Management Accounting Report: Techniques and Methods for Zylla

VerifiedAdded on 2020/06/05

|12

|4108

|46

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its role in business decision-making. It explores various aspects, including different types of management accounting systems like inventory management, job costing, price optimization, and cost accounting systems. The report delves into the methods used for management accounting reporting, such as budget reporting, account receivable reporting, job cost reports, inventory reporting, and performance reporting. Furthermore, it provides a detailed comparison between marginal and absorption costing methods, illustrating the calculation of net profit under each approach. The report also discusses the advantages and disadvantages of planning tools used in budgetary control and examines how organizations utilize management accounting to address financial problems. Overall, the report offers valuable insights into the practical application of management accounting principles and techniques.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Management accounting and essential requirements of its different types .....................3

P2. Different methods used for management accounting reporting.......................................5

TASK 2 ...........................................................................................................................................6

P3 – Marginal and Absorption costing ..................................................................................6

TASK 3 ...........................................................................................................................................8

P4 Advantages and disadvantages of planning tools which are used in budgetary control...8

TASK 4 .........................................................................................................................................9

P5 - Ways in which organisations use management accounting to respond to......................9

financial problems.................................................................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Management accounting and essential requirements of its different types .....................3

P2. Different methods used for management accounting reporting.......................................5

TASK 2 ...........................................................................................................................................6

P3 – Marginal and Absorption costing ..................................................................................6

TASK 3 ...........................................................................................................................................8

P4 Advantages and disadvantages of planning tools which are used in budgetary control...8

TASK 4 .........................................................................................................................................9

P5 - Ways in which organisations use management accounting to respond to......................9

financial problems.................................................................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Management accounting means a system of finance that supports administration of a

business. It is formed with two words i.e. management and accounting. Thus, it helps

management in taking important decisions (Macintosh and Quattrone, 2010). Management

accounting is a preparation of administrative reports and accounts that deliver accurate and

timely data to make day-to-day and short term decisions. The administrative decisions in an

organisation on the basis of financial information are provided by management accounting. In

the case study, Zylla, a multinational organisation has undergone with number of changes over

time due to expansion, acquisition and restructuring of firm. The management accounting system

needs to be revamped due to such results. This report consists of different management

accounting techniques for determining the cost and planning tools used in a system. Management

accounting plays a key role in important decisions and strategies framed by an organisation. It

uses information of all types, not just financial to lead business towards success.

TASK 1

P1. Management accounting and essential requirements of its different types

Management accounting is one of the wide areas of financial system. It refers to

accounting for management. Management accounting is done for the administration of business

firm to make strategies and take necessary decisions (DRURY, 2013). Thus, it is system of

accounting that is carried out to assist management in important planning and strategies of

business organisation. It is basically concerned for information that supports management. It

produces the report that helps company's internal stakeholders as opposed to external. It provides

periodic reports to managers of an organisation. Usually management accounting reports consist

of cash availability, sales revenue generation, accounts payable and receivables status. It is a

deep study of managerial features of accounting. The main aim of management accounting is to

reframe whole system so that it will serve business organisation in strategies and decisions. It

creates monthly and weekly reports as and when required like budget report is for three months.

Needs of management accounting

It is required to properly evaluate and recognise present status of financial position of a

firm. It helps in different managerial functions such as planning, organising, directing and

controlling (Baldvinsdottir, Mitchell, and Nørreklit, 2010). It overall helps in the performance

Management accounting means a system of finance that supports administration of a

business. It is formed with two words i.e. management and accounting. Thus, it helps

management in taking important decisions (Macintosh and Quattrone, 2010). Management

accounting is a preparation of administrative reports and accounts that deliver accurate and

timely data to make day-to-day and short term decisions. The administrative decisions in an

organisation on the basis of financial information are provided by management accounting. In

the case study, Zylla, a multinational organisation has undergone with number of changes over

time due to expansion, acquisition and restructuring of firm. The management accounting system

needs to be revamped due to such results. This report consists of different management

accounting techniques for determining the cost and planning tools used in a system. Management

accounting plays a key role in important decisions and strategies framed by an organisation. It

uses information of all types, not just financial to lead business towards success.

TASK 1

P1. Management accounting and essential requirements of its different types

Management accounting is one of the wide areas of financial system. It refers to

accounting for management. Management accounting is done for the administration of business

firm to make strategies and take necessary decisions (DRURY, 2013). Thus, it is system of

accounting that is carried out to assist management in important planning and strategies of

business organisation. It is basically concerned for information that supports management. It

produces the report that helps company's internal stakeholders as opposed to external. It provides

periodic reports to managers of an organisation. Usually management accounting reports consist

of cash availability, sales revenue generation, accounts payable and receivables status. It is a

deep study of managerial features of accounting. The main aim of management accounting is to

reframe whole system so that it will serve business organisation in strategies and decisions. It

creates monthly and weekly reports as and when required like budget report is for three months.

