Management Accounting Report: Techniques and Systems for IG Group

VerifiedAdded on 2021/02/19

|17

|5276

|38

Report

AI Summary

This report offers a detailed examination of management accounting practices within the context of the IG Group, a financial accountancy firm. It begins by explaining the core concepts of management accounting, its systems, and the essential needs of various systems such as cost accounting, inventory management, job costing, and price optimization. The report then explores different reporting techniques, including budget reports, accounts receivable reports, cost management reports, and performance reports, evaluating their benefits and uses. A significant portion of the report is dedicated to preparing an income statement using both marginal and absorption costing methods, illustrating their application. Furthermore, it evaluates the benefits and limitations of various budgetary tools and planning tools. The report concludes by addressing how organizations like the IG Group adapt management accounting systems to respond to financial problems, providing a comprehensive overview of financial management strategies.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

P1. Explaining the concept of management accounting and the essential needs of various

systems of the management accounting......................................................................................1

P2. Explaining the different techniques that could be used as reporting under management

accounting...................................................................................................................................2

M1. Evaluating the benefits and the uses of the management accounting systems in an IG

Group..........................................................................................................................................3

LO2..................................................................................................................................................4

P3. Preparing the income statement with application of marginal and absorption costing

method.........................................................................................................................................4

LO3..................................................................................................................................................7

P4. Evaluating the benefits and the limitation of different budgetary tools................................7

M2.Explaining the uses and the application of the planning tools...........................................10

LO4................................................................................................................................................11

P5 Organisation adapting management accounting systems to respond to financial problems.

...................................................................................................................................................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

P1. Explaining the concept of management accounting and the essential needs of various

systems of the management accounting......................................................................................1

P2. Explaining the different techniques that could be used as reporting under management

accounting...................................................................................................................................2

M1. Evaluating the benefits and the uses of the management accounting systems in an IG

Group..........................................................................................................................................3

LO2..................................................................................................................................................4

P3. Preparing the income statement with application of marginal and absorption costing

method.........................................................................................................................................4

LO3..................................................................................................................................................7

P4. Evaluating the benefits and the limitation of different budgetary tools................................7

M2.Explaining the uses and the application of the planning tools...........................................10

LO4................................................................................................................................................11

P5 Organisation adapting management accounting systems to respond to financial problems.

...................................................................................................................................................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting refers to the practice of planning, directing, organising and

controlling the management functions within an IG Group. The present study is based on IG

group, a financial accountancy firm that provides the consultancy services to different IG

Groups. Furthermore, the report provides deep insights regarding the systems of the management

accounting and its applications. Moreover, it includes various techniques that can be used for

resolving the financial problems and also the different planning tools that can be used by the

firm.

LO1.

P1. Explaining the concept of management accounting and the essential needs of various systems

of the management accounting

Management accounting refers to the application of the appropriate methods and the

concepts in order to process historical and the estimated economic data of an enterprise for

helping the management in developing the plans for achieving the reasonable objectives. It also

ensures in making of the rational decisions towards reaching the goal effectively and efficiently

(Horton and de Araujo Wanderley, 2018). It is also known as the managerial or as cost

accounting, is referred as the process that is used for analysing the cost involved in the business

and the operations for preparing the financial report internally which in turn helps the managers

in making suitable decisions. Management accounting and financial accounting are the major

branch of the accounting and are different to a larger extent as MA deals with the formulation of

management reports while financial accounting relates to the framing of the financial statements.

Management accounting is optional on the part of the IG Group whereas financial accounting is

a compulsion for the company to adopt. There is no requirement for auditing the reports under

MA but it is mandatory for the enterprise to get auditing of its final reports from the statutory

auditor.

There are various systems under the management accounting which are important and plays a

crucial role in the smooth functioning of the operations of an entity is as follows-

Cost accounting system- It is called as the information system for the management in

terms of the determining the cost as it establishes the budget, actual cost and the standard cost. It

is the set of the procedures that are used for refining or converting the raw data into the usable

information in respect of making management decisions, for ascertaining the cost of the products

1

Management accounting refers to the practice of planning, directing, organising and

controlling the management functions within an IG Group. The present study is based on IG

group, a financial accountancy firm that provides the consultancy services to different IG

Groups. Furthermore, the report provides deep insights regarding the systems of the management

accounting and its applications. Moreover, it includes various techniques that can be used for

resolving the financial problems and also the different planning tools that can be used by the

firm.

LO1.

P1. Explaining the concept of management accounting and the essential needs of various systems

of the management accounting

Management accounting refers to the application of the appropriate methods and the

concepts in order to process historical and the estimated economic data of an enterprise for

helping the management in developing the plans for achieving the reasonable objectives. It also

ensures in making of the rational decisions towards reaching the goal effectively and efficiently

(Horton and de Araujo Wanderley, 2018). It is also known as the managerial or as cost

accounting, is referred as the process that is used for analysing the cost involved in the business

and the operations for preparing the financial report internally which in turn helps the managers

in making suitable decisions. Management accounting and financial accounting are the major

branch of the accounting and are different to a larger extent as MA deals with the formulation of

management reports while financial accounting relates to the framing of the financial statements.

Management accounting is optional on the part of the IG Group whereas financial accounting is

a compulsion for the company to adopt. There is no requirement for auditing the reports under

MA but it is mandatory for the enterprise to get auditing of its final reports from the statutory

auditor.

There are various systems under the management accounting which are important and plays a

crucial role in the smooth functioning of the operations of an entity is as follows-

Cost accounting system- It is called as the information system for the management in

terms of the determining the cost as it establishes the budget, actual cost and the standard cost. It

is the set of the procedures that are used for refining or converting the raw data into the usable

information in respect of making management decisions, for ascertaining the cost of the products

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and the services and assessing the profitability. This system plays an essential role in the IG

Group as it helps in making the analysis of the cost behaviour patterns of different items of the

expenditure within an IG Group (Messner, 2016). It enables an enterprise in estimating the future

cost with the reasonable accuracies.

