Comprehensive Management Accounting Report for ABC Ltd

VerifiedAdded on 2021/02/20

|18

|6066

|48

Report

AI Summary

This report delves into the realm of management accounting, focusing on its significance in the internal operations of organizations. It uses ABC Ltd., a manufacturing firm specializing in fresh juices, as a case study to illustrate different systems and reporting methods. The report covers key aspects of management accounting, including the difference between management and financial accounting, various systems such as inventory management, cost accounting, price optimization, and job costing. It also explores different reporting methods like budget reports, job costing reports, accounts receivable reports, and inventory reports. The report further examines the application of marginal and absorption costing techniques, comparing their benefits and limitations. Additionally, it analyzes the benefits and uses of management accounting systems and explores different management accounting systems that can be adopted to address financial problems, with a focus on budgeting and planning tools. Overall, the report provides a comprehensive overview of management accounting principles and practices, offering insights into its role in resolving financial issues within a business.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

P1. Explaining the meaning of management accounting and the significance of its systems....1

P2. Describing different methods that could be used by the company for reporting .................2

M1. Evaluating the benefits and the uses of the management systems. ....................................2

LO2..................................................................................................................................................2

P 3 Preparing income statements of the company using marginal and absorption costing

techniques....................................................................................................................................2

LO4..................................................................................................................................................3

P4. Explaining benefits and the limitation of the different planning tools.................................3

M3. Analysing the uses and the application of the budgeting tools ...........................................5

LO4..................................................................................................................................................6

P 5 Describing different management accounting systems to be adopted by companies in

order to respond to different financial problems.........................................................................6

M4 Analysis of different management accounting technique of responding to different

financial problems.......................................................................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

P1. Explaining the meaning of management accounting and the significance of its systems....1

P2. Describing different methods that could be used by the company for reporting .................2

M1. Evaluating the benefits and the uses of the management systems. ....................................2

LO2..................................................................................................................................................2

P 3 Preparing income statements of the company using marginal and absorption costing

techniques....................................................................................................................................2

LO4..................................................................................................................................................3

P4. Explaining benefits and the limitation of the different planning tools.................................3

M3. Analysing the uses and the application of the budgeting tools ...........................................5

LO4..................................................................................................................................................6

P 5 Describing different management accounting systems to be adopted by companies in

order to respond to different financial problems.........................................................................6

M4 Analysis of different management accounting technique of responding to different

financial problems.......................................................................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION

Management accounting refers to the effective management of the internal operations of

organizations. It is the practice that is adopted by the firm in order to efficiently organizing its

resources and provides for better controlling. The present study is based on ABC Ltd., a

manufacturing firm, deals in the production of fresh juices. Furthermore, the report highlights on

different system and the reporting under management accounting, Moreover, it also includes the

deep insights towards various planning tools and the systems that helps in resolving the financial

problems within the business.

LO1.

P1. Explaining the meaning of management accounting and the significance of its systems

Management accounting refers to the practice of framing the statistical and the financial

information to the managers with the help of which they could be able to make the routine and

the short-term decisions. Both management and financial accounting differs to a large extent as

follows-

Management Accounting Financial accounting

It provides for the ways in which the problems

could be resolved.

It reports for the profitability that is gained by

the ABC Ltd. from its business.

This branch of accounting doesn't have to

follow any of the standards at the time when

the information is been compiled in relation to

internal consumption.

Under this, the reports are been prepared in

compliance with the accounting standards as

stated by IFRS and GAAP.

It accounts for the reporting to internal

management and not to the outsiders.

However, financial accounting reports to

internal as well as the external users.

Various systems of management accounting are as follows-

Inventory management system- It means the system that accounts for maintaining the

appropriate records of the inventory. It is counted as an extremely important system because it

facilitates constant follow up regarding the incomings and the outgoings. It helps in measuring or

determining the requirement of the products in accordance with the demand of the customers. It

is the medium through which the ABC Ltd. can run its operations smoothly.

1

Management accounting refers to the effective management of the internal operations of

organizations. It is the practice that is adopted by the firm in order to efficiently organizing its

resources and provides for better controlling. The present study is based on ABC Ltd., a

manufacturing firm, deals in the production of fresh juices. Furthermore, the report highlights on

different system and the reporting under management accounting, Moreover, it also includes the

deep insights towards various planning tools and the systems that helps in resolving the financial

problems within the business.

LO1.

P1. Explaining the meaning of management accounting and the significance of its systems

Management accounting refers to the practice of framing the statistical and the financial

information to the managers with the help of which they could be able to make the routine and

the short-term decisions. Both management and financial accounting differs to a large extent as

follows-

Management Accounting Financial accounting

It provides for the ways in which the problems

could be resolved.

It reports for the profitability that is gained by

the ABC Ltd. from its business.

This branch of accounting doesn't have to

follow any of the standards at the time when

the information is been compiled in relation to

internal consumption.

