Management Accounting Report: Unit 5, BTEC Higher National Diploma

VerifiedAdded on 2023/01/12

|21

|6533

|61

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its application within a business context. It begins by defining management accounting and exploring different types of management accounting systems, such as cost accounting, inventory management, job order costing, and price optimization. The report then details various management accounting reporting methods, including job costing, inventory management, operating budget, accounts receivable aging, and performance reports. It highlights the benefits of these systems, such as improved cost control and enhanced decision-making. The report then delves into practical applications, including cost calculations, income statement preparation using marginal or absorption costing, and the use of planning tools for budgetary control. Furthermore, it examines how organizations adapt management accounting systems to address financial problems, emphasizing the role of these systems in achieving sustainable success. The report uses Grant Thornton and Creams Limited as case studies throughout the analysis, providing real-world examples of management accounting in practice. It addresses the essential requirements of management accounting systems, such as reliability, accuracy, and understandability, and concludes by evaluating how management accounting tools help organizations solve financial issues and achieve sustainable success.

Management

Accounting

1

Accounting

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................4

MAIN BODY...................................................................................................................................4

TASK 1............................................................................................................................................4

P1. Explain management accounting and different types of management accounting systems

along with its essential requirement.............................................................................................4

P2. Describe different method of management accounting reporting which are used by

organizations................................................................................................................................6

M1. Benefits of management accounting systems.......................................................................8

D1. Critically evaluate that how management accounting systems and management

accounting reporting are integrated within organisational processes..........................................8

TASK 2............................................................................................................................................9

P3. Calculate cost by using appreciate cost analysis techniques and prepare income statement

by using marginal or absorption costing method.........................................................................9

M2. Apply range of management accounting techniques and generate financial reporting

statements...................................................................................................................................13

D2.Produce financial reports that accurately apply and interpret data for a range of business

activities.....................................................................................................................................13

TASK 3..........................................................................................................................................14

P4. Explain the advantages and disadvantages of different types of planning tools used

for budgetary control...............................................................................................................14

M3. Analyze the use of different planning tools and their application for preparing

budgets and forecasts..............................................................................................................16

TASK 4..........................................................................................................................................16

P5. Compare how organizations are adapting management accounting systems to

respond to financial problems................................................................................................16

M4.Analyze how, in responding to financial problems, management accounting can lead

organizations to sustainable success......................................................................................19

D3.Evaluate how planning tools for accounting respond appropriately to solving financial

problems to lead organizations to sustainable success..............................................................20

CONCLUSION..............................................................................................................................20

2

MAIN BODY...................................................................................................................................4

TASK 1............................................................................................................................................4

P1. Explain management accounting and different types of management accounting systems

along with its essential requirement.............................................................................................4

P2. Describe different method of management accounting reporting which are used by

organizations................................................................................................................................6

M1. Benefits of management accounting systems.......................................................................8

D1. Critically evaluate that how management accounting systems and management

accounting reporting are integrated within organisational processes..........................................8

TASK 2............................................................................................................................................9

P3. Calculate cost by using appreciate cost analysis techniques and prepare income statement

by using marginal or absorption costing method.........................................................................9

M2. Apply range of management accounting techniques and generate financial reporting

statements...................................................................................................................................13

D2.Produce financial reports that accurately apply and interpret data for a range of business

activities.....................................................................................................................................13

TASK 3..........................................................................................................................................14

P4. Explain the advantages and disadvantages of different types of planning tools used

for budgetary control...............................................................................................................14

M3. Analyze the use of different planning tools and their application for preparing

budgets and forecasts..............................................................................................................16

TASK 4..........................................................................................................................................16

P5. Compare how organizations are adapting management accounting systems to

respond to financial problems................................................................................................16

M4.Analyze how, in responding to financial problems, management accounting can lead

organizations to sustainable success......................................................................................19

D3.Evaluate how planning tools for accounting respond appropriately to solving financial

problems to lead organizations to sustainable success..............................................................20

CONCLUSION..............................................................................................................................20

2

REFERENCES..............................................................................................................................21

3

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is defined as an accounting method that helps an organization to

function better(Weetman, 2019) (Muller, 2019). This can be described as implementing

management approaches and knowledge required to assist all department heads in managing and

controlling the business. It focuses on accounting aspects. The primary role in accounting units is

the compilation and analysis of data. Managers have used the gathered information to routinely

decide. Management accounting required information for managers to fulfil strategic

requirements. In financial reports various management decisions are presented.This report is

based on Grant Thornton which is UK based company and provides professional network

services.They offer financial services to their clients and Creams Limited is one of them. It is UK

based medium size organization which offersice creams, doughnuts, waffles etc.

This assessment covers several topics such as management accounting systems, range of

different accounting techniques which are used to evaluate operational performance. In addition,

it involves planning tools that are used for budgetary control and further evaluate the ways which

helps firms to resolve their financial issues through implementing range of management

accounting techniques.