Inventory management system- It refers to the system of management accounting that

tracks the goods throughout the supply chain or in the overall portion within which the business

operates. This system plays a significant role in managing the order as it helps in integrating and

tracking the orders from the different marketplaces (Quattrone, 2016). It enables the mangers in

creating the appropriate purchase order from their suppliers and also helps in managing the

inventory in the smart way against the competitors of the company.

Job costing system- It is the system that includes the processing of accumulating the

information relating to the cost attached with the particular production or the services. The

information provided by this system is essential for submitting the information of the cost to the

customers under the contract where the cost could be reimbursed. Such information is useful for

determining accuracy in the estimating system of the company that could help in quoting or

fixing the prices which allows for the reasonable profit.

Price optimization system- It is the system of the management accounting that

mathematically analyse the response of the customer towards different price level of the IG

Group's product and the services through the various channels (Sinaga and et.al., 2019). This

helps an entity in determining or fixing the best possible prices so that larger profits could be

generated and this in turn results in the achievement of the objective of a business that is profit

maximization.

P2. Explaining the different techniques that could be used as reporting under management

accounting

Management accounting reports is been used by the IG Group for the purpose of

planning, decision making, regulating and in measuring the performance. Such reports are been

continuously been generated in order to keep the appropriate records regarding the internal

working of an enterprise. Most of the critical decisions are based on the accuracy of such reports.

Therefore, preparation of these reports requires the highly skilled people or the experts so that

useful information could be gathered by the company (Malina, ed., 2018). Different reports that

are been framed by the managers are as follows-

2

Group as it helps in making the analysis of the cost behaviour patterns of different items of the

expenditure within an IG Group (Messner, 2016). It enables an enterprise in estimating the future

cost with the reasonable accuracies.

Inventory management system- It refers to the system of management accounting that

tracks the goods throughout the supply chain or in the overall portion within which the business

operates. This system plays a significant role in managing the order as it helps in integrating and

tracking the orders from the different marketplaces (Quattrone, 2016). It enables the mangers in

creating the appropriate purchase order from their suppliers and also helps in managing the

inventory in the smart way against the competitors of the company.

Job costing system- It is the system that includes the processing of accumulating the

information relating to the cost attached with the particular production or the services. The

information provided by this system is essential for submitting the information of the cost to the

customers under the contract where the cost could be reimbursed. Such information is useful for

determining accuracy in the estimating system of the company that could help in quoting or

fixing the prices which allows for the reasonable profit.

Price optimization system- It is the system of the management accounting that

mathematically analyse the response of the customer towards different price level of the IG

Group's product and the services through the various channels (Sinaga and et.al., 2019). This

helps an entity in determining or fixing the best possible prices so that larger profits could be

generated and this in turn results in the achievement of the objective of a business that is profit

maximization.

P2. Explaining the different techniques that could be used as reporting under management

accounting

Management accounting reports is been used by the IG Group for the purpose of

planning, decision making, regulating and in measuring the performance. Such reports are been

continuously been generated in order to keep the appropriate records regarding the internal

working of an enterprise. Most of the critical decisions are based on the accuracy of such reports.

Therefore, preparation of these reports requires the highly skilled people or the experts so that

useful information could be gathered by the company (Malina, ed., 2018). Different reports that

