Comprehensive Management Accounting Report: GSQ Ltd Case Study

VerifiedAdded on 2023/01/13

|13

|2945

|55

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its application within the context of GSQ Ltd. It begins with an introduction to management accounting, differentiating it from financial accounting, and exploring various management accounting systems such as inventory management, cost accounting, and job costing systems. The report delves into the benefits and applications of these systems, emphasizing their integration within organizational processes. Furthermore, it examines different costing techniques, including marginal costing and absorption costing, providing comparative analyses through cost cards and profit or loss statements. The report also covers various planning tools used in management accounting, such as operational budgets, flexible budgets, and cash budgets, highlighting their advantages and disadvantages. Finally, it addresses methods organizations employ to respond to financial problems using management accounting principles, culminating in a conclusion summarizing the key findings.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION ..........................................................................................................................1

LO1 .................................................................................................................................................1

Types and benefits of management accounting systems and its application in organisational

context..........................................................................................................................................1

Integration with the organisational process.................................................................................3

Methods used in management accounting reporting. .................................................................3

LO2 .................................................................................................................................................4

Different types of costing techniques used by GSK ltd...............................................................4

LO3..................................................................................................................................................5

Different types of planning tools used in management accounting ............................................5

LO4 .................................................................................................................................................7

Methods which organisation uses in management accounting for responding to the financial

problems. .....................................................................................................................................7

CONCLUSION ...............................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION ..........................................................................................................................1

LO1 .................................................................................................................................................1

Types and benefits of management accounting systems and its application in organisational

context..........................................................................................................................................1

Integration with the organisational process.................................................................................3

Methods used in management accounting reporting. .................................................................3

LO2 .................................................................................................................................................4

Different types of costing techniques used by GSK ltd...............................................................4

LO3..................................................................................................................................................5

Different types of planning tools used in management accounting ............................................5

LO4 .................................................................................................................................................7

Methods which organisation uses in management accounting for responding to the financial

problems. .....................................................................................................................................7

CONCLUSION ...............................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Management accounting is the process where internal systems are used by organisation

for measuring and evaluating the process for management of organisation. Management

accounting has been used by organisation for achieving sustainable growth and success in the

organisation. GSQ is a manufacturing concern on which present report is based. Report will

cover meaning of management accounting and different types of management accounting

systems used in the business with their benefits and limitations and their application in the

organisation. It will cover the methods used for management accounting reporting. Different

techniques of costing used in management accounting will also be explained. Also t will give an

understanding about the management accounting planning tools and the use of management

accounting in solving financial problems.

LO1

Management accounting

Management accounting involves preparation and making available the financial &

statistical information’s to the business managers for carrying out managerial decisions for day

to day activities of business (Bui and De Villiers, 2017). It is different from financial accounting

as management accounting is of importance to internal management where the financial

accounting is for external reporting to stakeholders.

Types and benefits of management accounting systems and its application in organisational

context.

There are different types of management accounting systems which are used by GSQ ltd.

Inventory Management Systems

Inventory management is a technological and process & procedures combination which

oversee maintenance and monitoring of the stocks, whether the stocks are related with the assets

of company, supplies, raw materials or the finished products manufactured by the organisation

for sale to customers. Inventory management is widely used process that is essential for keeping

track of the movement of inventory within the processes and out of the organisation. The

methods used in inventory management are just in time and material requirement planning

Just-in-time-

1

Management accounting is the process where internal systems are used by organisation

for measuring and evaluating the process for management of organisation. Management

accounting has been used by organisation for achieving sustainable growth and success in the

organisation. GSQ is a manufacturing concern on which present report is based. Report will

cover meaning of management accounting and different types of management accounting

systems used in the business with their benefits and limitations and their application in the

organisation. It will cover the methods used for management accounting reporting. Different

techniques of costing used in management accounting will also be explained. Also t will give an

understanding about the management accounting planning tools and the use of management

accounting in solving financial problems.

LO1

Management accounting

Management accounting involves preparation and making available the financial &

statistical information’s to the business managers for carrying out managerial decisions for day

to day activities of business (Bui and De Villiers, 2017). It is different from financial accounting

as management accounting is of importance to internal management where the financial

accounting is for external reporting to stakeholders.

Types and benefits of management accounting systems and its application in organisational

context.

There are different types of management accounting systems which are used by GSQ ltd.

Inventory Management Systems

Inventory management is a technological and process & procedures combination which

oversee maintenance and monitoring of the stocks, whether the stocks are related with the assets

of company, supplies, raw materials or the finished products manufactured by the organisation

for sale to customers. Inventory management is widely used process that is essential for keeping

track of the movement of inventory within the processes and out of the organisation. The

methods used in inventory management are just in time and material requirement planning

Just-in-time-

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In this method organisations do not tend to store the stocks of inventory in the organisation.