MAIN BODY

TASK 1

P1. Explain management accounting and different types of management accounting systems

along with its essential requirement

Managerial accounting is an accounting division that deals with the identification,

calculation, review, and evaluation of accounting data so that it can be always had to help

managers make the required decisions to handle the activities of a organization

effectively(Singhand Verma, 2018). In order to perform accounting activities, there are several

management accounting systems which are used by the Creams Limited to improve their

operational efficiency as well as effectiveness. Some of them are as follow:

Cost accounting system: It is known to be the type of accounting management approach

encompassing a variety of activities as well as monetary factors(Cristea, 2018). For businesses it

is necessary to keep costs under estimated. In the Cream Ltd context, this accounting is used to

keep the costs of sales below the estimated costs. The main purpose of this system is to

4

Management accounting is defined as an accounting method that helps an organization to

function better(Weetman, 2019) (Muller, 2019). This can be described as implementing

management approaches and knowledge required to assist all department heads in managing and

controlling the business. It focuses on accounting aspects. The primary role in accounting units is

the compilation and analysis of data. Managers have used the gathered information to routinely

decide. Management accounting required information for managers to fulfil strategic

requirements. In financial reports various management decisions are presented.This report is

based on Grant Thornton which is UK based company and provides professional network

services.They offer financial services to their clients and Creams Limited is one of them. It is UK

based medium size organization which offersice creams, doughnuts, waffles etc.

This assessment covers several topics such as management accounting systems, range of

different accounting techniques which are used to evaluate operational performance. In addition,

it involves planning tools that are used for budgetary control and further evaluate the ways which

helps firms to resolve their financial issues through implementing range of management

accounting techniques.

MAIN BODY

TASK 1

P1. Explain management accounting and different types of management accounting systems

along with its essential requirement

Managerial accounting is an accounting division that deals with the identification,

calculation, review, and evaluation of accounting data so that it can be always had to help

managers make the required decisions to handle the activities of a organization

effectively(Singhand Verma, 2018). In order to perform accounting activities, there are several

management accounting systems which are used by the Creams Limited to improve their

operational efficiency as well as effectiveness. Some of them are as follow:

Cost accounting system: It is known to be the type of accounting management approach

encompassing a variety of activities as well as monetary factors(Cristea, 2018). For businesses it

is necessary to keep costs under estimated. In the Cream Ltd context, this accounting is used to

keep the costs of sales below the estimated costs. The main purpose of this system is to

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

concentrate as much as feasible on keeping the costs of various activities lower. Cost accounting

system essentially required by the Creams Ltd to estimate their product cost and make sure that,

production cost will not going to exceed. Otherwise, it minimise the profit margin which is not

good for the company to run their production so long in this situations.

Inventory management system: The inventory management system is an instrument for

improved stock control across the distribution chain of the company(Welsh, 2018). In Creams

limited the entire delivery process from placing an order to vendors is controlled by this

approach and makes the entire route of one business towards the customer. Through

using inventory management system, sales companies, suppliers, producers, and vendors may

make their businesses successful through making appropriate stock buying decisions. The

program contains critical methodologies such as LIFO, FIFO and Average Costs. Corrective

steps are important for businesses to take to control stored inventories. Company follow FIFO

inventory method which is essentially required to avoid wastage or damage due to store stock for

longer period. Due to this reason, this system essentially required by the organization to keep

tracks their inventory position and make further buying decisions accordingly.

Job order costing: The method of job order tracks the cost of each function within the

company. The management will closely monitor the costs of each job and assess if the real costs

produced are fairly similar and the costs estimated are higher (Hashorva and et.al., 2018). Large

cost shortfalls would compel managers to evaluate and enforce proactive measures to fix the

cause of cost increases. This method gathers and absorbs costs for individual jobs, tasks or work

orders. The cost of each function is correctly measured and each job is individually defined.

They apply such accounting method in the dimension of the above business, in order to

efficiently control the cost of each job. It is essentially required for managers of Cream Ltd, so

they can formulate effective strategies which are essentially required evaluating each order cost

and taking necessary actions accordingly.

Price optimising system: This is a type of management system which involves a detailed

pricing system and customer satisfaction requirements (Bottomleyand Bosman, 2018). This

method of accounting lets companies obtain valuable business trends and information on

customer demands. Basically this accounting method is essential for businesses to change the

market level of products and services. In the case of chosen business their marketing department

adjusts pricing strategies according to the desires of the customer. This system is essential to set

5

system essentially required by the Creams Ltd to estimate their product cost and make sure that,

production cost will not going to exceed. Otherwise, it minimise the profit margin which is not

good for the company to run their production so long in this situations.

Inventory management system: The inventory management system is an instrument for

improved stock control across the distribution chain of the company(Welsh, 2018). In Creams

limited the entire delivery process from placing an order to vendors is controlled by this

approach and makes the entire route of one business towards the customer. Through

using inventory management system, sales companies, suppliers, producers, and vendors may

make their businesses successful through making appropriate stock buying decisions. The

program contains critical methodologies such as LIFO, FIFO and Average Costs. Corrective

steps are important for businesses to take to control stored inventories. Company follow FIFO

inventory method which is essentially required to avoid wastage or damage due to store stock for

longer period. Due to this reason, this system essentially required by the organization to keep

tracks their inventory position and make further buying decisions accordingly.

Job order costing: The method of job order tracks the cost of each function within the

company. The management will closely monitor the costs of each job and assess if the real costs

produced are fairly similar and the costs estimated are higher (Hashorva and et.al., 2018). Large

cost shortfalls would compel managers to evaluate and enforce proactive measures to fix the

cause of cost increases. This method gathers and absorbs costs for individual jobs, tasks or work

orders. The cost of each function is correctly measured and each job is individually defined.

They apply such accounting method in the dimension of the above business, in order to

efficiently control the cost of each job. It is essentially required for managers of Cream Ltd, so

they can formulate effective strategies which are essentially required evaluating each order cost

and taking necessary actions accordingly.