are been framed by the managers are as follows-

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

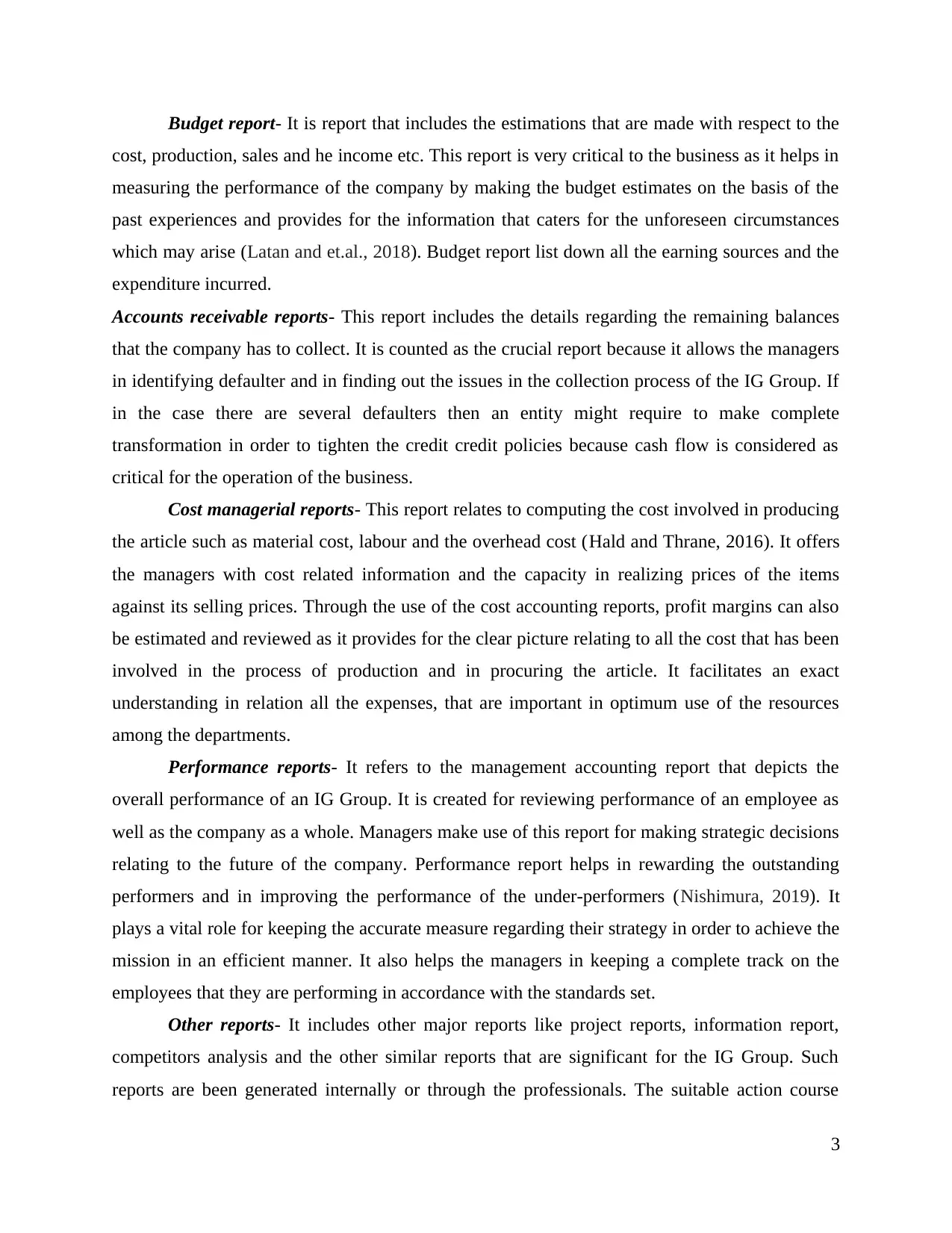

Budget report- It is report that includes the estimations that are made with respect to the

cost, production, sales and he income etc. This report is very critical to the business as it helps in

measuring the performance of the company by making the budget estimates on the basis of the

past experiences and provides for the information that caters for the unforeseen circumstances

which may arise (Latan and et.al., 2018). Budget report list down all the earning sources and the

expenditure incurred.

Accounts receivable reports- This report includes the details regarding the remaining balances

that the company has to collect. It is counted as the crucial report because it allows the managers

in identifying defaulter and in finding out the issues in the collection process of the IG Group. If

in the case there are several defaulters then an entity might require to make complete

transformation in order to tighten the credit credit policies because cash flow is considered as

critical for the operation of the business.

Cost managerial reports- This report relates to computing the cost involved in producing

the article such as material cost, labour and the overhead cost (Hald and Thrane, 2016). It offers

the managers with cost related information and the capacity in realizing prices of the items

against its selling prices. Through the use of the cost accounting reports, profit margins can also

be estimated and reviewed as it provides for the clear picture relating to all the cost that has been

involved in the process of production and in procuring the article. It facilitates an exact

understanding in relation all the expenses, that are important in optimum use of the resources

among the departments.

Performance reports- It refers to the management accounting report that depicts the

overall performance of an IG Group. It is created for reviewing performance of an employee as

well as the company as a whole. Managers make use of this report for making strategic decisions

relating to the future of the company. Performance report helps in rewarding the outstanding

performers and in improving the performance of the under-performers (Nishimura, 2019). It

plays a vital role for keeping the accurate measure regarding their strategy in order to achieve the

mission in an efficient manner. It also helps the managers in keeping a complete track on the

employees that they are performing in accordance with the standards set.

Other reports- It includes other major reports like project reports, information report,

competitors analysis and the other similar reports that are significant for the IG Group. Such

reports are been generated internally or through the professionals. The suitable action course

3

cost, production, sales and he income etc. This report is very critical to the business as it helps in

measuring the performance of the company by making the budget estimates on the basis of the

past experiences and provides for the information that caters for the unforeseen circumstances

which may arise (Latan and et.al., 2018). Budget report list down all the earning sources and the

expenditure incurred.

Accounts receivable reports- This report includes the details regarding the remaining balances

that the company has to collect. It is counted as the crucial report because it allows the managers

in identifying defaulter and in finding out the issues in the collection process of the IG Group. If

in the case there are several defaulters then an entity might require to make complete

transformation in order to tighten the credit credit policies because cash flow is considered as

critical for the operation of the business.

Cost managerial reports- This report relates to computing the cost involved in producing

the article such as material cost, labour and the overhead cost (Hald and Thrane, 2016). It offers

the managers with cost related information and the capacity in realizing prices of the items

against its selling prices. Through the use of the cost accounting reports, profit margins can also

be estimated and reviewed as it provides for the clear picture relating to all the cost that has been

involved in the process of production and in procuring the article. It facilitates an exact

understanding in relation all the expenses, that are important in optimum use of the resources

among the departments.

Performance reports- It refers to the management accounting report that depicts the

overall performance of an IG Group. It is created for reviewing performance of an employee as

well as the company as a whole. Managers make use of this report for making strategic decisions

relating to the future of the company. Performance report helps in rewarding the outstanding

performers and in improving the performance of the under-performers (Nishimura, 2019). It

plays a vital role for keeping the accurate measure regarding their strategy in order to achieve the

mission in an efficient manner. It also helps the managers in keeping a complete track on the

employees that they are performing in accordance with the standards set.

Other reports- It includes other major reports like project reports, information report,

competitors analysis and the other similar reports that are significant for the IG Group. Such

reports are been generated internally or through the professionals. The suitable action course

3

depends on the capabilities in handling to the reporting requirements of firm. Ideal choice could

differ from person to person but the professional services is having the experience and the skills

in carrying out the task in a better way. For reaching out to major of the decisions, managers of

the IG Group must be having the access to the authentic and the credible reports of management

accounting.

