Management Accounting Systems and Reporting for BAM Construction

VerifiedAdded on 2021/02/20

|18

|5042

|396

Report

AI Summary

This report analyzes the management accounting practices of BAM Construction Limited, a civil engineering company. It explores various management accounting systems, including price optimization, job costing, inventory management, and cost accounting, and their application within the company. The report also examines different types of management accounting reports, such as inventory reports, cost accounting reports, performance reports, and accounts receivable aging reports, highlighting their importance in decision-making. Furthermore, it presents profit statements under both marginal and absorption costing principles, providing a comprehensive understanding of financial reporting methods. The report emphasizes the integration of management accounting systems and reporting with the company's processes, demonstrating how these tools support effective financial management and strategic planning.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

ACTIVITY 1....................................................................................................................................3

PART (A)....................................................................................................................................3

PART(B).....................................................................................................................................7

ACTIVITY 2..................................................................................................................................12

PART (A)..................................................................................................................................12

PART(B)...................................................................................................................................14

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION...........................................................................................................................3

ACTIVITY 1....................................................................................................................................3

PART (A)....................................................................................................................................3

PART(B).....................................................................................................................................7

ACTIVITY 2..................................................................................................................................12

PART (A)..................................................................................................................................12

PART(B)...................................................................................................................................14

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION

The management accounting is as significance as financial accounting. It can be defined

as a different part of accounting in that internal reports are prepared for internal stakeholders

(Cooper, 2017). These reports can be prepared only by this accounting because it consists

monetary and non monetary information. In today's context mostly organisations are

implementing this accounting because of its increasing importance. With the use of it, managers

of companies can evaluate the actual financial performance that helps in preparing competitive

strategies and plans as well as in major decision making. For better understanding of it, BAM

construction limited company is selected which is basically a civil engineering company. It is

located in London and deals in small, large construction projects. The project report contains two

activities in which, first activity describes about management accounting systems and reports as

well as income statement is produced as per given information. Further, in second activity

planning tools and role of MA systems to solve the monetary issues is included. Along with

solution of given practical parts is mentioned.

ACTIVITY 1

PART (A)

Management accounting and essential requirement of different accounting method.

Types of management accounting systems:

Price optimisation system- This is a part of management accounting which is related to

sales department of companies. It is so because this provides a detailed information

regarding to the customer's reaction on various prices (Jacobs, 2012). With the help of it

companies can set the prices of their products and services on which customers can be

satisfy. Like in the aspect of above BAM construction limited company, they operate in

wide range of construction projects and they determine the expected price of their civil

engineering projects with the help of it. This helps them a lot because as per their

customer's reaction on various prices they set the estimated price. Hence, it is essential

for companies to draw an effective pricing pattern which can benefit to companies as well

as can satisfy the customers.

The management accounting is as significance as financial accounting. It can be defined

as a different part of accounting in that internal reports are prepared for internal stakeholders

(Cooper, 2017). These reports can be prepared only by this accounting because it consists

monetary and non monetary information. In today's context mostly organisations are

implementing this accounting because of its increasing importance. With the use of it, managers

of companies can evaluate the actual financial performance that helps in preparing competitive

strategies and plans as well as in major decision making. For better understanding of it, BAM

construction limited company is selected which is basically a civil engineering company. It is

located in London and deals in small, large construction projects. The project report contains two

activities in which, first activity describes about management accounting systems and reports as

well as income statement is produced as per given information. Further, in second activity

planning tools and role of MA systems to solve the monetary issues is included. Along with

solution of given practical parts is mentioned.

ACTIVITY 1

PART (A)

Management accounting and essential requirement of different accounting method.

Types of management accounting systems:

Price optimisation system- This is a part of management accounting which is related to

sales department of companies. It is so because this provides a detailed information

regarding to the customer's reaction on various prices (Jacobs, 2012). With the help of it

companies can set the prices of their products and services on which customers can be

satisfy. Like in the aspect of above BAM construction limited company, they operate in

wide range of construction projects and they determine the expected price of their civil

engineering projects with the help of it. This helps them a lot because as per their

customer's reaction on various prices they set the estimated price. Hence, it is essential

for companies to draw an effective pricing pattern which can benefit to companies as well

as can satisfy the customers.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Job costing system- It is a type of accounting system of management accounting that is

linked to the finance department of companies (Guthrie, Parker, 2014). In this, various

cost such as labour cost, material cost etc. are estimated and calculated. With the help of

it, companies can assess the total cost of their various kind of jobs allocated to multiple

operations. Such as in the context of above BAM construction limited company, there are

a wide range of labour cost, material cost etc. All these costs are being managed with the

help of this accounting system. So overall, it is essential to companies for proper

management of cost in the various operations.

Inventory management system-In this type of management accounting, a detailed track

record of various kind of inventories such as work in progress stock, raw material,

finished commodities etc. is included. Along with under it, the information related to how

much quantity of material is consumed and how much is remaining. On the basis of it,

companies' production department takes crucial decisions. Herein, the context of above

selected, BAM construction limited company their contractors use this accounting that

helps them in effective allocation of raw material in construction projects. It is essentially

required in organisations for two purposes which are keeping track record of materials as

well as for taking important decision in relation to production and purchasing.