Price optimising system: This is a type of management system which involves a detailed

pricing system and customer satisfaction requirements (Bottomleyand Bosman, 2018). This

method of accounting lets companies obtain valuable business trends and information on

customer demands. Basically this accounting method is essential for businesses to change the

market level of products and services. In the case of chosen business their marketing department

adjusts pricing strategies according to the desires of the customer. This system is essential to set

5

the product price which satisfy consumers as well as meet business objectives. It is essentially

required for the organizations to set suitable price which increase consumers’ willingness to buy

goods and services.

Essential requirement of management accounting systems:

Management accounting systems are essentially required for the organization and make

sure the available information should be reliable, accurate, presentable, updated and in

understanding form. So people can understand and further managers of Cream Ltd can used such

information in decision making process. All essential requirements mentioned below:

Reliable: In context of management accounting systems, all the information should be

reliable because managers will take strategic decisions on the basis of it.

Accurate: Accounting information should be accurate which an essential requirement of

management accounting is. Because it helps in identifying true financial position of the

Cream Ltd in terms of profit and loss.

Presentable: All the accounting information is presented in standard format structure

which is globally used by the organizations to understand other’s financial reports.

Up to date and on time: In the financial report, data recorded on quarterly or yearly

basis because managers of Cream Ltd make decisions on the basis of it and it is an

essentially required for decision making process to get updated data.

Understandable and relevant: Data should be recorded in understandable manner, so

people of Cream Ltd can understand or perform their task accordingly.

Above discussed management accounting systems are very essential for organization to

perform their operational activities and make sure that it will maximise their efficiency as well as

effectiveness. By using these systems, managers of Creams Ltd build effective strategies to

maximise their production, profitability, performance and minimise overall cost of

manufacturing to meet their business goals & objectives.

P2. Describe different method of management accounting reporting which are used by

organizations

Job costing report: Job costing reports are administrative mechanisms used to assess the

performance of a project or output against a defined or expected norm (Quilty, Cosentinoand

Bagby, 2018). They have been used in areas of the market and their associated industries. The

primary objective of reporting on job costing is to recognize differences or favourable results,

6

required for the organizations to set suitable price which increase consumers’ willingness to buy

goods and services.

Essential requirement of management accounting systems:

Management accounting systems are essentially required for the organization and make

sure the available information should be reliable, accurate, presentable, updated and in

understanding form. So people can understand and further managers of Cream Ltd can used such

information in decision making process. All essential requirements mentioned below:

Reliable: In context of management accounting systems, all the information should be

reliable because managers will take strategic decisions on the basis of it.

Accurate: Accounting information should be accurate which an essential requirement of

management accounting is. Because it helps in identifying true financial position of the

Cream Ltd in terms of profit and loss.

Presentable: All the accounting information is presented in standard format structure

which is globally used by the organizations to understand other’s financial reports.

Up to date and on time: In the financial report, data recorded on quarterly or yearly

basis because managers of Cream Ltd make decisions on the basis of it and it is an

essentially required for decision making process to get updated data.

Understandable and relevant: Data should be recorded in understandable manner, so

people of Cream Ltd can understand or perform their task accordingly.

Above discussed management accounting systems are very essential for organization to

perform their operational activities and make sure that it will maximise their efficiency as well as

effectiveness. By using these systems, managers of Creams Ltd build effective strategies to

maximise their production, profitability, performance and minimise overall cost of

manufacturing to meet their business goals & objectives.

P2. Describe different method of management accounting reporting which are used by

organizations

Job costing report: Job costing reports are administrative mechanisms used to assess the

performance of a project or output against a defined or expected norm (Quilty, Cosentinoand

Bagby, 2018). They have been used in areas of the market and their associated industries. The

primary objective of reporting on job costing is to recognize differences or favourable results,

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

typically as financial values. These can be used for recording results in both monetary and

statistical growth. This report assesses the amount of production as against time. When volume

falls within a given time limit, the primary reason must be resolved by management. Many

sources describe the quantity and waste of the raw materials such as chocolate, sugar and nuts.

The final average production cost per unit is measured to the norm when the reports are merged.

Creams Ltd uses this reporting technique to record particular job cost and further strategic

decisions take accordingly.

Inventory management report: This report provides information on the stock of goods in

warehouse. This report is designed with the aid of the inventory management program (Hicks

and et.al., 2019). Main objective of this report is to support the department of production in

taking the necessary actions regarding how many units are required. Above mentioned company

such as Creams Ltd in compliance with the details of this study, manufactures various types of

food items.This report used by the organizations to keep track inventory level for the

manufacturing purpose and makes sure to avoid the situations like shortage of raw material as

well as wastage due to order bulk material at one time. This report helps the managers to

estimate accurate volume of raw material for manufacturing of goods.

Operating budget report:It shows the company's estimated profits and related costs for

the current year, usually the following year and is also displayed in the style of an income

statement (Fleischmanand McLean, 2020). Management usually goes through the process of

preparing the plan before the next year begins and then conducts continuing updates every

month. An operating budget report may consist of a high-level overview plan, accompanied by

information in the budget to substantiate each line item. Managers of Creams Ltd follow this

report and prepare all it, which include the estimated revenue or cost of production that further

helps to take managerial decisions or build strategies.

