Management Accounting Report: Nisa Retail Business Case Study Analysis

VerifiedAdded on 2023/01/12

|16

|4716

|30

Report

AI Summary

This report provides a comprehensive overview of management accounting (MA), its principles, and its role in business decision-making. It defines MA, explores its functions like planning, controlling, and organizing, and then delves into various MA systems such as cost accounting, inventory management, job costing, and price optimization, detailing their benefits. The report further examines different MA reporting methods, including inventory reports, accounts receivable aging reports, budget reports, cost reports, and performance reports, highlighting their significance and integration within an organization. It also discusses various MA techniques like marginal costing, absorption costing, and activity-based costing, providing a detailed analysis of their application. The report uses Nisa, a retail business, as a case study to illustrate the practical application of these concepts and techniques, offering insights into how MA can be used to improve business efficiency and decision-making. Finally, the report highlights the importance of integrating MA systems and reporting for effective business management, ultimately contributing to the sustainable success of an organization.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Management Accounting (MA) is the accounting system. It encompasses the various

facets of accounting with the objective of improving the quality of information provided to the

management. It helps in identifying and analyzing financial information which assist the internal

management team to take effective decisions with respect to planning and exercising control.

Management accounting is very helpful in knowing efficiency of the business on account of

budget, cost related to business operation and allocating resources as the requirement of various

departments. In this report, Nisa is taken as a small organization. It provides help to retailers for

flourishing their business in the retail market by providing quality products all round UK. This

report, present about the role of management accounting (MA), various types of MA systems

along with their benefits. It also includes different methods of reporting and costing techniques

that can be used by management. Along with this, it covers various planning tools which can be

utilized for budgetary control and identifying the ways management handles the financial

problems leading to sustainable success.

Task 1

Definition of management accounting

According IMA, management accounting (MA) can be defined as a profession which the

key personnel’s in the organization to take relevant managerial decision for the business (Malina

ed., 2018). These strategic business decisions are in respect to the planning and controlling of

strategies and providing expertise in financial reporting.”

Principles of Management Accounting

There are two types of principles of management accounting which are discuss below.

Principle of casualty: It enables modelling the cost by establishes the relationship between the

input and output involved in the production (Butterfield, 2016).

Principle of analogy: It governs the user of management accounting information with the ability

reply the knowledge and skills which are gained from the casual relationship like in planning,

what if analysis. It uses inductive and deductive reasoning with future outcomes.

Role and functions of management accounting

Planning: MA helps in establishing Future Plans by providing relevant accounting

information which can be used for or better decision making (Järvinen, J. T., 2016). For

Management Accounting (MA) is the accounting system. It encompasses the various

facets of accounting with the objective of improving the quality of information provided to the

management. It helps in identifying and analyzing financial information which assist the internal

management team to take effective decisions with respect to planning and exercising control.

Management accounting is very helpful in knowing efficiency of the business on account of

budget, cost related to business operation and allocating resources as the requirement of various

departments. In this report, Nisa is taken as a small organization. It provides help to retailers for

flourishing their business in the retail market by providing quality products all round UK. This

report, present about the role of management accounting (MA), various types of MA systems

along with their benefits. It also includes different methods of reporting and costing techniques

that can be used by management. Along with this, it covers various planning tools which can be

utilized for budgetary control and identifying the ways management handles the financial

problems leading to sustainable success.

Task 1

Definition of management accounting

According IMA, management accounting (MA) can be defined as a profession which the

key personnel’s in the organization to take relevant managerial decision for the business (Malina

ed., 2018). These strategic business decisions are in respect to the planning and controlling of

strategies and providing expertise in financial reporting.”

Principles of Management Accounting

There are two types of principles of management accounting which are discuss below.

Principle of casualty: It enables modelling the cost by establishes the relationship between the

input and output involved in the production (Butterfield, 2016).

Principle of analogy: It governs the user of management accounting information with the ability

reply the knowledge and skills which are gained from the casual relationship like in planning,

what if analysis. It uses inductive and deductive reasoning with future outcomes.

Role and functions of management accounting

Planning: MA helps in establishing Future Plans by providing relevant accounting

information which can be used for or better decision making (Järvinen, J. T., 2016). For

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

example, which product to be sold and at what price. It also helps in evaluating capital

expenditure.

Controlling: In this comparison is drawn by comparing the actual performance with the

budgeted ones (Biondi and et.al, 2017). It helps in evaluating and warning the manager about the

activities which are not according to the plan.

Organizing: Management Accounting performs various functions which helps the

manager for properly coordinating and regulating the different business activities in an

organization.

Various types of management accounting (MA) system and its essentials

MA refers to the accounting system which is deployed by the organization with the

objective to systematically manage the business information which will be helpful to the

management in making better and improved decisions. Different types of Management

Accounting system (MA) stated below.

