Financial Analysis of Management Accounting Report and Techniques

VerifiedAdded on 2021/02/19

|27

|7693

|20

Report

AI Summary

This report provides a comprehensive overview of management accounting, encompassing various aspects such as cost accounting systems, price optimization, job costing, and inventory management. It delves into different types of accounting reports, including performance reports, budget reports, and accounts receivable aging reports, and explores the purpose of these reports in aiding organizational decision-making. The report further examines appropriate cost analysis techniques for preparing income statements, emphasizing the importance of relevant and accurate information. Additionally, it discusses the advantages and disadvantages of planning tools used for budgetary control and analyzes how organizations adapt management accounting systems to address financial challenges, drawing comparisons between different companies. The report concludes by highlighting measures to overcome financial issues, providing a well-rounded perspective on the significance and application of management accounting principles.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and its different types of system...................................................1

P2. Explain different method of management accounting reporting.........................................3

TASK 2............................................................................................................................................4

P3 .Appropriate techniques of cost analysis to prepare an income statement.................................4

TASK 3............................................................................................................................................6

P4. Advantages and disadvantages of different types of planning tools used for budgetary

control.........................................................................................................................................6

TASK 4............................................................................................................................................8

P5. Organisations are adapting management accounting systems to respond to financial

problems......................................................................................................................................8

CONCLUSION .............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and its different types of system...................................................1

P2. Explain different method of management accounting reporting.........................................3

TASK 2............................................................................................................................................4

P3 .Appropriate techniques of cost analysis to prepare an income statement.................................4

TASK 3............................................................................................................................................6

P4. Advantages and disadvantages of different types of planning tools used for budgetary

control.........................................................................................................................................6

TASK 4............................................................................................................................................8

P5. Organisations are adapting management accounting systems to respond to financial

problems......................................................................................................................................8

CONCLUSION .............................................................................................................................10

REFERENCES..............................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is also termed as an managerial accounting. In this form of

accounting system there are different types of accounts and reports that are required by managers

to conduct their daily basis operations along with making short term decisions. In simple terms,

this system is mainly related with proper monitoring, interpreting and analysing financial data in

well effective manner to frame internal decisions in best effective manner (Adler, 2013).

Management accounting include information in the form of non-financial and financial form.

This acts as an key essential element in an organisation with the help of which financial

transactions can be conducted in well effective manner. In this project formative discussions has

been made on, concept of management accounting along with its benefits. In addition with this

various form of managerial reports in addition with accounting techniques and advantages and

disadvantages are included in this report. Furthermore, to justify different techniques used by

organisations to deal with financial issues, a comparison is made between Capricorn Wealth

Management Brightstar and Financial Limited Company of UK. Lastly, different measures with

the help of which financial issues can be overcome are also included in this report.

TASK 1

P1. Management accounting and its different types of system

Management Accounting:

Management accounting term include combination of two elements management and

accounting. It is mainly a type of accounting system which is mainly linked with business

organisation internal part. With the help of this, managerial decisions can be effectively framed

in best effective manner along with this managerial reports can be made that will directly help in

framing plans and policies. Organisations are not bound to make managerial reports, it is all on

their will to frame that or not. Moreover, this accounting system have their own importance in an

organisation internal framework. Mentioned below there are different types of accounting sytsem

which is described below in descriptive manner.

Cost Accounting System:

This system is one of the crucial element in management accounting structure as this

effectively helps in evaluating cost of products that include, variable and fixed cost etc. in order

to effectively conduct business operations it is essential for an organisation to have proper

1

Management accounting is also termed as an managerial accounting. In this form of

accounting system there are different types of accounts and reports that are required by managers

to conduct their daily basis operations along with making short term decisions. In simple terms,

this system is mainly related with proper monitoring, interpreting and analysing financial data in

well effective manner to frame internal decisions in best effective manner (Adler, 2013).

Management accounting include information in the form of non-financial and financial form.

This acts as an key essential element in an organisation with the help of which financial

transactions can be conducted in well effective manner. In this project formative discussions has

been made on, concept of management accounting along with its benefits. In addition with this

various form of managerial reports in addition with accounting techniques and advantages and

disadvantages are included in this report. Furthermore, to justify different techniques used by

organisations to deal with financial issues, a comparison is made between Capricorn Wealth

Management Brightstar and Financial Limited Company of UK. Lastly, different measures with

the help of which financial issues can be overcome are also included in this report.

