Management Accounting Report: Activity Based Costing and Budgeting

VerifiedAdded on 2020/05/28

|10

|2211

|63

Report

AI Summary

This report provides an executive summary, table of contents, and detailed analysis of two case studies in management accounting. The first case focuses on US Bright product company and its use of activity-based costing (ABC) to determine per-unit costs, billing amounts, and additional costs related to Lamington production. It includes calculations of cost per activity driver and a bill of activities. The second case examines Hawthorn Leisure Works, a physical fitness center and tennis court facility, evaluating its budgeting methods and a proposed new revenue plan based solely on membership fees. The report compares the old and new plans, assessing their potential impact on revenue and recommending the adoption of the new plan due to its increased revenue potential and simplified fee structure. The report references key concepts of ABC, budgeting and financial analysis to support its conclusions.

Running Head: Management Accounting

Management Accounting

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting 2

Executive Summary:

This report is about the evaluation of two cases, first case is about activity based costing and

the second one is about Budgeting. In the first case evaluation of US bright product company

which is manufacture of cakes and pastries is to be done. The evaluation is regarding the

allocation of cost on the basis of cost drivers. The cost per unit is calculated by dividing the

overall cost or we can say total cost from the annual production quantity. Activity based

costing elaborates the relationship between activities, cost and products.

In this case the three parts need to be evaluated in first part per unit cost needs to be

calculated based on the activity cost drivers. In the second part the billing amount needs to be

calculated as well as the per unit cost need to be evaluated and lastly the additional cost

which is required to reach at the product cost of the US Bright need to be estimated.

The second case is about Hawthorn Leisure works which is a physical fitness centre and it

also offers tennis court facilities to its members. The budgeting is actually done to know

about the companies coming growth prospects and helps in the further decision making

process. In this scenario HLW want to implement a new plan to change the revenue structure

as under the old plan the revenue is collect from membership fee and the court fee and under

the new plan the revenue comprised of only membership fee.

Executive Summary:

This report is about the evaluation of two cases, first case is about activity based costing and

the second one is about Budgeting. In the first case evaluation of US bright product company

which is manufacture of cakes and pastries is to be done. The evaluation is regarding the

allocation of cost on the basis of cost drivers. The cost per unit is calculated by dividing the

overall cost or we can say total cost from the annual production quantity. Activity based

costing elaborates the relationship between activities, cost and products.

In this case the three parts need to be evaluated in first part per unit cost needs to be

calculated based on the activity cost drivers. In the second part the billing amount needs to be

calculated as well as the per unit cost need to be evaluated and lastly the additional cost

which is required to reach at the product cost of the US Bright need to be estimated.

The second case is about Hawthorn Leisure works which is a physical fitness centre and it

also offers tennis court facilities to its members. The budgeting is actually done to know

about the companies coming growth prospects and helps in the further decision making

process. In this scenario HLW want to implement a new plan to change the revenue structure

as under the old plan the revenue is collect from membership fee and the court fee and under

the new plan the revenue comprised of only membership fee.

Management Accounting 3

Table of Contents

Task A. (Activity Based Costing)..........................................................................................................4

Introduction:......................................................................................................................................4

Part (a) Cost per unit of activity driver..............................................................................................4

Part (b) Bill of Activities...................................................................................................................5

Part (c)...............................................................................................................................................6

Conclusion:........................................................................................................................................6

Task B Budgets to evaluate Business Decision.....................................................................................7

Introduction:......................................................................................................................................7

Part (a)...............................................................................................................................................8

Part (b)...............................................................................................................................................8

Part (c)...............................................................................................................................................9

Conclusion:........................................................................................................................................9

References:..........................................................................................................................................10

Table of Contents

Task A. (Activity Based Costing)..........................................................................................................4

Introduction:......................................................................................................................................4

Part (a) Cost per unit of activity driver..............................................................................................4

Part (b) Bill of Activities...................................................................................................................5

Part (c)...............................................................................................................................................6

Conclusion:........................................................................................................................................6

Task B Budgets to evaluate Business Decision.....................................................................................7

Introduction:......................................................................................................................................7

Part (a)...............................................................................................................................................8

Part (b)...............................................................................................................................................8

Part (c)...............................................................................................................................................9

Conclusion:........................................................................................................................................9

References:..........................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management Accounting 4

Task A. (Activity Based Costing)

Introduction:

Activity Based costing is the method of accounting that identifies the activities that are

performed by the firm and then allocate the cost on the basis of the activities performed by

the firm. ABC costing system is usually used in most of the manufacturing companies as it

enhances the cost classification and made the allocation of indirect easy (Heisinger, 2009).