Under this, the reports are been prepared in

compliance with the accounting standards as

stated by IFRS and GAAP.

It accounts for the reporting to internal

management and not to the outsiders.

However, financial accounting reports to

internal as well as the external users.

Various systems of management accounting are as follows-

Inventory management system- It means the system that accounts for maintaining the

appropriate records of the inventory. It is counted as an extremely important system because it

facilitates constant follow up regarding the incomings and the outgoings. It helps in measuring or

determining the requirement of the products in accordance with the demand of the customers. It

is the medium through which the ABC Ltd. can run its operations smoothly.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost accounting system- This system is been used by the ABC Ltd. in order to record the

production activities by using the system of perpetual inventory. It plays an essential role in

tracking the raw material at the time when they go through stages of the production till it turns

into the finished goods. It enables the firm in examining cost structure within the business by

gathering the information in relation to the cost involved in the activities of the company. It also

assigns the cost towards the products, cost objects and services for the purpose of evaluating

efficiency in usage of the cost. It is majorly concerned with developing detailed understanding

on the key areas from which the company earns maximum profits.

Price optimization system- This system provides for making the analysis of the customer's

response towards the product at the different level of price mathematically. It plays a significant

role in fixing the most suitable price for the ABC Ltd. so that higher demand could be created for

its product in the market which in turn helps in gaining larger profitability.

Job costing system- It refers to the practice of accumulating the information in relation to the

cost attached to particular job or the unit of production. Information provided by this system is

essential in terms of identifying accuracy in the estimating system of an entity.

P2. Describing different methods that could be used by the company for reporting

Managerial reports are been prepared for facilitating the information relating to the cost,

high performing staff, reward, product lines and making investment in such goods that serves

best returns for the business. There are different reports which are been formulated for running

the operations effectively as follows-

Budget report- It means the report that makes the list of the budgeted expenses and the

revenues. It helps the ABC Ltd. in analysing the performance of its business and enables the

managers in assessing the performance of the department and in keeping the control over the

cost. The budget estimates that are made for the upcoming or the new period are on the basis of

the actual expenses from the previous years. This report is also useful for the managers and the

company in order to provide the rewards or incentives for the employees. The budgeted funds are

been used for providing the bonuses to staff in respect of achieving the financial goals.

Job costing report- This report is been prepared for showing the expenses for the

particular proposal which is being financed by the organization’s business. It is been actually

matched up by making an estimation of the revenues so that appropriate evaluation could be

made regarding the profitability of the job. It helps in determining the areas that are higher

2

production activities by using the system of perpetual inventory. It plays an essential role in

tracking the raw material at the time when they go through stages of the production till it turns

into the finished goods. It enables the firm in examining cost structure within the business by

gathering the information in relation to the cost involved in the activities of the company. It also

assigns the cost towards the products, cost objects and services for the purpose of evaluating

efficiency in usage of the cost. It is majorly concerned with developing detailed understanding

on the key areas from which the company earns maximum profits.

Price optimization system- This system provides for making the analysis of the customer's

response towards the product at the different level of price mathematically. It plays a significant

role in fixing the most suitable price for the ABC Ltd. so that higher demand could be created for

its product in the market which in turn helps in gaining larger profitability.

Job costing system- It refers to the practice of accumulating the information in relation to the

cost attached to particular job or the unit of production. Information provided by this system is

essential in terms of identifying accuracy in the estimating system of an entity.

P2. Describing different methods that could be used by the company for reporting

Managerial reports are been prepared for facilitating the information relating to the cost,

high performing staff, reward, product lines and making investment in such goods that serves

best returns for the business. There are different reports which are been formulated for running

the operations effectively as follows-

Budget report- It means the report that makes the list of the budgeted expenses and the

revenues. It helps the ABC Ltd. in analysing the performance of its business and enables the

managers in assessing the performance of the department and in keeping the control over the

cost. The budget estimates that are made for the upcoming or the new period are on the basis of

the actual expenses from the previous years. This report is also useful for the managers and the

company in order to provide the rewards or incentives for the employees. The budgeted funds are

been used for providing the bonuses to staff in respect of achieving the financial goals.

Job costing report- This report is been prepared for showing the expenses for the

particular proposal which is being financed by the organization’s business. It is been actually

matched up by making an estimation of the revenues so that appropriate evaluation could be

made regarding the profitability of the job. It helps in determining the areas that are higher

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

earning so that ABC Ltd.could emphasize on the additional efforts rather than wasting the money

and the time on the jobs with the lower profit margins. This report is also useful in computing the

expenses at the time when the project is progressing so that optimum use of the resources can be

made.