Inventory is made available on demand by the production departments which saves the carrying

cost and risk of becoming outdated.

Material Requirement Planning-

In this method company stores the inventory that cannot be made ordered on urgent basis.

This involves planning about the requirement of inventory base on the previous trends. Bulk

purchases provide discounts.

Benefits

Inventory management systems helps GSQ to have proper record of all the movement of

inventory.

It also helps the company to reduce its costs using the approaches like just-in-time and

MRP.

Inventory prevents interruptions in production process as it helps company to order in

time.

Application

Inventory management is applied in the production process for ordering the materials as

and when required (Hiebl, 2018). It helps GSQ in having proper record of the inventory stored in

warehouse.

Cost Accounting Systems

Cost accounting systems refers to recording all the costs incurred in manufacturing a

product. It account for all the direct and indirect costs associated with the product. Cost

accounting systems estimates the profitability of every item manufactured. It provide and

important base to management of GSQ for decision-making. The costing methods are direct cost

Direct costing – In this costing systems only variables costs associated with the products are

considered. Fixed costs are treated as period cost incurred during the period.

Standard costing – It refers to costing method in which actual output are compared with the

budgeted output. Corrective measures are taken for reducing the variances.

Benefits

It helps the management in implementing improved methods for reducing the cost.

It aims at identifying the reasons of variances between the outputs.

2

Inventory is made available on demand by the production departments which saves the carrying

cost and risk of becoming outdated.

Material Requirement Planning-

In this method company stores the inventory that cannot be made ordered on urgent basis.

This involves planning about the requirement of inventory base on the previous trends. Bulk

purchases provide discounts.

Benefits

Inventory management systems helps GSQ to have proper record of all the movement of

inventory.

It also helps the company to reduce its costs using the approaches like just-in-time and

MRP.

Inventory prevents interruptions in production process as it helps company to order in

time.

Application

Inventory management is applied in the production process for ordering the materials as

and when required (Hiebl, 2018). It helps GSQ in having proper record of the inventory stored in

warehouse.

Cost Accounting Systems

Cost accounting systems refers to recording all the costs incurred in manufacturing a

product. It account for all the direct and indirect costs associated with the product. Cost

accounting systems estimates the profitability of every item manufactured. It provide and

important base to management of GSQ for decision-making. The costing methods are direct cost

Direct costing – In this costing systems only variables costs associated with the products are

considered. Fixed costs are treated as period cost incurred during the period.

Standard costing – It refers to costing method in which actual output are compared with the

budgeted output. Corrective measures are taken for reducing the variances.

Benefits

It helps the management in implementing improved methods for reducing the cost.

It aims at identifying the reasons of variances between the outputs.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost accounting helps GSQ in deciding its profit margins based on the cost information

derived.

Application

Cost accounting is applied by GSQ in the manufacturing processes for recording all the

variable and fixed costs incurred for producing a product and keeping the costs under control.

Job Costing Systems

Job costing refers to the process of collecting informations related to costs which are

associated with specific productions or the service job. The information helps in providing

costing information to customers under contracts where cost is reimbursed. It is also referred as

method where the costs the costs are compiled for work order or job (Granlund and Lukka,

2017).

Benefits

It helps GSQ in identifying profitability of each job separately.

Costs of similar jobs can be estimated on the information available from existing jobs.

Detailed analysis of costs helps in taking cost control measures.

Application

It is applied in processes for identifying the cost of contractual specific products by GSQ.

It provides detailed cost information for manufacturing product separately.

Integration with the organisational process.

The above management accounting systems are used by the GSQ for having proper

management of the products or services produced by company. Integrating these systems with

the production processes helps the company in managing the costs and keeping them under

control to the extent possible.

Methods used in management accounting reporting.

The management accounting reports provide important information for taking strategic

and operational decisions.

Budget Reports

Budget reports are prepared by the organisation before the start of the production process.

These reports are the spending plans of company about the future activities and operations of

company. It provides clear structure for the organisation to follow. The budget reports are

3

derived.

Application

Cost accounting is applied by GSQ in the manufacturing processes for recording all the

variable and fixed costs incurred for producing a product and keeping the costs under control.

Job Costing Systems

Job costing refers to the process of collecting informations related to costs which are

associated with specific productions or the service job. The information helps in providing

costing information to customers under contracts where cost is reimbursed. It is also referred as

method where the costs the costs are compiled for work order or job (Granlund and Lukka,

2017).

