Detailed Management Accounting Report: Imda Tech Analysis

VerifiedAdded on 2020/06/05

|16

|4607

|39

Report

AI Summary

This report provides a detailed analysis of management accounting practices within Imda Tech. It begins by outlining the core functions of management accounting, emphasizing its role in achieving organizational objectives, strategic planning, and risk management. The report then explores various management accounting systems, including inventory management, job costing, cost accounting, and price optimization systems, highlighting their importance in decision-making. A significant portion of the report focuses on marginal and absorption costing methods, demonstrating their application in preparing income statements and analyzing profitability. The report also examines the merits and demerits of different budgeting techniques and introduces the concept of the balanced scorecard. The financial statements were prepared using both marginal and absorption costing. The report concludes with an assessment of the financial performance, revealing that Imda Tech is experiencing net losses using both costing methods. The report emphasizes the significance of management accounting in enhancing business performance.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

P.1 Functions of management accounting:.............................................................................1

P2 Management accounting systems and its kinds:...............................................................3

M1...........................................................................................................................................3

D1 ..........................................................................................................................................4

TASK 2............................................................................................................................................4

P3 Marginal and absorption costing for making income statement:......................................4

M2...........................................................................................................................................7

D2...........................................................................................................................................7

TASK 3............................................................................................................................................7

P4 Merits and demerits of the various budgets......................................................................7

M3...........................................................................................................................................9

D3...........................................................................................................................................9

P5 Balance score card.............................................................................................................9

M4.........................................................................................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

P.1 Functions of management accounting:.............................................................................1

P2 Management accounting systems and its kinds:...............................................................3

M1...........................................................................................................................................3

D1 ..........................................................................................................................................4

TASK 2............................................................................................................................................4

P3 Marginal and absorption costing for making income statement:......................................4

M2...........................................................................................................................................7

D2...........................................................................................................................................7

TASK 3............................................................................................................................................7

P4 Merits and demerits of the various budgets......................................................................7

M3...........................................................................................................................................9

D3...........................................................................................................................................9

P5 Balance score card.............................................................................................................9

M4.........................................................................................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is a mandatory tool which is used in the business for attaining

their pre-set objectives. Now, this has been seen that the management accounting becomes the

most imperative tool for making the business sustainable and prosperous (Baldvinsdottir,

Mitchell and Nørreklit, 2010). For applying the management accounting practices, the talented

staff is required in order to assess the business in a great manner. Under this report, Imda tech

company would emphasis all the factors which are carried out and through which developed be

attained. Management accounting helps the business to communicate across the department in

an efficient manner. MA is the combination of accounting, finance and management with the

firm skills and tools which are need to add real value to any firm. Management Accountants

implement information of all types which covers financial and non financial information that

would help out the firm to gain the competitive advantages.

TASK 1

P.1 Functions of management accounting:

The enhancement of the value of the firm is the ultimate objective and this could be attain

with the help of implication of management accounting practices within the cited organisation.

For attaining the pre-set objectives of the firm, there are various methods which can be used. All

the policies which are framed in order to attain the pre set objectives, complies in such a way so

that the optimum outcome could be generated (Banerjee, 2010).

MA reports helps the various key managers to frame the policies in an effective manner.

MA helps the business to analyse the various reports, to frame strategies for making business

sustainable, to control risk in order to attain the manage risk, to frame planning and

communication in order to attain management objectives.

BASIS FINANCIAL

ACCOUNTING

MANAGEMENT

ACCOUNTING

Definition FA is the systematic recording

of finance related transactions

which are connected to the

firm. This additionally covers

It is the tool which covers

financial and non financial

information which helps for

achieving pre set goals and

1

Management accounting is a mandatory tool which is used in the business for attaining

their pre-set objectives. Now, this has been seen that the management accounting becomes the

most imperative tool for making the business sustainable and prosperous (Baldvinsdottir,

Mitchell and Nørreklit, 2010). For applying the management accounting practices, the talented

staff is required in order to assess the business in a great manner. Under this report, Imda tech

company would emphasis all the factors which are carried out and through which developed be

attained. Management accounting helps the business to communicate across the department in

an efficient manner. MA is the combination of accounting, finance and management with the

firm skills and tools which are need to add real value to any firm. Management Accountants

implement information of all types which covers financial and non financial information that

would help out the firm to gain the competitive advantages.

TASK 1

P.1 Functions of management accounting:

The enhancement of the value of the firm is the ultimate objective and this could be attain

with the help of implication of management accounting practices within the cited organisation.

