Comprehensive Analysis of Management Accounting in Hammond Electronics

VerifiedAdded on 2023/06/08

|16

|4764

|402

Report

AI Summary

This report delves into the core principles of management accounting, exploring its significance in organizational decision-making and financial control. It provides a comprehensive overview of management accounting systems, methods, and techniques, including variable and absorption costing, and their impact on financial statements. The report analyzes the role of management accounting within organizations, using Hammond Electronics as a case study, highlighting the benefits of the function and its integration into business operations. Furthermore, it explains various planning tools in management accounting, such as capital budgeting and budgeting analysis. The report also assesses how organizations adapt to financial problems and concludes with recommendations for effective management accounting practices.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

PART-1............................................................................................................................................3

1. Principles of management accounting.....................................................................................3

2. Role of Management accounting and Management accounting systems................................4

3. Techniques and methods used in management accounting, and income statements using

both variable costing and absorption costing...............................................................................4

4. Management accounting within the organization....................................................................7

5. Benefits of the function to the organization.............................................................................7

6. Conclusion on the reflection of application of management accounting.................................8

PART 2............................................................................................................................................9

Explaining three planning tools in management accounting.......................................................9

Comparing how organization adapt the management accounting system to respond financial

problems.....................................................................................................................................11

Recommendations .....................................................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

PART-1............................................................................................................................................3

1. Principles of management accounting.....................................................................................3

2. Role of Management accounting and Management accounting systems................................4

3. Techniques and methods used in management accounting, and income statements using

both variable costing and absorption costing...............................................................................4

4. Management accounting within the organization....................................................................7

5. Benefits of the function to the organization.............................................................................7

6. Conclusion on the reflection of application of management accounting.................................8

PART 2............................................................................................................................................9

Explaining three planning tools in management accounting.......................................................9

Comparing how organization adapt the management accounting system to respond financial

problems.....................................................................................................................................11

Recommendations .....................................................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES................................................................................................................................1

INTRODUCTION

Management accounting refers to the practice of identifying, analysing, interpreting and

communicating with the financial information of the company to the managers in order to

achieve goals. This used to play a vital role in the company as this helps to record the financial

transactions of the company. The current report is based on Hammond Electronics which is the

medium- sized manufacturing company in the market of UK. This report will put some focus on

the meaning of management accounting and the different types of management accounting

systems. Further this report will outline the different methods that are used for doing the

management accounting reporting in the company. This will also include the income statement

of the company by using the marginal and absorption costs. Moreover, there will also be

inclusion of different planning tools with its advantages and disadvantages. At last this report

will include the ways that the organizations can adapt in order to respond financial problems.

PART-1

1. Principles of management accounting

There are number of principles of management accounting which are used in order to

hike managerial efficiency in making decisions pertaining to organizational management. The

principles of management accounting helps to ensure higher quality of management accounting

practises (Johnstone, 2020) The principles are as-

1. Accuracy of accounts

2. Punctuality

3. Stability and consistency

4. Measuring efficiency

5. Maximization of use of resources

6. Presentation of unbiased data

7. principle of exception

8. Forecasting the problems.

These principles are having their great importance since they are driving the management

accounting practises in the organization. These factors can be sited as governing factors of

management accounting.

Management accounting refers to the practice of identifying, analysing, interpreting and

communicating with the financial information of the company to the managers in order to

achieve goals. This used to play a vital role in the company as this helps to record the financial

transactions of the company. The current report is based on Hammond Electronics which is the

medium- sized manufacturing company in the market of UK. This report will put some focus on

the meaning of management accounting and the different types of management accounting

systems. Further this report will outline the different methods that are used for doing the

management accounting reporting in the company. This will also include the income statement

of the company by using the marginal and absorption costs. Moreover, there will also be

inclusion of different planning tools with its advantages and disadvantages. At last this report

will include the ways that the organizations can adapt in order to respond financial problems.

PART-1

1. Principles of management accounting

There are number of principles of management accounting which are used in order to

hike managerial efficiency in making decisions pertaining to organizational management. The

principles of management accounting helps to ensure higher quality of management accounting

practises (Johnstone, 2020) The principles are as-

1. Accuracy of accounts

2. Punctuality

3. Stability and consistency

4. Measuring efficiency

5. Maximization of use of resources

6. Presentation of unbiased data

7. principle of exception

8. Forecasting the problems.

These principles are having their great importance since they are driving the management

accounting practises in the organization. These factors can be sited as governing factors of

management accounting.

2. Role of Management accounting and Management accounting systems

Management accounting is very much essential for an organization. The “Hammond Electronics”

is engaged in different manufacturing businesses such as Classic audio transformers, rack

mounting solutions, small enclosures etc. the management is supposed to make some drastic

decisions in order to ensure higher ability and performance of the company, which can only be

ensured by management accounting (Pelz, 2019)

Management accounting helps to record the key actions which are having potential to

affect managerial decision making.

At the same time it helps to choose the best set of investments, since by the additional

funds are supposed to get managed.

The key tools such as cash flow management is also used, which helps to known the flow

of cash. It paves the way that how the movement of cash is happening and how it can be

controlled.

Ratio analysis is another aspect which aids to understand the relationship between range

of factors and drive to take rational and lucrative decisions.

Management accounting system is an intended method of making statements, reports in

order to help management to take them into consideration in order to make managerial decisions.

There are number of management accounting system types such as cost accounting system, job

costing system, cash flow analysis, capital budgeting, leverage metrics, constraint analysis etc.

The biggest advantage of the management accounting system is to ensure such

accounting practises to be well structured in nature.

The maximum advantage can only be curbed if the system is aligning with the

organizational needs (Hiromoto, 2019)

It further helps to reduce the cost factor and soaring their outcomes in attempt to make it

a rational practise.

3. Techniques and methods used in management accounting, and income statements using both

variable costing and absorption costing

There are number of methods, which are used in management accounting. Since the main

aim of management accounting is to help management in making rational, appropriate and the

most logical decisions. With this regard, some key methods of management accounting are as-

Capital budgeting analysis-

Management accounting is very much essential for an organization. The “Hammond Electronics”

is engaged in different manufacturing businesses such as Classic audio transformers, rack

mounting solutions, small enclosures etc. the management is supposed to make some drastic

decisions in order to ensure higher ability and performance of the company, which can only be

ensured by management accounting (Pelz, 2019)

Management accounting helps to record the key actions which are having potential to

affect managerial decision making.

At the same time it helps to choose the best set of investments, since by the additional

funds are supposed to get managed.

The key tools such as cash flow management is also used, which helps to known the flow

of cash. It paves the way that how the movement of cash is happening and how it can be

controlled.

Ratio analysis is another aspect which aids to understand the relationship between range

of factors and drive to take rational and lucrative decisions.

Management accounting system is an intended method of making statements, reports in

order to help management to take them into consideration in order to make managerial decisions.

There are number of management accounting system types such as cost accounting system, job

costing system, cash flow analysis, capital budgeting, leverage metrics, constraint analysis etc.

The biggest advantage of the management accounting system is to ensure such

accounting practises to be well structured in nature.

The maximum advantage can only be curbed if the system is aligning with the

organizational needs (Hiromoto, 2019)

It further helps to reduce the cost factor and soaring their outcomes in attempt to make it

a rational practise.

