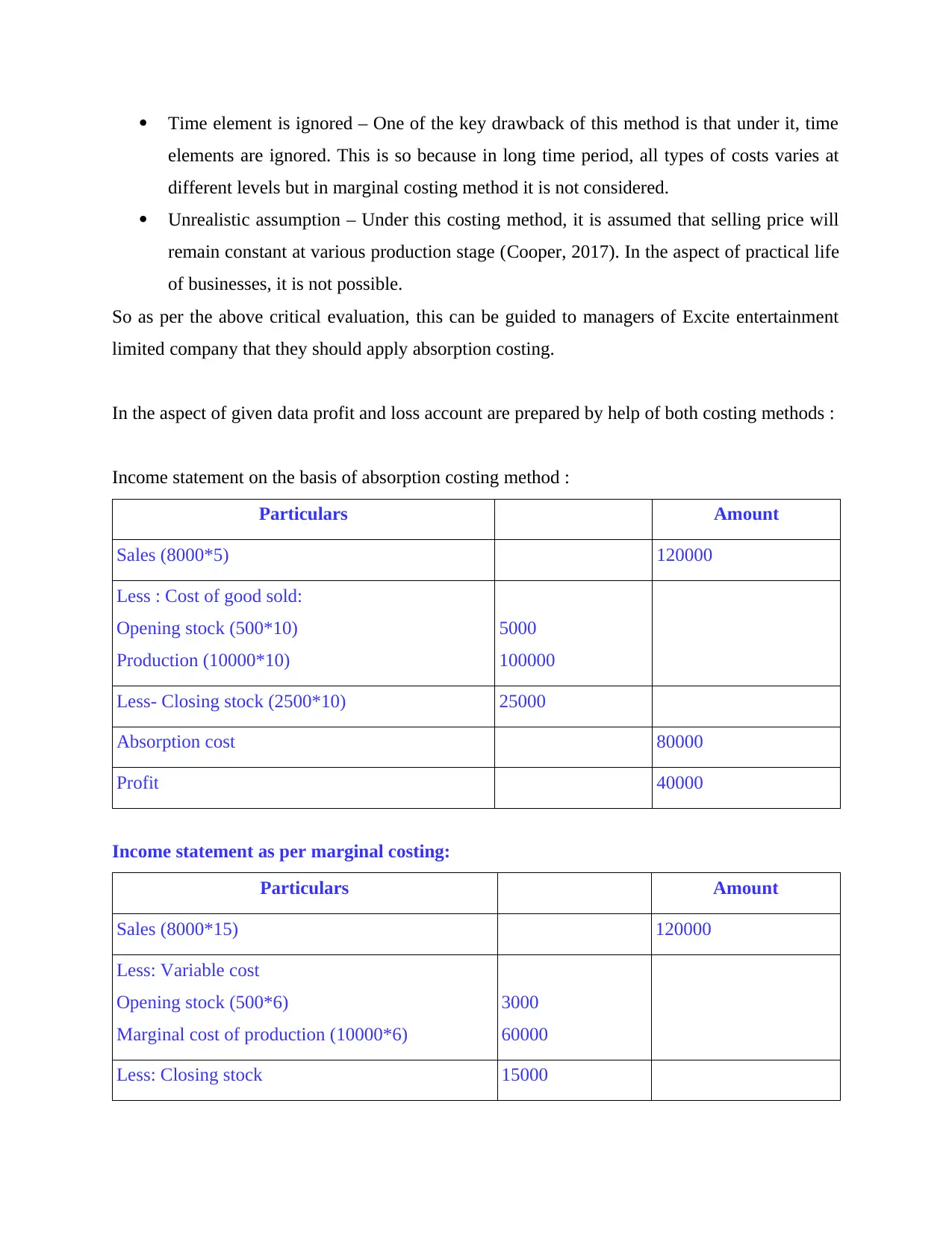

Income statement on the basis of absorption costing method :

Particulars Amount

Sales (8000*5) 120000

Less : Cost of good sold:

Opening stock (500*10)

Production (10000*10)

5000

100000

Less- Closing stock (2500*10) 25000

Absorption cost 80000

Profit 40000

Income statement as per marginal costing:

Particulars Amount

Sales (8000*15) 120000

Less: Variable cost

Opening stock (500*6)

Marginal cost of production (10000*6)

