Management Accounting: Techniques, Systems, and Financial Reporting

VerifiedAdded on 2020/06/04

|17

|5561

|36

Report

AI Summary

This report delves into the realm of management accounting, exploring its core concepts and diverse applications within organizations. It begins by defining management accounting and outlining its essential requirements, differentiating between various types such as cost accounting, financial management, and inventory management systems. The report then examines different methods of management accounting reporting, including budgetary reports, cost reports, and performance reports, emphasizing their role in providing crucial financial insights to managers. Furthermore, it assesses the benefits of management accounting systems in organizational contexts, highlighting their contribution to cost reduction, improved financial planning, and strategic decision-making. The report also investigates cost approaches to prepare income statements, and analyzes different types of planning tools, such as budgetary control, and their advantages and disadvantages. Finally, the report analyzes how organizations adapt management accounting systems to address financial problems and achieve their strategic goals, offering a comprehensive overview of the subject.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and essential requirements of its different types..........................1

P2 Various type of methods of management accounting reporting............................................4

M1 Measurement the benefits of management accounting systems used in organisational

context.........................................................................................................................................5

D1 Management accounting system and management accounting reporting.............................5

TASK 2............................................................................................................................................6

P3 Calculation of cost approaches to prepare income statement................................................6

M2 Using the wide range of management accounting techniques..............................................8

D2 Financial reports properly applied in organisation and interpret data of organisation..........8

TASK 3............................................................................................................................................8

P4 Advantages and disadvantages of different types of planning tools for budgetary control...8

M3 Analysing the use various type planning tools and their application for preparing budget

...................................................................................................................................................10

D3 How planning tools helps to solve the financial problems..................................................10

TASK 4..........................................................................................................................................11

P5 Compare how organisations are adapting management accounting system........................11

M4 how management accounting helps to managed financial problems to lead the

organisation...............................................................................................................................11

CONCLUSION .............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and essential requirements of its different types..........................1

P2 Various type of methods of management accounting reporting............................................4

M1 Measurement the benefits of management accounting systems used in organisational

context.........................................................................................................................................5

D1 Management accounting system and management accounting reporting.............................5

TASK 2............................................................................................................................................6

P3 Calculation of cost approaches to prepare income statement................................................6

M2 Using the wide range of management accounting techniques..............................................8

D2 Financial reports properly applied in organisation and interpret data of organisation..........8

TASK 3............................................................................................................................................8

P4 Advantages and disadvantages of different types of planning tools for budgetary control...8

M3 Analysing the use various type planning tools and their application for preparing budget

...................................................................................................................................................10

D3 How planning tools helps to solve the financial problems..................................................10

TASK 4..........................................................................................................................................11

P5 Compare how organisations are adapting management accounting system........................11

M4 how management accounting helps to managed financial problems to lead the

organisation...............................................................................................................................11

CONCLUSION .............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Accounting concept and methods have been mould as per the requirement and nature of

business. Management accounting is a concept used to maintain discipline and ethical manner in

operations (Baldvinsdottir, Mitchell and Nørreklit, 2010). Phenomenon of management and

accounting has become modern and are implemented in organisations as per the nature of their

administration and operation type. This report describes the meaning of management accounting

and various types of its tools used by organisation. Integration of direction accounting system

and management accounting reporting are also defined in this context. Absorption and marginal

costing techniques are explained in respect of evaluating the profit. Different types of planning

tools are defined subjected to make budgets and do strategic planning. Advantages and

disadvantages of planning tools are explained here as well. Importance of management

accounting is defined in respect of resolving the issues and problems associated with financial

planning. It is tried to connect the financial problems with management accounting.

TASK 1

P1. Management accounting and essential requirements of its different types

As per the definition given by IMA (Institute of Management Accountants), a

professional manner of keeping records, transactions and tracking of financial information are

considered as management accounting. The accounting system which remains essential in

respect of decision making, planning and performance management is considered in management

accounting. The accounting procedure and system remain important form the management point

of view are known as managerial accounting. Management accounting system provides a path to

achieve the core competence in task and helps to attain the desired goals in given deadline.

A system which provides a medium and tools to operate the management and operations

to keep the accounting records, financial information and forecasting plans in a proper manner is

also considered as management accounting (Herzig, Viere, and Burritt, 2012). An effective

management accounting system is the key to develop a strong organisational structure and

sustainable growth. It helps the managers and accountants to prepare the financial statements and

annual reports. These information are useful for the stake holders, shareholders, financial

institutions, banks and owners of company.

1

Accounting concept and methods have been mould as per the requirement and nature of

business. Management accounting is a concept used to maintain discipline and ethical manner in

operations (Baldvinsdottir, Mitchell and Nørreklit, 2010). Phenomenon of management and

accounting has become modern and are implemented in organisations as per the nature of their

administration and operation type. This report describes the meaning of management accounting

and various types of its tools used by organisation. Integration of direction accounting system

and management accounting reporting are also defined in this context. Absorption and marginal

costing techniques are explained in respect of evaluating the profit. Different types of planning

tools are defined subjected to make budgets and do strategic planning. Advantages and

disadvantages of planning tools are explained here as well. Importance of management

accounting is defined in respect of resolving the issues and problems associated with financial

planning. It is tried to connect the financial problems with management accounting.