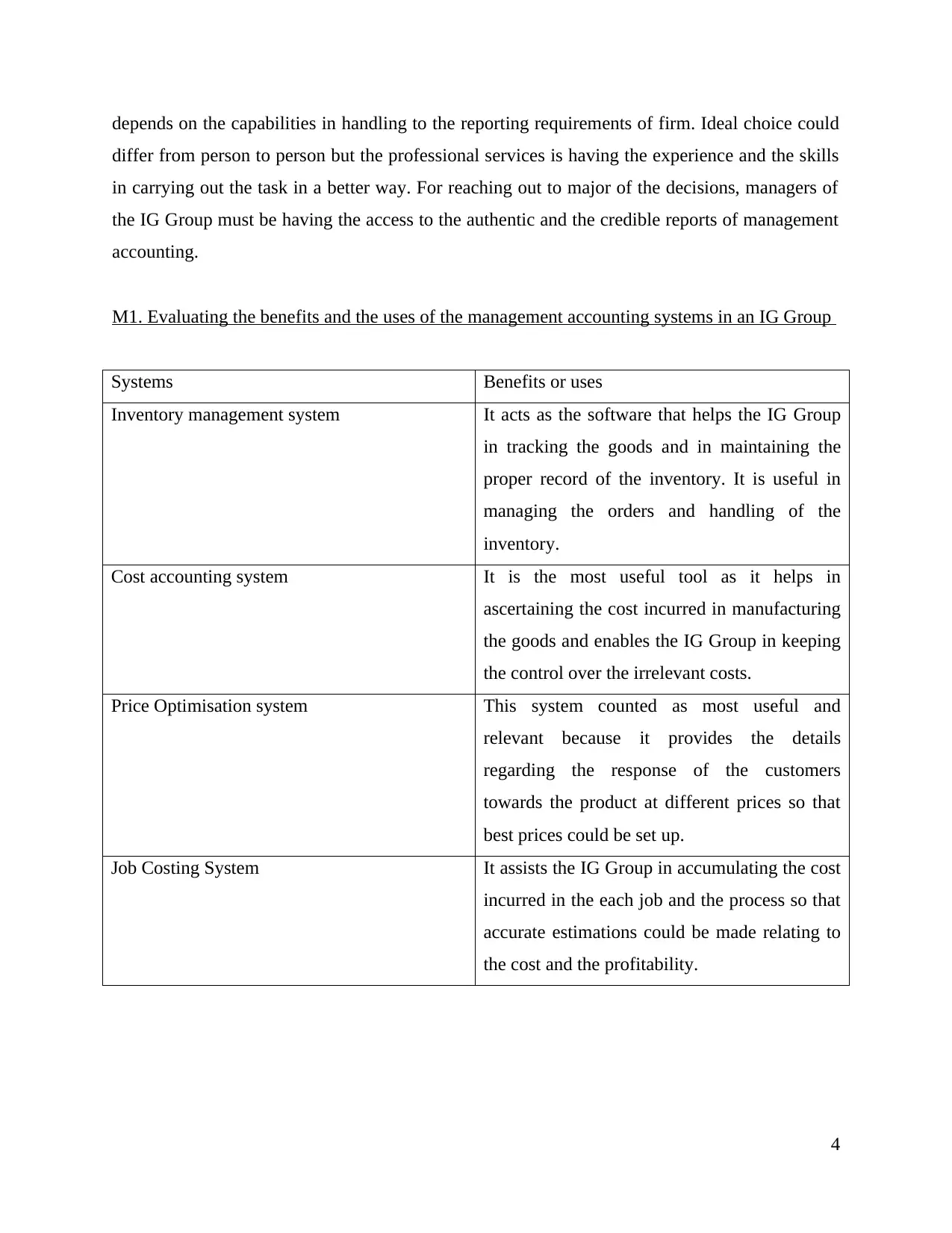

M1. Evaluating the benefits and the uses of the management accounting systems in an IG Group

Systems Benefits or uses

Inventory management system It acts as the software that helps the IG Group

in tracking the goods and in maintaining the

proper record of the inventory. It is useful in

managing the orders and handling of the

inventory.

Cost accounting system It is the most useful tool as it helps in

ascertaining the cost incurred in manufacturing

the goods and enables the IG Group in keeping

the control over the irrelevant costs.

Price Optimisation system This system counted as most useful and

relevant because it provides the details

regarding the response of the customers

towards the product at different prices so that

best prices could be set up.

Job Costing System It assists the IG Group in accumulating the cost

incurred in the each job and the process so that

accurate estimations could be made relating to

the cost and the profitability.

4

differ from person to person but the professional services is having the experience and the skills

in carrying out the task in a better way. For reaching out to major of the decisions, managers of

the IG Group must be having the access to the authentic and the credible reports of management

accounting.

M1. Evaluating the benefits and the uses of the management accounting systems in an IG Group

Systems Benefits or uses

Inventory management system It acts as the software that helps the IG Group

in tracking the goods and in maintaining the

proper record of the inventory. It is useful in

managing the orders and handling of the

inventory.

Cost accounting system It is the most useful tool as it helps in

ascertaining the cost incurred in manufacturing

the goods and enables the IG Group in keeping

the control over the irrelevant costs.

Price Optimisation system This system counted as most useful and

relevant because it provides the details

regarding the response of the customers

towards the product at different prices so that

best prices could be set up.