Cost accounting system- It can be defined as an accounting system that is linked with the

finance department of companies (Mussnig, 2013). In other words, this accounting

system forecast and calculate actual amount of cost that occur in multiple operations. The

primary objective of this accounting system is to keep the total cost of various activities

under control as much as possible. With the effective implementation of this accounting

system, companies can evaluate about how much cost will be occurred in production of

one unit and on the basis of it they try to keep below forecasted amount. Such as in the

BAM construction limited company, their finance department is using this accounting

system to track the difference between actual and estimated cost. Thus, this accounting

system is essentially required by companies to keep the cost below budgeted cost.

Various kind of management accounting reporting.

The management accounting reports are kind of written document that are prepared on

the basis of an organisation's financial and non financial transactions for a particular time period

linked to the finance department of companies (Guthrie, Parker, 2014). In this, various

cost such as labour cost, material cost etc. are estimated and calculated. With the help of

it, companies can assess the total cost of their various kind of jobs allocated to multiple

operations. Such as in the context of above BAM construction limited company, there are

a wide range of labour cost, material cost etc. All these costs are being managed with the

help of this accounting system. So overall, it is essential to companies for proper

management of cost in the various operations.

Inventory management system-In this type of management accounting, a detailed track

record of various kind of inventories such as work in progress stock, raw material,

finished commodities etc. is included. Along with under it, the information related to how

much quantity of material is consumed and how much is remaining. On the basis of it,

companies' production department takes crucial decisions. Herein, the context of above

selected, BAM construction limited company their contractors use this accounting that

helps them in effective allocation of raw material in construction projects. It is essentially

required in organisations for two purposes which are keeping track record of materials as

well as for taking important decision in relation to production and purchasing.

Cost accounting system- It can be defined as an accounting system that is linked with the

finance department of companies (Mussnig, 2013). In other words, this accounting

system forecast and calculate actual amount of cost that occur in multiple operations. The

primary objective of this accounting system is to keep the total cost of various activities

under control as much as possible. With the effective implementation of this accounting

system, companies can evaluate about how much cost will be occurred in production of

one unit and on the basis of it they try to keep below forecasted amount. Such as in the

BAM construction limited company, their finance department is using this accounting

system to track the difference between actual and estimated cost. Thus, this accounting

system is essentially required by companies to keep the cost below budgeted cost.

Various kind of management accounting reporting.

The management accounting reports are kind of written document that are prepared on

the basis of an organisation's financial and non financial transactions for a particular time period

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Harrison and Lock, 2017). These reports are being used by managers of companies as they take

important decisions on the basis it. Additionally, these reports are presented only to the internal

aspects of companies not to the external parties. In the aspect of above BAM construction limited

company, their management accountant produces different types of reports to help their

managers and some of them are mentioned below:

Inventory reports- These are kind of reports that consists information regarding to

quantitative aspects of various kind of stock including raw material, work in progress and

finished goods (Evans, Burritt and Guthrie, 2013). This type of report is very important

for production department because with the help of it, they manage entire production

process. The importance of this report is not limited till the production department but

also it is useful for minimising the cost of storing the materials in warehouses. Such as in

the BAM construction limited company, their accountant is preparing this report which

includes information related of raw material like cement, iron, concrete etc. for

compilation of any civil project.

Cost accounting report- It has been defined as a type of report which is linked with

finance department. This is so because in it, information related to the cost of each

activity is included. Its importance can not be ignored by companies because in the

absence of it they will not be able to forecast total cost as well as actual occurred cost.

Such as in the above BAM construction limited company, their management accountant

produce this report which helps them in evaluating the cost of various civil engineering

projects. As well as on the basis of it, they make estimation of their projects.

Performance report- It is a type of report that is prepared on the basis of aspect of

performance of various aspects such as estimated financial goal and actual performance

(Schaltegger and Zvezdov, 2015). As well as this is aligned with the evaluation of actual

position of company in front of stakeholders. Such as in the aspect of above BAM

construction limited company, they are preparing this report for managing the financial

performance of their various kind of civil engineering projects. Along with this report is

almost necessary for them to prepare just because they are engaged in dealing large

construction projects. With the help of it, they assess the growth of their projects. Apart

from it, this report is not limited till the financial performance of projects but also it

evaluates performance of employees separately.

important decisions on the basis it. Additionally, these reports are presented only to the internal

aspects of companies not to the external parties. In the aspect of above BAM construction limited

company, their management accountant produces different types of reports to help their

managers and some of them are mentioned below:

Inventory reports- These are kind of reports that consists information regarding to

quantitative aspects of various kind of stock including raw material, work in progress and

finished goods (Evans, Burritt and Guthrie, 2013). This type of report is very important

for production department because with the help of it, they manage entire production

process. The importance of this report is not limited till the production department but

also it is useful for minimising the cost of storing the materials in warehouses. Such as in

the BAM construction limited company, their accountant is preparing this report which

includes information related of raw material like cement, iron, concrete etc. for

compilation of any civil project.

Cost accounting report- It has been defined as a type of report which is linked with

finance department. This is so because in it, information related to the cost of each

activity is included. Its importance can not be ignored by companies because in the

absence of it they will not be able to forecast total cost as well as actual occurred cost.

Such as in the above BAM construction limited company, their management accountant

produce this report which helps them in evaluating the cost of various civil engineering

projects. As well as on the basis of it, they make estimation of their projects.