3. Techniques and methods used in management accounting, and income statements using both

variable costing and absorption costing

There are number of methods, which are used in management accounting. Since the main

aim of management accounting is to help management in making rational, appropriate and the

most logical decisions. With this regard, some key methods of management accounting are as-

Capital budgeting analysis-

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

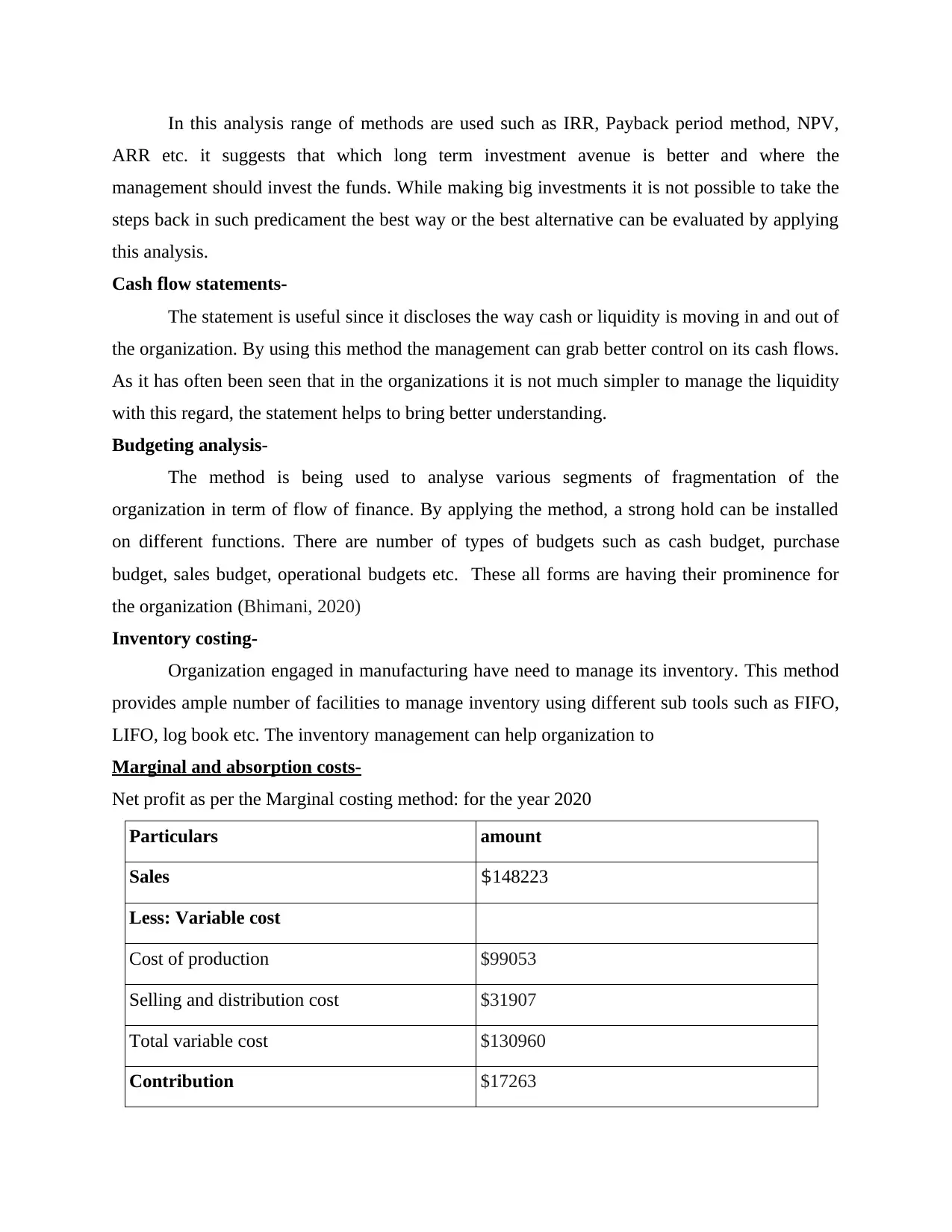

In this analysis range of methods are used such as IRR, Payback period method, NPV,

ARR etc. it suggests that which long term investment avenue is better and where the

management should invest the funds. While making big investments it is not possible to take the

steps back in such predicament the best way or the best alternative can be evaluated by applying

this analysis.

Cash flow statements-

The statement is useful since it discloses the way cash or liquidity is moving in and out of

the organization. By using this method the management can grab better control on its cash flows.

As it has often been seen that in the organizations it is not much simpler to manage the liquidity

with this regard, the statement helps to bring better understanding.

Budgeting analysis-

The method is being used to analyse various segments of fragmentation of the

organization in term of flow of finance. By applying the method, a strong hold can be installed

on different functions. There are number of types of budgets such as cash budget, purchase

budget, sales budget, operational budgets etc. These all forms are having their prominence for

the organization (Bhimani, 2020)

Inventory costing-

Organization engaged in manufacturing have need to manage its inventory. This method

provides ample number of facilities to manage inventory using different sub tools such as FIFO,

LIFO, log book etc. The inventory management can help organization to

Marginal and absorption costs-

Net profit as per the Marginal costing method: for the year 2020

Particulars amount

Sales $148223

Less: Variable cost

Cost of production $99053

Selling and distribution cost $31907

Total variable cost $130960

Contribution $17263

ARR etc. it suggests that which long term investment avenue is better and where the

management should invest the funds. While making big investments it is not possible to take the

steps back in such predicament the best way or the best alternative can be evaluated by applying

this analysis.

Cash flow statements-

The statement is useful since it discloses the way cash or liquidity is moving in and out of

the organization. By using this method the management can grab better control on its cash flows.

As it has often been seen that in the organizations it is not much simpler to manage the liquidity

with this regard, the statement helps to bring better understanding.

Budgeting analysis-

The method is being used to analyse various segments of fragmentation of the

organization in term of flow of finance. By applying the method, a strong hold can be installed

on different functions. There are number of types of budgets such as cash budget, purchase

budget, sales budget, operational budgets etc. These all forms are having their prominence for

the organization (Bhimani, 2020)

Inventory costing-

Organization engaged in manufacturing have need to manage its inventory. This method

provides ample number of facilities to manage inventory using different sub tools such as FIFO,