Cost accounting system

In this MA system, various aspects of costs are considered. Generally this method is

adopted in the organizations which are required to ascertain the inventory cost startup cost along

with the measures to control it (Weetman, 2019). This framework works by following the

material when it experiences various phases of production process. For instance, when the raw

material moves from one phase to second phase, the cost accounting framework tracks the

advancement and updates the equivalent on the mechanized framework. The essential

requirement of this system is to manage the cost structure of the business.

Benefits:

Cost accounting system assists in recognizing the productive and non - beneficial

exercises of the business.

The information furnished about the expense related with various procedures aids future

arranging.

This framework likewise helps in deciding the benefit or loss of the item occasionally.

Cost bookkeeping framework helps in practicing power over the material and different

business supplies.

Inventory management system

expenditure.

Controlling: In this comparison is drawn by comparing the actual performance with the

budgeted ones (Biondi and et.al, 2017). It helps in evaluating and warning the manager about the

activities which are not according to the plan.

Organizing: Management Accounting performs various functions which helps the

manager for properly coordinating and regulating the different business activities in an

organization.

Various types of management accounting (MA) system and its essentials

MA refers to the accounting system which is deployed by the organization with the

objective to systematically manage the business information which will be helpful to the

management in making better and improved decisions. Different types of Management

Accounting system (MA) stated below.

Cost accounting system

In this MA system, various aspects of costs are considered. Generally this method is

adopted in the organizations which are required to ascertain the inventory cost startup cost along

with the measures to control it (Weetman, 2019). This framework works by following the

material when it experiences various phases of production process. For instance, when the raw

material moves from one phase to second phase, the cost accounting framework tracks the

advancement and updates the equivalent on the mechanized framework. The essential

requirement of this system is to manage the cost structure of the business.

Benefits:

Cost accounting system assists in recognizing the productive and non - beneficial

exercises of the business.

The information furnished about the expense related with various procedures aids future

arranging.

This framework likewise helps in deciding the benefit or loss of the item occasionally.

Cost bookkeeping framework helps in practicing power over the material and different

business supplies.

Inventory management system

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inventory management system is a system conveyed by the organization with the goal to

direct the observing and upkeep of the stock of the items independent of whether those are raw

materials, completed products or under progress products. This framework gives a unified

database capacity to create pertinent reports, compelling administration of stock and furthermore

in future determining of the equivalent (Tirinato and et.al, 2018). In case of large manufacturing

organizations, having complex production network and procedures, this framework will be

exceptionally useful in dealing with the stock overabundances along with times of deficiencies.

This system is extremely fundamental for varied organizations independent of size. It helps in

deciding the correct time to put in the request and putting away and expecting cost and

additionally it helps in distinguishing what add up to be bought and at what value which some of

the time turns into the perplexing procedure. Implementation of this system is very essential for

the organizations for effectively and efficiently handling the stock of the product and materials.

Benefits:

This system works on maintaining a strategic distance from the circumstance of

unavailable or overabundance stock.

Improved business exchanges with the providers and sellers which results into profiting

the business.

It likewise helps the organizations in timely placing the order for the supplies required.

This system additionally assists in carry out projections about the future patterns.

Job costing system

This MA system is most appropriate for circumstances where products are created

according to the determination and request given by the client for instance, the boat maker will

like to know the cost of each boat delivered. This system involves the process of collecting all

the pertinent data identified with cost with a particular job work (Weygandt and et.al, 2018). It

empowers the organization in providing the cost estimate of the item with a sensible benefit. It

quantifies all the immediate and roundabout expense in association with the specific job. It

empowers the organization in making right decisions concerning cost. This strategy is extremely

essential for the organizations where various items are delivered which are adequately unique in

relation to one another with a noteworthy expense. This method is essential for determining the

cost and profits related to various activities.

Benefits:

direct the observing and upkeep of the stock of the items independent of whether those are raw

materials, completed products or under progress products. This framework gives a unified

database capacity to create pertinent reports, compelling administration of stock and furthermore

in future determining of the equivalent (Tirinato and et.al, 2018). In case of large manufacturing

organizations, having complex production network and procedures, this framework will be

exceptionally useful in dealing with the stock overabundances along with times of deficiencies.

This system is extremely fundamental for varied organizations independent of size. It helps in

deciding the correct time to put in the request and putting away and expecting cost and

additionally it helps in distinguishing what add up to be bought and at what value which some of

the time turns into the perplexing procedure. Implementation of this system is very essential for

the organizations for effectively and efficiently handling the stock of the product and materials.

Benefits:

This system works on maintaining a strategic distance from the circumstance of

unavailable or overabundance stock.

Improved business exchanges with the providers and sellers which results into profiting

the business.

It likewise helps the organizations in timely placing the order for the supplies required.

This system additionally assists in carry out projections about the future patterns.