For attaining the pre-set objectives of the firm, there are various methods which can be used. All

the policies which are framed in order to attain the pre set objectives, complies in such a way so

that the optimum outcome could be generated (Banerjee, 2010).

MA reports helps the various key managers to frame the policies in an effective manner.

MA helps the business to analyse the various reports, to frame strategies for making business

sustainable, to control risk in order to attain the manage risk, to frame planning and

communication in order to attain management objectives.

BASIS FINANCIAL

ACCOUNTING

MANAGEMENT

ACCOUNTING

Definition FA is the systematic recording

of finance related transactions

which are connected to the

firm. This additionally covers

It is the tool which covers

financial and non financial

information which helps for

achieving pre set goals and

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

summarizing, examine and

reporting these transactions to

oversight agencies and tax

collection firms.

objectives.

Format In this case, there are certain

standards which are need to be

considered while formulating

financial reports.

Under this, there is no certain

standards through which the

data could be framed.

Aim FA report helps investors and

other outsiders to analyse

about the company and then

take their discretionary

decisions.

MA helps the mangers to

frame the decisions in order to

attain the pre set targets and

goals.

Time frame Financial accounting report are

generally having the time

frame. Which is basically for

one year.

While management accounting

does not have any specific

time limit.

Legal requirement Financial accounting is much

essential as there are so many

regulatory bodies which are

required to be complied.

Management accounting does

not have legal requirement in

relation to it.

Importance of management accounting

In order to control the work in an adequate way, there would be need for using of such

accounting practices. The business is performed in an optimum manner via using management

accounting practices. The key benefits of MA are:

Different strategies for the benefits of the firm would be framed.

Efficiency in terms of cost is assessed by using management accounting and the

unnecessary cost are being avoided (Chenhall and Smith, 2011).

2

reporting these transactions to

oversight agencies and tax

collection firms.

objectives.

Format In this case, there are certain

standards which are need to be

considered while formulating

financial reports.

Under this, there is no certain

standards through which the

data could be framed.

Aim FA report helps investors and

other outsiders to analyse

about the company and then

take their discretionary

decisions.

MA helps the mangers to

frame the decisions in order to

attain the pre set targets and

goals.

Time frame Financial accounting report are

generally having the time

frame. Which is basically for

one year.

While management accounting

does not have any specific

time limit.

Legal requirement Financial accounting is much

essential as there are so many

regulatory bodies which are

required to be complied.

Management accounting does

not have legal requirement in

relation to it.

Importance of management accounting

In order to control the work in an adequate way, there would be need for using of such

accounting practices. The business is performed in an optimum manner via using management

accounting practices. The key benefits of MA are:

Different strategies for the benefits of the firm would be framed.

Efficiency in terms of cost is assessed by using management accounting and the

unnecessary cost are being avoided (Chenhall and Smith, 2011).

2

MA helps the firm to boost the profitability that would help out the firm to develop the

firm in a great extent.

P2 Management accounting systems and its kinds:

For gathering of essential information, there are so many frameworks which are available and

they are described in details hereunder:

1. Inventory management system: For manufacturing of any item, there is a need of stock

and that will be control in a best possible manner. Under this, there would be so many

decisions that are required to be framed and for that information is to be gathered with the

help of this framework. With an effective implication of inventory management system,

problems are to be resolved and the firm is managed in an effective manner.

2. Job costing system: There are so many frameworks which are need to be performed and

cost are to be covered in relation to them. However, this is not possible for the

manufacturer to apportion the cost of each job for entire products henceforth, it is

essential that entire cost would be assembled and after that the cost would be distributed

among all (Cinquini and Tenucci, 2010). For controlling the cost, there is a need to

determine the factors which affect the cost and then measure would be taken in order to

control it.

3. Cost accounting system: This system is used specifically in the manufacturing segment.

As there are so many cost which are to be incurred and they are to be distributed among

all in an efficient manner in order to attain the pre-set objectives. The key cost which

would be covered that are connected to material, labour and other overheads. For this

standards, that would be fix through which entire cost would be controlled as this will be

covered on the basis of the pre-set parameters.

4. Price optimisation system: The price and demand are those factors which are inversely

connected to each other. If the product price would go high then demand will goes down

and vice versa. Henceforth, it is very much important that price is need to be maintained

in an optimum level so that the utmost profits could be attained and for this aim this

system would be used.

M1

Under this cited business, there is dependably an extension for the development and for having

diversification, the primary concern that is required to be done is to settle on the best choices by

3

firm in a great extent.