LIFO, log book etc. The inventory management can help organization to

Marginal and absorption costs-

Net profit as per the Marginal costing method: for the year 2020

Particulars amount

Sales $148223

Less: Variable cost

Cost of production $99053

Selling and distribution cost $31907

Total variable cost $130960

Contribution $17263

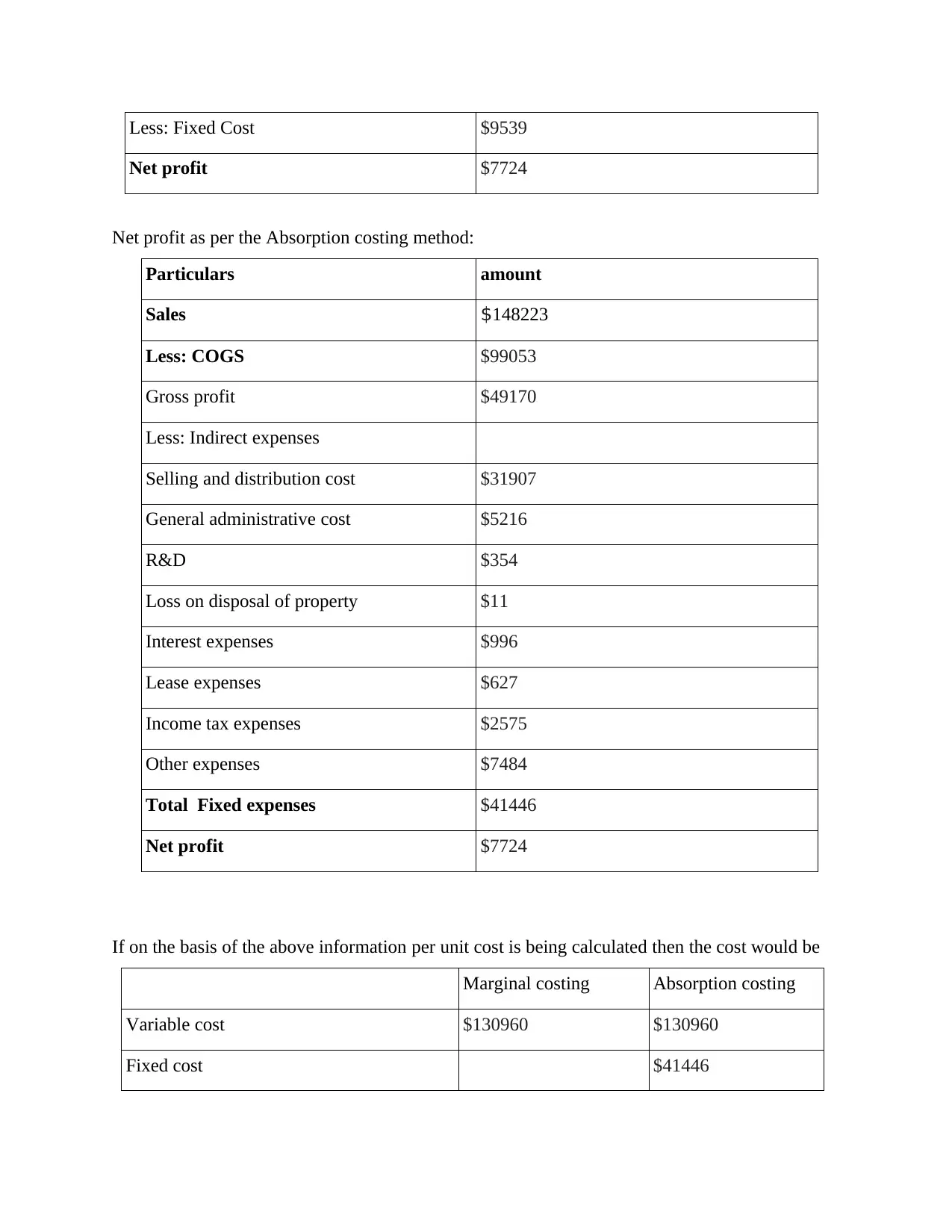

Less: Fixed Cost $9539

Net profit $7724

Net profit as per the Absorption costing method:

Particulars amount

Sales $148223

Less: COGS $99053

Gross profit $49170

Less: Indirect expenses

Selling and distribution cost $31907

General administrative cost $5216

R&D $354

Loss on disposal of property $11

Interest expenses $996

Lease expenses $627

Income tax expenses $2575

Other expenses $7484

Total Fixed expenses $41446

Net profit $7724

If on the basis of the above information per unit cost is being calculated then the cost would be

Marginal costing Absorption costing

Variable cost $130960 $130960

Fixed cost $41446

Net profit $7724

Net profit as per the Absorption costing method:

Particulars amount

Sales $148223

Less: COGS $99053

Gross profit $49170

Less: Indirect expenses

Selling and distribution cost $31907

General administrative cost $5216

R&D $354

Loss on disposal of property $11

Interest expenses $996

Lease expenses $627

Income tax expenses $2575

Other expenses $7484

Total Fixed expenses $41446

Net profit $7724

If on the basis of the above information per unit cost is being calculated then the cost would be

Marginal costing Absorption costing

Variable cost $130960 $130960

Fixed cost $41446

Products cost $130960 $172406

From the above statements it can be deciphered that by applying these methods the

valuation would be quite different since the marginal cost just consider variable costs but on the

other hands for valuation of units, the absorption costing uses both variable and fixed costs.

Firstly marginal costing method has been used in order to prepare net income statement,

it shows only variable costs when it comes to unit cost calculation at the same time the

absorption costing method uses both variable and fixed costs in order to charge them against

units produced (Eldenburg, 2020)

This difference in these costing methods are having their great influence on the final

outcomes and brings greater impact on cost management factors. If there is inventory then the

valuation of inventory would be differing due to the difference these both methods have. The

cost of products is $130960 if the variable costing method is being applied at the same time if the

absorption costing is used then the product costs would be $172406 so the difference between

these costs would also impact the valuation.

4. Management accounting within the organization

The Hammond Electronics is engaged in manufacturing work and the organization is

supposed to make decisions in order to be remained profitable and competitive in the market.

The organization is producing range of items such as diecast enclosures, Plastic

enclosures, General purpose metal, Chassis, Industrial enclosures etc. The market of electronics

in the nation is well expanded and it is supposed to work with better inclination.

With the progress of time the organization is making great progress and its market size is

also getting expanded. For being competitive and leader of the product line in the market the sole

way is installation of strong management accounting practise, that's how it becomes integrated

part of the business.

The organization is active form the year 1934 and in this duration it has made great

progress with appropriate decision making. It faced range of circumstances but strong regimes

and managerial advancement has eradicated all perils (Ilkhom, 2022)

Earlier it did not have need to keep such accounting system since the conventional

methods used to be practised to make decisions but in the modern age market dynamics are

prevailing with greater influence.

From the above statements it can be deciphered that by applying these methods the

valuation would be quite different since the marginal cost just consider variable costs but on the

other hands for valuation of units, the absorption costing uses both variable and fixed costs.

Firstly marginal costing method has been used in order to prepare net income statement,

it shows only variable costs when it comes to unit cost calculation at the same time the

absorption costing method uses both variable and fixed costs in order to charge them against

units produced (Eldenburg, 2020)

This difference in these costing methods are having their great influence on the final

outcomes and brings greater impact on cost management factors. If there is inventory then the

valuation of inventory would be differing due to the difference these both methods have. The

cost of products is $130960 if the variable costing method is being applied at the same time if the

absorption costing is used then the product costs would be $172406 so the difference between

these costs would also impact the valuation.

4. Management accounting within the organization

The Hammond Electronics is engaged in manufacturing work and the organization is

supposed to make decisions in order to be remained profitable and competitive in the market.

The organization is producing range of items such as diecast enclosures, Plastic

enclosures, General purpose metal, Chassis, Industrial enclosures etc. The market of electronics

in the nation is well expanded and it is supposed to work with better inclination.

With the progress of time the organization is making great progress and its market size is

also getting expanded. For being competitive and leader of the product line in the market the sole

way is installation of strong management accounting practise, that's how it becomes integrated

part of the business.

The organization is active form the year 1934 and in this duration it has made great

progress with appropriate decision making. It faced range of circumstances but strong regimes

and managerial advancement has eradicated all perils (Ilkhom, 2022)

Earlier it did not have need to keep such accounting system since the conventional

methods used to be practised to make decisions but in the modern age market dynamics are

prevailing with greater influence.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

So keeping the above shared notions in mind it would be fair enough to articulate that

management accounting is integrated within the organization.

5. Benefits of the function to the organization

Management accounts department performs those all functions which are inevitable in the

present market circumstances. Earlier the market was not that much drastic but with the progress

of time it became highly unpredicted and the competition level is also getting up.

If the department is working with greater efficiency then it paves the way for more

feasible planning. The organization can fabricate better plans favouring organizational

success.

The business operations can be controlled with the help of management accounts. It drops

the possibility to be in fuzzy direction and can let the organization know prevailing

loopholes.