Benefits

It helps GSQ in identifying profitability of each job separately.

Costs of similar jobs can be estimated on the information available from existing jobs.

Detailed analysis of costs helps in taking cost control measures.

Application

It is applied in processes for identifying the cost of contractual specific products by GSQ.

It provides detailed cost information for manufacturing product separately.

Integration with the organisational process.

The above management accounting systems are used by the GSQ for having proper

management of the products or services produced by company. Integrating these systems with

the production processes helps the company in managing the costs and keeping them under

control to the extent possible.

Methods used in management accounting reporting.

The management accounting reports provide important information for taking strategic

and operational decisions.

Budget Reports

Budget reports are prepared by the organisation before the start of the production process.

These reports are the spending plans of company about the future activities and operations of

company. It provides clear structure for the organisation to follow. The budget reports are

3

prepared based on the previous budgets and information. Managers make adjustments related to

inflations, demand and other factors in the current budgets. This helps GSQ in proper allocation

of resources among various processes and activities.

Cost Accounting Reports

These reports cover all the information regarding the costs that are related with

manufacturing of products or services. It contains detailed information about the all the items of

costs separately. On the previous trends forecast about the future income and revenues are made

and resources are allocated accordingly. They help the managers of GSQ in deciding the profit

margin for each product. The information is very useful for decision making on the variances

between the budgeted and actual results. On the basis of this reports strategic policies and

procedures are taken.

Performance Reports

The performance reports contain the analysis of the performance of company and it

operations. They provide the company whether the targeted level of performance has been

achieved or not. If the performance targets are not achieved than company may take corrective

measures for increasing the efficiency and productivity. These reports also assess the

performance of individual and employees that helps company in rewarding them for future

growth and success.

LO2

Different types of costing techniques used by GSK ltd.

Marginal Costing

Marginal costing refers to the accounting technique where the amount at the given

volumes of outputs by which the cost in aggregate could be changed if volume of outputs are

decreased or increased by 1 unit. Marginal costing technique is used for identifying and

evaluating the cost of product being manufactured within the organisation. This costing

technique only considers the variable cost associated with the products. Fixed costs under

marginal costing are treated as period cost and are not included in product cost.

Advantages

The marginal costing is used in management decisions as comparison is possible. Linear relationship between variable cost and output may not be accurate.

Disadvantage

4

inflations, demand and other factors in the current budgets. This helps GSQ in proper allocation

of resources among various processes and activities.

Cost Accounting Reports

These reports cover all the information regarding the costs that are related with

manufacturing of products or services. It contains detailed information about the all the items of

costs separately. On the previous trends forecast about the future income and revenues are made

and resources are allocated accordingly. They help the managers of GSQ in deciding the profit

margin for each product. The information is very useful for decision making on the variances

between the budgeted and actual results. On the basis of this reports strategic policies and

procedures are taken.

Performance Reports

The performance reports contain the analysis of the performance of company and it

operations. They provide the company whether the targeted level of performance has been

achieved or not. If the performance targets are not achieved than company may take corrective

measures for increasing the efficiency and productivity. These reports also assess the

performance of individual and employees that helps company in rewarding them for future

growth and success.

LO2

Different types of costing techniques used by GSK ltd.

Marginal Costing

Marginal costing refers to the accounting technique where the amount at the given

volumes of outputs by which the cost in aggregate could be changed if volume of outputs are

decreased or increased by 1 unit. Marginal costing technique is used for identifying and

evaluating the cost of product being manufactured within the organisation. This costing

technique only considers the variable cost associated with the products. Fixed costs under

marginal costing are treated as period cost and are not included in product cost.

Advantages

The marginal costing is used in management decisions as comparison is possible. Linear relationship between variable cost and output may not be accurate.

Disadvantage

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fixed costs are considered period costs.

Company may face difficulty in segregation of cost between variable and fixd.

Absorption Costing

It is a costing method which is used by organisation for measuring the cost of products. It

is also known as the full costing method. The costing methods accumulates all the cost

associated with production process & apportion them to individual products. All the variable and

fixed overhead are absorbed by the units produced. This costing method includes both variable

and fixed manufacturing overhead in the product's cost.

Advantages

The method considers both variable and fixed cost in product cost.

The method is accepted by the accounting standards This provide more accurate and reliable information.

Disadvantage

It is not useful for decision-making purposes.

Comparison of two products cannot be made in this costing.