Performance report- It is a type of report that is prepared on the basis of aspect of

performance of various aspects such as estimated financial goal and actual performance

(Schaltegger and Zvezdov, 2015). As well as this is aligned with the evaluation of actual

position of company in front of stakeholders. Such as in the aspect of above BAM

construction limited company, they are preparing this report for managing the financial

performance of their various kind of civil engineering projects. Along with this report is

almost necessary for them to prepare just because they are engaged in dealing large

construction projects. With the help of it, they assess the growth of their projects. Apart

from it, this report is not limited till the financial performance of projects but also it

evaluates performance of employees separately.

Account receivable ageing report- This may be defined as a kind of report which is

prepared by accountant to help the finance department so that it can be evaluated that

how much amount is due and overdue by debtors. With the help of this report, companies

can make their financial plan for future activities because on the basis of it they can

assess total expected fund which is required to collect from debtors. In the context of

above BAM construction limited company, they are preparing this report with an

objective to analyse their debtors. One of the key feature of this report is that in it

companies can identify those debtors who do not make payment even after the expected

date. It overall helps in computing the total payable interest amount by debtors.

Advantage of management accounting systems and their application in context of

companies.

Each type of management accounting has some importance in the aspect of companies. It

depends on organisations that how they use these accounting systems to get benefit. Such as in

the aspect of above BAM construction limited company, they have implemented multi-pal types

of accounting systems whose benefits are described below:

Importance of cost accounting system- This accounting system has its importance for

finance department of any type of organisation (Soltes, 2014). It is so because by this

companies can allocate their funds in a better way so that expenditures can be eliminated.

Like in the BAM construction limited company, it is benefiting them in management of

cost of their various construction projects.

Importance of price optimisation system- It has its importance in the context of sales

department of any kind of company. This is so because firstly it gather customer's

opinion on price segments and after that determines prices of products & services. Like in

the chosen company, they estimate the price of their construction projects with help of it.

Importance of inventory management system- This part of management accounting is

beneficial for companies because it is linked with production department. With the help

of it organisations can assess the need of material for further. In the BAM construction

limited company, they manage their inventories such as iron, cement, concrete, bricks,

stones etc. with the help of it.

prepared by accountant to help the finance department so that it can be evaluated that

how much amount is due and overdue by debtors. With the help of this report, companies

can make their financial plan for future activities because on the basis of it they can

assess total expected fund which is required to collect from debtors. In the context of

above BAM construction limited company, they are preparing this report with an

objective to analyse their debtors. One of the key feature of this report is that in it

companies can identify those debtors who do not make payment even after the expected

date. It overall helps in computing the total payable interest amount by debtors.

Advantage of management accounting systems and their application in context of

companies.

Each type of management accounting has some importance in the aspect of companies. It

depends on organisations that how they use these accounting systems to get benefit. Such as in

the aspect of above BAM construction limited company, they have implemented multi-pal types

of accounting systems whose benefits are described below:

Importance of cost accounting system- This accounting system has its importance for

finance department of any type of organisation (Soltes, 2014). It is so because by this

companies can allocate their funds in a better way so that expenditures can be eliminated.

Like in the BAM construction limited company, it is benefiting them in management of

cost of their various construction projects.

Importance of price optimisation system- It has its importance in the context of sales

department of any kind of company. This is so because firstly it gather customer's

opinion on price segments and after that determines prices of products & services. Like in

the chosen company, they estimate the price of their construction projects with help of it.

Importance of inventory management system- This part of management accounting is

beneficial for companies because it is linked with production department. With the help

of it organisations can assess the need of material for further. In the BAM construction

limited company, they manage their inventories such as iron, cement, concrete, bricks,

stones etc. with the help of it.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Importance of job costing system- This is useful for companies because it helps in

assessing the cost of job which is aligned in various activities. Such as in the BAM

construction limited company, they trace the cost of various job like labour, supervisors

in any construction project.

Integration of management accounting systems and reporting with process of companies.

The integration of both management accounting system and reporting is linked to the

process of companies (Sisaye and Birnberg, 2012). It is so because each type of MAS and

reporting has link with the various department of organisations. Such as in the above BAM

construction limited company, different types of MA like cost accounting system is aligned to

finance department for proper allocation of funds. As well as price optimisation system is linked

to the sales department and inventory management system with production department. It stats

that systems of MA is aligned with the organisational process. While the management

accounting reports, like cost accounting reports have interrelation with evaluation of financial

position as well as other reports also aligned with other activities of above company. So MAS

and MA reports are integrated within company's process.

PART(B)

ANNEX(A)

Question 2.

(A) Profit statements under marginal costing principles:

Marginal costing- It is a type of costing system that is relates to producing the income statements

by taking fixed cost as periodic expenses (Sedevich Fons, 2012). While variable cost as cost of

product.

1) 1st quarter (contribution & profit/loss)

Income statement by marginal costing method:

PARTICULAR

AMOUNT

(in £)

SALES REVENUE 427500 427500

LESS: VARIABLE COST

assessing the cost of job which is aligned in various activities. Such as in the BAM

construction limited company, they trace the cost of various job like labour, supervisors

in any construction project.

Integration of management accounting systems and reporting with process of companies.

The integration of both management accounting system and reporting is linked to the

process of companies (Sisaye and Birnberg, 2012). It is so because each type of MAS and

reporting has link with the various department of organisations. Such as in the above BAM

construction limited company, different types of MA like cost accounting system is aligned to

finance department for proper allocation of funds. As well as price optimisation system is linked

to the sales department and inventory management system with production department. It stats

that systems of MA is aligned with the organisational process. While the management

accounting reports, like cost accounting reports have interrelation with evaluation of financial

position as well as other reports also aligned with other activities of above company. So MAS

and MA reports are integrated within company's process.