The financial data which is provided by the department can help to manage the funds and

liquidity in appropriate manner.

It is oftne seen that the organizations which are very much successful are having good

control on range of notions such as their liquidity, finance, resources etc. The best part of

management accounting is that it brings these all superiority in favour of the

organization.

In the present market dynamics, having a long visionary strategy is quite essential so can

be remained profitable in longer run, with this regard, it makes the task simpler to install

strategic management.

Business is engaged in manufacturing work so the department can help them to trace and

point out the areas with shortcomings and can take immediate actions to cope up with

them (Sakun, Prystemskyi and Kartashova, 2021)

Management accounting covers up some key areas, such as long term investments. If the

organization is striving to invest for longer then by using capital budgeting tool it can

choose the best alternative out of the given.

So it can be summarized that the management accounting function is very much needed for the

growth and better operations of an organization.

management accounting is integrated within the organization.

5. Benefits of the function to the organization

Management accounts department performs those all functions which are inevitable in the

present market circumstances. Earlier the market was not that much drastic but with the progress

of time it became highly unpredicted and the competition level is also getting up.

If the department is working with greater efficiency then it paves the way for more

feasible planning. The organization can fabricate better plans favouring organizational

success.

The business operations can be controlled with the help of management accounts. It drops

the possibility to be in fuzzy direction and can let the organization know prevailing

loopholes.

The financial data which is provided by the department can help to manage the funds and

liquidity in appropriate manner.

It is oftne seen that the organizations which are very much successful are having good

control on range of notions such as their liquidity, finance, resources etc. The best part of

management accounting is that it brings these all superiority in favour of the

organization.

In the present market dynamics, having a long visionary strategy is quite essential so can

be remained profitable in longer run, with this regard, it makes the task simpler to install

strategic management.

Business is engaged in manufacturing work so the department can help them to trace and

point out the areas with shortcomings and can take immediate actions to cope up with

them (Sakun, Prystemskyi and Kartashova, 2021)

Management accounting covers up some key areas, such as long term investments. If the

organization is striving to invest for longer then by using capital budgeting tool it can

choose the best alternative out of the given.

So it can be summarized that the management accounting function is very much needed for the

growth and better operations of an organization.

6. Conclusion on the reflection of application of management accounting

Form the evaluation above it can be concluded that the management accounting is the

practise which is no longer a luxury but is having its mammoth usefulness for the organization.

There are range of benefits it comes up with, but now the biggest advantage is driving

management in their decision making process.

At the same time it can be reflected that there are some issues or can be sited jeopardies

too with management accounting. Firstly it is very much expensive to install a management

accounting system in an organization.

If the company is a middle sized, then it may be highly expensive for them.

Organizations like Hammond Electronics, are still practising management accounting as a

luxury tool. Their most of the decisions are driven by the moves of driving forces and market

dynamics, so the role of management accounting do not remain same (Rikhardsson, and

Yigitbasioglu, 2018)

One of the biggest thing, that intensively affect the application of management

accounting. The entire management accounting is based on historical data, if the recorded data is

not absolute then the outcomes it drives would be improper and would lead to malfunctioning.

The institutive decision-making process may get dis-stabilized since it has been

experienced that some time the factual drivers do not lead to better decision making and it tosses

the need to use intuition but management accounting application may hinder that (Amir, and

Chaudhry, 2019)

So it can be concluded that management accounting is having some limitations yet it is

comprehensively lucrative.

PART 2

Explaining three planning tools in management accounting

Cash budget: A cash budget is termed as the estimation of the company's cash outflows

and inflows in the specific period of time. The cash budget of the company can be prepared

weekly, monthly, quarterly or annually. The company uses the cash budget must determine that

the company is having sufficient cash in order to operate in the market (Salamah and Susilo,

2020). Main purpose of making the cash budget is to forecast the cash balance that helps the

company to identify the deficits and surpluses. Cash budget is basically the document that helps

the business to manage the cash flow in the company. By making the cash budget it makes the

Form the evaluation above it can be concluded that the management accounting is the

practise which is no longer a luxury but is having its mammoth usefulness for the organization.

There are range of benefits it comes up with, but now the biggest advantage is driving

management in their decision making process.

At the same time it can be reflected that there are some issues or can be sited jeopardies

too with management accounting. Firstly it is very much expensive to install a management

accounting system in an organization.

If the company is a middle sized, then it may be highly expensive for them.

Organizations like Hammond Electronics, are still practising management accounting as a

luxury tool. Their most of the decisions are driven by the moves of driving forces and market

dynamics, so the role of management accounting do not remain same (Rikhardsson, and

Yigitbasioglu, 2018)

One of the biggest thing, that intensively affect the application of management

accounting. The entire management accounting is based on historical data, if the recorded data is

not absolute then the outcomes it drives would be improper and would lead to malfunctioning.

The institutive decision-making process may get dis-stabilized since it has been

experienced that some time the factual drivers do not lead to better decision making and it tosses

the need to use intuition but management accounting application may hinder that (Amir, and

Chaudhry, 2019)

So it can be concluded that management accounting is having some limitations yet it is

comprehensively lucrative.

PART 2

Explaining three planning tools in management accounting

Cash budget: A cash budget is termed as the estimation of the company's cash outflows

and inflows in the specific period of time. The cash budget of the company can be prepared

weekly, monthly, quarterly or annually. The company uses the cash budget must determine that

the company is having sufficient cash in order to operate in the market (Salamah and Susilo,

2020). Main purpose of making the cash budget is to forecast the cash balance that helps the

company to identify the deficits and surpluses. Cash budget is basically the document that helps

the business to manage the cash flow in the company. By making the cash budget it makes the

company to have proper estimation of the cash receipts, cash payments and the remaining cash

balances in the future.