ABC Costing system is used in product costing, customer profitability analysis and target

costing.

This present case is about the US Bright product company which produces cakes and pastries.

They use Activity Based Costing as their costing system. In the first part they need to know

the product cost on the basis of allocating the cost to the cost drivers. In the second part they

want the billing amount as well as per unit cost of producing cakes and pastries of

Lamington. Lastly the additional cost need to be determined which can be added in the

product cost to arrive at the total cost of Lamington.

Part (a) Cost per unit of activity driver

The cost per unit of activity driver is calculated by allocating the cost to their allocated cost

drivers (Wiese, 2009). With this we can also calculate the cost of producing one unit by

adding all the allocated costs. The cost drivers are assigned as per the nature of the cost. The

allocation is done by dividing the cost with its cost drivers. The statement need to be prepared

for allocating the cost to its cost drivers. That clearly shows the amount of cost and the

activity driver.

Calculation of Cost per Unit

Activity Activity Cost

Activity

Driver

Rate per

unit

Prepare annual Accounts 5,000.00

Process Receivables 15,000.00 5000 3.00

Process payables 25,000.00 2500 10.00

Program production 28,000.00 1000 28.00

Process Sales Order 40,000.00 4000 10.00

Dispatch sales Order 30,000.00 2500 12.00

Develop and test products 60,000.00

Load Mixers 14,050.00 1000 14.05

Operate Mixers 45,900.00 200000 0.23

Clean mixers 6,900.00 1000 6.90

Move mixture to filling 3,450.00 200000 0.02

Clean Trays 20,000.00 16000 1.25

Fill trays 16,000.00 800000 0.02

Move to Baking 8,000.00 16000 0.50

Set up ovens 50,000.00 1000 50.00

Task A. (Activity Based Costing)

Introduction:

Activity Based costing is the method of accounting that identifies the activities that are

performed by the firm and then allocate the cost on the basis of the activities performed by

the firm. ABC costing system is usually used in most of the manufacturing companies as it

enhances the cost classification and made the allocation of indirect easy (Heisinger, 2009).

ABC Costing system is used in product costing, customer profitability analysis and target

costing.

This present case is about the US Bright product company which produces cakes and pastries.

They use Activity Based Costing as their costing system. In the first part they need to know

the product cost on the basis of allocating the cost to the cost drivers. In the second part they

want the billing amount as well as per unit cost of producing cakes and pastries of

Lamington. Lastly the additional cost need to be determined which can be added in the

product cost to arrive at the total cost of Lamington.

Part (a) Cost per unit of activity driver

The cost per unit of activity driver is calculated by allocating the cost to their allocated cost

drivers (Wiese, 2009). With this we can also calculate the cost of producing one unit by

adding all the allocated costs. The cost drivers are assigned as per the nature of the cost. The

allocation is done by dividing the cost with its cost drivers. The statement need to be prepared

for allocating the cost to its cost drivers. That clearly shows the amount of cost and the

activity driver.

Calculation of Cost per Unit

Activity Activity Cost

Activity

Driver

Rate per

unit

Prepare annual Accounts 5,000.00

Process Receivables 15,000.00 5000 3.00

Process payables 25,000.00 2500 10.00

Program production 28,000.00 1000 28.00

Process Sales Order 40,000.00 4000 10.00

Dispatch sales Order 30,000.00 2500 12.00

Develop and test products 60,000.00

Load Mixers 14,050.00 1000 14.05

Operate Mixers 45,900.00 200000 0.23

Clean mixers 6,900.00 1000 6.90

Move mixture to filling 3,450.00 200000 0.02

Clean Trays 20,000.00 16000 1.25

Fill trays 16,000.00 800000 0.02

Move to Baking 8,000.00 16000 0.50

Set up ovens 50,000.00 1000 50.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting 5

