Management Accounting Report: Cost Analysis, Planning Methodologies

VerifiedAdded on 2020/01/07

|15

|5172

|186

Report

AI Summary

This report provides a comprehensive overview of management accounting, encompassing essential concepts and practical applications. It begins by defining management accounting and its significance in strategic decision-making, emphasizing the need for qualified professionals to guide companies toward their objectives. The report delves into various methods, including traditional and lean accounting, highlighting their roles in cost reduction, efficiency, and strategic planning. It explores different reporting tools such as job cost reports and inventory management reports, crucial for assessing performance and making informed decisions. Furthermore, the report analyzes cost computation techniques, specifically absorption and marginal costing, and demonstrates their application in framing income statements. It also examines the benefits and drawbacks of different planning methodologies used for budgetary control, and how management accounting systems can be utilized to address financial challenges. Finally, the report provides a detailed income statement comparison using both absorption and marginal costing methods, offering a practical understanding of their impact on financial reporting and decision-making.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

P.1 Management accounting and its mandatory requirements for making ................................3

P.2 Methods used for the management accounting:....................................................................5

P.3 Computation costs via adequate techniques of cost analysis to frame an income statement

through marginal and absorption costs:......................................................................................7

P.4 Benefits and disadvantages of different kinds of planning methodologies used for

budgetary control:.......................................................................................................................9

P.5 Management accounting system is used to face the financial problems:...........................12

CONCLUSION:.............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

P.1 Management accounting and its mandatory requirements for making ................................3

P.2 Methods used for the management accounting:....................................................................5

P.3 Computation costs via adequate techniques of cost analysis to frame an income statement

through marginal and absorption costs:......................................................................................7

P.4 Benefits and disadvantages of different kinds of planning methodologies used for

budgetary control:.......................................................................................................................9

P.5 Management accounting system is used to face the financial problems:...........................12

CONCLUSION:.............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accountants are the qualified specialist through which company is able to make

their strategy for the attainment of their set objectives and goals. With the help of management

accounting practice, company will frame their strategy in order to attain the goals. Nowadays,

decision making is an important task for making company sustainable(Talha, Raja and

Seetharaman, 2010). It requires the quality team to make the effective decision for the viable of

the firm. This is the main tool so that the management can be effectively made and make the

company profitable. Now effective decision making is necessary for the development of the

company and this could be done with the help of qualified management accountants. Now, there

is need for selecting the qualified staff and this is done via effective HR policies.

P.1 Management accounting and its mandatory requirements for making

Management accounting is the process by which reports and accounts are made and also

provides the exact and beneficial information which is needed by the managers of the company

to make their routine operation in a better way(Vaivio and Sirén, 2010). Management accounting

is a different from the financial accounting and make monthly and quarterly reports for the

company’s inner management or staff like production managers and managing directors so that

they could frame their better policies and also assist in getting the sustainable development.

Mainly these kind of reports displays the current cash, sales outstanding debts, company’s stock

etc. and also assist the company to make trend chart, variance research. However, management

accounting helps the company to frame the accounting information for providing effective

information within the organization(0van der Meer-Kooistra and Vosselman, 2012). However,

there are the three main areas where management accounting practices can be done. These are:

1.Strategic management: Management accountant plays a crucial role for making the

effective strategy so that the effective policies could frame and also better decision can be

designed.

2.Performance management: Management accountant emerges the practice of designing

better decision making and handling the performance of the company.

3. Risk management: Management accounting helps the firm to effectively mange the

risk and also try to eliminate it with the better performance for the firm’s division. With the help

Management accountants are the qualified specialist through which company is able to make

their strategy for the attainment of their set objectives and goals. With the help of management

accounting practice, company will frame their strategy in order to attain the goals. Nowadays,

decision making is an important task for making company sustainable(Talha, Raja and

Seetharaman, 2010). It requires the quality team to make the effective decision for the viable of

the firm. This is the main tool so that the management can be effectively made and make the

company profitable. Now effective decision making is necessary for the development of the

company and this could be done with the help of qualified management accountants. Now, there

is need for selecting the qualified staff and this is done via effective HR policies.

P.1 Management accounting and its mandatory requirements for making

Management accounting is the process by which reports and accounts are made and also

provides the exact and beneficial information which is needed by the managers of the company

to make their routine operation in a better way(Vaivio and Sirén, 2010). Management accounting

is a different from the financial accounting and make monthly and quarterly reports for the

company’s inner management or staff like production managers and managing directors so that

they could frame their better policies and also assist in getting the sustainable development.

Mainly these kind of reports displays the current cash, sales outstanding debts, company’s stock

etc. and also assist the company to make trend chart, variance research. However, management

accounting helps the company to frame the accounting information for providing effective

information within the organization(0van der Meer-Kooistra and Vosselman, 2012). However,

there are the three main areas where management accounting practices can be done. These are:

1.Strategic management: Management accountant plays a crucial role for making the

effective strategy so that the effective policies could frame and also better decision can be

designed.

2.Performance management: Management accountant emerges the practice of designing

better decision making and handling the performance of the company.