Accounts receivable report- It refers to the report that includes the details regarding the

balances that are to be received to the organization. It is critical for the company in order to

manage its cash flow in case credit is extended to the customers of business. It is the report that

breakdown the balances of the customer for the purpose of finding out the time period for which

they are been owed. In case there is large no. of people who have not paid the balances then an

ABC Ltd.has to take appropriate steps for tightening its credit policies. Thus, it helps in

overlooking on the old debts and in making timely recovery of it.

Inventory report- This report helps in keeping the track over the physical stock that the

company is manufacturing and provides for the ways for making the manufacturing process

much better and efficient. It assists the ABC Ltd. in finding out the areas that need improvement

and in knowing out the best-performing functional departments.

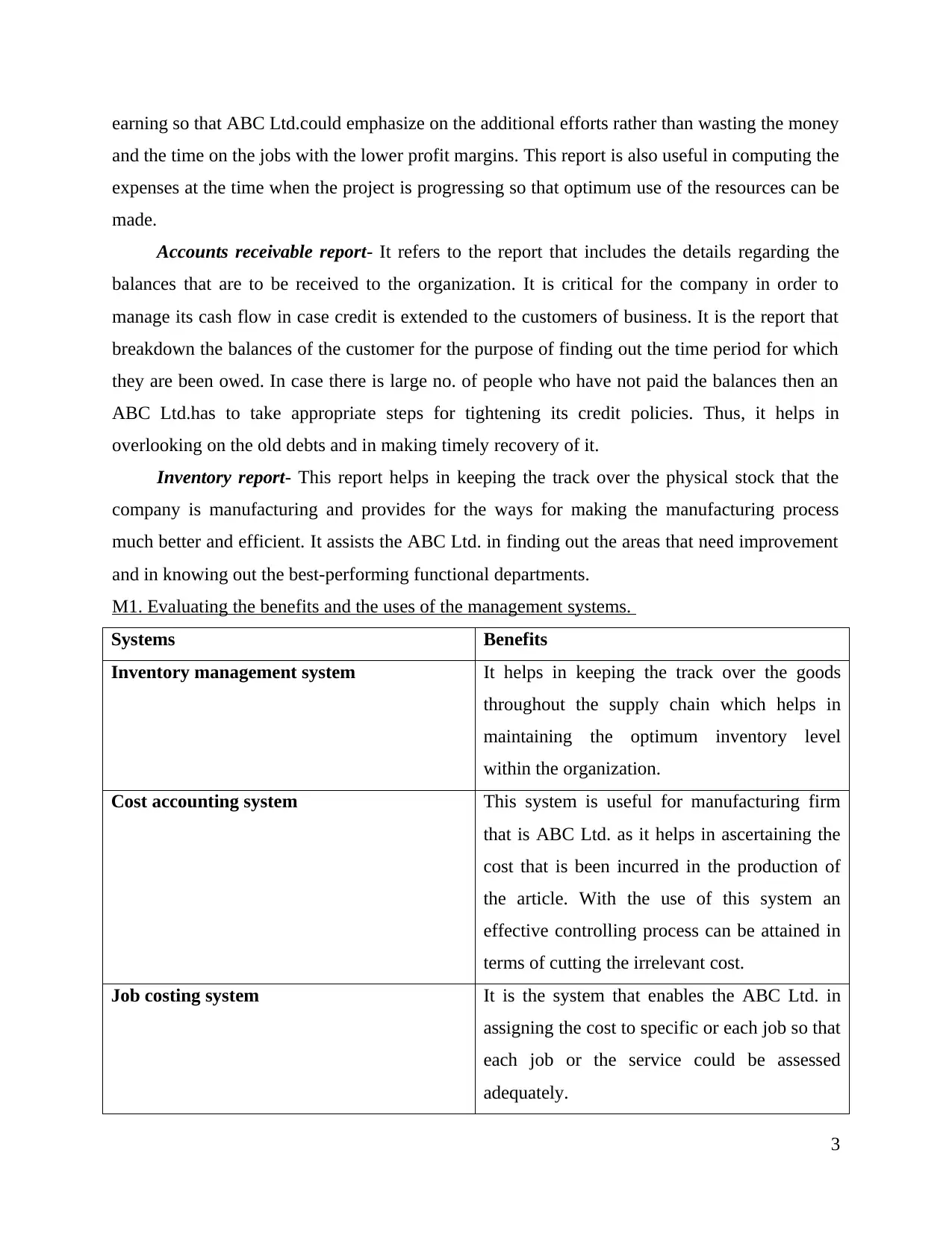

M1. Evaluating the benefits and the uses of the management systems.

Systems Benefits

Inventory management system It helps in keeping the track over the goods

throughout the supply chain which helps in

maintaining the optimum inventory level

within the organization.

Cost accounting system This system is useful for manufacturing firm

that is ABC Ltd. as it helps in ascertaining the

cost that is been incurred in the production of

the article. With the use of this system an

effective controlling process can be attained in

terms of cutting the irrelevant cost.

