Management Accounting Report: Financial Problem Solving and MAS Tools

VerifiedAdded on 2023/01/06

|10

|2495

|49

Report

AI Summary

This management accounting report analyzes the financial health of Prime Furnitures, a London-based furniture company, through the lens of various management accounting techniques. The report delves into cost analysis, including absorption and marginal costing, and explores the application of management accounting tools such as budgeting, sales forecasting, and capital budgeting. Furthermore, it addresses financial problems like declining sales and rising costs, proposing solutions using benchmarking, key performance indicators, and financial governance. The report highlights the role of management accountants in leveraging Management Accounting Systems (MAS) to aid in strategic decision-making and improve the overall financial performance of the organization. The analysis provides insights into how MAS can be utilized to identify and resolve financial issues, ultimately contributing to the long-term success of the business.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

TASK 1............................................................................................................................................3

(covered in ppt).......................................................................................................................3

TASK 2............................................................................................................................................3

P3 Calculation of cost using appropriate cost analysis techniques........................................3

TASK 3............................................................................................................................................5

P4 Management accounting tools...........................................................................................5

TASK 4............................................................................................................................................7

P5 Different MAS to solve financial problems......................................................................7

Conclusion.......................................................................................................................................9

References......................................................................................................................................10

2

Introduction......................................................................................................................................3

TASK 1............................................................................................................................................3

(covered in ppt).......................................................................................................................3

TASK 2............................................................................................................................................3

P3 Calculation of cost using appropriate cost analysis techniques........................................3

TASK 3............................................................................................................................................5

P4 Management accounting tools...........................................................................................5

TASK 4............................................................................................................................................7

P5 Different MAS to solve financial problems......................................................................7

Conclusion.......................................................................................................................................9

References......................................................................................................................................10

2

Introduction

Management Accounting is a form of accounting whose users are only internal

management of the company. Information extracted by these accounts are used for strategic

decision making (Ahmad, 2017). It includes both financial as well as non financial factors into

its consideration. It considers that as much as financial information is important, non financial

information also has a huge affect on business operations which is not recognised anywhere else.

Several techniques are applied on a range of information and the best alternative is observed.

These information are then developed in reports which help management in identifying course of

financial problems and their possible solutions. Corrective action plans are then developed and

executed.

This report is prepared in context of London based furniture company, Prime Furnitures.

Initially, management accounting and its importance is discussed in the decision making process.

Several techniques and planning tools used used by management such as budgets, pricing

strategies, cost accounting, etc. are explained for a brief understanding. Financial governance and

usage of accounting techniques in maintaining financial health of the organisation are also

highlighted.

TASK 1

(covered in ppt)

TASK 2

P3 Calculation of cost using appropriate cost analysis techniques

Cost is defined as monetary value that an organization spends to create or produce some

product or service. It is calculated sans profit mark up. Cost can be classified into various types

such direct and indirect cost, variable and fixed cost, controllable and uncontrollable costs,

operating and opportunity cost, sunk cost, etc.

Cost analysis refers to determination of relationship between cost and output. In other

words, it is determining money value of input factors such material, labor, etc in deciding

optimum level of production (Rozhkova, Blinova and Rozhkova, 2017). Method of determining

impact of varying level of costs and volume on operational profit of the company is called cost-

volume-profit analysis. Companies prepare cost budget which is used to find variance in actual

3

Management Accounting is a form of accounting whose users are only internal

management of the company. Information extracted by these accounts are used for strategic

decision making (Ahmad, 2017). It includes both financial as well as non financial factors into

its consideration. It considers that as much as financial information is important, non financial

information also has a huge affect on business operations which is not recognised anywhere else.

Several techniques are applied on a range of information and the best alternative is observed.

These information are then developed in reports which help management in identifying course of

financial problems and their possible solutions. Corrective action plans are then developed and

executed.

This report is prepared in context of London based furniture company, Prime Furnitures.

Initially, management accounting and its importance is discussed in the decision making process.