TASK 1

P1. Management accounting and essential requirements of its different types

As per the definition given by IMA (Institute of Management Accountants), a

professional manner of keeping records, transactions and tracking of financial information are

considered as management accounting. The accounting system which remains essential in

respect of decision making, planning and performance management is considered in management

accounting. The accounting procedure and system remain important form the management point

of view are known as managerial accounting. Management accounting system provides a path to

achieve the core competence in task and helps to attain the desired goals in given deadline.

A system which provides a medium and tools to operate the management and operations

to keep the accounting records, financial information and forecasting plans in a proper manner is

also considered as management accounting (Herzig, Viere, and Burritt, 2012). An effective

management accounting system is the key to develop a strong organisational structure and

sustainable growth. It helps the managers and accountants to prepare the financial statements and

annual reports. These information are useful for the stake holders, shareholders, financial

institutions, banks and owners of company.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

There are three types considered in managerial accounting which are commonly used in

organisation. Strategic management, performance and risk management are the branch of

management accounting. To maintain the financial position of organisation at optimum level.

There are various type of management accounting systems are used like:

Cost accounting system: Cost accounting is one of the branches of management

accounting which remains essential and important for manufacturing and production industries.

This accounting system is also known as product costing system or system of accounting

(Lambert and Sponem, 2012). Cost accounting system furnish a structure of analysing the cost of

the product and determine the profit. It is also considered as profitability analysis and evaluate

the amount of stock. It become difficult to determine the cost of product and profitability, in

those organisation which remain align with multiple manufacturing process. Cost accounting

helps to execute the relevant data and bifurcate information which are useful to determine the

cost of product and profitability.

There are basically two major costing approaches divided in organisational context as

process costing and job order costing.

Job order costing: Organisation which operates multiple manufacturing and producing

activities are considered as separate jobs. This costing system bifurcates different the

costs of distinct types of products which are produced through various types of business

process.

Process costing: This cost accounting system is used in large manufacturing and

production firms. There are various types of processes remain associated in the

manufacturing process. Requirement of material, labour and wages are incurred

separately in these processes. This costing system helps to determine the cost of product

at every process. There is separate accounting records are maintained for these type of

manufacturing processes.

Hybrid cost accounting system: Combination of process costing and job costing is

considered as hybrid cost accounting system. In this accounting system, there are certain

elements used from both the accounting systems to evaluate the cost of product. Cost

allocation and annexation of overheads based upon activity based costing system and

traditional accounting system.

2

organisation. Strategic management, performance and risk management are the branch of

management accounting. To maintain the financial position of organisation at optimum level.

There are various type of management accounting systems are used like:

Cost accounting system: Cost accounting is one of the branches of management

accounting which remains essential and important for manufacturing and production industries.

This accounting system is also known as product costing system or system of accounting

(Lambert and Sponem, 2012). Cost accounting system furnish a structure of analysing the cost of

the product and determine the profit. It is also considered as profitability analysis and evaluate

the amount of stock. It become difficult to determine the cost of product and profitability, in

those organisation which remain align with multiple manufacturing process. Cost accounting

helps to execute the relevant data and bifurcate information which are useful to determine the

cost of product and profitability.

There are basically two major costing approaches divided in organisational context as

process costing and job order costing.

Job order costing: Organisation which operates multiple manufacturing and producing

activities are considered as separate jobs. This costing system bifurcates different the

costs of distinct types of products which are produced through various types of business

process.

Process costing: This cost accounting system is used in large manufacturing and

production firms. There are various types of processes remain associated in the

manufacturing process. Requirement of material, labour and wages are incurred

separately in these processes. This costing system helps to determine the cost of product

at every process. There is separate accounting records are maintained for these type of

manufacturing processes.

Hybrid cost accounting system: Combination of process costing and job costing is

considered as hybrid cost accounting system. In this accounting system, there are certain

elements used from both the accounting systems to evaluate the cost of product. Cost

allocation and annexation of overheads based upon activity based costing system and

traditional accounting system.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Traditional cost accounting system uses the applied theories and approaches to determine

the cost to each job and department.

Financial management and risk analysis: This is the accounting system that helps to

analyse the risk factors to determine the cost of product and for enhancing the profitability in

near future (Lukka and Modell, 2010). Risk is defined as a probability and possibility of happen

something wrong. This accounting system helps to analyse the factors and elements which affect

managing and operating skills of managers and organisation. This is a process which helps in

decision making and strategic planning process. It is an important tool used to identify the risk

factors. Managers and accountants become eligible to detect the potential issues and problems

which resist the growth and profitability of organisation. This is one of the complex parts of

managerial accounting. This process is divided in majorly three parts as identifying the risk,

estimated risk and solutions as well as managing the risk. This management system is very useful

for the organisations which deal in equities, shareholding, mutual funds and stock holdings.

Inventory and equity management: Managing the amount of stock and holding properly

and avoid the risk factors from the main objective of this management system. The organisation

which are connected with the business activities as retail sector, delivering the goods and

products from one place to another use this management accounting system (Budgetary control,

2017). It is a process which contains the process of ordering the amount of stock and storing

them in to a storage house using the inventory management system. This accounting system

provides the path to determine the optimum level of inventory to be store in storage house,

purchase order and break down points. Inventories are considered as current assents of an

organisation. There are various type of valuation methods are used under this accounting system

to calculate the cost of inventories. Just in time, material requirement planning, break down

analysis are the part of inventory management accounting system. This accounting helps to

reduce the carrying cost of inventories and prevent the extra cost of retaining the goods in

process.