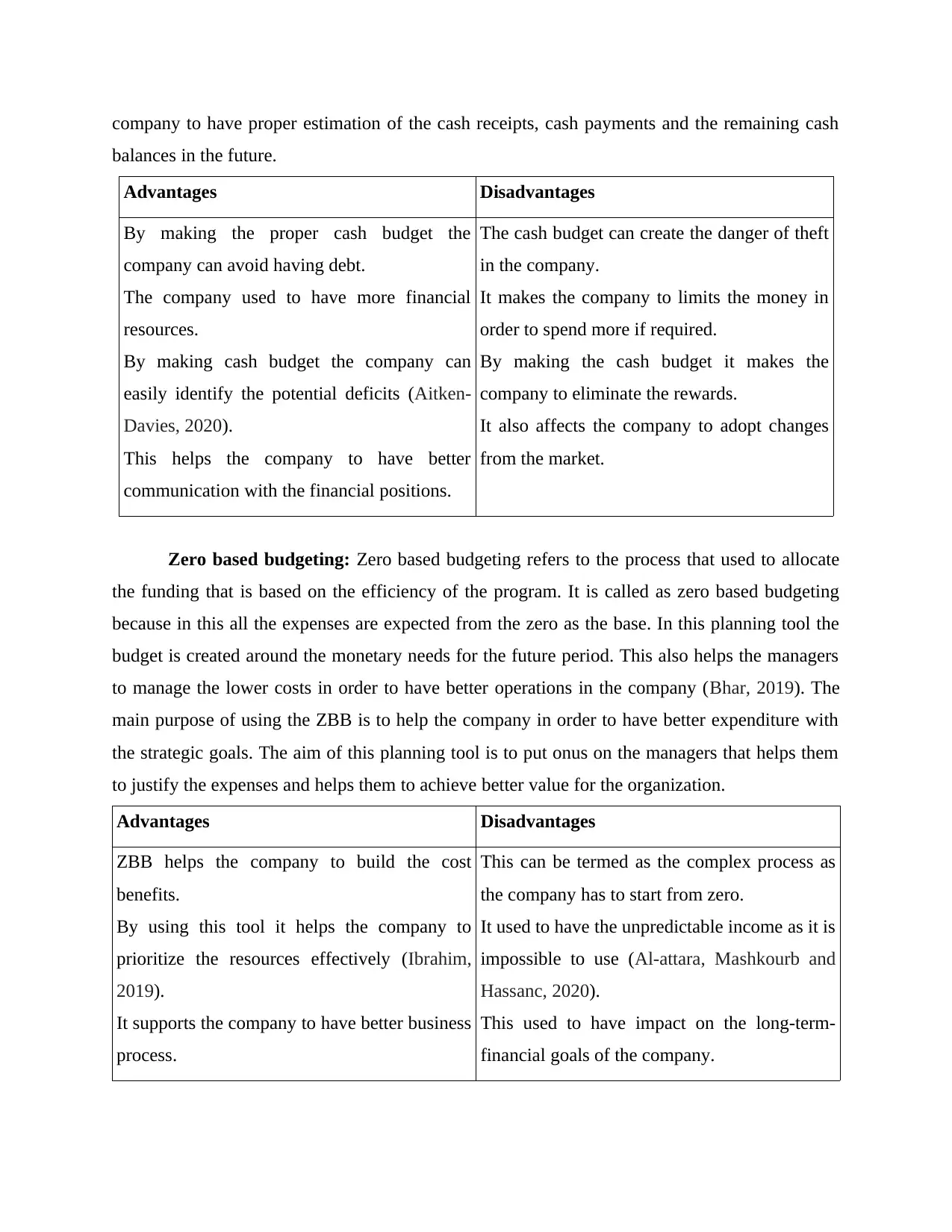

Advantages Disadvantages

By making the proper cash budget the

company can avoid having debt.

The company used to have more financial

resources.

By making cash budget the company can

easily identify the potential deficits (Aitken-

Davies, 2020).

This helps the company to have better

communication with the financial positions.

The cash budget can create the danger of theft

in the company.

It makes the company to limits the money in

order to spend more if required.

By making the cash budget it makes the

company to eliminate the rewards.

It also affects the company to adopt changes

from the market.

Zero based budgeting: Zero based budgeting refers to the process that used to allocate

the funding that is based on the efficiency of the program. It is called as zero based budgeting

because in this all the expenses are expected from the zero as the base. In this planning tool the

budget is created around the monetary needs for the future period. This also helps the managers

to manage the lower costs in order to have better operations in the company (Bhar, 2019). The

main purpose of using the ZBB is to help the company in order to have better expenditure with

the strategic goals. The aim of this planning tool is to put onus on the managers that helps them

to justify the expenses and helps them to achieve better value for the organization.

Advantages Disadvantages

ZBB helps the company to build the cost

benefits.

By using this tool it helps the company to

prioritize the resources effectively (Ibrahim,

2019).

It supports the company to have better business

process.

This can be termed as the complex process as

the company has to start from zero.

It used to have the unpredictable income as it is

impossible to use (Al-attara, Mashkourb and

Hassanc, 2020).

This used to have impact on the long-term-

financial goals of the company.

balances in the future.

Advantages Disadvantages

By making the proper cash budget the

company can avoid having debt.

The company used to have more financial

resources.

By making cash budget the company can

easily identify the potential deficits (Aitken-

Davies, 2020).

This helps the company to have better

communication with the financial positions.

The cash budget can create the danger of theft

in the company.

It makes the company to limits the money in

order to spend more if required.

By making the cash budget it makes the

company to eliminate the rewards.

It also affects the company to adopt changes

from the market.

Zero based budgeting: Zero based budgeting refers to the process that used to allocate

the funding that is based on the efficiency of the program. It is called as zero based budgeting

because in this all the expenses are expected from the zero as the base. In this planning tool the

budget is created around the monetary needs for the future period. This also helps the managers

to manage the lower costs in order to have better operations in the company (Bhar, 2019). The

main purpose of using the ZBB is to help the company in order to have better expenditure with

the strategic goals. The aim of this planning tool is to put onus on the managers that helps them

to justify the expenses and helps them to achieve better value for the organization.

Advantages Disadvantages

ZBB helps the company to build the cost

benefits.

By using this tool it helps the company to

prioritize the resources effectively (Ibrahim,

2019).

It supports the company to have better business

process.

This can be termed as the complex process as

the company has to start from zero.

It used to have the unpredictable income as it is

impossible to use (Al-attara, Mashkourb and

Hassanc, 2020).

This used to have impact on the long-term-

financial goals of the company.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Activity based budgeting: This is the method of budgeting the activities that used to

incur the costs that are recorded, analysed and researched. It is considered as the hard and

complex process as this used to depend upon the previous budgets of the company. This method

is basically used in order to predict the future costs of the company in order to have better

planning (Maulana and Asmeri, 2020). It is the management accounting tool that helps the

company to make the new budget without considering the previous years profit. This used to

bring out the efficiency to have the proper allocation of the activities in the organization.

Advantages Disadvantages

By having good ABB this helps the company

to have better competitive edge in the market.

This planning tools eliminates the bottlenecks

and have better research.

This improves the relationship between the

organization and its customers (Eisert and

et.al., 2020).

This is time- consuming process as no previous

years data is taken.

This process used to consume more resources

in the organization.

ABB only focuses on the short term goals of

the organization.

Comparing how organization adapt the management accounting system to respond financial

problems

Benchmarking: Benchmarking refers to the process of measuring the key business

metrics and comparing them with the business or with the competitors. This helps the company

to understand what changes that the company must adopt in order to improve performance

(Mangul and et.al., 2019). By using this method it helps the company to have better response

with the financial problems. The advantages and disadvantages of Benchmarking is stated below:

Advantages Disadvantages

This used to improve the internal operations

of the company.

Reduces the costs of the company by

increasing the efficiency.

Adopt the better practices in order to perform

well.

This used to provide insufficient information to

the company.

This decreases the customer satisfaction in the

company.

Using this method it increases the dependency.

incur the costs that are recorded, analysed and researched. It is considered as the hard and

complex process as this used to depend upon the previous budgets of the company. This method

is basically used in order to predict the future costs of the company in order to have better

planning (Maulana and Asmeri, 2020). It is the management accounting tool that helps the

company to make the new budget without considering the previous years profit. This used to

bring out the efficiency to have the proper allocation of the activities in the organization.

Advantages Disadvantages

By having good ABB this helps the company

to have better competitive edge in the market.

This planning tools eliminates the bottlenecks

and have better research.

This improves the relationship between the

organization and its customers (Eisert and

et.al., 2020).

This is time- consuming process as no previous

years data is taken.

This process used to consume more resources

in the organization.

ABB only focuses on the short term goals of

the organization.

Comparing how organization adapt the management accounting system to respond financial

problems

Benchmarking: Benchmarking refers to the process of measuring the key business

metrics and comparing them with the business or with the competitors. This helps the company

to understand what changes that the company must adopt in order to improve performance

(Mangul and et.al., 2019). By using this method it helps the company to have better response

with the financial problems. The advantages and disadvantages of Benchmarking is stated below:

Advantages Disadvantages

This used to improve the internal operations

of the company.

Reduces the costs of the company by

increasing the efficiency.