Several techniques and planning tools used used by management such as budgets, pricing

strategies, cost accounting, etc. are explained for a brief understanding. Financial governance and

usage of accounting techniques in maintaining financial health of the organisation are also

highlighted.

TASK 1

(covered in ppt)

TASK 2

P3 Calculation of cost using appropriate cost analysis techniques

Cost is defined as monetary value that an organization spends to create or produce some

product or service. It is calculated sans profit mark up. Cost can be classified into various types

such direct and indirect cost, variable and fixed cost, controllable and uncontrollable costs,

operating and opportunity cost, sunk cost, etc.

Cost analysis refers to determination of relationship between cost and output. In other

words, it is determining money value of input factors such material, labor, etc in deciding

optimum level of production (Rozhkova, Blinova and Rozhkova, 2017). Method of determining

impact of varying level of costs and volume on operational profit of the company is called cost-

volume-profit analysis. Companies prepare cost budget which is used to find variance in actual

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

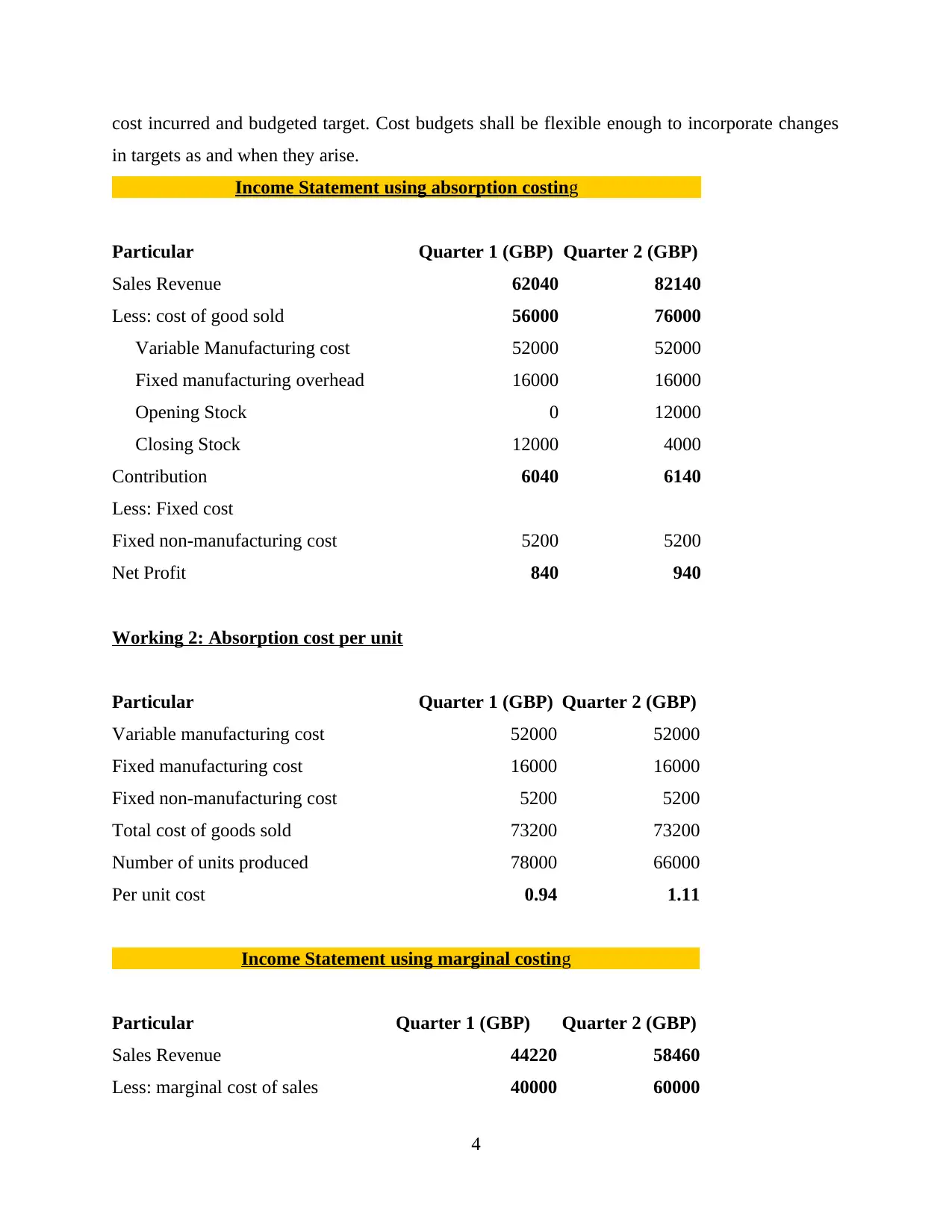

cost incurred and budgeted target. Cost budgets shall be flexible enough to incorporate changes

in targets as and when they arise.

Income Statement using absorption costing

Particular Quarter 1 (GBP) Quarter 2 (GBP)

Sales Revenue 62040 82140