Trend analysis and forecasting: Changes are the parts of the life and the same rule also

implemented to the business and organisations. This is a system helps to communicate the future

growth and development opportunities to the managers. It is an statistical analysis of customer's

interest and involvement for particular tasks and projects. It is a process of calculating the figures

amount of change in respect of sales of products and services. Customers interest and

3

the cost to each job and department.

Financial management and risk analysis: This is the accounting system that helps to

analyse the risk factors to determine the cost of product and for enhancing the profitability in

near future (Lukka and Modell, 2010). Risk is defined as a probability and possibility of happen

something wrong. This accounting system helps to analyse the factors and elements which affect

managing and operating skills of managers and organisation. This is a process which helps in

decision making and strategic planning process. It is an important tool used to identify the risk

factors. Managers and accountants become eligible to detect the potential issues and problems

which resist the growth and profitability of organisation. This is one of the complex parts of

managerial accounting. This process is divided in majorly three parts as identifying the risk,

estimated risk and solutions as well as managing the risk. This management system is very useful

for the organisations which deal in equities, shareholding, mutual funds and stock holdings.

Inventory and equity management: Managing the amount of stock and holding properly

and avoid the risk factors from the main objective of this management system. The organisation

which are connected with the business activities as retail sector, delivering the goods and

products from one place to another use this management accounting system (Budgetary control,

2017). It is a process which contains the process of ordering the amount of stock and storing

them in to a storage house using the inventory management system. This accounting system

provides the path to determine the optimum level of inventory to be store in storage house,

purchase order and break down points. Inventories are considered as current assents of an

organisation. There are various type of valuation methods are used under this accounting system

to calculate the cost of inventories. Just in time, material requirement planning, break down

analysis are the part of inventory management accounting system. This accounting helps to

reduce the carrying cost of inventories and prevent the extra cost of retaining the goods in

process.

Trend analysis and forecasting: Changes are the parts of the life and the same rule also

implemented to the business and organisations. This is a system helps to communicate the future

growth and development opportunities to the managers. It is an statistical analysis of customer's

interest and involvement for particular tasks and projects. It is a process of calculating the figures

amount of change in respect of sales of products and services. Customers interest and

3

involvements are the main base of trend analysis. This management accounting system also

known as behavioural analysis. Records and information are maintained in graphical form. This

is one of the branch of management accounting which helps to identify the trend lines and

pattern in respect of product and services.

P2 Various type of methods of management accounting reporting

Methods and approaches of accounting helps to interpret the data and information in

adequate manner. There are varous type of evaluating methods and approaches used in

management accounting (Macintosh and Quattrone, 2010) Management accounting system and

management accounting reports are the summarised reports submitted to managers to make

effective analysing report. This reports are useful to managers and higher level authorities to

analysing the financial position of organisation and build a strong capital structure. Accounting

reports are the parts of financial planning and decision making process. Various type of

accounting reports are submitted to managers and higher level of management such as

Budgetary reports: this is format of producing the information related to upcoming

durations and times. These are the types of internal reports provided to the managers and

supervisors for related analysing the cost of future management and operations. Budgets are the

projections made to analyse the effective cost to be incurred in production, manufacturing and

administration activities. Budgetary reports are made with the helps of past financial and

accounting records. Financial statements of previous years, annual reports, sales and purchase

records, tax and provisions are the main sources used in framing the budgets. Budgetary reports

connect the current position with the desired goals of an organisation. Budgets are prepared

monthly, quarterly and annually as per the nature and type of business organisation.

Cost reports: these are the reports contains the details and information related to

expenses incurred for a particular time duration. Cost reports are prepared with the helps of

various type of cost records (Parker, 2012). There is a separate books are maintain to record the

purchase orders and invoice numbers. Raw material cost, labour cost, direct expenses and

overheads are record in the books. Overall analysis done in the end of year and a conclusive cost

report is prepared to analyse the total cost and requirement of resources for a year. This reports

helps to analyse the overall requirement of resources in terms of monetary and non monetary

funds.

4

known as behavioural analysis. Records and information are maintained in graphical form. This

is one of the branch of management accounting which helps to identify the trend lines and

pattern in respect of product and services.

P2 Various type of methods of management accounting reporting

Methods and approaches of accounting helps to interpret the data and information in

adequate manner. There are varous type of evaluating methods and approaches used in

management accounting (Macintosh and Quattrone, 2010) Management accounting system and

management accounting reports are the summarised reports submitted to managers to make

effective analysing report. This reports are useful to managers and higher level authorities to

analysing the financial position of organisation and build a strong capital structure. Accounting

reports are the parts of financial planning and decision making process. Various type of

accounting reports are submitted to managers and higher level of management such as

Budgetary reports: this is format of producing the information related to upcoming

durations and times. These are the types of internal reports provided to the managers and

supervisors for related analysing the cost of future management and operations. Budgets are the

projections made to analyse the effective cost to be incurred in production, manufacturing and

administration activities. Budgetary reports are made with the helps of past financial and

accounting records. Financial statements of previous years, annual reports, sales and purchase

records, tax and provisions are the main sources used in framing the budgets. Budgetary reports

connect the current position with the desired goals of an organisation. Budgets are prepared

monthly, quarterly and annually as per the nature and type of business organisation.