PART(B)

ANNEX(A)

Question 2.

(A) Profit statements under marginal costing principles:

Marginal costing- It is a type of costing system that is relates to producing the income statements

by taking fixed cost as periodic expenses (Sedevich Fons, 2012). While variable cost as cost of

product.

1) 1st quarter (contribution & profit/loss)

Income statement by marginal costing method:

PARTICULAR

AMOUNT

(in £)

SALES REVENUE 427500 427500

LESS: VARIABLE COST

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

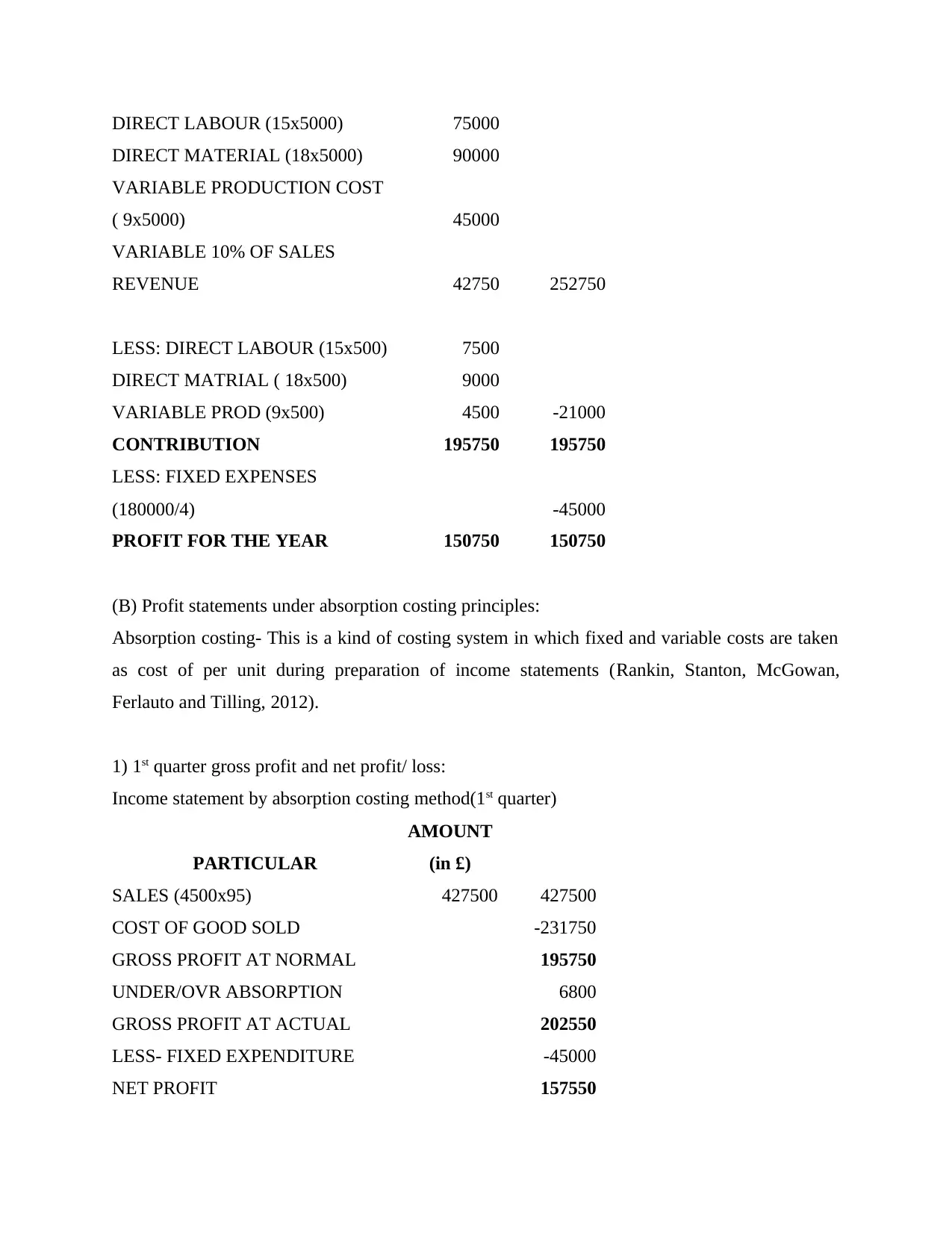

DIRECT LABOUR (15x5000) 75000

DIRECT MATERIAL (18x5000) 90000

VARIABLE PRODUCTION COST

( 9x5000) 45000

VARIABLE 10% OF SALES

REVENUE 42750 252750

LESS: DIRECT LABOUR (15x500) 7500

DIRECT MATRIAL ( 18x500) 9000

VARIABLE PROD (9x500) 4500 -21000

CONTRIBUTION 195750 195750

LESS: FIXED EXPENSES

(180000/4) -45000

PROFIT FOR THE YEAR 150750 150750

(B) Profit statements under absorption costing principles:

Absorption costing- This is a kind of costing system in which fixed and variable costs are taken

as cost of per unit during preparation of income statements (Rankin, Stanton, McGowan,

Ferlauto and Tilling, 2012).