Adopt the better practices in order to perform

well.

This used to provide insufficient information to

the company.

This decreases the customer satisfaction in the

company.

Using this method it increases the dependency.

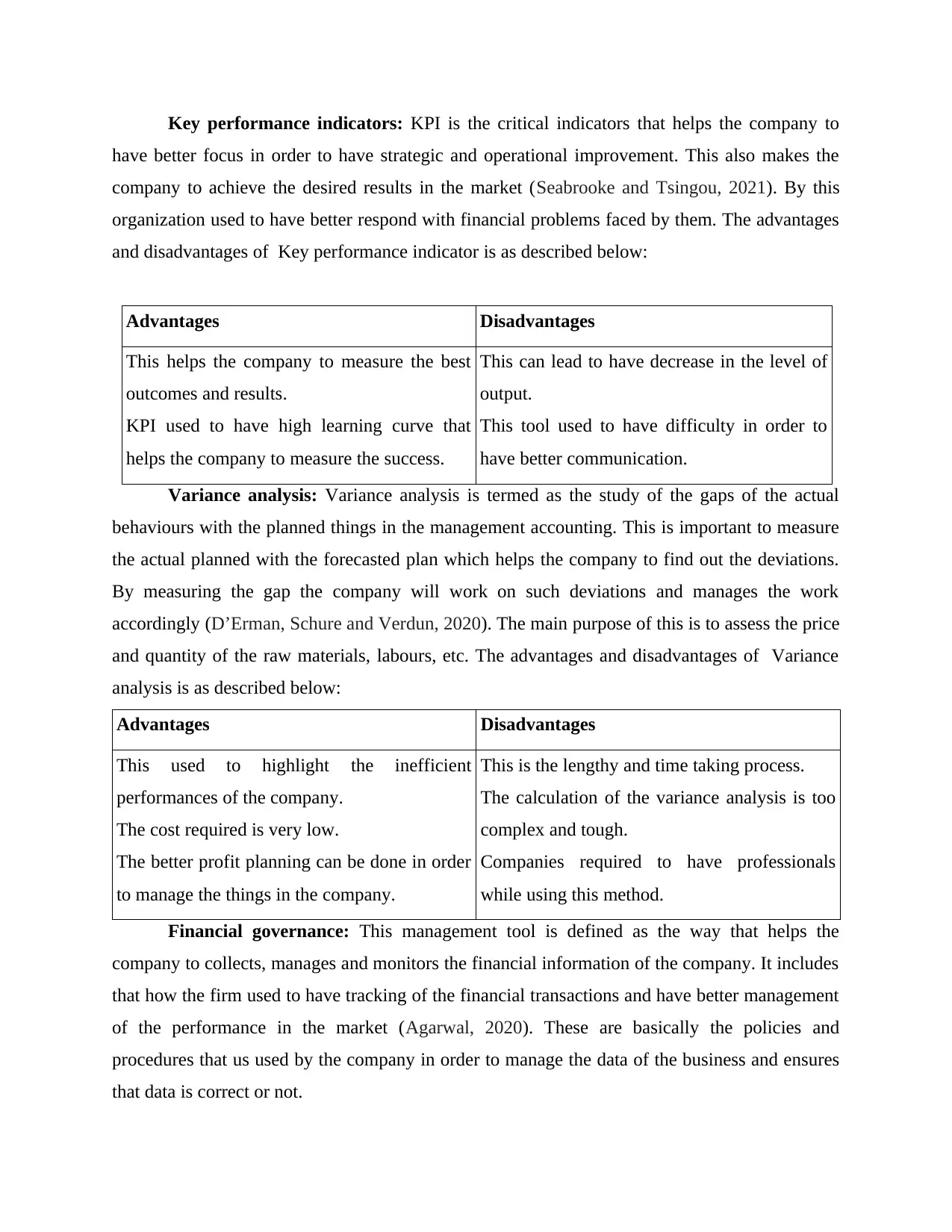

Key performance indicators: KPI is the critical indicators that helps the company to

have better focus in order to have strategic and operational improvement. This also makes the

company to achieve the desired results in the market (Seabrooke and Tsingou, 2021). By this

organization used to have better respond with financial problems faced by them. The advantages

and disadvantages of Key performance indicator is as described below:

Advantages Disadvantages

This helps the company to measure the best

outcomes and results.

KPI used to have high learning curve that

helps the company to measure the success.

This can lead to have decrease in the level of

output.

This tool used to have difficulty in order to

have better communication.

Variance analysis: Variance analysis is termed as the study of the gaps of the actual

behaviours with the planned things in the management accounting. This is important to measure

the actual planned with the forecasted plan which helps the company to find out the deviations.

By measuring the gap the company will work on such deviations and manages the work

accordingly (D’Erman, Schure and Verdun, 2020). The main purpose of this is to assess the price

and quantity of the raw materials, labours, etc. The advantages and disadvantages of Variance

analysis is as described below:

Advantages Disadvantages

This used to highlight the inefficient

performances of the company.

The cost required is very low.

The better profit planning can be done in order

to manage the things in the company.

This is the lengthy and time taking process.

The calculation of the variance analysis is too

complex and tough.

Companies required to have professionals

while using this method.

Financial governance: This management tool is defined as the way that helps the

company to collects, manages and monitors the financial information of the company. It includes

that how the firm used to have tracking of the financial transactions and have better management

of the performance in the market (Agarwal, 2020). These are basically the policies and

procedures that us used by the company in order to manage the data of the business and ensures

that data is correct or not.

have better focus in order to have strategic and operational improvement. This also makes the

company to achieve the desired results in the market (Seabrooke and Tsingou, 2021). By this

organization used to have better respond with financial problems faced by them. The advantages

and disadvantages of Key performance indicator is as described below:

Advantages Disadvantages

This helps the company to measure the best

outcomes and results.

KPI used to have high learning curve that

helps the company to measure the success.

This can lead to have decrease in the level of

output.

This tool used to have difficulty in order to

have better communication.

Variance analysis: Variance analysis is termed as the study of the gaps of the actual

behaviours with the planned things in the management accounting. This is important to measure

the actual planned with the forecasted plan which helps the company to find out the deviations.

By measuring the gap the company will work on such deviations and manages the work

accordingly (D’Erman, Schure and Verdun, 2020). The main purpose of this is to assess the price

and quantity of the raw materials, labours, etc. The advantages and disadvantages of Variance

analysis is as described below:

Advantages Disadvantages

This used to highlight the inefficient

performances of the company.

The cost required is very low.

The better profit planning can be done in order

to manage the things in the company.

This is the lengthy and time taking process.

The calculation of the variance analysis is too

complex and tough.

Companies required to have professionals

while using this method.

Financial governance: This management tool is defined as the way that helps the

company to collects, manages and monitors the financial information of the company. It includes

that how the firm used to have tracking of the financial transactions and have better management

of the performance in the market (Agarwal, 2020). These are basically the policies and

procedures that us used by the company in order to manage the data of the business and ensures

that data is correct or not.