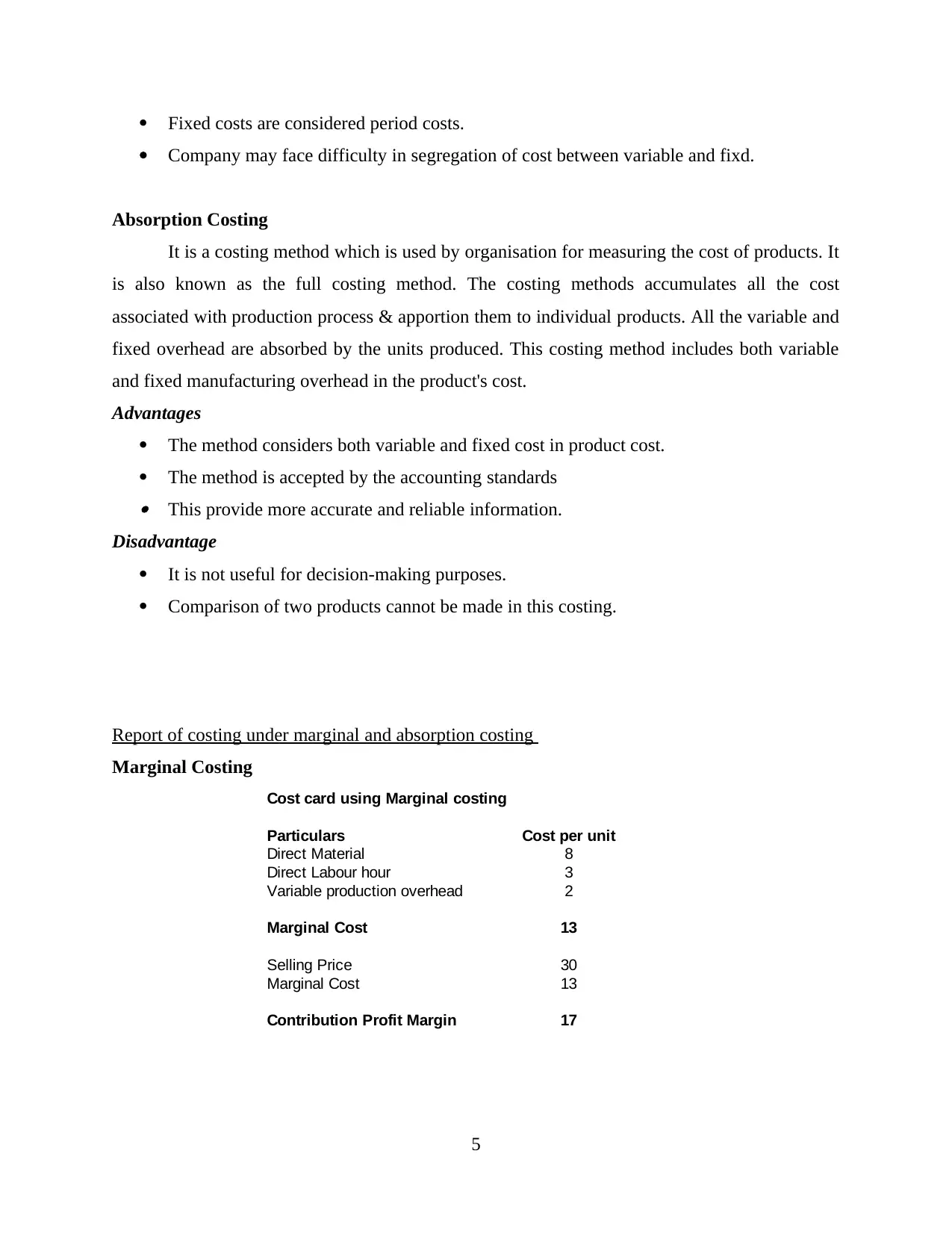

Report of costing under marginal and absorption costing

Marginal Costing

5

Cost card using Marginal costing

Particulars Cost per unit

Direct Material 8

Direct Labour hour 3

Variable production overhead 2

Marginal Cost 13

Selling Price 30

Marginal Cost 13

Contribution Profit Margin 17

Company may face difficulty in segregation of cost between variable and fixd.

Absorption Costing

It is a costing method which is used by organisation for measuring the cost of products. It

is also known as the full costing method. The costing methods accumulates all the cost

associated with production process & apportion them to individual products. All the variable and

fixed overhead are absorbed by the units produced. This costing method includes both variable

and fixed manufacturing overhead in the product's cost.

Advantages

The method considers both variable and fixed cost in product cost.

The method is accepted by the accounting standards This provide more accurate and reliable information.

Disadvantage

It is not useful for decision-making purposes.

Comparison of two products cannot be made in this costing.