TASK 1

P1. Management accounting and its different types of system

Management Accounting:

Management accounting term include combination of two elements management and

accounting. It is mainly a type of accounting system which is mainly linked with business

organisation internal part. With the help of this, managerial decisions can be effectively framed

in best effective manner along with this managerial reports can be made that will directly help in

framing plans and policies. Organisations are not bound to make managerial reports, it is all on

their will to frame that or not. Moreover, this accounting system have their own importance in an

organisation internal framework. Mentioned below there are different types of accounting sytsem

which is described below in descriptive manner.

Cost Accounting System:

This system is one of the crucial element in management accounting structure as this

effectively helps in evaluating cost of products that include, variable and fixed cost etc. in order

to effectively conduct business operations it is essential for an organisation to have proper

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

estimation of their products and services cost as this will further aid in analysing and evaluating

products and loss ratio of a product and a service. Organisations by taking advantage of this

accounting system can effectively able to check and evaluate different type of cost related to

financial products and services. It further helps organisation to have proper check on their profit

and loss balance along with financial services and products this will benefit them to focus on

those products and services that will prove more beneficial for organisation.

Cost Accounting System must be practical, simple, tailor-made and capable of meeting

the necessitate of organisations in making more effective plans. The data or information to be

followed by the Cost Accounting System must be accurate or relevant; otherwise it may distort

the result of the system. Along with this, the system of costing must not sacrifice the utility by

presenting meticulous as well as unnecessary details. In this, Management of an organisation

must have a faith or belief in the Costing System and must also give a helping hand for its

improvement and success.

Price Optimisation System:

Price optimisation system acts as an key essential framework with the help of which

organisation can easily able to determine price of services and products which will prove suitable

for organisation as well as for organisation. This will further aid in evaluating consumers review

on different pricing level. Main aim or price optimisation system is to offer factors with the help

of which price can can be set in well effective manner. With the help of this form of accounting

system, companies can effectively set their price at numerous level which further aid in

providing benefits for company along with consumers. In order to set price, Mathematical

calculation is most essential and important which will help an organisation in managing its

transaction in systematic manner. Calculation introduces as an important act of calculating,

which is applying maths as well as logic to figure out a problem.

Job Costing System:

This system in tend towards, proper calculation of overall cost that occurs while offering

services and products in addition with after assignment of cost to every individual unit relating to

product and service. Job costing system effectively helps in those organisations that provide

different types of products and services (Ward, 2012). In order to offer numerous form of

products and services it become essential for organisations to effectively estimate every

2

products and loss ratio of a product and a service. Organisations by taking advantage of this

accounting system can effectively able to check and evaluate different type of cost related to

financial products and services. It further helps organisation to have proper check on their profit

and loss balance along with financial services and products this will benefit them to focus on

those products and services that will prove more beneficial for organisation.

Cost Accounting System must be practical, simple, tailor-made and capable of meeting

the necessitate of organisations in making more effective plans. The data or information to be

followed by the Cost Accounting System must be accurate or relevant; otherwise it may distort

the result of the system. Along with this, the system of costing must not sacrifice the utility by

presenting meticulous as well as unnecessary details. In this, Management of an organisation

must have a faith or belief in the Costing System and must also give a helping hand for its

improvement and success.

Price Optimisation System:

Price optimisation system acts as an key essential framework with the help of which

organisation can easily able to determine price of services and products which will prove suitable

for organisation as well as for organisation. This will further aid in evaluating consumers review

on different pricing level. Main aim or price optimisation system is to offer factors with the help

of which price can can be set in well effective manner. With the help of this form of accounting

system, companies can effectively set their price at numerous level which further aid in

providing benefits for company along with consumers. In order to set price, Mathematical

calculation is most essential and important which will help an organisation in managing its

transaction in systematic manner. Calculation introduces as an important act of calculating,

which is applying maths as well as logic to figure out a problem.

Job Costing System:

This system in tend towards, proper calculation of overall cost that occurs while offering

services and products in addition with after assignment of cost to every individual unit relating to

product and service. Job costing system effectively helps in those organisations that provide

different types of products and services (Ward, 2012). In order to offer numerous form of

products and services it become essential for organisations to effectively estimate every

2

individual unit cost. For this, company can effectively take advantage of job costing system in

order to effectively evaluate and analyse cost of various services and products.

Inventory Management System:

This system is one of the most effective and crucial system in management accounting

system. As with the help of this organisation can able to track status of their products and

services. This further benefits of using evaluate and measure their products and services

availability. Inventory management system proves to be beneficial in supply chain management.