Needs of management accounting

It is required to properly evaluate and recognise present status of financial position of a

firm. It helps in different managerial functions such as planning, organising, directing and

controlling (Baldvinsdottir, Mitchell, and Nørreklit, 2010). It overall helps in the performance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

evaluation of an organisation. The reports are made to take appropriate decisions and plan future

oriented activities. It helps in handling the future contingencies of business (Lukka and Modell,

2010). A system of information is required to assist management to investigate, evaluate and

verify smooth functioning of each division and take necessary steps as and when required. The

different types of management accounting systems and their benefits are as follows-

Inventory management system- Inventory management system is the planning, recording

and analysing stocks of a firm. It is used to plan and track inventory levels and those related

activities. Management accounting is an ongoing process of movement of products in and out

from the warehouse of company (Ward, 2012). Management of stocks is done on daily basis.

Inventory management is an important part of business organisation. Any mistake in such system

will lead to failure of business organisation . It covers every movement of part or product of a

firm. One of the best systems followed to recognise the same is use of bar codes. Even malls and

stores are using such system as when stock is sold, it will automatically be deducted from

inventory. One of the innovative technologies used now a days is Radio frequency identification

(RFID). It is the use of signals to record inventory addition and subtraction. Zylla is also using

one of such system of inventory management.

Job costing- This costing is basically used by a construction company like Zylla, to ssign

cost to incur for a particular job. It means allocating cost to individual job projects. This system

determine materials, labour and direct expenses and also overheads to find out cost of production

(Parker, 2012.). If an organisation's products is not identical such system of costing is effective.

It is accounting of direct and indirect costs.

Price optimisation- Price optimisation is the numerical way of finding out how customers

respond to different prices adopted by an organisation. It also determine the pricing policy that a

firm like Zylla should adopt to gain more customers by satisfying their needs. Companies like

Zylla spend massive amount of time to determine the prices so that firm will gain more

customers and maximise their profits . Various components used in such system is management

analysis, customer elasticity model, etc. It is basically collection of cost history and fixing

different prices by a firm to improve profitability.

Cost accounting system- Cost accounting system is used by management accountants to

estimate the cost incurred by company. Profitability analysis is done based on the same. It is the

determination of cost, inventory valuation and control. Any company that is selling different

oriented activities. It helps in handling the future contingencies of business (Lukka and Modell,

2010). A system of information is required to assist management to investigate, evaluate and

verify smooth functioning of each division and take necessary steps as and when required. The

different types of management accounting systems and their benefits are as follows-

Inventory management system- Inventory management system is the planning, recording

and analysing stocks of a firm. It is used to plan and track inventory levels and those related

activities. Management accounting is an ongoing process of movement of products in and out

from the warehouse of company (Ward, 2012). Management of stocks is done on daily basis.

Inventory management is an important part of business organisation. Any mistake in such system

will lead to failure of business organisation . It covers every movement of part or product of a

firm. One of the best systems followed to recognise the same is use of bar codes. Even malls and

stores are using such system as when stock is sold, it will automatically be deducted from

inventory. One of the innovative technologies used now a days is Radio frequency identification

(RFID). It is the use of signals to record inventory addition and subtraction. Zylla is also using

one of such system of inventory management.

Job costing- This costing is basically used by a construction company like Zylla, to ssign

cost to incur for a particular job. It means allocating cost to individual job projects. This system

determine materials, labour and direct expenses and also overheads to find out cost of production

(Parker, 2012.). If an organisation's products is not identical such system of costing is effective.

It is accounting of direct and indirect costs.

Price optimisation- Price optimisation is the numerical way of finding out how customers

respond to different prices adopted by an organisation. It also determine the pricing policy that a

firm like Zylla should adopt to gain more customers by satisfying their needs. Companies like

Zylla spend massive amount of time to determine the prices so that firm will gain more

customers and maximise their profits . Various components used in such system is management

analysis, customer elasticity model, etc. It is basically collection of cost history and fixing

different prices by a firm to improve profitability.

Cost accounting system- Cost accounting system is used by management accountants to

estimate the cost incurred by company. Profitability analysis is done based on the same. It is the

determination of cost, inventory valuation and control. Any company that is selling different

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

products must know their cost and profit generated per unit. The determination of cost is

essential for any organisation . It is a critical task to estimate the profitability of a firm. Cost

accounting aims at capturing the cost of production including input as well as overall production

cost.

P2. Different methods used for management accounting reporting

Managerial reporting helps the managers of an organisation to monitor firm's

performance and usually prepared frequently to provide suitable information. Depending on the

project kind and information required, reports are asked from management accountants. It may

be prepared daily, weekly, monthly or quarterly basis based on requirement of an organisation.

There are various types of reports prepared by management accountants to monitor the

performance. The different methods of management accounting reports are as follows-

Budget reporting – Budgets are prepared to know where company has to spend more

and where not. For a construction company like Zylla, Budget is the most important. It helps in

analysing company's performance and cost control. Different types of budgets such as sales

budget, purchase budget and cash budget are prepared by company to control the cost (Parker,

2012). For providing incentives to employees, sometimes budgets are prepared. Usually, by

analysing the cost incurred in prior years, budget are prepared.