Less: cost of good sold 56000 76000

Variable Manufacturing cost 52000 52000

Fixed manufacturing overhead 16000 16000

Opening Stock 0 12000

Closing Stock 12000 4000

Contribution 6040 6140

Less: Fixed cost

Fixed non-manufacturing cost 5200 5200

Net Profit 840 940

Working 2: Absorption cost per unit

Particular Quarter 1 (GBP) Quarter 2 (GBP)

Variable manufacturing cost 52000 52000

Fixed manufacturing cost 16000 16000

Fixed non-manufacturing cost 5200 5200

Total cost of goods sold 73200 73200

Number of units produced 78000 66000

Per unit cost 0.94 1.11

Income Statement using marginal costing

Particular Quarter 1 (GBP) Quarter 2 (GBP)

Sales Revenue 44220 58460

Less: marginal cost of sales 40000 60000

4

in targets as and when they arise.

Income Statement using absorption costing

Particular Quarter 1 (GBP) Quarter 2 (GBP)

Sales Revenue 62040 82140

Less: cost of good sold 56000 76000

Variable Manufacturing cost 52000 52000

Fixed manufacturing overhead 16000 16000

Opening Stock 0 12000

Closing Stock 12000 4000

Contribution 6040 6140

Less: Fixed cost

Fixed non-manufacturing cost 5200 5200

Net Profit 840 940

Working 2: Absorption cost per unit

Particular Quarter 1 (GBP) Quarter 2 (GBP)

Variable manufacturing cost 52000 52000

Fixed manufacturing cost 16000 16000

Fixed non-manufacturing cost 5200 5200

Total cost of goods sold 73200 73200

Number of units produced 78000 66000

Per unit cost 0.94 1.11

Income Statement using marginal costing

Particular Quarter 1 (GBP) Quarter 2 (GBP)