3000

60000

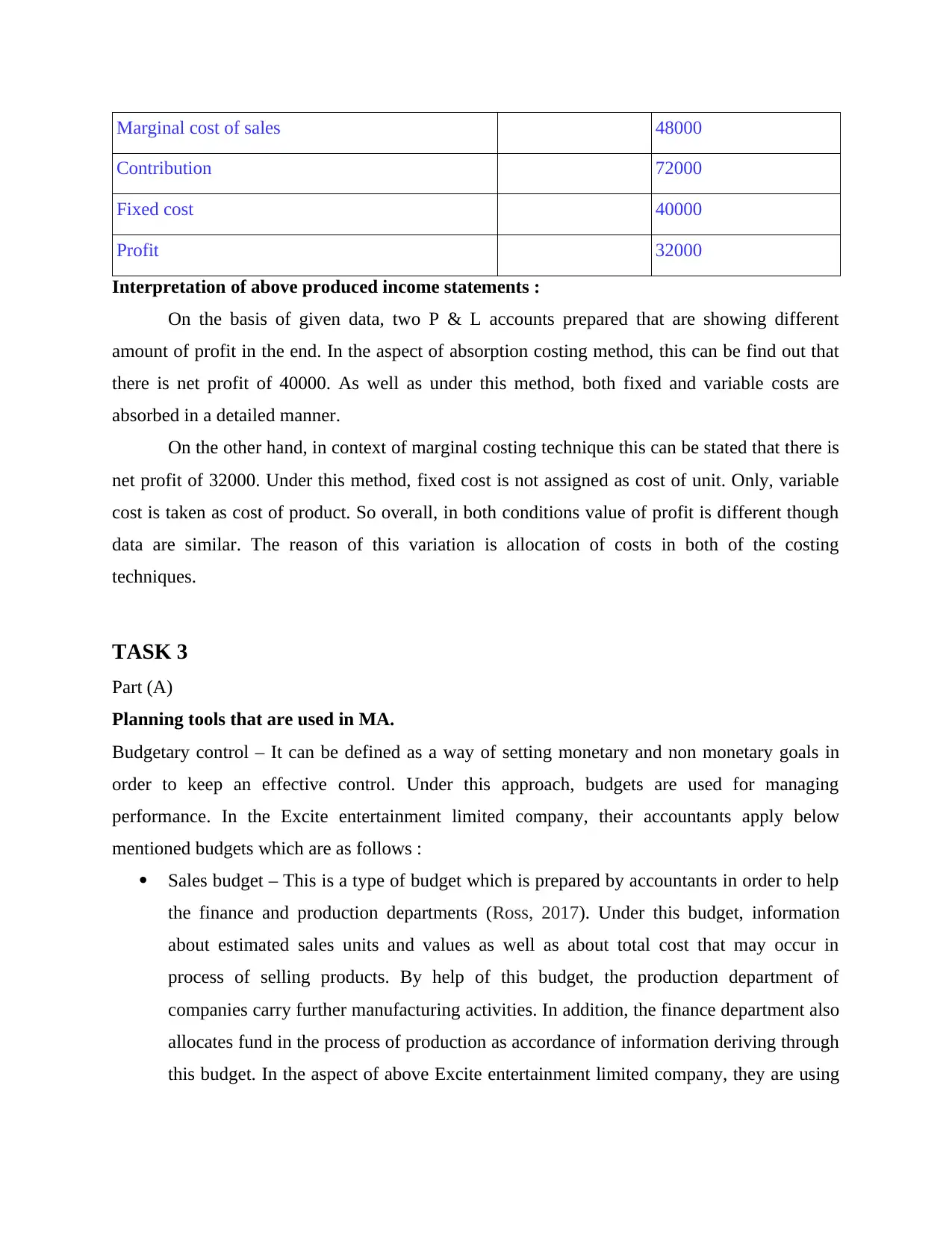

Less: Closing stock 15000

elements are ignored. This is so because in long time period, all types of costs varies at

different levels but in marginal costing method it is not considered.

Unrealistic assumption – Under this costing method, it is assumed that selling price will

remain constant at various production stage (Cooper, 2017). In the aspect of practical life

of businesses, it is not possible.

So as per the above critical evaluation, this can be guided to managers of Excite entertainment

limited company that they should apply absorption costing.

In the aspect of given data profit and loss account are prepared by help of both costing methods :

Income statement on the basis of absorption costing method :

Particulars Amount

Sales (8000*5) 120000

Less : Cost of good sold:

Opening stock (500*10)

Production (10000*10)

5000

100000

Less- Closing stock (2500*10) 25000

Absorption cost 80000

Profit 40000

Income statement as per marginal costing:

Particulars Amount

Sales (8000*15) 120000

Less: Variable cost

Opening stock (500*6)

Marginal cost of production (10000*6)

3000

60000

Less: Closing stock 15000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Marginal cost of sales 48000

Contribution 72000

Fixed cost 40000

Profit 32000

Interpretation of above produced income statements :

On the basis of given data, two P & L accounts prepared that are showing different

amount of profit in the end. In the aspect of absorption costing method, this can be find out that

there is net profit of 40000. As well as under this method, both fixed and variable costs are

absorbed in a detailed manner.