With the help of this management system, companies can track availability of their products and

services and measure status. For instance, in order to effectively track, mortgage loan's

clarification then by taking advantage of this method company can able to effectively check

status of service. There are different system of inventory management such as EOQ, ROP, JIT

etc. All these are essential and effective systems which will help an organisation to manage

inventory and achieve better outcomes within given time duration. In organsations, EOQ is most

effective and essential method which will support an enterprise to analyse how much to buy and

when to buy.

For Example:

Mentioned below there are Six roles of management accounting

Accounting: In this role of management accounting, responsibilities relating to

calculation of profit and loss, financial transactions and expenses are done as to handle

bookkeeping responsibilities.

3

order to effectively evaluate and analyse cost of various services and products.

Inventory Management System:

This system is one of the most effective and crucial system in management accounting

system. As with the help of this organisation can able to track status of their products and

services. This further benefits of using evaluate and measure their products and services

availability. Inventory management system proves to be beneficial in supply chain management.

With the help of this management system, companies can track availability of their products and

services and measure status. For instance, in order to effectively track, mortgage loan's

clarification then by taking advantage of this method company can able to effectively check

status of service. There are different system of inventory management such as EOQ, ROP, JIT

etc. All these are essential and effective systems which will help an organisation to manage

inventory and achieve better outcomes within given time duration. In organsations, EOQ is most

effective and essential method which will support an enterprise to analyse how much to buy and

when to buy.

For Example:

Mentioned below there are Six roles of management accounting

Accounting: In this role of management accounting, responsibilities relating to

calculation of profit and loss, financial transactions and expenses are done as to handle

bookkeeping responsibilities.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Planning: This role holds great importance in management accounting, as in this

formation of long and short terms actions and plans are undertaken as per according to budget

and available resources.

Control: In order to ensure effective outcomes it is essential for organisations to monitor,

measure, evaluate correct actual outcomes as to make sure that actions are as per accordance to

original plan.

Cost accounting: In management accounting, it is essential to effectively evaluate cost

related factor in each and every aspect as to conduct operations in well defined manner.

Financial management: This is one of the most effective role in which management

accountant is responsible to effectively prepare and evaluate financial statements, budgets,

preparation of reports and commentaries.

Auditing: In this accounting department manager is required to review and audit

financial statements in order to effectively take advantage of financial statement and further

increase profitability.

Decision making: In management accounting, decisions related to discounting a product,

make- or-buy, pricing of product, optimum product mix is taken within short-term decision.

While in within long term decisions related to project financing, capital budgeting, investment

appraisals are considered.

P2. Explain different method of management accounting reporting.

Numerous form of accounting reports acts as an essential element in an business along

with this management accounting report proves to be beneficial in an organisation. Accounting

reports is a crucial element that perform key essential role within internal management of an

organisation day to day business functions. As it effectively aid managers to take decisions in

best effective manner along with framing strategies as according to actual need. In this report,

both the form of monetary and non monetary informations are included that are undertaken by

various organisations are –

Performance Reports:

Performance report is a well effective measure with the help of which performance can

be effectively evaluate. In relation with management accounting, performance report tend

towards effective evaluation of organisation and employees. It further helps in reducing

4

formation of long and short terms actions and plans are undertaken as per according to budget

and available resources.

Control: In order to ensure effective outcomes it is essential for organisations to monitor,

measure, evaluate correct actual outcomes as to make sure that actions are as per accordance to

original plan.

Cost accounting: In management accounting, it is essential to effectively evaluate cost

related factor in each and every aspect as to conduct operations in well defined manner.

Financial management: This is one of the most effective role in which management

accountant is responsible to effectively prepare and evaluate financial statements, budgets,

preparation of reports and commentaries.

Auditing: In this accounting department manager is required to review and audit

financial statements in order to effectively take advantage of financial statement and further

increase profitability.

Decision making: In management accounting, decisions related to discounting a product,

make- or-buy, pricing of product, optimum product mix is taken within short-term decision.

While in within long term decisions related to project financing, capital budgeting, investment

appraisals are considered.

P2. Explain different method of management accounting reporting.