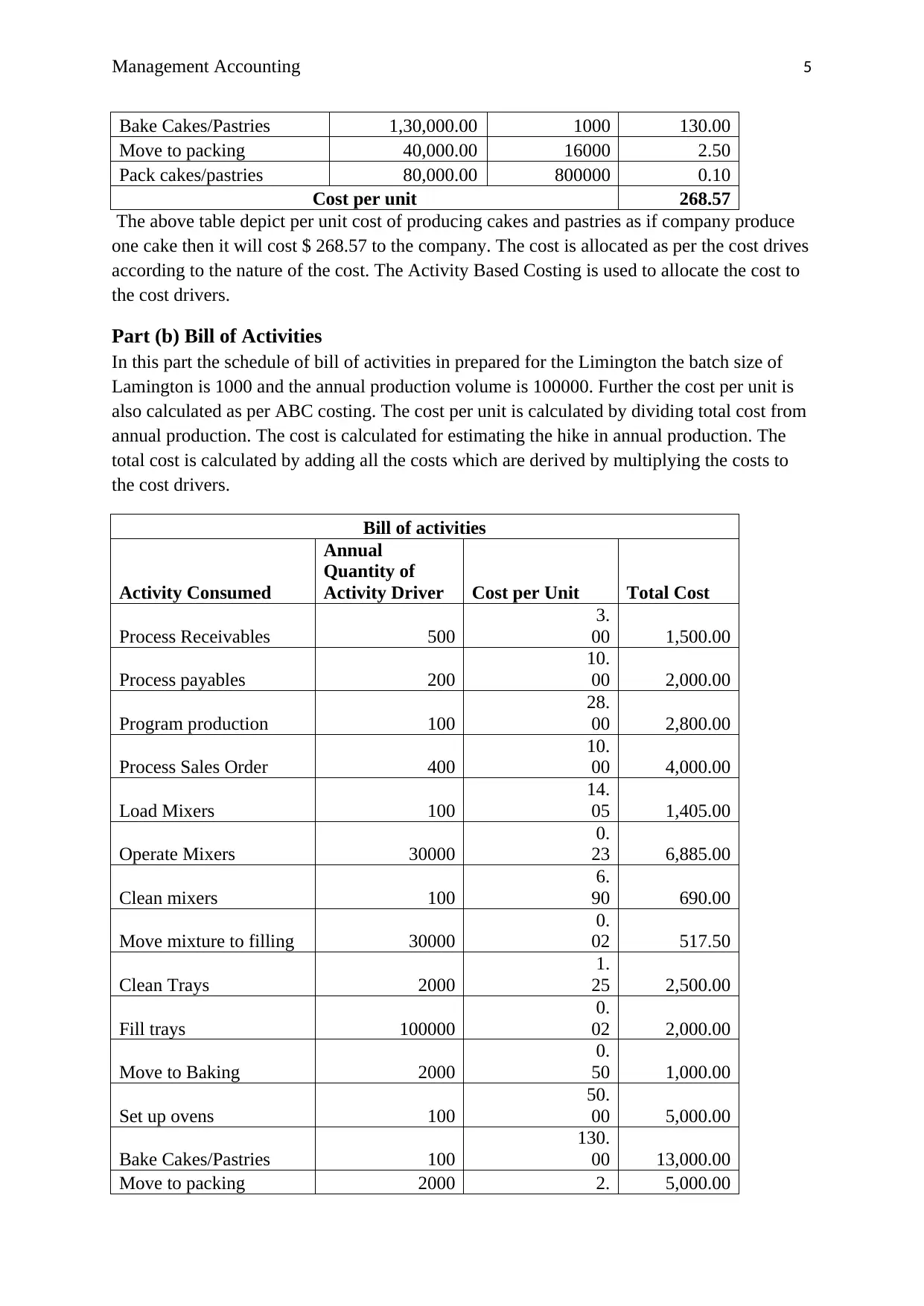

Bake Cakes/Pastries 1,30,000.00 1000 130.00

Move to packing 40,000.00 16000 2.50

Pack cakes/pastries 80,000.00 800000 0.10

Cost per unit 268.57

The above table depict per unit cost of producing cakes and pastries as if company produce

one cake then it will cost $ 268.57 to the company. The cost is allocated as per the cost drives

according to the nature of the cost. The Activity Based Costing is used to allocate the cost to

the cost drivers.

Part (b) Bill of Activities

In this part the schedule of bill of activities in prepared for the Limington the batch size of

Lamington is 1000 and the annual production volume is 100000. Further the cost per unit is

also calculated as per ABC costing. The cost per unit is calculated by dividing total cost from

annual production. The cost is calculated for estimating the hike in annual production. The

total cost is calculated by adding all the costs which are derived by multiplying the costs to

the cost drivers.