Job costing system It is the system that enables the ABC Ltd. in

assigning the cost to specific or each job so that

each job or the service could be assessed

adequately.

3

and the time on the jobs with the lower profit margins. This report is also useful in computing the

expenses at the time when the project is progressing so that optimum use of the resources can be

made.

Accounts receivable report- It refers to the report that includes the details regarding the

balances that are to be received to the organization. It is critical for the company in order to

manage its cash flow in case credit is extended to the customers of business. It is the report that

breakdown the balances of the customer for the purpose of finding out the time period for which

they are been owed. In case there is large no. of people who have not paid the balances then an

ABC Ltd.has to take appropriate steps for tightening its credit policies. Thus, it helps in

overlooking on the old debts and in making timely recovery of it.

Inventory report- This report helps in keeping the track over the physical stock that the

company is manufacturing and provides for the ways for making the manufacturing process

much better and efficient. It assists the ABC Ltd. in finding out the areas that need improvement

and in knowing out the best-performing functional departments.

M1. Evaluating the benefits and the uses of the management systems.

Systems Benefits

Inventory management system It helps in keeping the track over the goods

throughout the supply chain which helps in

maintaining the optimum inventory level

within the organization.

Cost accounting system This system is useful for manufacturing firm

that is ABC Ltd. as it helps in ascertaining the

cost that is been incurred in the production of

the article. With the use of this system an

effective controlling process can be attained in

terms of cutting the irrelevant cost.

Job costing system It is the system that enables the ABC Ltd. in

assigning the cost to specific or each job so that

each job or the service could be assessed

adequately.

3

Price optimization system It helps in knowing the demand for the product

by mathematically determining the response of

the customers at various price levels. This in

turn allows the ABC Ltd. in setting up the most

suitable prices.

LO2.

P 3 Preparing income statements of the company using marginal and absorption costing

techniques

Marginal costing:

Marginal costing is a technique used by the managerial accountant for preparing i9ncome

statements of the firm. Under this technique, the profit generated by the business is being

calculated after deducting marginal costs of production from the sales revenue earned by it

during a specific time period (Spraakman and et.al., 2018). Under this technique, for the purpose

of computing marginal cost of production, each variable cost incurred by the business is being

treated as product cost on the other hand, all the fixed production costs are treated as the period

costs and hence, do not become a part of marginal cost.

Absorption costing:

Absorption costing is also a widely used technique of management accounting system in

order to net profit generated by the firm from the sale of a specific volume of goods. In this

technique, each and every costs beared by the company in order to produce any goods or services

becomes a part of production cost regardless of whether they are fixed or variable. Hence, the

profit generated by the firm is being calculated after deducting all the production costs from the

amount of sales revenue.

Difference between marginal and absorption costing

Both marginal and absorption costing are the techniques of management accounting used

for the preparation of income statement of the firm in order to determine the amount of profit

generated by the company by selling a specific volume of products. Due to difference in method

of calculating profit and different assumptions, both techniques provide different results to the

managers in terms of profit.

4

by mathematically determining the response of

the customers at various price levels. This in

turn allows the ABC Ltd. in setting up the most

suitable prices.

LO2.

P 3 Preparing income statements of the company using marginal and absorption costing

techniques

Marginal costing:

Marginal costing is a technique used by the managerial accountant for preparing i9ncome

statements of the firm. Under this technique, the profit generated by the business is being

calculated after deducting marginal costs of production from the sales revenue earned by it

during a specific time period (Spraakman and et.al., 2018). Under this technique, for the purpose

of computing marginal cost of production, each variable cost incurred by the business is being

treated as product cost on the other hand, all the fixed production costs are treated as the period

costs and hence, do not become a part of marginal cost.

Absorption costing:

Absorption costing is also a widely used technique of management accounting system in

order to net profit generated by the firm from the sale of a specific volume of goods. In this

technique, each and every costs beared by the company in order to produce any goods or services

becomes a part of production cost regardless of whether they are fixed or variable. Hence, the

profit generated by the firm is being calculated after deducting all the production costs from the

amount of sales revenue.

Difference between marginal and absorption costing

Both marginal and absorption costing are the techniques of management accounting used

for the preparation of income statement of the firm in order to determine the amount of profit

generated by the company by selling a specific volume of products. Due to difference in method

of calculating profit and different assumptions, both techniques provide different results to the

managers in terms of profit.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

One of the essential differences between these techniques occurs at the time of

calculating cost of production of the company. In the absorption costing technique, each

manufacturing cost of production becomes part of production cost. On the other hand, only

variable costs of production are taken into account at the time of computing cost of production

under marginal cost system (Chen and Yin, 2019). Further, amount of profit of the company

derived from the marginal costing techniques comes more than the amount derived from

absorption costing. The major reason behind it is the difference in the assumptions taken by both

the techniques. Due to exclusion of fixed manufacturing overheads from the amount of cost of

production, the marginal costing techniques shows more profit to the company.