Numerous form of accounting reports acts as an essential element in an business along

with this management accounting report proves to be beneficial in an organisation. Accounting

reports is a crucial element that perform key essential role within internal management of an

organisation day to day business functions. As it effectively aid managers to take decisions in

best effective manner along with framing strategies as according to actual need. In this report,

both the form of monetary and non monetary informations are included that are undertaken by

various organisations are –

Performance Reports:

Performance report is a well effective measure with the help of which performance can

be effectively evaluate. In relation with management accounting, performance report tend

towards effective evaluation of organisation and employees. It further helps in reducing

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

complexity related to deciding employees eligibility for rewards. With the help of this report,

organisation can easily able to evaluate organisation and employees performance.

Budget Report:

Budget report is one of the most important report in management accounting with the

help of which organisation can effectively able to compare their estimated performance against

actual performance. Along with this, it further benefits in framing strategies and policies with the

help of which organisation can able to effectively estimate about their expenses and income for a

specific period of time and can fulfil this in order to achieve their objectives. With the help of

budget report, organisations can make perfect comparison in between their budget goals and

actual financial performance. This further helps in framing strategies in best effective manner

within proper budget.

Accounts Receivable ageing report:

In this report, informations related to credit transactions are included. Account receivable

ageing report proves to be beneficial for those organisations who mainly indulge in credit basis

transactions. With the help this organisation can effectively able to manage their financial

transactions and key regular measure on their due amount in market. In addition with this, it also

cover credit transaction data on which transaction was made, it helps in resolving credit

calculation complexity. With the help of account receivable ageing report, companies can easily

analyse total collection that has been made by customer. It helps in bringing transparency within

credit collection.

Cost managerial accounting report:

Cost managerial accounting report effectively helps an organisation to check estimation

of their profit and loss against numerous form of activities in a particular formative framework.

This further helps in making proper calculation of all related expenses before and after the

selling was made in order to compare total expenses that has been earned from selling. In this, if

expenses emerged to be more as compared to selling then it tend towards loss for an

organisation but if selling money termed to be more than expenses them it is profit.

Organisations can take advantage of this report in order to properly evaluate profit and loss as to

frame plans and policies in well effective manner.

Purpose of management accounting reports.

5

organisation can easily able to evaluate organisation and employees performance.

Budget Report:

Budget report is one of the most important report in management accounting with the

help of which organisation can effectively able to compare their estimated performance against

actual performance. Along with this, it further benefits in framing strategies and policies with the

help of which organisation can able to effectively estimate about their expenses and income for a

specific period of time and can fulfil this in order to achieve their objectives. With the help of

budget report, organisations can make perfect comparison in between their budget goals and

actual financial performance. This further helps in framing strategies in best effective manner

within proper budget.

Accounts Receivable ageing report:

In this report, informations related to credit transactions are included. Account receivable

ageing report proves to be beneficial for those organisations who mainly indulge in credit basis

transactions. With the help this organisation can effectively able to manage their financial

transactions and key regular measure on their due amount in market. In addition with this, it also

cover credit transaction data on which transaction was made, it helps in resolving credit

calculation complexity. With the help of account receivable ageing report, companies can easily

analyse total collection that has been made by customer. It helps in bringing transparency within

credit collection.

Cost managerial accounting report:

Cost managerial accounting report effectively helps an organisation to check estimation

of their profit and loss against numerous form of activities in a particular formative framework.

This further helps in making proper calculation of all related expenses before and after the

selling was made in order to compare total expenses that has been earned from selling. In this, if

expenses emerged to be more as compared to selling then it tend towards loss for an

organisation but if selling money termed to be more than expenses them it is profit.

Organisations can take advantage of this report in order to properly evaluate profit and loss as to

frame plans and policies in well effective manner.

Purpose of management accounting reports.

5

Management accounting reports serve the purpose to organisations as to effectively make

decisions as per according to plan. Major purpose of management accounting report is to

decrease ambiguity and assist organisation to formulate decision-making process in best

effective manner.

TASK 2

P3 .Appropriate techniques of cost analysis to prepare an income statement

Information must be relevant, accurate and current which will help an organisation in its

success and growth. Accurate information will also support an enterprise to attain long term

goals and objectives within given time duration.

In context to selected firm these method are used to prepare statements for three year that is

discussed below:

6

decisions as per according to plan. Major purpose of management accounting report is to

decrease ambiguity and assist organisation to formulate decision-making process in best

effective manner.

TASK 2

P3 .Appropriate techniques of cost analysis to prepare an income statement

Information must be relevant, accurate and current which will help an organisation in its

success and growth. Accurate information will also support an enterprise to attain long term

goals and objectives within given time duration.