Account Receivable reporting – Any business organisation who is providing credit

facilities to customers should prepare such report. It also determines credit policies adopted by

business firm. It usually provides an overview of credit balances from 30 to 90 days. It helps in

recovering from debtors of an organisation. It is one of the tool to manage cash recovery of a

firm. The issues and problems occurring in cash collection can be sort out. The report is being

prepared based on prior history of debtors (Ward, 2012).

Job cost report – This report is prepared to shoe cost incurred on a single project and

revenue generated from the same. This type of report focuses on each job and work assigned to

them. How quickly tasks has been completed to improve profitability of a firm. Company can

easily able to analyse single job and task assigned (DRURY, 2013). This helps in finding highly

revenue generated areas and focusing more on the same.

essential for any organisation . It is a critical task to estimate the profitability of a firm. Cost

accounting aims at capturing the cost of production including input as well as overall production

cost.

P2. Different methods used for management accounting reporting

Managerial reporting helps the managers of an organisation to monitor firm's

performance and usually prepared frequently to provide suitable information. Depending on the

project kind and information required, reports are asked from management accountants. It may

be prepared daily, weekly, monthly or quarterly basis based on requirement of an organisation.

There are various types of reports prepared by management accountants to monitor the

performance. The different methods of management accounting reports are as follows-

Budget reporting – Budgets are prepared to know where company has to spend more

and where not. For a construction company like Zylla, Budget is the most important. It helps in

analysing company's performance and cost control. Different types of budgets such as sales

budget, purchase budget and cash budget are prepared by company to control the cost (Parker,

2012). For providing incentives to employees, sometimes budgets are prepared. Usually, by

analysing the cost incurred in prior years, budget are prepared.

Account Receivable reporting – Any business organisation who is providing credit

facilities to customers should prepare such report. It also determines credit policies adopted by

business firm. It usually provides an overview of credit balances from 30 to 90 days. It helps in

recovering from debtors of an organisation. It is one of the tool to manage cash recovery of a

firm. The issues and problems occurring in cash collection can be sort out. The report is being

prepared based on prior history of debtors (Ward, 2012).

Job cost report – This report is prepared to shoe cost incurred on a single project and

revenue generated from the same. This type of report focuses on each job and work assigned to

them. How quickly tasks has been completed to improve profitability of a firm. Company can

easily able to analyse single job and task assigned (DRURY, 2013). This helps in finding highly

revenue generated areas and focusing more on the same.

Inventory Reporting – These reports generally include material, labour cost as well as

overhead expenses. The per unit cost can be determined based on same (Banerjee, 2010).

Manufacturing industry usually have more advantages from such reports and thus, helps in

strategies and decisions. This report shows the problems of over or under stocking. This report

help manager in finding the right quantity of goods that should be kept in warehouse. Techniques

like EOQ can be used for resolving the problems which are identified through inventory report.

This report also contain the data of stock which is currently present in the company.

Performance reporting – Performance reporting is way of finding performances

expected from business firm in a specific period of time. The analysis has done to find suitable

information for investors and creditors of an organisation (Caglio and Ditillo, 2012). This report

is made for analysing the performance of employees or division. It shows the mistakes which

they have done and the areas where improvement can be done. This right is mainly used for

setting future goals for workers of various department of the company.