3. Risk management: Management accounting helps the firm to effectively mange the

risk and also try to eliminate it with the better performance for the firm’s division. With the help

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of management accountant officer, company could able to manage their risk and that is why it

can focus on the development of the firm(Van Helden and et. al., 2010).

However, management accounting main task is for planning and providing decision support for

the management of the firm for effective and efficient running of the company. Management also

assist the company’s management in framing and presentation of financial and other decision

oriented information for formulation of strategy for the planning and control of the routine

activities of the company.

There are so many accounting practices have been adopted since the emergence of the

corporate world.

Traditional management accounting: Earlier, organizations were limited to the traditional

management accounting approach that was mainly applied to cost accounting. And this was only

concerned to the cost of the product, as it is also depends on how to calculate and minimize the

cost and additionally, helps to minimize the cost. During the modern company concept, a great

deal of creation was transferred from people to huge organizations. The entire manufacturing and

selling comprised of a few change forms which were altogether performed in these huge firms.

Transformation procedure that some time ago were provided at a cost through market exchanges

moved toward becoming performed inside one association(Weißenberger and Angelkort, 2011).

A great deal of internal transaction happened as transformation procedures provided their profits

to a next procedure inside the association as opposed to offering their profit available.

Proprietors of these big organizations conceived frameworks to abridge the productivity by

which labour and material were converted over to finished product. These traditional accounting

system delivered proficiency measures, for example, cost every hour or cost per pound created

per process and per laborer.

Lean accounting: this accounting technique is differ from the traditional accounting

system. As, this accounting system does not only focus in the cost reduction process but also to

help the management of the company to make the strategy for the producing the better output

with the least cost. As this is the modern accounting technique(marginal cost. 2017). Lean

accounting helps the company to change the accounting , management procedure so that

effective manufacturing process can be done. Lean accounting technique enhanced the cost as

standard costing implement the labour and overheads cost. There is only one negative impact of

lean accounting which associated the standard costing in the manufacturing process. Lean

can focus on the development of the firm(Van Helden and et. al., 2010).

However, management accounting main task is for planning and providing decision support for

the management of the firm for effective and efficient running of the company. Management also

assist the company’s management in framing and presentation of financial and other decision

oriented information for formulation of strategy for the planning and control of the routine

activities of the company.

There are so many accounting practices have been adopted since the emergence of the

corporate world.

Traditional management accounting: Earlier, organizations were limited to the traditional

management accounting approach that was mainly applied to cost accounting. And this was only

concerned to the cost of the product, as it is also depends on how to calculate and minimize the

cost and additionally, helps to minimize the cost. During the modern company concept, a great

deal of creation was transferred from people to huge organizations. The entire manufacturing and

selling comprised of a few change forms which were altogether performed in these huge firms.

Transformation procedure that some time ago were provided at a cost through market exchanges

moved toward becoming performed inside one association(Weißenberger and Angelkort, 2011).

A great deal of internal transaction happened as transformation procedures provided their profits

to a next procedure inside the association as opposed to offering their profit available.

Proprietors of these big organizations conceived frameworks to abridge the productivity by

which labour and material were converted over to finished product. These traditional accounting

system delivered proficiency measures, for example, cost every hour or cost per pound created

per process and per laborer.

Lean accounting: this accounting technique is differ from the traditional accounting

system. As, this accounting system does not only focus in the cost reduction process but also to

help the management of the company to make the strategy for the producing the better output

with the least cost. As this is the modern accounting technique(marginal cost. 2017). Lean

accounting helps the company to change the accounting , management procedure so that

effective manufacturing process can be done. Lean accounting technique enhanced the cost as

standard costing implement the labour and overheads cost. There is only one negative impact of

lean accounting which associated the standard costing in the manufacturing process. Lean

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accounting is worked hard to overcome the waste cost from the cost process so that the company

will able to make company’s product profitable.

Importance of lean accounting: with the assistance of lean accounting , Astra Zeneca’s

management accountant can make the policies for the cost diminishment of goods. It is assessed

that if every one of the employee or member have thought regarding the lean accounting then

they could see how to segregate cost in various division in orderly way. This kind of accounting

data gives extensive variety of information to top administration to settle on most decision(Cost-

Volume Profit Analysis. 2017). Lean accounting additionally roll out successful improvements

in value chain exercises of firm which provides absorption of cost in various operational division

of Astra Zeneca. Management of firms implement this data to settle on an important decision

making and furthermore gives extensive variety of data to reviewers of organization to review

interior and outside elements of associations.

Cost accounting system: This is the system under which all the costs related to the cost of

production assessed in a great manner. With the help of this framework, company is able to

lower the cost in a most effective manner. The cited company also need to make their

business operations in an effective manner. As, this technique, eliminate the wastage costs

form the production process.

Inventory management system: This is the system which is used in order to control the

inventory in an effective manner (Ward, 2012). Inventory management also helps the firm to

assess the stock level and tries to optimum utilise it in a most effective manner.

Job costing system: This is the costing tool which is used in the firm in order to assess the

individual costs or each job cost. Job costs is assigned for a batch of products. Ususally, such

kind of system is implemented at the time when the goods are different from others. Such job

costs reflects direct material, labour and overheads costs connected to the production.