On the other hand, in context of marginal costing technique this can be stated that there is

net profit of 32000. Under this method, fixed cost is not assigned as cost of unit. Only, variable

cost is taken as cost of product. So overall, in both conditions value of profit is different though

data are similar. The reason of this variation is allocation of costs in both of the costing

techniques.

TASK 3

Part (A)

Planning tools that are used in MA.

Budgetary control – It can be defined as a way of setting monetary and non monetary goals in

order to keep an effective control. Under this approach, budgets are used for managing

performance. In the Excite entertainment limited company, their accountants apply below

mentioned budgets which are as follows :

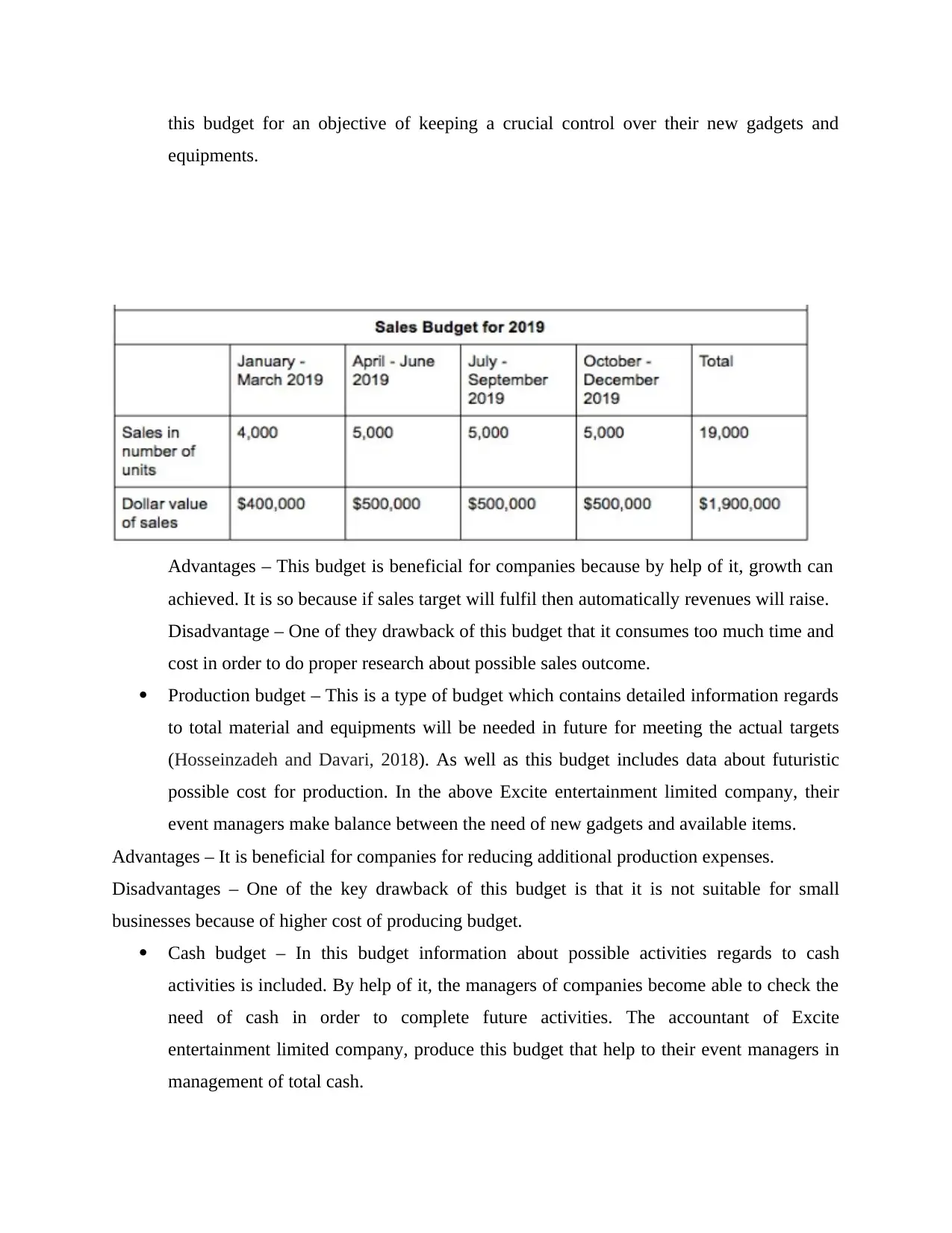

Sales budget – This is a type of budget which is prepared by accountants in order to help

the finance and production departments (Ross, 2017). Under this budget, information

about estimated sales units and values as well as about total cost that may occur in

process of selling products. By help of this budget, the production department of

companies carry further manufacturing activities. In addition, the finance department also

allocates fund in the process of production as accordance of information deriving through

this budget. In the aspect of above Excite entertainment limited company, they are using