Accounts receivable aging report: This contains information on both the volume of

debtors who are responsible to businesses without the appropriate selling date. The report's

purpose is to assist the division of finance to formulate clear policies and tactics. The financial

department in the Creams Ltd produce this report by using vital information to recover payments

from debtors on deadline. The report is arranged by customer name, with those invoices

expressed immediately below client name of each consumer, generally sorted by either payment

number or date of invoice.

7

statistical growth. This report assesses the amount of production as against time. When volume

falls within a given time limit, the primary reason must be resolved by management. Many

sources describe the quantity and waste of the raw materials such as chocolate, sugar and nuts.

The final average production cost per unit is measured to the norm when the reports are merged.

Creams Ltd uses this reporting technique to record particular job cost and further strategic

decisions take accordingly.

Inventory management report: This report provides information on the stock of goods in

warehouse. This report is designed with the aid of the inventory management program (Hicks

and et.al., 2019). Main objective of this report is to support the department of production in

taking the necessary actions regarding how many units are required. Above mentioned company

such as Creams Ltd in compliance with the details of this study, manufactures various types of

food items.This report used by the organizations to keep track inventory level for the

manufacturing purpose and makes sure to avoid the situations like shortage of raw material as

well as wastage due to order bulk material at one time. This report helps the managers to

estimate accurate volume of raw material for manufacturing of goods.

Operating budget report:It shows the company's estimated profits and related costs for

the current year, usually the following year and is also displayed in the style of an income

statement (Fleischmanand McLean, 2020). Management usually goes through the process of

preparing the plan before the next year begins and then conducts continuing updates every

month. An operating budget report may consist of a high-level overview plan, accompanied by

information in the budget to substantiate each line item. Managers of Creams Ltd follow this

report and prepare all it, which include the estimated revenue or cost of production that further

helps to take managerial decisions or build strategies.

Accounts receivable aging report: This contains information on both the volume of

debtors who are responsible to businesses without the appropriate selling date. The report's

purpose is to assist the division of finance to formulate clear policies and tactics. The financial

department in the Creams Ltd produce this report by using vital information to recover payments

from debtors on deadline. The report is arranged by customer name, with those invoices

expressed immediately below client name of each consumer, generally sorted by either payment

number or date of invoice.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Performance reports: A performance report deals with a person's result of an action or

function. The report will equate real results with a estimate or norm and the discrepancy between

both the two figures (Feldmanand Paul, 2019). If there is an adverse difference, the receiver of a

results assessment is supposed to take action. This report is not only to measure employee’s

performance, but also evaluate the overall performance of the organization. On the basis of

performance report, management provide rewards to their employees and plays as motivation

factor which improve their overall performance and productivity.

Above mention reports are used by the managers of Creams Ltd to measure the

performance of organization. Using above discussed reports managers able to formulate

strategies which required to enhance employees as well as business efficiency.

M1. Benefits of management accounting systems

There are several management accounting systems which provide various benefits to the

company in different ways. Cost accounting system helps in measuring actual degree of volatility

is related to the control of overall expenditure for particular activities. This accounting approach

used by the Creams Ltd to estimate the cost of product and try to control cost throughout the

period. Job order costing is beneficial for businesses in quantifying the cost of each produced

output number (An, Wang, Emrouznejad, 2020). Such accounting is done by calculating and

evaluating the costs of workers in the above organization for an examination of the costs of each

produced goods. Price optimization system is enables companies to assess the price of the

product in line with the recent trend in the industry. Their logistics team sets prices of products

according to customer needs in Creams limited and as per their competitors 'actions in the area

above. The value of the inventory reserved is essentially calculated by this accounting

(Maggardand Barlow, 2018). This method of accounting is intended to reduce the processing

costs. This accounting scheme is implemented at the Creams limited to lower their cost of

production. These systems help the managers to make effective decisions which further helps in

achieving operational goals & objectives.

D1. Critically evaluate that how management accounting systems and management accounting

reporting are integrated within organisational processes

Management accounting includes a number of accounting systems and reports which are

compatible with administrative processes and companies. According to Creams Ltd, specific

departments are related to accounting systems. The market optimisation program is integrated

8

function. The report will equate real results with a estimate or norm and the discrepancy between

both the two figures (Feldmanand Paul, 2019). If there is an adverse difference, the receiver of a

results assessment is supposed to take action. This report is not only to measure employee’s

performance, but also evaluate the overall performance of the organization. On the basis of

performance report, management provide rewards to their employees and plays as motivation

factor which improve their overall performance and productivity.

Above mention reports are used by the managers of Creams Ltd to measure the

performance of organization. Using above discussed reports managers able to formulate

strategies which required to enhance employees as well as business efficiency.

M1. Benefits of management accounting systems

There are several management accounting systems which provide various benefits to the

company in different ways. Cost accounting system helps in measuring actual degree of volatility

is related to the control of overall expenditure for particular activities. This accounting approach

used by the Creams Ltd to estimate the cost of product and try to control cost throughout the

period. Job order costing is beneficial for businesses in quantifying the cost of each produced

output number (An, Wang, Emrouznejad, 2020). Such accounting is done by calculating and

evaluating the costs of workers in the above organization for an examination of the costs of each

produced goods. Price optimization system is enables companies to assess the price of the

product in line with the recent trend in the industry. Their logistics team sets prices of products

according to customer needs in Creams limited and as per their competitors 'actions in the area

above. The value of the inventory reserved is essentially calculated by this accounting

(Maggardand Barlow, 2018). This method of accounting is intended to reduce the processing

costs. This accounting scheme is implemented at the Creams limited to lower their cost of

production. These systems help the managers to make effective decisions which further helps in

achieving operational goals & objectives.