P2 Management accounting systems and its kinds:

For gathering of essential information, there are so many frameworks which are available and

they are described in details hereunder:

1. Inventory management system: For manufacturing of any item, there is a need of stock

and that will be control in a best possible manner. Under this, there would be so many

decisions that are required to be framed and for that information is to be gathered with the

help of this framework. With an effective implication of inventory management system,

problems are to be resolved and the firm is managed in an effective manner.

2. Job costing system: There are so many frameworks which are need to be performed and

cost are to be covered in relation to them. However, this is not possible for the

manufacturer to apportion the cost of each job for entire products henceforth, it is

essential that entire cost would be assembled and after that the cost would be distributed

among all (Cinquini and Tenucci, 2010). For controlling the cost, there is a need to

determine the factors which affect the cost and then measure would be taken in order to

control it.

3. Cost accounting system: This system is used specifically in the manufacturing segment.

As there are so many cost which are to be incurred and they are to be distributed among

all in an efficient manner in order to attain the pre-set objectives. The key cost which

would be covered that are connected to material, labour and other overheads. For this

standards, that would be fix through which entire cost would be controlled as this will be

covered on the basis of the pre-set parameters.

4. Price optimisation system: The price and demand are those factors which are inversely

connected to each other. If the product price would go high then demand will goes down

and vice versa. Henceforth, it is very much important that price is need to be maintained

in an optimum level so that the utmost profits could be attained and for this aim this

system would be used.

M1

Under this cited business, there is dependably an extension for the development and for having

diversification, the primary concern that is required to be done is to settle on the best choices by

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

which this can be made conceivable (Fullerton, Kennedy and Widener, 2014). For this data will

be required and that will be gathered with the assistance of the diverse MA system. Imda tech

will have the capacity to keep up its position in the market and will have the capacity to get by

for long period of time.

D1

With a specific end goal to make the upgrades in the business, this is required that

execution of the organization might be assessed on general premise. For this there are different

arrangements which are made with the goal that this can be accomplished. Likewise, the

frameworks will help in acquiring the extra advantages in the aggressive market and this will be

finished with the assistance of the different reports that are defined in the entire procedure.

TASK 2

P3 Marginal and absorption costing for making income statement:

The income statement is framed so that the income statements could be prepared and the

profits could be derived from. For preparing these statements these are implemented below:

Marginal Costing: Under this method, the cost of production of any product are divided into

two parts which are named as fixed and variable cost (Haiza Muhammad Zawawi and Hoque,

2010). Fixed cost includes those cost that remains same irrespective of change in the level of

units and variable cost are those which very as per the change in production of the product. With

the help of marginal costing, the contribution can be calculated and this would be help out to

draw a valid conclusion. With the help of this the decisions would be framed and under this the

fixed cost is not required to be considered.

Absorption costing: Under absorption costing, the total cost of the product is required to be

considered and for that the entire cost is need to be apportioned. Under this the over and under

absorption cost are made available that would be covered in the calculation of the amount of

profits which are framed.

With implementing these methods, income statement are required to be framed that would assist

in attaining financial firmness and the issues which are required that the profit.