Bill of activities

Activity Consumed

Annual

Quantity of

Activity Driver Cost per Unit Total Cost

Process Receivables 500

3.

00 1,500.00

Process payables 200

10.

00 2,000.00

Program production 100

28.

00 2,800.00

Process Sales Order 400

10.

00 4,000.00

Load Mixers 100

14.

05 1,405.00

Operate Mixers 30000

0.

23 6,885.00

Clean mixers 100

6.

90 690.00

Move mixture to filling 30000

0.

02 517.50

Clean Trays 2000

1.

25 2,500.00

Fill trays 100000

0.

02 2,000.00

Move to Baking 2000

0.

50 1,000.00

Set up ovens 100

50.

00 5,000.00

Bake Cakes/Pastries 100

130.

00 13,000.00

Move to packing 2000 2. 5,000.00

Bake Cakes/Pastries 1,30,000.00 1000 130.00

Move to packing 40,000.00 16000 2.50

Pack cakes/pastries 80,000.00 800000 0.10

Cost per unit 268.57

The above table depict per unit cost of producing cakes and pastries as if company produce

one cake then it will cost $ 268.57 to the company. The cost is allocated as per the cost drives

according to the nature of the cost. The Activity Based Costing is used to allocate the cost to

the cost drivers.

Part (b) Bill of Activities

In this part the schedule of bill of activities in prepared for the Limington the batch size of

Lamington is 1000 and the annual production volume is 100000. Further the cost per unit is

also calculated as per ABC costing. The cost per unit is calculated by dividing total cost from

annual production. The cost is calculated for estimating the hike in annual production. The

total cost is calculated by adding all the costs which are derived by multiplying the costs to

the cost drivers.

Bill of activities

Activity Consumed

Annual

Quantity of

Activity Driver Cost per Unit Total Cost

Process Receivables 500

3.

00 1,500.00

Process payables 200

10.

00 2,000.00

Program production 100

28.

00 2,800.00

Process Sales Order 400

10.

00 4,000.00

Load Mixers 100

14.

05 1,405.00

Operate Mixers 30000

0.

23 6,885.00

Clean mixers 100

6.

90 690.00

Move mixture to filling 30000

0.

02 517.50

Clean Trays 2000

1.

25 2,500.00

Fill trays 100000

0.

02 2,000.00

Move to Baking 2000

0.

50 1,000.00

Set up ovens 100

50.

00 5,000.00

Bake Cakes/Pastries 100

130.

