Management Accounting Report: Financial Problem Solving and Success

VerifiedAdded on 2023/01/13

|22

|4158

|72

Report

AI Summary

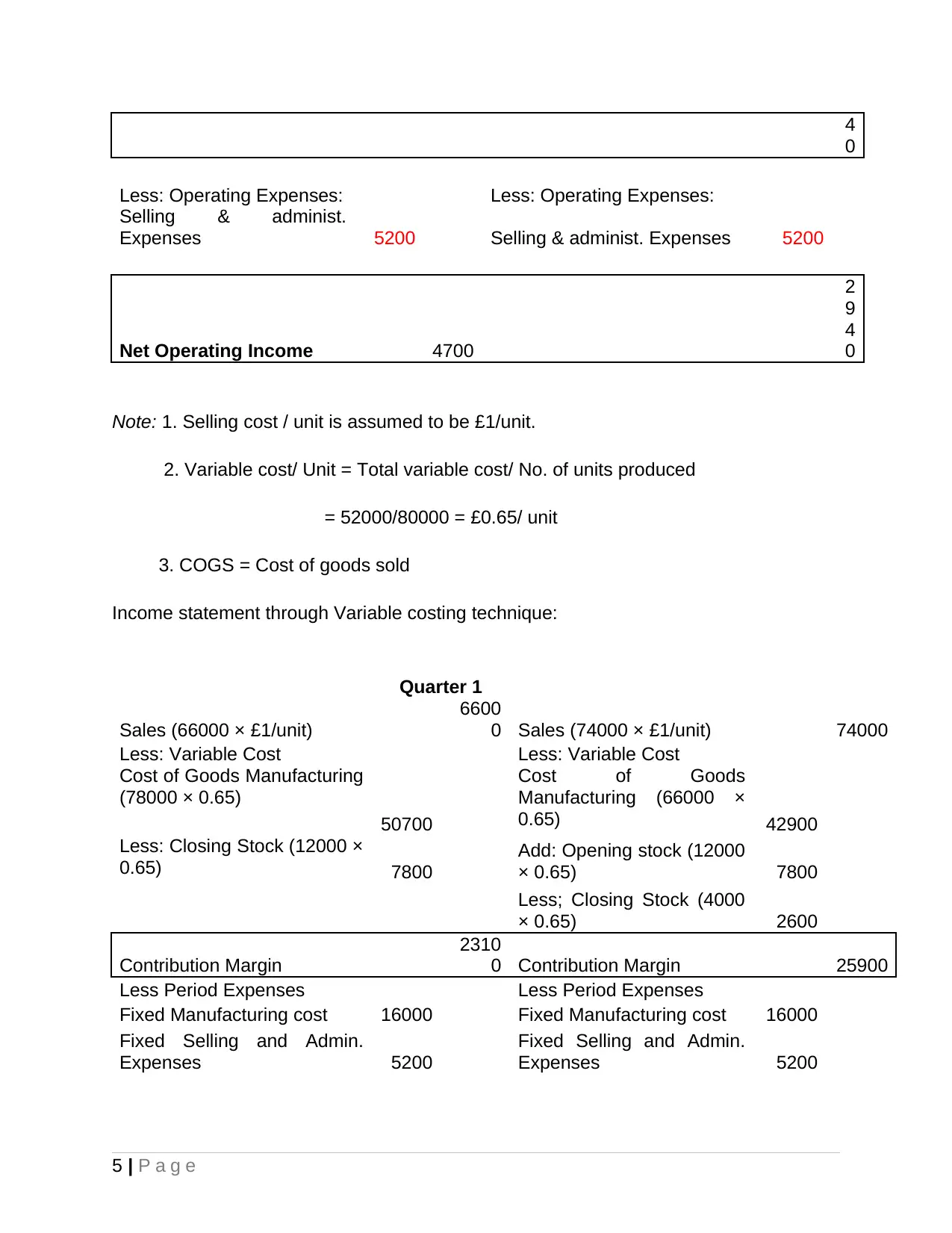

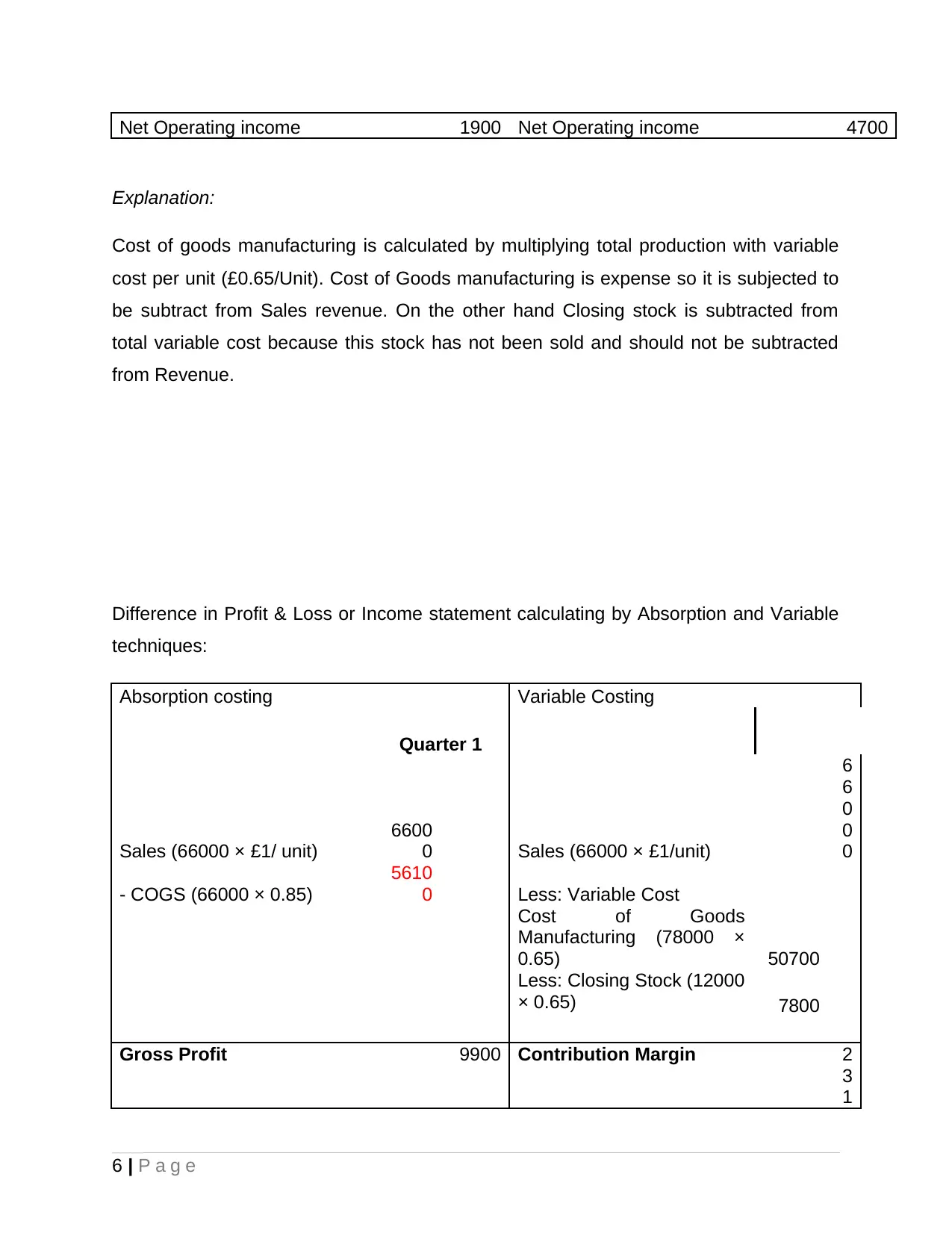

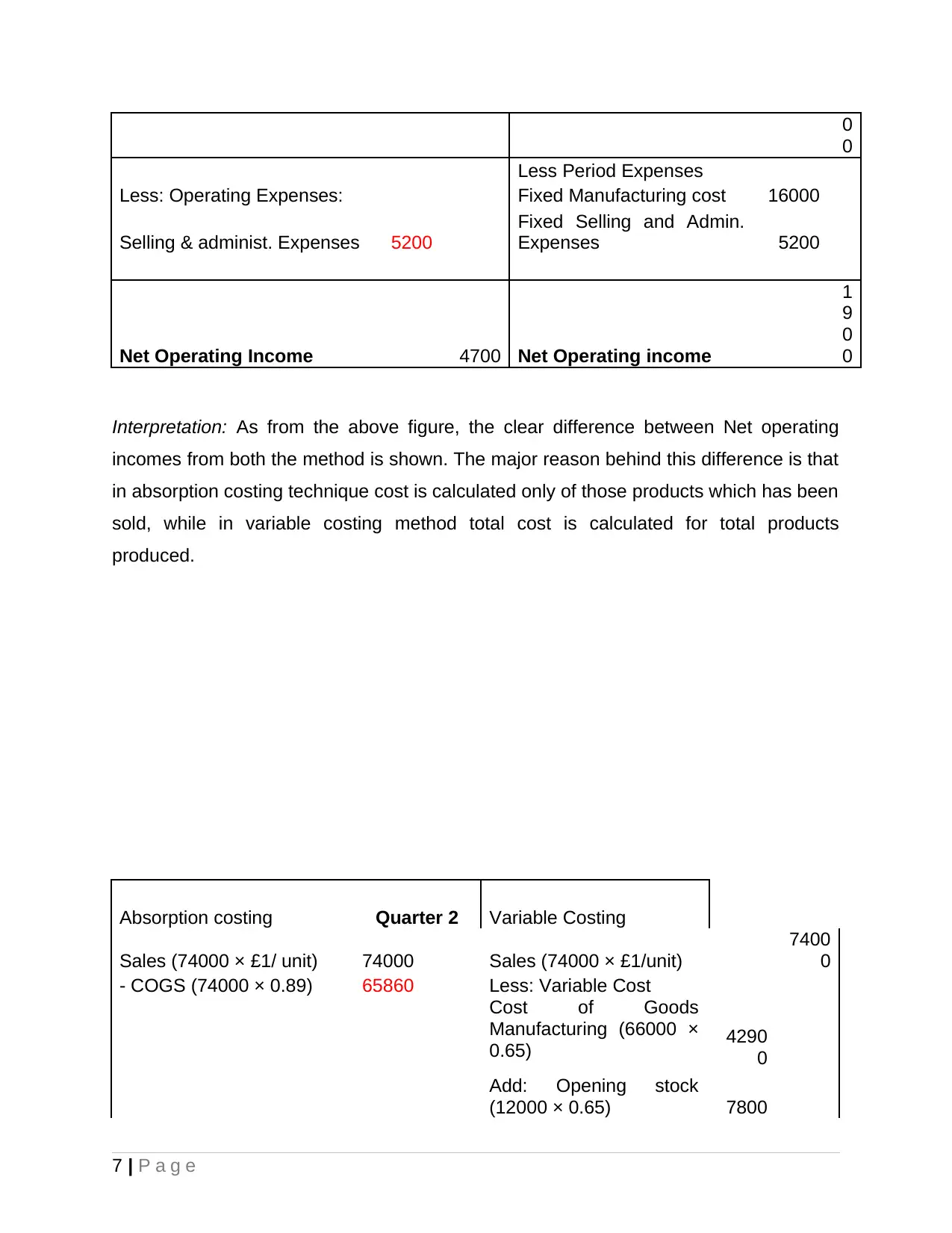

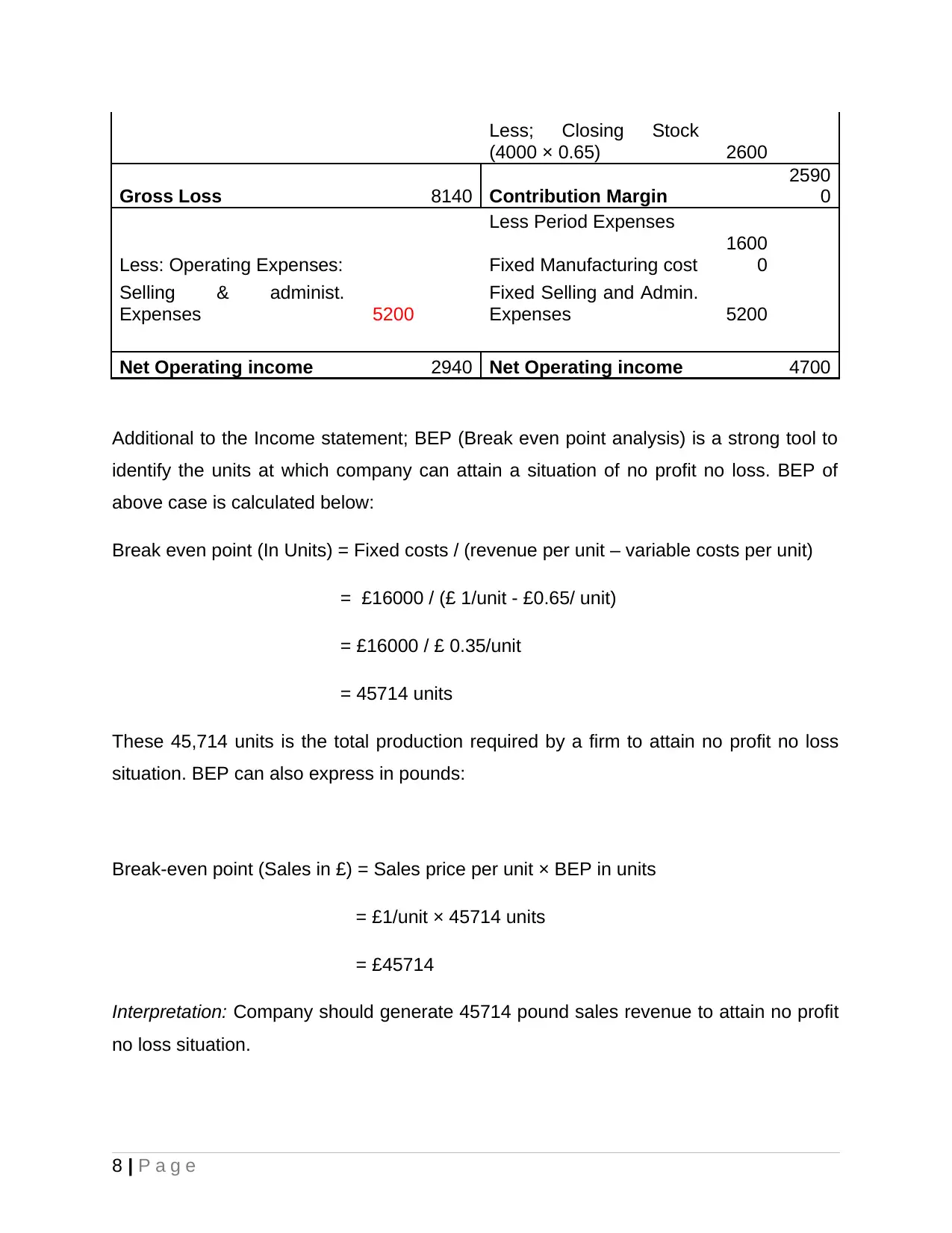

This report delves into the core principles of management accounting, providing a comprehensive overview of its application in a business environment. It begins by introducing the fundamentals and explores the use of financial data for planning, monitoring, and controlling finances. The report analyzes two types of income statements: marginal costing and absorption costing, demonstrating how direct and indirect costs are treated. It also examines various financial problems, such as low revenue and high debt, and presents management accounting tools and techniques to overcome these challenges, including margin analysis, capital budgeting, and demand forecasting. The report further discusses the advantages and disadvantages of budgetary control and pricing strategies. Finally, it addresses the concept of sustainable success within the context of management accounting systems, emphasizing the importance of adapting these systems to solve financial problems and achieve long-term goals. The report includes calculations and interpretations to illustrate the practical application of these concepts.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.