Cost reports: these are the reports contains the details and information related to

expenses incurred for a particular time duration. Cost reports are prepared with the helps of

various type of cost records (Parker, 2012). There is a separate books are maintain to record the

purchase orders and invoice numbers. Raw material cost, labour cost, direct expenses and

overheads are record in the books. Overall analysis done in the end of year and a conclusive cost

report is prepared to analyse the total cost and requirement of resources for a year. This reports

helps to analyse the overall requirement of resources in terms of monetary and non monetary

funds.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Performance Reports: Information and data related to performance of employees and

management departments are considered in performance reports. Organisational structure remain

divided in multiple structure and divisions. Leaders and departmental managers analyse the

performance of each and every individual. Outcomes are of each departments analysed in respect

of desired goals of organisation. Overall performance is consolidated in single format to evaluate

the performance of overall organisation.

Subsidiary or other reports: Figures and data which helps to complete the prime reports

and task are considered as subsidiary or other reports. This reports defines the sub divisions

progress and their achievements (Renz and Herman, 2016). Income and expenditure, cash flow

statements are analysed for small divisions and a separate reports is prepared. This report is

helpful and beneficial to mangers to analyse the cost structure for sub departments. It is a part of

internal reporting.

Account receivable and ageing reports: there is record of cash inflow from debtors and

selling records, getting the payments and cheques from lenders are considered in account

receivable and ageing reports. There is a proper analysis of sales records and lending. To

analysing the cash requirement this reports are prepared.

Inventory management related reports: This reports are prepared to analyse the

requirement of raw stock, material to produce and manufacturing the goods. This reports helps

the managers to manage the optimum level of inventories in stocks. It is require to maintain the

minimum level of raw material stock for manufacturing process.

M1 Measurement the benefits of management accounting systems used in organisational context

Management accounting is a tools used to reduce the management and operation cost.

Improving the scale of accounting and management in respect of preparing cash flow statements,

income and expenditure statemented and financial potion statement (Soin and Collier, 2011).

Management accounting system is not only the key of effective management but also a

supporting tools to get competitive advantage and sustainable growth.

D1 Management accounting system and management accounting reporting

Scope of management accounting system is found vast in comparison of accounting

reporting. Accounting system provides a tools and paths to make accounting reports to managers

and accountants to organisation (Vaivio and Sirén, 2010). Management accounting system helps

to analyse the financial statements and accounting reports in effective manner. Accounting

5

management departments are considered in performance reports. Organisational structure remain

divided in multiple structure and divisions. Leaders and departmental managers analyse the

performance of each and every individual. Outcomes are of each departments analysed in respect

of desired goals of organisation. Overall performance is consolidated in single format to evaluate

the performance of overall organisation.

Subsidiary or other reports: Figures and data which helps to complete the prime reports

and task are considered as subsidiary or other reports. This reports defines the sub divisions

progress and their achievements (Renz and Herman, 2016). Income and expenditure, cash flow

statements are analysed for small divisions and a separate reports is prepared. This report is

helpful and beneficial to mangers to analyse the cost structure for sub departments. It is a part of

internal reporting.

Account receivable and ageing reports: there is record of cash inflow from debtors and

selling records, getting the payments and cheques from lenders are considered in account

receivable and ageing reports. There is a proper analysis of sales records and lending. To

analysing the cash requirement this reports are prepared.

Inventory management related reports: This reports are prepared to analyse the

requirement of raw stock, material to produce and manufacturing the goods. This reports helps

the managers to manage the optimum level of inventories in stocks. It is require to maintain the

minimum level of raw material stock for manufacturing process.

M1 Measurement the benefits of management accounting systems used in organisational context

Management accounting is a tools used to reduce the management and operation cost.

Improving the scale of accounting and management in respect of preparing cash flow statements,

income and expenditure statemented and financial potion statement (Soin and Collier, 2011).

Management accounting system is not only the key of effective management but also a

supporting tools to get competitive advantage and sustainable growth.

D1 Management accounting system and management accounting reporting

Scope of management accounting system is found vast in comparison of accounting

reporting. Accounting system provides a tools and paths to make accounting reports to managers

and accountants to organisation (Vaivio and Sirén, 2010). Management accounting system helps

to analyse the financial statements and accounting reports in effective manner. Accounting

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

resorting is a work of responsibility and good managerial skills. Management accounting system

will help the managers of TESCO to manage the operations and functions in effective manner.