In context to selected firm these method are used to prepare statements for three year that is

discussed below:

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

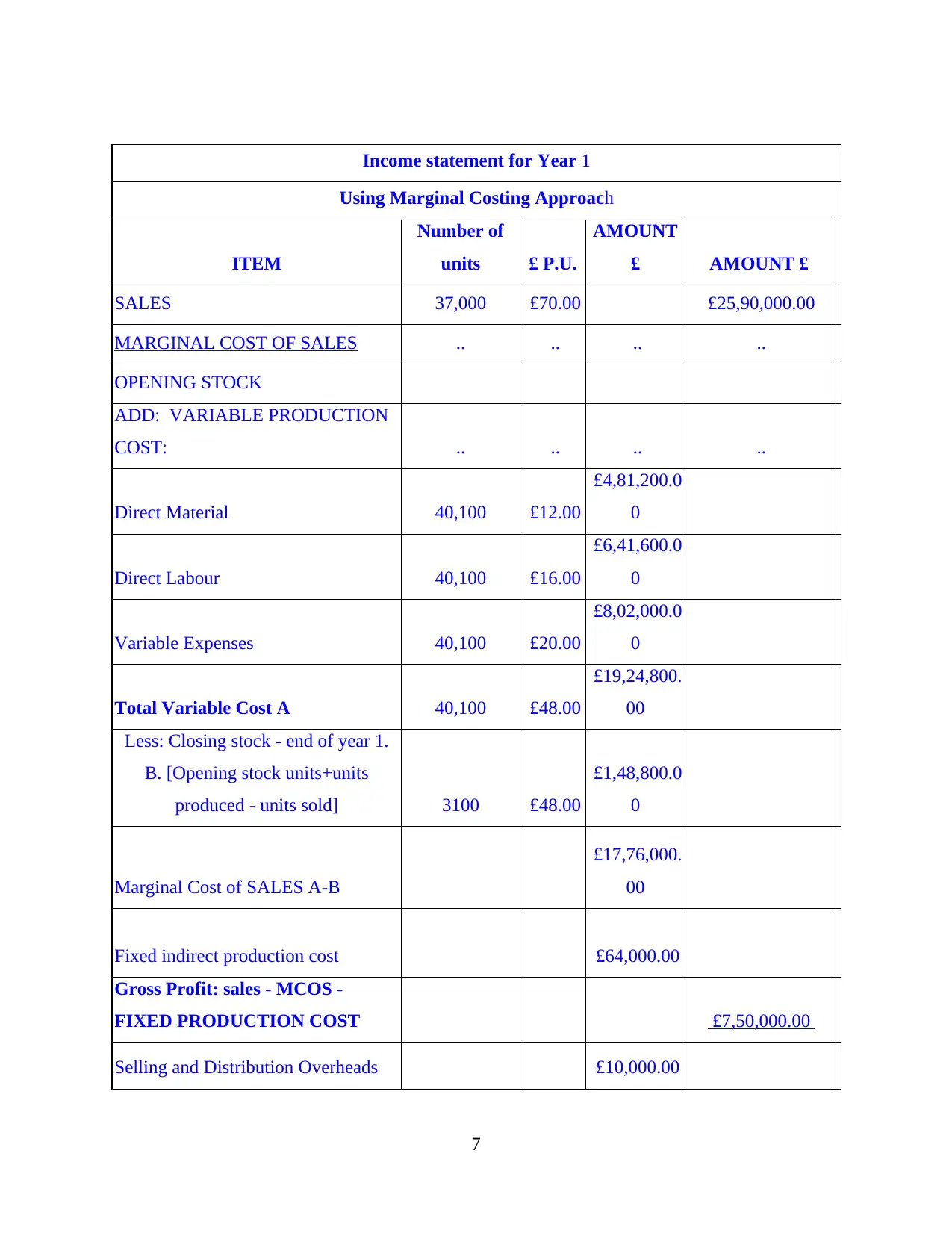

Income statement for Year 1

Using Marginal Costing Approach

ITEM

Number of

units £ P.U.

AMOUNT

£ AMOUNT £

SALES 37,000 £70.00 £25,90,000.00

MARGINAL COST OF SALES .. .. .. ..

OPENING STOCK

ADD: VARIABLE PRODUCTION

COST: .. .. .. ..