D1. Critically evaluate that how management accounting systems and management accounting

reporting are integrated within organisational processes

Management accounting includes a number of accounting systems and reports which are

compatible with administrative processes and companies. According to Creams Ltd, specific

departments are related to accounting systems. The market optimisation program is integrated

8

into the sales department as a way of growing selling revenues. Accounting Statements are often

aligned with the sales cycle, near the accounting systems. Inventory report is in relation to the

unit of development. In the latter organization, for example their managers use various reports

for corrective steps in the retail sector.In order to run business process properly, managers of

Creams Ltd need to implement various systems such as inventory management to keep track

their stock level and then prepare inventory report to review level or make decisions accordingly.

TASK 2

P3. Calculate cost by using appreciate cost analysis techniques and prepare income statement by

using marginal or absorption costing method

There are various types of cost which has different nature and these are discussed below:

Fixed cost: Fixed costs are costs which will not alter with each increasing or decreasing in

the quantity of products or services manufactured or sold. Leasing, insurance premiums, or

mortgage payments are fixed costs (Modell, 2014). Fixed costs will build economy of scale that

is decreases in per-unit costs by increasing the amount of production. This concept is often called

marginal cost decrease. At the end, all prices are ultimately variable.

Variable cost: Variable costs are company's expenses which change in relation to the

performance of the output. Depending on the level of output of a business variable costs increase

or decrease. They rise as output rises and decline as production decreases. Examples of variable

costs included the raw material and shipping costs.

Real cost: The cumulative real cost involved in producing a perishable product or service

to customers. For Creams Ltd, the overall cost of production usually involves the cost of all

measurable resources such as labour and raw materials used in the manufacturing process.

Prime cost: Prime costs are the expenditures of a business which are directly linked to the

products and resources used in manufacturing. The prime cost estimates the direct costs of the

raw materials and labour involved in manufacturing an item. Direct costs such as advertisement

and operating costs and do not include indirect expenses.

Total cost: The overall cost of a product portfolio contains not only the variable cost of the

items sold as well as the cost of marketing and operating the manufacturing line on which goods

are produced. View of the overall cost for the project.

9

aligned with the sales cycle, near the accounting systems. Inventory report is in relation to the

unit of development. In the latter organization, for example their managers use various reports

for corrective steps in the retail sector.In order to run business process properly, managers of

Creams Ltd need to implement various systems such as inventory management to keep track

their stock level and then prepare inventory report to review level or make decisions accordingly.

TASK 2

P3. Calculate cost by using appreciate cost analysis techniques and prepare income statement by

using marginal or absorption costing method

There are various types of cost which has different nature and these are discussed below:

Fixed cost: Fixed costs are costs which will not alter with each increasing or decreasing in

the quantity of products or services manufactured or sold. Leasing, insurance premiums, or

mortgage payments are fixed costs (Modell, 2014). Fixed costs will build economy of scale that

is decreases in per-unit costs by increasing the amount of production. This concept is often called

marginal cost decrease. At the end, all prices are ultimately variable.

Variable cost: Variable costs are company's expenses which change in relation to the

performance of the output. Depending on the level of output of a business variable costs increase

or decrease. They rise as output rises and decline as production decreases. Examples of variable

costs included the raw material and shipping costs.

Real cost: The cumulative real cost involved in producing a perishable product or service

to customers. For Creams Ltd, the overall cost of production usually involves the cost of all

measurable resources such as labour and raw materials used in the manufacturing process.

Prime cost: Prime costs are the expenditures of a business which are directly linked to the

products and resources used in manufacturing. The prime cost estimates the direct costs of the

raw materials and labour involved in manufacturing an item. Direct costs such as advertisement

and operating costs and do not include indirect expenses.

Total cost: The overall cost of a product portfolio contains not only the variable cost of the

items sold as well as the cost of marketing and operating the manufacturing line on which goods

are produced. View of the overall cost for the project.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