1) 1st quarter gross profit and net profit/ loss:

Income statement by absorption costing method(1st quarter)

PARTICULAR

AMOUNT

(in £)

SALES (4500x95) 427500 427500

COST OF GOOD SOLD -231750

GROSS PROFIT AT NORMAL 195750

UNDER/OVR ABSORPTION 6800

GROSS PROFIT AT ACTUAL 202550

LESS- FIXED EXPENDITURE -45000

NET PROFIT 157550

DIRECT MATERIAL (18x5000) 90000

VARIABLE PRODUCTION COST

( 9x5000) 45000

VARIABLE 10% OF SALES

REVENUE 42750 252750

LESS: DIRECT LABOUR (15x500) 7500

DIRECT MATRIAL ( 18x500) 9000

VARIABLE PROD (9x500) 4500 -21000

CONTRIBUTION 195750 195750

LESS: FIXED EXPENSES

(180000/4) -45000

PROFIT FOR THE YEAR 150750 150750

(B) Profit statements under absorption costing principles:

Absorption costing- This is a kind of costing system in which fixed and variable costs are taken

as cost of per unit during preparation of income statements (Rankin, Stanton, McGowan,

Ferlauto and Tilling, 2012).

1) 1st quarter gross profit and net profit/ loss:

Income statement by absorption costing method(1st quarter)

PARTICULAR

AMOUNT

(in £)

SALES (4500x95) 427500 427500

COST OF GOOD SOLD -231750

GROSS PROFIT AT NORMAL 195750

UNDER/OVR ABSORPTION 6800

GROSS PROFIT AT ACTUAL 202550

LESS- FIXED EXPENDITURE -45000

NET PROFIT 157550

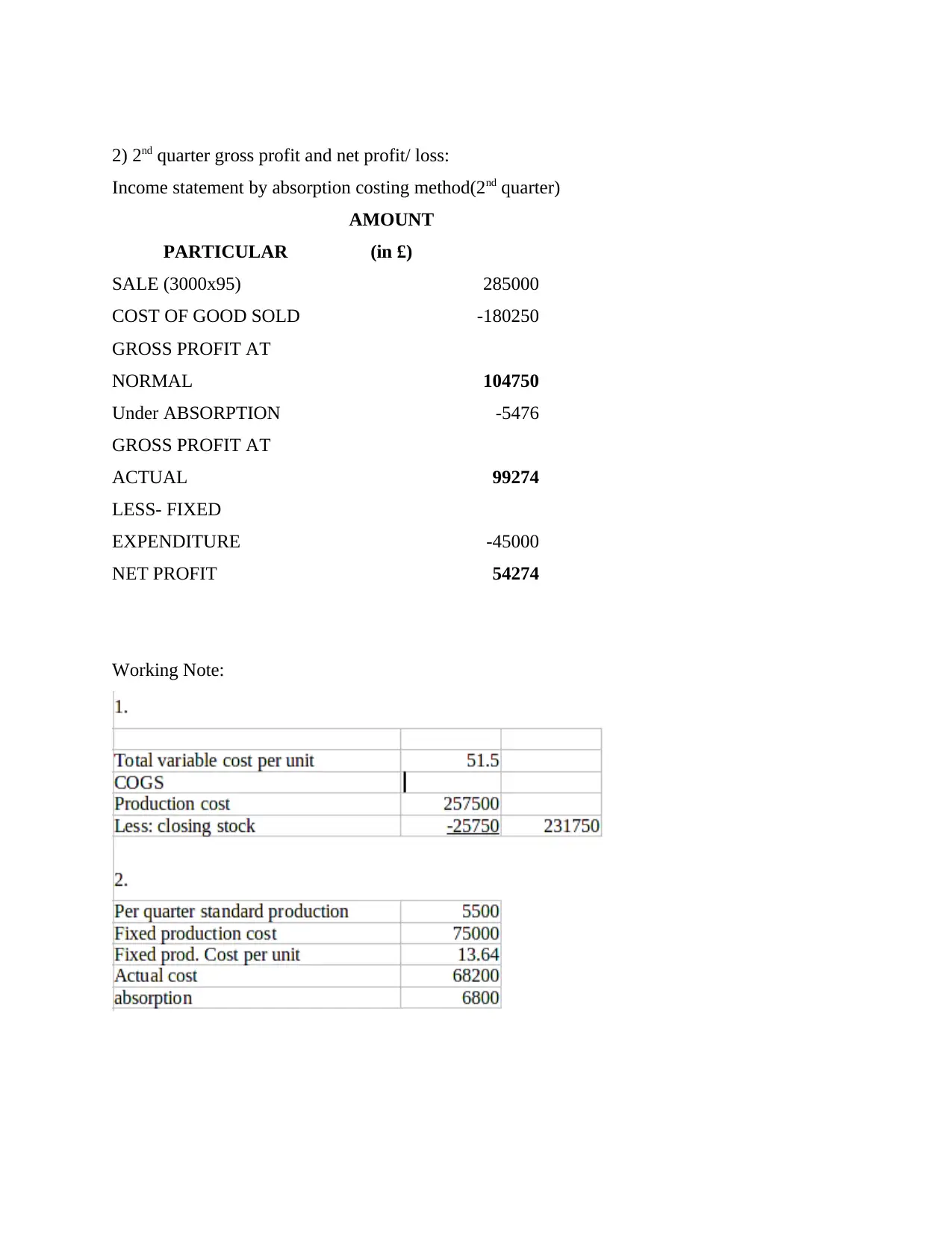

2) 2nd quarter gross profit and net profit/ loss:

Income statement by absorption costing method(2nd quarter)

PARTICULAR

AMOUNT

(in £)

SALE (3000x95) 285000

COST OF GOOD SOLD -180250

GROSS PROFIT AT

NORMAL 104750

Under ABSORPTION -5476

GROSS PROFIT AT

ACTUAL 99274

LESS- FIXED

EXPENDITURE -45000

NET PROFIT 54274

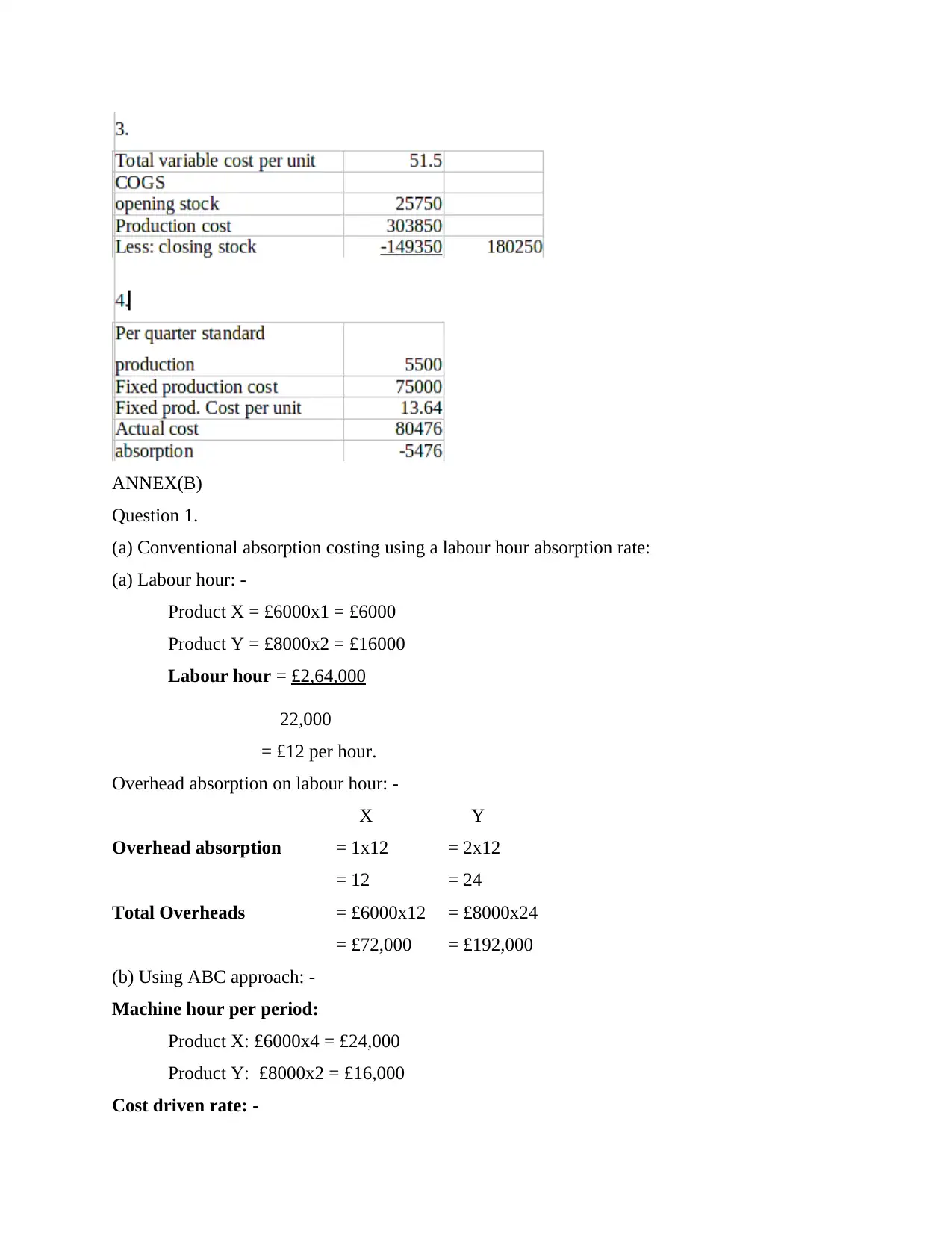

Working Note:

Income statement by absorption costing method(2nd quarter)

PARTICULAR

AMOUNT

(in £)

SALE (3000x95) 285000

COST OF GOOD SOLD -180250

GROSS PROFIT AT

NORMAL 104750

Under ABSORPTION -5476

GROSS PROFIT AT

ACTUAL 99274

LESS- FIXED

EXPENDITURE -45000

NET PROFIT 54274

Working Note:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ANNEX(B)

Question 1.

(a) Conventional absorption costing using a labour hour absorption rate:

(a) Labour hour: -

Product X = £6000x1 = £6000

Product Y = £8000x2 = £16000

Labour hour = £2,64,000

22,000

= £12 per hour.

Overhead absorption on labour hour: -

X Y

Overhead absorption = 1x12 = 2x12

= 12 = 24

Total Overheads = £6000x12 = £8000x24

= £72,000 = £192,000

(b) Using ABC approach: -

Machine hour per period:

Product X: £6000x4 = £24,000

Product Y: £8000x2 = £16,000

Cost driven rate: -

Question 1.