P.2 Methods used for the management accounting reporting:

There are different instruments to report the management accounting. These strategies

can be utilized to make for the organization's future venture of the organization. Such tools and

methodologies are used in management accounting reporting for effective running of the firm

and also to make the company to make profitable and viable. These will also assist the firm for

making efficient decision making. Some of the management accounting reporting tools are

mentioned hereunder:

will able to make company’s product profitable.

Importance of lean accounting: with the assistance of lean accounting , Astra Zeneca’s

management accountant can make the policies for the cost diminishment of goods. It is assessed

that if every one of the employee or member have thought regarding the lean accounting then

they could see how to segregate cost in various division in orderly way. This kind of accounting

data gives extensive variety of information to top administration to settle on most decision(Cost-

Volume Profit Analysis. 2017). Lean accounting additionally roll out successful improvements

in value chain exercises of firm which provides absorption of cost in various operational division

of Astra Zeneca. Management of firms implement this data to settle on an important decision

making and furthermore gives extensive variety of data to reviewers of organization to review

interior and outside elements of associations.

Cost accounting system: This is the system under which all the costs related to the cost of

production assessed in a great manner. With the help of this framework, company is able to

lower the cost in a most effective manner. The cited company also need to make their

business operations in an effective manner. As, this technique, eliminate the wastage costs

form the production process.

Inventory management system: This is the system which is used in order to control the

inventory in an effective manner (Ward, 2012). Inventory management also helps the firm to

assess the stock level and tries to optimum utilise it in a most effective manner.

Job costing system: This is the costing tool which is used in the firm in order to assess the

individual costs or each job cost. Job costs is assigned for a batch of products. Ususally, such

kind of system is implemented at the time when the goods are different from others. Such job

costs reflects direct material, labour and overheads costs connected to the production.

P.2 Methods used for the management accounting reporting:

There are different instruments to report the management accounting. These strategies

can be utilized to make for the organization's future venture of the organization. Such tools and

methodologies are used in management accounting reporting for effective running of the firm

and also to make the company to make profitable and viable. These will also assist the firm for

making efficient decision making. Some of the management accounting reporting tools are

mentioned hereunder:

Job cost reports: With the help of this report, the company would get to know about the actual

performance of the company (Shah, Malik and Malik, 2011). Under this, various costs reports

are used such as, work in progress, variance reports, sales recovery, value added profit summary

and so on. These all are included by the firm in order to have the business in an effective manner.

Inventory management reports: this covers three stock reports. Which are: inventory status

reports. With the help of these reports, company would recheck the status of the company by

locations, time gap and others. Implementing such reports to assess the profitability, turnover and

others for the stock. This is the reports where the company would get to about its actual profits

margin. With the help of this, company would get to assess the business performance. Under

this, various costs are analysed.

Cost accounting reporting: This accounting reporting is a system through which firm can

appoint its cost and it can display its cost figures as per the unit of thing. Cost accounting

supports the firm for solving the cost issue and attempt to understand them with the assistance of

cost accountant inside the firm. Cost accounting is essentially is required in the assembling firm

and organization likewise makes the procedure related technique for the limiting of the cost of

products with the assistance of cost accountants (Sánchez-Rodríguez and Spraakman, 2012).

Through a predominant cost distribution system, Astra Zeneca could execute better techniques

which can help them in diminish the cost of the manufacturing the product (Quinn, 2011).

P.3 Computation costs via adequate techniques of cost analysis to frame an income statement

through marginal and absorption costs:

There are such a large number of routes by which organization can figure the net benefits.

Management accounting helps the organization to compute the net profits of the

organization. By means of absorption costing and marginal costing, Astra Zeneca can

ascertain the net profits.

Absorption costing: it is the procedure which is utilized to separate the diverse costs which

are connected to the different production processes(Pipan and Czarniawska, 2010). This

philosophy additionally help the organization to evaluate the stock of a firm. Estimating is

additionally the main segments of the firm. Through this strategies whole assembling costs

can be ascertained when they really happened, budgeted costs could fluctuate from the actual

one. By means of absorption costing, over and under absorption could be dealt with in like

manner.

performance of the company (Shah, Malik and Malik, 2011). Under this, various costs reports

are used such as, work in progress, variance reports, sales recovery, value added profit summary

and so on. These all are included by the firm in order to have the business in an effective manner.

Inventory management reports: this covers three stock reports. Which are: inventory status

reports. With the help of these reports, company would recheck the status of the company by

locations, time gap and others. Implementing such reports to assess the profitability, turnover and

others for the stock. This is the reports where the company would get to about its actual profits

margin. With the help of this, company would get to assess the business performance. Under

this, various costs are analysed.

Cost accounting reporting: This accounting reporting is a system through which firm can

appoint its cost and it can display its cost figures as per the unit of thing. Cost accounting

supports the firm for solving the cost issue and attempt to understand them with the assistance of

cost accountant inside the firm. Cost accounting is essentially is required in the assembling firm

and organization likewise makes the procedure related technique for the limiting of the cost of

products with the assistance of cost accountants (Sánchez-Rodríguez and Spraakman, 2012).

Through a predominant cost distribution system, Astra Zeneca could execute better techniques

which can help them in diminish the cost of the manufacturing the product (Quinn, 2011).