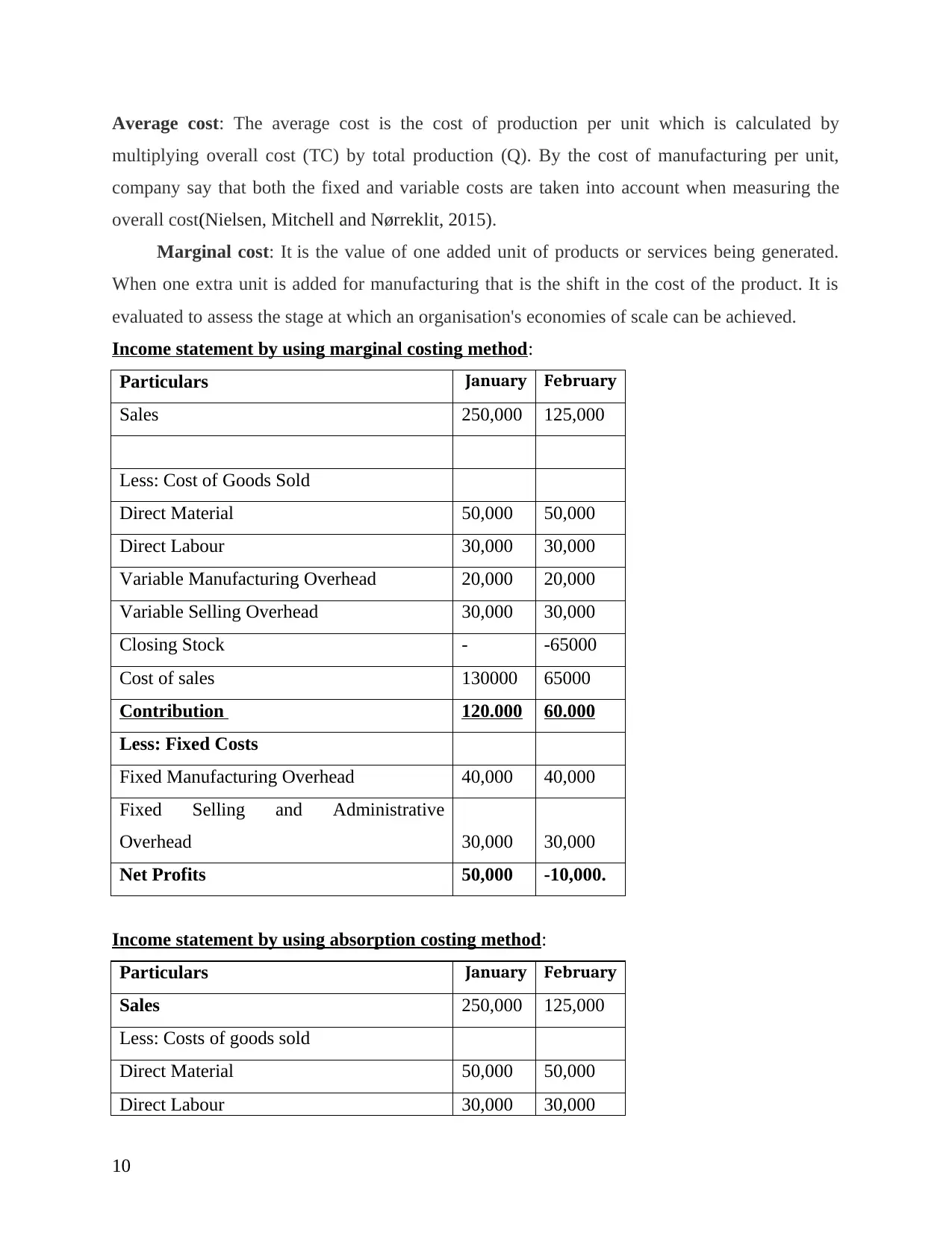

Average cost: The average cost is the cost of production per unit which is calculated by

multiplying overall cost (TC) by total production (Q). By the cost of manufacturing per unit,

company say that both the fixed and variable costs are taken into account when measuring the

overall cost(Nielsen, Mitchell and Nørreklit, 2015).

Marginal cost: It is the value of one added unit of products or services being generated.

When one extra unit is added for manufacturing that is the shift in the cost of the product. It is

evaluated to assess the stage at which an organisation's economies of scale can be achieved.

Income statement by using marginal costing method:

Particulars January February

Sales 250,000 125,000

Less: Cost of Goods Sold

Direct Material 50,000 50,000

Direct Labour 30,000 30,000

Variable Manufacturing Overhead 20,000 20,000

Variable Selling Overhead 30,000 30,000

Closing Stock - -65000

Cost of sales 130000 65000

Contribution 120.000 60.000

Less: Fixed Costs

Fixed Manufacturing Overhead 40,000 40,000

Fixed Selling and Administrative

Overhead 30,000 30,000

Net Profits 50,000 -10,000.

Income statement by using absorption costing method:

Particulars January February

Sales 250,000 125,000

Less: Costs of goods sold

Direct Material 50,000 50,000

Direct Labour 30,000 30,000

10

multiplying overall cost (TC) by total production (Q). By the cost of manufacturing per unit,

company say that both the fixed and variable costs are taken into account when measuring the

overall cost(Nielsen, Mitchell and Nørreklit, 2015).

Marginal cost: It is the value of one added unit of products or services being generated.

When one extra unit is added for manufacturing that is the shift in the cost of the product. It is

evaluated to assess the stage at which an organisation's economies of scale can be achieved.

Income statement by using marginal costing method:

Particulars January February

Sales 250,000 125,000

Less: Cost of Goods Sold

Direct Material 50,000 50,000

Direct Labour 30,000 30,000

Variable Manufacturing Overhead 20,000 20,000

Variable Selling Overhead 30,000 30,000

Closing Stock - -65000

Cost of sales 130000 65000

Contribution 120.000 60.000

Less: Fixed Costs

Fixed Manufacturing Overhead 40,000 40,000

Fixed Selling and Administrative

Overhead 30,000 30,000

Net Profits 50,000 -10,000.

