Management Accounting Report: Budgeting, Variance, and Apple Inc.

VerifiedAdded on 2023/04/21

|8

|1195

|232

Report

AI Summary

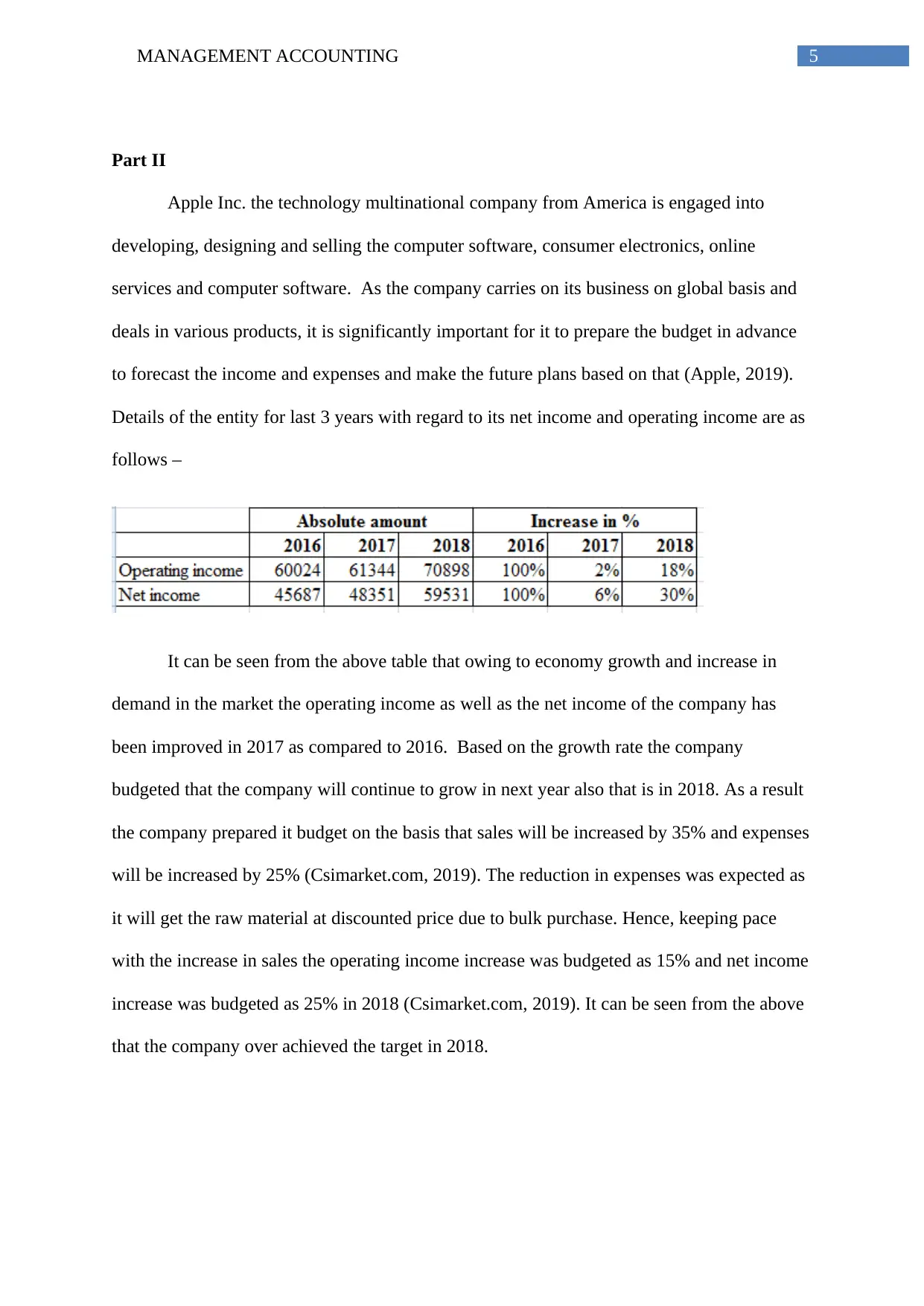

This report on management accounting explores the purposes and principles of budgeting, including forecasting, decision-making, and performance monitoring. It delves into different types of budgets such as master, operating, and financial budgets, and explains their relationships with management by exception. The report also covers budget variance analysis, highlighting favorable and unfavorable variances. Furthermore, it examines the budgeting process, assumptions, and how budgeted performance compares to past results. The second part of the report provides a case study on Apple Inc., analyzing its financial performance and budgeting practices, including its revenue, expenses, and income growth over a three-year period and evaluating its budgeting accuracy and forecasting methods. The report concludes with a list of references.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.