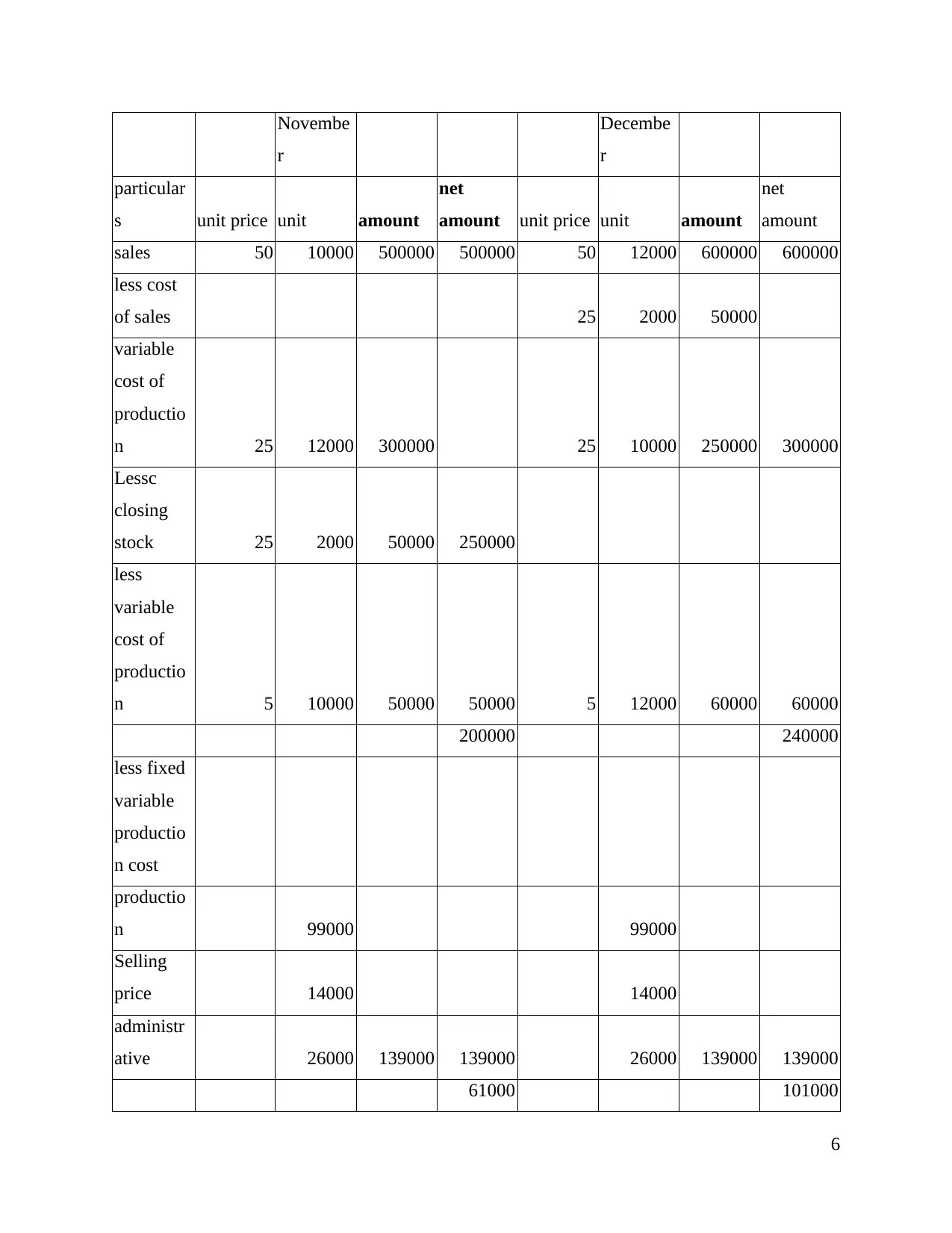

Under marginal costing

Cost per unit

Direst Material 18

Direst Labour 4

Variable O/H 3

Marginal cost per unit 25

Selling price 50

-Marginal cost per unit -25

-variable selling price -5.00

Contribution per unit 20.00

profit and

loss

statement

by using

marginal

costing

method

5

calculating cost of production of the company. In the absorption costing technique, each

manufacturing cost of production becomes part of production cost. On the other hand, only

variable costs of production are taken into account at the time of computing cost of production

under marginal cost system (Chen and Yin, 2019). Further, amount of profit of the company

derived from the marginal costing techniques comes more than the amount derived from

absorption costing. The major reason behind it is the difference in the assumptions taken by both

the techniques. Due to exclusion of fixed manufacturing overheads from the amount of cost of

production, the marginal costing techniques shows more profit to the company.