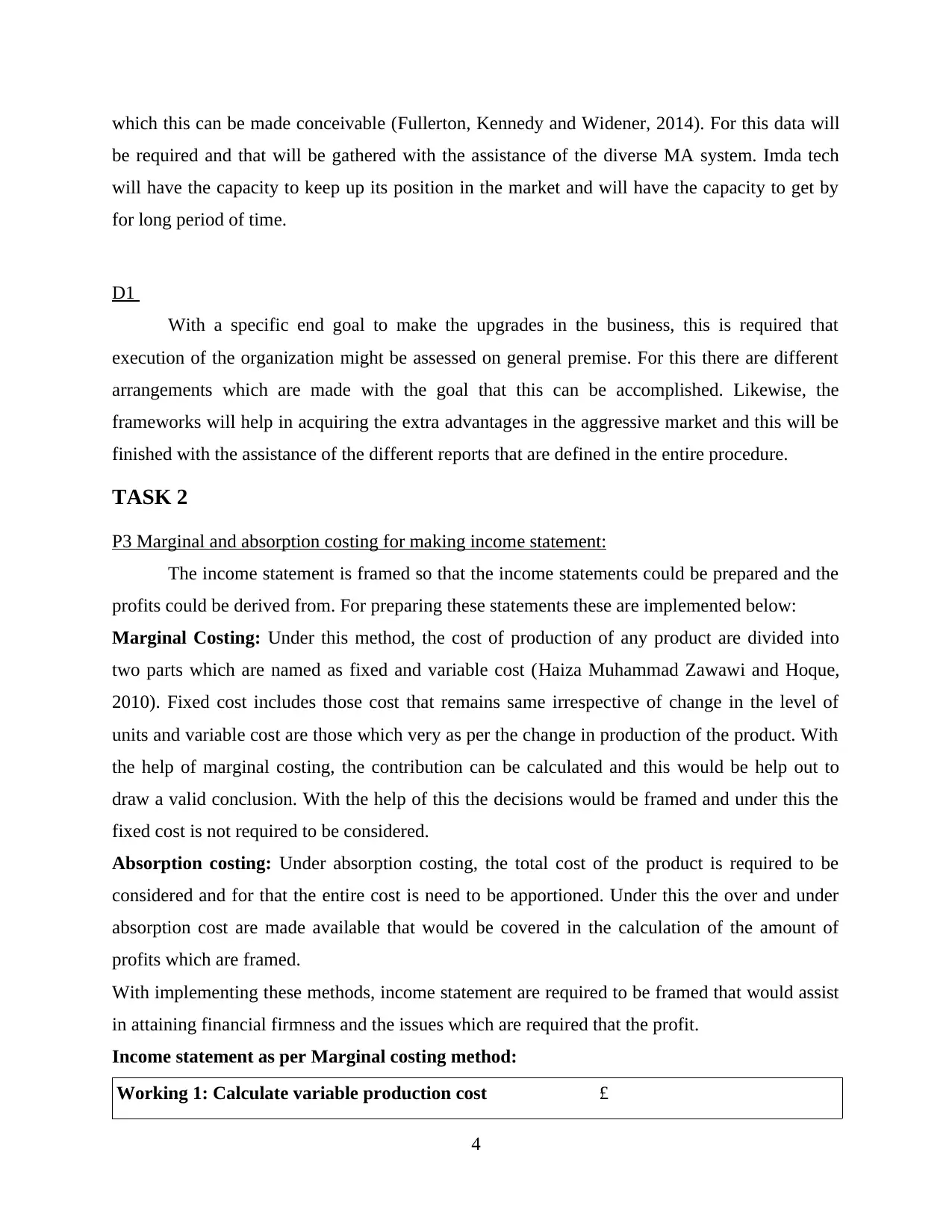

Income statement as per Marginal costing method:

Working 1: Calculate variable production cost £

4

be required and that will be gathered with the assistance of the diverse MA system. Imda tech

will have the capacity to keep up its position in the market and will have the capacity to get by

for long period of time.

D1

With a specific end goal to make the upgrades in the business, this is required that

execution of the organization might be assessed on general premise. For this there are different

arrangements which are made with the goal that this can be accomplished. Likewise, the

frameworks will help in acquiring the extra advantages in the aggressive market and this will be

finished with the assistance of the different reports that are defined in the entire procedure.

TASK 2

P3 Marginal and absorption costing for making income statement:

The income statement is framed so that the income statements could be prepared and the

profits could be derived from. For preparing these statements these are implemented below:

Marginal Costing: Under this method, the cost of production of any product are divided into

two parts which are named as fixed and variable cost (Haiza Muhammad Zawawi and Hoque,

2010). Fixed cost includes those cost that remains same irrespective of change in the level of

units and variable cost are those which very as per the change in production of the product. With

the help of marginal costing, the contribution can be calculated and this would be help out to

draw a valid conclusion. With the help of this the decisions would be framed and under this the

fixed cost is not required to be considered.

Absorption costing: Under absorption costing, the total cost of the product is required to be

considered and for that the entire cost is need to be apportioned. Under this the over and under

absorption cost are made available that would be covered in the calculation of the amount of

profits which are framed.

With implementing these methods, income statement are required to be framed that would assist

in attaining financial firmness and the issues which are required that the profit.

Income statement as per Marginal costing method:

Working 1: Calculate variable production cost £

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Direct material cost 8

Direct labour cost 5

Variable production expenses 2

Total Variable production cost 15

Working 2: Calculate value of closing inventory and production

Opening inventory Production Closing inventory

Nil 2000*15 = 30000 500*15 = 7500

Net profit in case of marginal costing £Amount £ Amount

Sales value

Less: Variable costs

Stock at the opening

Cost of production

Stock at the closing

Variable sales overheads

Contribution

Less: Fixed costs:

Fixed Production overheads

Fixed Selling overheads

NIL

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

Net loss -2875

Income statement as per Absorption costing method

Selling Price per unit £35

Unit costs

Direct materials cost £8

Direct Labour cost £5

Variable Production overhead £2

5

Direct labour cost 5

Variable production expenses 2

Total Variable production cost 15

Working 2: Calculate value of closing inventory and production

Opening inventory Production Closing inventory

Nil 2000*15 = 30000 500*15 = 7500

Net profit in case of marginal costing £Amount £ Amount

Sales value

Less: Variable costs

Stock at the opening

Cost of production

Stock at the closing

Variable sales overheads

Contribution

Less: Fixed costs:

Fixed Production overheads

Fixed Selling overheads

NIL

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

Net loss -2875

Income statement as per Absorption costing method

Selling Price per unit £35

Unit costs

Direct materials cost £8

Direct Labour cost £5

Variable Production overhead £2

5

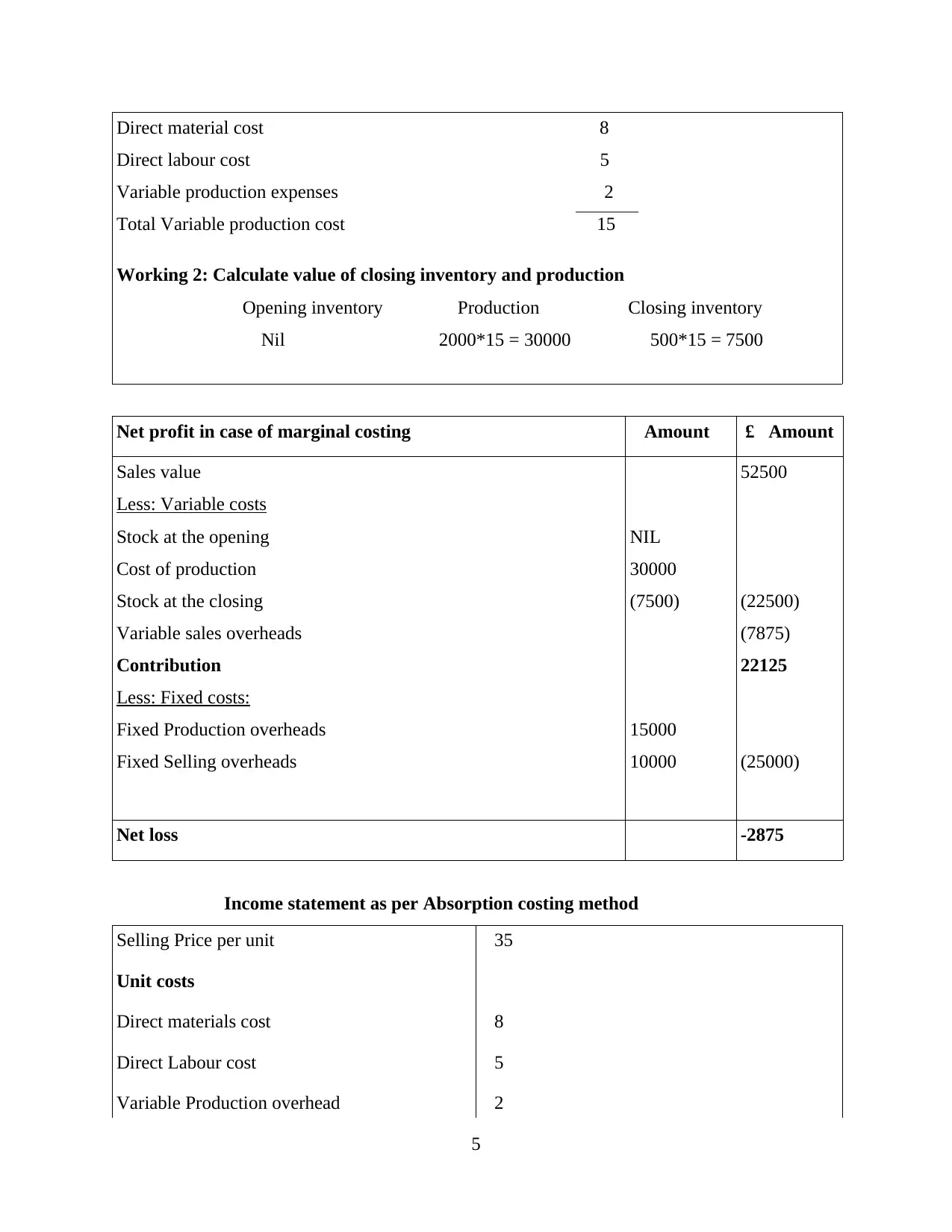

Variable sales overhead £5.25

Budgeted production during the year is 3000

units

Production overhead: In this Actual cost is £10,000 and budgeted cost is £15,000

Selling cost: In this Actual cost is £7875 and budgeted cost is £10,000

Absorption costing working notes

Working Note 1: Calculate full production cost

Direct labour £5

Direct material £8

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40,000 500*20 = £10,000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000 (under absorbed)