Report of costing under marginal and absorption costing

Marginal Costing

5

Cost card using Marginal costing

Particulars Cost per unit

Direct Material 8

Direct Labour hour 3

Variable production overhead 2

Marginal Cost 13

Selling Price 30

Marginal Cost 13

Contribution Profit Margin 17

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

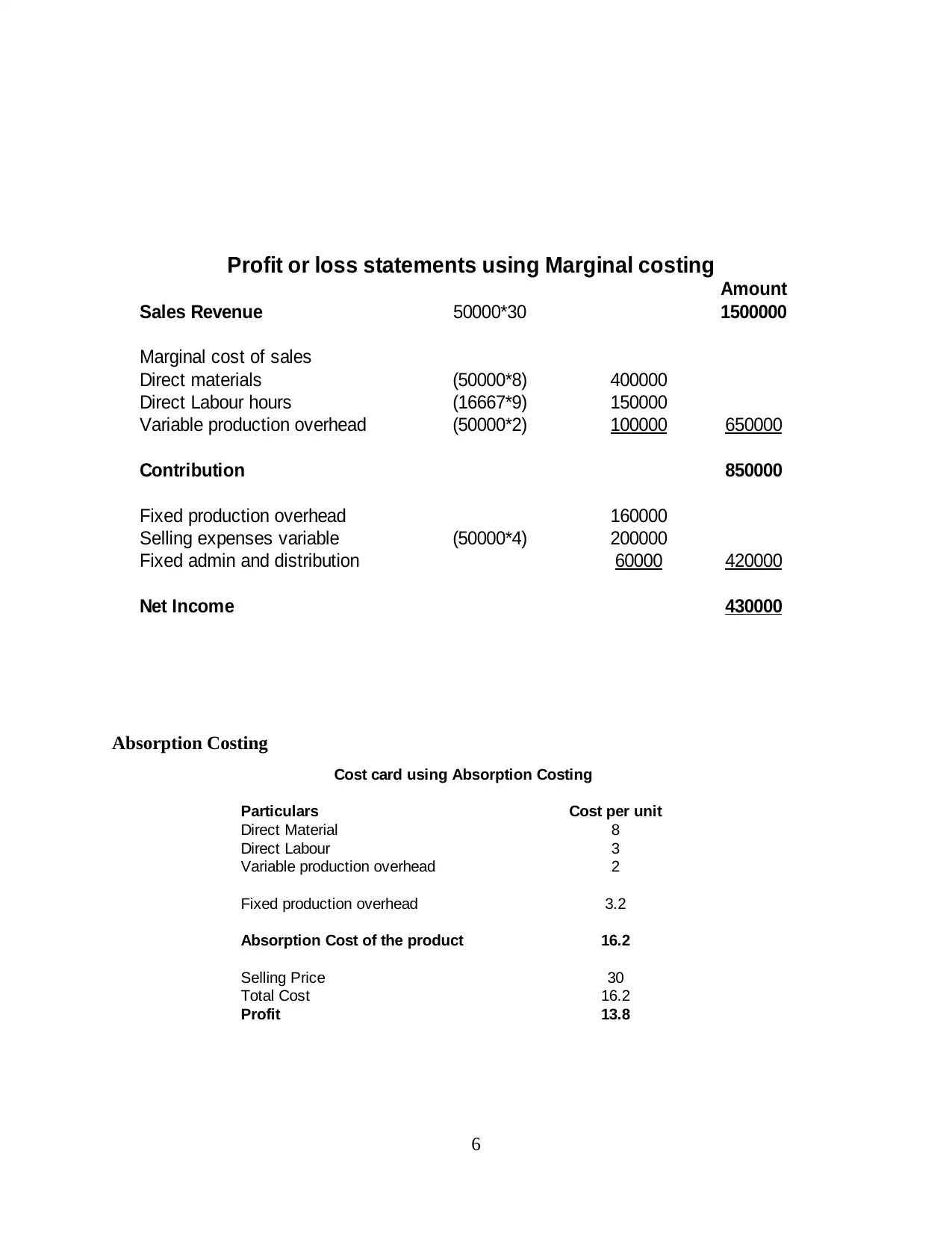

Absorption Costing

6

Cost card using Absorption Costing

Particulars Cost per unit

Direct Material 8

Direct Labour 3

Variable production overhead 2

Fixed production overhead 3.2

Absorption Cost of the product 16.2

Selling Price 30

Total Cost 16.2

Profit 13.8

Profit or loss statements using Marginal costing

Amount

Sales Revenue 50000*30 1500000

Marginal cost of sales

Direct materials (50000*8) 400000

Direct Labour hours (16667*9) 150000

Variable production overhead (50000*2) 100000 650000

Contribution 850000

Fixed production overhead 160000

Selling expenses variable (50000*4) 200000

Fixed admin and distribution 60000 420000

Net Income 430000

6

Cost card using Absorption Costing

Particulars Cost per unit

Direct Material 8

Direct Labour 3

Variable production overhead 2

Fixed production overhead 3.2

Absorption Cost of the product 16.2

Selling Price 30

Total Cost 16.2

Profit 13.8

Profit or loss statements using Marginal costing

Amount

Sales Revenue 50000*30 1500000

Marginal cost of sales

Direct materials (50000*8) 400000

Direct Labour hours (16667*9) 150000

Variable production overhead (50000*2) 100000 650000

Contribution 850000

Fixed production overhead 160000

Selling expenses variable (50000*4) 200000

Fixed admin and distribution 60000 420000

Net Income 430000

LO3

Different types of planning tools used in management accounting

Operational Budgets

It refers to he forecast about the expenses and revenue for single or more periods.

Operational budgets are formulated typically by management of company prior to beginning of

years. It provides the expected level of activities of business. It provides the management of

GSQ a structured framework to be followed. They enable the company to keep the workforce

and operations in right directions (Latan and et.al., 2018). On the basis of these budgets the

manufacturing process is monitored with increased efficiency and reducing wastages and more

effective utilisation of the available resources by company.