Sales Revenue 44220 58460

Less: marginal cost of sales 40000 60000

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

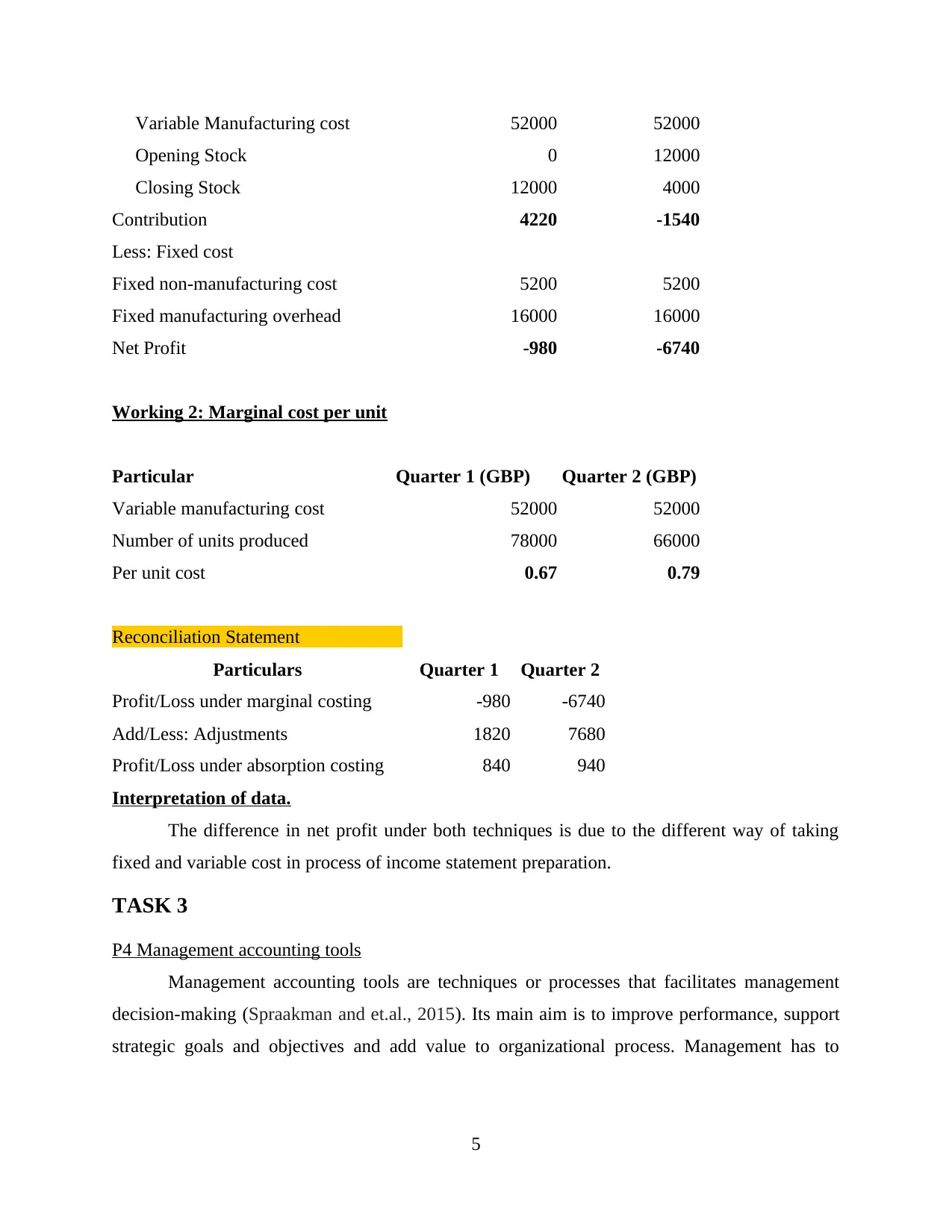

Variable Manufacturing cost 52000 52000

Opening Stock 0 12000

Closing Stock 12000 4000

Contribution 4220 -1540

Less: Fixed cost

Fixed non-manufacturing cost 5200 5200

Fixed manufacturing overhead 16000 16000

Net Profit -980 -6740

Working 2: Marginal cost per unit

Particular Quarter 1 (GBP) Quarter 2 (GBP)

Variable manufacturing cost 52000 52000

Number of units produced 78000 66000

Per unit cost 0.67 0.79

Reconciliation Statement

Particulars Quarter 1 Quarter 2

Profit/Loss under marginal costing -980 -6740

Add/Less: Adjustments 1820 7680

Profit/Loss under absorption costing 840 940

Interpretation of data.

The difference in net profit under both techniques is due to the different way of taking

fixed and variable cost in process of income statement preparation.

TASK 3

P4 Management accounting tools

Management accounting tools are techniques or processes that facilitates management

decision-making (Spraakman and et.al., 2015). Its main aim is to improve performance, support

strategic goals and objectives and add value to organizational process. Management has to

5

Opening Stock 0 12000

Closing Stock 12000 4000

Contribution 4220 -1540

Less: Fixed cost

Fixed non-manufacturing cost 5200 5200

Fixed manufacturing overhead 16000 16000

Net Profit -980 -6740

Working 2: Marginal cost per unit

Particular Quarter 1 (GBP) Quarter 2 (GBP)

Variable manufacturing cost 52000 52000

Number of units produced 78000 66000

Per unit cost 0.67 0.79

Reconciliation Statement

Particulars Quarter 1 Quarter 2

Profit/Loss under marginal costing -980 -6740

Add/Less: Adjustments 1820 7680

Profit/Loss under absorption costing 840 940

Interpretation of data.