Net profit in case of absorption costings £Amount £Amount

Sales value

Less: Cost of Sales:

Opening stock

Cost of production

NIL

40000

52500

6

Budgeted production during the year is 3000

units

Production overhead: In this Actual cost is £10,000 and budgeted cost is £15,000

Selling cost: In this Actual cost is £7875 and budgeted cost is £10,000

Absorption costing working notes

Working Note 1: Calculate full production cost

Direct labour £5

Direct material £8

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40,000 500*20 = £10,000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000 (under absorbed)

Net profit in case of absorption costings £Amount £Amount

Sales value

Less: Cost of Sales:

Opening stock

Cost of production

NIL

40000

52500

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

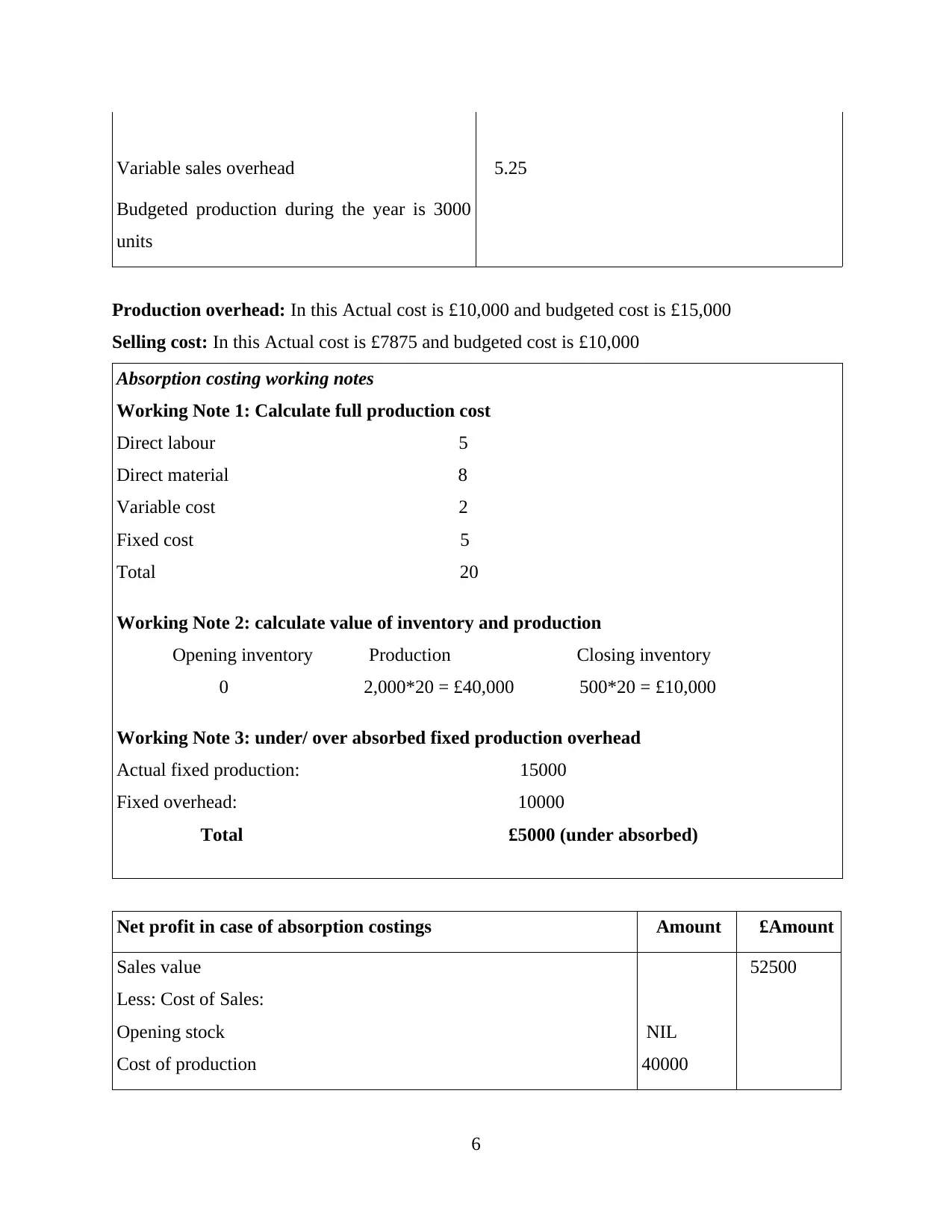

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

Less: Selling Expenses

Variable sales expenses

Fixed selling expenses

(10000)