Income statement by using absorption costing method:

Particulars January February

Sales 250,000 125,000

Less: Costs of goods sold

Direct Material 50,000 50,000

Direct Labour 30,000 30,000

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

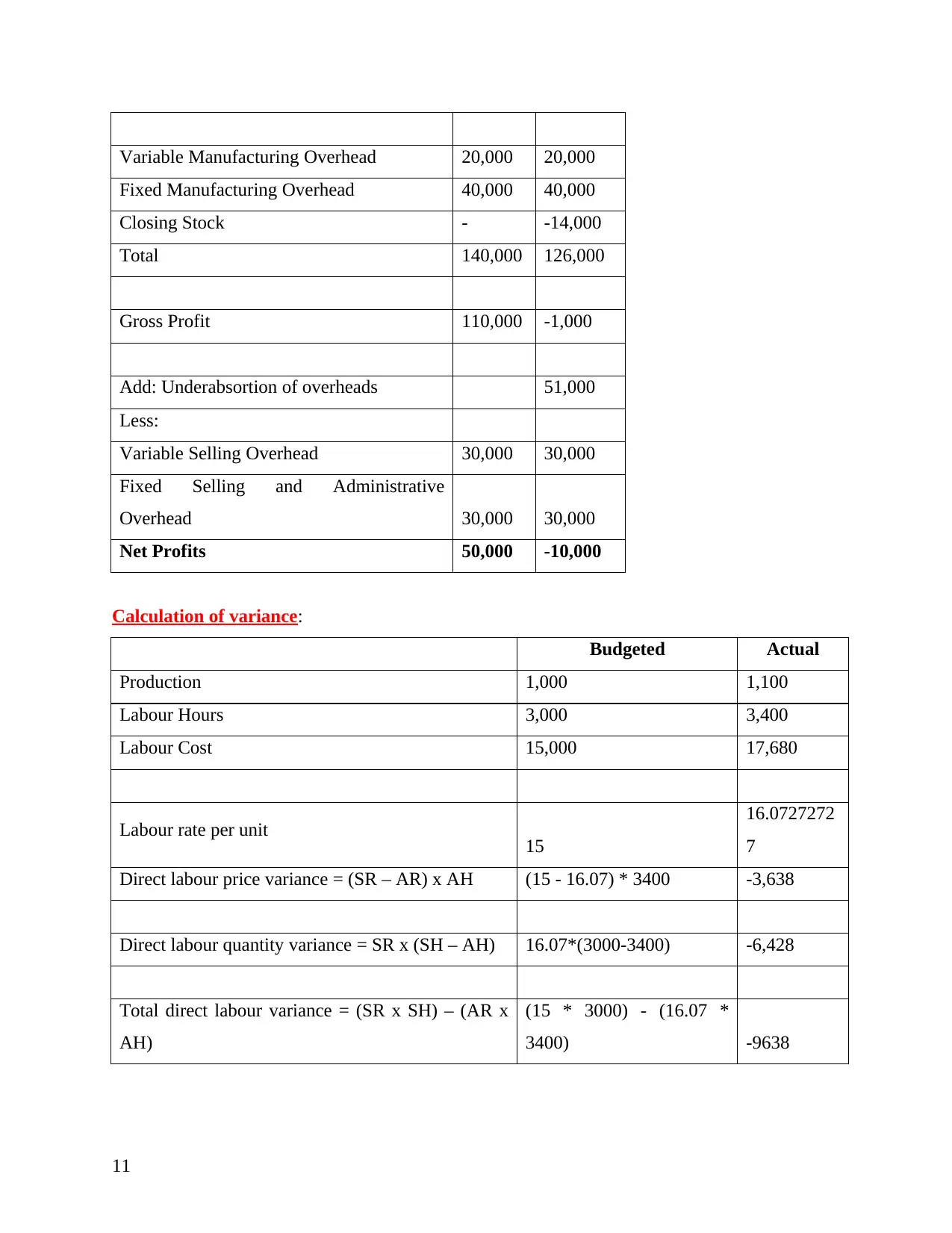

Variable Manufacturing Overhead 20,000 20,000

Fixed Manufacturing Overhead 40,000 40,000

Closing Stock - -14,000

Total 140,000 126,000

Gross Profit 110,000 -1,000

Add: Underabsortion of overheads 51,000

Less:

Variable Selling Overhead 30,000 30,000

Fixed Selling and Administrative

Overhead 30,000 30,000

Net Profits 50,000 -10,000

Calculation of variance:

Budgeted Actual

Production 1,000 1,100

Labour Hours 3,000 3,400

Labour Cost 15,000 17,680

Labour rate per unit 15

16.0727272

7

Direct labour price variance = (SR – AR) x AH (15 - 16.07) * 3400 -3,638

Direct labour quantity variance = SR x (SH – AH) 16.07*(3000-3400) -6,428

Total direct labour variance = (SR x SH) – (AR x

AH)

(15 * 3000) - (16.07 *

3400) -9638

11

Fixed Manufacturing Overhead 40,000 40,000

Closing Stock - -14,000

Total 140,000 126,000

Gross Profit 110,000 -1,000

Add: Underabsortion of overheads 51,000

Less:

Variable Selling Overhead 30,000 30,000

Fixed Selling and Administrative

Overhead 30,000 30,000

Net Profits 50,000 -10,000

Calculation of variance:

Budgeted Actual

Production 1,000 1,100

Labour Hours 3,000 3,400

Labour Cost 15,000 17,680

Labour rate per unit 15

16.0727272

7

Direct labour price variance = (SR – AR) x AH (15 - 16.07) * 3400 -3,638

Direct labour quantity variance = SR x (SH – AH) 16.07*(3000-3400) -6,428

Total direct labour variance = (SR x SH) – (AR x

AH)