(a) Conventional absorption costing using a labour hour absorption rate:

(a) Labour hour: -

Product X = £6000x1 = £6000

Product Y = £8000x2 = £16000

Labour hour = £2,64,000

22,000

= £12 per hour.

Overhead absorption on labour hour: -

X Y

Overhead absorption = 1x12 = 2x12

= 12 = 24

Total Overheads = £6000x12 = £8000x24

= £72,000 = £192,000

(b) Using ABC approach: -

Machine hour per period:

Product X: £6000x4 = £24,000

Product Y: £8000x2 = £16,000

Cost driven rate: -

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

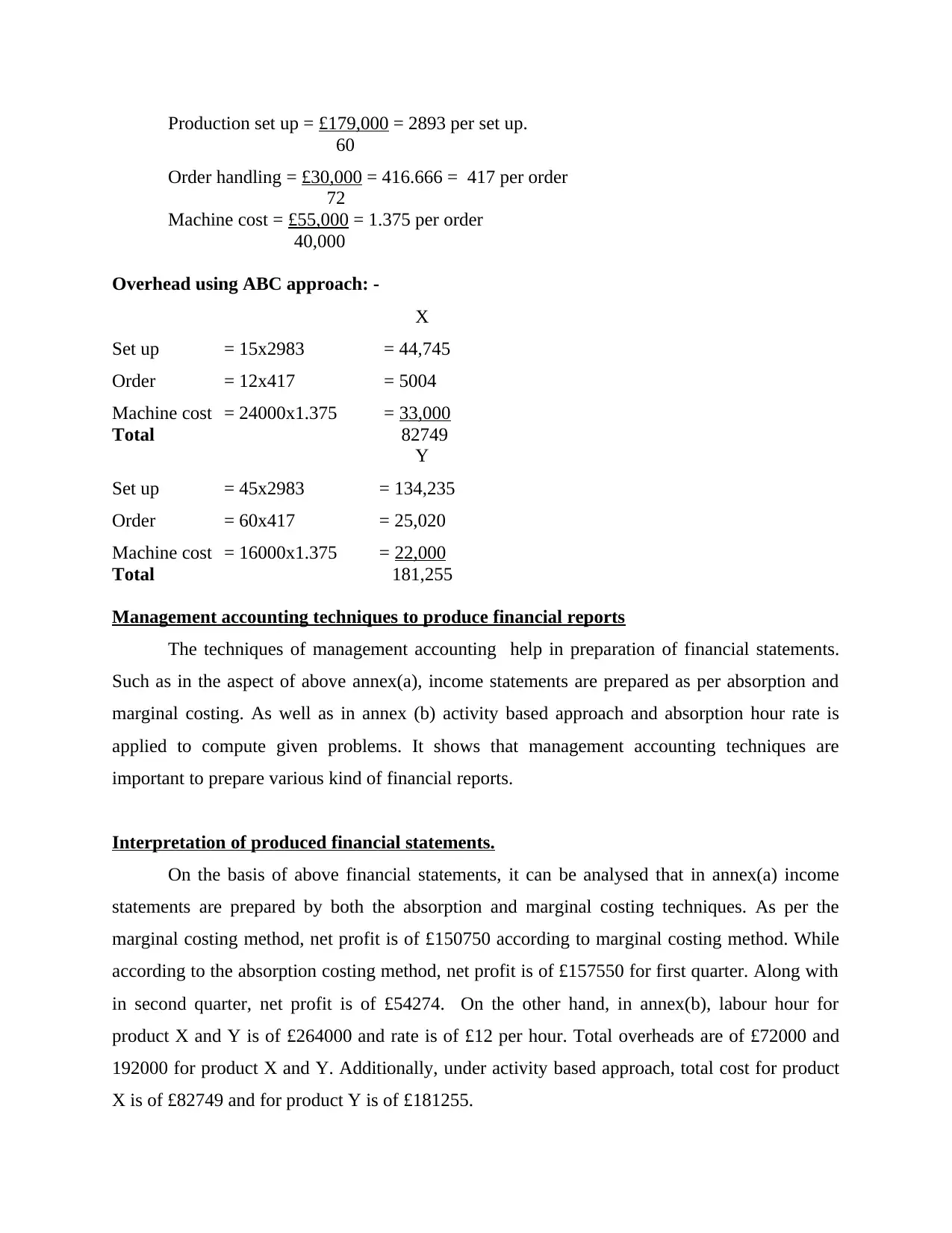

Production set up = £179,000 = 2893 per set up.

60

Order handling = £30,000 = 416.666 = 417 per order

72

Machine cost = £55,000 = 1.375 per order

40,000

Overhead using ABC approach: -

X

Set up = 15x2983 = 44,745

Order = 12x417 = 5004

Machine cost = 24000x1.375 = 33,000

Total 82749

Y

Set up = 45x2983 = 134,235

Order = 60x417 = 25,020

Machine cost = 16000x1.375 = 22,000

Total 181,255

Management accounting techniques to produce financial reports

The techniques of management accounting help in preparation of financial statements.

Such as in the aspect of above annex(a), income statements are prepared as per absorption and

marginal costing. As well as in annex (b) activity based approach and absorption hour rate is

applied to compute given problems. It shows that management accounting techniques are

important to prepare various kind of financial reports.