00 13,000.00

Move to packing 2000 2. 5,000.00

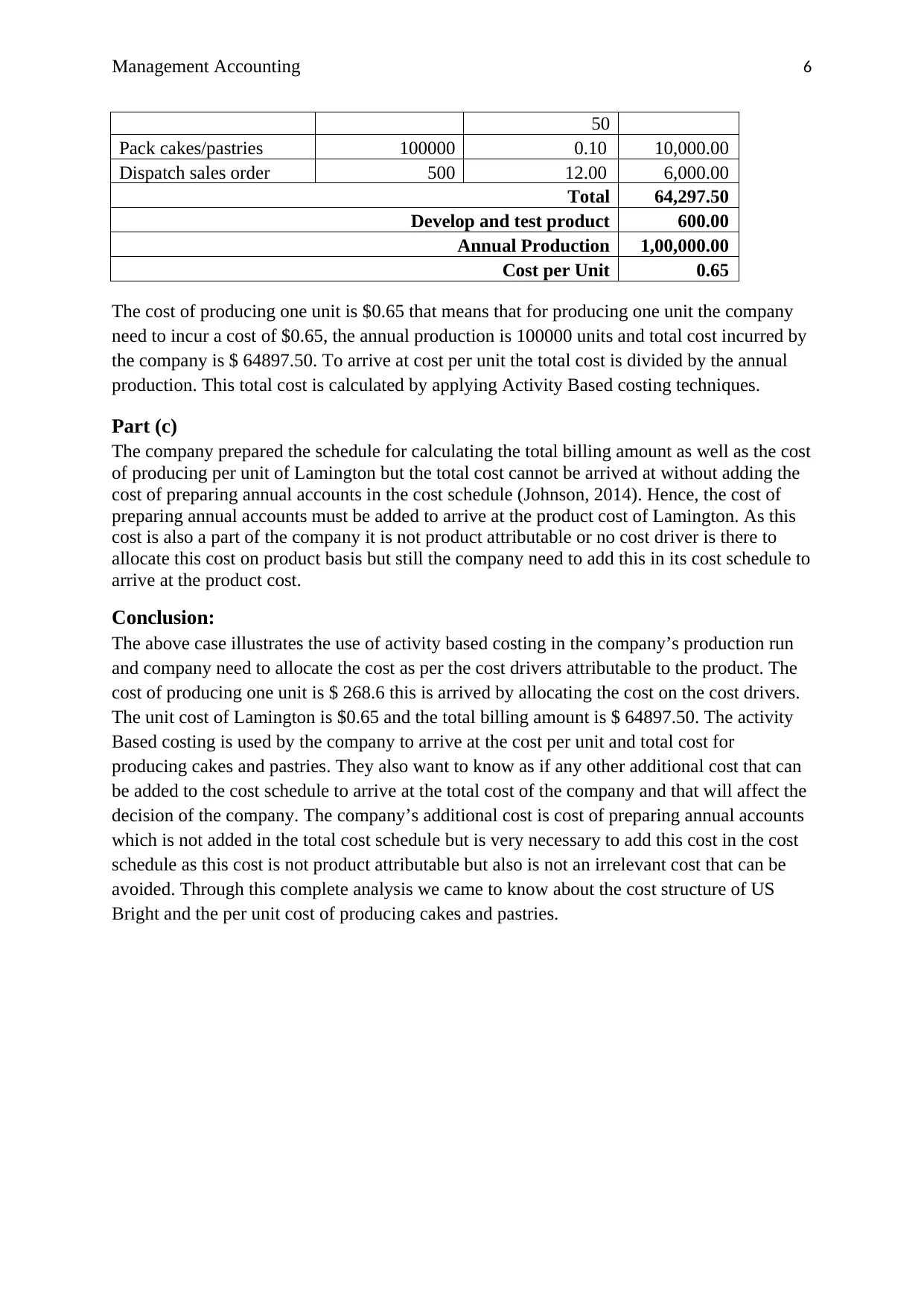

Management Accounting 6

50

Pack cakes/pastries 100000 0.10 10,000.00

Dispatch sales order 500 12.00 6,000.00

Total 64,297.50

Develop and test product 600.00

Annual Production 1,00,000.00

Cost per Unit 0.65

The cost of producing one unit is $0.65 that means that for producing one unit the company

need to incur a cost of $0.65, the annual production is 100000 units and total cost incurred by

the company is $ 64897.50. To arrive at cost per unit the total cost is divided by the annual

production. This total cost is calculated by applying Activity Based costing techniques.

Part (c)

The company prepared the schedule for calculating the total billing amount as well as the cost

of producing per unit of Lamington but the total cost cannot be arrived at without adding the

cost of preparing annual accounts in the cost schedule (Johnson, 2014). Hence, the cost of

preparing annual accounts must be added to arrive at the product cost of Lamington. As this

cost is also a part of the company it is not product attributable or no cost driver is there to

allocate this cost on product basis but still the company need to add this in its cost schedule to

arrive at the product cost.

Conclusion:

The above case illustrates the use of activity based costing in the company’s production run

and company need to allocate the cost as per the cost drivers attributable to the product. The

cost of producing one unit is $ 268.6 this is arrived by allocating the cost on the cost drivers.

The unit cost of Lamington is $0.65 and the total billing amount is $ 64897.50. The activity

Based costing is used by the company to arrive at the cost per unit and total cost for

producing cakes and pastries. They also want to know as if any other additional cost that can

be added to the cost schedule to arrive at the total cost of the company and that will affect the

decision of the company. The company’s additional cost is cost of preparing annual accounts

which is not added in the total cost schedule but is very necessary to add this cost in the cost

schedule as this cost is not product attributable but also is not an irrelevant cost that can be

avoided. Through this complete analysis we came to know about the cost structure of US

Bright and the per unit cost of producing cakes and pastries.