TASK 2

P3 Calculation of cost approaches to prepare income statement

Cost accounting is one of the branch of management accounting. Analysing the cost and

determine the profit margin is the main objective of this accounting system. This accounting

system remain beneficial and useful to the organisations which are engaging in manufacturing

and production activities (Management accounting, 2017). There are various type of

methodologies and approaches used to calculate the amount of profit and profitability of

organisation. It helps to calculate the cost of inputs incurred in manufacturing and production

process. This is the process helps to bifurcate the cost of company and organisation among

various divisions. Various type of cost techniques are used in cost accounting system. Such as Absorption costing: this technique is called as overall costing approach. This approach is

widely used in business and organisation to analyse the cost of product and evaluate the

profitability for each product (Qian, Burritt and Monroe, 2011). All the variable and fixed

expenses are considered in this cost technique. This cost approach is used in those

organisation which remain aligned with fixed and variable process of manufacturing. Direct costing: this is one of the cost technique used to calculate the direct cost of

material, wages, expenses subject to evaluate the profitability. All the direct variable and

fixed cost are considered in this technique to calculate the profit. Indirect material and

labour cost are calculated separately. Historical costing: It is a method of evaluation of profitability and cost of product in

respect of production and manufacturing process. This cost technique is fund in limited

areas. Cost for specific period are analysed as per this analysing method. Marginal costing: this costing techniques is used to bifurcate the variable and fixed cost

in manufacturing and production process (Fullerton, Kennedy and Widener, 2014). Cost

is calculated in respect of change of per unit. Variation in the cost evaluated parallel to

change in one production unit. All the variable expenses and cost are considered in this

costing technique and fixed expenses are not considered in while calculating the profit. Standard costing: There are two type of formats prepared in standard costing approach.

Actual cost and standard cost are bifurcated to find out variances and difference. Its helps

6

will help the managers of TESCO to manage the operations and functions in effective manner.

TASK 2

P3 Calculation of cost approaches to prepare income statement

Cost accounting is one of the branch of management accounting. Analysing the cost and

determine the profit margin is the main objective of this accounting system. This accounting

system remain beneficial and useful to the organisations which are engaging in manufacturing

and production activities (Management accounting, 2017). There are various type of

methodologies and approaches used to calculate the amount of profit and profitability of

organisation. It helps to calculate the cost of inputs incurred in manufacturing and production

process. This is the process helps to bifurcate the cost of company and organisation among

various divisions. Various type of cost techniques are used in cost accounting system. Such as Absorption costing: this technique is called as overall costing approach. This approach is

widely used in business and organisation to analyse the cost of product and evaluate the

profitability for each product (Qian, Burritt and Monroe, 2011). All the variable and fixed

expenses are considered in this cost technique. This cost approach is used in those

organisation which remain aligned with fixed and variable process of manufacturing. Direct costing: this is one of the cost technique used to calculate the direct cost of

material, wages, expenses subject to evaluate the profitability. All the direct variable and

fixed cost are considered in this technique to calculate the profit. Indirect material and

labour cost are calculated separately. Historical costing: It is a method of evaluation of profitability and cost of product in

respect of production and manufacturing process. This cost technique is fund in limited

areas. Cost for specific period are analysed as per this analysing method. Marginal costing: this costing techniques is used to bifurcate the variable and fixed cost

in manufacturing and production process (Fullerton, Kennedy and Widener, 2014). Cost

is calculated in respect of change of per unit. Variation in the cost evaluated parallel to

change in one production unit. All the variable expenses and cost are considered in this

costing technique and fixed expenses are not considered in while calculating the profit. Standard costing: There are two type of formats prepared in standard costing approach.

Actual cost and standard cost are bifurcated to find out variances and difference. Its helps

6

the managers to understand the changes in cost and measurement of profit. It helps to find

out the difference creating factors from manufacturing process. Uniform costing: this cost approach is used to analyse the difference between the

principles and practices to undertake the control and distinguish the cost.