Job costing system

This MA system is most appropriate for circumstances where products are created

according to the determination and request given by the client for instance, the boat maker will

like to know the cost of each boat delivered. This system involves the process of collecting all

the pertinent data identified with cost with a particular job work (Weygandt and et.al, 2018). It

empowers the organization in providing the cost estimate of the item with a sensible benefit. It

quantifies all the immediate and roundabout expense in association with the specific job. It

empowers the organization in making right decisions concerning cost. This strategy is extremely

essential for the organizations where various items are delivered which are adequately unique in

relation to one another with a noteworthy expense. This method is essential for determining the

cost and profits related to various activities.

Benefits:

It assists in providing detailed analysis of different cost which helps in deciding the

operational productivity of the business.

It determines the cost more precisely which encourages cost control by contrasting

planned and the actual results.

It gives the organization a premise to estimate the cost of the similar job that might be

taken up later in the future work jobs.

It additionally helps in distinguishing any waste or imperfections in the production

procedure which empowers the supervisor to take viable steps.

Price optimization system

Price optimization system is the scientific program which utilizes different computations

to decide the cost of the item. It determines the change in price with respect to change in the

level of demand (Simon and Fassnacht, 2019). This system additionally thinks about the

eagerness of the clients to pay for the specific item. This strategy decides the cost of the item that

helps in accomplishing the ideal goals alongside expanding the benefits to the organization. This

system is crucial for deciding the price of the product with respect to its demand.

Benefits:

It helps in analyzing the adjustment in the demand in concern to the change in the price

of the product.

This procedure works on improving the productivity of the business.

It enables the businesses in determining the changing market trends which helps in better

and improved decision taking process.

It streamlines the whole procedure which helps in limiting the manual assignment and

lessens mistakes.

Different methods for MA reporting

Inventory report: This report gives the summary of existing supply of the business. It

gives complete bits of knowledge in regards to the how much stock is there, which thing is

selling speedier and the group wise performance (Zhang and Shi, 2016). It incorporates all record

keeping of all the trade autonomously and monitors every improvement of stock. Taking into

account the information given in the report, helps the business organization in making

projections about the future necessities. It moreover helps in perceiving the any wastage of the

stock and highlights the zones of progress. In this way, it prompts perfect utilization of resources.

operational productivity of the business.

It determines the cost more precisely which encourages cost control by contrasting

planned and the actual results.

It gives the organization a premise to estimate the cost of the similar job that might be

taken up later in the future work jobs.

It additionally helps in distinguishing any waste or imperfections in the production

procedure which empowers the supervisor to take viable steps.

Price optimization system

Price optimization system is the scientific program which utilizes different computations

to decide the cost of the item. It determines the change in price with respect to change in the

level of demand (Simon and Fassnacht, 2019). This system additionally thinks about the

eagerness of the clients to pay for the specific item. This strategy decides the cost of the item that

helps in accomplishing the ideal goals alongside expanding the benefits to the organization. This

system is crucial for deciding the price of the product with respect to its demand.

Benefits:

It helps in analyzing the adjustment in the demand in concern to the change in the price

of the product.

This procedure works on improving the productivity of the business.

It enables the businesses in determining the changing market trends which helps in better

and improved decision taking process.

It streamlines the whole procedure which helps in limiting the manual assignment and

lessens mistakes.

Different methods for MA reporting

Inventory report: This report gives the summary of existing supply of the business. It

gives complete bits of knowledge in regards to the how much stock is there, which thing is

selling speedier and the group wise performance (Zhang and Shi, 2016). It incorporates all record

keeping of all the trade autonomously and monitors every improvement of stock. Taking into

account the information given in the report, helps the business organization in making

projections about the future necessities. It moreover helps in perceiving the any wastage of the

stock and highlights the zones of progress. In this way, it prompts perfect utilization of resources.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Account Receivable Aging report: It is the MA reporting method which is utilized for

managing the income of the business in case goods are sold to the customers on credit. This

report gives the absolute bifurcation of the client’s due balance (H Roy Austin CMA, 2019). This

report is critical as it empowers the organization in perceiving the any issue in the association's

arrangement to process. Apart from this, it likewise permits supervisor in recognizing the

defaulters. In light of this report, arrangement is made for defaulters and if any adjustment in the

credit approach is required, the equivalent is additionally done.

Budget report: the budget report is the formal document that evaluates the income and

expenses of the business for particular period.In this, the actual performance of the business is

evaluated based on the standard set (Cools, Stouthuysen and Van den Abbeele, 2017). In case if

there is any difference in the performance, corrective steps are taken. It also helps in determining

the whether the expenditure is too high so that timely actions can be taken in order to exercise

control over it. The budget differs from year to year and also from one organization to another

mainly because of different organizational objectives and goals.