7875

10000

(30000)

(5000)

17500

17875

Net loss -375

M2

During the time of preparation of financial statements, there will be necessity of the

different strategies that should be connected (Herzig and et.al. 2012). By them the data will be

obtained and that will be utilized as a part of the report development. Administrators will be

utilizing them keeping in mind the end goal to settle on the choices that will be in general

enthusiasm of the organization.

D2

During the time spent accomplishing targets just count of the benefits is insufficient in

actuality there assessment should be done as such that execution can be measures and afterwards

promote change can be made. In the given case it can be seen that Imda tech is confronting

misfortunes which are 2875 and 375 in regard of minimal ans retention costing. The misfortune

is more in peripheral costing on the grounds that in that the settled cost is not allotted so the

entire sum is assumed and by that misfortune is expanded. During the time spent arrangement of

money related reports there will be necessity of the different strategies that should be connected .

By them the data will be obtained and that will be utilized as a part of the report development.

Administrators will be utilizing them keeping in mind the end goal to settle on the choices that

will be in general enthusiasm of the organization.

anded.

7

(Under)/Over absorbed fixed prod. O/h

Gross Profit

Less: Selling Expenses

Variable sales expenses

Fixed selling expenses

(10000)

7875

10000

(30000)

(5000)

17500

17875

Net loss -375

M2

During the time of preparation of financial statements, there will be necessity of the

different strategies that should be connected (Herzig and et.al. 2012). By them the data will be

obtained and that will be utilized as a part of the report development. Administrators will be

utilizing them keeping in mind the end goal to settle on the choices that will be in general

enthusiasm of the organization.

D2

During the time spent accomplishing targets just count of the benefits is insufficient in

actuality there assessment should be done as such that execution can be measures and afterwards

promote change can be made. In the given case it can be seen that Imda tech is confronting

misfortunes which are 2875 and 375 in regard of minimal ans retention costing. The misfortune

is more in peripheral costing on the grounds that in that the settled cost is not allotted so the

entire sum is assumed and by that misfortune is expanded. During the time spent arrangement of

money related reports there will be necessity of the different strategies that should be connected .

By them the data will be obtained and that will be utilized as a part of the report development.

Administrators will be utilizing them keeping in mind the end goal to settle on the choices that

will be in general enthusiasm of the organization.

anded.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 3

P4 Merits and demerits of the various budgets.

In the business there are various decisions which will be made and for that proper

planning will be required to be made. In this the budgets will be made in which the estimation

will be made in relation to the amounts of the expense and incomes which will be made. The

data of the past years will be examined and then the research will be conducted with the help of

which the future projections will be made and then they will be used in the preparation of the

budgets. They will be made for the fixed time span and for that the standards which will be set

will have to be followed (Lukka and Modell, 2010).

They will be useful in the calculation of the performance and that will be done by

comparing the various figures of the actuals and the budgeted data. By the help of this the

deviations among them will be found and they will be used to know the reasons which will be

involved behind them. This will be then used to take the measures by which the elimination of

them will be made possible. The work will then in performed in the better manner and by that the

highest level of the efficiency and effectiveness will be maintained. The different forms which

will be used in this are mentioned below:

Master budget: this budget will be the one in which the summary of all will be provided.

The decisions will be taken by the managers on the basis of it in relation to the various

departments and in them the time will be saved due to this.

Advantages: In this the requirement to make the different budgets will be removed as all of the

task will be performed with the one budget so the time and money both will be saved.

Disadvantages: The changes which will be occurring will be difficult to be included in the

budget as there will be lot of amendments and this will not be easy to know about all of them.

Operating budget: The incomes and expenses which will have to be incurred in relation

to the various operations will have to be controlled and for that this budget will be very

useful. The expenses which will be required to be made in the particular time will be

incorporated in this. By this the chances of the wastage will be reduced and this will be

the main advantage.

Advantages: in this the manner in which the expenses will have to be met will be identified

before so they will be arranged in the advance and then the problems will not have to be faced in

relation to them.

8

P4 Merits and demerits of the various budgets.

