Management Accounting for Planning and Control: ABC System Analysis

VerifiedAdded on 2022/11/23

|7

|1269

|384

Report

AI Summary

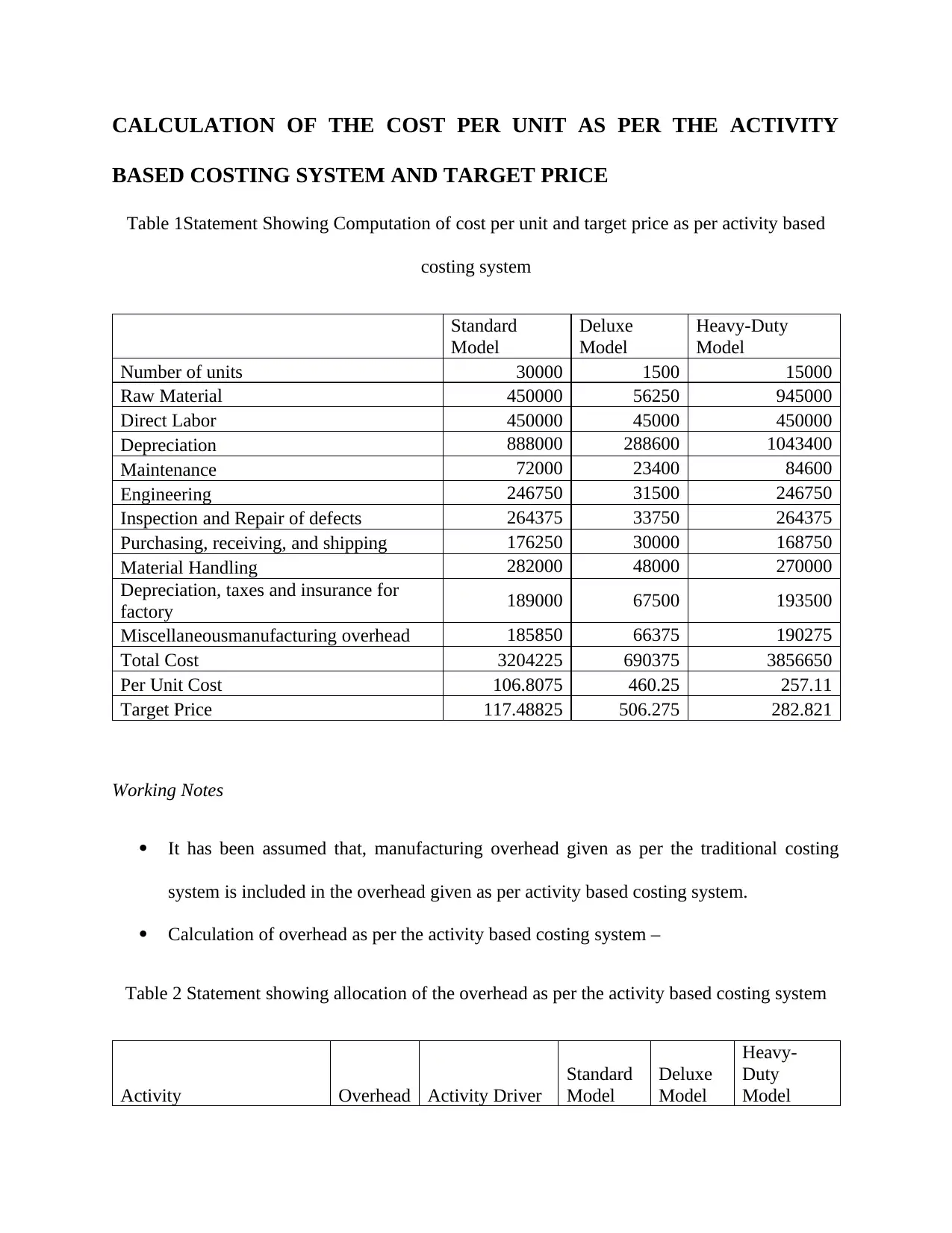

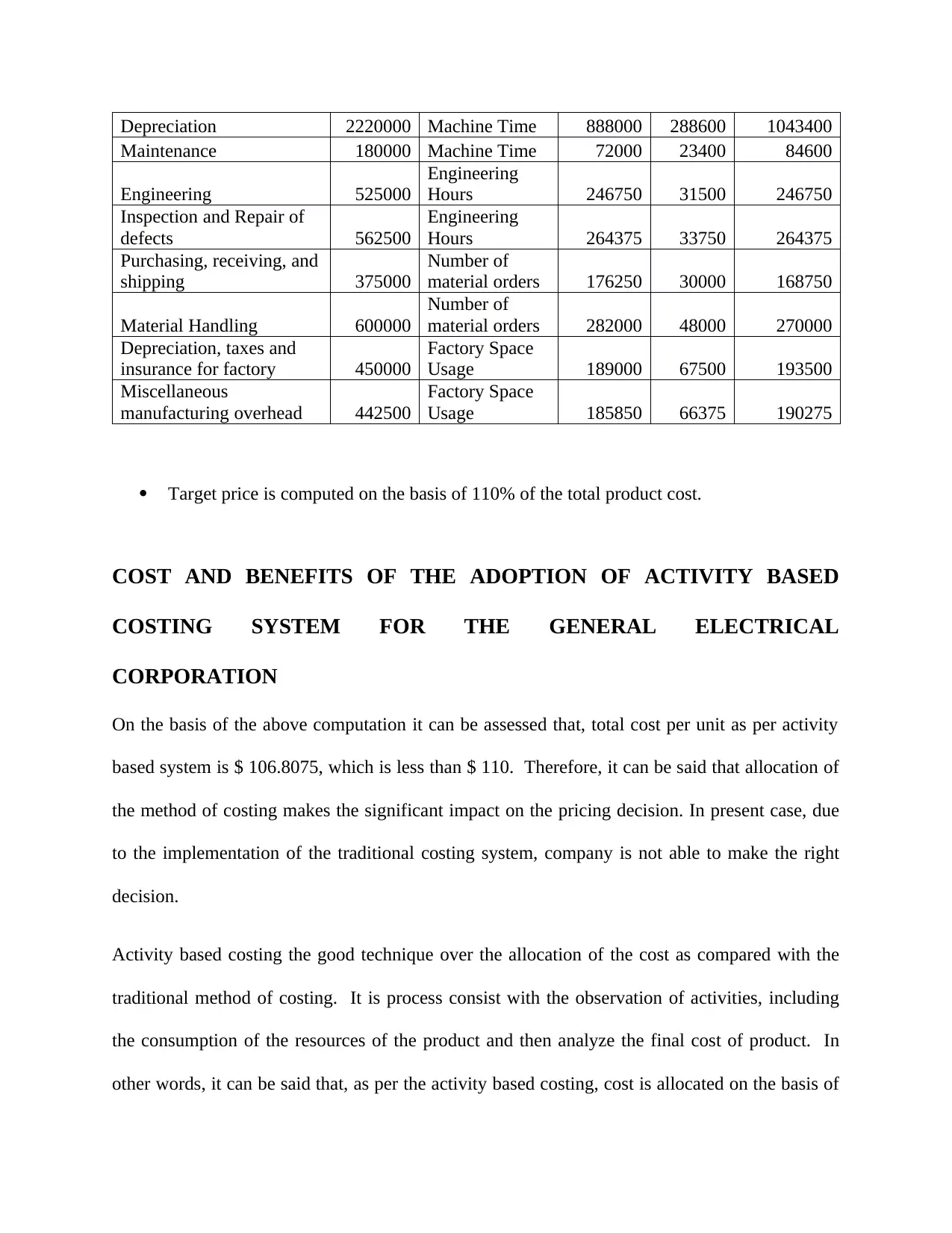

This report analyzes the implementation of activity-based costing (ABC) in comparison to traditional costing systems for the General Electrical Corporation. It begins by outlining the problems associated with traditional costing, such as inaccurate overhead allocation and its impact on pricing decisions. The report then presents detailed calculations of cost per unit and target prices using the ABC system for three product models. A comparative analysis is provided, highlighting the benefits of adopting ABC, including improved cost accuracy, better resource utilization, and enhanced decision-making capabilities. The report concludes with a discussion on the advantages and challenges of implementing ABC, supported by relevant references.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.