50

Pack cakes/pastries 100000 0.10 10,000.00

Dispatch sales order 500 12.00 6,000.00

Total 64,297.50

Develop and test product 600.00

Annual Production 1,00,000.00

Cost per Unit 0.65

The cost of producing one unit is $0.65 that means that for producing one unit the company

need to incur a cost of $0.65, the annual production is 100000 units and total cost incurred by

the company is $ 64897.50. To arrive at cost per unit the total cost is divided by the annual

production. This total cost is calculated by applying Activity Based costing techniques.

Part (c)

The company prepared the schedule for calculating the total billing amount as well as the cost

of producing per unit of Lamington but the total cost cannot be arrived at without adding the

cost of preparing annual accounts in the cost schedule (Johnson, 2014). Hence, the cost of

preparing annual accounts must be added to arrive at the product cost of Lamington. As this

cost is also a part of the company it is not product attributable or no cost driver is there to

allocate this cost on product basis but still the company need to add this in its cost schedule to

arrive at the product cost.

Conclusion:

The above case illustrates the use of activity based costing in the company’s production run

and company need to allocate the cost as per the cost drivers attributable to the product. The

cost of producing one unit is $ 268.6 this is arrived by allocating the cost on the cost drivers.

The unit cost of Lamington is $0.65 and the total billing amount is $ 64897.50. The activity

Based costing is used by the company to arrive at the cost per unit and total cost for

producing cakes and pastries. They also want to know as if any other additional cost that can

be added to the cost schedule to arrive at the total cost of the company and that will affect the

decision of the company. The company’s additional cost is cost of preparing annual accounts

which is not added in the total cost schedule but is very necessary to add this cost in the cost

schedule as this cost is not product attributable but also is not an irrelevant cost that can be

avoided. Through this complete analysis we came to know about the cost structure of US

Bright and the per unit cost of producing cakes and pastries.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management Accounting 7