The difference in net profit under both techniques is due to the different way of taking

fixed and variable cost in process of income statement preparation.

TASK 3

P4 Management accounting tools

Management accounting tools are techniques or processes that facilitates management

decision-making (Spraakman and et.al., 2015). Its main aim is to improve performance, support

strategic goals and objectives and add value to organizational process. Management has to

5

perform various processes such as planning and control, pricing decisions, etc. Different tools are

used for different purposes:

First thing to be undertaken by management is to plan out business activities. These plans

act as basis for monitoring and controlling function. Plan and controlling occurs at all level of

management. For planning and controlling, basic tool used by management is budgeting.

Budget is statement of estimated income and expenses prepared on the basis of historical

data and future expectations. This estimate is then compared at the year end to find out variances

from targets. Corrective actions are then decided on the basis of variances. Budgets can be

classified into two categories: operational and capital budget. Operational budget is prepared for

projected operational revenues and expenses company will be having in a year while capital

budget is prepared for some long term capital investment decision. Different types of budgets

that managers of Prime Furniture ca prepare are below mentioned:

Cash Budget

It is statement of estimated inflow and outflow of cash and cash equivalents in a specific

business period (Tucker and Schaltegger, 2016). It helps management in determining sources and

nature of inflow and outflow. It will help managers of Prime Furniture ascertain the availability

of cash and smooth cash allocation over budgeted period. It will help them determine whether

they will be needing additional financing in budgeted year. Advantages – It helps company avoid situation of under liquidation and over liquidation.

It helps company in planning smooth operations of business activities. Disadvantages – Cash budget is based on estimation which makes operations in cash

rigid. Rigidity in dealing in uncertain business environment can contribute to losses for

the company. Thus, cash budget shall be flexible enough to incorporate mid-year

changes.

Sales Budget

It is forecasting the sales of product in an year. It helps company organize its production

schedule. Also, managers of Prime Furniture can use it to determine the period when its sales

decline and then can plan necessary promotional strategies. Advantages – An accurate sales budget is preliminary to the preparation of master budget.

It gives an estimation of the revenue business would be earning which will help

management plan other activities effectively.

6

used for different purposes:

First thing to be undertaken by management is to plan out business activities. These plans

act as basis for monitoring and controlling function. Plan and controlling occurs at all level of

management. For planning and controlling, basic tool used by management is budgeting.

Budget is statement of estimated income and expenses prepared on the basis of historical

data and future expectations. This estimate is then compared at the year end to find out variances

from targets. Corrective actions are then decided on the basis of variances. Budgets can be

classified into two categories: operational and capital budget. Operational budget is prepared for

projected operational revenues and expenses company will be having in a year while capital

budget is prepared for some long term capital investment decision. Different types of budgets

that managers of Prime Furniture ca prepare are below mentioned:

Cash Budget

It is statement of estimated inflow and outflow of cash and cash equivalents in a specific

business period (Tucker and Schaltegger, 2016). It helps management in determining sources and

nature of inflow and outflow. It will help managers of Prime Furniture ascertain the availability

of cash and smooth cash allocation over budgeted period. It will help them determine whether

they will be needing additional financing in budgeted year. Advantages – It helps company avoid situation of under liquidation and over liquidation.

It helps company in planning smooth operations of business activities. Disadvantages – Cash budget is based on estimation which makes operations in cash

rigid. Rigidity in dealing in uncertain business environment can contribute to losses for

the company. Thus, cash budget shall be flexible enough to incorporate mid-year

changes.

Sales Budget

It is forecasting the sales of product in an year. It helps company organize its production

schedule. Also, managers of Prime Furniture can use it to determine the period when its sales

decline and then can plan necessary promotional strategies. Advantages – An accurate sales budget is preliminary to the preparation of master budget.