P.3 Computation costs via adequate techniques of cost analysis to frame an income statement

through marginal and absorption costs:

There are such a large number of routes by which organization can figure the net benefits.

Management accounting helps the organization to compute the net profits of the

organization. By means of absorption costing and marginal costing, Astra Zeneca can

ascertain the net profits.

Absorption costing: it is the procedure which is utilized to separate the diverse costs which

are connected to the different production processes(Pipan and Czarniawska, 2010). This

philosophy additionally help the organization to evaluate the stock of a firm. Estimating is

additionally the main segments of the firm. Through this strategies whole assembling costs

can be ascertained when they really happened, budgeted costs could fluctuate from the actual

one. By means of absorption costing, over and under absorption could be dealt with in like

manner.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

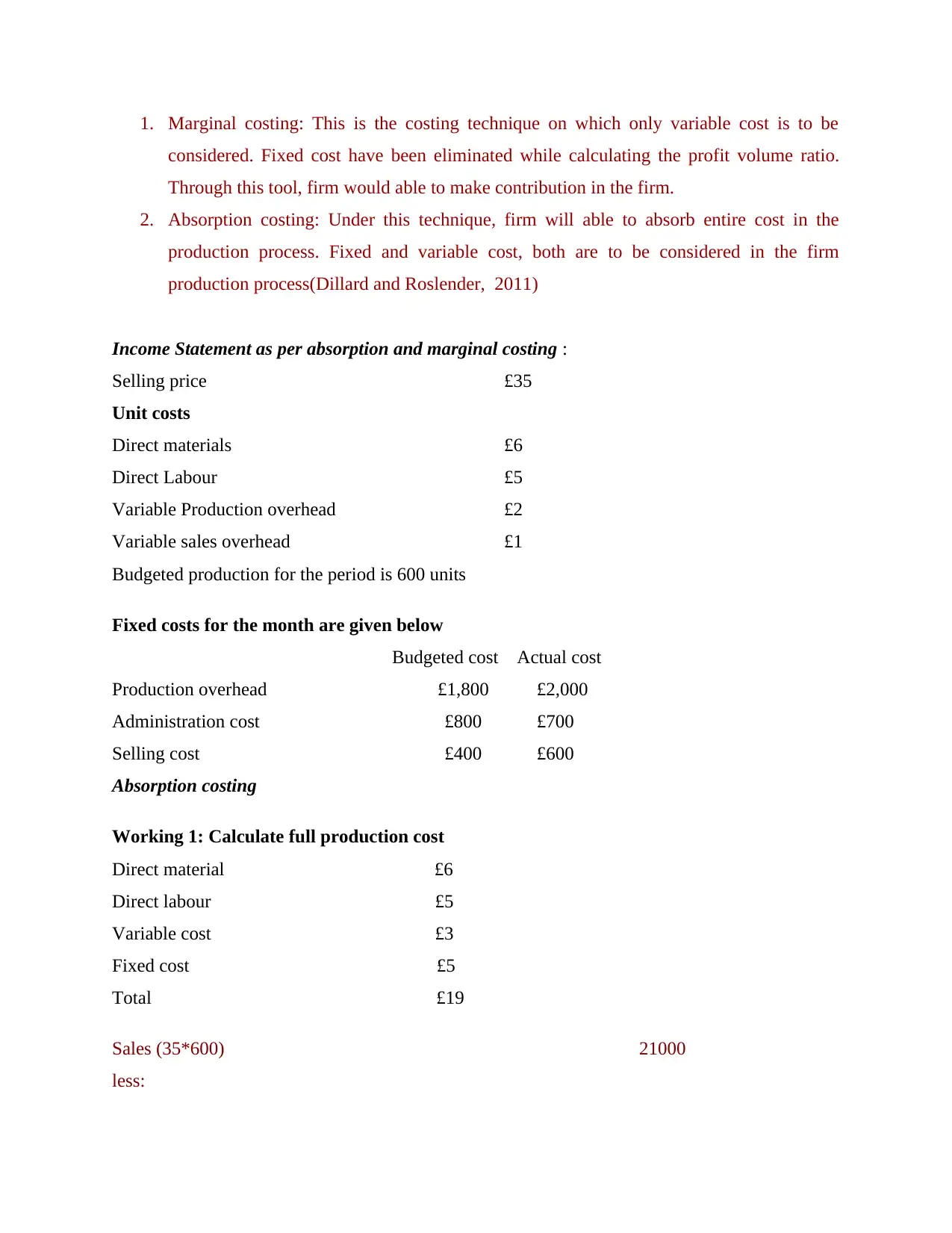

1. Marginal costing: This is the costing technique on which only variable cost is to be

considered. Fixed cost have been eliminated while calculating the profit volume ratio.

Through this tool, firm would able to make contribution in the firm.