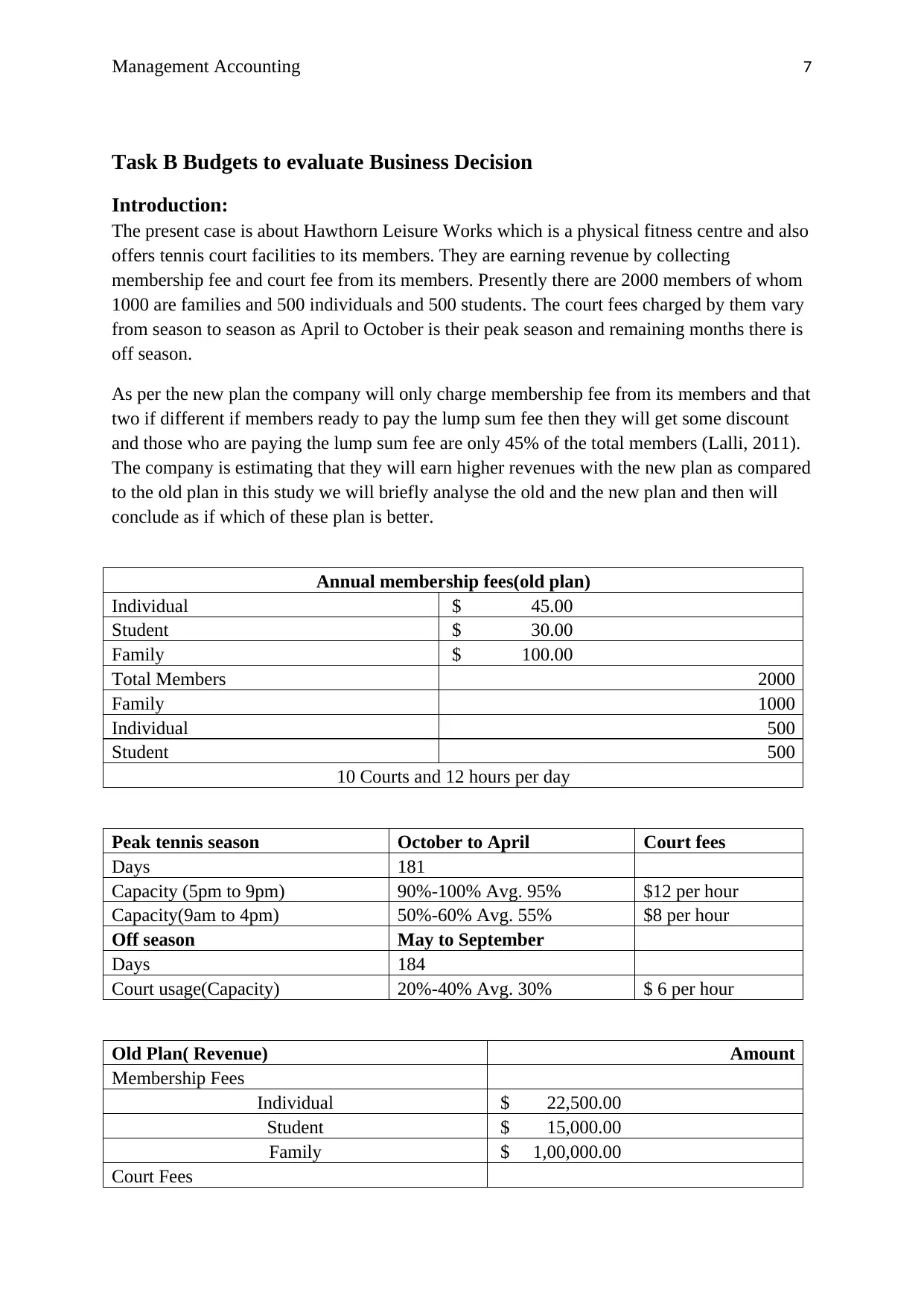

Task B Budgets to evaluate Business Decision

Introduction:

The present case is about Hawthorn Leisure Works which is a physical fitness centre and also

offers tennis court facilities to its members. They are earning revenue by collecting

membership fee and court fee from its members. Presently there are 2000 members of whom

1000 are families and 500 individuals and 500 students. The court fees charged by them vary

from season to season as April to October is their peak season and remaining months there is

off season.

As per the new plan the company will only charge membership fee from its members and that

two if different if members ready to pay the lump sum fee then they will get some discount

and those who are paying the lump sum fee are only 45% of the total members (Lalli, 2011).

The company is estimating that they will earn higher revenues with the new plan as compared

to the old plan in this study we will briefly analyse the old and the new plan and then will

conclude as if which of these plan is better.

Annual membership fees(old plan)

Individual $ 45.00

Student $ 30.00

Family $ 100.00

Total Members 2000

Family 1000

Individual 500

Student 500

10 Courts and 12 hours per day

Peak tennis season October to April Court fees

Days 181

Capacity (5pm to 9pm) 90%-100% Avg. 95% $12 per hour

Capacity(9am to 4pm) 50%-60% Avg. 55% $8 per hour

Off season May to September

Days 184

Court usage(Capacity) 20%-40% Avg. 30% $ 6 per hour

Old Plan( Revenue) Amount

Membership Fees

Individual $ 22,500.00

Student $ 15,000.00

Family $ 1,00,000.00

Court Fees

Task B Budgets to evaluate Business Decision

Introduction:

The present case is about Hawthorn Leisure Works which is a physical fitness centre and also

offers tennis court facilities to its members. They are earning revenue by collecting

membership fee and court fee from its members. Presently there are 2000 members of whom

1000 are families and 500 individuals and 500 students. The court fees charged by them vary

from season to season as April to October is their peak season and remaining months there is

off season.

As per the new plan the company will only charge membership fee from its members and that

two if different if members ready to pay the lump sum fee then they will get some discount

and those who are paying the lump sum fee are only 45% of the total members (Lalli, 2011).

The company is estimating that they will earn higher revenues with the new plan as compared

to the old plan in this study we will briefly analyse the old and the new plan and then will

conclude as if which of these plan is better.

Annual membership fees(old plan)

Individual $ 45.00

Student $ 30.00

Family $ 100.00

Total Members 2000

Family 1000

Individual 500

Student 500

10 Courts and 12 hours per day

Peak tennis season October to April Court fees

Days 181

Capacity (5pm to 9pm) 90%-100% Avg. 95% $12 per hour

Capacity(9am to 4pm) 50%-60% Avg. 55% $8 per hour

Off season May to September

Days 184

Court usage(Capacity) 20%-40% Avg. 30% $ 6 per hour

Old Plan( Revenue) Amount

Membership Fees

Individual $ 22,500.00

Student $ 15,000.00

Family $ 1,00,000.00

Court Fees

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting 8

Peak Season

5pm-9pm $ 82,536.00

9am-4pm $ 63,712.00

Off Season $ 39,744.00

Total Revenue $ 3,23,492.00

Part (a)

In the new plan the members reduced from 2000 to its 70% but the membership fee increased

and also promotional benefit given to the members 45% members adopted the promotional

bonus. The new membership fee increased the revenue and we should implement the new

plan from July. The new plan only based on the membership fee no extra court fee is charged

from the members on the basis of the usage of the court.