Advantages

7

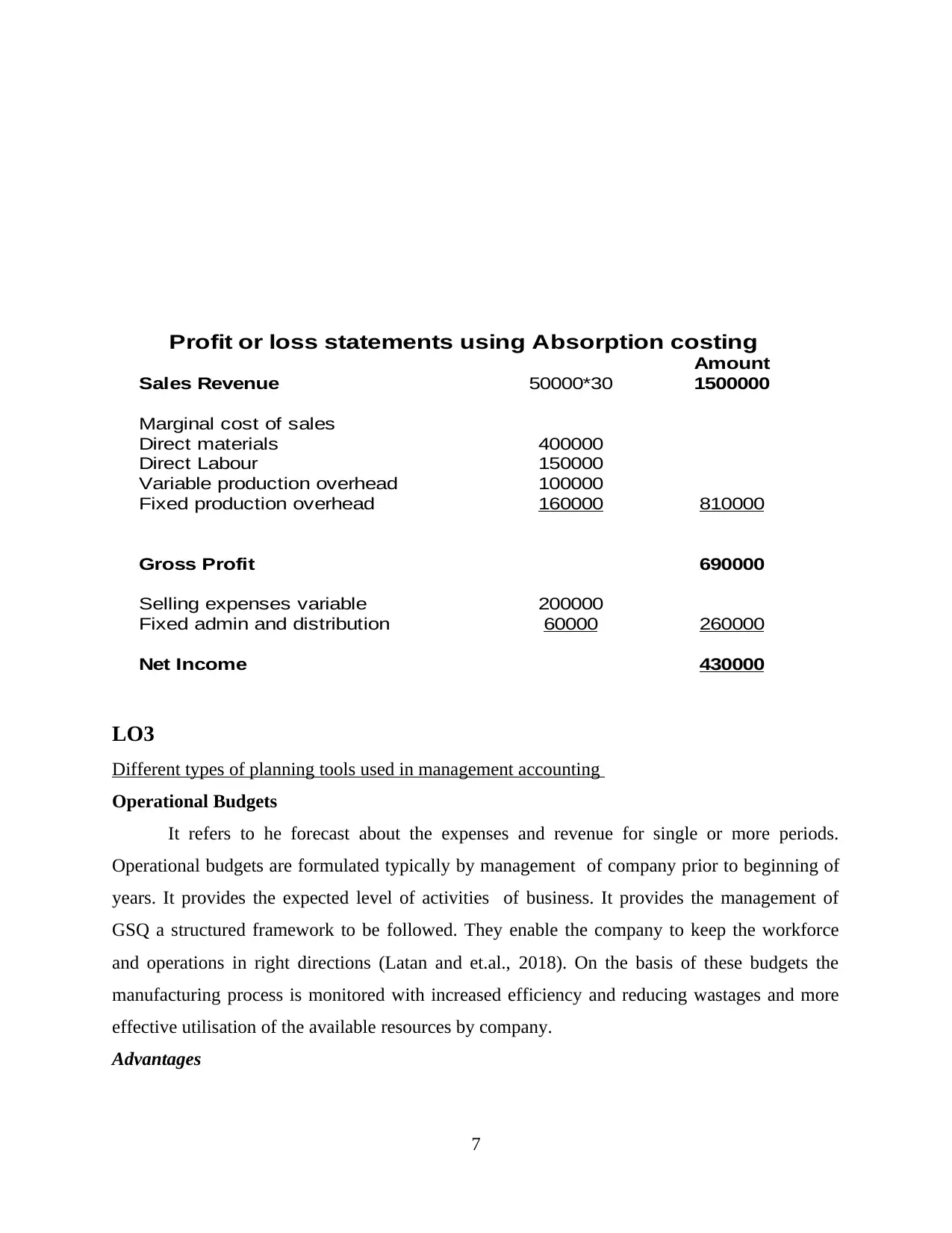

Profit or loss statements using Absorption costing

Amount

Sales Revenue 50000*30 1500000

Marginal cost of sales

Direct materials 400000

Direct Labour 150000

Variable production overhead 100000

Fixed production overhead 160000 810000

Gross Profit 690000

Selling expenses variable 200000

Fixed admin and distribution 60000 260000

Net Income 430000

Different types of planning tools used in management accounting

Operational Budgets

It refers to he forecast about the expenses and revenue for single or more periods.

Operational budgets are formulated typically by management of company prior to beginning of

years. It provides the expected level of activities of business. It provides the management of

GSQ a structured framework to be followed. They enable the company to keep the workforce

and operations in right directions (Latan and et.al., 2018). On the basis of these budgets the

manufacturing process is monitored with increased efficiency and reducing wastages and more

effective utilisation of the available resources by company.

Advantages

7

Profit or loss statements using Absorption costing

Amount

Sales Revenue 50000*30 1500000

Marginal cost of sales

Direct materials 400000

Direct Labour 150000

Variable production overhead 100000

Fixed production overhead 160000 810000

Gross Profit 690000

Selling expenses variable 200000

Fixed admin and distribution 60000 260000

Net Income 430000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The operational budgets helps the management of GSQ to keep the costs of operations

within control. It helps the business to forecast about the future incomes and expenses on

previous trends.

Disadvantages

The long range planning may be not accurate as they are based over the estimates. There

are various factors that are not considered. Wrong forecasts can affect the operations of

company.

Flexible Budget

It is defined as a budget which flexes or adjusts according to the changes in activities or

volume of output. These budget are more useful and sophisticated than the static budgets. In

static budgets amounts could not be changed. They remain same as they were when approved.

Flexible budgets provide the scope for company to make required changes as required by the

management. Business operates in a dynamic environments where the changes are required to be

made for responding to these changes in the budgets. This become more easy for GSK to make

adjustments without affecting the whole budgets and operations.