It gives an estimation of the revenue business would be earning which will help

management plan other activities effectively.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Disadvantages – Market conditions are uncertain (Wouters and Kirchberger, 2015.).

Inaccurate sales forecasts can lead to over production and under production, both of

which can lead to losses for the company.

Management of Prime Furniture can also prepare other budgets such as production

budget, materials purchase and usage budget, labor and overhead budget, etc. to help and aid

them in preparing master budget for the organizational goal and objectives.

Capital Budgeting

It is the method by which an organization analyses the multiple options available to it for

financing new investment and expansion projects. Managers use multiple models such as net

present value, pay-back period, etc. to compare financial alternatives. Managers of Prime

Furniture shall also undertake tools of capital budgeting to select best option available to them. Advantages – Capital investments require huge funds. Capital budgeting tools help

company avoid the risk of choosing wrong investment which can be fatal to financial

health of the organization.

Disadvantages - Capital budgeting tools involves predictions. Any wrong prediction can

take company away from the growth path.

TASK 4

P5 Different MAS to solve financial problems

Financial problem- Effective financial management is the essence of a successful

organisation and failure of management on this part may lead to serious hazards causing to

organisation (Weygandt, Kimmel and Kieso, 2020). Financial management consists of

preparation of budgets, deciding source of finance, formulation of cost efficient capital structure,

etc. If managers fails in all above operations, then business faces financial problems. There are

several financial crisis that a business can confront. Some of them are explained below: Decline in sales revenue: In this problem, business faces great fall in sales revenue, due

to this decline business is not able to generate profits and hence, finally results in

declining graph of growth of business. This decrease in sales is continued over number of

years (Schaltegger and Zvezdov, 2015). Reason behind this fall may relate to weak

marketing policies, strong competition, inappropriate pricing strategy or weak product. In

context of Prime furniture, reason behind this issue is ineffective marketing strategies.

7

Inaccurate sales forecasts can lead to over production and under production, both of

which can lead to losses for the company.

Management of Prime Furniture can also prepare other budgets such as production

budget, materials purchase and usage budget, labor and overhead budget, etc. to help and aid

them in preparing master budget for the organizational goal and objectives.

Capital Budgeting

It is the method by which an organization analyses the multiple options available to it for

financing new investment and expansion projects. Managers use multiple models such as net

present value, pay-back period, etc. to compare financial alternatives. Managers of Prime

Furniture shall also undertake tools of capital budgeting to select best option available to them. Advantages – Capital investments require huge funds. Capital budgeting tools help

company avoid the risk of choosing wrong investment which can be fatal to financial

health of the organization.

Disadvantages - Capital budgeting tools involves predictions. Any wrong prediction can

take company away from the growth path.

TASK 4

P5 Different MAS to solve financial problems

Financial problem- Effective financial management is the essence of a successful

organisation and failure of management on this part may lead to serious hazards causing to

organisation (Weygandt, Kimmel and Kieso, 2020). Financial management consists of

preparation of budgets, deciding source of finance, formulation of cost efficient capital structure,

etc. If managers fails in all above operations, then business faces financial problems. There are

several financial crisis that a business can confront. Some of them are explained below: Decline in sales revenue: In this problem, business faces great fall in sales revenue, due

to this decline business is not able to generate profits and hence, finally results in

declining graph of growth of business. This decrease in sales is continued over number of

years (Schaltegger and Zvezdov, 2015). Reason behind this fall may relate to weak

marketing policies, strong competition, inappropriate pricing strategy or weak product. In

context of Prime furniture, reason behind this issue is ineffective marketing strategies.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Unwanted higher cost: This problem relates with increase in cost incurred, which results

in decrease in profits margins of company. Possible reason for increase in cost can be

faulted budgeting, employee performance not as per requirements, continuous use of

obsolete technology in business operations, etc. This situation can turn out to be very

hazardous for the survival of business in market. In relation of Prime furniture, this is a

serious threat as there is cut throat competition in industry and to survive that

competition, they have to spend excessively on marketing strategies.