Cost report: This reporting method demonstrates the different cost elements in the

organization. This report is very helpful for the organizations like Nisa for evaluating the cost

which can help in taking better strategic business decisions (Aleem, Khan and Hamad,

2016).This report also guides the organization in finding ways to improve its efficiency which

will have long run impact on the business.

Performance report: This report is set up for reviewing the performance of the business.

It contemplates entire organization including every single worker independently. In huge

associations, division savvy reports are readied (Hecht, Hobson and Wang, 2016). These reports

are helpful for the association so as to take key business choices concerning the fate of the

association. In light of this reporting method, representatives are remunerated for their

responsibility towards work and the organization and the underperformers are either laid off or

managed in other manner. It gives profound knowledge about the working state of the

organization dependent on its presentation concerning the specific standards. It demonstrates any

flaw in the system which is confining it for accomplishing desired goals. Along these lines, the

job of this report is exceptionally important for any business entity in keeping appropriate

measure of the tactic for achieving the targeted goals.

Integration of MA system and reporting within the organization

managing the income of the business in case goods are sold to the customers on credit. This

report gives the absolute bifurcation of the client’s due balance (H Roy Austin CMA, 2019). This

report is critical as it empowers the organization in perceiving the any issue in the association's

arrangement to process. Apart from this, it likewise permits supervisor in recognizing the

defaulters. In light of this report, arrangement is made for defaulters and if any adjustment in the

credit approach is required, the equivalent is additionally done.

Budget report: the budget report is the formal document that evaluates the income and

expenses of the business for particular period.In this, the actual performance of the business is

evaluated based on the standard set (Cools, Stouthuysen and Van den Abbeele, 2017). In case if

there is any difference in the performance, corrective steps are taken. It also helps in determining

the whether the expenditure is too high so that timely actions can be taken in order to exercise

control over it. The budget differs from year to year and also from one organization to another

mainly because of different organizational objectives and goals.

Cost report: This reporting method demonstrates the different cost elements in the

organization. This report is very helpful for the organizations like Nisa for evaluating the cost

which can help in taking better strategic business decisions (Aleem, Khan and Hamad,

2016).This report also guides the organization in finding ways to improve its efficiency which

will have long run impact on the business.

Performance report: This report is set up for reviewing the performance of the business.

It contemplates entire organization including every single worker independently. In huge

associations, division savvy reports are readied (Hecht, Hobson and Wang, 2016). These reports

are helpful for the association so as to take key business choices concerning the fate of the

association. In light of this reporting method, representatives are remunerated for their

responsibility towards work and the organization and the underperformers are either laid off or

managed in other manner. It gives profound knowledge about the working state of the

organization dependent on its presentation concerning the specific standards. It demonstrates any

flaw in the system which is confining it for accomplishing desired goals. Along these lines, the

job of this report is exceptionally important for any business entity in keeping appropriate

measure of the tactic for achieving the targeted goals.

Integration of MA system and reporting within the organization

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The integration of MA and reporting will help in successfully accomplishing the

organizations goals and targets. It will help the organization in dealing with its business activities

and performance in a precise way with the auspicious accessibility of data. It helps in

determining the areas of progress of the business which will result into increase in the

performance and efficiency level of the entity. This combination will likewise help in appropriate

decision making and provides guidance for effective planning.

Types of MA techniques

There are various types of MA techniques that can be used by the organization Nisa

which will help it in accomplishing the targeted goals. A detailed description is given below.

Marginal costing

It is the most relevant technique for the decision-making purpose. In this accounting

system variable cost are distributed to the unit cost (Labro, 2019). It is a very simple technique

with the purpose of analyzing the cost information and its effect on the profitability with respect

to change in the level of production. The fixed cost for the specific period completely written off

against the total contribution. In UK, marginal costing is very popular. It also helps in identifying

the point after which business starts earning profits, it is also called break-even point which is

different for different levels of activities. It determines the optimum production level with the

least production cost. It is also useful in determining the product pricing when customers are

willing to pay lower price for certain orders.

Absorption costing

This method includes into valuation all the expenses that are incurred in relation to the

cost of production and are thus included the cost of production irrespective of whether it is fixed

cost or variable cost (Geiszler, Baker and Lippitt, 2017). However, in this method the proportion

of fixed overhead expenses is allocated to each unit of the product just like variable

manufacturing cost. This method is widely used since it is required for external financial

reporting such as GAAP and International Financial Reporting Standards (IFRS).

Cost profit volume analysis

This analysis technique is used by the organization for determining how the change in

level of output and cost can impact organization’s income (Lulaj and Iseni, 2018). This technique

is based on certain assumptions such as sales price per unit variable cost per unit and fixed cost

are constant and everything that is produced is sold. The cost profit volume analysis requires to

organizations goals and targets. It will help the organization in dealing with its business activities

and performance in a precise way with the auspicious accessibility of data. It helps in

determining the areas of progress of the business which will result into increase in the

performance and efficiency level of the entity. This combination will likewise help in appropriate

decision making and provides guidance for effective planning.