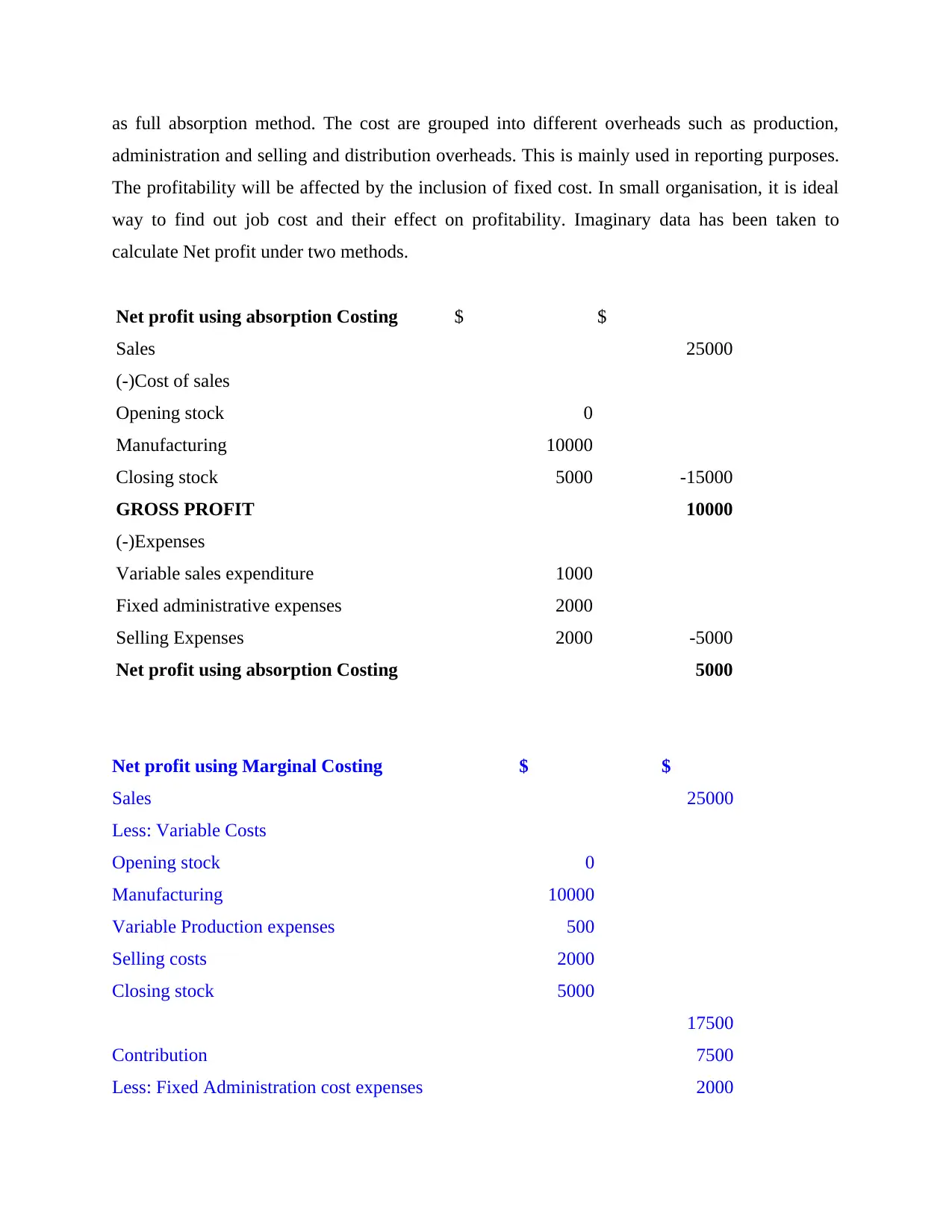

TASK 2

P3 – Marginal and Absorption costing

There are two methods available with an organisation for valuation of stock. These are

Marginal and Absorption costing. The marginal costing and absorption costing can be explained

as follows-

Marginal Costing – This is also known as variable costing. Ascertainment of fixed and

variable cost is done under this method to make appropriate decision of production. It determines

marginal cost of products and their influence on profit for the change in output. Marginal costing

is determined on the basis of fixed and variable cost (Banerjee, 2010). The profitability is

evaluated based on profit-volume ratio of a firm. It can be said as changes in total cost of

production by producing one additional unit. In such costing, fixed cost are of less relevance as

compare to variable cost. It is one of the decision making techniques. It helps management to

focus on changes occurring due to marginal cost of production.

Absorption Costing – Absorption costing is a method of inventory valuation where cost

are grouped into cost centres to determine total cost of production. In such costing, both fixed

and variable cost are of relevance. Such system of costing is one of traditional method also called

overhead expenses. The per unit cost can be determined based on same (Banerjee, 2010).

Manufacturing industry usually have more advantages from such reports and thus, helps in

strategies and decisions. This report shows the problems of over or under stocking. This report

help manager in finding the right quantity of goods that should be kept in warehouse. Techniques

like EOQ can be used for resolving the problems which are identified through inventory report.

This report also contain the data of stock which is currently present in the company.

Performance reporting – Performance reporting is way of finding performances

expected from business firm in a specific period of time. The analysis has done to find suitable

information for investors and creditors of an organisation (Caglio and Ditillo, 2012). This report

is made for analysing the performance of employees or division. It shows the mistakes which

they have done and the areas where improvement can be done. This right is mainly used for

setting future goals for workers of various department of the company.

TASK 2

P3 – Marginal and Absorption costing

There are two methods available with an organisation for valuation of stock. These are

Marginal and Absorption costing. The marginal costing and absorption costing can be explained

as follows-

Marginal Costing – This is also known as variable costing. Ascertainment of fixed and

variable cost is done under this method to make appropriate decision of production. It determines

marginal cost of products and their influence on profit for the change in output. Marginal costing

is determined on the basis of fixed and variable cost (Banerjee, 2010). The profitability is

evaluated based on profit-volume ratio of a firm. It can be said as changes in total cost of

production by producing one additional unit. In such costing, fixed cost are of less relevance as

compare to variable cost. It is one of the decision making techniques. It helps management to

focus on changes occurring due to marginal cost of production.

Absorption Costing – Absorption costing is a method of inventory valuation where cost

are grouped into cost centres to determine total cost of production. In such costing, both fixed

and variable cost are of relevance. Such system of costing is one of traditional method also called

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

as full absorption method. The cost are grouped into different overheads such as production,

administration and selling and distribution overheads. This is mainly used in reporting purposes.