2. Absorption costing: Under this technique, firm will able to absorb entire cost in the

production process. Fixed and variable cost, both are to be considered in the firm

production process(Dillard and Roslender, 2011)

Income Statement as per absorption and marginal costing :

Selling price £35

Unit costs

Direct materials £6

Direct Labour £5

Variable Production overhead £2

Variable sales overhead £1

Budgeted production for the period is 600 units

Fixed costs for the month are given below

Budgeted cost Actual cost

Production overhead £1,800 £2,000

Administration cost £800 £700

Selling cost £400 £600

Absorption costing

Working 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £3

Fixed cost £5

Total £19

Sales (35*600) 21000

less:

considered. Fixed cost have been eliminated while calculating the profit volume ratio.

Through this tool, firm would able to make contribution in the firm.

2. Absorption costing: Under this technique, firm will able to absorb entire cost in the

production process. Fixed and variable cost, both are to be considered in the firm

production process(Dillard and Roslender, 2011)

Income Statement as per absorption and marginal costing :

Selling price £35

Unit costs

Direct materials £6

Direct Labour £5

Variable Production overhead £2

Variable sales overhead £1

Budgeted production for the period is 600 units

Fixed costs for the month are given below

Budgeted cost Actual cost

Production overhead £1,800 £2,000

Administration cost £800 £700

Selling cost £400 £600

Absorption costing

Working 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £3

Fixed cost £5

Total £19

Sales (35*600) 21000

less:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

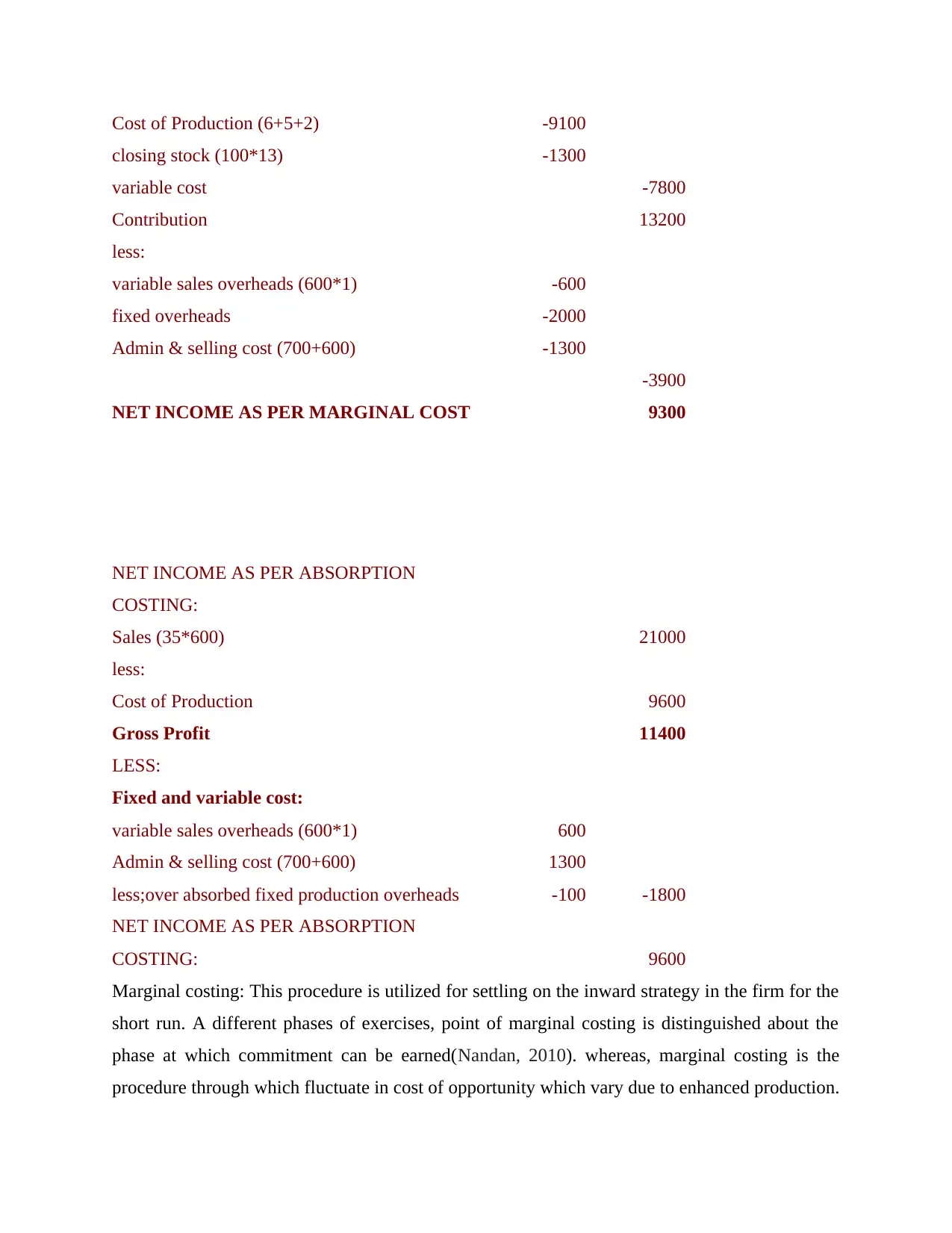

Cost of Production (6+5+2) -9100

closing stock (100*13) -1300

variable cost -7800

Contribution 13200

less:

variable sales overheads (600*1) -600

fixed overheads -2000

Admin & selling cost (700+600) -1300

-3900

NET INCOME AS PER MARGINAL COST 9300

NET INCOME AS PER ABSORPTION

COSTING:

Sales (35*600) 21000

less:

Cost of Production 9600

Gross Profit 11400

LESS:

Fixed and variable cost:

variable sales overheads (600*1) 600

Admin & selling cost (700+600) 1300

less;over absorbed fixed production overheads -100 -1800

NET INCOME AS PER ABSORPTION

COSTING: 9600

Marginal costing: This procedure is utilized for settling on the inward strategy in the firm for the

short run. A different phases of exercises, point of marginal costing is distinguished about the

phase at which commitment can be earned(Nandan, 2010). whereas, marginal costing is the

procedure through which fluctuate in cost of opportunity which vary due to enhanced production.

closing stock (100*13) -1300

variable cost -7800

Contribution 13200

less:

variable sales overheads (600*1) -600

fixed overheads -2000

Admin & selling cost (700+600) -1300

-3900

NET INCOME AS PER MARGINAL COST 9300

NET INCOME AS PER ABSORPTION

COSTING:

Sales (35*600) 21000

less:

Cost of Production 9600

Gross Profit 11400

LESS:

Fixed and variable cost:

variable sales overheads (600*1) 600

Admin & selling cost (700+600) 1300

less;over absorbed fixed production overheads -100 -1800

NET INCOME AS PER ABSORPTION

COSTING: 9600

Marginal costing: This procedure is utilized for settling on the inward strategy in the firm for the

short run. A different phases of exercises, point of marginal costing is distinguished about the

phase at which commitment can be earned(Nandan, 2010). whereas, marginal costing is the

procedure through which fluctuate in cost of opportunity which vary due to enhanced production.

Fluctuate in the opportunity cost because of improved production by unit over the specific level

can be recognized as marginal cost for the organization. Marginal costing manages the

managerial cost of creating that additional unit.

P.4 Benefits and disadvantages of different kinds of planning methodologies used for budgetary

control:

Budgetary control is necessary for the effective operation of business and this could help

in making the company sustainable. Now, there has been some advantages and disadvantages as

well of for budgetary control(Lee, 2011). Budgetary control assist the Astra Geneca company so

that the company could able to make the effective plan for the business, improved the efficiency

as well, improving the communication as well for the betterment of the firm, control the firm, co-

ordination the entire departments of the firm, motivation of the employees, maximizing the

revenues of the firm, estimating the loan or funding requirement of the firm and assist in making

the uniform policies. There are different types of budgets which are designed in order to maintain

balance in the organisation. Some of them are:

Master budget – it is the biggest budget which is made after analysing al the other small

budgets. It controls the overall inflow and outflow of funds which is necessary to

maintain the overall performance of the organisation.

Cash budget – It is specifically design to set the cash targets against each department.

Through this system allocation of finance is done in the most productive manner.

Capital expenditure budget – every year management needs to take decision regarding

purchase of fixed assets in order to increase the scale of operations. Under this budgeting

system an amount is kept aside which will be utilised to acquire new resources.

Each of the above budgetary tool has their own advantages and disadvantages which are

discussed below:

Positives:

Assist in planning: Planning is the basic requirement for any firm's development. This is

the tool by which company would able to make the effective decision and strategy for the

betterment of the objectives. This is the primary stage which is needed before

implementing the plan of the firm (Luft and Shields, 2010). By this tool, company would

able to know the in and out about the future projects on which company need to work.

like- cost of project, labour requirements, material requirements and so many things have

can be recognized as marginal cost for the organization. Marginal costing manages the

managerial cost of creating that additional unit.

P.4 Benefits and disadvantages of different kinds of planning methodologies used for budgetary

control:

Budgetary control is necessary for the effective operation of business and this could help

in making the company sustainable. Now, there has been some advantages and disadvantages as

well of for budgetary control(Lee, 2011). Budgetary control assist the Astra Geneca company so

that the company could able to make the effective plan for the business, improved the efficiency

as well, improving the communication as well for the betterment of the firm, control the firm, co-

ordination the entire departments of the firm, motivation of the employees, maximizing the

revenues of the firm, estimating the loan or funding requirement of the firm and assist in making

the uniform policies. There are different types of budgets which are designed in order to maintain

balance in the organisation. Some of them are:

Master budget – it is the biggest budget which is made after analysing al the other small

budgets. It controls the overall inflow and outflow of funds which is necessary to

maintain the overall performance of the organisation.

Cash budget – It is specifically design to set the cash targets against each department.

Through this system allocation of finance is done in the most productive manner.

Capital expenditure budget – every year management needs to take decision regarding

purchase of fixed assets in order to increase the scale of operations. Under this budgeting

system an amount is kept aside which will be utilised to acquire new resources.

Each of the above budgetary tool has their own advantages and disadvantages which are

discussed below:

Positives:

Assist in planning: Planning is the basic requirement for any firm's development. This is

the tool by which company would able to make the effective decision and strategy for the

betterment of the objectives. This is the primary stage which is needed before

implementing the plan of the firm (Luft and Shields, 2010). By this tool, company would

able to know the in and out about the future projects on which company need to work.

like- cost of project, labour requirements, material requirements and so many things have

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

to know in advance. Astra Geneca will also know the money that company are going to

spend on a certain project and company also know the incoming of capital which have

been received in future year.