Under marginal costing

Cost per unit

Direst Material 18

Direst Labour 4

Variable O/H 3

Marginal cost per unit 25

Selling price 50

-Marginal cost per unit -25

-variable selling price -5.00

Contribution per unit 20.00

profit and

loss

statement

by using

marginal

costing

method

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Novembe

r

Decembe

r

particular

s unit price unit amount

net

amount unit price unit amount

net

amount

sales 50 10000 500000 500000 50 12000 600000 600000

less cost

of sales 25 2000 50000

variable

cost of

productio

n 25 12000 300000 25 10000 250000 300000

Lessc

closing

stock 25 2000 50000 250000

less

variable

cost of

productio

n 5 10000 50000 50000 5 12000 60000 60000

200000 240000

less fixed

variable

productio

n cost

productio

n 99000 99000

Selling

price 14000 14000

administr

ative 26000 139000 139000 26000 139000 139000

61000 101000

6

r

Decembe

r

particular

s unit price unit amount

net

amount unit price unit amount

net

amount

sales 50 10000 500000 500000 50 12000 600000 600000

less cost

of sales 25 2000 50000

variable

cost of

productio

n 25 12000 300000 25 10000 250000 300000

Lessc

closing

stock 25 2000 50000 250000

less

variable

cost of

productio

n 5 10000 50000 50000 5 12000 60000 60000

200000 240000

less fixed

variable

productio

n cost

productio

n 99000 99000

Selling

price 14000 14000

administr

ative 26000 139000 139000 26000 139000 139000

61000 101000

6

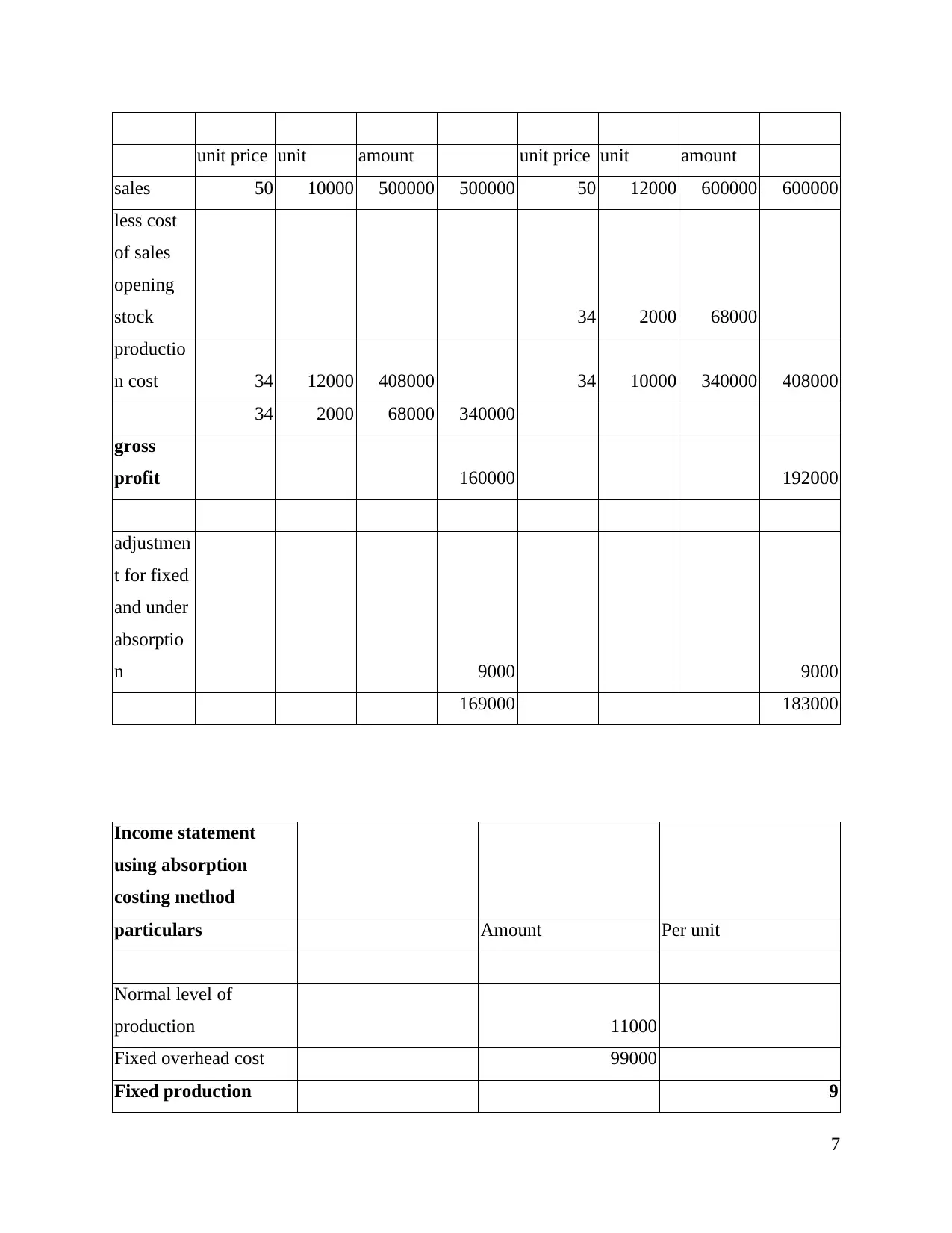

unit price unit amount unit price unit amount

sales 50 10000 500000 500000 50 12000 600000 600000

less cost

of sales

opening

stock 34 2000 68000

productio

n cost 34 12000 408000 34 10000 340000 408000

34 2000 68000 340000

gross

profit 160000 192000

adjustmen

t for fixed

and under

absorptio

n 9000 9000

169000 183000

Income statement

using absorption

costing method

particulars Amount Per unit

Normal level of

production 11000

Fixed overhead cost 99000

Fixed production 9

7

sales 50 10000 500000 500000 50 12000 600000 600000

less cost

of sales

opening

stock 34 2000 68000

productio

n cost 34 12000 408000 34 10000 340000 408000

34 2000 68000 340000

gross

profit 160000 192000

adjustmen

t for fixed

and under

absorptio

n 9000 9000

169000 183000

Income statement

using absorption

costing method

particulars Amount Per unit

Normal level of

production 11000

Fixed overhead cost 99000

Fixed production 9

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

overhead

Total production cost

variable cost 25

Fixed cost 9

Total 34

LO3.

P4. Explaining benefits and the limitation of the different planning tools

Budgetary control- It refers to the practice for the managers in setting of the financial

and the performance goals regarding the budgets, in comparing actual results and in making the

adjustment within the performance as required.

Advantages Disadvantages

It is useful in monitoring the current trends

within the business and in identifying the

future trends.

It provides for the effective utilisation of the

resources that includes the factors of the

production like material, money, human

resource and the machines.

In the changing conditions, it might not

possible for the company in achieving the

targets that are budgeted (Schlegel, Frank and

Britzelmaier, 2016).

Coordination and the correlation of the several

budget is tend to be expensive.

Capital budget- It means the budget that allocates the money for the purpose of acquiring