Advantages

Flexible budgets allow the company to make adjustments in the budgets for responding to

the changes. It is more preferred by GSK in its management as it more easily adapts the financial

needs of company. Requirements are reflected in budgets in advance.

Disadvantage

Changes in the budget may affect the management of resources. It makes difficult for the

company to disagree with changes. Department makes the changes to budget on their own which

may not be essential (Quattrone, 2016).

Cash Budgets

Cash budget is referred as the budget containing the information about the cash inflow

and outflow. This budget contains information about the monetary funds. It represents where and

how much cash is allocated to the activities. It ensures that sufficient funds are allocated to the

departments and operations carrying out proper analysis of the budgets. These budgets enable the

GSQ in identifying whether it will having sufficient funds for carrying out the operations or not.

On the basis of this budget company makes necessary arrangements of the funds so that

operations are not interrupted.

8

within control. It helps the business to forecast about the future incomes and expenses on

previous trends.

Disadvantages

The long range planning may be not accurate as they are based over the estimates. There

are various factors that are not considered. Wrong forecasts can affect the operations of

company.

Flexible Budget

It is defined as a budget which flexes or adjusts according to the changes in activities or

volume of output. These budget are more useful and sophisticated than the static budgets. In

static budgets amounts could not be changed. They remain same as they were when approved.

Flexible budgets provide the scope for company to make required changes as required by the

management. Business operates in a dynamic environments where the changes are required to be

made for responding to these changes in the budgets. This become more easy for GSK to make

adjustments without affecting the whole budgets and operations.

Advantages

Flexible budgets allow the company to make adjustments in the budgets for responding to

the changes. It is more preferred by GSK in its management as it more easily adapts the financial

needs of company. Requirements are reflected in budgets in advance.

Disadvantage

Changes in the budget may affect the management of resources. It makes difficult for the

company to disagree with changes. Department makes the changes to budget on their own which

may not be essential (Quattrone, 2016).