Types of MA techniques

There are various types of MA techniques that can be used by the organization Nisa

which will help it in accomplishing the targeted goals. A detailed description is given below.

Marginal costing

It is the most relevant technique for the decision-making purpose. In this accounting

system variable cost are distributed to the unit cost (Labro, 2019). It is a very simple technique

with the purpose of analyzing the cost information and its effect on the profitability with respect

to change in the level of production. The fixed cost for the specific period completely written off

against the total contribution. In UK, marginal costing is very popular. It also helps in identifying

the point after which business starts earning profits, it is also called break-even point which is

different for different levels of activities. It determines the optimum production level with the

least production cost. It is also useful in determining the product pricing when customers are

willing to pay lower price for certain orders.

Absorption costing

This method includes into valuation all the expenses that are incurred in relation to the

cost of production and are thus included the cost of production irrespective of whether it is fixed

cost or variable cost (Geiszler, Baker and Lippitt, 2017). However, in this method the proportion

of fixed overhead expenses is allocated to each unit of the product just like variable

manufacturing cost. This method is widely used since it is required for external financial

reporting such as GAAP and International Financial Reporting Standards (IFRS).

Cost profit volume analysis

This analysis technique is used by the organization for determining how the change in

level of output and cost can impact organization’s income (Lulaj and Iseni, 2018). This technique

is based on certain assumptions such as sales price per unit variable cost per unit and fixed cost

are constant and everything that is produced is sold. The cost profit volume analysis requires to

have all the cost including production and selling and administration cost which are divided into

fixed and variable.