Job Costing System It assists the IG Group in accumulating the cost

incurred in the each job and the process so that

accurate estimations could be made relating to

the cost and the profitability.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

LO2

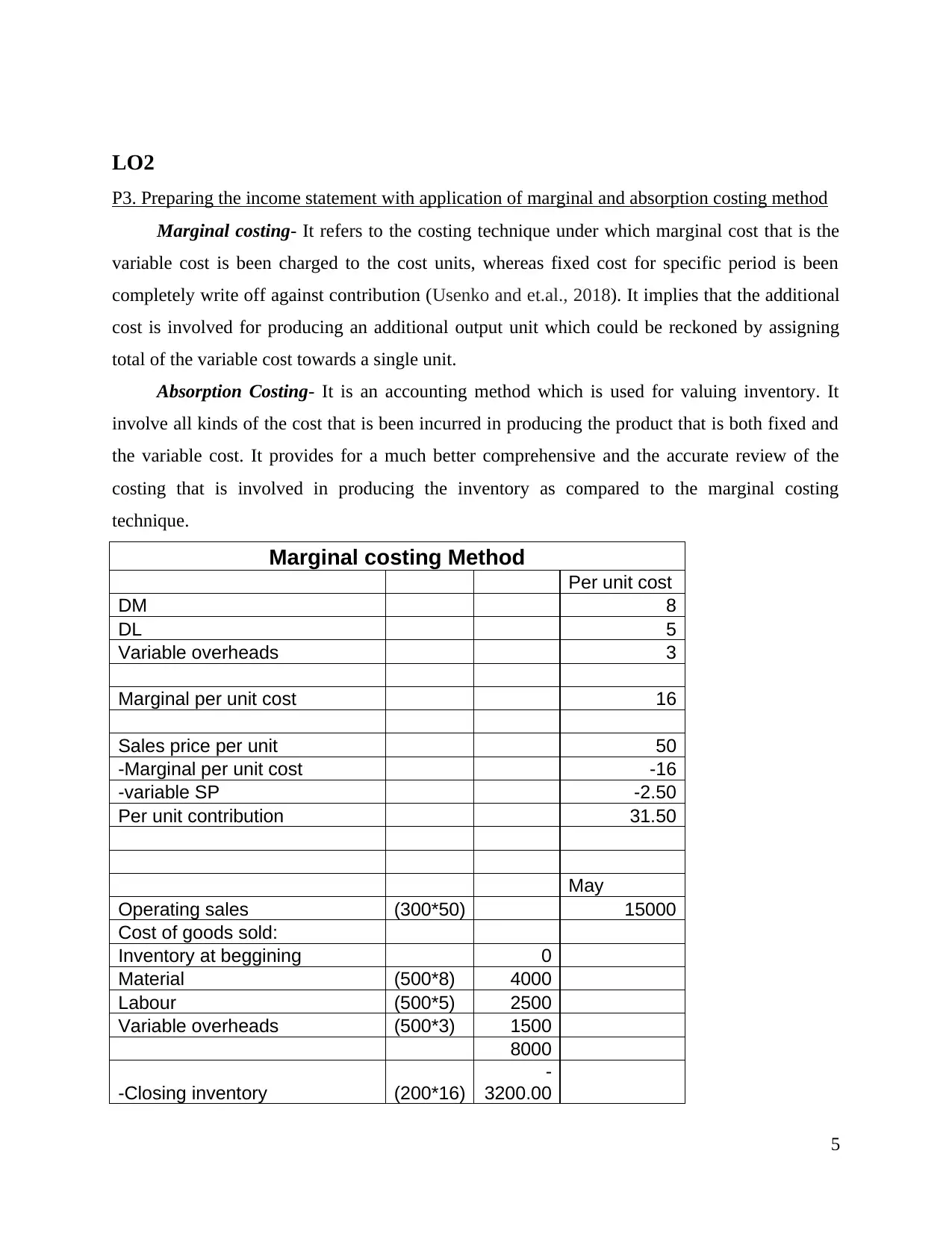

P3. Preparing the income statement with application of marginal and absorption costing method

Marginal costing- It refers to the costing technique under which marginal cost that is the

variable cost is been charged to the cost units, whereas fixed cost for specific period is been

completely write off against contribution (Usenko and et.al., 2018). It implies that the additional

cost is involved for producing an additional output unit which could be reckoned by assigning

total of the variable cost towards a single unit.

Absorption Costing- It is an accounting method which is used for valuing inventory. It

involve all kinds of the cost that is been incurred in producing the product that is both fixed and

the variable cost. It provides for a much better comprehensive and the accurate review of the

costing that is involved in producing the inventory as compared to the marginal costing

technique.

Marginal costing Method

Per unit cost

DM 8

DL 5

Variable overheads 3

Marginal per unit cost 16

Sales price per unit 50

-Marginal per unit cost -16

-variable SP -2.50

Per unit contribution 31.50

May

Operating sales (300*50) 15000

Cost of goods sold:

Inventory at beggining 0

Material (500*8) 4000

Labour (500*5) 2500

Variable overheads (500*3) 1500

8000

-Closing inventory (200*16)

-

3200.00

5

P3. Preparing the income statement with application of marginal and absorption costing method

Marginal costing- It refers to the costing technique under which marginal cost that is the

variable cost is been charged to the cost units, whereas fixed cost for specific period is been

completely write off against contribution (Usenko and et.al., 2018). It implies that the additional

cost is involved for producing an additional output unit which could be reckoned by assigning

total of the variable cost towards a single unit.

Absorption Costing- It is an accounting method which is used for valuing inventory. It

involve all kinds of the cost that is been incurred in producing the product that is both fixed and

the variable cost. It provides for a much better comprehensive and the accurate review of the

costing that is involved in producing the inventory as compared to the marginal costing

technique.