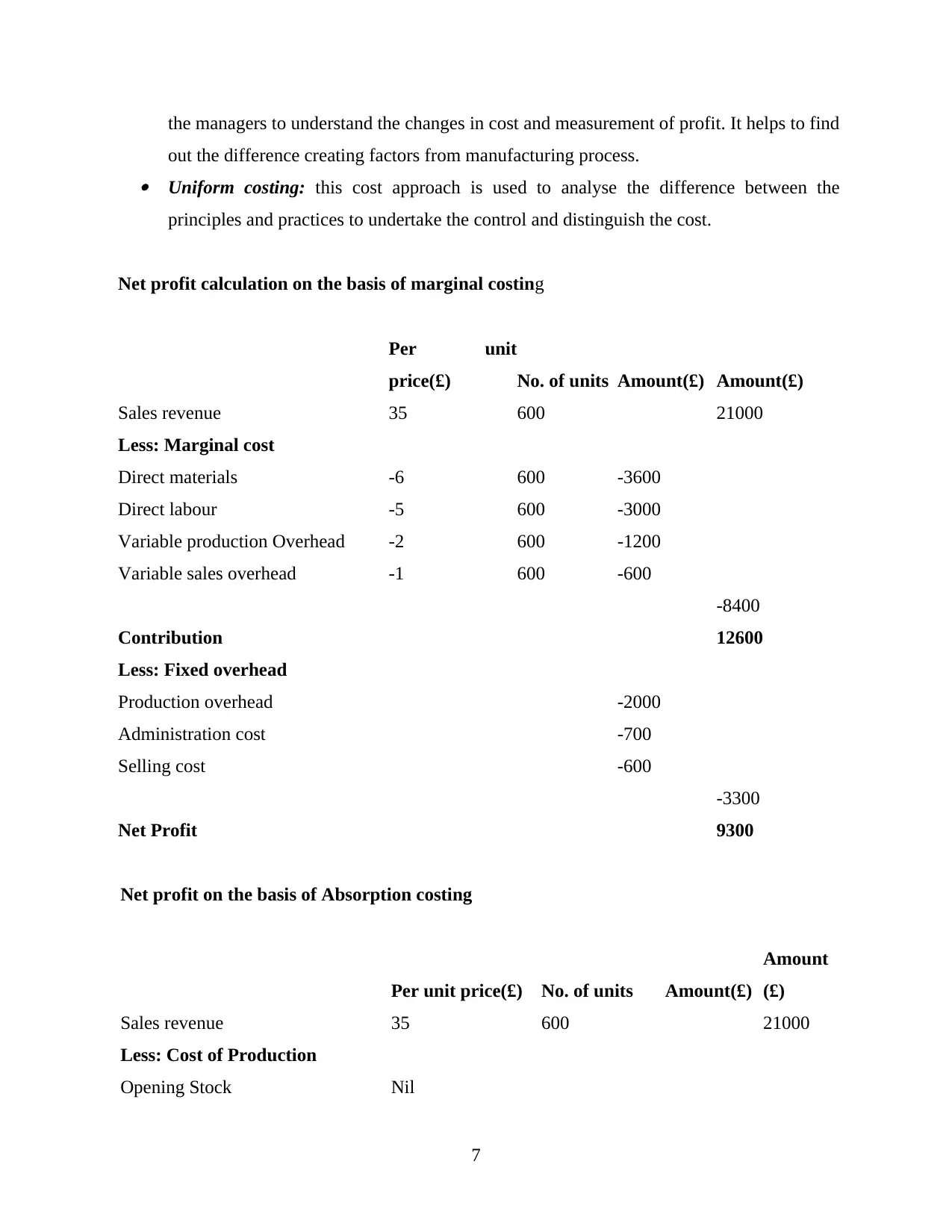

Net profit calculation on the basis of marginal costing

Per unit

price(£) No. of units Amount(£) Amount(£)

Sales revenue 35 600 21000

Less: Marginal cost

Direct materials -6 600 -3600

Direct labour -5 600 -3000

Variable production Overhead -2 600 -1200

Variable sales overhead -1 600 -600

-8400

Contribution 12600

Less: Fixed overhead

Production overhead -2000

Administration cost -700

Selling cost -600

-3300

Net Profit 9300

Net profit on the basis of Absorption costing

Per unit price(£) No. of units Amount(£)

Amount

(£)

Sales revenue 35 600 21000

Less: Cost of Production

Opening Stock Nil

7

out the difference creating factors from manufacturing process. Uniform costing: this cost approach is used to analyse the difference between the

principles and practices to undertake the control and distinguish the cost.

Net profit calculation on the basis of marginal costing

Per unit

price(£) No. of units Amount(£) Amount(£)

Sales revenue 35 600 21000

Less: Marginal cost

Direct materials -6 600 -3600

Direct labour -5 600 -3000

Variable production Overhead -2 600 -1200

Variable sales overhead -1 600 -600

-8400

Contribution 12600

Less: Fixed overhead

Production overhead -2000

Administration cost -700

Selling cost -600

-3300

Net Profit 9300

Net profit on the basis of Absorption costing

Per unit price(£) No. of units Amount(£)

Amount

(£)