Applying a range of MA techniques and producing appropriate financial reporting

documents

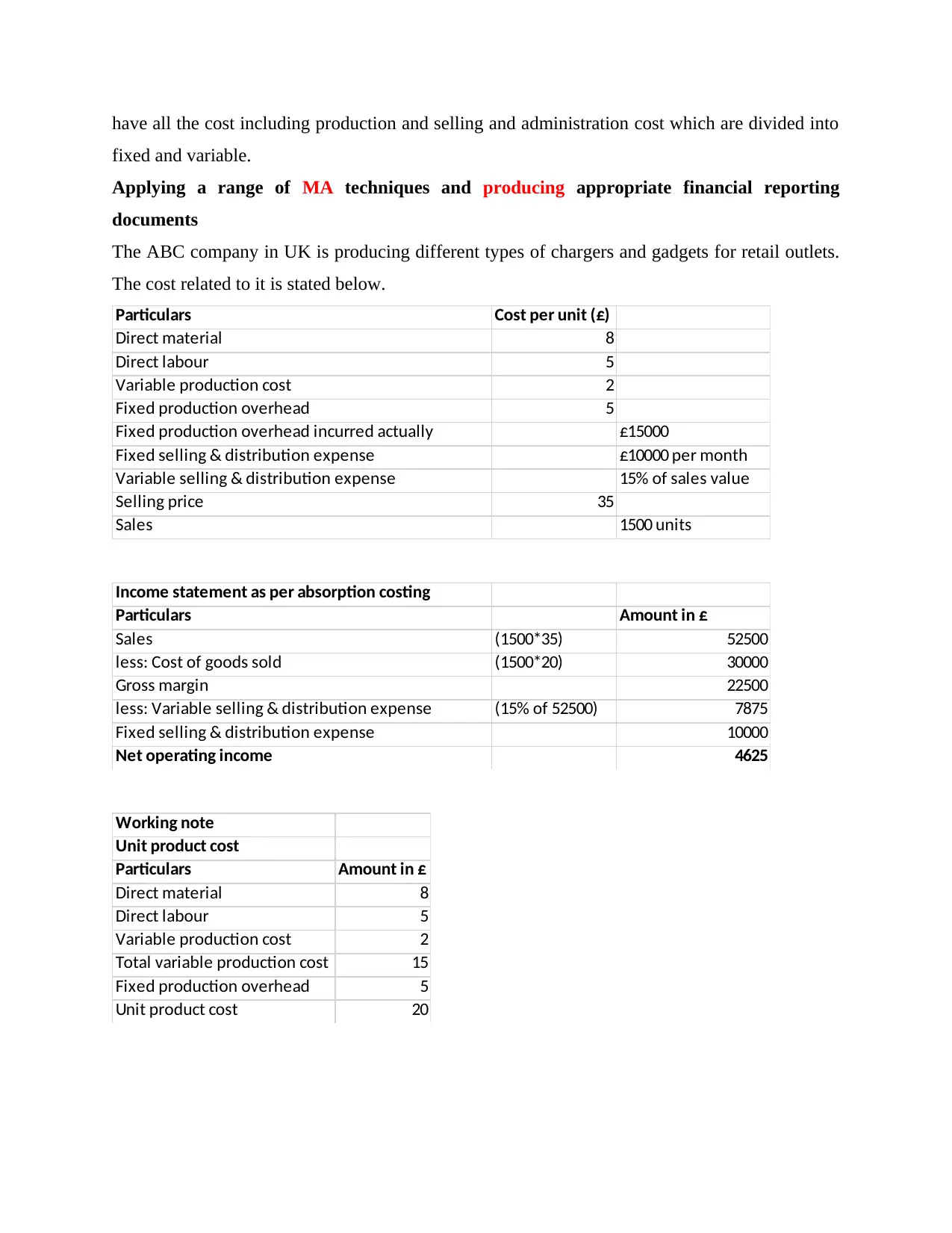

The ABC company in UK is producing different types of chargers and gadgets for retail outlets.

The cost related to it is stated below.

Particulars Cost per unit (£)

Direct material 8

Direct labour 5

Variable production cost 2

Fixed production overhead 5

Fixed production overhead incurred actually £15000

Fixed selling & distribution expense £10000 per month

Variable selling & distribution expense 15% of sales value

Selling price 35

Sales 1500 units

Income statement as per absorption costing

Particulars Amount in £

Sales (1500*35) 52500

less: Cost of goods sold (1500*20) 30000

Gross margin 22500

less: Variable selling & distribution expense (15% of 52500) 7875

Fixed selling & distribution expense 10000

Net operating income 4625

Working note

Unit product cost

Particulars Amount in £

Direct material 8

Direct labour 5

Variable production cost 2

Total variable production cost 15

Fixed production overhead 5

Unit product cost 20

fixed and variable.

Applying a range of MA techniques and producing appropriate financial reporting

documents

The ABC company in UK is producing different types of chargers and gadgets for retail outlets.

The cost related to it is stated below.

Particulars Cost per unit (£)