Direct Material 40,100 £12.00

£4,81,200.0

0

Direct Labour 40,100 £16.00

£6,41,600.0

0

Variable Expenses 40,100 £20.00

£8,02,000.0

0

Total Variable Cost A 40,100 £48.00

£19,24,800.

00

Less: Closing stock - end of year 1.

B. [Opening stock units+units

produced - units sold] 3100 £48.00

£1,48,800.0

0

Marginal Cost of SALES A-B

£17,76,000.

00

Fixed indirect production cost £64,000.00

Gross Profit: sales - MCOS -

FIXED PRODUCTION COST £7,50,000.00

Selling and Distribution Overheads £10,000.00

7

Using Marginal Costing Approach

ITEM

Number of

units £ P.U.

AMOUNT

£ AMOUNT £

SALES 37,000 £70.00 £25,90,000.00

MARGINAL COST OF SALES .. .. .. ..

OPENING STOCK

ADD: VARIABLE PRODUCTION

COST: .. .. .. ..

Direct Material 40,100 £12.00

£4,81,200.0

0

Direct Labour 40,100 £16.00

£6,41,600.0

0

Variable Expenses 40,100 £20.00

£8,02,000.0

0

Total Variable Cost A 40,100 £48.00

£19,24,800.

00

Less: Closing stock - end of year 1.

B. [Opening stock units+units

produced - units sold] 3100 £48.00

£1,48,800.0

0

Marginal Cost of SALES A-B

£17,76,000.