Sales revenue 35 600 21000

Less: Cost of Production

Opening Stock Nil

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

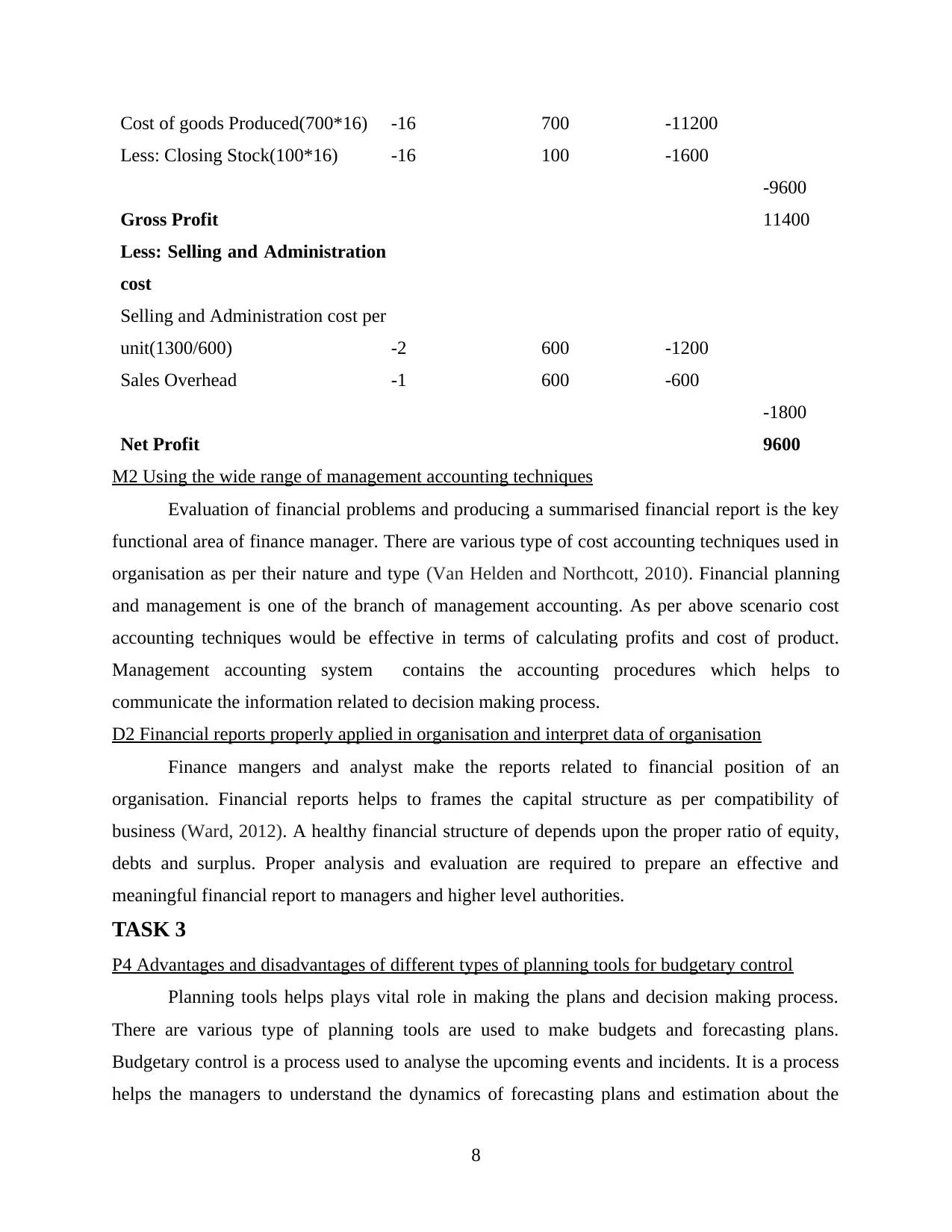

Cost of goods Produced(700*16) -16 700 -11200

Less: Closing Stock(100*16) -16 100 -1600

-9600

Gross Profit 11400

Less: Selling and Administration

cost

Selling and Administration cost per

unit(1300/600) -2 600 -1200

Sales Overhead -1 600 -600

-1800

Net Profit 9600

M2 Using the wide range of management accounting techniques

Evaluation of financial problems and producing a summarised financial report is the key

functional area of finance manager. There are various type of cost accounting techniques used in

organisation as per their nature and type (Van Helden and Northcott, 2010). Financial planning

and management is one of the branch of management accounting. As per above scenario cost

accounting techniques would be effective in terms of calculating profits and cost of product.

Management accounting system contains the accounting procedures which helps to

communicate the information related to decision making process.

D2 Financial reports properly applied in organisation and interpret data of organisation

Finance mangers and analyst make the reports related to financial position of an

organisation. Financial reports helps to frames the capital structure as per compatibility of

business (Ward, 2012). A healthy financial structure of depends upon the proper ratio of equity,

debts and surplus. Proper analysis and evaluation are required to prepare an effective and

meaningful financial report to managers and higher level authorities.

TASK 3

P4 Advantages and disadvantages of different types of planning tools for budgetary control

Planning tools helps plays vital role in making the plans and decision making process.

There are various type of planning tools are used to make budgets and forecasting plans.

Budgetary control is a process used to analyse the upcoming events and incidents. It is a process

helps the managers to understand the dynamics of forecasting plans and estimation about the

8

Less: Closing Stock(100*16) -16 100 -1600

-9600

Gross Profit 11400

Less: Selling and Administration

cost

Selling and Administration cost per

unit(1300/600) -2 600 -1200

Sales Overhead -1 600 -600

-1800

Net Profit 9600

M2 Using the wide range of management accounting techniques

Evaluation of financial problems and producing a summarised financial report is the key

functional area of finance manager. There are various type of cost accounting techniques used in

organisation as per their nature and type (Van Helden and Northcott, 2010). Financial planning

and management is one of the branch of management accounting. As per above scenario cost

accounting techniques would be effective in terms of calculating profits and cost of product.

Management accounting system contains the accounting procedures which helps to

communicate the information related to decision making process.

D2 Financial reports properly applied in organisation and interpret data of organisation

Finance mangers and analyst make the reports related to financial position of an

organisation. Financial reports helps to frames the capital structure as per compatibility of

business (Ward, 2012). A healthy financial structure of depends upon the proper ratio of equity,

debts and surplus. Proper analysis and evaluation are required to prepare an effective and

meaningful financial report to managers and higher level authorities.

TASK 3

P4 Advantages and disadvantages of different types of planning tools for budgetary control

Planning tools helps plays vital role in making the plans and decision making process.

There are various type of planning tools are used to make budgets and forecasting plans.

Budgetary control is a process used to analyse the upcoming events and incidents. It is a process

helps the managers to understand the dynamics of forecasting plans and estimation about the

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

future cost. Budgets provides a projected score in respect of management and operation for

subsiding years. There are some formal financial statements prepared in respect of business

activities and operations. This is the technique which helps to make projected details as per the

data and informations of precious year. Various type of analysation and differences are identified

in respect of detecting the problems and issues. Results and outcomes are evaluated with the

projected plans.

Advantages of budgetary control

Budgetary control process helps to understand the cost of production and manufacturing

process. Budgets provides an estimation subject to operation and management for

upcoming years. This process remain associated with future planning and strategic

planning to control over all cost of organisation. This is the part of managerial accounting

and assist managers to take risk for garbing the growth and developing opportunities.