Accounting techniques to solve financial problems: Benchmarking: Benchmarking refers to the comparison tool that is used to compare

performance of a business with the other companies existing in industry. With help of

this technique, managers are able to identify points that will lead to lag in performance of

business. This monitoring will help in identifying areas that need attention of managers. Key performance indicators: It is a monitoring tool that keeps check on financial and

non financial aspects that puts effect on a business. Financial aspects include profits,

losses, debts, assets, etc., on the other hand non financial aspects includes external

environmental factors like political, technological, economical, etc. (Kokubu and Kitada,

2015) This measuring technique helps managers to consider cause of financial issues

confronted by company.

Financial governance: This is a process of regulating, controlling, monitoring and

managing monetary transactions of business. If there is continuous check on transactions,

it will lead to resolution of financial problems at the source itself. This tool also helps in

maintaining record of financial transaction in a systematic order.

Comparison:

Base for

comparison

Prime furniture London furniture outlet

Financial issue Major issue faced by this company

is that their revenues are constant

over the years and still their profit

margin is decreasing.

London furniture outlet are

continuously coming up with new

range of products but still their

market share is constant and not

coming up on growth pace.

Technique to With the help of technique of Benchmarking technique is useful for

8

in decrease in profits margins of company. Possible reason for increase in cost can be

faulted budgeting, employee performance not as per requirements, continuous use of

obsolete technology in business operations, etc. This situation can turn out to be very

hazardous for the survival of business in market. In relation of Prime furniture, this is a

serious threat as there is cut throat competition in industry and to survive that

competition, they have to spend excessively on marketing strategies.

Accounting techniques to solve financial problems: Benchmarking: Benchmarking refers to the comparison tool that is used to compare

performance of a business with the other companies existing in industry. With help of

this technique, managers are able to identify points that will lead to lag in performance of

business. This monitoring will help in identifying areas that need attention of managers. Key performance indicators: It is a monitoring tool that keeps check on financial and

non financial aspects that puts effect on a business. Financial aspects include profits,

losses, debts, assets, etc., on the other hand non financial aspects includes external

environmental factors like political, technological, economical, etc. (Kokubu and Kitada,

2015) This measuring technique helps managers to consider cause of financial issues

confronted by company.

Financial governance: This is a process of regulating, controlling, monitoring and

managing monetary transactions of business. If there is continuous check on transactions,

it will lead to resolution of financial problems at the source itself. This tool also helps in

maintaining record of financial transaction in a systematic order.

Comparison:

Base for

comparison

Prime furniture London furniture outlet

Financial issue Major issue faced by this company

is that their revenues are constant

over the years and still their profit

margin is decreasing.

London furniture outlet are

continuously coming up with new

range of products but still their

market share is constant and not

coming up on growth pace.

Technique to With the help of technique of Benchmarking technique is useful for

8

recognize issue budgetary control, it was detected

that there is increase in operational

cost of company, hence, profit

margins are in decline mode.

this organisation. As with its

assistance, cause of lag in coverage

of market share can be identified, i.e.

ineffective marketing policies

MAS Useful policy in solving problem

related to increased cost is cost

accounting system. This system will

help in identifying reason for

incurring cost than what was

estimated (Shil, Hoque and Akter,

2019). To resolve this issue,

corrective actions are taken by

managers.

To increase market share, one

important tool is to create

competitive advantage by using

differential pricing strategy. In this

system, prices are set according to the

willingness and ability to pay by

customers. Also various promotional

strategies like offers, coupons, etc.

can be utilised in order to enhance

market share.

Management Accountant to solve financial problems

Management accountants possess best combinational streak of managerial expertise and

leadership qualities. They help preparation of financial accounts and multiple MAS techniques

reports such as pricing decisions, budgetary control, etc. These reports are then presented before

senior management. With the help of MAS reports, they also help senior management in

planning and formulating strategies that can improve financial health of the organisation

(Mahmoudian and et.al., 2020).