Marginal costing Method

Per unit cost

DM 8

DL 5

Variable overheads 3

Marginal per unit cost 16

Sales price per unit 50

-Marginal per unit cost -16

-variable SP -2.50

Per unit contribution 31.50

May

Operating sales (300*50) 15000

Cost of goods sold:

Inventory at beggining 0

Material (500*8) 4000

Labour (500*5) 2500

Variable overheads (500*3) 1500

8000

-Closing inventory (200*16)

-

3200.00

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

-4800

10200

-Variable cost -750

Contribution 9450

-FC -10000

(Net Loss) -550

June

Operating revenue (500*50) 25000

Cost of goods sold:

Inventory at beginning (200*16) 3200

Material (380*8) 3040

Labour (380*5) 1900

Variable overhead (380*3) 1140

9280

-inventory at ending (80*16) -1280

-8000

17000

-Variable cost -1250

Contribution 15750

-FC -10000

Net profit 5750

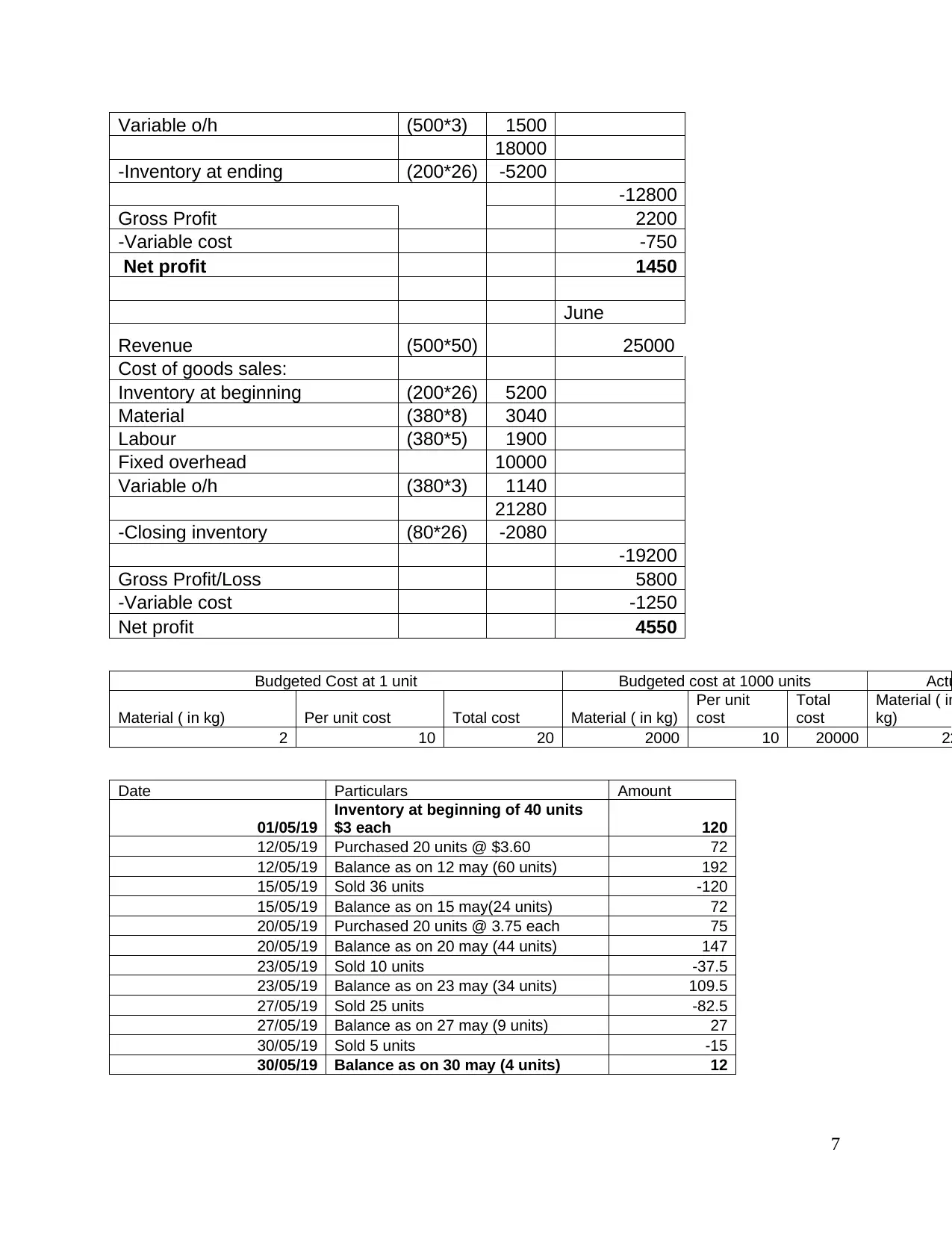

Absorption Costing Method

Cost per unit

Direst Material 8

Direst Labour 5

Variable Overhead 3

Fixed overhead 10

Total absorption per unit cost 26

May

Revenue (300*50) 15000

Cost of goods sales:

Inventory at beginning 0

Material (500*8) 4000

Labour (500*5) 2500

Fixed overhead 10000

6

10200

-Variable cost -750

Contribution 9450

-FC -10000

(Net Loss) -550

June

Operating revenue (500*50) 25000

Cost of goods sold:

Inventory at beginning (200*16) 3200

Material (380*8) 3040

Labour (380*5) 1900

Variable overhead (380*3) 1140

9280

-inventory at ending (80*16) -1280

-8000

17000

-Variable cost -1250

Contribution 15750

-FC -10000

Net profit 5750

Absorption Costing Method

Cost per unit

Direst Material 8

Direst Labour 5

Variable Overhead 3

Fixed overhead 10

Total absorption per unit cost 26

May

Revenue (300*50) 15000

Cost of goods sales:

Inventory at beginning 0

Material (500*8) 4000

Labour (500*5) 2500

Fixed overhead 10000

6

Variable o/h (500*3) 1500

18000

-Inventory at ending (200*26) -5200

-12800

Gross Profit 2200

-Variable cost -750

Net profit 1450

June

Revenue (500*50) 25000

Cost of goods sales:

Inventory at beginning (200*26) 5200

Material (380*8) 3040

Labour (380*5) 1900

Fixed overhead 10000

Variable o/h (380*3) 1140

21280

-Closing inventory (80*26) -2080

-19200

Gross Profit/Loss 5800

-Variable cost -1250

Net profit 4550

Budgeted Cost at 1 unit Budgeted cost at 1000 units Actu

Material ( in kg) Per unit cost Total cost Material ( in kg)