Budgets helps to communicate the multiple departments of an organisation and also helps

to promote the coordinator approach of together working (Zimmerman and Yahya-Zadeh,

2011). It helps to maintain an effective communication system with in the organisation.

Budgets helps to build a disciplined and ethical structure in organisation.

Budgets ensure the credibility and future comparability in respect of achieving the

targets. It forces the manages to look forward and beyond the limits. Budgetary control

process encourage the spirit of thinking for future. It is a process provides opportunities

to participate independently and effectively.

Disadvantage of budgetary control process

This is the critical process contains large amount of risk and uncertainty. Budgets do not

provide surety of guaranteed success. It is an estimation about furture operations and

activities to attain organisational goals.

Traditional approaches and applied theories only used in budgetary control process.

Major parts remain avoided from the criteria of making budgets. Traditional approaches

and theories remain the part of budgetary control process.

Managers and accountants are answerable to the higher level authorities. Budgetary

control is a process include various type of risks and uncertainties which create

complexities.

9

subsiding years. There are some formal financial statements prepared in respect of business

activities and operations. This is the technique which helps to make projected details as per the

data and informations of precious year. Various type of analysation and differences are identified

in respect of detecting the problems and issues. Results and outcomes are evaluated with the

projected plans.

Advantages of budgetary control

Budgetary control process helps to understand the cost of production and manufacturing

process. Budgets provides an estimation subject to operation and management for

upcoming years. This process remain associated with future planning and strategic

planning to control over all cost of organisation. This is the part of managerial accounting

and assist managers to take risk for garbing the growth and developing opportunities.

Budgets helps to communicate the multiple departments of an organisation and also helps

to promote the coordinator approach of together working (Zimmerman and Yahya-Zadeh,

2011). It helps to maintain an effective communication system with in the organisation.

Budgets helps to build a disciplined and ethical structure in organisation.

Budgets ensure the credibility and future comparability in respect of achieving the

targets. It forces the manages to look forward and beyond the limits. Budgetary control

process encourage the spirit of thinking for future. It is a process provides opportunities

to participate independently and effectively.

Disadvantage of budgetary control process

This is the critical process contains large amount of risk and uncertainty. Budgets do not

provide surety of guaranteed success. It is an estimation about furture operations and

activities to attain organisational goals.

Traditional approaches and applied theories only used in budgetary control process.

Major parts remain avoided from the criteria of making budgets. Traditional approaches

and theories remain the part of budgetary control process.

Managers and accountants are answerable to the higher level authorities. Budgetary

control is a process include various type of risks and uncertainties which create

complexities.

9

It resist the new managers and employees to participate in making plans and taking

decisions. Results and outcomes remain uncertain in respect of proposed plans. Complex

situations and diverse business environment reduce the credibility.

There is lack of communication found while making plans and project to allocate the

resources in effective manner. In appropriate manner of allocating resources and

mediums becomes the reason of departmental conflicts and issues.

It also effect the actions and performance of employees. Individual aims, objectives and

goals could not be determine by this process. This process remain centralised towards

organisational growth rather than developing the performance and capacity of individual.

This process contain huge amount of investment in the form of monetary and non

monetary funds. It is a time consuming approach which take to much time to sort out the

issues and conflicts in time.

Different types of planning tools which are used in budgeting, there advantages and

disadvantages.

Incremental budgeting methods; Incremental budgeting is essential part of

management accounting which are concerned with making small assessment to existing

budget for making new budget. In this budgeting method only incremental amount are

added to new budgeting numbers. There are various advantages and disadvantages of

incremental budgeting methods are given below.

Advantages:

This method is easy to implement because it does not contain any complex calculations.

It ensure continuity of funding for various departments without mentioning detailed

information of funds requirement.

There is no large deviations are seen in the budget year after year because change year

after year.

The changes made in budget can be seen immediately which are related to incremental

budgeting.

Disadvantages

it is usually incremental in nature because it change the overall structure of budget which

respect to company which are different from present year to existing year.

10

decisions. Results and outcomes remain uncertain in respect of proposed plans. Complex

situations and diverse business environment reduce the credibility.

There is lack of communication found while making plans and project to allocate the

resources in effective manner. In appropriate manner of allocating resources and

mediums becomes the reason of departmental conflicts and issues.

It also effect the actions and performance of employees. Individual aims, objectives and

goals could not be determine by this process. This process remain centralised towards

organisational growth rather than developing the performance and capacity of individual.

This process contain huge amount of investment in the form of monetary and non

monetary funds. It is a time consuming approach which take to much time to sort out the

issues and conflicts in time.

Different types of planning tools which are used in budgeting, there advantages and

disadvantages.

Incremental budgeting methods; Incremental budgeting is essential part of

management accounting which are concerned with making small assessment to existing

budget for making new budget. In this budgeting method only incremental amount are

added to new budgeting numbers. There are various advantages and disadvantages of

incremental budgeting methods are given below.

Advantages:

This method is easy to implement because it does not contain any complex calculations.

It ensure continuity of funding for various departments without mentioning detailed

information of funds requirement.

There is no large deviations are seen in the budget year after year because change year

after year.

The changes made in budget can be seen immediately which are related to incremental

budgeting.

Disadvantages

it is usually incremental in nature because it change the overall structure of budget which

respect to company which are different from present year to existing year.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.