Contribution 72000

Fixed cost 40000

Profit 32000

Interpretation of above produced income statements :

On the basis of given data, two P & L accounts prepared that are showing different

amount of profit in the end. In the aspect of absorption costing method, this can be find out that

there is net profit of 40000. As well as under this method, both fixed and variable costs are

absorbed in a detailed manner.

On the other hand, in context of marginal costing technique this can be stated that there is

net profit of 32000. Under this method, fixed cost is not assigned as cost of unit. Only, variable

cost is taken as cost of product. So overall, in both conditions value of profit is different though

data are similar. The reason of this variation is allocation of costs in both of the costing

techniques.

TASK 3

Part (A)

Planning tools that are used in MA.

Budgetary control – It can be defined as a way of setting monetary and non monetary goals in

order to keep an effective control. Under this approach, budgets are used for managing

performance. In the Excite entertainment limited company, their accountants apply below

mentioned budgets which are as follows :

Sales budget – This is a type of budget which is prepared by accountants in order to help

the finance and production departments (Ross, 2017). Under this budget, information

about estimated sales units and values as well as about total cost that may occur in

process of selling products. By help of this budget, the production department of

companies carry further manufacturing activities. In addition, the finance department also

allocates fund in the process of production as accordance of information deriving through

this budget. In the aspect of above Excite entertainment limited company, they are using

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

this budget for an objective of keeping a crucial control over their new gadgets and

equipments.

Advantages – This budget is beneficial for companies because by help of it, growth can

achieved. It is so because if sales target will fulfil then automatically revenues will raise.

Disadvantage – One of they drawback of this budget that it consumes too much time and

cost in order to do proper research about possible sales outcome.

Production budget – This is a type of budget which contains detailed information regards

to total material and equipments will be needed in future for meeting the actual targets

(Hosseinzadeh and Davari, 2018). As well as this budget includes data about futuristic

possible cost for production. In the above Excite entertainment limited company, their

event managers make balance between the need of new gadgets and available items.

Advantages – It is beneficial for companies for reducing additional production expenses.

Disadvantages – One of the key drawback of this budget is that it is not suitable for small

businesses because of higher cost of producing budget.