and maintaining the fixed assets like equipment, buildings etc.

It enables ABC Ltd in making the anticipation

regarding which of the investment option will

be yielding better profits.

It helps the firm in making the long run

strategic investments.

The decisions that are been made under this

method are for long term purpose which are

irreversible in the nature.

Under this budget, discounting and the risk

factor stays subjective to the perception of

manager.

8

Total production cost

variable cost 25

Fixed cost 9

Total 34

LO3.

P4. Explaining benefits and the limitation of the different planning tools

Budgetary control- It refers to the practice for the managers in setting of the financial

and the performance goals regarding the budgets, in comparing actual results and in making the

adjustment within the performance as required.

Advantages Disadvantages

It is useful in monitoring the current trends

within the business and in identifying the

future trends.

It provides for the effective utilisation of the

resources that includes the factors of the

production like material, money, human

resource and the machines.

In the changing conditions, it might not

possible for the company in achieving the

targets that are budgeted (Schlegel, Frank and

Britzelmaier, 2016).

Coordination and the correlation of the several

budget is tend to be expensive.

Capital budget- It means the budget that allocates the money for the purpose of acquiring

and maintaining the fixed assets like equipment, buildings etc.

It enables ABC Ltd in making the anticipation

regarding which of the investment option will

be yielding better profits.

It helps the firm in making the long run

strategic investments.

The decisions that are been made under this

method are for long term purpose which are

irreversible in the nature.

Under this budget, discounting and the risk

factor stays subjective to the perception of

manager.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Master budget-It refers to the document which integrates the individual budget that is

been formulated by different departments in the company.

It provides for the summary of divisional

budget and encourages the managers in

comparing actual results with that of the

budgeted results (Opgenoord and Willcox,

2016).

It helps the company in achieving the goals

with making an effective plan in advance.

This budget is rigid because as it does not takes

into account the new opportunities in order to

attain growth in the long run.

It is very difficult to modify the master budget

as it is a lengthy process and could not be

understood easily.

Operating budget- It is been referred as the budget that comprises of the expenses and

the revenues over the time period, which is been used for planning the operations of an entity.

This budget provides for the information in

relation to long range needs of an enterprise.

It develops the flexibility in the budget as by

building the flexible amount of spendings in

order to meet the unanticipated cost

(Kengatharan, 2016).

There are various federal tax related

complication included in the operational

budget.

It requires the adjustments on a regular interval

of time which in turn consumes a lot of time

for the managers and they could not focus on

important task.

Financial budget- It means the financial plan prepared for the defined period and

includes details regarding the allocation of the resources the towards different departments for

the purpose of managing cash flows in effective manner.