In the business there are various decisions which will be made and for that proper

planning will be required to be made. In this the budgets will be made in which the estimation

will be made in relation to the amounts of the expense and incomes which will be made. The

data of the past years will be examined and then the research will be conducted with the help of

which the future projections will be made and then they will be used in the preparation of the

budgets. They will be made for the fixed time span and for that the standards which will be set

will have to be followed (Lukka and Modell, 2010).

They will be useful in the calculation of the performance and that will be done by

comparing the various figures of the actuals and the budgeted data. By the help of this the

deviations among them will be found and they will be used to know the reasons which will be

involved behind them. This will be then used to take the measures by which the elimination of

them will be made possible. The work will then in performed in the better manner and by that the

highest level of the efficiency and effectiveness will be maintained. The different forms which

will be used in this are mentioned below:

Master budget: this budget will be the one in which the summary of all will be provided.

The decisions will be taken by the managers on the basis of it in relation to the various

departments and in them the time will be saved due to this.

Advantages: In this the requirement to make the different budgets will be removed as all of the

task will be performed with the one budget so the time and money both will be saved.

Disadvantages: The changes which will be occurring will be difficult to be included in the

budget as there will be lot of amendments and this will not be easy to know about all of them.

Operating budget: The incomes and expenses which will have to be incurred in relation

to the various operations will have to be controlled and for that this budget will be very

useful. The expenses which will be required to be made in the particular time will be

incorporated in this. By this the chances of the wastage will be reduced and this will be

the main advantage.

Advantages: in this the manner in which the expenses will have to be met will be identified

before so they will be arranged in the advance and then the problems will not have to be faced in

relation to them.

8

Disadvantages: They are made on the basis of the estimates and it is not possible that they will

be relevant so there will be chances that mistakes will be made.

Cash flow budget: all the transactions of the cash will be included in this and by this the

cash deficit will not be involved and also the other problems will be eliminated. The

sources by which the cash will be obtained will be identified and then the theyw ill be

utilised in the manner which is specified in this (Macintosh and Quattrone, 2010).

Advantages: The company will be able to deal with the problem of the cash deficit as they will

be arranging the funds in advance and that will be of great help.

Disadvantages: In this there will be no accuracy and that will be the major disadvantage.

Budget making process: In this there will be various steps which will be involved and the first

one will be to collect the information and for that historical data will be used and then the

research will be conducted so that the required information can be collected and then the

planning will be made and the budget will be prepared on the basis of it. The risk will be

measured and it will be reduced to the required level. Also the help of the professionals will be

taken in this.

Pricing strategy: There are various strategies which can be used by which the price that will

have to be charged from the customers will be determined. The main methods will be cost plus

pricing, penetration pricing and the other methods. The most beneficial price will be set and will

be the one by which the customers will also be benefited.

M3

The advantage will be gained by the business will be help of the planning tools as by

them the conduction of it will be maintained and the successful conduction will be carried out.

Also the business will be continued in long run (Parker, 2012).

D3

The tools which are present will be used so that the problems and the issues will be

resolved in the best possible manner. The main reason because of which this will be made

possible is that all the issues will be determined on time and then the growth will be achieved by

the correction of them.

9

be relevant so there will be chances that mistakes will be made.

Cash flow budget: all the transactions of the cash will be included in this and by this the

cash deficit will not be involved and also the other problems will be eliminated. The

sources by which the cash will be obtained will be identified and then the theyw ill be

utilised in the manner which is specified in this (Macintosh and Quattrone, 2010).

Advantages: The company will be able to deal with the problem of the cash deficit as they will

be arranging the funds in advance and that will be of great help.

Disadvantages: In this there will be no accuracy and that will be the major disadvantage.

Budget making process: In this there will be various steps which will be involved and the first

one will be to collect the information and for that historical data will be used and then the

research will be conducted so that the required information can be collected and then the

planning will be made and the budget will be prepared on the basis of it. The risk will be

measured and it will be reduced to the required level. Also the help of the professionals will be

taken in this.

Pricing strategy: There are various strategies which can be used by which the price that will

have to be charged from the customers will be determined. The main methods will be cost plus

pricing, penetration pricing and the other methods. The most beneficial price will be set and will

be the one by which the customers will also be benefited.

M3

The advantage will be gained by the business will be help of the planning tools as by

them the conduction of it will be maintained and the successful conduction will be carried out.

Also the business will be continued in long run (Parker, 2012).

D3

The tools which are present will be used so that the problems and the issues will be

resolved in the best possible manner. The main reason because of which this will be made

possible is that all the issues will be determined on time and then the growth will be achieved by

the correction of them.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.