(15 * 3000) - (16.07 *

3400) -9638

11

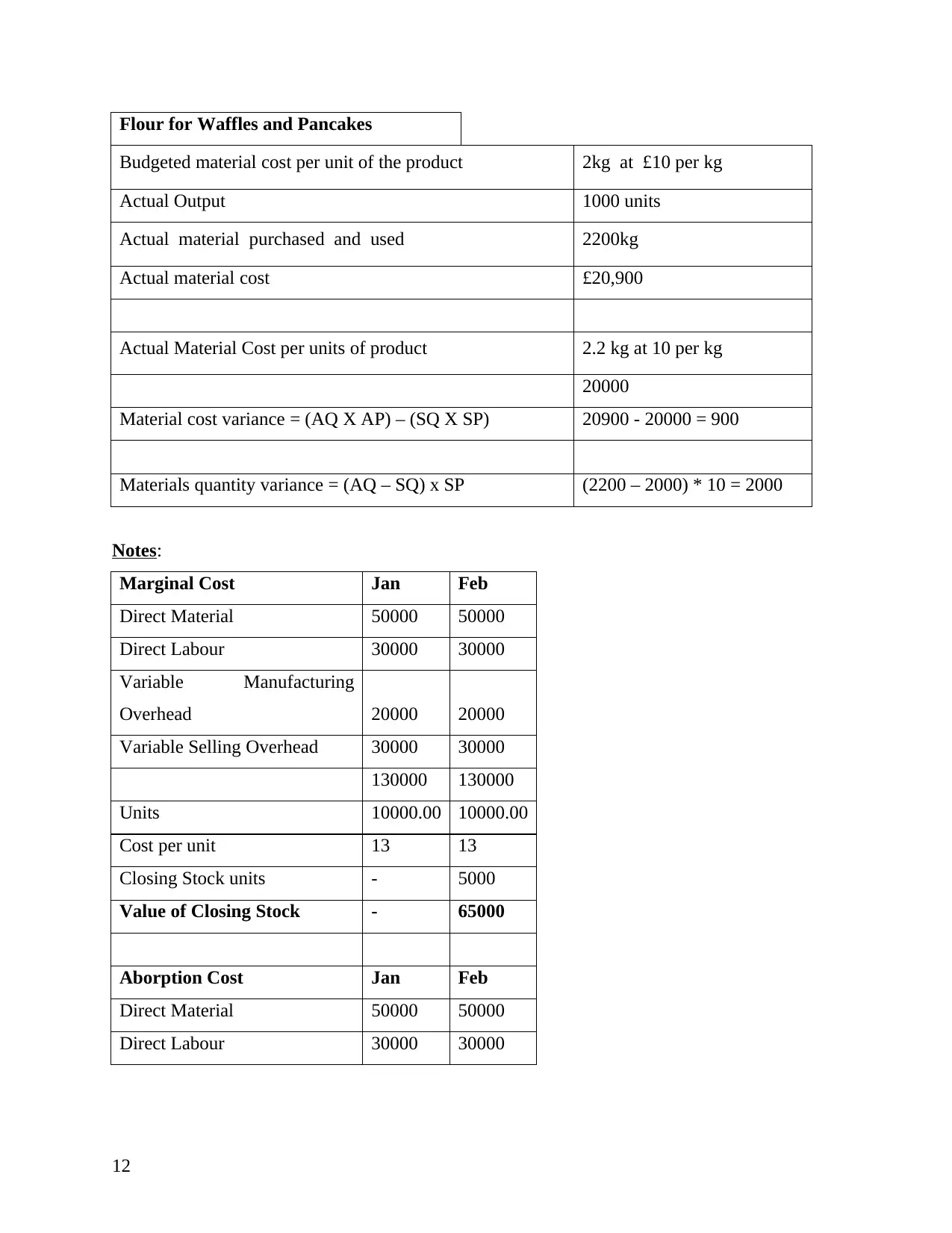

Flour for Waffles and Pancakes

Budgeted material cost per unit of the product 2kg at £10 per kg

Actual Output 1000 units

Actual material purchased and used 2200kg

Actual material cost £20,900

Actual Material Cost per units of product 2.2 kg at 10 per kg

20000

Material cost variance = (AQ X AP) – (SQ X SP) 20900 - 20000 = 900

Materials quantity variance = (AQ – SQ) x SP (2200 – 2000) * 10 = 2000

Notes:

Marginal Cost Jan Feb

Direct Material 50000 50000

Direct Labour 30000 30000

Variable Manufacturing

Overhead 20000 20000

Variable Selling Overhead 30000 30000

130000 130000

Units 10000.00 10000.00

Cost per unit 13 13

Closing Stock units - 5000

Value of Closing Stock - 65000

Aborption Cost Jan Feb

Direct Material 50000 50000

Direct Labour 30000 30000

12

Budgeted material cost per unit of the product 2kg at £10 per kg

Actual Output 1000 units

Actual material purchased and used 2200kg

Actual material cost £20,900

Actual Material Cost per units of product 2.2 kg at 10 per kg

20000

Material cost variance = (AQ X AP) – (SQ X SP) 20900 - 20000 = 900

Materials quantity variance = (AQ – SQ) x SP (2200 – 2000) * 10 = 2000

Notes:

Marginal Cost Jan Feb

Direct Material 50000 50000

Direct Labour 30000 30000

Variable Manufacturing

Overhead 20000 20000

Variable Selling Overhead 30000 30000

130000 130000

Units 10000.00 10000.00

Cost per unit 13 13

Closing Stock units - 5000

Value of Closing Stock - 65000

Aborption Cost Jan Feb

Direct Material 50000 50000

Direct Labour 30000 30000

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.