It assist the managers of ABC Ltd in creating

the financial awareness relating to their

spending and the earnings (Hatcher, 2015).

For preparation of this budget highly skilled

staff is required which in turn increases the

cost of the company in terms of training.

9

been formulated by different departments in the company.

It provides for the summary of divisional

budget and encourages the managers in

comparing actual results with that of the

budgeted results (Opgenoord and Willcox,

2016).

It helps the company in achieving the goals

with making an effective plan in advance.

This budget is rigid because as it does not takes

into account the new opportunities in order to

attain growth in the long run.

It is very difficult to modify the master budget

as it is a lengthy process and could not be

understood easily.

Operating budget- It is been referred as the budget that comprises of the expenses and

the revenues over the time period, which is been used for planning the operations of an entity.

This budget provides for the information in

relation to long range needs of an enterprise.

It develops the flexibility in the budget as by

building the flexible amount of spendings in

order to meet the unanticipated cost

(Kengatharan, 2016).

There are various federal tax related

complication included in the operational

budget.

It requires the adjustments on a regular interval

of time which in turn consumes a lot of time

for the managers and they could not focus on

important task.

Financial budget- It means the financial plan prepared for the defined period and

includes details regarding the allocation of the resources the towards different departments for

the purpose of managing cash flows in effective manner.

It assist the managers of ABC Ltd in creating

the financial awareness relating to their

spending and the earnings (Hatcher, 2015).

For preparation of this budget highly skilled

staff is required which in turn increases the

cost of the company in terms of training.

9

This budget helps the business in recognizing

the opportunities which will be helpful in

expanding the business.

It is difficult to prepare as it deals with

numerical data and its evaluation.

Flexible budget- It means the budget that accounts for the adjustment of the changes in

the activities of the business. It is also called as the variable budget. It makes use o0f the

revenues and the expenses that are been produced in present production in terms of the baseline

and makes estimations on the ways in which these revenues and expenses will be changing on

the basis of the modifications in output. An ABC Ltd (Hopper and Bui, 2016). makes use of this

budget in order to predict the best or the worse scenarios for upcoming periods.

Advantages Disadvantages

Flexible budget allows for adjustment of the

changes in terms of the costa and the profit

margins within the activities of the business so

that such changes can be easily handled.

It facilitates the control over the cost in the

better way as it helps in reacting quickly

towards the adverse conditions.

As under this budget the sales revenue and the

expenses are consistently adjusted based on the

present operating conditions, so the ABC Ltd.

can get the updated data with current trends.

It provides for forecasting of the receipts and

the expenses for the coming period (Latan and

et.al., 2018). It also facilitates comparison in

between previous and the present results so

that reasons for decrease in the particular items

could be assessed.

It referred as the time extensive technique

because adjusting the changes on a regular

basis almost accounts for the preparation of the

new budget (Curry, 2019). Due to this a lot of

time of the managers gets wasted in making

budget and he couldn't focus on the important

task within the business.

Managers of the ABC Ltd. faces difficulty in

forecasting the flexible expenses. For example-

changes in the legislation relating to increase in

the labour cost cannot be forecasted.

Formulating a flexible budget is stated as the

complex task because it includes timely

recording of the changes.

10

the opportunities which will be helpful in

expanding the business.

It is difficult to prepare as it deals with

numerical data and its evaluation.

Flexible budget- It means the budget that accounts for the adjustment of the changes in

the activities of the business. It is also called as the variable budget. It makes use o0f the

revenues and the expenses that are been produced in present production in terms of the baseline

and makes estimations on the ways in which these revenues and expenses will be changing on

the basis of the modifications in output. An ABC Ltd (Hopper and Bui, 2016). makes use of this

budget in order to predict the best or the worse scenarios for upcoming periods.

Advantages Disadvantages

Flexible budget allows for adjustment of the

changes in terms of the costa and the profit

margins within the activities of the business so

that such changes can be easily handled.

It facilitates the control over the cost in the

better way as it helps in reacting quickly

towards the adverse conditions.

As under this budget the sales revenue and the

expenses are consistently adjusted based on the

present operating conditions, so the ABC Ltd.

can get the updated data with current trends.

It provides for forecasting of the receipts and

the expenses for the coming period (Latan and

et.al., 2018). It also facilitates comparison in

between previous and the present results so

that reasons for decrease in the particular items

could be assessed.

It referred as the time extensive technique

because adjusting the changes on a regular

basis almost accounts for the preparation of the

new budget (Curry, 2019). Due to this a lot of

time of the managers gets wasted in making

budget and he couldn't focus on the important

task within the business.

Managers of the ABC Ltd. faces difficulty in

forecasting the flexible expenses. For example-

changes in the legislation relating to increase in

the labour cost cannot be forecasted.

Formulating a flexible budget is stated as the

complex task because it includes timely

recording of the changes.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.