The profitability will be affected by the inclusion of fixed cost. In small organisation, it is ideal

way to find out job cost and their effect on profitability. Imaginary data has been taken to

calculate Net profit under two methods.

Net profit using absorption Costing $ $

Sales 25000

(-)Cost of sales

Opening stock 0

Manufacturing 10000

Closing stock 5000 -15000

GROSS PROFIT 10000

(-)Expenses

Variable sales expenditure 1000

Fixed administrative expenses 2000

Selling Expenses 2000 -5000

Net profit using absorption Costing 5000

Net profit using Marginal Costing $ $

Sales 25000

Less: Variable Costs

Opening stock 0

Manufacturing 10000

Variable Production expenses 500

Selling costs 2000

Closing stock 5000

17500

Contribution 7500

Less: Fixed Administration cost expenses 2000

administration and selling and distribution overheads. This is mainly used in reporting purposes.

The profitability will be affected by the inclusion of fixed cost. In small organisation, it is ideal

way to find out job cost and their effect on profitability. Imaginary data has been taken to

calculate Net profit under two methods.

Net profit using absorption Costing $ $

Sales 25000

(-)Cost of sales

Opening stock 0

Manufacturing 10000

Closing stock 5000 -15000

GROSS PROFIT 10000

(-)Expenses

Variable sales expenditure 1000

Fixed administrative expenses 2000

Selling Expenses 2000 -5000

Net profit using absorption Costing 5000

Net profit using Marginal Costing $ $

Sales 25000

Less: Variable Costs

Opening stock 0

Manufacturing 10000

Variable Production expenses 500

Selling costs 2000

Closing stock 5000

17500

Contribution 7500

Less: Fixed Administration cost expenses 2000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net profit 5500

Interpretation -

On the basis of above calculation it can be concluded that Net profit in marginal costing

is more than absorption costing methods net profit. The difference is 500$, this variance is due to

nature of accounting treatment by both methods. As in absorption costing all expenses either

fixed or variable are included but marginal costing only calculates costs on the basis of variable

cost per unit.

TASK 3

P4 Advantages and disadvantages of planning tools which are used in budgetary control

The budgetary is the process of preparation of various budget for future course of time

based on the history of such component. Actual performance will be compared with the planned

performance, differences if arise, will be sort out (Caglio and Ditillo, 2012). This helps

management to take necessary steps at appropriate time for smooth functioning of business

organisation. Budgets usually fixes targets for each department and it should be accomplished

within a given period of time. But organisation has to spend massive time to prepare such

budgets. Preparation of budgets can be done for units, division, departments or whole enterprise.

An organisation may use number of budgets that are classified as follows-

Master Budget – It is a comprehensive budget involves different aspects of firm in a

budgeted time frame. It usually consist of cash flow, budgeted Statement and Budgeted balance

sheet. This type of budget interrelates with different divisions and thus, an important planning

tool used in budgetary control. Manger use such type of budgets to plan and set performance

objectives. Organisation like Zylla uses such type of budget to get picture view of different

components of business. Thus, large firms usually prepare such type of budgets.

Operational Budget - Operational budget are prepared based on different operations of

business. It usually covers expenses and revenues associated with operational aspects of firm.

Revenue and expenses, also different overheads are considered which are directly related to

manufacturing of products. Such type of budgets are prepared weekly, monthly or quarterly

based on reporting periods. Managers also compare actual performance with planned one to find

out derivates, if any.

Interpretation -

On the basis of above calculation it can be concluded that Net profit in marginal costing

is more than absorption costing methods net profit. The difference is 500$, this variance is due to

nature of accounting treatment by both methods. As in absorption costing all expenses either

fixed or variable are included but marginal costing only calculates costs on the basis of variable

cost per unit.

TASK 3

P4 Advantages and disadvantages of planning tools which are used in budgetary control

The budgetary is the process of preparation of various budget for future course of time

based on the history of such component. Actual performance will be compared with the planned

performance, differences if arise, will be sort out (Caglio and Ditillo, 2012). This helps

management to take necessary steps at appropriate time for smooth functioning of business

organisation. Budgets usually fixes targets for each department and it should be accomplished

within a given period of time. But organisation has to spend massive time to prepare such

budgets. Preparation of budgets can be done for units, division, departments or whole enterprise.

An organisation may use number of budgets that are classified as follows-

Master Budget – It is a comprehensive budget involves different aspects of firm in a

budgeted time frame. It usually consist of cash flow, budgeted Statement and Budgeted balance

sheet. This type of budget interrelates with different divisions and thus, an important planning

tool used in budgetary control. Manger use such type of budgets to plan and set performance

objectives. Organisation like Zylla uses such type of budget to get picture view of different

components of business. Thus, large firms usually prepare such type of budgets.

Operational Budget - Operational budget are prepared based on different operations of

business. It usually covers expenses and revenues associated with operational aspects of firm.