Interpretation of produced financial statements.

On the basis of above financial statements, it can be analysed that in annex(a) income

statements are prepared by both the absorption and marginal costing techniques. As per the

marginal costing method, net profit is of £150750 according to marginal costing method. While

according to the absorption costing method, net profit is of £157550 for first quarter. Along with

in second quarter, net profit is of £54274. On the other hand, in annex(b), labour hour for

product X and Y is of £264000 and rate is of £12 per hour. Total overheads are of £72000 and

192000 for product X and Y. Additionally, under activity based approach, total cost for product

X is of £82749 and for product Y is of £181255.

60

Order handling = £30,000 = 416.666 = 417 per order

72

Machine cost = £55,000 = 1.375 per order

40,000

Overhead using ABC approach: -

X

Set up = 15x2983 = 44,745

Order = 12x417 = 5004

Machine cost = 24000x1.375 = 33,000

Total 82749

Y

Set up = 45x2983 = 134,235

Order = 60x417 = 25,020

Machine cost = 16000x1.375 = 22,000

Total 181,255

Management accounting techniques to produce financial reports

The techniques of management accounting help in preparation of financial statements.

Such as in the aspect of above annex(a), income statements are prepared as per absorption and

marginal costing. As well as in annex (b) activity based approach and absorption hour rate is

applied to compute given problems. It shows that management accounting techniques are

important to prepare various kind of financial reports.

Interpretation of produced financial statements.

On the basis of above financial statements, it can be analysed that in annex(a) income

statements are prepared by both the absorption and marginal costing techniques. As per the

marginal costing method, net profit is of £150750 according to marginal costing method. While

according to the absorption costing method, net profit is of £157550 for first quarter. Along with

in second quarter, net profit is of £54274. On the other hand, in annex(b), labour hour for

product X and Y is of £264000 and rate is of £12 per hour. Total overheads are of £72000 and

192000 for product X and Y. Additionally, under activity based approach, total cost for product

X is of £82749 and for product Y is of £181255.

ACTIVITY 2

PART (A)

Benefits and drawbacks of planning tools.

The budgetary control is a kind of technique which manages the financial progress of

companies as per setting different kind of budgets. In general, budgetary control consists a wide

range of planning tools such as cash budget, capital, static, variable budget etc. Herein, below

some planning tools of budgetary control are mentioned that are as follows:

Capital budget- It is a kind of budget which provide guidance to companies for making

long term investment as well as assess the effectiveness of huge capitalized projects.

Such as the BAM construction company deals in large construction projects and for them

this budget is very crucial. This is so because as per it, they evaluate the effectiveness of

large capital invested projects. As well as they take decisions about investment in large

projects according to this budget.

Advantage- It is beneficial for companies in understanding the different kind of risks

which involves in any project. Due to this organisations can make profitable decisions.

Disadvantage- This budget makes an estimation of future risks of investments but

sometimes estimation can be wrong. It is so because future is uncertain and any change in

economic condition can make estimation totally wrong.

Operating budget- It can be defined as a type of budget that contains completed

information regarding to the estimated revenues and expenses of different operations

(Rieckhof, Bergmann and Guenther, 2015). This budget is prepared by companies for a

particular time segment. In the context of above selected civil engineering company,

BAM construction limited they allocate their financial resources in different construction

projects as per the projection done by this budget.

Advantage- This budget is helpful for proper management of current expenditures and

income. Along with it is important for creating financial reserves from profits which

exceeds the budgeted limit.

Disadvantage- This budget's drawback is that it takes too much time in preparation. As

well as it is not so effective in allocations of expenditure.

Cash budget- This is a budget which includes information related to the activities which

have their link with cash generating and outing (Storey, 2014). With the help of this

PART (A)

Benefits and drawbacks of planning tools.

The budgetary control is a kind of technique which manages the financial progress of

companies as per setting different kind of budgets. In general, budgetary control consists a wide

range of planning tools such as cash budget, capital, static, variable budget etc. Herein, below

some planning tools of budgetary control are mentioned that are as follows:

Capital budget- It is a kind of budget which provide guidance to companies for making

long term investment as well as assess the effectiveness of huge capitalized projects.

Such as the BAM construction company deals in large construction projects and for them

this budget is very crucial. This is so because as per it, they evaluate the effectiveness of

large capital invested projects. As well as they take decisions about investment in large

projects according to this budget.

Advantage- It is beneficial for companies in understanding the different kind of risks

which involves in any project. Due to this organisations can make profitable decisions.

Disadvantage- This budget makes an estimation of future risks of investments but

sometimes estimation can be wrong. It is so because future is uncertain and any change in

economic condition can make estimation totally wrong.

Operating budget- It can be defined as a type of budget that contains completed

information regarding to the estimated revenues and expenses of different operations

(Rieckhof, Bergmann and Guenther, 2015). This budget is prepared by companies for a

particular time segment. In the context of above selected civil engineering company,

BAM construction limited they allocate their financial resources in different construction

projects as per the projection done by this budget.

Advantage- This budget is helpful for proper management of current expenditures and

income. Along with it is important for creating financial reserves from profits which

exceeds the budgeted limit.

Disadvantage- This budget's drawback is that it takes too much time in preparation. As

well as it is not so effective in allocations of expenditure.

Cash budget- This is a budget which includes information related to the activities which

have their link with cash generating and outing (Storey, 2014). With the help of this

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.