Increase the productivity: The firm total output can be improved with the help of

budgetary control. This is the tool by which company would able to make their

productivity better so that the company would able to gain the better profits and that is

why firm can make sustainable development (Kaplan and Atkinson, 2015).

Adequate communication: With the help of proper communication among the each

departments of the firm, company could perform in a better way and also make their

operation so effective at providing timely information.

Control: Budgetary control assist the organisation to control the whole firm so that the

firm could eliminate the waste from each divisions and make the company so profitable.

Budget makes the firm to compare the actual outcomes with the expected outcomes and

then strive hard to eliminate the deviation between the two process(Lukka and Modell,

2010). Also, company will take a decisions effectively via controlling.

Co-ordination: This will assist the company to co-ordinate each departments for the

effective utilization of human resources. Budget process encourage the co-ordination

among various department of the firm. It supports the centralised regulations of

heterogeneous operations. The budget committee perform as a co-ordinator of operations,

sales and other divisions. The significant quality of budget planning is that it organizes

exercises across over other departments.

Delegation of authority: Budget appreciates the delegation of authority. It set the target

within which the delegated authority can be implemented(Jansen, 2011). Lower level

authority could act initiatives and judgement within the budgetary limits.

Motivation: Budget assist the company to stimulate the performance of the firm and also

motivates the employees to do better with the company's operations. Motivation is the

tool by which employees feel associated to the firm and do work with more efficiency so

that the firm would able to make its operations more profitable.

Maximization of revenues: Budget helps the company to utilize firms human and other

resources effectively so that the maximum output can gain. This is the tool by which the

firm would able to boost their revenues and also think about their diversification.

spend on a certain project and company also know the incoming of capital which have

been received in future year.

Increase the productivity: The firm total output can be improved with the help of

budgetary control. This is the tool by which company would able to make their

productivity better so that the company would able to gain the better profits and that is

why firm can make sustainable development (Kaplan and Atkinson, 2015).

Adequate communication: With the help of proper communication among the each

departments of the firm, company could perform in a better way and also make their

operation so effective at providing timely information.

Control: Budgetary control assist the organisation to control the whole firm so that the

firm could eliminate the waste from each divisions and make the company so profitable.

Budget makes the firm to compare the actual outcomes with the expected outcomes and

then strive hard to eliminate the deviation between the two process(Lukka and Modell,

2010). Also, company will take a decisions effectively via controlling.

Co-ordination: This will assist the company to co-ordinate each departments for the

effective utilization of human resources. Budget process encourage the co-ordination

among various department of the firm. It supports the centralised regulations of

heterogeneous operations. The budget committee perform as a co-ordinator of operations,

sales and other divisions. The significant quality of budget planning is that it organizes

exercises across over other departments.

Delegation of authority: Budget appreciates the delegation of authority. It set the target

within which the delegated authority can be implemented(Jansen, 2011). Lower level

authority could act initiatives and judgement within the budgetary limits.

Motivation: Budget assist the company to stimulate the performance of the firm and also

motivates the employees to do better with the company's operations. Motivation is the

tool by which employees feel associated to the firm and do work with more efficiency so

that the firm would able to make its operations more profitable.

Maximization of revenues: Budget helps the company to utilize firms human and other

resources effectively so that the maximum output can gain. This is the tool by which the

firm would able to boost their revenues and also think about their diversification.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Estimating fund requirement: budget is the technique which is used to make their

operation effective and also helps the finance managers to understand the need of the

capital for their existing operations or new one(Macintosh and Quattrone, 2010).

Budget plans can possibly help associations and their employees achieve their objectives.

Budget control offers a few points of interest to supervisors. Some of these are:

Budget plan make an interpretation of vital arrangements enthusiastically. They

determine the resources, incomes, and exercises required to complete the vital strategic

plan for the next year.

Budget plans convert strategic plan into action .

Enhance communication with workers.

Budget enhance resource allocation, since all request are explained and supported.

These above mentioned are the advantages of the budget. However, there are some

disadvantages as well which also need to discuss by the company so that the managers of the

firm would analyse the disadvantages as well for taking decisions effectively(.Hiebl, 2014).

Disadvantages of budgetary tool

The significant issue happens when budget plans are connected mechanically and

inflexibly.

Budget plans can demotivate workers on account of absence of support in the work. If,

the budget plans are forced top down, representatives won't know the purpose behind

budgeted expenditure, and won't be focused on them.

Budget plans can bring about view of unfairness.

It can make rivalry for resources and legislative issues.

A inflexible budget structure decreases activity and advancement at lower levels, making

it difficult to get funds for new thoughts.

It is a complex process to design a master budget

Much cost has to be incurred in hiring a capable individual who can design an effective

budget.

It reduces the level of flexibility in operation's.

These aspects of budget plans frameworks may interfere for the accomplishment of the

Astra Zeneca objectives. One for the most part acknowledged rule for powerful budgeting is to

build up objectives that are troublesome yet achievable. Therefore, most proficient managers or

operation effective and also helps the finance managers to understand the need of the

capital for their existing operations or new one(Macintosh and Quattrone, 2010).