Per unit

cost

Total

cost

Material ( in

kg)

2 10 20 2000 10 20000 22

Date Particulars Amount

01/05/19

Inventory at beginning of 40 units

$3 each 120

12/05/19 Purchased 20 units @ $3.60 72

12/05/19 Balance as on 12 may (60 units) 192

15/05/19 Sold 36 units -120

15/05/19 Balance as on 15 may(24 units) 72

20/05/19 Purchased 20 units @ 3.75 each 75

20/05/19 Balance as on 20 may (44 units) 147

23/05/19 Sold 10 units -37.5

23/05/19 Balance as on 23 may (34 units) 109.5

27/05/19 Sold 25 units -82.5

27/05/19 Balance as on 27 may (9 units) 27

30/05/19 Sold 5 units -15

30/05/19 Balance as on 30 may (4 units) 12

7

18000

-Inventory at ending (200*26) -5200

-12800

Gross Profit 2200

-Variable cost -750

Net profit 1450

June

Revenue (500*50) 25000

Cost of goods sales:

Inventory at beginning (200*26) 5200

Material (380*8) 3040

Labour (380*5) 1900

Fixed overhead 10000

Variable o/h (380*3) 1140

21280

-Closing inventory (80*26) -2080

-19200

Gross Profit/Loss 5800

-Variable cost -1250

Net profit 4550

Budgeted Cost at 1 unit Budgeted cost at 1000 units Actu

Material ( in kg) Per unit cost Total cost Material ( in kg)

Per unit

cost

Total

cost

Material ( in

kg)

2 10 20 2000 10 20000 22

Date Particulars Amount

01/05/19

Inventory at beginning of 40 units

$3 each 120

12/05/19 Purchased 20 units @ $3.60 72

12/05/19 Balance as on 12 may (60 units) 192

15/05/19 Sold 36 units -120

15/05/19 Balance as on 15 may(24 units) 72

20/05/19 Purchased 20 units @ 3.75 each 75

20/05/19 Balance as on 20 may (44 units) 147

23/05/19 Sold 10 units -37.5

23/05/19 Balance as on 23 may (34 units) 109.5

27/05/19 Sold 25 units -82.5

27/05/19 Balance as on 27 may (9 units) 27

30/05/19 Sold 5 units -15

30/05/19 Balance as on 30 may (4 units) 12

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Interpretation- From the above interpretation it has been interpreted that in the month of

May marginal costing method is showing the net loss amounting to 550 while absorption costing

reflecting the net profit resulted as 1450. On the other hand, In the month of June, net profit

gained by applying marginal costing equated to 5750 while through absorption costing, net profit

of 4550 is been gained. This means that absorption costing provides a better and accurate view of

the profits rather than the marginal costing because it takes into account both variable and fixed

cost whereas marginal costing involves only variable cost.

LO3

P4. Evaluating the benefits and the limitation of different budgetary tools

Zero based budget- It refers to the preparation of the budget from the grounds or scratch

and involves the re-evaluation of each line item from the statement of cash flow with

justification of each and every expenditure which is been incurred by department within IG

Group (Mills, 2018). Under this budget all expenses are been in respect of new period are

computed based on the actual expenses and not on basis of differential in which only the changes

incurred under the operational activity are taken into account.

Advantages: It is the budgeting tool that is useful at the time when IG Group desires to

assess the activities of its business from the zero bases. Zero based budgets provides for the

allocation of the resources efficiently within the entire department because it doesn’t considers

historical figures but accounts for the actual numbers (Zero Based Budgeting ( ZBB ) –

Overview & Advantages, 2018). This budget enables the enterprise in determining the new

schemes and using effective tools for optimum use of the resources and eliminating irrelevant

activities within the IG Group. It helps the organization in achieving its objective of profit

maximization as it facilitates orientation for attaining economies of scale in the operation of

business. This budgeting technique helps in responding towards the changes within the company

as with the changes in the technology, the assumptions and the expenses in the processes also

changes.

Disadvantages : The nature of this planning tool is subjective as it provides for the

qualitative benefits which couldn’t be measured in terms of numbers. This budget is detrimental

towards long run goals and runs on the basis of the cost benefit analysis for a specific period. It

includes more expenses and large number of the decision packages are been prepared which in

turn results in time consuming task.

8

May marginal costing method is showing the net loss amounting to 550 while absorption costing

reflecting the net profit resulted as 1450. On the other hand, In the month of June, net profit

gained by applying marginal costing equated to 5750 while through absorption costing, net profit

of 4550 is been gained. This means that absorption costing provides a better and accurate view of

the profits rather than the marginal costing because it takes into account both variable and fixed

cost whereas marginal costing involves only variable cost.

LO3

P4. Evaluating the benefits and the limitation of different budgetary tools

Zero based budget- It refers to the preparation of the budget from the grounds or scratch

and involves the re-evaluation of each line item from the statement of cash flow with

justification of each and every expenditure which is been incurred by department within IG

Group (Mills, 2018). Under this budget all expenses are been in respect of new period are

computed based on the actual expenses and not on basis of differential in which only the changes

incurred under the operational activity are taken into account.

Advantages: It is the budgeting tool that is useful at the time when IG Group desires to

assess the activities of its business from the zero bases. Zero based budgets provides for the

allocation of the resources efficiently within the entire department because it doesn’t considers

historical figures but accounts for the actual numbers (Zero Based Budgeting ( ZBB ) –

Overview & Advantages, 2018). This budget enables the enterprise in determining the new

schemes and using effective tools for optimum use of the resources and eliminating irrelevant

activities within the IG Group. It helps the organization in achieving its objective of profit

maximization as it facilitates orientation for attaining economies of scale in the operation of

business. This budgeting technique helps in responding towards the changes within the company

as with the changes in the technology, the assumptions and the expenses in the processes also

changes.