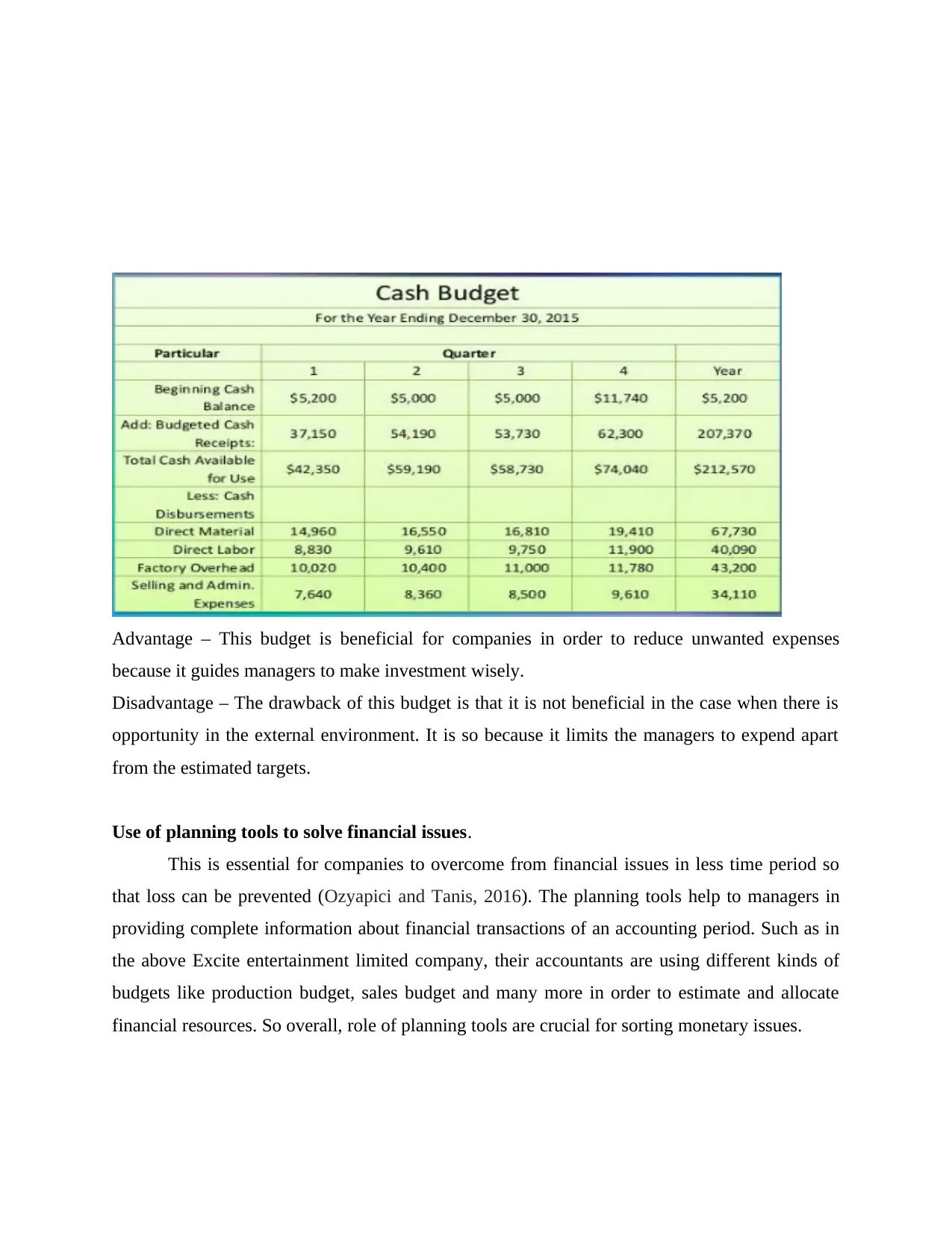

Cash budget – In this budget information about possible activities regards to cash

activities is included. By help of it, the managers of companies become able to check the

need of cash in order to complete future activities. The accountant of Excite

entertainment limited company, produce this budget that help to their event managers in

management of total cash.

equipments.

Advantages – This budget is beneficial for companies because by help of it, growth can

achieved. It is so because if sales target will fulfil then automatically revenues will raise.

Disadvantage – One of they drawback of this budget that it consumes too much time and

cost in order to do proper research about possible sales outcome.

Production budget – This is a type of budget which contains detailed information regards

to total material and equipments will be needed in future for meeting the actual targets

(Hosseinzadeh and Davari, 2018). As well as this budget includes data about futuristic

possible cost for production. In the above Excite entertainment limited company, their

event managers make balance between the need of new gadgets and available items.

Advantages – It is beneficial for companies for reducing additional production expenses.

Disadvantages – One of the key drawback of this budget is that it is not suitable for small

businesses because of higher cost of producing budget.

Cash budget – In this budget information about possible activities regards to cash

activities is included. By help of it, the managers of companies become able to check the

need of cash in order to complete future activities. The accountant of Excite

entertainment limited company, produce this budget that help to their event managers in

management of total cash.

Advantage – This budget is beneficial for companies in order to reduce unwanted expenses

because it guides managers to make investment wisely.

Disadvantage – The drawback of this budget is that it is not beneficial in the case when there is

opportunity in the external environment. It is so because it limits the managers to expend apart

from the estimated targets.

Use of planning tools to solve financial issues.

This is essential for companies to overcome from financial issues in less time period so

that loss can be prevented (Ozyapici and Tanis, 2016). The planning tools help to managers in

providing complete information about financial transactions of an accounting period. Such as in

the above Excite entertainment limited company, their accountants are using different kinds of

budgets like production budget, sales budget and many more in order to estimate and allocate

financial resources. So overall, role of planning tools are crucial for sorting monetary issues.

because it guides managers to make investment wisely.

Disadvantage – The drawback of this budget is that it is not beneficial in the case when there is

opportunity in the external environment. It is so because it limits the managers to expend apart

from the estimated targets.

Use of planning tools to solve financial issues.

This is essential for companies to overcome from financial issues in less time period so

that loss can be prevented (Ozyapici and Tanis, 2016). The planning tools help to managers in

providing complete information about financial transactions of an accounting period. Such as in

the above Excite entertainment limited company, their accountants are using different kinds of

budgets like production budget, sales budget and many more in order to estimate and allocate

financial resources. So overall, role of planning tools are crucial for sorting monetary issues.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.