Revenue and expenses, also different overheads are considered which are directly related to

manufacturing of products. Such type of budgets are prepared weekly, monthly or quarterly

based on reporting periods. Managers also compare actual performance with planned one to find

out derivates, if any.

Cash flow Budget –The budget that show inflow and outflow of cash during some

specified period is known as cash flow budget. Managers monitors such budgets to pinpoint

shortfalls. The cash management is necessary for any business organisation. Large organisations

such as Zylla need effective monitoring of cash flow during a specified period, so that cash will

always be available for firm.

Financial Budget – Such budget plays a vital role for an organisation considering how

an organisation spend and receive money including revenue from different operations as well as

cost from capital expenditures (ter Bogt, and van Helden, 2012). Management of fixed assets

such as land and building, inventory, major equipment always influence performance of business

organisation. Such budget are used to leverage performance of business and value company for

mergers and public offerings.

Static Budget – Such budget consist of components where expenditures remains constant

with changes in levels of sales. Cost of overhead can be one of kind of such budgets. Managers

have to see each division of business organisation and plan budgets accordingly. Some divisions

have fixed amount to spend so budgets are prepared keeping it in mind. If in case expenses are

going above, it will surely make business functioning ineffective.

Capital budgeting – taking decisions relating to investment is not an easy task. Capital

budget is the estimation of future fixed expenditure and income. Techniques like IRR and NPV

is used in formation of this budget. NPV shows the present value of a future investment. If NPV

is more than current cost then company should invest in particular product and if it is less then

they should. Internal rate of return shows the amount of return which company will get on

investment. It depicts the time period in which amount can be recovered.

TASK 4

P5 - Ways in which organisations use management accounting to respond to

financial problems

Firms are using problems of adaption of their strategies, and practices to respond to

dynamic environment. The ways in which organisation respond to dynamic environment

describes whether business will lead to success or failure. Management accounting plays a key

role today by providing firm with essential information needed to achieve its goals and

objectives (Fullerton, Kennedy and Widener, 2013). Decision makers of an organisation should

specified period is known as cash flow budget. Managers monitors such budgets to pinpoint

shortfalls. The cash management is necessary for any business organisation. Large organisations

such as Zylla need effective monitoring of cash flow during a specified period, so that cash will

always be available for firm.

Financial Budget – Such budget plays a vital role for an organisation considering how

an organisation spend and receive money including revenue from different operations as well as

cost from capital expenditures (ter Bogt, and van Helden, 2012). Management of fixed assets

such as land and building, inventory, major equipment always influence performance of business

organisation. Such budget are used to leverage performance of business and value company for

mergers and public offerings.

Static Budget – Such budget consist of components where expenditures remains constant

with changes in levels of sales. Cost of overhead can be one of kind of such budgets. Managers

have to see each division of business organisation and plan budgets accordingly. Some divisions

have fixed amount to spend so budgets are prepared keeping it in mind. If in case expenses are

going above, it will surely make business functioning ineffective.

Capital budgeting – taking decisions relating to investment is not an easy task. Capital

budget is the estimation of future fixed expenditure and income. Techniques like IRR and NPV

is used in formation of this budget. NPV shows the present value of a future investment. If NPV

is more than current cost then company should invest in particular product and if it is less then

they should. Internal rate of return shows the amount of return which company will get on

investment. It depicts the time period in which amount can be recovered.

TASK 4

P5 - Ways in which organisations use management accounting to respond to

financial problems

Firms are using problems of adaption of their strategies, and practices to respond to

dynamic environment. The ways in which organisation respond to dynamic environment

describes whether business will lead to success or failure. Management accounting plays a key

role today by providing firm with essential information needed to achieve its goals and

objectives (Fullerton, Kennedy and Widener, 2013). Decision makers of an organisation should

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

know how information should be used to make their firm recognizable. In a dynamic business

environment, organisation have to properly analyse their cost incurred in various components

and plan accordingly to make firm effective and profitable. Good management accounting

depends on using information in an effective way and use different techniques as marginal

accounting, ratio analysis, cost- volume profit analysis etc. to determine planned targets and

accomplish same within specified time. Following are some of the financial troubles which can

be solved by using management accounting systems:

Management of cash – The importance of liquid assets has always remained high because

it is considered as the backbone of a company. Management accounting techniques help in right

allocation of liquid asset. Cash budget shows the right amount of cash which is needed in a

particular time. This reduces the wastage of cash and mainly liquidity in the organisation.

Timely payment – An organisation can fail to make or receive payment because of

various reasons. This issue can be solved by making account receivable and payment report.

These report contain systematic details about debtors and creditors of the company.

Management accounting is of utmost importance of any organisation. However such

system of accounting undergone different changes over the years. Earlier traditional method of

management accounting was followed however, now innovative modern method has been in

role. Management accountants plays key role in business organisation devoted resources to

make an enterprise best among others. Traditionally management accountants have less options

to use, but now they have plenty of options to provide administration with number of useful

information. The modern system of accounting uses Key performance indicators, Bench marking

and financial governance which make an organisation profitable. Earlier such components were

not available (Schaltegger, Gibassier, and Zvezdov, 2013). Thus, we can say that management

accounting will lead business towards sustainable success.