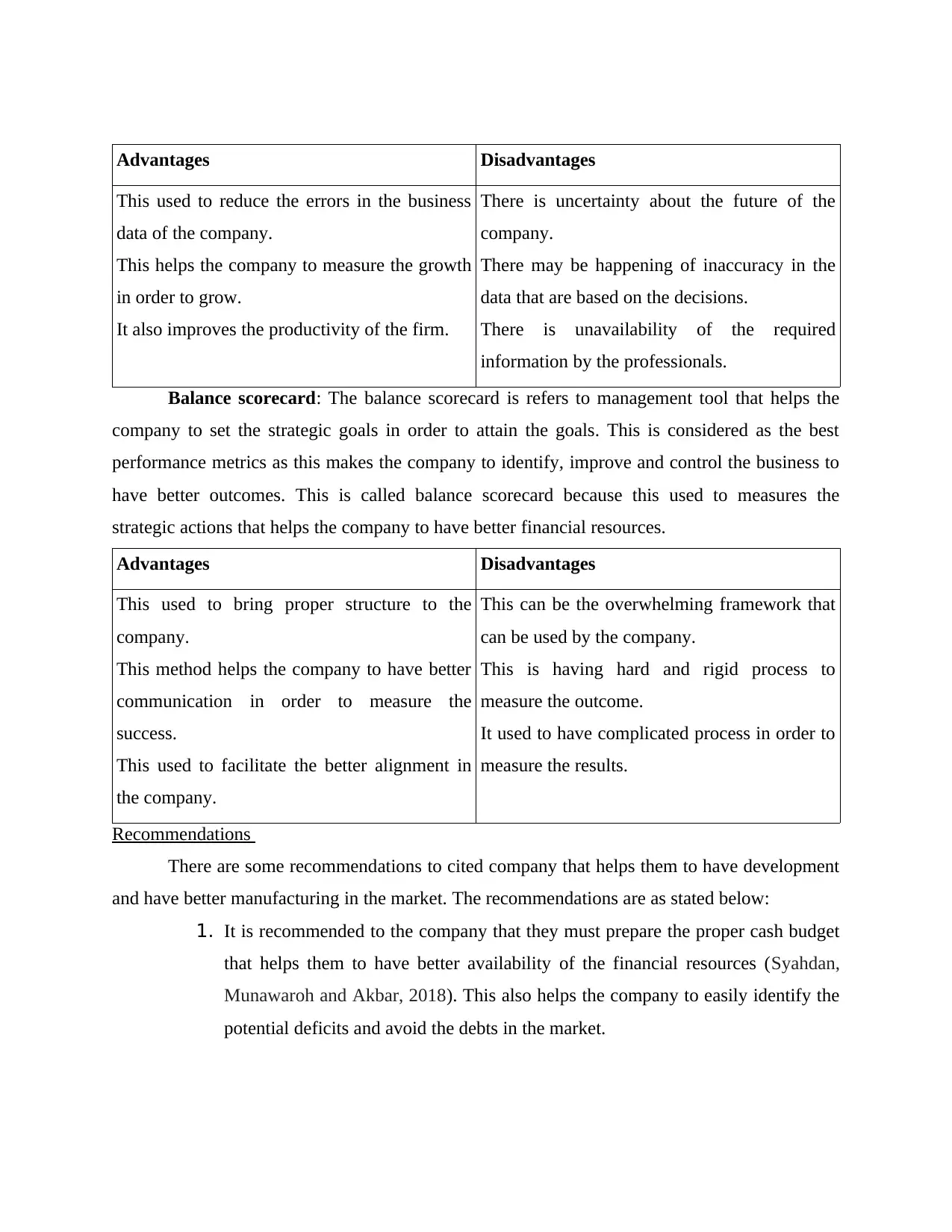

Advantages Disadvantages

This used to reduce the errors in the business

data of the company.

This helps the company to measure the growth

in order to grow.

It also improves the productivity of the firm.

There is uncertainty about the future of the

company.

There may be happening of inaccuracy in the

data that are based on the decisions.

There is unavailability of the required

information by the professionals.

Balance scorecard: The balance scorecard is refers to management tool that helps the

company to set the strategic goals in order to attain the goals. This is considered as the best

performance metrics as this makes the company to identify, improve and control the business to

have better outcomes. This is called balance scorecard because this used to measures the

strategic actions that helps the company to have better financial resources.

Advantages Disadvantages

This used to bring proper structure to the

company.

This method helps the company to have better

communication in order to measure the

success.

This used to facilitate the better alignment in

the company.

This can be the overwhelming framework that

can be used by the company.

This is having hard and rigid process to

measure the outcome.

It used to have complicated process in order to

measure the results.

Recommendations

There are some recommendations to cited company that helps them to have development

and have better manufacturing in the market. The recommendations are as stated below:

1. It is recommended to the company that they must prepare the proper cash budget

that helps them to have better availability of the financial resources (Syahdan,

Munawaroh and Akbar, 2018). This also helps the company to easily identify the

potential deficits and avoid the debts in the market.

This used to reduce the errors in the business

data of the company.

This helps the company to measure the growth

in order to grow.

It also improves the productivity of the firm.

There is uncertainty about the future of the

company.

There may be happening of inaccuracy in the

data that are based on the decisions.

There is unavailability of the required

information by the professionals.

Balance scorecard: The balance scorecard is refers to management tool that helps the

company to set the strategic goals in order to attain the goals. This is considered as the best

performance metrics as this makes the company to identify, improve and control the business to

have better outcomes. This is called balance scorecard because this used to measures the

strategic actions that helps the company to have better financial resources.

Advantages Disadvantages

This used to bring proper structure to the

company.

This method helps the company to have better

communication in order to measure the

success.

This used to facilitate the better alignment in

the company.

This can be the overwhelming framework that

can be used by the company.

This is having hard and rigid process to

measure the outcome.

It used to have complicated process in order to

measure the results.

Recommendations

There are some recommendations to cited company that helps them to have development

and have better manufacturing in the market. The recommendations are as stated below:

1. It is recommended to the company that they must prepare the proper cash budget

that helps them to have better availability of the financial resources (Syahdan,

Munawaroh and Akbar, 2018). This also helps the company to easily identify the

potential deficits and avoid the debts in the market.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Further it is also suggested to the company that they can use the variance analysis

in order to measure the success and have better respond to financial systems. This

helps the company to know about the actual outcome with the planned behaviour.

CONCLUSION

From the above report it is concluded about the management accounting done by the

company in order to have better records. The report has evaluated about the different accounting

systems that includes cost accounting system, job costing system, inventory management system,

etc. Further this report has described about the different methods that is used in management

accounting report included cost report, inventory report, budget report etc. Moreover, the above

report has calculated the cost of the company by preparing income statement. This report has

further evaluated about the advantages and disadvantages of the different planning tools that are

used in budgetary control. Furthermore, this report has indicated about the management

accounting systems that helps the company to have better respond to the financial problems. At

last there some recommendations to the company that helps increases the profitability and have

development in the UK market.

in order to measure the success and have better respond to financial systems. This

helps the company to know about the actual outcome with the planned behaviour.

CONCLUSION

From the above report it is concluded about the management accounting done by the

company in order to have better records. The report has evaluated about the different accounting

systems that includes cost accounting system, job costing system, inventory management system,

etc. Further this report has described about the different methods that is used in management

accounting report included cost report, inventory report, budget report etc. Moreover, the above

report has calculated the cost of the company by preparing income statement. This report has

further evaluated about the advantages and disadvantages of the different planning tools that are

used in budgetary control. Furthermore, this report has indicated about the management

accounting systems that helps the company to have better respond to the financial problems. At

last there some recommendations to the company that helps increases the profitability and have

development in the UK market.

REFERENCES

Books and journals

Agarwal, A., 2020. Investigating design targets for effective performance management system:

an application of balance scorecard using QFD. Journal of Advances in Management

Research.

Aitken-Davies, R., 2020. The Cash Forecast. In Handbook of Financial Planning and

Control (pp. 101-108). Routledge.