Disadvantages : The nature of this planning tool is subjective as it provides for the

qualitative benefits which couldn’t be measured in terms of numbers. This budget is detrimental

towards long run goals and runs on the basis of the cost benefit analysis for a specific period. It

includes more expenses and large number of the decision packages are been prepared which in

turn results in time consuming task.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity based budget- It refers to the planning tool that allocated the resources on the

basis of the relationship in between the activities and the cost that facilitates more details in

relation to the overheads than normal budgeting (Curry, 2019). It provides for refining the cost

and emphasizing on the number of activities that are been occurred in the IG Group.

Advantages : It is the budgetary tool that involves each and every step within the activity

which in turn results in elimination of the unnecessary activities and determining the relevant

activities. This planning tool enables in reviewing the business of the entire organization as one

business unit, not as department wise. The budget under this method is been prepared after

detailed analysis which helps in removing all kinds of the bottlenecks if any present in the

activity of the business. Activity based budget allows for balancing the operational requirements

and highlights the inefficient and imbalance sources for making improvements .

Disadvantages : For implementing this budget technique an organization needs highly

skilled and trained employees. This result in huge cost involvement for providing raining to the

employees. It emphasizes on the short term objectives and not considers the long term goals of

business. The budgeting process under this technique consumes ample of the resources and

requires to involve top executives in order to conduct the numerous analyses. Activity based

budget involves duplication as it is not counted as the control budget which in turn do not replace

line item of budget.

Rolling budget- This budgetary tool referred as the revised or consistently updated budget

in order to add the budget for the new period (Chenhall and Moers, 2015). It includes

incremental extension from the existing model of the budget. This budget facilitates the

extension for the future accounting periods.

Advantages : Rolling budget facilitates flexibility in context of incorporating the changes

from past years into the coming periods. This helps the enterprise in getting more updated

information. It enables the organization in being responsive towards the uncertain changes and

allows for adjusting the changes that could be occurred in the future. It provides for continuous

revision of the budget. Rolling budget assist the firm in controlling and planning accurately

which in turn reduces uncertainty in the long run.

9

basis of the relationship in between the activities and the cost that facilitates more details in

relation to the overheads than normal budgeting (Curry, 2019). It provides for refining the cost

and emphasizing on the number of activities that are been occurred in the IG Group.

Advantages : It is the budgetary tool that involves each and every step within the activity

which in turn results in elimination of the unnecessary activities and determining the relevant

activities. This planning tool enables in reviewing the business of the entire organization as one

business unit, not as department wise. The budget under this method is been prepared after

detailed analysis which helps in removing all kinds of the bottlenecks if any present in the

activity of the business. Activity based budget allows for balancing the operational requirements

and highlights the inefficient and imbalance sources for making improvements .

Disadvantages : For implementing this budget technique an organization needs highly

skilled and trained employees. This result in huge cost involvement for providing raining to the

employees. It emphasizes on the short term objectives and not considers the long term goals of

business. The budgeting process under this technique consumes ample of the resources and

requires to involve top executives in order to conduct the numerous analyses. Activity based

budget involves duplication as it is not counted as the control budget which in turn do not replace

line item of budget.

Rolling budget- This budgetary tool referred as the revised or consistently updated budget

in order to add the budget for the new period (Chenhall and Moers, 2015). It includes

incremental extension from the existing model of the budget. This budget facilitates the

extension for the future accounting periods.

Advantages : Rolling budget facilitates flexibility in context of incorporating the changes

from past years into the coming periods. This helps the enterprise in getting more updated

information. It enables the organization in being responsive towards the uncertain changes and

allows for adjusting the changes that could be occurred in the future. It provides for continuous

revision of the budget. Rolling budget assist the firm in controlling and planning accurately

which in turn reduces uncertainty in the long run.

9

Disadvantages : This budget method is not suitable in case the conditions are not been

continuously changing as it results in wastage of the resources as well as the time. Rolling

budget accounts for the formulation of entirely new budget on a frequent basis and needs robust

information with highly professional personnel for extracting the information. Creation of rolling

budget involves lot of time and in order forecast the expenses and the revenues of the business,

budget needs to be prepared every month.

M2.Explaining the uses and the application of the planning tools

Planning tools Uses and application

Zero based budgeting It is the most useful tool as it provides for re-

examination and the re-evaluation of all the

items and also provides for the justification of

each and every expense that is incurred by the

IG Group. This tool is applied where the new

product or the business is to be begun.

Activity based budget This budgetary tool is counted as useful

because it takes into account the changes and

the cost involved in each activity so that

relevant anticipations could be made (Alamri,

2019). It is been applied in the business where

there are several activities running within the

work environment of IG Group.

Rolling budget This tool provides for continuous revision of

the budget for each new period so that

flexibility could be ascertained and facilitates

for assessing the changes that had been

occurred in the operations of the business.

10

continuously changing as it results in wastage of the resources as well as the time. Rolling

budget accounts for the formulation of entirely new budget on a frequent basis and needs robust

information with highly professional personnel for extracting the information. Creation of rolling

budget involves lot of time and in order forecast the expenses and the revenues of the business,

budget needs to be prepared every month.

M2.Explaining the uses and the application of the planning tools

Planning tools Uses and application

Zero based budgeting It is the most useful tool as it provides for re-

examination and the re-evaluation of all the

items and also provides for the justification of

each and every expense that is incurred by the

IG Group. This tool is applied where the new

product or the business is to be begun.

Activity based budget This budgetary tool is counted as useful

because it takes into account the changes and

the cost involved in each activity so that

relevant anticipations could be made (Alamri,

2019). It is been applied in the business where

there are several activities running within the

work environment of IG Group.

Rolling budget This tool provides for continuous revision of

the budget for each new period so that

flexibility could be ascertained and facilitates

for assessing the changes that had been

occurred in the operations of the business.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.