Key performance indicators – It identifies how effectively a firm achieve

predetermined targets. Selecting right KPIs is an important task as it depend on which industry

business is operating. It helps managers of an organisation to identify effectiveness of different

functions. It is one of kind of performance measurement. SMART objectives has to set by the

firm for resolving financial troubles. They should set specific goals like decrease the cost of

business by 15%, their targets should be measurable like from last year and they should be time

environment, organisation have to properly analyse their cost incurred in various components

and plan accordingly to make firm effective and profitable. Good management accounting

depends on using information in an effective way and use different techniques as marginal

accounting, ratio analysis, cost- volume profit analysis etc. to determine planned targets and

accomplish same within specified time. Following are some of the financial troubles which can

be solved by using management accounting systems:

Management of cash – The importance of liquid assets has always remained high because

it is considered as the backbone of a company. Management accounting techniques help in right

allocation of liquid asset. Cash budget shows the right amount of cash which is needed in a

particular time. This reduces the wastage of cash and mainly liquidity in the organisation.

Timely payment – An organisation can fail to make or receive payment because of

various reasons. This issue can be solved by making account receivable and payment report.

These report contain systematic details about debtors and creditors of the company.

Management accounting is of utmost importance of any organisation. However such

system of accounting undergone different changes over the years. Earlier traditional method of

management accounting was followed however, now innovative modern method has been in

role. Management accountants plays key role in business organisation devoted resources to

make an enterprise best among others. Traditionally management accountants have less options

to use, but now they have plenty of options to provide administration with number of useful

information. The modern system of accounting uses Key performance indicators, Bench marking

and financial governance which make an organisation profitable. Earlier such components were

not available (Schaltegger, Gibassier, and Zvezdov, 2013). Thus, we can say that management

accounting will lead business towards sustainable success.

Key performance indicators – It identifies how effectively a firm achieve

predetermined targets. Selecting right KPIs is an important task as it depend on which industry

business is operating. It helps managers of an organisation to identify effectiveness of different

functions. It is one of kind of performance measurement. SMART objectives has to set by the

firm for resolving financial troubles. They should set specific goals like decrease the cost of

business by 15%, their targets should be measurable like from last year and they should be time

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

bounded. Targets should be attainable and realistic so employee do not feel demotivated if they

fail to attain them.

Bench marking – It is measurement of performance of organisational products and

strategies in comparison with standard one. The main aim of such system is to find out

improving areas and analyse how information is used in a best way. To achieve greater success

by improvement in different functional areas is main motive (Ferreira, Moulang, and Hendro,

2010). It also focuses on how others use information and accomplish their targets. Management

accountants compare own operations with those of competitors.

Financial Governance – Financial governance is process of ensuring that financial

processes are governed effectively. It involves everything from internal control to auditing of

different components. By conducting internal audit and providing more power to audit company,

many financials issues can be resolved at the place of their generation. If a problem in identified

in internal audit then it can be resolved in right time and the damage can be minimised.

CONCLUSION

By this report, it has been concluded that management accounting is an integral part of

any business organisation. It is one of the system that provide management with the useful

information. This information is helpful in framing strategies and taking appropriate decisions at

the right time. Management accounting is a preparation of administrative reports and accounts

that deliver accurate and timely data to make day-to-day and short term decisions. Management

accounting provides administration different tools and techniques required to plan different

strategies and work accordingly. Ratio analysis, Cash flow statement, Fund flow statement,

Marginal Costing, Cost- Volume profit analysis, Budgeting are all components of such

accounting system and helps organisation with useful informations to take right decisions. It

analyses business cost and operations to prepare financial reports and records. It helps in future

forecasting activities. Thus, helps in achievement of organisational goals.

fail to attain them.

Bench marking – It is measurement of performance of organisational products and

strategies in comparison with standard one. The main aim of such system is to find out

improving areas and analyse how information is used in a best way. To achieve greater success

by improvement in different functional areas is main motive (Ferreira, Moulang, and Hendro,

2010). It also focuses on how others use information and accomplish their targets. Management

accountants compare own operations with those of competitors.

Financial Governance – Financial governance is process of ensuring that financial

processes are governed effectively. It involves everything from internal control to auditing of

different components. By conducting internal audit and providing more power to audit company,

many financials issues can be resolved at the place of their generation. If a problem in identified

in internal audit then it can be resolved in right time and the damage can be minimised.

CONCLUSION

By this report, it has been concluded that management accounting is an integral part of

any business organisation. It is one of the system that provide management with the useful

information. This information is helpful in framing strategies and taking appropriate decisions at

the right time. Management accounting is a preparation of administrative reports and accounts

that deliver accurate and timely data to make day-to-day and short term decisions. Management

accounting provides administration different tools and techniques required to plan different

strategies and work accordingly. Ratio analysis, Cash flow statement, Fund flow statement,

Marginal Costing, Cost- Volume profit analysis, Budgeting are all components of such

accounting system and helps organisation with useful informations to take right decisions. It

analyses business cost and operations to prepare financial reports and records. It helps in future

forecasting activities. Thus, helps in achievement of organisational goals.