New Plan of annual membership fees

Individual $ 300.00

Family $ 500.00

Promotional( for complete year)

Individual $ 250.00

Family $ 450.00

New Plan (Revenue) Amount

Membership Fees

Normal

Individual $ 75,000.00

Family $ 1,25,000.00

Promotional

Individual $ 1,12,500.00

Family $ 2,02,500.00

Total Revenue $ 5,15,000.00

Part (b)

The sales revenue will increase resulting from the planned change in the fee structure for next

financial year. The sales revenue under old plan was $ 3,23,492.00 and the sales revenue

under new plan $ 5,15,000.00.

The assumption made by me is regarding the calculation of court fees as the percentage range

is given for the occupancy of the court. So, I took the average of the given range. As either

we need to take any of the upper or lower range or average of the range one fixed criteria

need to be followed.

Part (c)

HLW should accept the new plan as the revenue will increase and the complexity of

managing the fee structure will decrease on part of the management. The members will also

Peak Season

5pm-9pm $ 82,536.00

9am-4pm $ 63,712.00

Off Season $ 39,744.00

Total Revenue $ 3,23,492.00

Part (a)

In the new plan the members reduced from 2000 to its 70% but the membership fee increased

and also promotional benefit given to the members 45% members adopted the promotional

bonus. The new membership fee increased the revenue and we should implement the new

plan from July. The new plan only based on the membership fee no extra court fee is charged

from the members on the basis of the usage of the court.

New Plan of annual membership fees

Individual $ 300.00

Family $ 500.00

Promotional( for complete year)

Individual $ 250.00

Family $ 450.00

New Plan (Revenue) Amount

Membership Fees

Normal

Individual $ 75,000.00

Family $ 1,25,000.00

Promotional

Individual $ 1,12,500.00

Family $ 2,02,500.00

Total Revenue $ 5,15,000.00

Part (b)

The sales revenue will increase resulting from the planned change in the fee structure for next

financial year. The sales revenue under old plan was $ 3,23,492.00 and the sales revenue

under new plan $ 5,15,000.00.

The assumption made by me is regarding the calculation of court fees as the percentage range

is given for the occupancy of the court. So, I took the average of the given range. As either

we need to take any of the upper or lower range or average of the range one fixed criteria

need to be followed.

Part (c)

HLW should accept the new plan as the revenue will increase and the complexity of

managing the fee structure will decrease on part of the management. The members will also

Management Accounting 9

be happy as there will be no separate fee regarding court usage. The fall in the no. of

members will be combat by the new fee structure very soon as the membership fee increased

as compared to the old plan.

Conclusion:

As per the analysis being done regarding the acceptance of new plan or continuing with the

old plan it is recommended to accept the new plan as the revenue got increased. The revenue

under old plan was $ 323492 and the revenue as per the new plan is $ 515000. The benefit is

clearly there and no other contention is required to support the new plan.

be happy as there will be no separate fee regarding court usage. The fall in the no. of

members will be combat by the new fee structure very soon as the membership fee increased

as compared to the old plan.

Conclusion:

As per the analysis being done regarding the acceptance of new plan or continuing with the

old plan it is recommended to accept the new plan as the revenue got increased. The revenue

under old plan was $ 323492 and the revenue as per the new plan is $ 515000. The benefit is

clearly there and no other contention is required to support the new plan.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management Accounting 10

References:

Heisinger, K 2009, Essentials to Managerial Accounting, Cengage Learning.

Johnson, P. F. 2014, Purchasing and Supply Management, McGraw-Hill Higher Education.

Lalli, W. R. 2011, Handbook of Budgeting, John Wiley & Sons.

Wiese, N 2009, Activity Based Costing, GRIN Verlag.

References:

Heisinger, K 2009, Essentials to Managerial Accounting, Cengage Learning.

Johnson, P. F. 2014, Purchasing and Supply Management, McGraw-Hill Higher Education.

Lalli, W. R. 2011, Handbook of Budgeting, John Wiley & Sons.

Wiese, N 2009, Activity Based Costing, GRIN Verlag.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.