Conclusion

Above report show that management accounting system is key to sound financial health

of an organization. Integrating MAS techniques in business process helps management in

integrating efforts of various departments of an organization in direction to achieve

organizational objectives. Business Environment is complex and competitive. It helps

management in devising strategies that can give an edge to company over its competitors and

lead it to path of sustainable growth.

9

that there is increase in operational

cost of company, hence, profit

margins are in decline mode.

this organisation. As with its

assistance, cause of lag in coverage

of market share can be identified, i.e.

ineffective marketing policies

MAS Useful policy in solving problem

related to increased cost is cost

accounting system. This system will

help in identifying reason for

incurring cost than what was

estimated (Shil, Hoque and Akter,

2019). To resolve this issue,

corrective actions are taken by

managers.

To increase market share, one

important tool is to create

competitive advantage by using

differential pricing strategy. In this

system, prices are set according to the

willingness and ability to pay by

customers. Also various promotional

strategies like offers, coupons, etc.

can be utilised in order to enhance

market share.

Management Accountant to solve financial problems

Management accountants possess best combinational streak of managerial expertise and

leadership qualities. They help preparation of financial accounts and multiple MAS techniques

reports such as pricing decisions, budgetary control, etc. These reports are then presented before

senior management. With the help of MAS reports, they also help senior management in

planning and formulating strategies that can improve financial health of the organisation

(Mahmoudian and et.al., 2020).

Conclusion

Above report show that management accounting system is key to sound financial health

of an organization. Integrating MAS techniques in business process helps management in

integrating efforts of various departments of an organization in direction to achieve

organizational objectives. Business Environment is complex and competitive. It helps

management in devising strategies that can give an edge to company over its competitors and

lead it to path of sustainable growth.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Books and Journals

Rozhkova, N., Blinova, U. and Rozhkova, D., 2017, December. The concept of management

accounting based on the information technologies application. In International

Conference on Information Technology Science (pp. 89-95). Springer, Cham.

Schaltegger, S. and Zvezdov, D., 2015. Expanding material flow cost accounting. Framework,

review and potentials. Journal of Cleaner Production. 108. pp.1333-1341.

Shil, N.C., Hoque, M. and Akter, M., 2019. Revisiting Management Accounting Practice Gap: A

Proposed PERAPPGAP Model.Journal of Accounting and Finance. 19(1). pp.135-155.

Spraakman, G. and et.al., 2015. Employers’ perceptions of information technology competency

requirements for management accounting graduates. Accounting Education. 24(5).

pp.403-422.

Tucker, B.P. and Schaltegger, S., 2016. Comparing the research-practice gap in management

accounting. Accounting, Auditing & Accountability Journal.

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2020. Managerial accounting: tools for business

decision making. John Wiley & Sons.

Wouters, M. and Kirchberger, M.A., 2015. Customer value propositions as interorganizational

management accounting to support customer collaboration. Industrial Marketing

Management. 46. pp.54-67.

10

Books and Journals

Rozhkova, N., Blinova, U. and Rozhkova, D., 2017, December. The concept of management

accounting based on the information technologies application. In International

Conference on Information Technology Science (pp. 89-95). Springer, Cham.

Schaltegger, S. and Zvezdov, D., 2015. Expanding material flow cost accounting. Framework,

review and potentials. Journal of Cleaner Production. 108. pp.1333-1341.

Shil, N.C., Hoque, M. and Akter, M., 2019. Revisiting Management Accounting Practice Gap: A

Proposed PERAPPGAP Model.Journal of Accounting and Finance. 19(1). pp.135-155.

Spraakman, G. and et.al., 2015. Employers’ perceptions of information technology competency

requirements for management accounting graduates. Accounting Education. 24(5).

pp.403-422.

Tucker, B.P. and Schaltegger, S., 2016. Comparing the research-practice gap in management

accounting. Accounting, Auditing & Accountability Journal.

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2020. Managerial accounting: tools for business

decision making. John Wiley & Sons.

Wouters, M. and Kirchberger, M.A., 2015. Customer value propositions as interorganizational

management accounting to support customer collaboration. Industrial Marketing

Management. 46. pp.54-67.

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.