REFERENCES

Books and Journals

Macintosh, N.B. and Quattrone, P., 2010. Management accounting and control systems: An

organizational and sociological approach. John Wiley & Sons.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Baldvinsdottir, G., Mitchell, F. and Nørreklit, H., 2010. Issues in the relationship between theory

and practice in management accounting. Management Accounting Research. 21(2).

pp.79-82.

Lukka, K. and Modell, S., 2010. Validation in interpretive management accounting

research. Accounting, Organizations and Society. 35(4). pp.462-477.

Ward, K., 2012. Strategic management accounting. Routledge.

Parker, L.D., 2012. Qualitative management accounting research: Assessing deliverables and

relevance. Critical perspectives on accounting. 23(1). pp.54-70.

Ferreira, A., Moulang, C. and Hendro, B., 2010. Environmental management accounting and

innovation: an exploratory analysis. Accounting, Auditing & Accountability

Journal. 23(7). pp.920-948.

Schaltegger, S., Gibassier, D. and Zvezdov, D., 2013. Is environmental management accounting

a discipline? A bibliometric literature review. Meditari Accountancy Research. 21(1).

pp.4-31.

Cinquini, L. and Tenucci, A., 2010. Strategic management accounting and business strategy: a

loose coupling?. Journal of Accounting & organizational change. 6(2). pp.228-259.

Renz, D.O., 2016. The Jossey-Bass handbook of nonprofit leadership and management. John

Wiley & Sons.

Scapens, R.W. and Bromwich, M., 2010. Management accounting research: 20 years on.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2013. Management accounting and control

practices in a lean manufacturing environment. Accounting, Organizations and

Society. 38(1). pp.50-71.

ter Bogt, H. and van Helden, J., 2012. The practical relevance of management accounting

research and the role of qualitative methods therein: The debate continues. Qualitative

Research in Accounting & Management. 9(3). pp.265-273.

Caglio, A. and Ditillo, A., 2012. Opening the black box of management accounting information

exchanges in buyer–supplier relationships. Management Accounting Research. 23(2).

pp.61-78.

Banerjee, B., 2010. Financial policy and management accounting. PHI Learning Pvt. Ltd..

Online

management accounting. 2017. [online]. Available through

<http://www.mbacrystalball.com/blog/accounting/management-accounting> [Accessed

on 13th November 2017].

Books and Journals

Macintosh, N.B. and Quattrone, P., 2010. Management accounting and control systems: An

organizational and sociological approach. John Wiley & Sons.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Baldvinsdottir, G., Mitchell, F. and Nørreklit, H., 2010. Issues in the relationship between theory

and practice in management accounting. Management Accounting Research. 21(2).

pp.79-82.

Lukka, K. and Modell, S., 2010. Validation in interpretive management accounting

research. Accounting, Organizations and Society. 35(4). pp.462-477.

Ward, K., 2012. Strategic management accounting. Routledge.

Parker, L.D., 2012. Qualitative management accounting research: Assessing deliverables and

relevance. Critical perspectives on accounting. 23(1). pp.54-70.

Ferreira, A., Moulang, C. and Hendro, B., 2010. Environmental management accounting and

innovation: an exploratory analysis. Accounting, Auditing & Accountability

Journal. 23(7). pp.920-948.

Schaltegger, S., Gibassier, D. and Zvezdov, D., 2013. Is environmental management accounting

a discipline? A bibliometric literature review. Meditari Accountancy Research. 21(1).

pp.4-31.

Cinquini, L. and Tenucci, A., 2010. Strategic management accounting and business strategy: a

loose coupling?. Journal of Accounting & organizational change. 6(2). pp.228-259.

Renz, D.O., 2016. The Jossey-Bass handbook of nonprofit leadership and management. John

Wiley & Sons.

Scapens, R.W. and Bromwich, M., 2010. Management accounting research: 20 years on.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2013. Management accounting and control

practices in a lean manufacturing environment. Accounting, Organizations and

Society. 38(1). pp.50-71.

ter Bogt, H. and van Helden, J., 2012. The practical relevance of management accounting

research and the role of qualitative methods therein: The debate continues. Qualitative

Research in Accounting & Management. 9(3). pp.265-273.

Caglio, A. and Ditillo, A., 2012. Opening the black box of management accounting information

exchanges in buyer–supplier relationships. Management Accounting Research. 23(2).

pp.61-78.

Banerjee, B., 2010. Financial policy and management accounting. PHI Learning Pvt. Ltd..

Online

management accounting. 2017. [online]. Available through

<http://www.mbacrystalball.com/blog/accounting/management-accounting> [Accessed

on 13th November 2017].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.