Al-attara, H. A., Mashkourb, S. C. and Hassanc, M. G., 2020. Zero-based budget system and its

active role in choosing the best alternative to rationalise government

spending. International Journal of Innovation, Creativity and Change. 13(9). pp.244-

265.

Bhar, A. K., 2019. Design & implementation of a personal Cash flow program using Microsoft

Excel. Global Journal of Business, Economics and Management: Current Issues. 9(1).

pp.29-40.

D’Erman, V., Schure, P. and Verdun, A., 2020. Introduction to “Economic and Financial

Governance in the European Union after a decade of Economic and Political

Crises.”. Journal of Economic Policy Reform. 23(3). pp.267-272.

Eisert, J. and et.al., 2020. Quantum certification and benchmarking. Nature Reviews Physics.

2(7). pp.382-390.

Ibrahim, M. M., 2019. Designing zero-based budgeting for public organizations. Problems and

Perspectives in Management. 17(2).

Mangul, S. and et.al., 2019. Systematic benchmarking of omics computational tools. Nature

communications. 10(1). pp.1-11.

Maulana, M. R. and Asmeri, R., 2020. Analisis Pengaruh Penerapan Activity Based Budgeting

Terhadap Anggaran Belanja Dinas Perkebunan Kabupaten Tebo. Pareso Jurnal. 2(3).

pp.111-122.

Salamah, L. and Susilo, G. F. A., 2020. Analysis of Implementation in Cash Budgeting to

Facilities and Setting of the Residential Area in Public Housing Department (DPRKP)

of Magelang District. Journal of Contemporary Information Technology, Management,

and Accounting. 1(2). pp.80-89.

Seabrooke, L. and Tsingou, E., 2021. Revolving doors in international financial

governance. Global Networks. 21(2). pp.294-319.

Syahdan, S.A., Munawaroh, R.S. and Akbar, M., 2018. Balance Scorecard Implementation in

Public Sector Organization, A Problem?. International Journal of Accounting, Finance,

and Economics. 1(1). pp.1-6.

Johnstone, L., 2020. A systematic analysis of environmental management systems in SMEs:

Possible research directions from a management accounting and control stance. Journal

of Cleaner Production. 244. p.118802.

Pelz, M., 2019. Can management accounting be helpful for young and small companies?

Systematic review of a paradox. International Journal of Management Reviews. 21(2).

pp.256-274.

Hiromoto, T., 2019. Restoring the relevance of management accounting. In Management

Control Theory (pp. 273-288). Routledge.

Bhimani, A., 2020. Digital data and management accounting: why we need to rethink research

methods. Journal of Management Control. 31(1). pp.9-23.

1

Books and journals

Agarwal, A., 2020. Investigating design targets for effective performance management system:

an application of balance scorecard using QFD. Journal of Advances in Management

Research.

Aitken-Davies, R., 2020. The Cash Forecast. In Handbook of Financial Planning and

Control (pp. 101-108). Routledge.

Al-attara, H. A., Mashkourb, S. C. and Hassanc, M. G., 2020. Zero-based budget system and its

active role in choosing the best alternative to rationalise government

spending. International Journal of Innovation, Creativity and Change. 13(9). pp.244-

265.

Bhar, A. K., 2019. Design & implementation of a personal Cash flow program using Microsoft

Excel. Global Journal of Business, Economics and Management: Current Issues. 9(1).

pp.29-40.

D’Erman, V., Schure, P. and Verdun, A., 2020. Introduction to “Economic and Financial

Governance in the European Union after a decade of Economic and Political

Crises.”. Journal of Economic Policy Reform. 23(3). pp.267-272.

Eisert, J. and et.al., 2020. Quantum certification and benchmarking. Nature Reviews Physics.

2(7). pp.382-390.

Ibrahim, M. M., 2019. Designing zero-based budgeting for public organizations. Problems and

Perspectives in Management. 17(2).

Mangul, S. and et.al., 2019. Systematic benchmarking of omics computational tools. Nature

communications. 10(1). pp.1-11.

Maulana, M. R. and Asmeri, R., 2020. Analisis Pengaruh Penerapan Activity Based Budgeting

Terhadap Anggaran Belanja Dinas Perkebunan Kabupaten Tebo. Pareso Jurnal. 2(3).

pp.111-122.

Salamah, L. and Susilo, G. F. A., 2020. Analysis of Implementation in Cash Budgeting to

Facilities and Setting of the Residential Area in Public Housing Department (DPRKP)

of Magelang District. Journal of Contemporary Information Technology, Management,

and Accounting. 1(2). pp.80-89.

Seabrooke, L. and Tsingou, E., 2021. Revolving doors in international financial

governance. Global Networks. 21(2). pp.294-319.

Syahdan, S.A., Munawaroh, R.S. and Akbar, M., 2018. Balance Scorecard Implementation in

Public Sector Organization, A Problem?. International Journal of Accounting, Finance,

and Economics. 1(1). pp.1-6.

Johnstone, L., 2020. A systematic analysis of environmental management systems in SMEs:

Possible research directions from a management accounting and control stance. Journal

of Cleaner Production. 244. p.118802.

Pelz, M., 2019. Can management accounting be helpful for young and small companies?

Systematic review of a paradox. International Journal of Management Reviews. 21(2).

pp.256-274.

Hiromoto, T., 2019. Restoring the relevance of management accounting. In Management

Control Theory (pp. 273-288). Routledge.

Bhimani, A., 2020. Digital data and management accounting: why we need to rethink research

methods. Journal of Management Control. 31(1). pp.9-23.

1

Eldenburg, L. G., 2020. Management accounting. John Wiley & Sons.

Ilkhom, G., 2022. MANAGEMENT ACCOUNTING AT ROAD TRANSPORT

ENTERPRISES AND ISSUES OF ITS IMPROVEMENT. Бюллетень науки и

практики. 8(3). pp.311-316.

Sakun, A. Z., Prystemskyi, O. and Kartashova, O., 2021. Innovative paradigm of management

accounting and development of controlling in the entrepreneurship.

Rikhardsson, P. and Yigitbasioglu, O., 2018. Business intelligence & analytics in management

accounting research: Status and future focus. International Journal of Accounting

Information Systems. 29. pp.37-58.

Amir, M. and Chaudhry, N. I., 2019. Linking environmental strategy to firm performance: A

sequential mediation model via environmental management accounting and top

management commitment. Pakistan Journal of Commerce and Social Sciences

(PJCSS). 13(4). pp.849-867.

<https://www.hammfg.com/files/news/2021/2021-03-08-annual-report-2020.pdf>

2

Ilkhom, G., 2022. MANAGEMENT ACCOUNTING AT ROAD TRANSPORT

ENTERPRISES AND ISSUES OF ITS IMPROVEMENT. Бюллетень науки и

практики. 8(3). pp.311-316.

Sakun, A. Z., Prystemskyi, O. and Kartashova, O., 2021. Innovative paradigm of management

accounting and development of controlling in the entrepreneurship.

Rikhardsson, P. and Yigitbasioglu, O., 2018. Business intelligence & analytics in management

accounting research: Status and future focus. International Journal of Accounting

Information Systems. 29. pp.37-58.

Amir, M. and Chaudhry, N. I., 2019. Linking environmental strategy to firm performance: A

sequential mediation model via environmental management accounting and top

management commitment. Pakistan Journal of Commerce and Social Sciences

(PJCSS). 13(4). pp.849-867.

<https://www.hammfg.com/files/news/2021/2021-03-08-annual-report-2020.pdf>

2

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.