00

Fixed indirect production cost £64,000.00

Gross Profit: sales - MCOS -

FIXED PRODUCTION COST £7,50,000.00

Selling and Distribution Overheads £10,000.00

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Admin Overheads £15,000.00

Profit Before Interest & Tax

(PBIT) £7,25,000.00

Interest Expenses £1,000.00

Probit Before Tax [PBIT-interest] £7,24,000.00

Tax @19% £1,37,560.00

Net Profit: profit before tax - tax £5,86,440.00

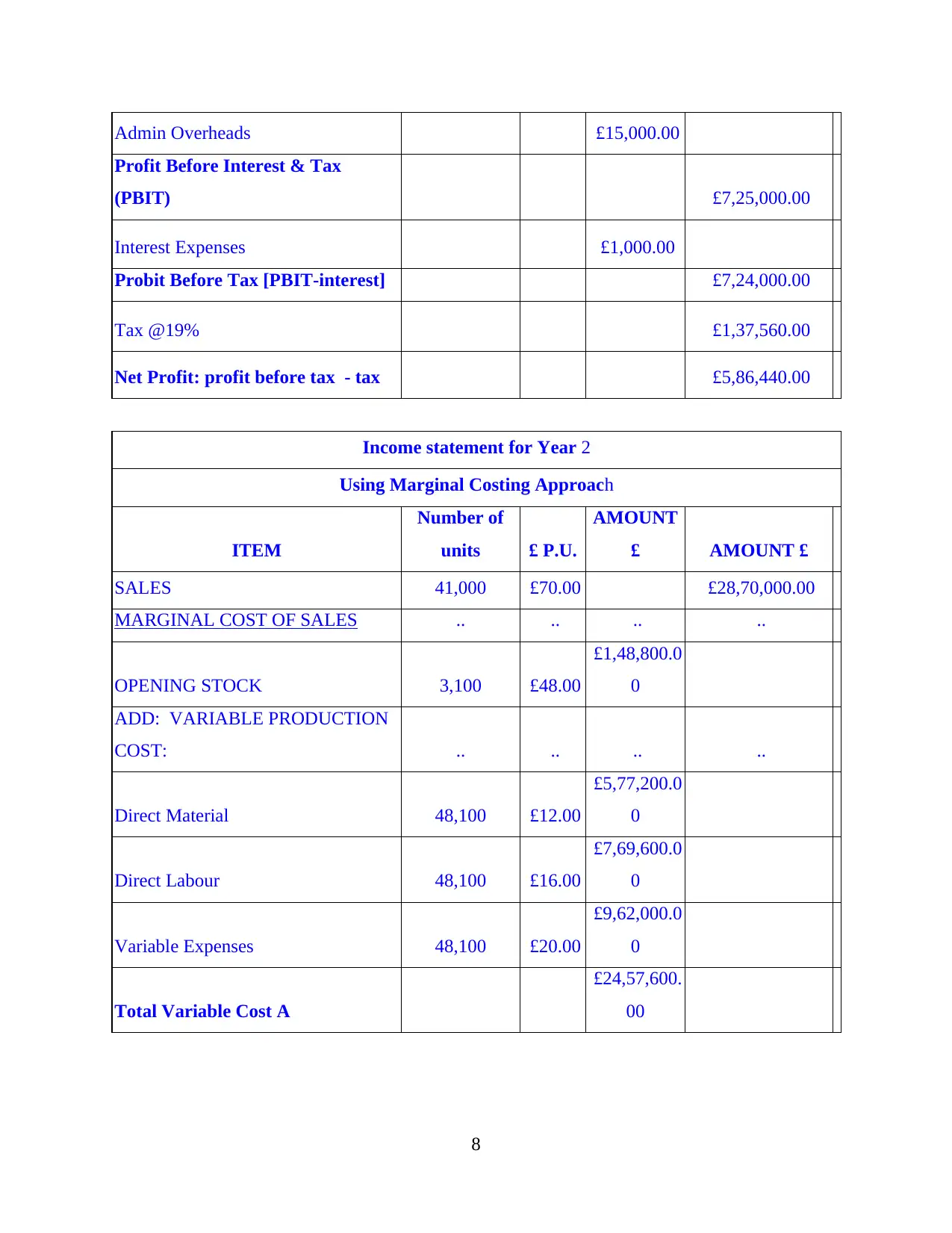

Income statement for Year 2

Using Marginal Costing Approach

ITEM

Number of

units £ P.U.

AMOUNT

£ AMOUNT £

SALES 41,000 £70.00 £28,70,000.00

MARGINAL COST OF SALES .. .. .. ..

OPENING STOCK 3,100 £48.00

£1,48,800.0

0

ADD: VARIABLE PRODUCTION

COST: .. .. .. ..

Direct Material 48,100 £12.00

£5,77,200.0

0

Direct Labour 48,100 £16.00

£7,69,600.0

0

Variable Expenses 48,100 £20.00

£9,62,000.0

0

Total Variable Cost A

£24,57,600.

00

8

Profit Before Interest & Tax

(PBIT) £7,25,000.00

Interest Expenses £1,000.00

Probit Before Tax [PBIT-interest] £7,24,000.00

Tax @19% £1,37,560.00

Net Profit: profit before tax - tax £5,86,440.00

Income statement for Year 2

Using Marginal Costing Approach

ITEM

Number of

units £ P.U.

AMOUNT

£ AMOUNT £

SALES 41,000 £70.00 £28,70,000.00

MARGINAL COST OF SALES .. .. .. ..

OPENING STOCK 3,100 £48.00

£1,48,800.0

0

ADD: VARIABLE PRODUCTION

COST: .. .. .. ..

Direct Material 48,100 £12.00

£5,77,200.0

0

Direct Labour 48,100 £16.00

£7,69,600.0

0

Variable Expenses 48,100 £20.00

£9,62,000.0

0

Total Variable Cost A

£24,57,600.