Cash Budgets

Cash budget is referred as the budget containing the information about the cash inflow

and outflow. This budget contains information about the monetary funds. It represents where and

how much cash is allocated to the activities. It ensures that sufficient funds are allocated to the

departments and operations carrying out proper analysis of the budgets. These budgets enable the

GSQ in identifying whether it will having sufficient funds for carrying out the operations or not.

On the basis of this budget company makes necessary arrangements of the funds so that

operations are not interrupted.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantages

Cash budgets helps company in proper allocation of funds among departments on the basis of its

budgeted productions. This helps company to identify the requirements of monetary funds so that

it can make available the required funds.

Disadvantage

If the budgets are not forecasted by making proper analysis of the past trends it can affect the

business. Less estimates will lead to insufficiency of funds and higher estimates will be leading

to finance cost.

LO4

Methods which organisation uses in management accounting for responding to the financial

problems.

A business runs in a dynamic environment and it is not possible for the company to operate

without adopting to the environment. Some of the issues can be controlled by the management

like scarce resources, collection problems, insufficiency of resources and like issues. The

management accounting methods can be used by GSK for adequately responding to these

financial problems.

Benchmarking

Benchmarking refers to setting targets and goals that are realistic and achievable. The set

goals and targets provide the management to work for achieving them. The achievable goals

boost the confidence of employees and motivate them to perform better. If the goals are realistic

and achievable, this would not be causing much variations in the budgets and actual figures. Gsk

can provide incentive and rewards for achieving the goals.

Key Performance Indicators

The Key performance indicators are the measurement used for evaluating success of

organisations, processes, activities, employees etc (Bromwich and Scapens, 2016). The objective

of key performance indicators is to identify whether the targets are achieved or not by the

company. KPI is used by GSQ for analysing its performance and requiring the company. If the

targeted objectives are not achieved than corrective measures are taken for improving the

performance of company. These covers setting sales targets, profitability, working capital and

like factors.

9

Cash budgets helps company in proper allocation of funds among departments on the basis of its

budgeted productions. This helps company to identify the requirements of monetary funds so that

it can make available the required funds.

Disadvantage

If the budgets are not forecasted by making proper analysis of the past trends it can affect the

business. Less estimates will lead to insufficiency of funds and higher estimates will be leading

to finance cost.

LO4

Methods which organisation uses in management accounting for responding to the financial

problems.

A business runs in a dynamic environment and it is not possible for the company to operate

without adopting to the environment. Some of the issues can be controlled by the management

like scarce resources, collection problems, insufficiency of resources and like issues. The

management accounting methods can be used by GSK for adequately responding to these

financial problems.

Benchmarking

Benchmarking refers to setting targets and goals that are realistic and achievable. The set

goals and targets provide the management to work for achieving them. The achievable goals

boost the confidence of employees and motivate them to perform better. If the goals are realistic

and achievable, this would not be causing much variations in the budgets and actual figures. Gsk

can provide incentive and rewards for achieving the goals.

Key Performance Indicators

The Key performance indicators are the measurement used for evaluating success of

organisations, processes, activities, employees etc (Bromwich and Scapens, 2016). The objective

of key performance indicators is to identify whether the targets are achieved or not by the

company. KPI is used by GSQ for analysing its performance and requiring the company. If the

targeted objectives are not achieved than corrective measures are taken for improving the

performance of company. These covers setting sales targets, profitability, working capital and

like factors.

9

Governance

It includes monitoring and controlling the activities of business. It refers to have

structured rules and regulation and policies for carrying out the work and activities. The

management of company is required to monitor all the activities and processes so that the

wastages are reduced and resources are used efficiently avoiding the wastages. Company by

keeping control systems in department can ensure that the defected or bad quality material are

identified at entrance. This saves time and wastage of resources.

CONCLUSION

The above report concludes that marginal costing is very important for the organisation.

All the business operations are carried out as per the rules and guidelines of management

accounting. It provides different management accounting systems for effective management of

business. The reporting methods provide the base for improving the performance of company.

The company with planning tools make forecast that helps in effective utilisation of resources.

10

It includes monitoring and controlling the activities of business. It refers to have

structured rules and regulation and policies for carrying out the work and activities. The

management of company is required to monitor all the activities and processes so that the

wastages are reduced and resources are used efficiently avoiding the wastages. Company by

keeping control systems in department can ensure that the defected or bad quality material are

identified at entrance. This saves time and wastage of resources.

CONCLUSION

The above report concludes that marginal costing is very important for the organisation.

All the business operations are carried out as per the rules and guidelines of management

accounting. It provides different management accounting systems for effective management of

business. The reporting methods provide the base for improving the performance of company.

The company with planning tools make forecast that helps in effective utilisation of resources.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.