Budget plans can possibly help associations and their employees achieve their objectives.

Budget control offers a few points of interest to supervisors. Some of these are:

Budget plan make an interpretation of vital arrangements enthusiastically. They

determine the resources, incomes, and exercises required to complete the vital strategic

plan for the next year.

Budget plans convert strategic plan into action .

Enhance communication with workers.

Budget enhance resource allocation, since all request are explained and supported.

These above mentioned are the advantages of the budget. However, there are some

disadvantages as well which also need to discuss by the company so that the managers of the

firm would analyse the disadvantages as well for taking decisions effectively(.Hiebl, 2014).

Disadvantages of budgetary tool

The significant issue happens when budget plans are connected mechanically and

inflexibly.

Budget plans can demotivate workers on account of absence of support in the work. If,

the budget plans are forced top down, representatives won't know the purpose behind

budgeted expenditure, and won't be focused on them.

Budget plans can bring about view of unfairness.

It can make rivalry for resources and legislative issues.

A inflexible budget structure decreases activity and advancement at lower levels, making

it difficult to get funds for new thoughts.

It is a complex process to design a master budget

Much cost has to be incurred in hiring a capable individual who can design an effective

budget.

It reduces the level of flexibility in operation's.

These aspects of budget plans frameworks may interfere for the accomplishment of the

Astra Zeneca objectives. One for the most part acknowledged rule for powerful budgeting is to

build up objectives that are troublesome yet achievable. Therefore, most proficient managers or

directors who knows budget plans and how to utilize them so that they would able to attain the

effective control by which they are able to get firm's set objectives.

P.5 Management accounting system is used to face the financial problems:

Management accounting assumes a key part in the firm today. The top accountants in

many associations is the controller. Management accountant officer in the firm are the main

person who took all decisions in finance field and every departmental heads is required to

respond to him covering the cost accountant, finance and tax accountant, internal auditors etc..

Despite the fact that much management accounting starts inside these positions, entire decision

maker in the firm must see how to make and utilize great management accounting data. Today's

innovation permits administration to track performance data that goes beyond the cost-based

data. Great management accounting system includes an obligation to deal with a wide

assortment of crucial information(Herbert and Seal, 2012). Subsequently, those included need to

expect and be ready to manage different ethical dilemmas.

By utilizing diverse instruments and systems which are talked about above administration

become more acquainted with about its unmistakable issues and issues which impact the last

outcomes and execution of the organization. Through utilizing the budgetary apparatuses it is

distinguished that what is the distinction in organizations execution if contrasted it and the earlier

years comes about. Keeping in mind the end goal to defeat such issues a few procedures are

utilized by administration which help them in accomplishing the coveted outcomes and

recognizing the issues behind deviation in expected result. Some of them are given beneath in

detail :

Benchmarking – It is a procedure through which principles are set against a specific

undertaking which helps in influencing the correlation with errand all the more simple. Through

this idea a coveted standard is set which is being normal as a final product. It can be set against

an item, program, techniques and so forth. The principle objective of this arrangement of activity

is to decide the territories which needs additional care and advancement. The other target of

same is to contemplate how organizations is same field are effective in accomplishing their set

execution gauges and furthermore to build the present effectiveness level of workers. It is a

consistent procedure which proceeds till the outcomes are accomplished.

effective control by which they are able to get firm's set objectives.

P.5 Management accounting system is used to face the financial problems:

Management accounting assumes a key part in the firm today. The top accountants in

many associations is the controller. Management accountant officer in the firm are the main

person who took all decisions in finance field and every departmental heads is required to

respond to him covering the cost accountant, finance and tax accountant, internal auditors etc..

Despite the fact that much management accounting starts inside these positions, entire decision

maker in the firm must see how to make and utilize great management accounting data. Today's

innovation permits administration to track performance data that goes beyond the cost-based

data. Great management accounting system includes an obligation to deal with a wide

assortment of crucial information(Herbert and Seal, 2012). Subsequently, those included need to

expect and be ready to manage different ethical dilemmas.

By utilizing diverse instruments and systems which are talked about above administration

become more acquainted with about its unmistakable issues and issues which impact the last

outcomes and execution of the organization. Through utilizing the budgetary apparatuses it is

distinguished that what is the distinction in organizations execution if contrasted it and the earlier

years comes about. Keeping in mind the end goal to defeat such issues a few procedures are

utilized by administration which help them in accomplishing the coveted outcomes and

recognizing the issues behind deviation in expected result. Some of them are given beneath in

detail :

Benchmarking – It is a procedure through which principles are set against a specific

undertaking which helps in influencing the correlation with errand all the more simple. Through

this idea a coveted standard is set which is being normal as a final product. It can be set against

an item, program, techniques and so forth. The principle objective of this arrangement of activity

is to decide the territories which needs additional care and advancement. The other target of

same is to contemplate how organizations is same field are effective in accomplishing their set

execution gauges and furthermore to build the present effectiveness level of workers. It is a

consistent procedure which proceeds till the outcomes are accomplished.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.