00

8

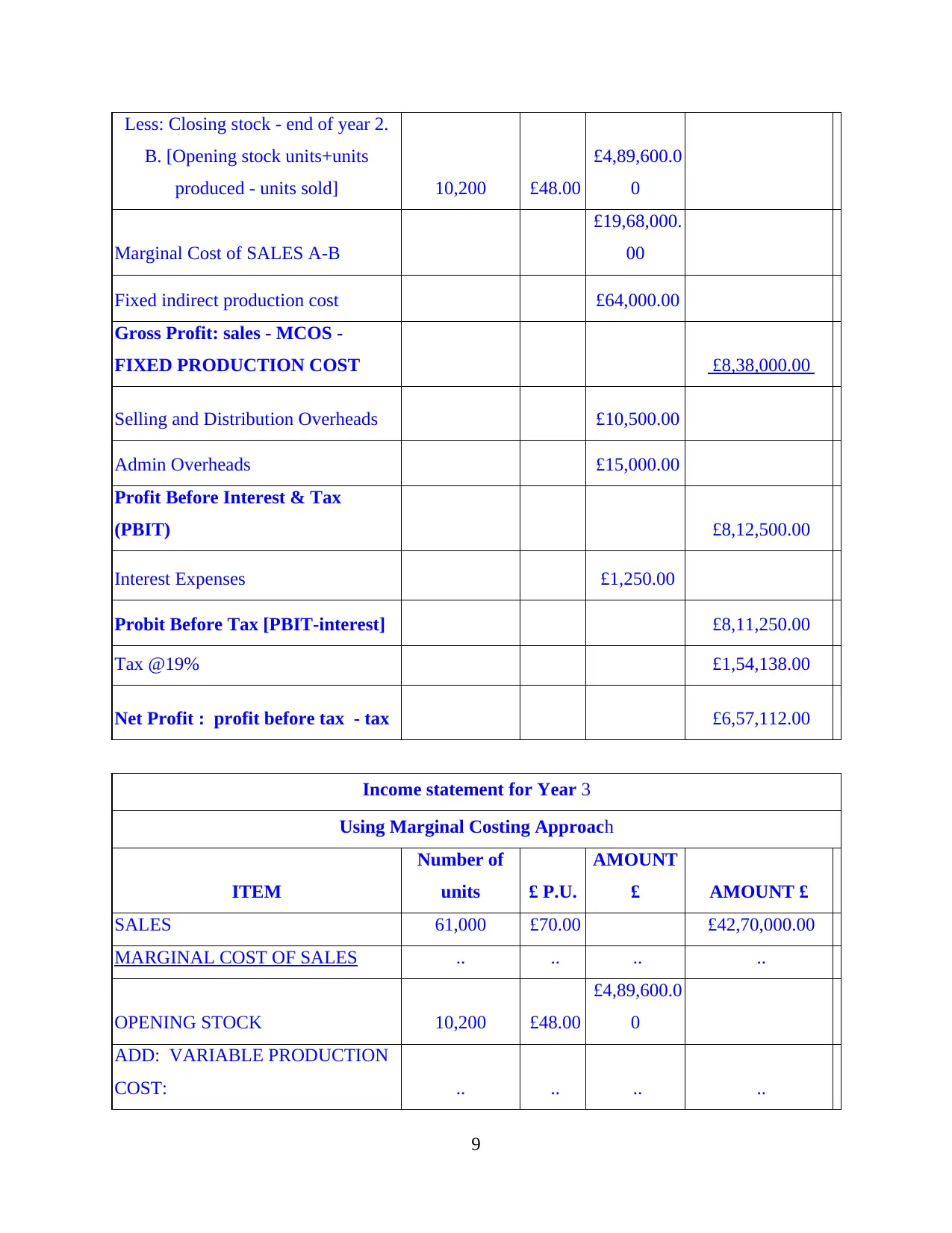

Less: Closing stock - end of year 2.

B. [Opening stock units+units

produced - units sold] 10,200 £48.00

£4,89,600.0

0

Marginal Cost of SALES A-B

£19,68,000.

00

Fixed indirect production cost £64,000.00

Gross Profit: sales - MCOS -

FIXED PRODUCTION COST £8,38,000.00

Selling and Distribution Overheads £10,500.00

Admin Overheads £15,000.00

Profit Before Interest & Tax

(PBIT) £8,12,500.00

Interest Expenses £1,250.00

Probit Before Tax [PBIT-interest] £8,11,250.00

Tax @19% £1,54,138.00

Net Profit : profit before tax - tax £6,57,112.00

Income statement for Year 3

Using Marginal Costing Approach

ITEM

Number of

units £ P.U.

AMOUNT

£ AMOUNT £

SALES 61,000 £70.00 £42,70,000.00

MARGINAL COST OF SALES .. .. .. ..

OPENING STOCK 10,200 £48.00

£4,89,600.0

0

ADD: VARIABLE PRODUCTION

COST: .. .. .. ..

9

B. [Opening stock units+units

produced - units sold] 10,200 £48.00

£4,89,600.0

0

Marginal Cost of SALES A-B

£19,68,000.

00

Fixed indirect production cost £64,000.00

Gross Profit: sales - MCOS -

FIXED PRODUCTION COST £8,38,000.00

Selling and Distribution Overheads £10,500.00

Admin Overheads £15,000.00

Profit Before Interest & Tax

(PBIT) £8,12,500.00

Interest Expenses £1,250.00

Probit Before Tax [PBIT-interest] £8,11,250.00

Tax @19% £1,54,138.00

Net Profit : profit before tax - tax £6,57,112.00

Income statement for Year 3

Using Marginal Costing Approach

ITEM

Number of

units £ P.U.

AMOUNT

£ AMOUNT £

SALES 61,000 £70.00 £42,70,000.00

MARGINAL COST OF SALES .. .. .. ..

OPENING STOCK 10,200 £48.00

£4,89,600.0

0

ADD: VARIABLE PRODUCTION

COST: .. .. .. ..

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.