Direct material 8

Direct labour 5

Variable production cost 2

Fixed production overhead 5

Fixed production overhead incurred actually £15000

Fixed selling & distribution expense £10000 per month

Variable selling & distribution expense 15% of sales value

Selling price 35

Sales 1500 units

Income statement as per absorption costing

Particulars Amount in £

Sales (1500*35) 52500

less: Cost of goods sold (1500*20) 30000

Gross margin 22500

less: Variable selling & distribution expense (15% of 52500) 7875

Fixed selling & distribution expense 10000

Net operating income 4625

Working note

Unit product cost

Particulars Amount in £

Direct material 8

Direct labour 5

Variable production cost 2

Total variable production cost 15

Fixed production overhead 5

Unit product cost 20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

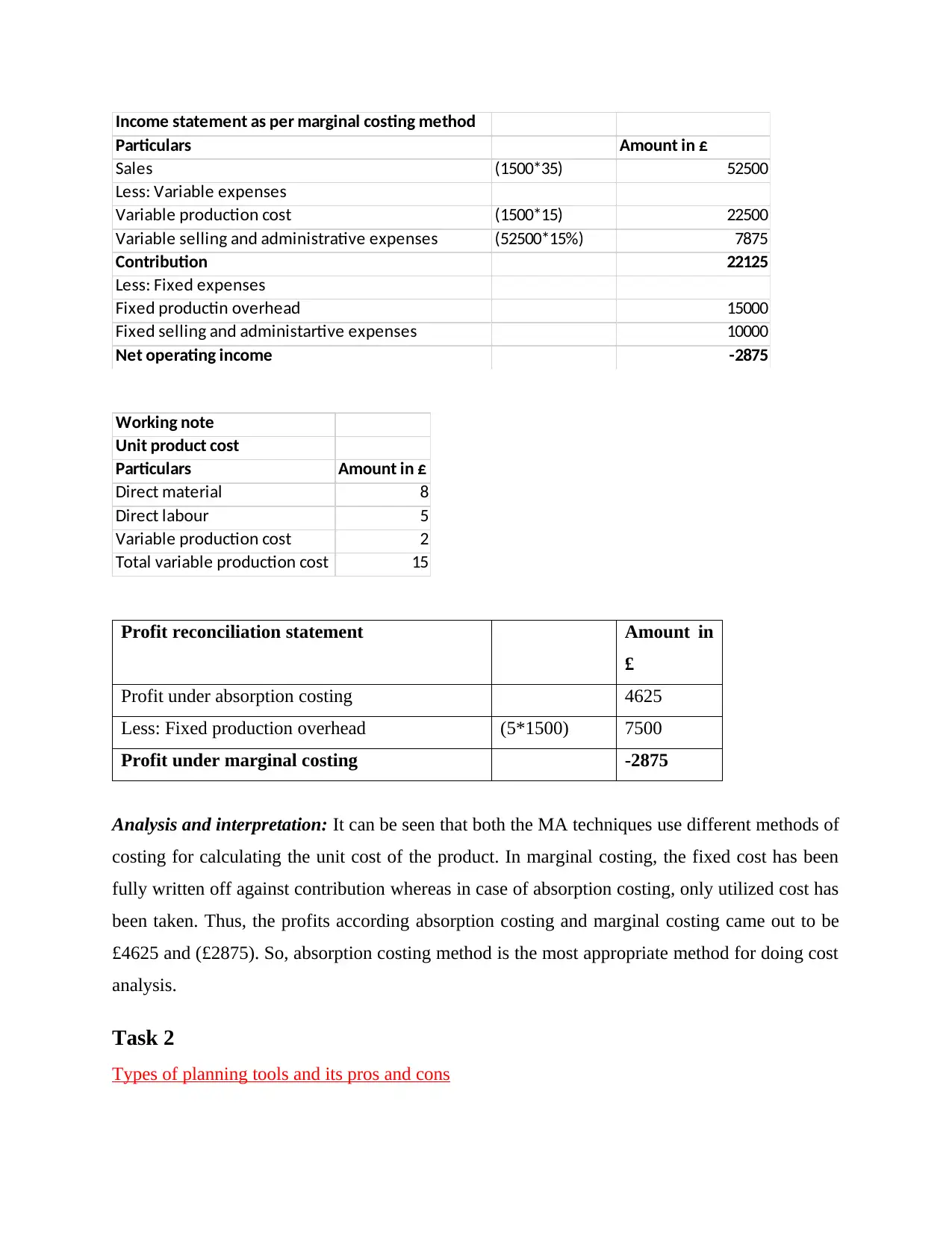

Income statement as per marginal costing method

Particulars Amount in £

Sales (1500*35) 52500

Less: Variable expenses

Variable production cost (1500*15) 22500

Variable selling and administrative expenses (52500*15%) 7875

Contribution 22125

Less: Fixed expenses

Fixed productin overhead 15000

Fixed selling and administartive expenses 10000

Net operating income -2875

Working note

Unit product cost

Particulars Amount in £

Direct material 8

Direct labour 5

Variable production cost 2

Total variable production cost 15

Profit reconciliation statement Amount in

£

Profit under absorption costing 4625

Less: Fixed production overhead (5*1500) 7500

Profit under marginal costing -2875

Analysis and interpretation: It can be seen that both the MA techniques use different methods of

costing for calculating the unit cost of the product. In marginal costing, the fixed cost has been

fully written off against contribution whereas in case of absorption costing, only utilized cost has

been taken. Thus, the profits according absorption costing and marginal costing came out to be

£4625 and (£2875). So, absorption costing method is the most appropriate method for doing cost

analysis.

Task 2

Types of planning tools and its pros and cons

Particulars Amount in £

Sales (1500*35) 52500

Less: Variable expenses

Variable production cost (1500*15) 22500

Variable selling and administrative expenses (52500*15%) 7875

Contribution 22125

Less: Fixed expenses

Fixed productin overhead 15000

Fixed selling and administartive expenses 10000

Net operating income -2875

Working note

Unit product cost

Particulars Amount in £

Direct material 8

Direct labour 5

Variable production cost 2

Total variable production cost 15

Profit reconciliation statement Amount in

£

Profit under absorption costing 4625

Less: Fixed production overhead (5*1500) 7500

Profit under marginal costing -2875

Analysis and interpretation: It can be seen that both the MA techniques use different methods of

costing for calculating the unit cost of the product. In marginal costing, the fixed cost has been

fully written off against contribution whereas in case of absorption costing, only utilized cost has

been taken. Thus, the profits according absorption costing and marginal costing came out to be

£4625 and (£2875). So, absorption costing method is the most appropriate method for doing cost

analysis.

Task 2

Types of planning tools and its pros and cons

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Budgeting is basically the planning of future operations by adequate allocation of funds

and resources among different departments. Budgeting refers to making forecast about the future

incomes and expenses of the company. this helps the business in keeping control over the costs

and expenses in the business. Budgeting helps the business in measuring variances between the

real and standard figures and taking corrective measures for reducing the variances. The various

forms of tools that can be used by the organisation are

Zero based Budgeting

It refers to the budgeting technique that do not consider the budgets of previous year in

the preparation of budget for current year. The entire budget is prepared after proper research and

analysis related to the budget. In this budget the errors and mistakes of previous budgets are not

carried forward in the budgets for current. This helps the business in framing more accurate

budgets with least variances as everything is started from the fresh (Hopper and Bui, 2016).

Justification is not required to be give for every item like the traditional budgeting method as

every item is inserted after research and its influence.

Advantages

ZBB do not consider previous budgets.

Research is done every time the budget is prepared.

More relevant for products prone to frequent changes.

Disadvantages

It is time consuming process.

Zero based budget are expensive to implement in enterprise.

Activity Based Budgeting

It is the budgeting method in which the organisation prepares budgets on the basis of

activities rather than the departments. The budgets are prepared on the basis of making forecast

of resources to be used and productivity generated under activity. The budgeting technique do

not use the budgets prepared for previous year for the preparation of current budget. It helps the

enterprise in identifying the costs and expenditures associated with the each activity being

performed in the production process of the enterprise. Activity based budgets helps the business

in identifying the loopholes of costs and wastages and according the companies take corrective

measures.

Advantages

and resources among different departments. Budgeting refers to making forecast about the future

incomes and expenses of the company. this helps the business in keeping control over the costs

and expenses in the business. Budgeting helps the business in measuring variances between the

real and standard figures and taking corrective measures for reducing the variances. The various

forms of tools that can be used by the organisation are

Zero based Budgeting

It refers to the budgeting technique that do not consider the budgets of previous year in

the preparation of budget for current year. The entire budget is prepared after proper research and

analysis related to the budget. In this budget the errors and mistakes of previous budgets are not

carried forward in the budgets for current. This helps the business in framing more accurate

budgets with least variances as everything is started from the fresh (Hopper and Bui, 2016).

Justification is not required to be give for every item like the traditional budgeting method as

every item is inserted after research and its influence.

Advantages

ZBB do not consider previous budgets.

Research is done every time the budget is prepared.

More relevant for products prone to frequent changes.

Disadvantages

It is time consuming process.

Zero based budget are expensive to implement in enterprise.

Activity Based Budgeting

It is the budgeting method in which the organisation prepares budgets on the basis of

activities rather than the departments. The budgets are prepared on the basis of making forecast

of resources to be used and productivity generated under activity. The budgeting technique do

not use the budgets prepared for previous year for the preparation of current budget. It helps the

enterprise in identifying the costs and expenditures associated with the each activity being

performed in the production process of the enterprise. Activity based budgets helps the business

in identifying the loopholes of costs and wastages and according the companies take corrective

measures.

Advantages

Activity based budgeting is easy to implement.

Help the enterprise in identifying the variations in production process.

Budgets are prepared new without considering previous budgets.

Disadvantages

It requires professional knowledge to make activity based budgets.

It is expensive process for implementation,

Operational Budgets

Operational budgets refers to the budgets prepared for the operating activities of the

organisation. It involves forecasting the future income and expenses of the enterprise based on

the previous trends. The operational budgets considers budgets of last year for preparing budgets

for current year(Otley, 2016). It helps the organisation in proper allocation of resources between

the different departments and various business operations.

Advantages

Operational budgets are easy and simple to prepare.

Adequate allocation of resources of company.

It helps in controlling the costs and expenses by giving defined spending plan.

Disadvantages

It is prepared over the budgets of previous year.

It is not possible to make accurate forecast about the future activities.

Comparing the organisations adapting MA systems for responding to its financial problems

With the new evolving businesses where information is considered the most important

with respect to measuring the performance of the business. The budgetary control methods that

can be used for identifying the financial problems is described below.

Benchmarking

It is the metrics used for checking the performance of the organization with other firm

within the industry. Benchmarking has some standards based on which performance can be

assessed like expense of per unit items produced, working pattern of the item and so forth(Agrell

and Bogetoft, 2018). The actual performance is compared to the competitor best in industry and

discover deviation between the two. It helps organization in recognizing the zone of progress and

what makes the different business prevalent. Money related benchmarking encourages

Help the enterprise in identifying the variations in production process.

Budgets are prepared new without considering previous budgets.

Disadvantages

It requires professional knowledge to make activity based budgets.

It is expensive process for implementation,

Operational Budgets

Operational budgets refers to the budgets prepared for the operating activities of the

organisation. It involves forecasting the future income and expenses of the enterprise based on

the previous trends. The operational budgets considers budgets of last year for preparing budgets

for current year(Otley, 2016). It helps the organisation in proper allocation of resources between

the different departments and various business operations.

Advantages

Operational budgets are easy and simple to prepare.

Adequate allocation of resources of company.

It helps in controlling the costs and expenses by giving defined spending plan.

Disadvantages

It is prepared over the budgets of previous year.

It is not possible to make accurate forecast about the future activities.

Comparing the organisations adapting MA systems for responding to its financial problems

With the new evolving businesses where information is considered the most important

with respect to measuring the performance of the business. The budgetary control methods that

can be used for identifying the financial problems is described below.

Benchmarking

It is the metrics used for checking the performance of the organization with other firm

within the industry. Benchmarking has some standards based on which performance can be

assessed like expense of per unit items produced, working pattern of the item and so forth(Agrell

and Bogetoft, 2018). The actual performance is compared to the competitor best in industry and

discover deviation between the two. It helps organization in recognizing the zone of progress and

what makes the different business prevalent. Money related benchmarking encourages

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.